22

FUNDAMENTALS VALUATION ALOK INDUSTRIES LIMITED 13 th September 2010

FUNDAMENTALS VALUATION

ALOK INDUSTRIES LIMITED

13th

September 2010

ANALYTICAL CONTACT

Ms. Revati Kasture +91-22-6754 3465 [email protected]

BUSINESS DEVELOPMENT CONTACTS

MUMBAI

Mr. P. N. Satheeskumar +91-22-6754 3555 [email protected]

KOLKATA

Mr. Sukanta Nag +91-33- 2283 1800 [email protected]

CHENNAI

Mr. V Pradeep Kumar +91-44-2849 7812 [email protected]

AHMEDABAD

Mr. Mehul Pandya +91-79-40265656 [email protected]

NEW DELHI

Ms. Swati Agrawal +91- 11- 2331 8701 [email protected]

BANGALORE

Mr. G. Sundara Vathanan +91-80-2211 7140 [email protected]

HYDERABAD

Mr. Ashwini Kumar Jani +91-40-40102030 [email protected]

CARE EQUITY RESEARCH OFFERS

Independent Research of equities on fundamentals or valuations or both

IPO Grading

White Label Research

Valuation of companies for Institutional Investors, Asset Managers and Corporates

Sector Write-ups for Offer Documents of securities

ALOK INDUSTRIES LTD.

1 www.careratings.com

EQUIGRADE

EQUI-GRADE – Analytical Power for Investment Decision

ALOK INDUSTRIES LIMITED Integrated Textiles

Good Fundamentals; Moderate Upside Potential CMP : Rs. 20.35 / CIV: Rs. 23.00 1

13 September 2010

CARE Equity Research assigns 3/5 on fundamental grade to Alok

Industries Limited

CARE Equity Research assigns fundamental grade of 3/5 to Alok.

This indicates „Good Fundamentals‟. The grading draws its strength

from Alok‟s large integrated textile manufacturing capacities which

would not only help the company in garnering export market share

but also in becoming preferred sourcing point under the vendor

consolidation scenario by major global retailers. Furthermore,

CARE Equity Research views Alok‟s intentions to exit from its non-

core realty business as positive development that would significantly

reduce its debt from the sales proceeds.

However, CARE Equity Research expects Alok‟s domestic retail

business (H&A) to pick up slowly and thus is not value accretive in

the near term. Though Alok‟s business model is only cash and

carry, intense competition and slim margins would restrict

aggressive scalability. Finally, CARE Equity Research believe that

the concerns over high leverage and frequent equity dilution are of

lesser concern now, as the fund inflows are used in augmenting its

manufacturing capacities with potential to increase company‟s

future revenue and earnings.

Valuation

CARE Equity Research assigns valuation grade of 4/5 to Alok based

on the current Intrinsic Value (CIV) of Rs. 23 as against Current

Market Price (CMP) of 20.35, indicating „Moderate Upside

Potential‟ from CMP.

Financial Information Snapshot

(Rs Crore) FY09 FY10 FY11 P FY12 P

Operating Income 3,518 4,730 6,594 7,887

EBITDA 769 1,165 1,702 2,138

PAT (After minority interest) 74 138 382 667

Fully Diluted EPS* (Rs.) 3.0 2.5 4.8 8.5

Dividend Per Share (Rs.) 0.2 0.2 0.3 0.3

P/E (times) 8.0 4.2 2.4

EV/EBITDA (times) 8.8 6.2 5.1

* Calculated on Current Face Value of Rs. 10/- per share

ALOK INDUSTRIES LTD.

www.careratings.com 2

EQUIGRADE

Global economic recovery to boost export potential

Alok‟s product mix is balanced and the geographical markets are also diverse. Direct exports contributed close to

36% to Alok‟s top-line in FY10. The company‟s domestic market customers include various manufacturer and

traders, who in turn, export Alok‟s products with or without further processing. Therefore, sustainable demand

growth for textiles and made-ups in the international market becomes important for Alok to achieve overall

volume growth. During FY09, the global economy slowdown led to shrinkage in textile trade and closure of several

manufacturing capacities globally. Consecutively, share of Alok‟s exports revenue in its total revenue mix

decreased from 48% in FY08 to 35% in FY09. However, going forward, the global economy is projected to grow at

healthy rates of 4.6% in 2010 and 4.3% in 2011, as per International Monetary Fund (IMF) estimates. The US and

Europe, together contributing close to 60% of Alok‟s total export portfolio, are also expected to grow at about 1.0-

3.5%. It may be noted that this growth rates take into account the recent European debt crisis and tightening of

China‟s credit policy. Asia-Pacific, the second largest export market for Alok after the US, is also likely to report

one of the highest growth rates in the world. This augurs well for Alok, as recovery in the global economy would

inevitably increase demand for textile and made-ups industry.

World GDP Growth Rates (in %) Alok: Geographic Exposure

(as % of Exports-FY09)

Source: CARE Equity Research and International Monetary Fund (IMF)

FUNDAMENTAL GRADE Good Fundamentals 3/5

2008 2009 2010(F) 2011(F)

World 3.0 –0.6 4.6 4.3

US 0.4 –2.4 3.3 2.9

Europe 0.6 –4.1 1.0 1.3

Middle East and North Africa 5.3 2.4 4.5 4.9

Sub-Saharan Africa 5.6 2.2 5.0 5.9

South America 4.2 –1.8 4.8 4.0

Rest-of-North America

Canada 0.5 –2.5 3.6 2.8

Mexico 1.5 –6.5 4.5 4.4

Developing Asia 7.7 6.9 9.2 8.5

China 9.6 9.1 10.5 9.6

India 6.4 5.7 9.4 8.4

US, 43%

Asia

Pacific, 24%

Europe,

18%

South

America, 11%

North

America, 3%

Africa,

1%

ALOK INDUSTRIES LTD.

3 www.careratings.com

EQUIGRADE

Strong business model given Alok‟s presence across the entire textile value chain

Alok is currently one of the largest vertically integrated textile players in India having its presence across the entire

textile value chain. From yarn production, both cotton and synthetic, to garment and home textile production, the

company is providing end-to-end textile solutions. To cover the last mile connectivity, the company also ventured

into retail business through its wholly owned subsidiaries Alok H&A Ltd. in the domestic market and Grabal Alok

(UK) Ltd. in the United Kingdom market.

