23

FUNDAMENTALS VALUATION ELECON ENGINEERING COMPANY LIMITED 11 th May 2011

FUNDAMENTALS VALUATION

ELECON ENGINEERING

COMPANY LIMITED

11th

May 2011

ANALYTICAL CONTACT

Ms. Revati Kasture +91-22-6754 3465 [email protected]

BUSINESS DEVELOPMENT CONTACTS

MUMBAI

Mr. P. N. Satheeskumar +91-22-6754 3555 [email protected]

KOLKATA

Mr. Sukanta Nag +91-33- 2283 1800 [email protected]

CHENNAI

Mr. V Pradeep Kumar +91-44-2849 7812 [email protected]

AHMEDABAD

Mr. Mehul Pandya +91-79-40265656 [email protected]

NEW DELHI

Ms. Swati Agrawal +91- 11- 2331 8701 [email protected]

BANGALORE

Mr. G. Sundara Vathanan +91-80-2211 7140 [email protected]

HYDERABAD

Mr. Ashwini Kumar Jani +91-40-40102030 [email protected]

CARE EQUITY RESEARCH OFFERS

Independent Research of equities on fundamentals or valuations or both

IPO Grading

White Label Research

Valuation of companies for Institutional Investors, Asset Managers and Corporates

Sector Write-ups for Offer Documents of securities

ELECON ENGINEERING CO. LTD.

1 www.careratings.com

EQUIGRADE

EQUIGRADE – Analytical Power for Investment Decisions

ELECON ENGINEERING COMPANY LIMITED

Engineering – Industrial Machinery

Very Good Fundamentals; Considerable Upside Potential CMP : Rs. 68.35 / CIV : Rs. 98 1

Sensex 18,512.7

CARE Equity Research assigns 4/5 on fundamental grade to EECL

CARE Equity Research assigns fundamental grade of 4/5 to EECL. This

indicates ‘Very Good Fundamentals’. EECL, with close to six decades of

experience, is amongst the few large Indian companies in material handling

equipment (MHE) industry and market leader in domestic industrial gear

industry. Both these segments cater to the core sectors of the economy. This

places EECL in a sweet spot, as outlook for the growth in core sector remains

buoyant on the back of rising GDP, increased industrial output and

Government’s focus on development of infrastructure. EECL has revenue

visibility of around 2 years in case of MHE business and around 3 quarters in

gear business with buoyant order-book pipe-line. EECL’s business,

particularly MHE, is working capital intensive on account of large execution

period and significant portion of billed amount is held back as retention

money by the client. Timely execution of projects of the clients is imperative,

as it has fall-back impact on EECL by the way of delay/cancellation of orders

or in accepting delivery, thereby elongating the operating cycle, putting

pressure on profitability. Being part of the Elecon group that largely focuses

on engineering sector adds to the operational strength of EECL in terms of

sourcing some of the inputs like castings from the group company(ies) and

outsourcing some portion of job-work to the group company(ies). Acquisition

of Benzlers-Radicon group for £ 18.4 million (Rs. 130 – 135 crore) opens up

opportunity for EECL in the American and European countries.

Valuation

CARE Equity Research assigns valuation grade of 5/5 to EECL based on the

Current Intrinsic Value (CIV) of Rs. 98 per share as against Current Market

Price (CMP) of Rs. 68.35 per share. This indicates ‘Considerable Upside

Potential’. The CIV is arrived on the basis of DCF methodology.

Financial Information Snapshot

(Rs. Crore) FY09 FY10 FY11 P FY12 P FY13 P

Operating Income 965 1,071 1,274 1,648 1,895

EBITDA 159 174 203 252 299

PAT (After minority interest) 57 66 89 107 132

Fully Diluted EPS* (Rs.) 6.2 7.1 9.6 11.5 14.2

Dividend Per Share (Rs.) 1.5 1.5 1.5 2.0 2.5

P/E (times)

9.6 7.2 5.9 4.8

EV/EBITDA (times) 7.5 6.4 5.2 4.3

* Calculated on Current Face Value of Rs. 2/- per share

11th

May 2011

ELECON ENGINEERING CO. LTD.

www.careratings.com 2

EQUIGRADE

Buoyant long term outlook for the core sector places EECL in a sweet spot

Government’s focus on infrastructure development and the buoyancy in the economic activities translate into

healthy growth of the core sectors like steel, cement, power, mining, ports, etc. Similarly, rising level of

consumption expenditure of the Indian households translates into the growth of consumer industries that

percolates down to drive the growth of the core sector. In the economy like India, with increasing per capita

income, favourable demographic profile, relatively low penetration of various consumer goods and relatively

under-developed infrastructure than the developed nations, the scope for the growth of core sector remains huge.

According to CARE Research, the core sector is expected to witness healthy growth of 9 - 10 per cent growth in

the next 8 – 10 years.

