A study on fundamental equity valuation of the stock CHAPTER 1 INTRODUCTION 1.1 MEANING OF INVESTMENT Investment is time, energy, or matter spent in the hope of future benefits actualized within a specified date or time frame Investment is buying or creating an asset with the expectation of capital appreciation, dividends (profit), interest earnings, rents or some combination of these returns. This may or may not be backed by research and analysis. Most or all forms of investment involve some form of risk, such as investment in equities, property, and even fixed interest securities which are subject, among other things, to inflation risk. It is indispensable for project investors to identify and manage the risks related to the investment. 1.2 INVESTMENT OBJECTIVES The following are basic investment objectives. Maximization of return Investors always expect a good rate of return from their investments. Rate of return could be defined as the total income the investor receives during the holding period stated as a percentage of the purchasing price at the beginning of the holding period. Minimization of risk R. V. Institute of Management, Bengaluru Page 1

Transcript

A study on fundamental equity valuation of the stock

CHAPTER 1

INTRODUCTION

1.1 MEANING OF INVESTMENT

Investment is time, energy, or matter spent in the hope of future benefits actualized

within a specified date or time frame

Investment is buying or creating an asset with the expectation of capital appreciation,

dividends (profit), interest earnings, rents or some combination of these returns. This

may or may not be backed by research and analysis. Most or all forms of investment

involve some form of risk, such as investment in equities, property, and even fixed

interest securities which are subject, among other things, to inflation risk. It is

indispensable for project investors to identify and manage the risks related to the

investment.

1.2 INVESTMENT OBJECTIVES

The following are basic investment objectives.

Maximization of return

Investors always expect a good rate of return from their investments. Rate of

return could be defined as the total income the investor receives during the

holding period stated as a percentage of the purchasing price at the beginning of

the holding period.

Minimization of risk

Risk of holding securities is related with the probability of actual return becoming less

than the expected return. Investment risk is just as important as measuring its expected

rate of return because minimizing risk and maximizing rate of return are interrelated

objectives in the investment management.

Safety

The selected investment avenue should be under the legal and regulatory frame work. If

it is not under the legal frame work, it is difficult to represent the grievances, if any.

Approval of the law itself adds a flavour of safety. And investment done with the

government assures more safety than with the private party.

Liquidity

R. V. Institute of Management, Bengaluru Page 1

A study on fundamental equity valuation of the stock

Marketability of the investment provides liquidity to the investment. The liquidity

depends upon the marketing and trading facility. If a portion of the investment could be

converted into cash without much loss of time, it would help the investor meet the

emergencies. Stocks are liquid only if they command good market by providing adequate

return through dividends and capital appreciation.

Hedge against inflation

Since there is inflation in almost all the economy, the rate of return should ensure a

cover against the inflation. The rate of return should be higher than the rate of inflation,

otherwise the investor will have loss in real terms. Growth stocks would appreciate in

their values overtime and provide a protection against inflation. The return thus earned

should assure the safety of the principal amount, regular flow of income and be a hedge

against inflation.

R. V. Institute of Management, Bengaluru Page 2

A study on fundamental equity valuation of the stock

CHAPTER-2

2.1 INDUSTRY PROFILE

2.1 HISTORICAL BACKGROUND:

The equity brokerage industry in India is one of the oldest in the Asia region. India had

an active stock market for about 150 years that played a significant role developing risk

market as also promoting enterprise and supporting the growth of industry.

The roots of a stock market in India began in 1860s during the American civil war that

led to sudden surge in demand for cotton from India resulting in setting up of a number of

joint stock companies that issued securities to raise finance. This trend as akin to the

rapid growth of securities markets in Europe and the North America in the background of

expansion of railroads and exploration and natural resources and land development.

Historical records show that as early as 1864, there were about 1000 brokers with the

stock markets functioning from three places in Mumbai, between 9am to 7pm at the

junction of Meadows street and Rampart Row, from day break 9am and from 7pm to

early hours of next morning at Bazar gate.

Share prices rose sharply even at that time. A share of Colaba Land Company during the

boom period of the 1860s rose from Rs.10,000 at par to Rs.12,000 and that back day

shares went up from Rs.2,000 to Rs.54,000. Bombay, at that time, was major financial

center having housed 31 banks, 20 insurance companies and 62 joint stock companies.

Reports on stock markets around that time indicate that an ordinary broker in 1864 earned

about Rs.200 per day, a huge sum in those days. The boom period came to an abrupt end

in 1865. “Never had I witnesses in any place a run so widely distributed nor such distress

followed so quickly on the heels of such prosperity” thus wrote Richard Temple, who

served as the Governor of Bombay at that time. An interesting aspect is that despite the

collapse of the stock market, most of the brokers met their payment commitments.

R. V. Institute of Management, Bengaluru Page 3

A study on fundamental equity valuation of the stock

2.2CAPITAL MARKET OPERATIONS:

It consists mainly of primary market operation and secondary market operations. Primary

market or new issue market deals with the issue of new securities to investors on facilities

the corporate sectors in raising funds. The primary market is made up of two components:

where the firms go public for the first time through initial public offering and where the

firms which are already traded raise additional capital through seasoned equity offerings.

In the secondary market the securities which are floating and subscribed in the primary

market are traded with exchange. The primary function of stock exchange or secondary

market is providing liquidity of capital and continuous market for outstanding securities.

The stock exchange brings about a correct evaluation of securities and set prices of

securities close to their investment worth.

FOLLOWING ARE THE VARIOUS INVESTMENT ALTERNATIVES.

Negotiable and fixed income securities

1. Equity Shares

2. Preference Shares

3. Debentures

4. Bonds & Money Market Securities

5. Government Securities

Non – Negotiable Securities

1. Bank Deposits

R. V. Institute of Management, Bengaluru Page 4

A study on fundamental equity valuation of the stock

2. Post Office Deposit

3. NBFC Deposits

4. Tax Saving Schemes

5. Public Provident Fund

6. National Saving Scheme

7. Mutual Funds

8. Real Estate

9. Life Insurance

MARKETS:

In tune with the global stock markets that began to recover from the second half

of 2003, Indian stock markets too witnessed rapid growth. India’s two leading

indices, the most popular BSE Sensex, and the one most used by the markets the

National Stock Exchanges S&P CNX Nifty rose to record levels. Both primary

and secondary market activity experienced sharp surge. Much progress was made

in further strengthening and streamlining risk management, market regulation and

supervision. A few aspects of the major developments in the India’s stock markets

are described below.

MARKET STRUCTURE

Indian securities market is fairly large compared to several other emerging

markets. There are 28 stock exchanges in the country, through entire liquidity is

shared between the countries two national level exchanges namely, National

R. V. Institute of Management, Bengaluru Page 5

A study on fundamental equity valuation of the stock

Stock Exchange of India and the Bombay Stock Exchange Ltd. The regional

stock exchanges are in pursuit of business models that make them viable and

vibrant. Meanwhile, these exchanges have become members of the national

level exchanges through formation of subsidiaries whose business is showing

continuous growth and progress.

10.

With the abolition of the deferral products and introduction of uniform T+2

settlement cycle, the liquidity in these exchanges flowed to the national level

system consisting of NSE and BSE.

2.3 BOMBAY STOCK EXCHANGE AND ITS GROWTH

The Stock Exchange, Mumbai, popularly known as ‘BSE’ was established in 1875

as the native share and Stock Brokers Association. It is the oldest one in Asia, even

older than the Tokyo stock Exchange, which was established in 1878. It is a

voluntary non-profit making association of the persons and is currently engaged in

the process of converting itself into demutualized and corporate entity. It has

evolved over the years into its present status as the premier Stock Exchange in the

country. It is the first Stock Exchange in country to have obtained permanent

recognition in 1956 from the government of India under securities contracts act,

1956.

The Exchange while providing an efficient market also upholds the interest of

the

investors and insuresredressal of their grievances, whether against the companies or its

own member brokers. It also strives to educate the investors by making available

necessary informative inputs.