CARE Equity Research views this business model extremely robust as it gives Alok lot of flexibility in terms of

pricing, quality, adhering to delivery schedules and product selection. Company‟s backward integration to

cotton/synthetic yarn manufacturing enhances input cost efficiencies.

Alok plans to strengthen its presence in synthetic textile as well. The company is increasing the installed capacity

for producing partially oriented yarn (POY) from current 200,000 tonnes per annum to 400,000 tonnes per

annum. The POY is then further texturised and sold in the market. Furthermore, Alok is also building a

production facility for manufacturing various value added products such as Full Drawn Yarn (FDY) and Dyed

Polyester Yarn (DPY) and other products like cationic yarn. The polyester segment is expected to witness healthy

growth on account of polyester yarn being relatively cheaper to cotton yarn and its multiple utility.

Large integrated capacity to benefit Alok in the vendor consolidation scenario by major global retailers

The global retail industry is currently going through the phase of vendor consolidation. Major global retailers are

attempting to reduce the number of vendors in order to reduce their logistics and procurement costs. To illustrate,

JCPenney has reduced its sourcing locations from 50 countries in 2004 to 35 countries in 2006, and aims to

reduce it to about 20 countries in the next few years. By doing so, the company is expecting to reduce cost of its

apparel imports by 10%. China, the main beneficiary of this shift, is now becoming expensive primarily due to

rising yuan and a strong local demand and accordingly India, a cotton-rich country with end-to-end textile solutions

and good designing capabilities, is increasingly becoming preferred sourcing destination.

Under such scenario, Alok is likely to continue to be amongst the preferred vendors of global retail giants due to

its presence across the textile value chain with proven quality standards. The company has also significantly scaled

up its manufacturing capacities making it one of the largest integrated textile players in India. Such coverage

throughout the breadth and width of textile industry would not only help Alok in securing bulk and repeat orders

but also help in achieving economies of scale.

ALOK INDUSTRIES LTD.

www.careratings.com 4

EQUIGRADE

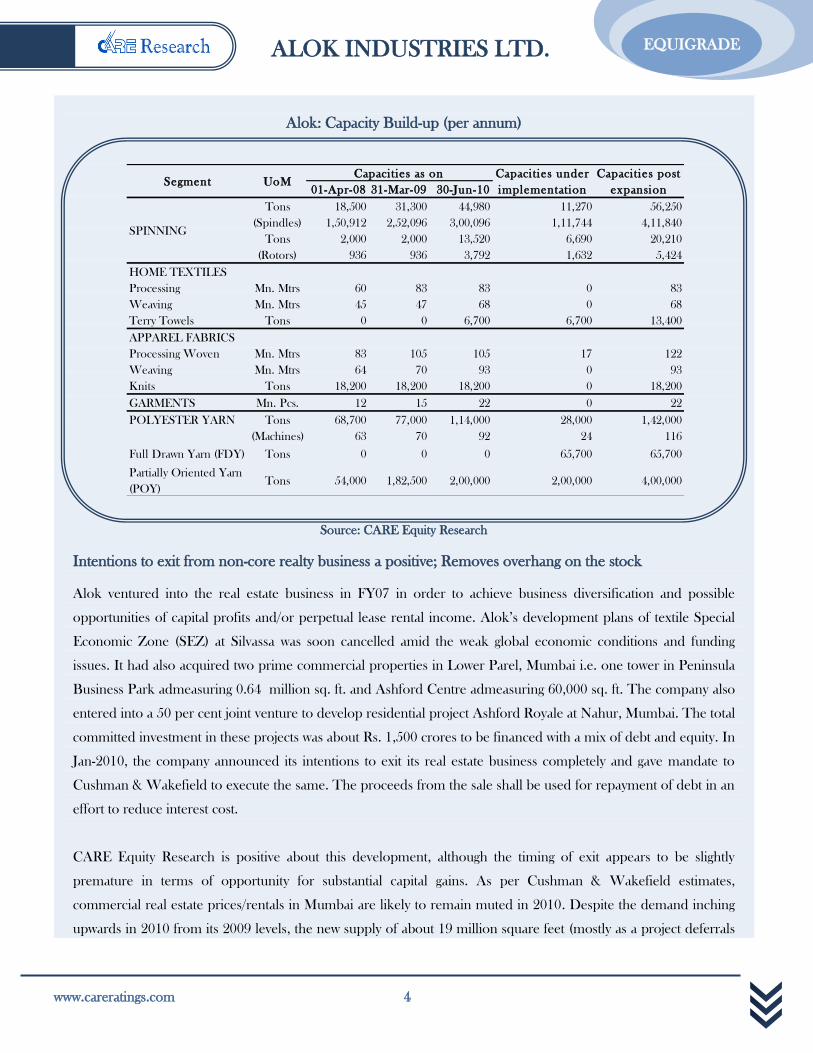

Alok: Capacity Build-up (per annum)

Source: CARE Equity Research

Intentions to exit from non-core realty business a positive; Removes overhang on the stock

Alok ventured into the real estate business in FY07 in order to achieve business diversification and possible

opportunities of capital profits and/or perpetual lease rental income. Alok‟s development plans of textile Special

Economic Zone (SEZ) at Silvassa was soon cancelled amid the weak global economic conditions and funding

issues. It had also acquired two prime commercial properties in Lower Parel, Mumbai i.e. one tower in Peninsula

Business Park admeasuring 0.64 million sq. ft. and Ashford Centre admeasuring 60,000 sq. ft. The company also

entered into a 50 per cent joint venture to develop residential project Ashford Royale at Nahur, Mumbai. The total

committed investment in these projects was about Rs. 1,500 crores to be financed with a mix of debt and equity. In

Jan-2010, the company announced its intentions to exit its real estate business completely and gave mandate to

Cushman & Wakefield to execute the same. The proceeds from the sale shall be used for repayment of debt in an

effort to reduce interest cost.