Buoyancy in the core sector places the players like EECL in a sweet spot by bringing opportunities for them in

terms of healthy order-book pipeline. Both the business segments of EECL – material handling equipments

(MHE) and industrial gears – cater to the core sector and thereby are expected to derive significant opportunities

from its growth.

EECL amongst the few large companies in MHE business

EECL is amongst the few large companies in Indian MHE industry, catering to almost all the industries in the core

sector like steel, fertilizer, cement, power, coal, lignite and iron ore mines, ports, etc. The company has close to six

decades of experience in this business and has a composite range of MHE and products to offer. EECL’s MHE

manufacturing facilities house state of the art technology with computerized Numerical Control (CNC) machines

that can achieve precision and minimise material wastage. Besides the strong in-house designing capabilities, the

company also has technical collaborations with various international companies. The prototype designs are

sourced from the technical collaborators and subsequently, the designs are customized in-house.

Technical Collaborations in MHE segment

Source: Company

Name of the company Technology

Huron Manufacturing Corp, USA Continuous surface miner

Koch GmbH, Germany Ship loader with slewing boom

CKIT Conveyors Engineers, South Africa Pipe Conveyor, Long Distance Through Conveyor,

High Speed Conveyors and Curve Conveyors.

FUNDAMENTAL GRADE Very Good Fundamentals 4/5

ELECON ENGINEERING CO. LTD.

3 www.careratings.com

EQUIGRADE

MHE segment has witnessed average annual growth of 9 per cent in its revenue and 10.5 per cent in segmental

EBIT. The EBIT margin has remained more or less stable, averaging around 12.5 per cent in the last few years.

EECL: Segmental revenue and EBIT for MHE segment

Source: Company

Healthy order-book in MHE segment

As on 31st December 2010, the company had orders worth Rs. 1,285 crore to be executed in the MHE segment,

which is close to 2 times the estimated revenue of the said segment in FY11. This provides revenue visibility for

the company for the next 7 – 8 quarters. Around 44 per cent of the order back-log in MHE segment relates to

power sector, while 30 per cent relates to steel sector. The company received new orders worth Rs. 797 crore in

the MHE segment during April – December 2010 period (9M FY11).

EECL’s Order back-log: MHE segment [Rs. 1,285 crore]

Source: Company

The dependence on power sector is relatively higher in the MHE segment. At the end of FY10, power sector

contributed to around 54 per cent of the orders for MHE. During 9M FY11 as well, of the total order booking of

Rs. 797 crore in the MHE segment, power sector contributed Rs. 525 crore or 66 per cent to the same.

448 471

588655

475

55 63 72 83 62

12.3%13.3%

12.2% 12.7% 13.0%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

0

200

400

600

800

1,000

FY07 FY08 FY09 FY10 9M FY11

EB

IT M

argin

Reve

nu

e / E

BIT

(R

s. c

rore

)

Revenue EBIT EBIT Margin

Power

44%

Steel

30%

Cement

10%

Port

7%

Mining

4%Others

5%

ELECON ENGINEERING CO. LTD.

www.careratings.com 4

EQUIGRADE

CARE Equity Research does not see the high dependence on power sector as a risk for the company, as India has

been facing deficit scenario and there are plans to add humungous capacities in the sector going forward. Rather,

the power sector offers opportunity for the company. The total energy deficit and peak deficit stood at

approximately 10.1 per cent and 12.7 per cent respectively in FY10. In the scenario of GDP growing at 8 per cent,

which according to CARE Equity Research seems realistic, the energy demand is likely to increase at compounded

annual growth rate (CAGR) of more than 6 per cent from around 110 Giga Watts (GW) in FY11E to 160 GW in

FY17. Accordingly, from the current capacity of around 162 GW, the power generation capacities need to grow to

around 230 GW by FY17 and 310 GW by FY22 assuming plant load factor at current level of 77.5 per cent.

EECL occupies leadership position in domestic industrial gear industry as well

EECL is the market leader in domestic industrial gears industry, with around 25 per cent market share. EECL was

the first company in India to introduce modular design concept, case hardened and ground gear technology. The

company has wide range of products to offer, both standardized as well as customized, to various industries

including MHE, marine, power, steel, cement, sugar, sponge iron, plastic and rubber, lift gears, chemical and

fertilizer, mining, wind mill, etc. EECL has expertise in providing customised gear boxes for steel mills, high speed

turbines, sugar mills, marine vessels, coast guard ships, plastic extrusions, antenna drives and for satellites in the

Indian Space Programme. EECL has technical collaboration with Haisung Industrial System for lift gear boxes

and Renk AG for technology to design and manufacture vertical roller mill gear boxes.

The gear segment has witnessed average annual growth of around 12.5 per cent in its revenue and 5 per cent in

segmental EBIT. The EBIT margin has witnessed falling trend on account of increasing depreciation costs on the

back of capital expenditure incurred by the company in this segment.