A Governing Body comprises nine of elected directors an Executive Director, a Reserve

Bank of India nominee and five Public representatives is the apex body, which regulates

the Exchanges and decides it policies.

The governing board following the election of directors annually elects a president, Vice-

President and an honorary treasurer from among the elected directors. The Executive

R. V. Institute of Management, Bengaluru Page 6

A study on fundamental equity valuation of the stock

Directors as the Chief Executive Officers is responsible for the day-to-day administration

of the Exchanges.

The Exchange has inserted new Rule No.126 A in its Rules, Bye-laws and Regulations

pertaining to constitution of the executive commission of the Exchange. Accordingly, an

Executive Committee, consisting of three elected directors, three SEBI nominees or

public representatives, Executive Directors and CEO and Chief Operating Officers has

been constituted. The committee considers judicial and quasi matters in which the

Governing Board has power’s as an Appellate Authority, matters regarding annulment of

transaction, admission, continuance of members brokers, declaration of a member-broker

as defaulter, norms, procedures and other matters relating to arbitration, fess, deposit,

margins, and other monies payable by the member-broker to the Exchange, etc.

2.4 NATIONAL STOCK EXCHANGE (NSE)

The high powered study group on establishment of new stock exchanges popularly

known as Pherwani Committee had in 1991 recommended the promotion of a new stocks

exchange at New Bombay as a model Stock Exchange and to act as National Stock

Exchange.

In order to provide nationwide Stock Exchange facilities to investors, upgrading the

facilities and to bring the Indian Capital market in line with the international markets in

1992, the National Stock Exchange was established. The exchange has two separate

segment viz., Capital market segment and money market segment. Capital market

segment would cover trading inequities, convertibles debenture, non-convertible

debentures etc., NSE provides access to investors from all across the

country on an equal footing and works as an integral component of the national stack

market system.

The growths of business on NSE in the recent years have been very impressive since

the time when exchanges started its operations, i.e., on November 3, 1994. Over the

period, the average trading volume has increased manifold.

The value of traded scrip’s during the year 1999 -2000 on NSE was Rs.8,39,052 crore

(40% of the total turnover of all the stock exchanges combined in India) compared to

R. V. Institute of Management, Bengaluru Page 7

A study on fundamental equity valuation of the stock

Rs.3,69,052 (30.49 % of the total turnover of all the stock exchangein India) on the

country’s premium bourse the BSE

2.5 INTRODUCTION TO EQUITY VALUATION

Equity Valuation:

The investor takes a number of decisions in the process of investment. The investor has to

decide about his risk tolerance level and the nature of assets to be brought weather they

are stocks or bonds or real estates. Once he decides the nature of the assets, he has to

select it from different alternatives. For example, if the common stock is chosen by the

investor he has to decide which company stock’s he has to buy. It may be Reliance

industry stock or the BHEL or IOC or any other company’s stock. Stocks are selected on

the basis of their return and risk. The investor analyses the risk and returns of holding a

particular stock for say five years or ten years. The risk and return analyses of the security

are known as security analysis.

Return:

The return from the stock includes both current income and capital gain caused by the

appreciation of the price. The income and capital gain are expressed as percentage of

money invested in the beginning. The historical returns are derived from the cash flow

received as well as the price changes that occur during the period of holding the stock or

any asset. The income flow is the dividend he receives during the holding period.

In simple terms

r = Price Change + Cash dividend x100

Purchase Price

Assumption;

While ascertaining the value of equity shares, different assumptions are made regarding

the company’s future profits, the amount and the timing of the dividends, the required

R. V. Institute of Management, Bengaluru Page 8

A study on fundamental equity valuation of the stock

rate of return etc. Therefore, different approaches have been developed for the valuation

of equity shares. These different approaches however, make the following assumptions

regarding the basic characteristics of equity shares:

1. Equity shares do not have any redemption date.

2. Equity shares do not have any given redemption or liquidating value. In case of

liquidation of the company, their claim is residual in nature and arising in the last

(after paying all external liabilities and the preference share holders).

3. Dividends on equity shares are neither guaranteed nor compulsory. Further,

neither the rate nor the timing of dividend is specified. So, the dividend can vary

in any directions.

Different approaches for the valuation of the equity shares can be analyzed as follows:

a) Valuation based on dividends.

b) Valuation based on earnings.

Valuation of Equity Shares based on Dividends

An investor buys an equity share in expectation of (i) a stream of future dividends from

the company and (ii) resale price of the equity share after some time when he is no longer

interested in holding the share. The owner of the share receives dividends as a

compensation for investing in the firm. So, as long as, the firm is operating profitable and

the investor holds the share, he would be expecting to receive a dividend from the

company. So, the dividends play a crucial and important role in determining the value of

equity shares. Though there is no legal compulsion to pay dividend on equity shares, still

most companies prefer to pay dividends in order to satisfy the expectation of their

shareholders.

R. V. Institute of Management, Bengaluru Page 9

A study on fundamental equity valuation of the stock

Assumptions: Valuation of the equity shares based on dividends requires the following

assumptions:

1 The dividends are payable annually.

2 The dividend is received after one year from the date of acquisition purchase.

3 Sale of equity share if any, occurs only at the end of a year and at the ex-dividend

terms.

Dividend Discount Model Single

Period Valuation Model

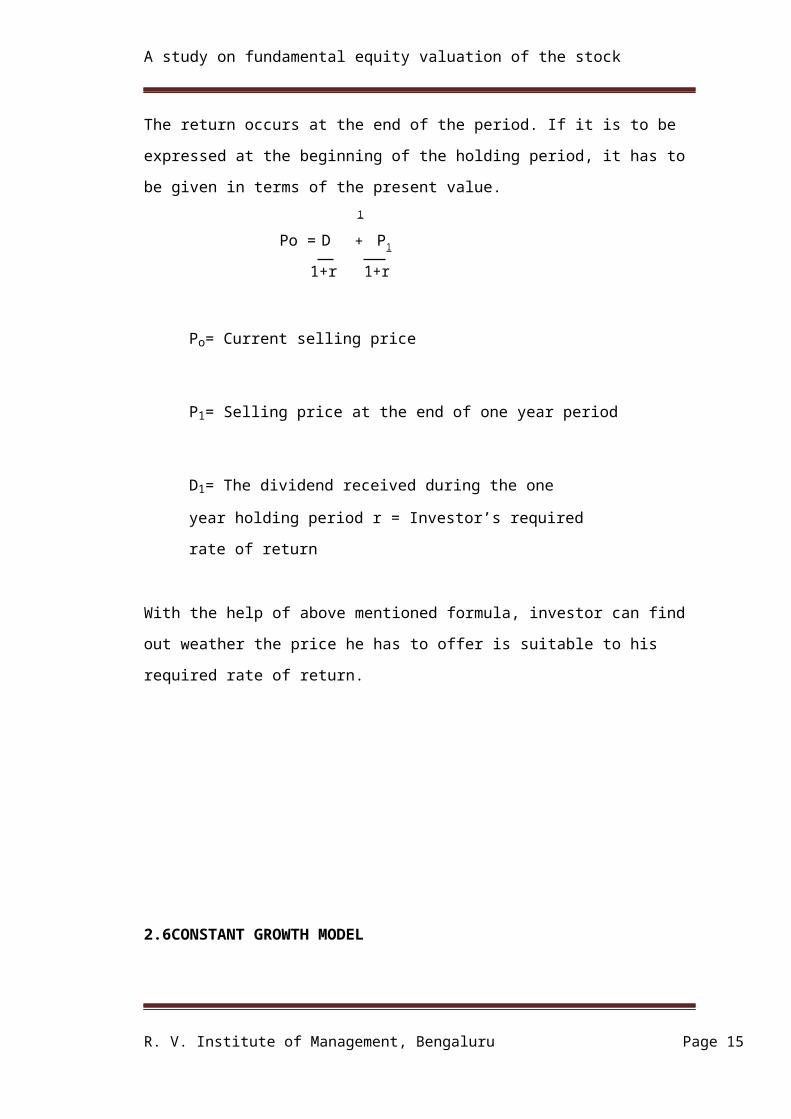

The return occurs at the end of the period. If it is to be expressed at the beginning of the

holding period, it has to be given in terms of the present value.