CARE Equity Research is positive about this development, although the timing of exit appears to be slightly

premature in terms of opportunity for substantial capital gains. As per Cushman & Wakefield estimates,

commercial real estate prices/rentals in Mumbai are likely to remain muted in 2010. Despite the demand inching

upwards in 2010 from its 2009 levels, the new supply of about 19 million square feet (mostly as a project deferrals

01-Apr-08 31-Mar-09 30-Jun-10

Tons 18,500 31,300 44,980 11,270 56,250

(Spindles) 1,50,912 2,52,096 3,00,096 1,11,744 4,11,840

Tons 2,000 2,000 13,520 6,690 20,210

(Rotors) 936 936 3,792 1,632 5,424

HOME TEXTILES

Processing Mn. Mtrs 60 83 83 0 83

Weaving Mn. Mtrs 45 47 68 0 68

Terry Towels Tons 0 0 6,700 6,700 13,400

APPAREL FABRICS

Processing Woven Mn. Mtrs 83 105 105 17 122

Weaving Mn. Mtrs 64 70 93 0 93

Knits Tons 18,200 18,200 18,200 0 18,200

GARMENTS Mn. Pcs. 12 15 22 0 22

POLYESTER YARN Tons 68,700 77,000 1,14,000 28,000 1,42,000

(Machines) 63 70 92 24 116

Full Drawn Yarn (FDY) Tons 0 0 0 65,700 65,700

Partially Oriented Yarn

(POY)Tons 54,000 1,82,500 2,00,000 2,00,000 4,00,000

SPINNING

Capacities as onUoMSegment

Capacities under

implementation

Capacities post

expansion

ALOK INDUSTRIES LTD.

5 www.careratings.com

EQUIGRADE

from 2009) and high vacancy rates of about 14% observed in 2009 will effectively act as a cap on rental

values/selling prices.

Nevertheless, the exit is likely to remove overhang from the stock as the proceeds from the sale would enable

company to allocate resources more efficiently to its core textile business. Our interaction with Alok management

has given us the confidence that Alok management is committed and making significant progress in this direction

given its reasonable price expectations and progress on financial closure of Peninsula Business Park project with

developers. CARE Equity Research has taken a more conservative outlook that Alok would lease-out its two

commercial properties at Lower Parel (Peninsula Corporate Park & Ashford Complex) at average rental values of

about Rs 150-175 per square feet per month till FY14x and would conclude the final sale in FY15 at a rate of

about Rs 26,000 per square feet and about Rs. 6,50,000 per slot of parking space. In light of these assumptions,

the exit from reality business would help Alok in reducing its debt by about Rs 2,000 crore by 2014-15.

De-risking revenue stream across all parameters

Over the years, Alok has diversified its revenue mix across all parameters. It forayed into cotton yarn business and

ramped up its garments business, bringing contribution of its apparel fabric division from 51% in FY05 to 44% in

FY10. The company also substantially increased its export revenue in order to reap the benefit of removal of

textile quota, but maintained its domestic focus with 64% revenue share. Prior to FY06, Alok was over-exposed to

the US market with more than 60% of its export revenue coming from that country. Realizing that any adverse

macroeconomic events, such as slowdown or unfavorable government policy may hit its profitability, Alok started

mitigating this risk by diversifying into other geographies especially in Central Europe, Africa, Asia and South

America. Alok currently supplies to over 70 countries in the world.

Alok: Revenue Diversification

*Export Revenue Break-up Source: CARE Equity Research

Across Segments Across Country Across Geography*

8

5144

22 16

1 3

26 28

0%

20%

40%

60%

80%

100%

FY06 FY10

Polyester

Yarn

Garments

Home

Textiles

Apparel

Fabric

Cotton

Yarn

2836

7264

0%

20%

40%

60%

80%

100%

FY06 FY10

Domestic

Sales

Export

Sales

6043

21

24

718

5 116 3

0%

20%

40%

60%

80%

100%

FY06 FY09

Africa

N. America

S. America

Europe

Asia-Pac

US

ALOK INDUSTRIES LTD.

www.careratings.com 6

EQUIGRADE

Domestic cash and carry expansion not value accretive in near term

Alok entered into domestic retail segment in FY07 through its “Home & Apparels” stores to capture the growing

domestic demand. The company adopted value retailing approach with franchise business model in order to lower

its capital expenditure requirement. Over the years, Alok has massively expanded its retail distribution network

from 14 stores in FY07 to 226 stores as on 30-June-2010, and aims to expand it to 450 operational stores by

March-2011.

Although, CARE Equity Research is positive about the prospects of value retailing in India and acknowledges

Alok‟s competitive advantage over other retailers in the form of a) integrated textile manufacturing capacity b) wide

textile experience and c) lower capex and working capital requirement amid franchise model, the company‟s

growth plans appears to be aggressive in medium term. Competition in domestic retail industry has intensified in

recent years leading to major retail players booking slim margins. For example, PAT margins for typical value

retailers merely ranges between 1.00 to 3.00%. Alok is unlikely to break-in the more profitable lifestyle segments

due to relatively lower brand recognition compared to PRIL, Shopper‟s Stop, Trent and Provogue. Under such

competitive scenario and razor thin margins, CARE Equity Research does not see the domestic retail segment

adding significant revenue or profitability to the company in FY11. Nevertheless, the cash and carry business

contributes less than 1 per cent of the company‟s consolidated top-line and hence no major impact is expected in

the operations of Alok.

Profitability Comparison of Major Retail Players

Notes: [1] Margins as reported for FY10. [2] Retail players in italics are active in life-style

Segment. PRIL is active in both life-style and value retail segment.

Source: CARE Equity Research

PRIL

Shopper's Stop

Trent

Provogue (India) Ltd.

Alok (H&A-

2012E)

5.00

7.00

9.00

11.00

13.00

15.00

2.00 3.00 4.00 5.00 6.00 7.00

PB

ILD

T M

argi

n (

%)

PAT Margin (%)

ALOK INDUSTRIES LTD.

7 www.careratings.com

EQUIGRADE

Reasonable corporate Governance practices

Alok‟s board comprises of 12 directors, of which 7 are independent directors. 5 independent directors are

nominees of various banks and financial institutions. This suggests well diversified composition of board with

adequate separation of ownership and management. Alok is in compliance with the provisions of the Listing

Agreement in respect of corporate governance, especially with respect to broad basing of the Board of Directors

and constituting committees. There are four Board level committees in Alok - (i) Audit Committee, (ii)

Shareholders‟/Investors‟ Grievances Committee; (iii) Remuneration Committee and (iv) Executive Committee.