EECL: Segmental revenue and EBIT for Industrial Gear Segment

Source: Company

311389 394 426

368

64 79 73 69 59

20.7% 20.4%18.4%

16.1% 15.9%

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

24.0%

0

200

400

600

800

1,000

FY07 FY08 FY09 FY10 9M FY11

Revenue EBIT EBIT Margin

ELECON ENGINEERING CO. LTD.

5 www.careratings.com

EQUIGRADE

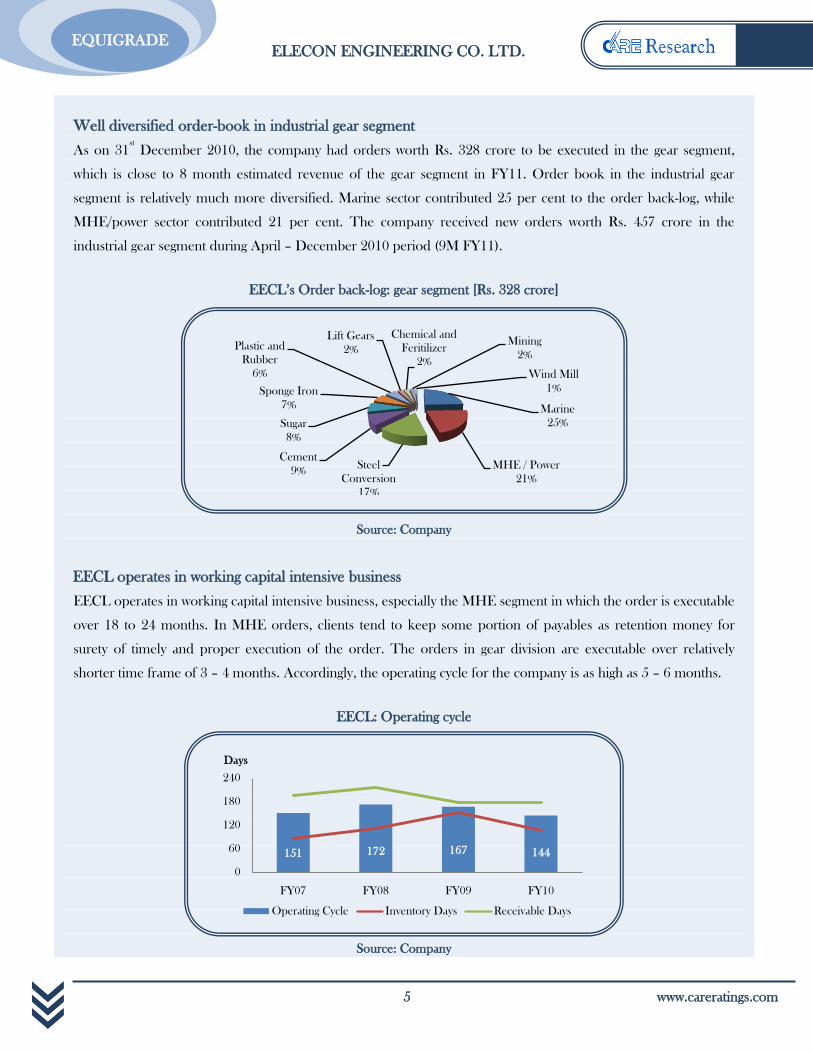

Well diversified order-book in industrial gear segment

As on 31st December 2010, the company had orders worth Rs. 328 crore to be executed in the gear segment,

which is close to 8 month estimated revenue of the gear segment in FY11. Order book in the industrial gear

segment is relatively much more diversified. Marine sector contributed 25 per cent to the order back-log, while

MHE/power sector contributed 21 per cent. The company received new orders worth Rs. 457 crore in the

industrial gear segment during April – December 2010 period (9M FY11).

EECL’s Order back-log: gear segment [Rs. 328 crore]

Source: Company

EECL operates in working capital intensive business

EECL operates in working capital intensive business, especially the MHE segment in which the order is executable

over 18 to 24 months. In MHE orders, clients tend to keep some portion of payables as retention money for

surety of timely and proper execution of the order. The orders in gear division are executable over relatively

shorter time frame of 3 – 4 months. Accordingly, the operating cycle for the company is as high as 5 – 6 months.