Po = D 1 + P 1

1+r 1+r

Po= Current selling price

P1= Selling price at the end of one year period

D1= The dividend received during the one year holding period r =

Investor’s required rate of return

With the help of above mentioned formula, investor can find out weather the price he has

to offer is suitable to his required rate of return.

R. V. Institute of Management, Bengaluru Page 10

A study on fundamental equity valuation of the stock

2.6CONSTANT GROWTH MODEL

In this model, the basic assumption is that dividends will grow at the same rate (g) into an

indefinite future.

Po = D(1+g) + D(1+g) 2 + D(1+g) 3 +…..+ D(1+g) N 1+r (1+r) 2

(1+r) 3 (1+r) n When the period approaches to infinity the

equation takes the form

Po = D1

r-g

Po= Present value of the stock r =

required rate of the return g = The

growth rate

D1=The next year dividend

This model is based on the assumption:

a) The firm’s dividend policy will be stable.

b) The firm will earn the stable return over the time.

This model is applicable when the analyst is able to predict all the three variable in the

equation namely (1) next years dividend, (2) the firm long term growth rate and,

(3) the required rate of return of the investor. Once the three values are known to the

analyst, the theoretical value or the present value of the stock can be computed and

compared with the driveling price, if

R. V. Institute of Management, Bengaluru Page 11

A study on fundamental equity valuation of the stock

Theoretical value > Actual price - >buy

Theoretical value < Actual price - >sell

Another advantage of this is that with the present selling price, next year’s dividend and

the growth rate, rate of return of the stock can be estimated.

Present rate of return > Required rate of return - > buy

Present rate of return < Required rate of return - < sell

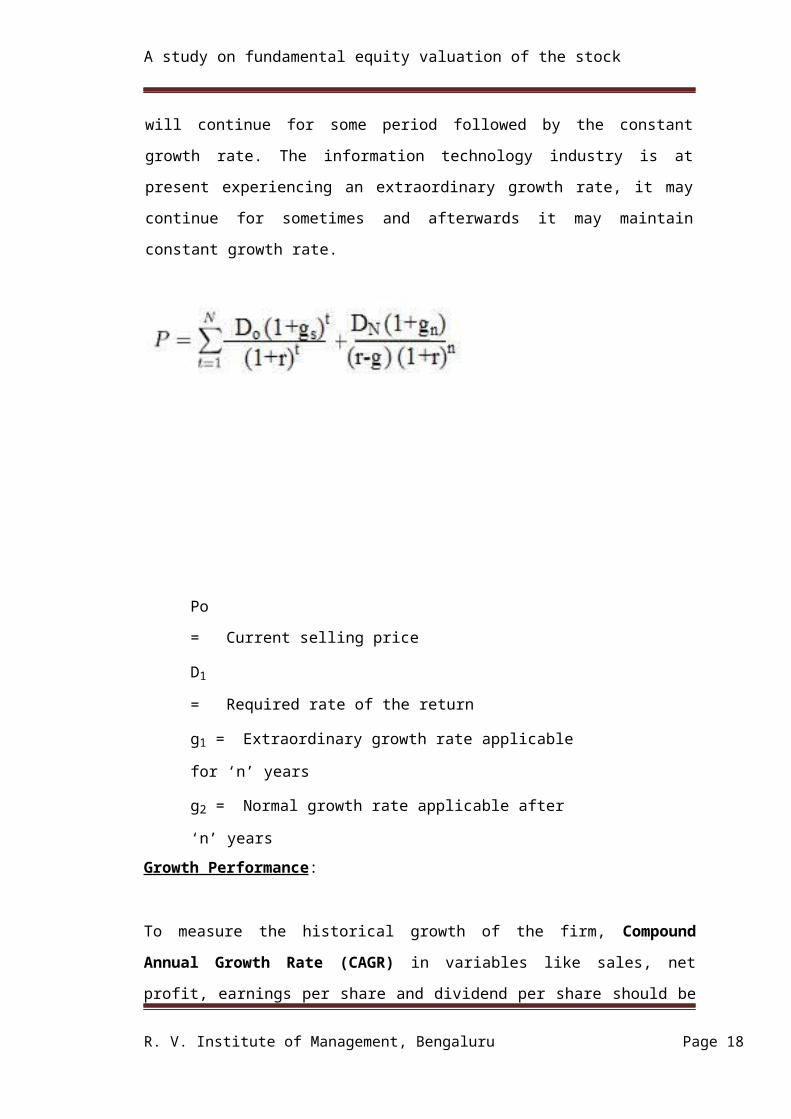

TWO STAGE GROWTH MODEL

The constant growth model is extended to two stage growth model. Here the growth

stages are divided into two, namely, a period of extraordinary growth and a constant

growth period of infinite nature. The extra ordinary growth period will continue for some

period followed by the constant growth rate. The information technology industry is at

present experiencing an extraordinary growth rate, it may continue for sometimes and

afterwards it may maintain constant growth rate.

Po = Current selling price

D1 = Required rate of the return

R. V. Institute of Management, Bengaluru Page 12

A study on fundamental equity valuation of the stock

g1 = Extraordinary growth rate applicable for ‘n’ years

g2 = Normal growth rate applicable after ‘n’ years

Growth Performance:

To measure the historical growth of the firm, Compound Annual Growth Rate

(CAGR) in variables like sales, net profit, earnings per share and dividend per share

should be calculated

CAGR of Dividend per Share: ( DPS for 2014 ÷ DPS for 2010) 1/5 - 1.

Sustainable Growth Rate: The sustainable growth rate is defined as:

Sustainable growth rate = Retention ratio × Return on equity.

Required Rate of return:

The investors required rate of return is calculated by applying Constant Dividend Growth

Model of Gordian.

2.7RELIANCE INDUSTRIES LTD:

Reliance Group;

The Reliance Group, founded by Dhirubhai H. Ambani (1932-2002), is India's largest

private sector enterprise, with businesses in the energy and materials value chain. Group's

annual revenues are in excess of US$ 58 billion. The flagship company, Reliance

Industries Limited, is a Fortune Global 500 company and is the largest private sector

company in India.

Backward vertical integration has been the cornerstone of the evolution and growth of

Reliance. Starting with textiles in the late seventies, Reliance pursued a strategy of

R. V. Institute of Management, Bengaluru Page 13

A study on fundamental equity valuation of the stock

backward vertical integration - in polyester, fibre intermediates, plastics, petrochemicals,

petroleum refining and oil and gas exploration and production - to be fully integrated

along the materials and energy value chain.

Reliance enjoys global leadership in its businesses, being the largest polyester yarn and

fiber producer in the world and among the top five to ten producers in the world in major

petrochemical products.

Major Group Companies are Reliance Industries Limited, including its subsidiaries and

Reliance Industrial Infrastructure Limited.

Significant contribution to India's economic growth

13.4 % of India’s total exports

6.9 % of the Government of India’s indirect tax revenues 4.8 %

of the total market capitalisation in India

Weightage of 11.9 % in the BSE Sensex

Weightage of 10.1 % in the S&P CNX Nifty Index

Growing importance across the globe

Largest refining capacity at any single location

Largest producer of Polyester Fibre and Yarn

5th largest producer of Paraxylene (PX) and Polypropylene (PP)

8th Largest producer of Purified Terephthalic Acid (PTA) and Mono Ethylene

Glycol (MEG)

R. V. Institute of Management, Bengaluru Page 14

A study on fundamental equity valuation of the stock

2.8INDIAN OIL CORPORATION LIMITED

IOC Overview

Indian Oil is India's flagship national oil company with business interests straddling the

entire hydrocarbon value chain – from refining, pipeline transportation and marketing of

petroleum products to exploration & production of crude oil & gas, marketing of natural

gas and petrochemicals. It is the leading Indian corporate in the fortune 'Global 500'

listing, ranked at the 98th position in the year 2011.

