49

FULL YEAR RESULTS 20 TH APRIL 2016

FULL YEAR RESULTS

20TH APRIL 2016

11% H2 PBT GROWTH A MAJOR MILESTONE

1

• 11% PBT growth delivered in H2

• Trading PBT in line with consensus

• Reported PBT ahead due to restatement

• Strategy working well with great progress in our digital KPIs

• Strong Power Brand performance, up 10%

• Headwind from the Traditional Segment

• FY17 focus: Fit 4 the Future implementation

AGENDA

FINANCIALS

STRATEGIC UPDATE

SUMMARY

ANY QUESTIONS?

2

CRAIG LOVELACE, CFO

FINANCIALS

3

FINANCIAL SUMMARY

• Revenue £866.2m, +3.5%

• Product revenue +4.1% and Financial Services revenue +2.1%

• Gross margin -10bps to 55.7%

• Trading profit* £84.5m, -2.0% yoy

• H2 trading profit* £49.5m, +11%

• Adjusted EPS 24.02p

• Net debt £289.7m

• Final dividend held at 8.56p

4* Defined as continuing PBT excluding exceptionals and unrealised FX movement, and prior to

impact of restatement

5

IAS39 RESTATEMENT

• No impact on business operations or cash flow

• Restated provision rate 18.3% FY14 and 16.1% FY15; FY16 15.6%

• Net asset write-down of £48.3m FY14 and £46.6m FY15; FY16

£43.9m

• Changes to Financial Services revenue, COGS and resultant gross

margin as a result of taking into account suspended interest

• FY15 PBT increased by £2.0m and FY16 by £3.8m as a result of the

reduction in provision yoy

• We view the P&L credit as a one-off and do not expect any impact in

FY17 and onwards

6

REVENUE

£m FY16 FY15 Change

Product 606.6 582.9 +4.1%

Financial Services 259.6 254.3 +2.1%

Cont. Revenue 866.2 837.2 +3.5%

% yoy growth Q1 (13wks) Q2 (13wks) Q3 (18wks) Q4 (8wks)