EECL: Operating cycle

Source: Company

151 172 167 144

0

60

120

180

240

FY07 FY08 FY09 FY10

Days

Operating Cycle Inventory Days Receivable Days

Marine

25%

MHE / Power

21%

Steel

Conversion

17%

Cement

9%

Sugar

8%

Sponge Iron

7%

Plastic and

Rubber

6%

Lift Gears

2%

Chemical and

Feritilizer

2%

Mining

2%

Wind Mill

1%

ELECON ENGINEERING CO. LTD.

www.careratings.com 6

EQUIGRADE

Timely execution of client’s projects is crucial for EECL

The execution of orders by EECL and its working capital cycle depends on the timely execution of respective

clients’ projects. If the client’s project gets delayed or cancelled, it has fall back impact on EECL. The project

delay at client’s end leads to either hold-back of the order or delay in execution / cancellation of order or delay in

acceptance of delivery. This leads to opportunity loss and/or increase in the working capital cycle for the company,

thereby leading to pressure on return on capital employed. This becomes much more crucial in MHE segment,

whereby the execution cycle is high at 18 – 24 months.

Alternate energy: a futuristic opportunity at nascent stage

EECL has presence in alternate energy through two segments, namely wind turbines and wind farms. The

company manufactures wind turbines in 50 and 60 hz frequencies with the technical know-how obtained from

Turbowinds N.V. of Belgium. EECL has successfully commissioned 600 kW wind turbine at Newburyport in

USA in February 2009. The wind turbine division currently does not have sizeable orders for wind turbines.

However, the company has got sizeable orders for planetary gears that can be manufactured in the wind turbine

division, which has taken its capacity utilisation rate to 45 – 50 per cent. The company also has wind farms in

Gujarat with total capacity of 75 MW. The wind energy has humungous opportunity, given the limited natural

resources and concerns of global warming. However, the opportunity is still at a nascent stage in India.

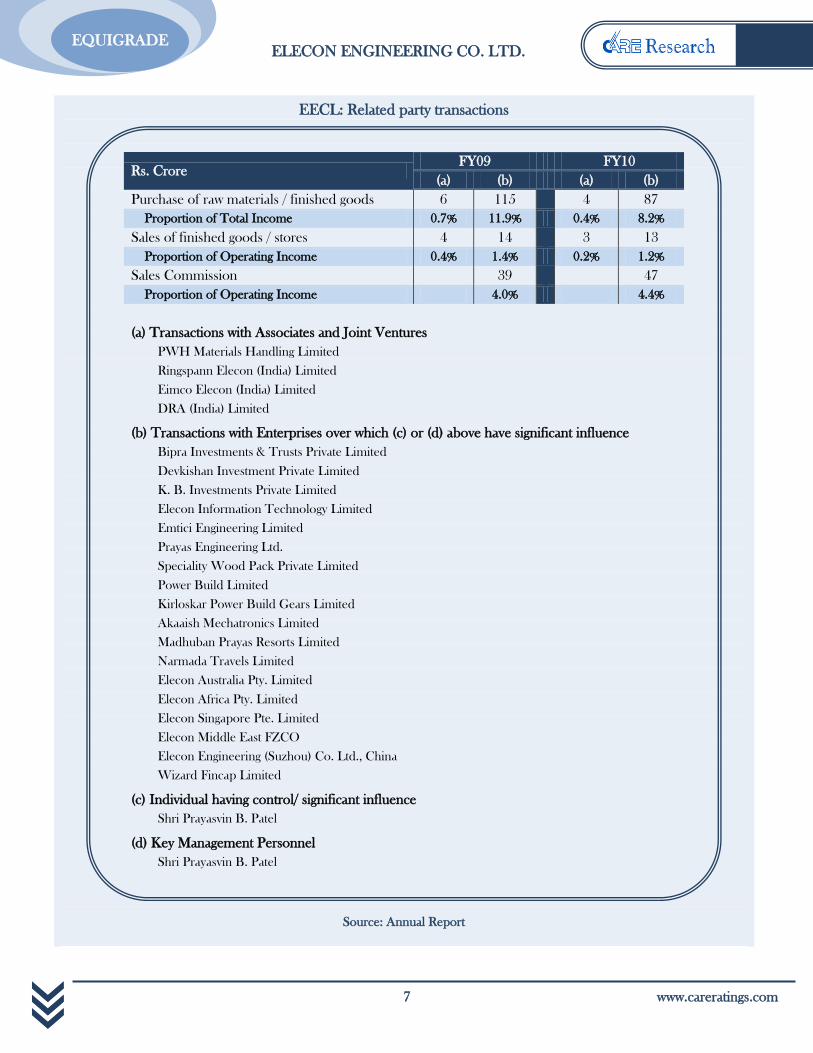

Group companies add to the company’s strengths

Emtici Engineering Limited (EEL), which is the part of the Elecon group and holds 23 per cent stake in EECL, is

the sole marketing agent for the company. EEL, incorporated in 1956, started its business as a company involved

in marketing, erection and servicing of imported machineries in the engineering sector. After developing its

expertise in the marketing field and looking at the growth prospects for the products it marketed, EEL promoted

EECL and other Elecon group companies as a step towards backward integration. EEL markets MHE and gear

division products of EECL and also provides after sales service to EECL’s customers. Orders procured by EEL

are with prior consent of EECL and are passed on to the company immediately upon receipt for which EEL

receives sales commission that varies from product to product.