The audit, the shareholders‟/investors‟ grievances and the remuneration committees are chaired by independent

directors. The board is supported by well experienced senior level managerial personnel.

Frequent equity dilution a sentiment negative but unfounded amid rapid expansion in capacity

In last few years, Alok has rapidly augmented its textile manufacturing capacities and forayed into new business

ventures such as realty. Apart from substantial debt financing under the Technology Upgradation Fund Scheme

(TUFS), the company has also raised equity capital in order to fund its sizeable growth plans.

Alok has significantly diluted its equity capital base from about Rs. 170 crore in FY07 to Rs 788 crore in FY10.

This equity dilution has lead to EPS falling at a faster annual rate of 34.0% compared to net profit declining at a

annual rate of about 6.0 per cent. Nevertheless, CARE Equity Research believes that the risk of frequent equity

dilution is unfounded as Alok has opted to invest the funds in augmenting its textile manufacturing capacities. The

additional production facilities have potential to increase company‟s future revenue and earnings. Furthermore,

accelerated economic recovery may lead to demand rising quickly than supply, and Alok, with already in-place

world-class manufacturing facilities across segments, can scale up its volumes promptly to take advantage of the

strengthening demand.

ALOK INDUSTRIES LTD.

www.careratings.com 8

EQUIGRADE

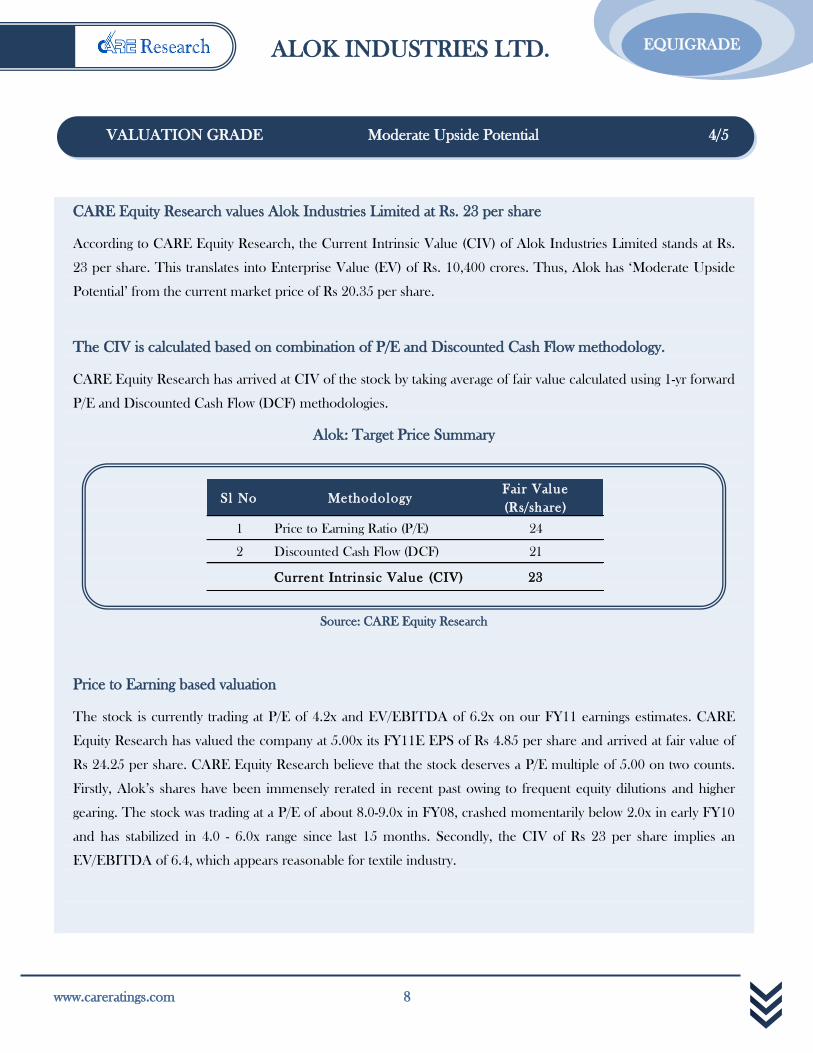

CARE Equity Research values Alok Industries Limited at Rs. 23 per share

According to CARE Equity Research, the Current Intrinsic Value (CIV) of Alok Industries Limited stands at Rs.

23 per share. This translates into Enterprise Value (EV) of Rs. 10,400 crores. Thus, Alok has „Moderate Upside

Potential‟ from the current market price of Rs 20.35 per share.

The CIV is calculated based on combination of P/E and Discounted Cash Flow methodology.

CARE Equity Research has arrived at CIV of the stock by taking average of fair value calculated using 1-yr forward

P/E and Discounted Cash Flow (DCF) methodologies.

Alok: Target Price Summary

Source: CARE Equity Research

Price to Earning based valuation

The stock is currently trading at P/E of 4.2x and EV/EBITDA of 6.2x on our FY11 earnings estimates. CARE

Equity Research has valued the company at 5.00x its FY11E EPS of Rs 4.85 per share and arrived at fair value of

Rs 24.25 per share. CARE Equity Research believe that the stock deserves a P/E multiple of 5.00 on two counts.

Firstly, Alok‟s shares have been immensely rerated in recent past owing to frequent equity dilutions and higher

gearing. The stock was trading at a P/E of about 8.0-9.0x in FY08, crashed momentarily below 2.0x in early FY10

and has stabilized in 4.0 - 6.0x range since last 15 months. Secondly, the CIV of Rs 23 per share implies an

EV/EBITDA of 6.4, which appears reasonable for textile industry.

VALUATION GRADE Moderate Upside Potential 4/5

Sl No MethodologyFair Value

(Rs/share)

1 Price to Earning Ratio (P/E) 24

2 Discounted Cash Flow (DCF) 21

Current Intrinsic Value (CIV) 23

ALOK INDUSTRIES LTD.

9 www.careratings.com

EQUIGRADE

Alok: 1-yr forward P/E contour Alok: Historic 1-yr forward EV/EBITDA

Source for all above graphs and tables: CARE Equity Research and Prowess

Discounted Cash Flow

The overall firm Weighted Average Cost of Capital (WACC) is calculated based on our long term

assumptions of cost of financing summarized in below table.