Product +4.3% +7.9% +4.3% -3.5%

Financial Services -1.9% +1.0% +3.7% +8.1%

Cont. Revenue +2.5% +5.8% +4.1% +0.2%

• Q4 (8wks) comparatives: Product +6.7%, Financial Services -8.8%

• January & February driven by sale activity, product volume up 2%

• Full price sales for SS16 started slowly in line with the industry

7

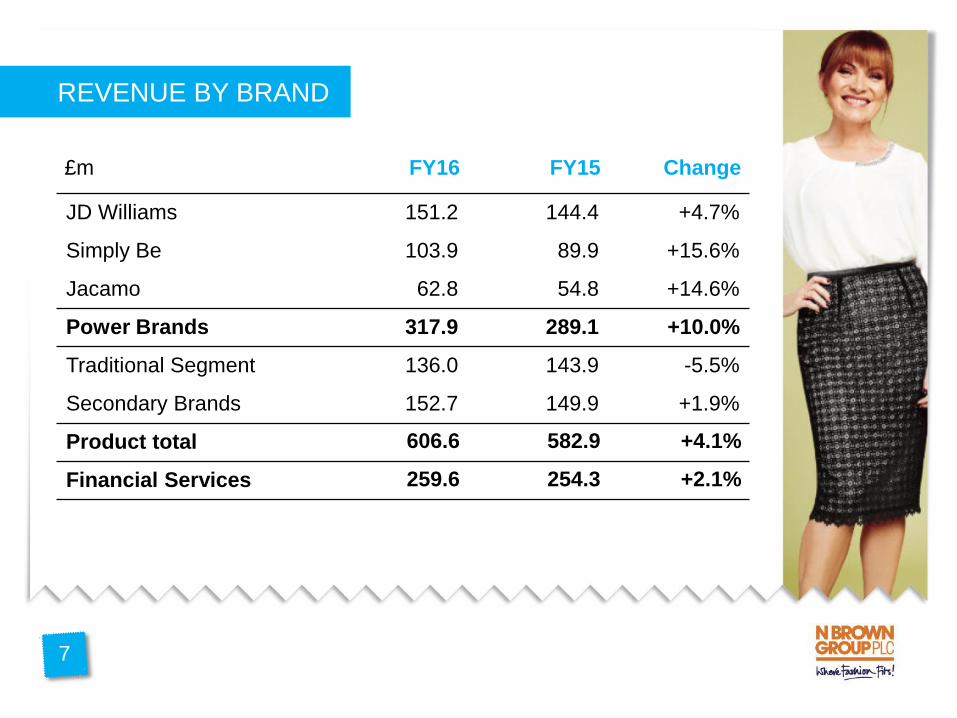

REVENUE BY BRAND

£m FY16 FY15 Change

JD Williams 151.2 144.4 +4.7%

Simply Be 103.9 89.9 +15.6%

Jacamo 62.8 54.8 +14.6%

Power Brands 317.9 289.1 +10.0%

Traditional Segment 136.0 143.9 -5.5%

Secondary Brands 152.7 149.9 +1.9%

Product total 606.6 582.9 +4.1%

Financial Services 259.6 254.3 +2.1%

8

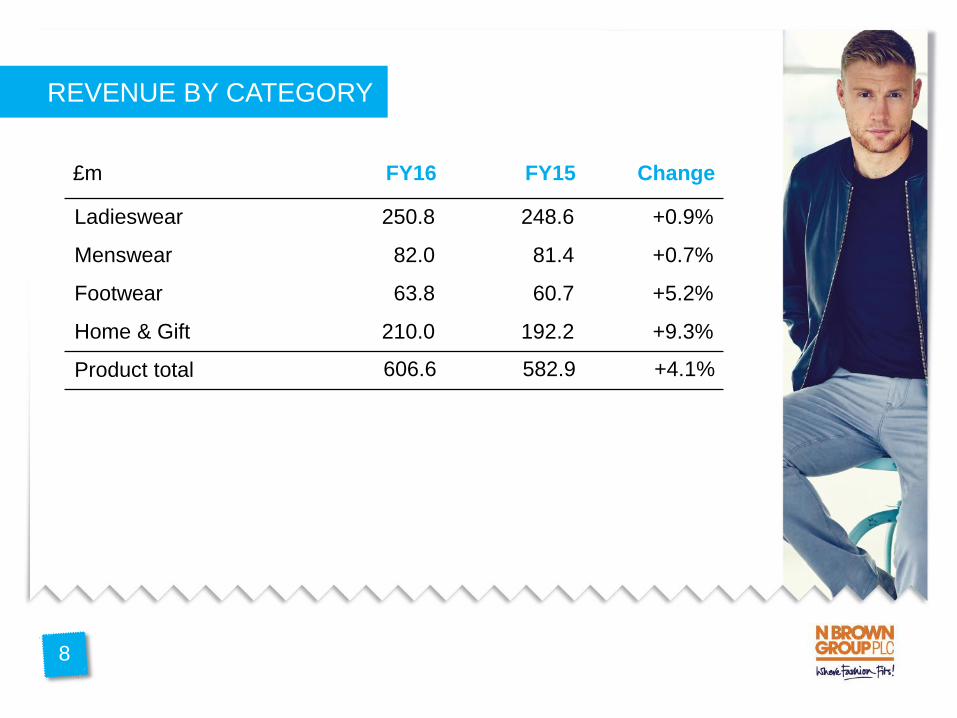

REVENUE BY CATEGORY

£m FY16 FY15 Change

Ladieswear 250.8 248.6 +0.9%

Menswear 82.0 81.4 +0.7%

Footwear 63.8 60.7 +5.2%

Home & Gift 210.0 192.2 +9.3%

Product total 606.6 582.9 +4.1%

9

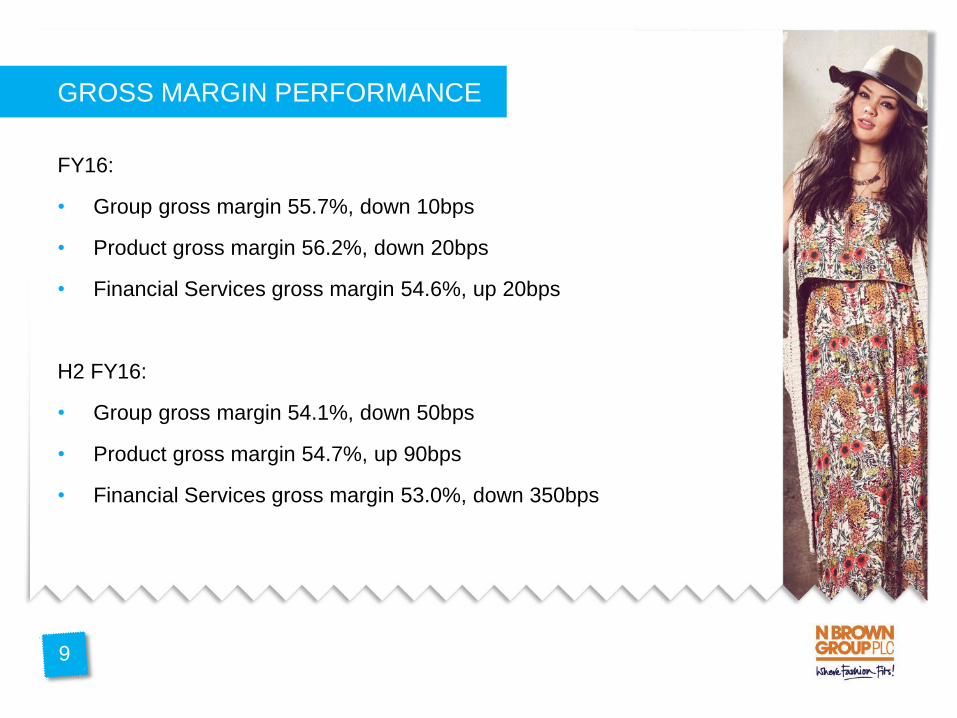

GROSS MARGIN PERFORMANCE

FY16:

• Group gross margin 55.7%, down 10bps

• Product gross margin 56.2%, down 20bps

• Financial Services gross margin 54.6%, up 20bps

H2 FY16:

• Group gross margin 54.1%, down 50bps

• Product gross margin 54.7%, up 90bps

• Financial Services gross margin 53.0%, down 350bps

OPERATING EXPENSES

£m FY16 FY15 Chg Chg % rev

Warehouse & fulfilment (76.7) (73.9) +3.8% Flat

Marketing & production (161.7) (154.7) +4.5% +20bps

Admin & payroll (122.6) (121.8) +0.7% -40bps

Depreciation & amortisation (25.2) (21.2) +18.9% +40bps

Operating Profit* 96.4 95.8 +0.6%

Operating Margin 11.1% 11.4% -30bps

IAS39 restatement credit 3.8 2.0

U’lying Operating Profit* 92.6 93.8 -1.3%

U’lying Operating Margin 10.7% 11.2% -50bps

* Continuing operations, pre-exceptional items

10

11

GROUP PROFIT & LOSS

£m FY16 FY15 Change

U’lying Operating Profit* 92.6 93.8 -1.3%

Finance Costs (net) (8.1) (7.6) +6.6%

Underlying Trading Profit 84.5 86.2 -2.0%

Exceptional Costs (17.2) (12.6)