With over 34,000-strong workforce, Indian Oil has been helping to meet India’s energy

demands for over half a century. With a corporate vision to be the Energy of India, Indian

Oil closed the year 2010-11 with a sales turnover of Rs. 3,28,744 crore ($ 68,837 million)

and profits of Rs. 7445.48 crore ($ 1,719 million).

At Indian Oil, operations are strategically structured along business verticals - Refineries,

Pipelines, Marketing, R&D Centre and Business Development – E&P, Petrochemicals

and Natural Gas. To achieve the next level of growth, Indian Oil is currently forging

ahead on a well laid-out road map through vertical integration— upstream into oil

exploration & production (E&P) and downstream into petrochemicals – and

diversification into natural gas marketing and alternative energy, besides globalization of

its downstream operations. Having set up subsidiaries in Sri Lanka, Mauritius and the

United Arab Emirates (UAE), Indian Oil is simultaneously scouting for new business

opportunities in the energy markets of Asia and Africa.

R. V. Institute of Management, Bengaluru Page 15

A study on fundamental equity valuation of the stock

Chapter 3

Design of Report

3.1LITERATURE REVIEW:

Technical Analysis as explained by “The technical approach to investing is essentially are

flection of the idea that prices move in trends which are determined by the changing attitudes

of investors toward a variety of economic, monetary, political and psychological forces. The

art of technical analysis ± for it is an art- is to identify trend changes at an early stage and to

maintain an investment posture until the weight of the evidence indicates that the trend has

been reversed.” A method of evaluating securities by analysing statistics generated by market

activity, such as past prices and volume, Technical analysts do not attempt to measure a

security’s intrinsic value, but instead use charts to identify patterns that can suggest future

activity. Technical analysts believe that the historical performance of stocks and markets are

indications of future performance. Technical Analysis has become increasingly popular over

the past several years, as more and more people believe that the historical performance of a

stock is a strong indication of future performance. People using fundamental analysis have

always looked at the past performance of companies by comparing fiscal data from previous

quarters and years to determine future growth. The difference lies in the technical analyst is

belief that securities move according to very predictable trends and patterns. These trends

continue until something happens to change the trend, and until this change occurs, Price

levels are predictable. Hence, testing of technical analysis is important in order to enjoy the

benefit. William Sharpe said ³If you torture the data long enough, it will confess to any crime.

So important is the rule must work on data other than that used to discover it. There are many

evidences which support technical analysis, in July 1990 Journal of Finance article, jagadeesh

found predictable pattern in monthly returns for the period 1934 to 1987. His study revealed

that stocks with large losses in one month tend to show a significant reversal in the following

month and vice versa. In December 2000 Journal of Finance article, Lo, Ma may sky, and

Wang found that several technical indicators have some practical value as they provide

incremental information. This study is also based on sector analysis where from 4

industries in that 4-5 companies are analyzed using technical indicators. If the indicators

show more than 50% of positive results then the relevance of technical tools in trading

increases which will be helpful for investors

R. V. Institute of Management, Bengaluru Page 16

A study on fundamental equity valuation of the stock

3.2NEED FOR THE STUDY:

Valuation of the stocks is the first step towards intelligent investing. The knowledge of

securities market, particularly of the equity markets, is essential to come to grips with the

industry analysis and performance of the company through fundamental ratios. An investor

attempts to determine the worth of their shares based on the fundamentals, real value of stock

and some news from the media. Equity valuation is the most important and needed so as to

know the competitiveness of company with other companies and with industry benchmark.

It’s also needed to predict the future prices of the company to know where the company

stands which would help the investor to make better investing decisions either for long-term

period or for short-term period. Hence the study on fundamental analysis of RIL and IOL is

carried out.

3.3 STATEMENT OF THE PROBLEM:

“A study on fundamental equity valuation of the stock”

A method of evaluating a security that entails attempting to measure its intrinsic value

by examining related economic, financial and other qualitative and quantitative

factors. Fundamental analysts attempt to study everything that can affect the security's

value, including macroeconomic factors (like the overall economy and industry

conditions) and company-specific factors (like financial condition and management

3.4OBJECTIVES OF THE STUDY:

The main objectives of the study are:

To study the Stock Market and its functions.

To identify and evaluate the equity shares of RIL & IOC

To compare the market performance with that of selected stocks.

To know whether the equities are under-priced or over-priced and to suggest

R. V. Institute of Management, Bengaluru Page 17

A study on fundamental equity valuation of the stock

which to buy or to sell or to hold.

To predict the direction of national economy because economic activity affects the

corporate profit, investors attitudes and expectations and ultimately security

prices.

3.5 RESEARCH METHODOLOGY:

The project is on equity valuation where the equity share prices of the companies

are analyzed. The study is based on the past financial information of the Five

years and with the help of current market price of both the stocks while

calculating the future price using model of equity valuation. The nature of data

collection is mainly based on the information available through Secondary Data

and with the help of analytical tools.

Secondary Data:

The main source of information is annual reports of the companies and related

websites which has enabled in analyzing the equities.

Internet sources

Annual Reports

Text Books

Primary Data:

The primary sources of information collection were through discussion with the

faculties and the advisors in the company.

R. V. Institute of Management, Bengaluru Page 18

A study on fundamental equity valuation of the stock

3.6SCOPE OF THE STUDY:

The concept of risk, return and dividend paid, as the determinants of the value are

fundamentals and valid to validation of the securities.

At the outset it’s not easy to predict the rates and prices of stocks.

Investor can design their investment and financing activities in the way which

exploits the relevant variables to maximize the shares value in market

3.7LIMITATIONS OF THE STUDY:

The study has certain limitations like;

Need to adapt to each company Methods of fundamental valuation may vary

depending on the industry and the unique factors of a particular company.

Lack of fundamental analysis is the hope for a certain outcomes

The adaptation of methods of analysis for each company or industry can be very

long.

Stock market and the prices of stock are driven by the desires of investors, any

news from Government and information from insider of the company.

Information on average normal growth rate of industry was not available.

R. V. Institute of Management, Bengaluru Page 19

A study on fundamental equity valuation of the stock

CHAPTER 4

DATA ANALYZING AND DATA INTERPRETATION

4.1 KEY FINANCIAL RATIOS OF RELIANCE INDUSTRIES LTD

CURRENT RATIO:

The current ratio is a financial ratio that measures whether or not a firm has enough

resources to pay its debts over the next 12 months. It compares a firm's current assets to

its current liabilities. To pay short-term obligations, it includes inventories. A current ratio

of assets to liabilities of 2:1 is usually considered to be acceptable

Current Ratios = Current assets

Current liabilities

Year 2014 2013 2012 2011 2010

Ratio 1.11 1.43 1.44 1.16 1.04

1.6

1.4

1.2

1

0.8Ratios

0.6

0.4

0.2

02014 2013 2012 2011 2010

Chart 4.1.1: current ratio of reliance industries ltd

R. V. Institute of Management, Bengaluru Page 20

A study on fundamental equity valuation of the stock

Interpretation:-

Current ratio of the company shows the decreasing from last year. In the year 2010 it

was 1.04, in the year 2011 it has been raised to 1.16 and in the year 2012 it has

reached to 1.44 and in the year 2013 it is steadily decrease by 0.01 to 1.43 and in the

year of 2014 rapidly decreased by 0.32 to1.11. It means that it is liable to pay its

liabilities for the upcoming periods. It has maintained the standard form i.e. 2:1.

QUICK RATIO:

An indicator of a company’s short-term liquidity. The quick ratio measures a

company’s ability to meet its short-term obligations with its most liquid assets. For

this reason, the ratio excludes inventories from current assets.

Year 2014 2013 2012 2011 2010

Ratio 1.03 1.12 1.17 0.94 0.69

1.2

1

0.8

0.6Ratios

0.4

0.2

02014 2013 2012 2011 2010

Chart 4.1.2: Quick Ratio of reliance industries ltd

Interpretation:

According above shown graph in the year 2010 there was lower ratio which was

0.69 compare to the other four years ratio so, that was bad sign for the company and

there was lower cash convertible assets. And in the year 2012 it was 1.17 higher than

the other four years ratio, and in the year 2014 it was 1.03.