EECL holds 16.6 per cent stake in Eimco Elecon (India) Limited (EEIL), which is engaged in manufacturing,

marketing and servicing equipments for mining and construction. EEIL is the domestic industry leader in

manufacturing of machinery for underground mining. The investment gives EECL exposure to the mining and

construction industry, which have significant growth prospects.

There are various other group companies, with operations largely concentrated in engineering sector. This gives

operational strength to EECL in terms of sourcing various inputs like castings from the group company(ies) and

outsourcing some portion of job-work to/from the group company(ies).

ELECON ENGINEERING CO. LTD.

7 www.careratings.com

EQUIGRADE

EECL: Related party transactions

Source: Annual Report

Rs. Crore FY09 FY10

(a) (b) (a) (b)

Purchase of raw materials / finished goods 6 115

4 87

Proportion of Total Income 0.7% 11.9% 0.4% 8.2%

Sales of finished goods / stores 4 14

3 13

Proportion of Operating Income 0.4% 1.4% 0.2% 1.2%

Sales Commission

39

47

Proportion of Operating Income 4.0% 4.4%

(a) Transactions with Associates and Joint Ventures

PWH Materials Handling Limited

Ringspann Elecon (India) Limited

Eimco Elecon (India) Limited

DRA (India) Limited

(b) Transactions with Enterprises over which (c) or (d) above have significant influence

Bipra Investments & Trusts Private Limited

Devkishan Investment Private Limited

K. B. Investments Private Limited

Elecon Information Technology Limited

Emtici Engineering Limited

Prayas Engineering Ltd.

Speciality Wood Pack Private Limited

Power Build Limited

Kirloskar Power Build Gears Limited

Akaaish Mechatronics Limited

Madhuban Prayas Resorts Limited

Narmada Travels Limited

Elecon Australia Pty. Limited

Elecon Africa Pty. Limited

Elecon Singapore Pte. Limited

Elecon Middle East FZCO

Elecon Engineering (Suzhou) Co. Ltd., China

Wizard Fincap Limited

(c) Individual having control/ significant influence

Shri Prayasvin B. Patel

(d) Key Management Personnel

Shri Prayasvin B. Patel

ELECON ENGINEERING CO. LTD.

www.careratings.com 8

EQUIGRADE

Acquisition of Benzlers - Radicon Group: access to American and European markets

EECL, through its subsidiaries in Mauritius, Sweden, UK & USA has acquired with effect from 26th

November,

2010, the operations of the Benzlers - Radicon Group (B-R Group) from David Brown Gear Systems Group

through a Sale and Purchase Agreement executed on 25th

October, 2010. The said acquisition include:

• 100 per cent share-holding of David Brown Systems Sweden AB or the Benzlers business

• Applied Products Division – Radicon – of David Brown Gear Systems, UK

• Certain assets of the gear motor business of Cone Drive Inc. US

These acquisitions have been made at a total cost of £ 18.4 million (Rs. 130 – 135 crore), funded through own

funds of £ 4.2 million (Rs. 30 crore) and foreign currency loan of £ 14.2 million (Rs. 100 – 105 crore) from Bank

of Baroda, Dubai at floating rate of LIBOR plus 375 basis points.

The acquisition would strengthen the industrial gear business of the company by the way of enhancement in the

product portfolio. The company, with leadership position in the domestic industrial gear industry, can leverage the

brand name of Benzlers - Radicon and widen its customer base, especially in the European, North American and

Scandinavian countries. With merely 6 per cent of the revenues from non-Indian markets in FY10, these

acquisitions would offer the company a platform to grow its non-domestic revenues to a larger international base

and thereby geographically diversify its revenue stream.

Over the period of time, the company can also have the execution of the orders of Benzlers – Radicon Group to

EECL’s Indian operations, which can reduce its costs and expand the margins. Currently, significant portion of

Benzlers - Radicon Group’s orders are outsourced to other companies in their respective local countries of

operation. Nevertheless, the conversion of the aforesaid opportunities into the EECL’s bottom-line needs to be

seen over the period of time.

EECL is in compliance with the listing agreement

EECL’s board comprises of six directors, of which three are non-independent and three are independent

directors. Thus, half of the board comprises of independent directors. The board is chaired by Shri Prayasvin

Patel, a non-independent executive director, who is also the managing director of the company.

EECL has formed three board level committees – Audit Committee, Shareholders’/Investors’ Grievance

Committee and Remuneration Committee. All three committees are chaired by independent director as required

by the Listing Agreement. Shri Paresh Shukla, Company Secretary, is the Compliance Officer for the company.

ELECON ENGINEERING CO. LTD.