CARE Equity Research has used Free Cash Flow (FCF) methodology to arrive at the firm value as Alok

has shown considerable volatility in its gearing ratio in last few years. The forecasted FCF is as per CARE

Equity Research estimates.

Alok: Fair Value Estimation using

P/E Multiple Method

Alok: Implied EV/EBITDA Calculation

based on Fair Value

PAT (2011) 382

No. of Shares (crore) 79

EPS(2011) 4.85

CMP 19.20

P/E (1 yr fwd P/E) 3.96

Justified P/E 5.00

Fair Value 24.25

P/E

EBITDA (2011) 1,702

Fair Value 23.17

No. of Shares (crore) 79

Market Cap (Rs crore) 1,825

Net Debt (2010) 9,050

EV 10,875

Implied EV/EBITDA 6.39

Implied EV/EBITDA

0

20

40

60

80

100

120

Oct

-05

Ap

r-06

Oct

-06

Ap

r-07

Oct

-07

Ap

r-08

Oct

-08

Ap

r-09

Oct

-09

Ap

r-10

Sh

are

Pri

ce (R

s.)

Share Price 2x 4x 6x 8x

4.00

6.00

8.00

10.00

12.00

14.00

Oct-05 Oct-06 Oct-07 Oct-08 Oct-09

EV

/EB

ITD

A (

1-y

r fo

rward

)

ALOK INDUSTRIES LTD.

www.careratings.com 10

EQUIGRADE

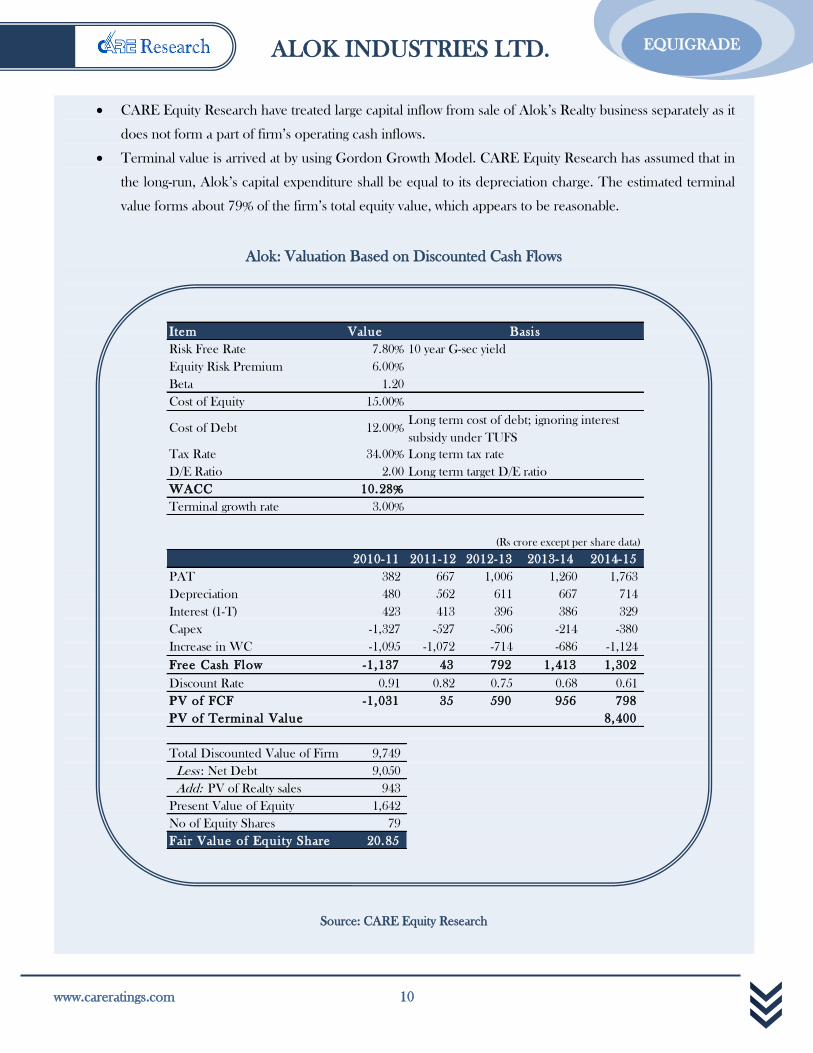

CARE Equity Research have treated large capital inflow from sale of Alok‟s Realty business separately as it

does not form a part of firm‟s operating cash inflows.

Terminal value is arrived at by using Gordon Growth Model. CARE Equity Research has assumed that in

the long-run, Alok‟s capital expenditure shall be equal to its depreciation charge. The estimated terminal

value forms about 79% of the firm‟s total equity value, which appears to be reasonable.

Alok: Valuation Based on Discounted Cash Flows

Source: CARE Equity Research

Item Value

Risk Free Rate 7.80% 10 year G-sec yield

Equity Risk Premium 6.00%

Beta 1.20

Cost of Equity 15.00%

Cost of Debt 12.00%

Tax Rate 34.00% Long term tax rate

D/E Ratio 2.00 Long term target D/E ratio

WACC 10.28%

Terminal growth rate 3.00%

(Rs crore except per share data)

2010-11 2011-12 2012-13 2013-14 2014-15

PAT 382 667 1,006 1,260 1,763

Depreciation 480 562 611 667 714

Interest (1-T) 423 413 396 386 329

Capex -1,327 -527 -506 -214 -380

Increase in WC -1,095 -1,072 -714 -686 -1,124

Free Cash Flow -1,137 43 792 1,413 1,302

Discount Rate 0.91 0.82 0.75 0.68 0.61

PV of FCF -1,031 35 590 956 798

PV of Terminal Value 8,400

Total Discounted Value of Firm 9,749

Less : Net Debt 9,050

Add: PV of Realty sales 943

Present Value of Equity 1,642

No of Equity Shares 79

Fair Value of Equity Share 20.85

Long term cost of debt; ignoring interest

subsidy under TUFS

Basis

ALOK INDUSTRIES LTD.