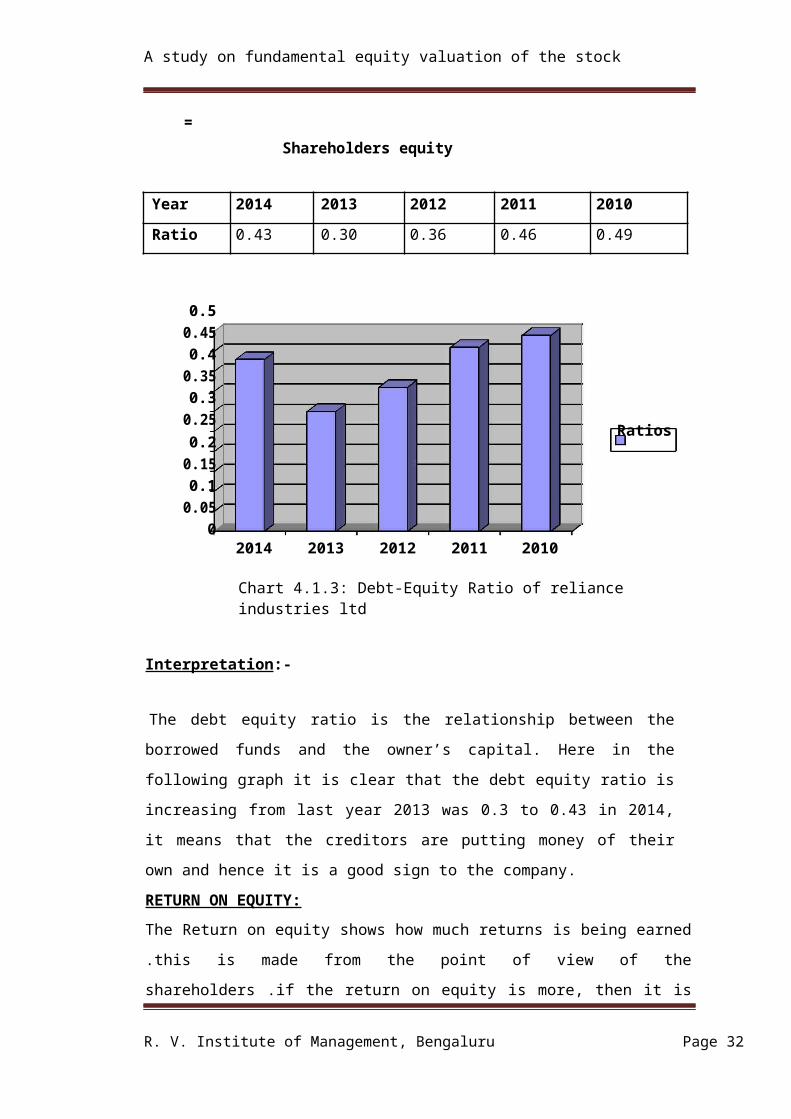

DEBT-EQUITY RATIO:

R. V. Institute of Management, Bengaluru Page 21

A study on fundamental equity valuation of the stock

The Debt / Equity ratio measures the long term financial solvency of firm. It also

measure of a company’s financial leverage calculated by dividing its total liabilities

by stockholders’ equity. It indicates what proportion of equity and debt the company

is using to finance its assets. It is calculated as follows

D/E Ratio = Total Liabilities

Shareholders equity

Year 2014 2013 2012 2011 2010

Ratio 0.43 0.30 0.36 0.46 0.49

0.50.450.4

0.350.3

0.25Ratios

0.20.150.1

0.050

2014 2013 2012 2011 2010

Chart 4.1.3: Debt-Equity Ratio of reliance industries ltd

Interpretation:-

The debt equity ratio is the relationship between the borrowed funds and the owner’s

capital. Here in the following graph it is clear that the debt equity ratio is increasing

from last year 2013 was 0.3 to 0.43 in 2014, it means that the creditors are putting

money of their own and hence it is a good sign to the company.

RETURN ON EQUITY:

The Return on equity shows how much returns is being earned .this is made from the

point of view of the shareholders .if the return on equity is more, then it is said to be the

most demanded shares in the market. Net income is for the fiscal year shareholders

equity does not include preferred shares. Also known as “return on net worth”(RONW).

R. V. Institute of Management, Bengaluru Page 22

A study on fundamental equity valuation of the stock

Return on equity = PAT *100

Shareholders fund

YEAR 2014 2013 2012 2011 2010

RATIO 11.15 11.66 12.30 13.88 12.64

14

12

10

8

6 Ratios

4

2

02014 2013 2012 2011 2010

Chart 4.1.4: Return on Equity Ratio of reliance industries ltd

Interpretation:

In the above graph there is steadily decrease in the ratio from 2012 to 2014. Which

shows the performance of the company in the market how bad it is? If the trend is

continuous in the future it is very bad sign to the company.

EARNING PER SHARE:

Earnings per-share (EPS) is the amount of earnings per each outstanding share of a

company's stock. The portion of a company’s profit allocated to each outstanding share

of common stock. EPS serves as an indicator of a company’s profitability. It can be

calculated in the following way

R. V. Institute of Management, Bengaluru Page 23

A study on fundamental equity valuation of the stock

EPS = Net profit available to the equity shareholders *100

Number of ordinary shares outstanding

Year 2014 2013 2012 2011 2010

Ratio 68.02 65.05 61.26 61.97 49.64

70

60

50

40

30 Ratios

20

10

02014 2013 2012 2011 2010

Chart 4.1.5: Earning Per Share Ratio of reliance industries ltd

Interpretation:-

The EPS indicates that the Earnings of a Share. By the following graph it is clear that

the EPS is continuously increasing from 2010 to 2014. And there was a drastic change

in the EPS in the year 2011, which was good turn point to the company.

DIVIDEND YEILD RATIO:

Dividend Yield or Dividends paid to holders of common stock are set by management,

usually with regard to the company's earnings. There is no guarantee that future

dividends will match past dividends or even be paid at all. The most commonly-cited

figure for dividend yield is the historic yield which is calculated using the following

formula

Dividend Yield Ratio = Dividend

Current Market Price

R. V. Institute of Management, Bengaluru Page 24

A study on fundamental equity valuation of the stock

YEAR 2014 2013 2012 2011 2010

RATIO 1.1 1.1 1 0.8 0.7

1.2

1

0.8

0.6 Ratios0.4

0.2

02014 2013 2012 2011 2010

Chart 4.1.6: Dividend Yield Ratio of reliance industries ltd

Interpretation:-

The dividends are paid on the face value of 10. The company paid the dividend in both

the year i.e. in 2013 and 2014 11 or 110 %. But in the year 2010 the company paid the

dividend of 7 or 70%. There is a increase of 4 or 40% in the payment of the dividend.

Which shows the good sign to the company for the long run.

DIVIDEND PAYOUT RATIO:

Dividend payout ratio is the fraction of net income a firm pays to its stockholders in

dividends. It is the percentage of earnings paid to shareholders in dividends. It is

calculated as follows;

R. V. Institute of Management, Bengaluru Page 25

A study on fundamental equity valuation of the stock

Dividend payout ratio = Dividend paid *100

EPS

Year 2014 2013 2012 2011 2010

Ratio 12.7 12.51 12.62 11.75 12.84

13

12.8

12.6

12.412.2

12 Ratios

11.8

11.6

11.411.2

2014 2013 2012 2011 2010

Chart 4.1.7: Dividend Payout Ratio of reliance industries ltd

Interpretation:-

In the above graph it states that the firm’s ability to pay the dividends to the

shareholders. Even firm’s payment ratio is increasing. The firm here is able to pay the

dividends. The payout ratio is minor fluctuation every year. In the year 2010 it was

12.84, in the year 2011 there was decrease to 11.75 in 2012 and it has increased to

12.51, in the year 2013 it was goes to12.62 and in the year 2014 it was goes up to 12.7.

EARNING RETANTION RATIO:

The percentage of a publicly-traded company's post-tax earnings that are not paid in

dividends. Most earnings retained are re-invested into the company's operations.