9 www.careratings.com

EQUIGRADE

EECL: Board of Directors

CMD: Chairman and Managing Director

Source: Company

Board of Directors

Shri Prayasvin B. Patel Non-Independent &

Executive CMD B.E. (Mech), MBA

Shri Pradeep M. Patel Non-Independent &

Non-executive Director MBA

Shri Prashant C. Amin Non-Independent &

Non-executive Director

Masters in Engineering,

Management and Finance

Shri Chirayu R. Amin Independent &

Non-executive Director MBA (CMD, Alembic Ltd.)

Shri Hasmukhlal S. Parikh Independent &

Non-executive Director CA

Dr. Amritlal C. Shah Independent &

Non-executive Director M.A., Ph.D. (Economics)

ELECON ENGINEERING CO. LTD.

www.careratings.com 10

EQUIGRADE

CARE Equity Research values EECL at Rs. 98 per share

According to CARE Equity Research, the Current Intrinsic Value (CIV) of EECL stands at Rs. 98 per share. This

translates into Enterprise Value (EV) of around Rs. 1,572 crore. Thus, the equity shares of EECL have

‘Considerable Upside Potential’ from current market price (CMP) of Rs 68.35 per share.

The CIV is calculated based on Discounted Cash Flow model

CARE Equity Research has arrived at CIV of the stock on the basis of Discounted Cash Flow (DCF) model. The

overall firm Weighted Average Cost of Capital (WACC) is calculated based on our long term assumptions of cost

of financing summarized in below table.

• CARE Equity Research has used Free Cash Flow (FCF) methodology to arrive at the firm value, as EECL’s

business is (working) capital intensive in nature.

• The forecasted FCF is as per CARE Equity Research estimates.

• Terminal value is arrived at by using Gordon Growth Model.

• Terminal value forms 81 per cent of the firm’s total equity value, which appears to be reasonable.

EECL: Valuation Based on Discounted Cash Flows (DCF)

VALUATION GRADE Considerable Upside Potential 5/5

Item Value Basis

Risk Free Rate 8.25% 10 year G-sec yield expected at year end FY11

Equity Risk Premium 6.00%

Beta 0.84 One year performance vis-à-vis Sensex

Cost of Equity 13.28%

Cost of Debt 11.00% Long term cost of debt

Tax Rate 33.00% Long term tax rate

D/E Ratio 1.25 Long term target D/E ratio

WACC 10.00%

Terminal growth rate 3.00%

ELECON ENGINEERING CO. LTD.