11 www.careratings.com

EQUIGRADE

Alok: Sensitivity Analysis – Share price

Source: CARE Equity Research

9.5% 10.0% 10.6% 11.0% 11.5%

2.0% 11.6 8.7 7.1 3.0 0.3

2.5% 18.3 15.2 13.5 9.2 6.4

3.0% 25.9 22.6 20.8 16.3 13.3

3.5% 34.6 31.2 29.3 24.5 21.3

4.0% 44.8 41.1 39.0 33.9 30.5

Te

rmin

al

Ye

ar

Gro

wth

Rate

(%

)

Weighted Average Cost of Capital (%)

ALOK INDUSTRIES LTD.

www.careratings.com 12

EQUIGRADE

Company Background

Alok Industries Ltd (Alok) was established in 1986 as private limited company and subsequently became a public

limited company in 1993. Alok is currently one of the largest vertically integrated textile players in India having its

presence across the textile value chain. The company is headquartered in Mumbai with its manufacturing units at

Silvassa, Vapi, Navi Mumbai and Bhiwandi. Alok has ventured into retail segment through its fully owned

subsidiary Alok H&A Ltd, which currently executes Alok‟s cash & carry operations through 248 stores across India.

The company intends to exit from its non-core real estate business in which it forayed in FY07.

Organization Chart

Source: CARE Equity Research

Business Mix

Alok has diversified revenue stream through five divisions namely, Cotton Yarn, Apparel Fabric, Home Textiles,

Garments and Polyester Yarn. The Apparel Fabric division is largest in terms of its contribution to the company‟s

overall revenue stream followed by Polyester Yarn division. Alok backward-integrated into the Cotton Yarn

COMPANY BACKGROUND

Alok Industries Ltd.

(textile manufacturing)

Alok Industries

International (BVI)100% subsidiary

(international business)

Alok H&A Ltd.

100% subsidiary

(domestic cash & carry)

Alok Infrastructure Ltd

100% subsidiary

(infrastructure & realty)

Alok Apparels Pvt Ltd

100% subsidiary(domestic garment

manufacturing)

Mileta International

93.2% holding Czech Republic

(textile man.)

Grabal Alok (UK) Ltd

42% holding (Store “Twenty one”

& qs)

Alok Realtors Pvt Ltd.

100% Subsidiary(Peninsula Project)

Ashford Infotech Pvt Ltd

50% holding

(Nahur Project)

ALOK INDUSTRIES LTD.

13 www.careratings.com

EQUIGRADE

business in FY07 in order to de-risk the overall business and enhance input cost efficiencies. Contribution of the

Cotton Yarn business to the company‟s overall sales dropped sharply in FY09 primarily due to the lack of profitable

trading opportunities and sluggish export markets, but rebounded in FY10. The Garment division was benefited the

most by removal of the textiles and clothing quotas in 2005. Subsequently, Alok increased its garment

manufacturing capacity from 1.0 million pieces in FY05 to 22.0 million pieces in FY09. As a result, share of the

Garments division in the company‟s revenue mix increased from about 1.0% in FY05 to 3.1% in FY10.

Nevertheless, Alok is currently not envisaging any further capacity addition in this segment.

Division-wise Revenue Break-up (in %)

Source: CARE Equity Research

Export Business

Removal of the textiles and clothing quotas in Jan-2005 changed the trade pattern of global textile industry

substantially. Low cost textile producers such as India and China benefited immensely as big importers like Wal-

Mart, GAP, Marks & Spencer, JC Penney, Macy's, Target, Liz Claiborne and IKEA set substantially higher long-

term sourcing targets. Consecutively, Alok‟s export sales surged by about 175% on y-o-y basis, as against India‟s

overall textile export growth rate of 25% in FY05. Since then, Alok has exhibited impressive growth on its export

sales, increasing at a CAGR of about 38% in last five year ending March-2010. Export sales stagnated during FY09

primarily due to the global economic conditions when global textile trade shrunk and several manufacturing

capacities were shut-down.

4.61 13.55 3.73 8.22

51.2 49.141.2 54.1 44.5

21.8 18.3 17.9 16.716.2

1.0 1.6 4.6 4.73.1

25.9 26.3 22.7 20.8 28.1

0%

20%

40%

60%

80%

100%

FY06

(1,421 Cr)

FY07

(1,825 Cr)

FY08

(2,170 Cr)

FY09

(2,977 Cr)

FY10

(4,311 Cr)

Cotton Yarn Apparel Fabric Home Textiles

Garments Polyester Yarn

ALOK INDUSTRIES LTD.

www.careratings.com 14

EQUIGRADE

Alok: Export Sales & Export as % of Total Sales

Source: CARE Equity Research

Geographic Exposure

Alok exports to over seventy countries across the US, Asia Pacific, Europe, South America, North America and

Africa. Although the US has remained as one of the biggest markets for Alok, the company has diversified its

export market to other regions such as Asia-Pacific and Europe. On the divisional side, the Home Textiles and

Garments businesses are primarily focused on export markets exporting almost 100% of their output.

Alok: Geographic Exposure as % of Exports

2004-05 2008-09

Source: CARE Equity Research

0

10

20

30

40

50

60

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY04 FY05 FY06 FY07 FY08 FY09 FY10

Ex

po

rt (

% o

f T

ota

l S

ales)

Ex

po

rt S

ales

(Rs

Cro

re)

Export Sales Export (% of total sales-RHS)

US, 57%

Asia

Pacific, 9%

Europe,

16%

South

America, 10%

North

America, 7%

Africa,

1%

US, 43%

Asia

Pacific, 24%

Europe,

18%

South

America, 11%

North

America, 3%

Africa,

1%

ALOK INDUSTRIES LTD.

15 www.careratings.com

EQUIGRADE

Division-wise Export/Domestic Revenue Break-up (in %)

Source: CARE Equity Research

Promoters

Mr. Ashok Jiwrajka: (Executive Chairman) is a commerce graduate and one of the founding members of Alok. He

has over three decades of experience in textile industry and currently overseeing Alok‟s marketing and export

activities.

Mr. Dilip B. Jiwrajka (Managing Director) is one of the founding members of Alok. He has done his post-

graduation in Business Entrepreneurship and Management and is associated with the textile industry for more than

25 years. His responsibilities at Alok include forming the Company's growth strategy, responsibility for the Apparel

Fabric and Garment divisions and overseeing the overall working of Alok and other group companies.