Unrealised FX movement 1.1 2.7

Profit Before Tax 68.4 76.3 -10.4%

IAS39 restatement credit 3.8 2.0

Taxation (17.3) (16.8) +3.0%

Profit from Cont. Ops 54.9 61.5 -12.5%

Discontinued Ops (G&O) (0.6) (10.4)

Group Profit 54.3 51.1 +6.3%

* Continuing operations, pre-exceptional items and restatement effect

NET ASSETS

12

£m FY16 FY15 Change

Non Current Assets 205.5 176.0 +16.8%

Inventories 101.5 94.8 +7.1%

Receivables/Prepayments 560.9 550.6 +1.9%

Creditors/Accruals (113.0) (121.5) -7.0%

Retirement Benefit Surplus /

(Deficit)

10.8 (3.3) -

Net Debt (289.7) (246.6) +17.5%

Net Assets 476.0 450.0 +5.8%

Gearing 61% 55%

13

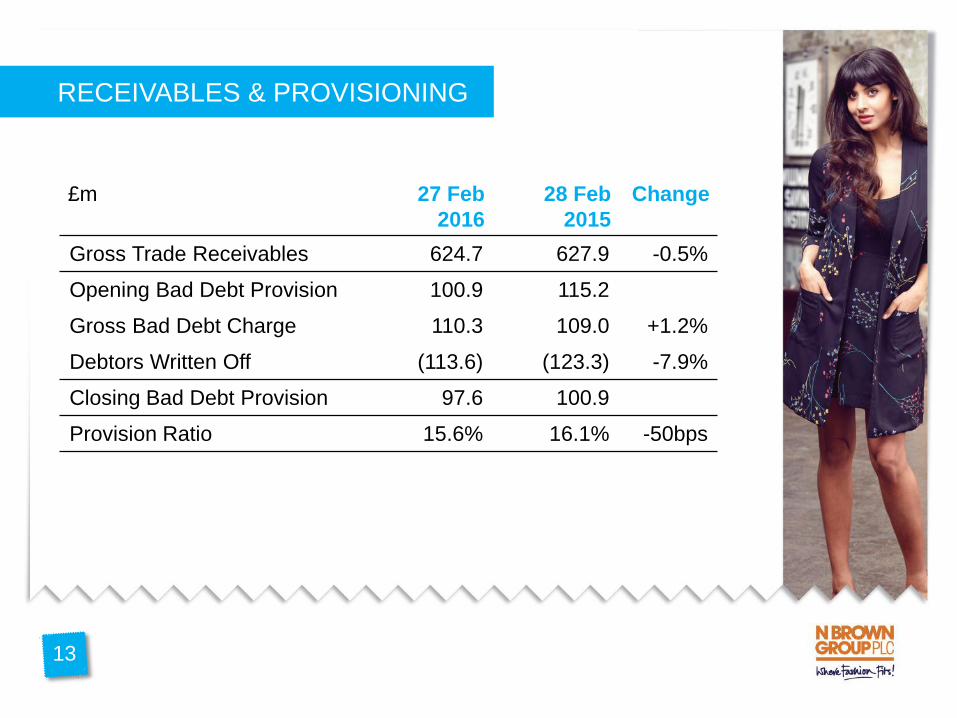

RECEIVABLES & PROVISIONING

£m 27 Feb

2016

28 Feb

2015

Change

Gross Trade Receivables 624.7 627.9 -0.5%

Opening Bad Debt Provision 100.9 115.2

Gross Bad Debt Charge 110.3 109.0 +1.2%

Debtors Written Off (113.6) (123.3) -7.9%

Closing Bad Debt Provision 97.6 100.9

Provision Ratio 15.6% 16.1% -50bps

17

CASH FLOW

14

Cash flow from operations: £86.9m

121.6 (17.9)(18.0)

(58.2)

(22.4)

(9.6)(40.2)

1.6

-60

-40

-20

0

20

40

60

80

100

120

140

(43.1)

15

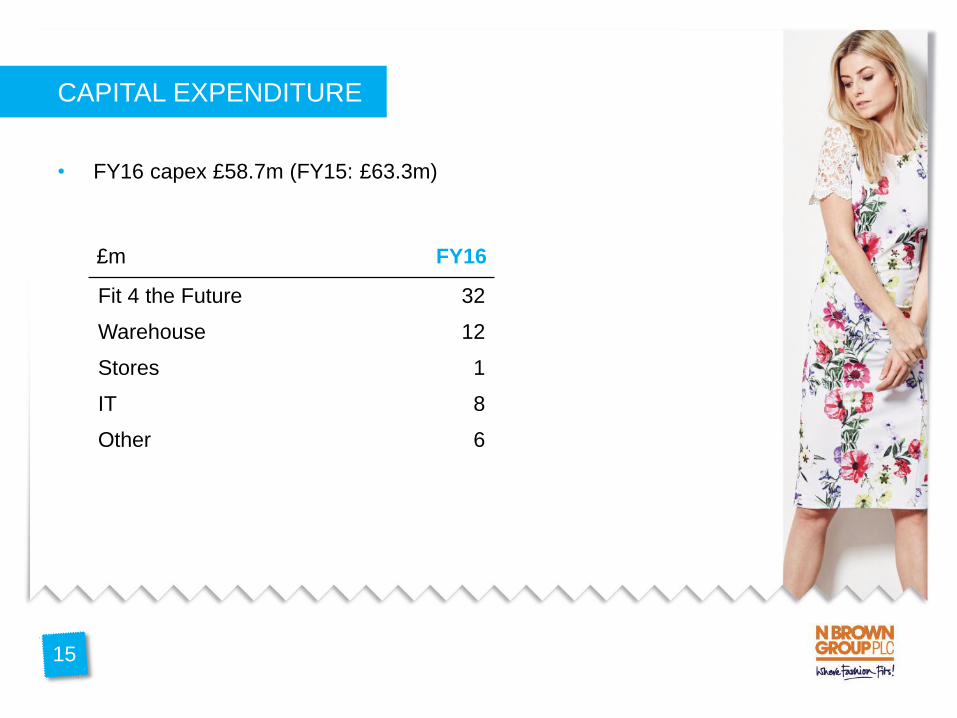

CAPITAL EXPENDITURE

15

• FY16 capex £58.7m (FY15: £63.3m)