11 www.careratings.com

EQUIGRADE

Source: CARE Equity Research

EECL: Sensitivity Analysis – Share price

Source: CARE Equity Research

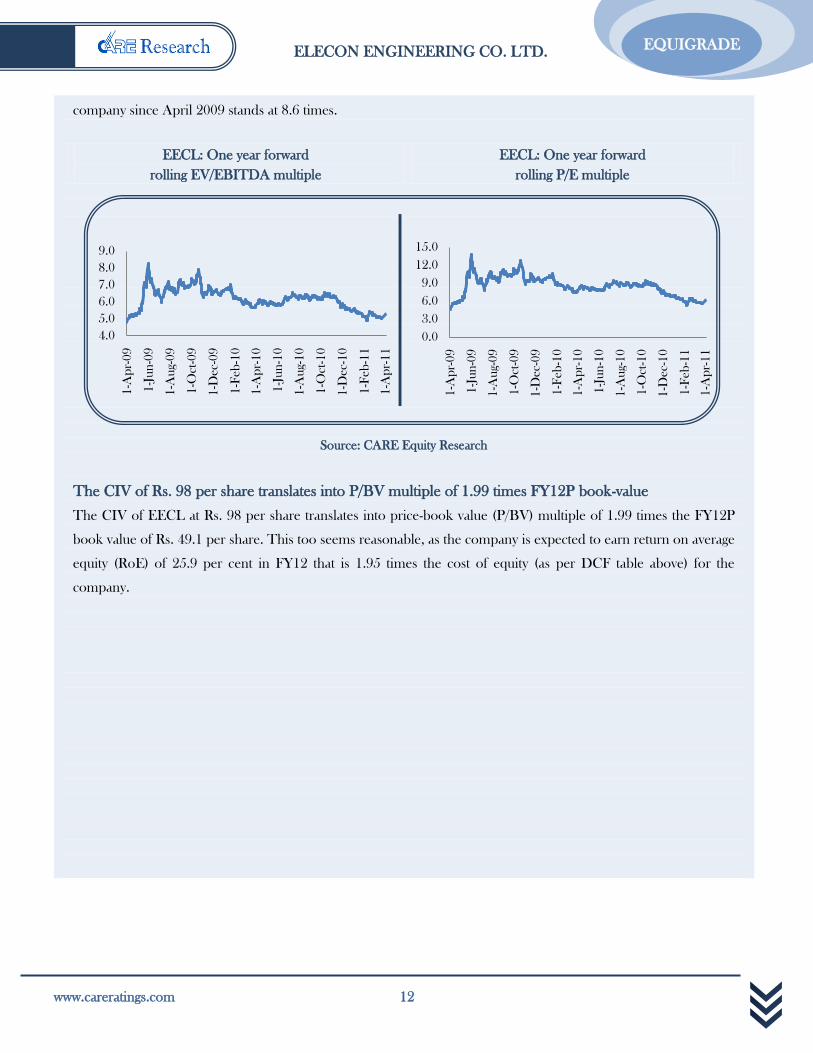

The CIV of Rs. 98 per share translates into EV/EBITDA multiple of 6.25 times FY12P EBITDA and

P/E of 8.5 times FY12P EPS

The CIV of EECL at Rs. 98 per share as arrived by CARE Equity Research translates into Enterprise Value to

EBITDA (EV/EBITDA) multiple of 6.25 times the FY12P EBITDA of Rs. 252 crore. This seems reasonable, as

the average one year forward rolling EV/EBITDA multiple for the company since April 2009 stands at 6.2 times.

Similarly, the CIV of Rs. 98 per share translates into price-earnings (P/E) multiple of 8.5 times the FY12P EPS of

Rs. 11.54 per share. This too seems reasonable, as the average one year forward rolling P/E multiple for the

(Rs crore except per share data)

2011-12 2012-13 2013-14 2014-15 2015-16

PAT 107 132 150 173 198

DTL 2 3 3 4 4

Depreciation 35 39 43 47 49

Interest (1-T) 42 48 55 58 61

Capex -75 -90 -90 -90 -90

Increase in WC -37 -101 -79 -97 -85

Free Cash Flow 75 31 81 95 137

Discount Rate 0.91 0.83 0.75 0.68 0.62

PV of FCF 68 25 61 65 85

PV of Terminal Value 1,267

Total Discounted Value of Firm 1,572

Less: Net Debt (FY11 P) 666

Present Value of Equity 906

No of Equity Shares (crore) 9.3

CIV 98

Term

inal

Year

Gro

wth

Rat

e

Weighted Average Cost of Capital (%)

9.0% 9.5% 10.0% 10.5% 11.0%

2.0% 86 83 79 76 73

2.5% 95 91 88 85 81

3.0% 105 101 98 94 91

3.5% 117 113 109 105 101

4.0% 130 126 122 118 114

ELECON ENGINEERING CO. LTD.

www.careratings.com 12

EQUIGRADE

company since April 2009 stands at 8.6 times.

EECL: One year forward

rolling EV/EBITDA multiple

EECL: One year forward

rolling P/E multiple

Source: CARE Equity Research

The CIV of Rs. 98 per share translates into P/BV multiple of 1.99 times FY12P book-value

The CIV of EECL at Rs. 98 per share translates into price-book value (P/BV) multiple of 1.99 times the FY12P

book value of Rs. 49.1 per share. This too seems reasonable, as the company is expected to earn return on average

equity (RoE) of 25.9 per cent in FY12 that is 1.95 times the cost of equity (as per DCF table above) for the

company.

4.0

5.0

6.0

7.0

8.0

9.0

1-A

pr-

09

1-J

un

-09

1-A

ug-

09

1-O

ct-0

9

1-D

ec-

09

1-F

eb

-10

1-A

pr-

10

1-J

un

-10

1-A

ug-

10

1-O

ct-1

0

1-D

ec-

10

1-F

eb

-11

1-A

pr-

11

0.0

3.0

6.0

9.0

12.0

15.0

1-A

pr-

09

1-J

un

-09

1-A

ug-

09

1-O

ct-0

9

1-D

ec-

09

1-F

eb

-10

1-A

pr-

10

1-J

un

-10

1-A

ug-

10

1-O

ct-1

0

1-D

ec-

10

1-F

eb

-11

1-A

pr-

11

ELECON ENGINEERING CO. LTD.

13 www.careratings.com

EQUIGRADE

History of EECL dates five decades back

The history of EECL dates back to 1951, when a small firm was established in Mumbai (then known as Bombay)

by Late Shri Ishwarbhai B. Patel for indigenously manufacturing conveying equipments. With increase in business

operations, it was converted into a private limited company – Elecon Engineering Private Limited – in January

1960. Later during 1960, it shifted its base to Vallabh Vidya Nagar, Gujarat and became a public limited company –

EECL – soon thereafter.

Company Overview

Source: Company, CARE Equity Research

Business Divisions

The company operates in two major reportable segments – Material Handling Equipment (MHE) and

Transmission Equipment (Gear Division). In FY10, company reported gross sales of Rs. 655 crore from MHE

segment or 61 per cent of EECL’s gross revenue and Rs. 426 crore from Transmission Equipment segment or 39

per cent of EECL’s gross revenue. The company also has presence in alternate energy, which currently being a

small segment, is not reported separately in the company’s segmental finance report.