Mr. Surendra B. Jiwrajka (Jt. Managing Director) is one of the founding members of Alok. He is a commerce

graduate with over two decades of experience in textile industry. His functions at Alok include forming the

Company's growth strategy, overseeing the manufacturing, marketing functions of the polyester and spinning

businesses and project implementation.

96

45

66

19 16 14

100 99 9890 91 93

21 20 21

34

81 84 86

10 9 7

79 80 79

0%

20%

40%

60%

80%

100%

FY

08

FY

09

FY

10

FY

08

FY

09

FY

10

FY

08

FY

09

FY

10

FY

08

FY

09

FY

10

FY

08

FY

09

FY

10

Cotton

Yarn

Apparel

Fabric

Home

Textiles

Garments Polyester

Yarn

Export Sales Domestic Sales

ALOK INDUSTRIES LTD.

www.careratings.com 16

EQUIGRADE

Abolition of quotas has opened up sea of opportunities for low cost producers like India

Abolition of quota regime from 1st January, 2005 has drastically changed the paradigm of the global textiles and

apparel trade. The T&A trade increased manifold between the nations with the manufacturing base being shifted to

relatively low cost Asian countries like India, China, Bangladesh, Indonesia and Malaysia. Asian countries became

the key exporters and the high cost centers as well as key consumers like US and EU became the key importers.

Asian countries account for approximately 71 per cent of the total apparel production, while US and EU contribute

11 per cent and 14 per cent respectively. However, US and EU account for more than 65 per cent of apparel

consumption.

Indian textile industry is fragmented in nature

India‟s textile industry primarily comprises of small-scale, non-integrated spinning, weaving, processing and made-

ups making units. There are only a few integrated units; fully integrated units like Alok are unique in this industry.

Close to 90 per cent of the spinning production is accounted for by more than 2,500 stand-alone units, with

integrated units accounting for merely 10 per cent of spun yarn production. Similarly, weaving and knitting sector is

too is highly fragmented, with unorganised sector accounting for close to 95 per cent of the total cloth production.

The processing industry is also largely decentralized, marked largely by hand processing units and independent

processing units. Composite mill sectors are very few falling into the organized category. Overall, there are about

2,300 – 2,500 processors operating in India, but only about 200 units are integrated with spinning, weaving or

knitting units. Small-scale fabricators dominate garment and home textile manufacturing. The bulk of apparel is

produced by more than 1,00,000 sub-contractors.

Indian textile industry projected to be on high growth trajectory

CARE Research estimates India‟s textile industry to be worth Rs. 2,700 billion in FY10, of which Rs. 950 billion

worth textile products are exported. The domestic market is estimated by CARE Research to grow at CAGR of 11

– 12 per cent in the next five years from Rs. 1,750 billion to Rs. 2,600 billion in FY15. Textile exports are expected

by CARE Research to grow at a faster CAGR of 17 – 18 per cent to Rs. 2,100 billion by FY15. Buoyant economy

will drive domestic sales, while increase in sourcing from low cost centers like India would drive textile exports.

SNAPSHOT OF THE INDIAN TEXTILE INDUSTRY

ALOK INDUSTRIES LTD.

17 www.careratings.com

EQUIGRADE

FINANCIAL STATISTICS

ALOK INDUSTRIES LTD.

www.careratings.com 18

EQUIGRADE

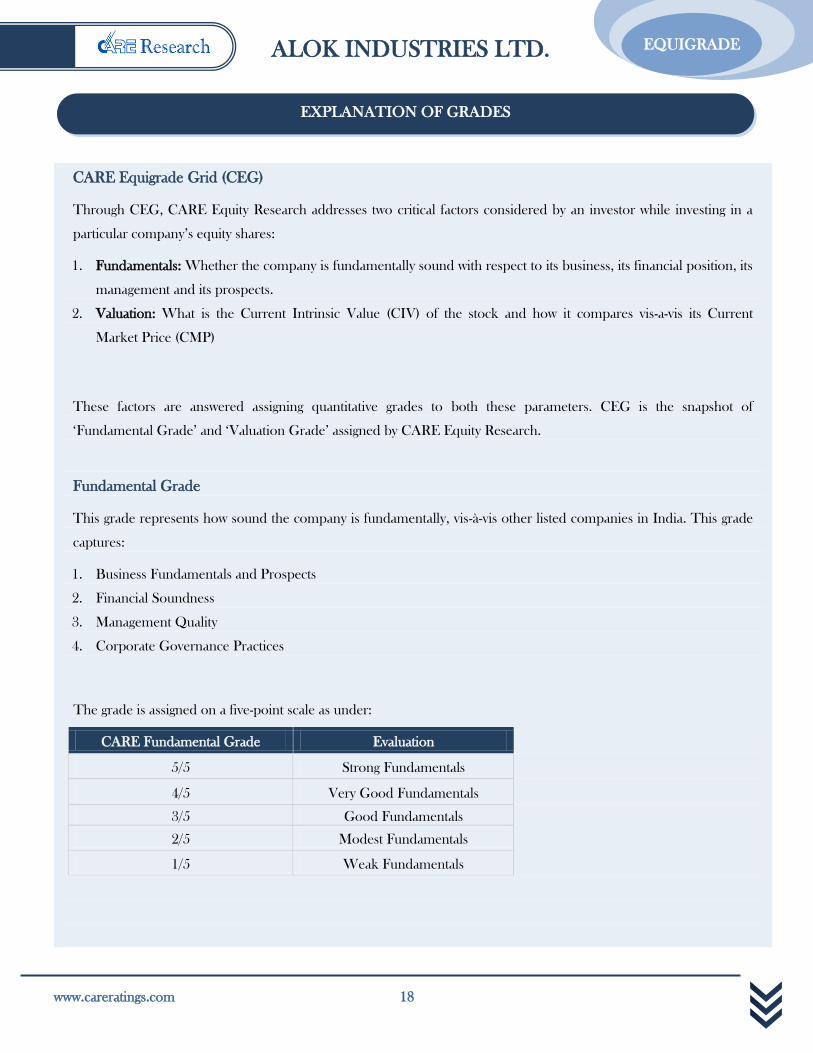

CARE Equigrade Grid (CEG)

Through CEG, CARE Equity Research addresses two critical factors considered by an investor while investing in a

particular company‟s equity shares:

1. Fundamentals: Whether the company is fundamentally sound with respect to its business, its financial position, its

management and its prospects.