£m FY16

Fit 4 the Future 32

Warehouse 12

Stores 1

IT 8

Other 6

19

BALANCE SHEET UNDERSTANDING

16

• Gross debt drawn £335m

– RCF £85m

– Securitisation £250m (secured on our £625m customer loan book)

• Net debt £289m

• EBITDA £122m

– Headline Leverage ratio 2.4x

– Indicative Leverage ratio on RCF 0.7x

20

FY17 GUIDANCE

• Gross margin:

– Product margin -50bps to -150bps; includes impact of non-trading

headwinds of FX and aged inventory clearance

– Financial Services margin +50bps to -50bps

• Group operating costs (excluding D&A) up 2% to 4%

• Depreciation & amortisation £29m-£30m

• Net interest costs £8m-£9m

17

41

FY17 GUIDANCE

• Capex £38m-£40m

• Net debt £270m - £290m

• Tax rate c.20%

• Exceptional costs c.£2m

18

19

STRATEGIC UPDATE

FINANCIALS

SUMMARY

ANY QUESTIONS?

OUR STRATEGY

20

22

H2 ACHIEVEMENTS

PROCESS

Continued focus on

product newness

Improving our

promotional

efficiency

Creation of a

dedicated Traditional

segment marketing

team

PEOPLE

Outsourced Creative

Production and IT

support

Digital marketing,

Merchandising,

Design and DCE

teams expanded

Digitalised all people

processes

SYSTEMS

Early releases of F4F

delivered and

programme

delivering well

Warehouse

extension completed

and currently coming

on stream

221

FY17 KEY PRIORITIES

22

• Fit 4 the Future:

– First stage of new merchandising tool rolled out in May

– First wave of new web platform live in August (USA), roll-out to main

brands early 2017

– New Financial Services system rolled out alongside web platform

– Focused on landing roll-out, minimising disruption and risk, and

maximising potential benefits

• Further developing our digital capabilities; launch of “JDWorks”

• Driving Power Brand growth

• Addressing the headwind from the Traditional Segment

• New customers +36%

• 89% online penetration, with first order penetration 97%

• Further increasing customer choice through new product collections

and brands

• Driving digital marketing techniques

• Planning to launch a loyalty app to further drive retention

SIMPLY BE

23

• New customers +12%

• 90% online penetration, with first order penetration 97%

• Refreshed brand look and feel

• Driving on Dave TV sponsorship

• Improved fit of our smaller sizes – driving increased revenues

and lower returns rates

24

JACAMO

2525

• Brand resonating well with our customers; new customers up 5%

• Increasingly digital:

– Online penetration 51%

– New customer online penetration +13ppts to 65%

– Online share up from 1.0% to 1.6% (Hitwise)