Tracking year-on-year earnings retention ratios is important to fundamental analysis to

investigate whether a company is increasing or decreasing its rate of re-investment.

R. V. Institute of Management, Bengaluru Page 26

A study on fundamental equity valuation of the stock

Calculated as:

Year 2014 2013 2012 2011 2010

Ratio 87.3 87.49 86.41 87.85 86.42

88

87.5

87

86.5Ratios

86

85.52014 2013 2012 2011 2010

Chart 4.1.8: Earning Retention Ratio of reliance industries ltd

Interpretation:-

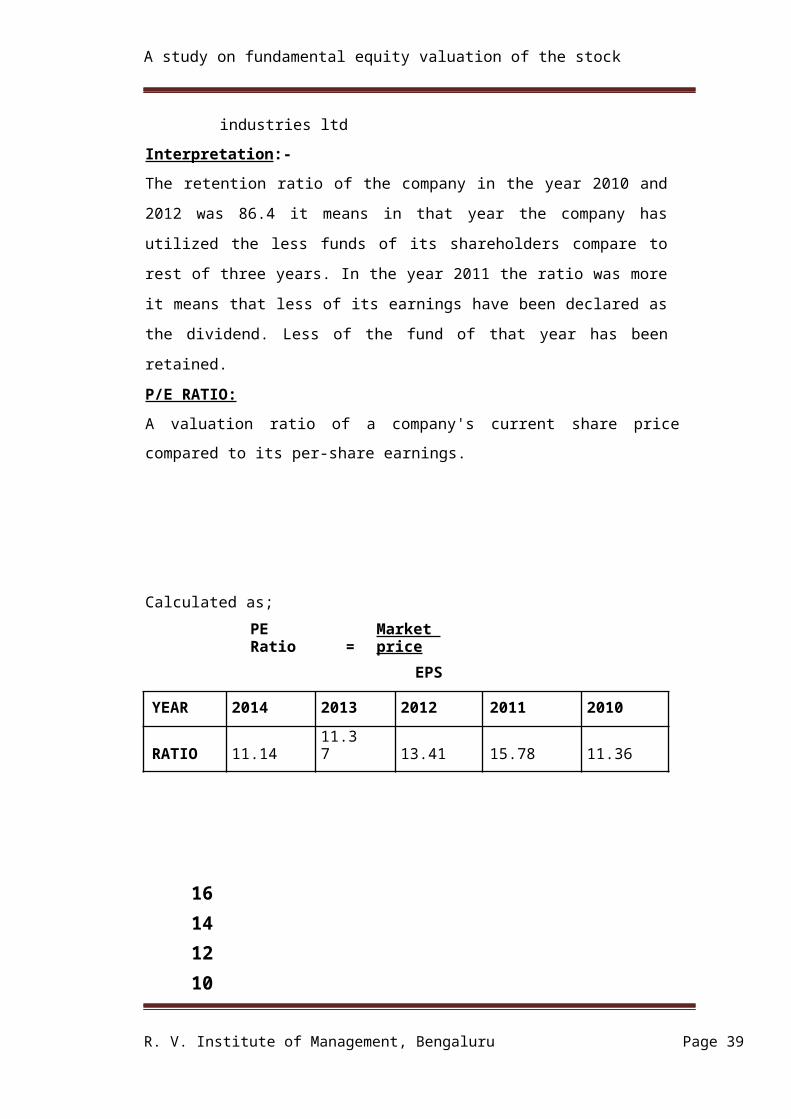

The retention ratio of the company in the year 2010 and 2012 was 86.4 it means in

that year the company has utilized the less funds of its shareholders compare to rest

of three years. In the year 2011 the ratio was more it means that less of its earnings

have been declared as the dividend. Less of the fund of that year has been retained.

P/E RATIO:

A valuation ratio of a company's current share price compared to its per-share

earnings.

R. V. Institute of Management, Bengaluru Page 27

A study on fundamental equity valuation of the stock

Calculated as;

PE Ratio = Market price

EPS

YEAR 2014 2013 2012 2011 2010

RATIO 11.14 11.37 13.41 15.78 11.36

16

14

12

10

8 Ratios6

4

20

2014 2013 2012 2011 2010

Chart 4.1.9: P/E Ratio of reliance industries ltd

Interpretation:-

The P/E Ratio (Prospective) is high in the year 2011. And in the year 2014 it was less

compare to other four years. It decreased in the 2014. This is only because of the

changes in the market price of the stock every year.

PRICE TO BOOK VALUE:

A ratio used to compare a stock's market value to its book value. It is calculated by

dividing the current closing price of the stock by the latest quarter's book value per

share. Also known as the "price-equity ratio".

R. V. Institute of Management, Bengaluru Page 28

A study on fundamental equity valuation of the stock

Calculated as:

Year 2014 2013 2012 2011 2010

Ratio 609.78 557.49 498.21 446.25 392.51

700

600

500

400

300 Ratios

200

100

02014 2013 2012 2011 2010

Chart 4.1.10: Price to Book Value of reliance industries ltd

Interpretation:-

The Book value is too high in the year 2014. It has increased from 2010. And there is

continuous increase in the share price. On the book value of the share we cannot take

any kind of decision for the investment. Because it is historical value.

R. V. Institute of Management, Bengaluru Page 29

A study on fundamental equity valuation of the stock

Fundamental Ratios of Reliance Industries Limited

2014 2013 2012 2011 2010

Current Ratio1.11 1.43 1.44 1.16 1.04

Quick Ratio 1.03 1.12 1.17 0.94 0.69

Return on Equity11.15 11.66 12.30 13.88 12.64

Debt Equity Ratio 0.43 0.30 0.36 0.46 0.49

Dividend Yield Ratio 1.1 1.1 1.0 0.8 0.7

Dividend Payout Ratio 12.7 12.51 12.62 11.75 12.84

Earnings Retention Ratio 87.3 87.49 86.41 87.85 86.42

P/E Ratio 11.14 11.37 13.41 15.78 11.36

Price to Book Value 609.78 557.49 498.21 446.25 392.51

EPS Ratio 68.02 65.05 61.26 61.97 49.64

4.1: Table showing Financial Ratios of Reliance Industries

CAGR of DPS = ( DPS of year 2015 ÷ DPS of year 2010) - 1

DPS for year 2014 is Rs.9.5 for a face value of Rs.10. (9.5 X 5years= 47.5)

= (9.5 ÷ 7) - 1

= 0.3157 OR 35.71 %

Average Retention Ratio = (0.873+0.875+0.864+0.878+0.864) / 5 =

0.871 OR 87.1%

Average Payout Ratio = (1 – 0.6241)

= 0.376 OR 37.6%

Average Return on equity = ( 0.11+0.12+0.12+0.14+0.13) / 5 =

0.1233 OR 12.33 %

Expected Growth Rate (g) = Average Retention Ratio X Average Return on Equity.

R. V. Institute of Management, Bengaluru Page 30

A study on fundamental equity valuation of the stock

= 0.871 X 0.123

= 0.1071 OR 10.71 %

Constant Growth Model:

Using this model Required rate of return is found.

Po = D1

r-g

Po= Present value of the stock= 861 as on Feb-2015

D1=The next year dividend = Do(1+g) = 9.5 (1 + 0.1071) = 10.52 per share r =

Required rate of the return = ?

g = the growth rate = 10.71% OR 0.1071

r = D1 + g

Po

r = 11.93%

The investors required rate of return would be r = 11.93%

Single Period Valuation Model:

Applying the single period valuation model and finding out share prices for next

year.

Po = D 1 + P 1

1+r 1+r

Where,

Po= Present selling price = Rs.861 as on Feb-2015 P1=

Selling price at the end of one year period

D1= the dividend received during the one year holding period, D1= Do (1+g)

Do = Current year dividend=9.5

r = Investor’s Required rate of return = 11.93%

D1= Do (1+g) = 9.5(1 + 0.1071) = 10.52 per share

P1 = 1068.16/per shareTwo Stage Growth Model:

R. V. Institute of Management, Bengaluru Page 31

A study on fundamental equity valuation of the stock

Po = Current selling price = ?

r = Required rate of the return = 0.1193 or 11.93%

g1 = Extraordinary growth rate applicable for ‘n’ years = 0.15 or 15% g2 =

Normal growth rate applicable after ‘n’ years = 0.1052 or 10.52% n = 5

years

D0 = 9.5

By substituting the above stated values the calculated current stock price is: Po

= Rs.864.04 per share.