2. Valuation: What is the Current Intrinsic Value (CIV) of the stock and how it compares vis-a-vis its Current

Market Price (CMP)

These factors are answered assigning quantitative grades to both these parameters. CEG is the snapshot of

„Fundamental Grade‟ and „Valuation Grade‟ assigned by CARE Equity Research.

Fundamental Grade

This grade represents how sound the company is fundamentally, vis-à-vis other listed companies in India. This grade

captures:

1. Business Fundamentals and Prospects

2. Financial Soundness

3. Management Quality

4. Corporate Governance Practices

The grade is assigned on a five-point scale as under:

CARE Fundamental Grade Evaluation

5/5 Strong Fundamentals

4/5 Very Good Fundamentals

3/5 Good Fundamentals

2/5 Modest Fundamentals

1/5 Weak Fundamentals

EXPLANATION OF GRADES

ALOK INDUSTRIES LTD.

19 www.careratings.com

EQUIGRADE

Valuation Grade

This grade represents the potential value in the company‟s equity share for the investor over a 1 year period. The

Current Intrinsic Value (CIV) or the price arrived by CARE Equity Research on fundamental basis is compared with

the current market price (CMP) of the stock and the grade is assigned based on the gap between CIV and CMP of the

stock.

The grade is assigned on a five-point scale as under:

CARE Valuation Grade Evaluation

5/5 Considerable Upside Potential

(>25% from CMP)

4/5 Moderate Upside Potential

(10-25% from CMP)

3/5 Fairly Priced

(+/- 10% from CMP)

2/5 Moderate Downside Potential

(Negative 10-25 from CMP)

1/5 Considerable Downside Potential

(<25% from CMP)

Grading determination is a matter of experienced and holistic judgment, based on relevant quantitative and qualitative factors of

the company in relation to other listed companies.

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there exists no conflict of interest that can bias

the grading recommendation of the company.

This report has been sponsored by the company.

DISLCLAIMER

This report is prepared by CARE Research, a division of Credit Analysis & REsearch Limited [CARE]. CARE Research has taken utmost care to

ensure accuracy and objectivity while developing this report based on information available in public domain or from sources considered reliable.

However, neither the accuracy nor completeness of information contained in this report is guaranteed. CARE Research operates independently of

ratings division and this report does not contain any confidential information obtained by ratings division, which they may have obtained in the

regular course of operations. Opinions expressed herein are our current opinions as on the date of this report. Nothing in this report can be

construed as either investment or any other advice or any solicitation, whatsoever. The subscriber / user assumes the entire risk of any use made of

this report or data herein. CARE specifically states that it or any of its divisions or employees have any financial liabilities whatsoever to the

subscribers / users of this report. This report is for personal information only of the authorised recipient in India only. This report or part of it

should not be reproduced or redistributed or communicated directly or indirectly in any form to any other person, especially outside India or

published or copied for any purpose.

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express Highway, Somaiya Hospital Road, Sion

East, Mumbai – 400 022.

CARE Research is not responsible for any errors or omissions in analysis/inferences/views or for results obtained from the use of information

contained in this report and especially states that CARE (including all divisions) has no financial liability whatsoever to the user of this product. This

report is for the information of the intended recipients only and no part of this report may be published or reproduced in any form or manner

without prior written permission of CARE Research.

ALOK INDUSTRIES LTD.

www.careratings.com 20

EQUIGRADE

+

Credit Analysis & REsearch Ltd. (CARE) is a full service rating company that offers a wide range of rating and grading services

across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in line with the best international

practices.

CARE Research

CARE Research is an independent research division of CARE Ratings, a full service rating company. CARE Research is

involved in preparing detailed industry research reports with 5 year demand and 2 year profitability outlook on the industry

besides providing comprehensive trend analysis and the current state of the industry. CARE Research also offers research that

is customised to client requirements. CARE Research currently offers reports on more than 21 industries that include Cement,

Steel, Aluminium, Construction, Shipping, Ship-building, Commercial Vehicles, Two-Wheelers, Tyres, Auto Components,

Pipes, Natural Gas, Retail, Sugar, etc. CARE Research now offers independent research of equities through its product

„EQUIGRADE‟.

CREDIT ANALYSIS & RESEARCH LTD

HEAD OFFICE |Mr. P. N. Satheeskumar | Cell: +91-9820416004 | Tel: +91-22-6754 3555 | E-mail:

4th Floor, Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai - 400 022 |

Tel: +91-022- 6754 3456 | E-mail: [email protected] | Fax: +91-022- 6754 3457

KOLKATA | Mr. Sukanta Nag | Cell: +91-98311 70075 | Tel: +91-33- 2283 1800/ 1803, 2280 8472 |

E- mail: [email protected] | 3rd Flr., Prasad Chambers (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata -700 071

CHENNAI | Mr. V Pradeep Kumar | Cell: +91 9840754521 | Tel: +91-44-2849 7812/2849 0811 | Fax: +91-44-2849 0876 |

Email: [email protected] | Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769, Anna Salai, Chennai - 600 002

AHMEDABAD | Mr. Mehul Pandya | Cell: +91-98242 56265 | Tel: +91-79-40265656 | Fax: +91-79-40265657 |

E-mail:[email protected] | 32, Titanium, Prahaladnagar Corporate Road, Satellite, Ahmedabad - 380 015.

NEW DELHI | Ms. Swati Agrawal | Cell: +91-98117 45677 | Tel: +91- 11- 2331 8701/ 2371 6199 |

E-mail: [email protected] | 710 Surya Kiran,19 K.G. Road, New Delhi - 110 001.

BANGALORE | Mr. G. Sundara Vathanan | Cell: +91 98860 24430 | Tel:+91-80-2211 7140 |

E-mail: [email protected] | Unit No. 8, I floor, Commander's Place, No. 6, Raja Ram Mohan Roy Road,

(Opp. P F Office), Richmond Circle, Bangalore - 560 025.

HYDERABAD | Mr. Ashwini Kumar Jani | Cell: +91-91766 47599 | Tel: +91-40-40102030 |

E-mail: [email protected] | 401, Ashoka Scintilla | 3-6-520, Himayat Nagar | Hyderabad - 500 029

ABOUT US