• Increased product newness

• Williams & Brown menswear offer relaunched, performing strongly

• VIP scheme performing ahead of expectations

• Over 50’s fashion show live-streamed onto JDWilliams.co.uk

JD WILLIAMS

5026

• Ambrose Wilson, Premier Man, Julipa, House of Bath

• Dedicated marketing team established

• Increasing variety of promotions and paper formats

• Optimise tablet – more important than mobile for these customers

• Increasing product choice and unifying home & gift offer

• Will take time (earliest AW16) to improve performance

TRADITIONAL SEGMENT

27

CUSTOMERS: CONTINUED GREAT PROGRESS

TY LY Change

Active customer accounts 4.14m 4.05m +2.2%

Power Brand active customer accounts 2.00m 1.87m +6.9%

% growth of most loyal* customers -0.4% +1.0% -140bps

Customer satisfaction rating 85.8% 85.9% -10bps

* Defined as those customers who have ordered in each of the last four seasons27

• Ranked third in the UK for customer service, behind only John Lewis

and Amazon

PRODUCT TY LY Change

Ladieswear share, size 16+ 4.0% 4.0% -

Menswear share, chest size 44”+ 1.7% 1.5% +20bps

Group returns rate 27.4% 28.6% -120bps

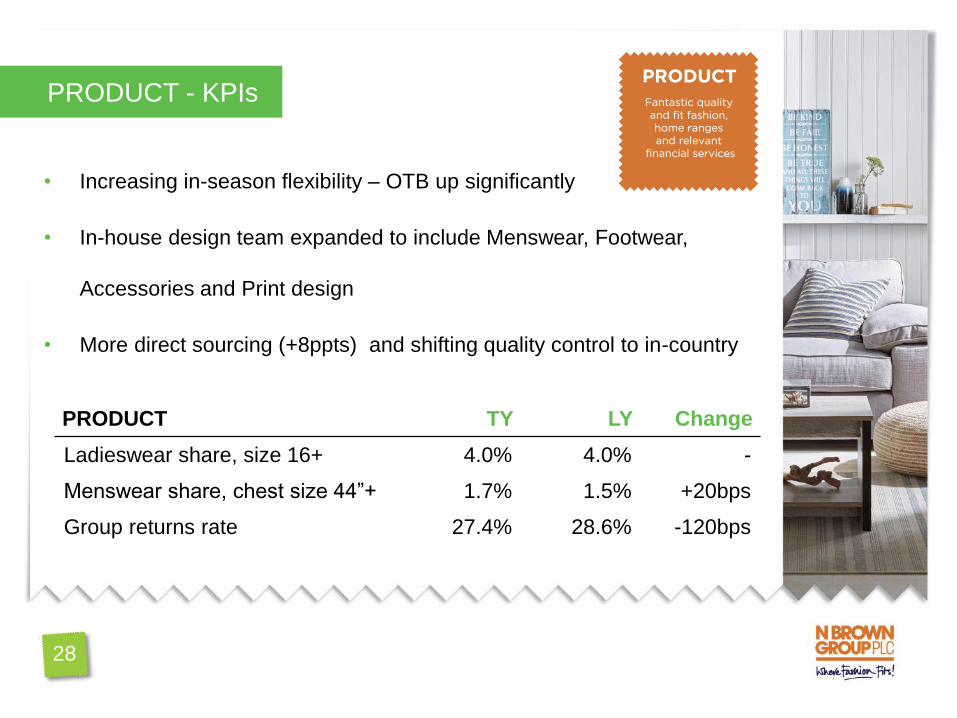

28

• Increasing in-season flexibility – OTB up significantly

• In-house design team expanded to include Menswear, Footwear,

Accessories and Print design

• More direct sourcing (+8ppts) and shifting quality control to in-country

PRODUCT - KPIs

PRICE ASSERTIVE

• Overall pricing strategy unchanged:

– Competitive with the mid-market

– Focused on value for money

– Strong price architecture

• Taking the opportunity to be assertive on price selectively

• More efficient, event-linked promotions

29

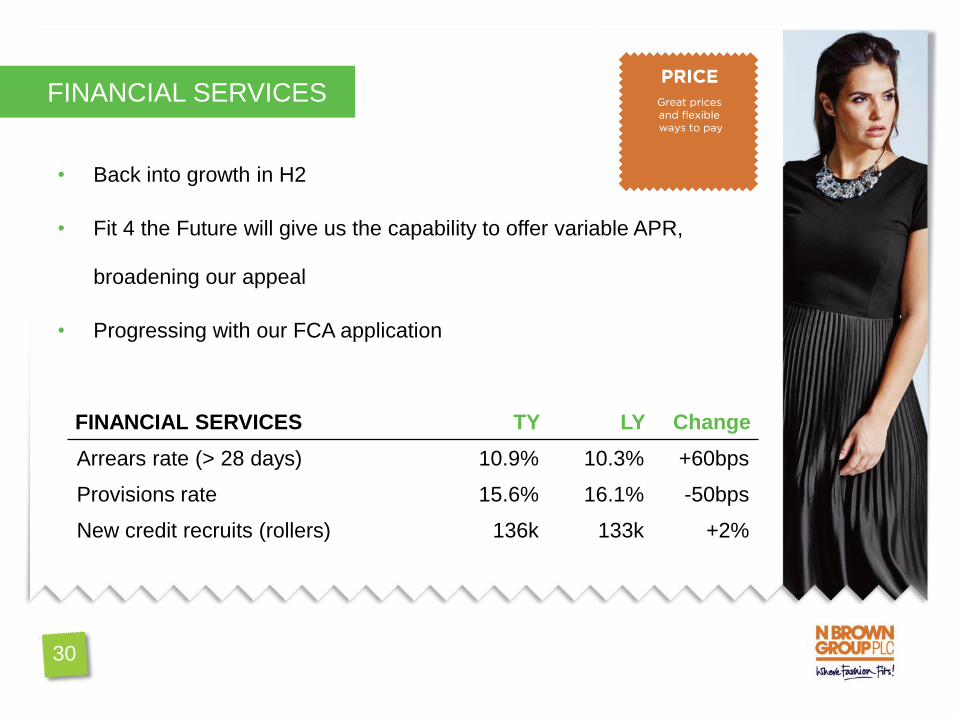

FINANCIAL SERVICES

FINANCIAL SERVICES TY LY Change

Arrears rate (> 28 days) 10.9% 10.3% +60bps

Provisions rate 15.6% 16.1% -50bps

New credit recruits (rollers) 136k 133k +2%

30

• Back into growth in H2

• Fit 4 the Future will give us the capability to offer variable APR,

broadening our appeal

• Progressing with our FCA application

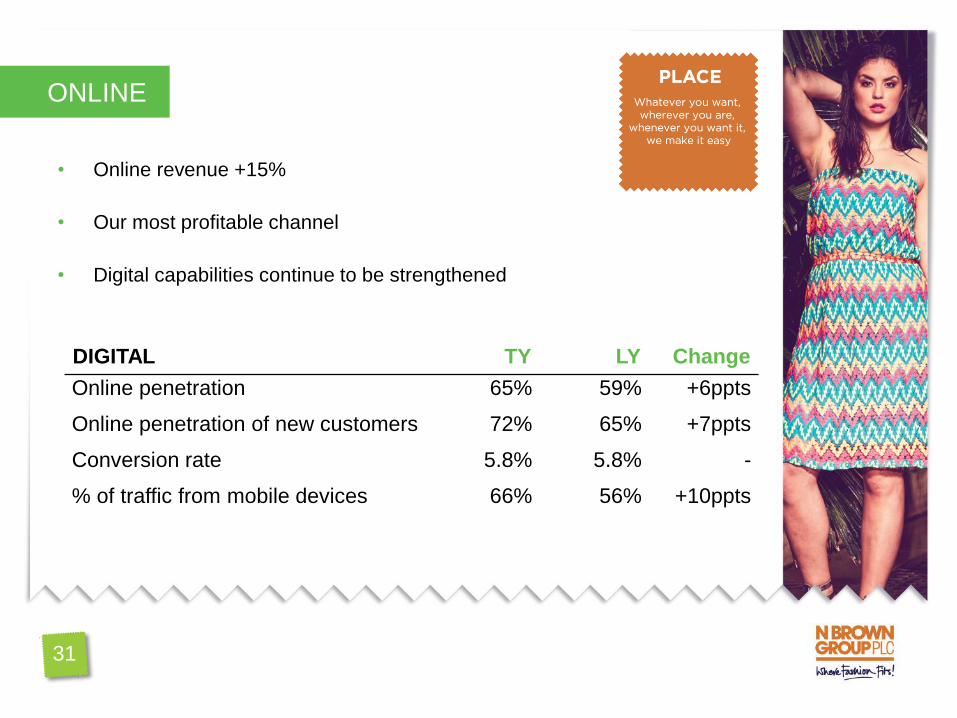

ONLINE

• Online revenue +15%

• Our most profitable channel

• Digital capabilities continue to be strengthened

DIGITAL TY LY Change

Online penetration 65% 59% +6ppts

Online penetration of new customers 72% 65% +7ppts

Conversion rate 5.8% 5.8% -

% of traffic from mobile devices 66% 56% +10ppts

31

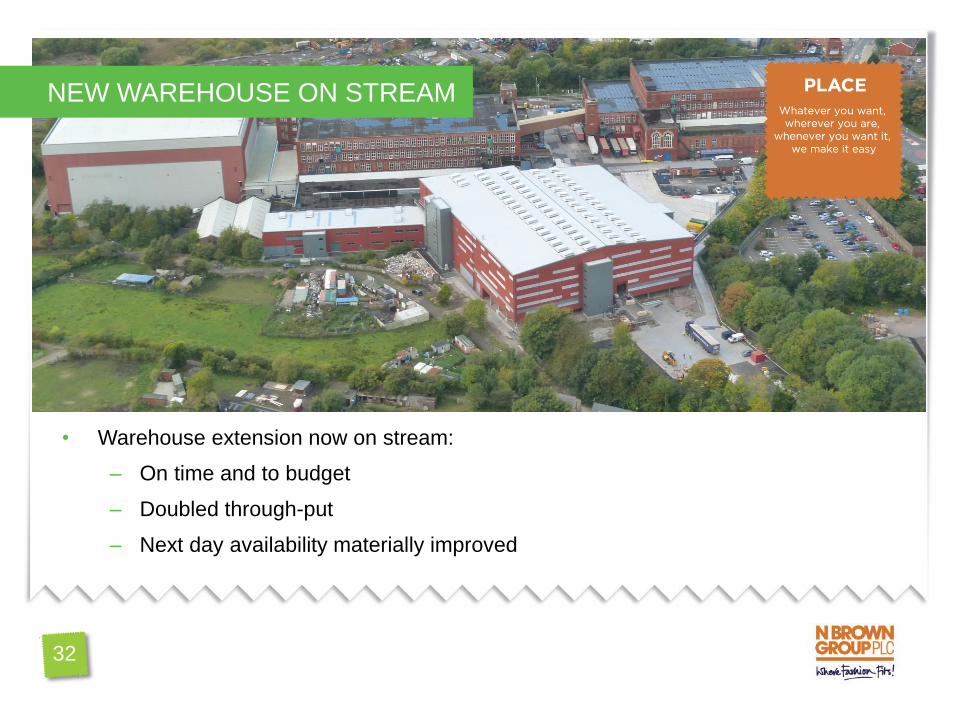

• Warehouse extension now on stream:

– On time and to budget

– Doubled through-put

– Next day availability materially improved

32

NEW WAREHOUSE ON STREAM

USA

33

• Revenue £14.3m, +29% (+20% constant fx)

• Operating loss £1.0m vs £2.5m FY15

• H2 $ profit: $0.2m profit vs $0.9m loss H2 FY15

• Improved profitability a result of:

– Customer order frequency

– Marketing efficiency

– Promotional efficiency

– Change to our delivery offering

• Launched JD Williams brand in March – early days but performing well

• New web platform live in USA in August

FINANCIALS

ANY QUESTIONS?

STRATEGIC UPDATE

SUMMARY

34

TRANSFORMATION DELIVERING RESULTS

35

• Clear evidence of strategic progress

• H2 profit growth represents a significant milestone

• Fit 4 the Future implementation a key priority for FY17

• Power Brands driving underlying growth

• Action under way to improve performance of Traditional segment

• Fashion industry backdrop suggests a challenging year

• Confident in our ability to make further progress this year

AGENDA

FINANCIALS & GUIDANCE

STRATEGY UPDATE

IMPROVING OUR RETAIL BASICS

FINANCIAL SERVICES

FIT 4 THE FUTURE

INTERNATIONAL & STORES UPDATE

Q&A

SUMMARY

43

FINANCIALS

STRATEGIC UPDATE

SUMMARY

ANY QUESTIONS?