4.2Key Financial Ratios of Indian Oil Corporation Ltd;

CURRENT RATIO:

The current ratio is a financial ratio that measures whether or not a firm has

enough resources to pay its debts over the next 12 months. It compares a firm's

current assets to its current liabilities. A current ratio of assets to liabilities of 2:1 is

usually considered to be acceptable

Current Ratios = Current assets

Current liabilities

Year 2014 2013 2012 2011 2010

Ratio 0.81 0.84 0.83 0.8 0.76

0.84

0.82

0.8

0.78Ratios

0.76

0.74

0.72

R. V. Institute of Management, Bengaluru Page 32

A study on fundamental equity valuation of the stock

2014 2013 2012 2011 2010

Chart 4.2.1: Current Ratio of Indian Oil Corporation Ltd

Interpretation:-

The current ratio in the year 2010 was 0.76, and in the year 2011 it has increased to

0.80 which shows the good indication to the company. And in the year 2012 it has

been increased again to 0.83,in the year 2013 it was 0.84, and in the year 2014 it

was decreased to 0.81. At least it has to maintain its current ratio= 2:1

QUICK RATIO:

Quick ratio is a test of liquidity than the current ratio. The term liquidity refers to the

ability of a firm to pay its short-term obligation as & when they become due. Quick ratio

may be defined as the relationship between quick or liquid assets and current liabilities.

An assets is said to be liquid if it is converted into cash within a short period without loss

of value.

Year 2014 2013 2012 2011 2010

Ratio 0.64 0.79 0.74 0.51 0.45

0.8

0.7

0.6

0.5

0.4Ratios

0.3

0.2

0.10

2014 2013 2012 2011 2010

Chart 4.2.2: Quick Ratio of Indian Oil Corporation Ltd

Interpretation:

According above shown graph in the year 2010 there was lower ratio compare to the

other four years ratio so, that was bad sign for the company and there was lower cash

R. V. Institute of Management, Bengaluru Page 33

A study on fundamental equity valuation of the stock

convertible assets. And in the year 2013 it was 0.79 higher than the other four years

ratio, and in the year 2014 it was 0.64.

DEBT-EQUITY RATIO:

The Debt / Equity ratio measures the long term financial solvency of firm. It also

reflects the relative proportion of debt and equity in financing the asset of the firm. It

is calculated as follows,

D/E Ratio = Total debt

Shareholders equity

Year 2014 2013 2012 2011 2010

Ratio 1.22 1.28 1.22 0.95 0.88

1.4

1.2

1

0.8

0.6 Ratios

0.4

0.2

02014 2013 2012 2011 2010

Chart 4.2.3: Debt-Equity Ratio of Indian Oil Corporation Ltd

Interpretation:-

The debt equity ratio is the relationship between the borrowed funds and the owner’s

capital. Here in the following graph it is declared that the debt equity ratio is

increasing comparing to past year. But in the year 2014 it is comparatively decrease.

It means that the creditors are putting more money of their own and hence it is a good

sign to the company.

RETURN ON EQUITY:

The Return on equity shows how much returns is being earned .this is made from the

point of view of the shareholders .if the return on equity is more then it is said to be the

R. V. Institute of Management, Bengaluru Page 34

A study on fundamental equity valuation of the stock

most demanded shares in the market.

Return on equity = PAT *100

Shareholders fund

YEAR 2014 2013 2012 2011 2010

RATIO 10.64 8.2 6.83 13.45 20.21

25

20

15

10Ratios

5

02014 2013 2012 2011 2010

Chart 4.2.4: Return on Equity Ratio of Indian Oil Corporation Ltd

Interpretation:

The Return on equity shows how much returns is being earned .this is made from the

point of view of the shareholders .if the return on equity is more then it is said to be the

most demanded shares in the market.

But in the following graph there was decrease in the ratio from 2008 to 2009. But there

was slight rise in the year 2010.

EARNING PER SHARE:

Earnings per-share (EPS) is the amount of earnings per each outstanding share of a

company's stock. It can be calculated in the following way

EPS = Net profit available to the equity shareholders *100

R. V. Institute of Management, Bengaluru Page 35

A study on fundamental equity valuation of the stock

Number of ordinary shares outstanding

Year 2014 2013 2012 2011 2010

Ratio 28.91 20.61 16.29 30.67 42.1

454035302520 Ratios151050

2014 2013 2012 2011 2010

Chart 4.2.5: Earning Per Share Ratio of Indian Oil Corporation Ltd

Interpretation:-

The EPS indicates the earnings of a share. By the following graph it is clear that the

EPS is fluctuated between the five years. But there was an increase in the year 2010

comparing to other four years. It shows that the company is going to be financially

strengthen in the years

DIVIDEND YIELD RATIO:

Dividend Yield or Dividends paid to holders of common stock are set by management,

usually with regard to the company's earnings. There is no guarantee that future

dividends will match past dividends or even be paid at all. The most commonly-cited

figure for dividend yield is the historic yield which is calculated using the following

formula

Dividend Yield Ratio = Dividend

R. V. Institute of Management, Bengaluru Page 36

A study on fundamental equity valuation of the stock

Current Market Price

YEAR 2014 2013 2012 2011 2010

RATIO 3.4 2 1.6 2.6 4.4

4.54

3.53

2.52 Ratios

1.51

0.50

2014 2013 2012 2011 2010

Chart 4.2.6: Dividend Yield Ratio of Indian Oil Corporation Ltd

Interpretation:-

In the year 2008 the company has announced the dividend of 5.50 or 55 % and in the

year 2009 it has been increased to 7.5 or 75 % which is a very good to the investors

and in the year 2010 it has been increased to 13 or 130 %. It depends upon the nature

of the investors, some are interested in the capital appreciation and few are in dividends.

The dividends are paid on face value of 10.

DIVIDEND PAYOUT RATIO:

Dividend payout ratio is the fraction of net income a firm pays to its stockholders in

dividends. It is calculated as follows;

Dividend payout ratio = Dividend paid *100

EPS

R. V. Institute of Management, Bengaluru Page 37

A study on fundamental equity valuation of the stock

Year 2014 2013 2012 2011 2010

Ratio 30.09 30.07 30.69 30.97 30.88

31

30.8

30.6

30.4

30.2 Ratios

30

29.8

29.62014 2013 2012 2011 2010

Chart 4.2.7: Dividend Payout Ratio of Indian Oil Corporation Ltd

Interpretation:-

This states the firm’s ability to pay the dividends to the shareholders. The dividend

payment ratio in the year 2011 is 30.97 that’s highest among the five years and in the

last two year 2013 and 2014 it were 30.07 and 30.09 are lower. The graph shows the

decreasing trend year by year.

EARNINGS RETANTION RATIO:

The percentage of a publicly-traded company's post-tax earnings that are not paid in

dividends. Most earnings retained are re-invested into the company's operations. Tracking

year-on-year earnings retention ratios is important to fundamental analysis to investigate

whether a company is increasing or decreasing its rate of re-investment.

R. V. Institute of Management, Bengaluru Page 38

A study on fundamental equity valuation of the stock

Calculated as:

Year 2014 2013 2012 2011 2010

Ratio 60.66 69.89 89.34 67.78 69.62

908070605040 Ratios3020100

2014 2013 2012 2011 2010

Chart 4.2.8: Earning Retention Ratio of Indian Oil Corporation Ltd

Interpretation:-

The retention ratio of the company in the year 2012 it was 89.34 it means in that year

the company has utilized the more funds of its shareholders comparing to both the

five years. In the year 2014 it was 60.66, the ratio was less it means that more of its

earnings have been declared as the dividend. Less of the fund of that year has been

retained.