36

APPENDIX

• Operating cash flow

• Group cash flow

• Exceptional cost breakdown

• Revenue by brand, H1 FY15, H1 FY16 and FY14

• Fit 4 the Future timescale, costs and benefits

• Financial Calendar

• Investor relations contacts

37

37

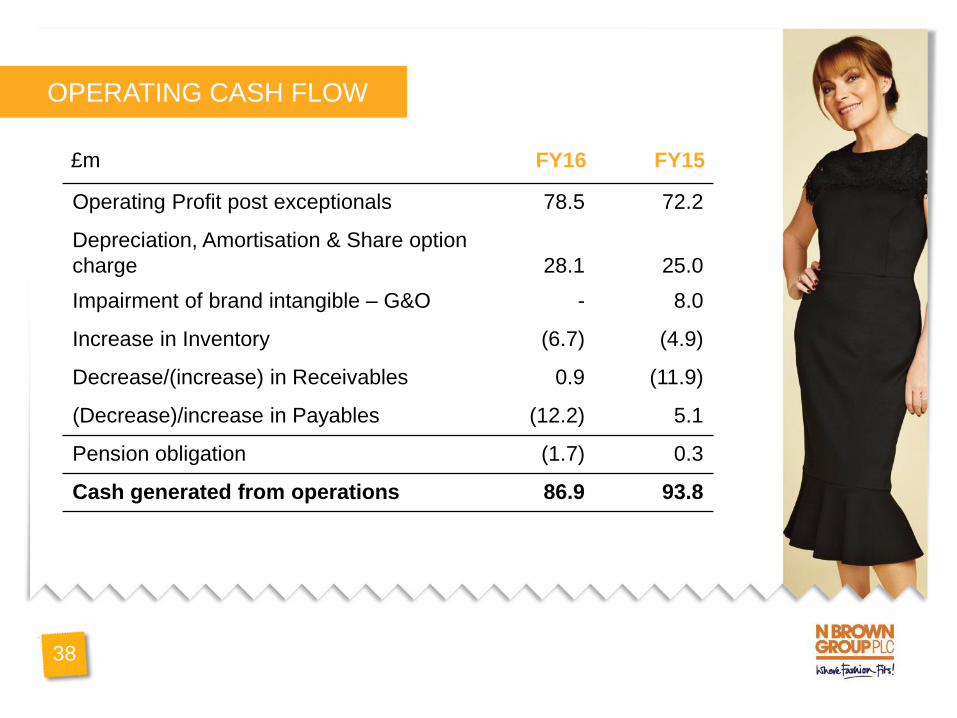

OPERATING CASH FLOW

38

£m FY16 FY15

Operating Profit post exceptionals 78.5 72.2

Depreciation, Amortisation & Share option

charge 28.1 25.0

Impairment of brand intangible – G&O - 8.0

Increase in Inventory (6.7) (4.9)

Decrease/(increase) in Receivables 0.9 (11.9)

(Decrease)/increase in Payables (12.2) 5.1

Pension obligation (1.7) 0.3

Cash generated from operations 86.9 93.8

17

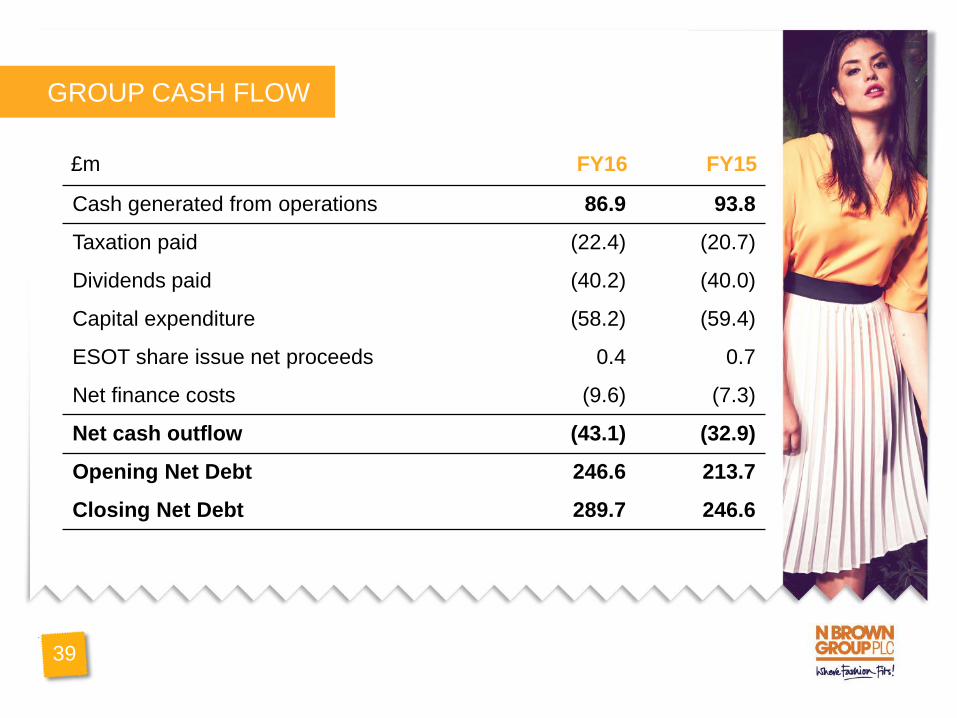

GROUP CASH FLOW

39

£m FY16 FY15

Cash generated from operations 86.9 93.8

Taxation paid (22.4) (20.7)

Dividends paid (40.2) (40.0)

Capital expenditure (58.2) (59.4)

ESOT share issue net proceeds 0.4 0.7

Net finance costs (9.6) (7.3)

Net cash outflow (43.1) (32.9)

Opening Net Debt 246.6 213.7

Closing Net Debt 289.7 246.6

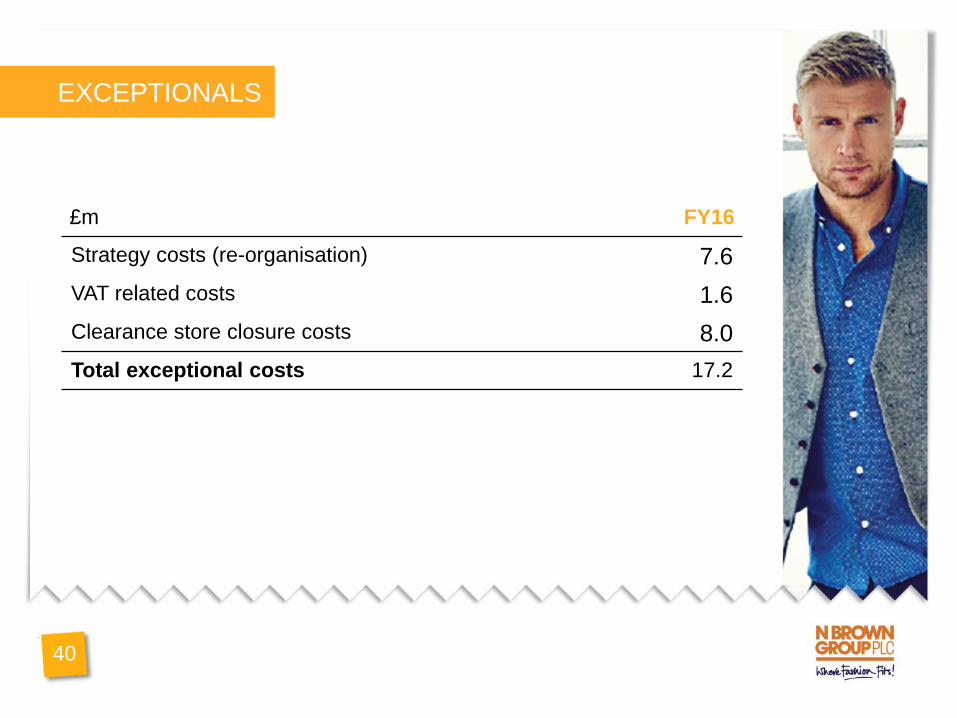

EXCEPTIONALS

£m FY16

Strategy costs (re-organisation) 7.6

VAT related costs 1.6

Clearance store closure costs 8.0

Total exceptional costs 17.2

40

REVENUE BY BRAND, FY14, H1 FY15 & H1 FY16

41

£m H1 FY16 H1 FY15 FY14

JD Williams 75.6 70.6 139.4

Simply Be 50.2 41.4 87.2

Jacamo 30.4 25.0 48.0

Power Brands 156.2 137.0 274.6

Traditional Brands 68.1 72.8 142.6

Secondary Brands 74.9 72.3 159.5

Product total 299.2 282.1 576.7

Test

International

Website Roll-Out

Planning

TransformationBuild

Test

UK

Website Roll-Out

Global

Multichannel

Transformation

Credit

Transformation

Build

Test

Live

Build

20162015 2017

Pilot

Live

FIT 4 THE FUTURE TIMESCALE

42

2019

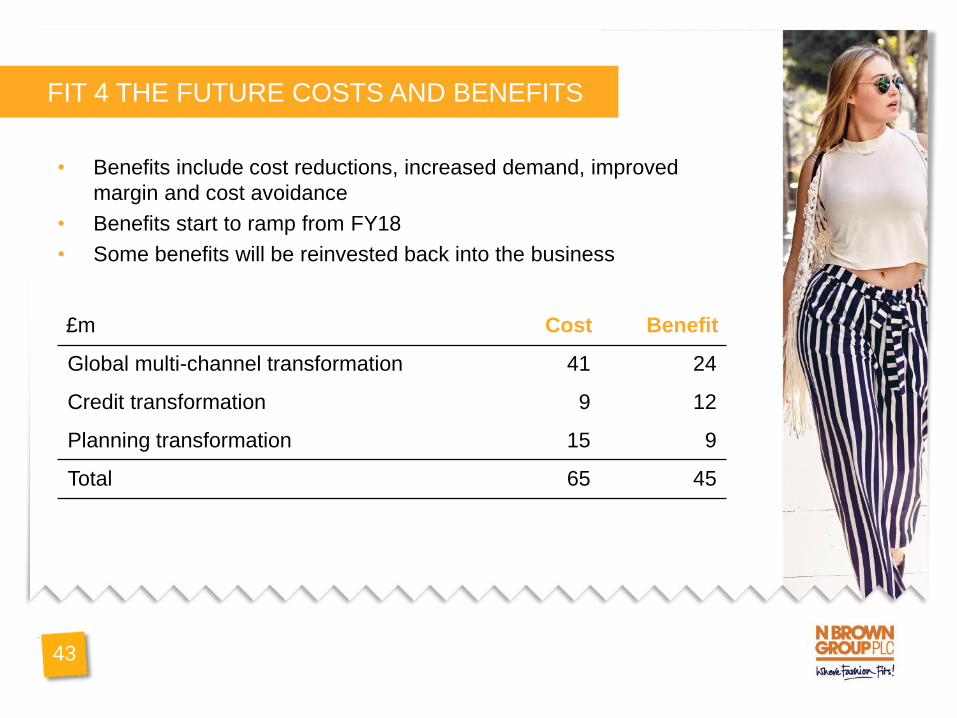

FIT 4 THE FUTURE COSTS AND BENEFITS

43

• Benefits include cost reductions, increased demand, improved

margin and cost avoidance

• Benefits start to ramp from FY18

• Some benefits will be reinvested back into the business

£m Cost Benefit

Global multi-channel transformation 41 24

Credit transformation 9 12

Planning transformation 15 9

Total 65 45

FINANCIAL CALENDAR

44

• Q1 trading statement 16th June 2016

• Interims 11th October 2016

IR CONTACT DETAILS

45

Bethany Hocking

Director of Investor Relations

Email: [email protected]

Tel: 0161 238 1845

Mobile: 07887 536 153