R. V. Institute of Management, Bengaluru Page 39

A study on fundamental equity valuation of the stock

P/E RATIO:

A valuation ratio of a company's current share price compared to its per-share earnings.

Calculated as;

PE Ratio = Market price

EPS

YEAR 2014 2013 2012 2011 2010

RATIO 8.6 16.8 17.6 11.4 6.6

18161412108 Ratios6420

2014 2013 2012 2011 2010

Chart 4.2.9: P/E Ratio of Indian Oil Corporation Ltd

Interpretation:

The P/E Ratio was high in the year 2012 i.e.,17.6 and in the year 2010 it was just 6.6.

And in decreased in the year 2014 it has come to 8.6. This is only because of the changes

in the market price every year.

PRICE TO BOOK VALUE:

A ratio used to compare a stock's market value to its book value. It is calculated by

dividing the current closing price of the stock by the latest quarter's book value per

share.

R. V. Institute of Management, Bengaluru Page 40

A study on fundamental equity valuation of the stock

Also known as the "price-equity ratio".

Calculated as:

Year 2014 2013 2012 2011 2010

Ratio 271.8 251.75 238.38 227.9 208.21

300

250

200

150 Ratios

100

50

02014 2013 2012 2011 2010

Chart 4.2.10: Price to Book Value of Indian Oil Corporation Ltd

Interpretation:-

The Book value is too high in the year 2014.It has increased from 2010. On the book

value of the share we cannot take any kind of decision for the investment. Because it is

historical value.

R. V. Institute of Management, Bengaluru Page 41

A study on fundamental equity valuation of the stock

Fundamental Ratios of Indian Oil Corporation

2014 2013 2012 2011 2010

Current Ratio 68.02 65.05 61.26 61.97 49.64

Quick Ratio 0.64 0.79 0.74 0.51 0.45

Return on Equity 10.64 8.2 6.83 13.45 20.21

Debt Equity Ratio 1.22 1.28 1.22 0.95 0.88

Dividend Yield Ratio 3.4 2.0 1.6 2.6 4.4

Dividend Payout Ratio 30.09 30.07 30.69 30.97 30.88

Earnings Retention

Ratio 60.66 69.89 89.34 67.78 69.62

P/E Ratio 8.6 16.8 17.6 11.4 6.6

Price to Book Value 271.8 251.75 238.38 227.9 208.21

EPS Ratio 28.91 20.61 16.29 30.67 42.1

4.2: Table Showing Financial Ratios of Indian Oil Corporation

CAGR of DPS = ( DPS of year 2015 ÷ DPS of year 2010) - 1

DPS for year 2015 is Rs.8.7 for a face value of Rs.10. (8.7 X 5 years)

= (8.7 ÷ 13) - 1

= 0.3307 or 33.07

Average Retention Ratio = (60.66+69.89+89.34+67.78+69.62) / 5

= 71.58%

Average Payout Ratio = (1 – Average Retention Ratio)

= 1-0.7146

= 0.2854 OR 28.54%

Average Return on equity = ( 10.64+8.2+6.83+13.45) /5 =

R. V. Institute of Management, Bengaluru Page 42

A study on fundamental equity valuation of the stock

0.0782 OR 7.82%

Expected Growth Rate (g) = Average Retention Ratio X Average Return on Equity.

= 0.7158 X 0.0782

= 0.056 OR 5.6 %

Constant Growth Model:

Using this model Required rate of return is found.

Po = D1 r-g

r = Required rate of the return =? Po=

Present value of the stock

g = the growth rate = 5.6 % or 0.056

D1=The next year dividend = Do(1+g) = 8.5 (1 + 0.056) = 8.97 per share

r = 8.3%

The investors required rate of return would be r =8.3 %

Single Period Valuation Model:

Applying the single period valuation model and finding out share prices for next

year.

Po = D 1 + P 1

1+r 1+r

Where,

Po= Present selling price = Rs. 330 as on Feb-2015 P1=

Selling price at the end of one year period

D1= the dividend received during the one year holding period, D1= Do (1+g)

Do = Current year dividend = 8.5

r = Investor’s Required rate of return = 8.3 or 0.083

D1= Do (1+g) = 8.5 (1 + 0.056) = 8.97 per share

P1 = 348.4 per share

R. V. Institute of Management, Bengaluru Page 43

A study on fundamental equity valuation of the stock

Two Stage Growth Model:

Po = Current selling price = ?

r = Required rate of the return = 0.083 or 8.3%

g1 = Extraordinary growth rate applicable for ‘n’ years = 0.24 or 24% g2 =

Normal growth rate applicable after ‘n’ years = 0.05 or 5%

n = 5 years

By substituting the above stated values the calculated current stock price is: Po

= Rs.610.93 per share

R. V. Institute of Management, Bengaluru Page 44

A study on fundamental equity valuation of the stock

4.3 COMPARISONS ANALYSIS:

The dividends are for the face value of Rs. 10

Particulars RIL IOC

Required Rate of Return ( r) using constant 10.72 8.3

growth model

Do: Current Year Dividend. 9.5 8.5

Expected Growth Rate ( g ) 10.71 5.6

D1: using [ Do (1 + g)] 10.52 8.97

P1: using Single Period Valuation (2013-2014) 942.78 339.60

Actual price of stock Feb-2015 861 331

Share price after 5 years using two stage 864.04 610.93

growth model

4.3: Table showing Comparison of Calculated prices and Actual prices of RIL & IOC

Interpretation based on the Intrinsic Value of the Stock;

If the actual price of the share in the market is more than the intrinsic value

(calculated price using models) of the stock then sell the share.

From the above table it can be seen that the intrinsic value of two companies is

less than the prevailing market price.

All the above stocks are over-valued or say over-priced as there’s a huge

difference between real and actual prices in the market.

Thus it can be interpreted that comparatively Reliance Industries Ltd & Indian Oil

Corporation stocks are better to hold on for some time. The dividend paid by Indian

Oil Corporation is lower than the Reliance Industries Ltd.

The investors can expect a moderate rate of return (8.3%) on stocks of Indian Oil

Corporation, with better growth rate of dividend (5.63%).

R. V. Institute of Management, Bengaluru Page 45

A study on fundamental equity valuation of the stock

An investor with a high risk and high expected earnings can invest into Reliance

Industries Ltd. and one with moderate risk taking ability can take up Indian Oil

Corporation Ltd. stocks.

R. V. Institute of Management, Bengaluru Page 46

A study on fundamental equity valuation of the stock

CHAPTER-5

FINDINGS, SUGGESTIONS AND CONCLUSION

5.1 FINDINGS:

Valuation of the stocks mainly has an impact of the dividend payout on it.

The intrinsic value of the stock at times will be lower than the actual prices of the

share due to the present value factor attached with it.

The intrinsic value of the stock also depends on the dividend declared to

shareholders, if the dividend paid is high then the intrinsic value will be higher,

compared to the one with low dividend.

If the actual prevailing price of the stock is less than that of Intrinsic then, its

suggested that investor can buy the share and can sell it back when prices reach its

true value. Thus the investor is assured to make a better profit out of the

difference.

5.2 SUGGESTIONS:

It is identified that by the analysis for both the company’s, RIL gives the good

return than the IOC.

Investors should be known about company information and financial related

information.

An investor need to go through the news about the company and have to specific

decision maker.

According to analysed stocks price might fail sometimes to meet the expected

return of the company.

Indian oil corporation stock price is expected to increase from 330 to 610.93 after

Five year i.e. near to double of the current price, so it suggest that investor go for

long term to IOC.

5.3 CONCLUSION:

R. V. Institute of Management, Bengaluru Page 47

A study on fundamental equity valuation of the stock

Through the analysis study concludes that the valuation of equity (stock) can be influenced by three factors: Required rate of return, Expected growth rate and the Dividend Payout policy of the company and also risk and return. The valuation of stock has different approaches. Application of all the approaches in practical is difficult and thus their results are different. From this analysis it can be conclude that Indian oil Corporation Ltd is better company to invest for the investors