COMPANY BACKGROUND

ELECON ENGINEERING CO. LTD.

www.careratings.com 14

EQUIGRADE

Material Handling Equipment (MHE) Division

EECL has been in the business of MHE for close to five decades. It supplies MHE to core sectors like mining,

cement, steel, fertilizer, power generation / coal handling and ports. Its products include:

• belt conveyors

• stacker-cum-reclaimers

• pusher cars

• idlers and pulleys

• barrel type blender reclaimers

• ship loaders and unloaders

• stacker

• bridge type bucket wheel reclaimers

• crawler mounted bucket wheel excavators

• reclaimers

• wagon tipplers and side arm chargers

• crushers

• feeders and

• a range of all type of bulk material handling equipments

Over the years, EECL has designed and executed turnkey contracts for crushing, screening, stacking, blinding and

reclaiming plants for bulk materials such as limestone, iron-ore, bauxite, overburden, rock phosphate and

fertilizers.

The MHE division reported gross sales of Rs. 655 crore or 61 per cent of EECL’s gross revenue, up by 11.5 per

cent over Rs. 588 crore reported in FY09. In the first 9 months of FY11 (9M-FY11), the revenues of this division

stood at Rs. 475 crore or 56 per cent of company’s gross revenue in the same period.

Transmission Equipment Division (Gear Division)

EECL has a separate gear division, which manufactures:

• helical and bevel helical gear boxes

• worm gear boxes

• elevator traction machines (lift gear boxes)

• couplings

• wind mill gear boxes

• high speed gear boxes

• planetary gear boxes

• marine gear boxes

ELECON ENGINEERING CO. LTD.

15 www.careratings.com

EQUIGRADE

• geared motors

• custom built gear boxes

• vertical roller mill drive

The company has expertise in providing customised gear boxes for steel mills, high speed turbines, sugar mills,

marine vessels, coast guard ships, plastic extrusions, antenna drives and for satellites in the Indian Space

Programme.

The gear division reported gross sales of Rs. 426 crore or 39 per cent of EECL’s gross revenue, up by 8 per cent

over Rs. 394 crore reported in FY09. In the first 9 months of FY11 (9M-FY11), the revenues of this division stood

at Rs. 368 crore or 44 per cent of company’s gross revenue in the same period.

Alternate Energy Division

EECL also has presence in alternate energy, which currently being a small segment, is not reported separately in the

company’s segmental finance report. Besides having wind farms in Varvala and Naransari in Gujarat, EECL

manufactures wind turbines with the technical know-how obtained from Turbowinds N.V. of Belgium. EECL has

successfully commissioned 600 kW wind turbine at Newburyport in USA in February 2009.

16.6 per cent stake in Eimco Elecon (India) Limited [EEIL]

EECL has 16.6 per cent stake in EEIL, which is a listed entity. EEIL provides technological solution for extracting

natural resources from earth by designing, manufacturing, marketing and servicing equipments for mining and

construction. EEIL was incorporated in 1974 and was first to introduce the intermediate technology of Side Dump

Loaders (SDL), Load Haul Dumpers (LHD) and Rocker Shovel Loaders (RSL) in India to partially mechanize the

underground mining.

Acquisition of Benzlers-Radicon Group

EECL, through Special Purpose Vehciles (SPVs) has acquired:

• 100 per cent share-holding of David Brown Systems Sweden AB or the Benzlers business

• Applied Products Division – Radicon – of David Brown Gear Systems, UK

• Certain assets of the gear motor business of Cone Drive Inc. US

The gross value of 100 per cent stake of these businesses as going concern on debt and cash free basis is £ 18.4

million (Rs. 130 – 135 crore). The acquisition has opened up opportunity for the company to strengthen its

product development and engineering capabilities and widen its customer base, especially in the European, North

American and Scandinavian countries.

ELECON ENGINEERING CO. LTD.

www.careratings.com 16

EQUIGRADE

EECL’s board comprises of six directors; three non-independent and three independent

EECL’s board comprises of six directors, of which three are non-independent and three are independent directors.

The board is chaired by Shri Prayasvin Patel, who is also the managing director of the company. The board is well

supported by professionals in senior and middle-level management positions.

EECL: Board and other key managerial personnel

CMD: Chairman and Managing Director

Source: Company

Board of Directors

Shri Prayasvin B. Patel Non-Independent &

Executive - CMD B.E. (Mech), MBA

Shri Pradeep M. Patel Non-Independent & Non-

executive Director MBA

Shri Prashant C. Amin Non-Independent & Non-

executive Director

Masters in Engineering,

Management and Finance

Shri Chirayu R. Amin Independent & Non-

executive Director MBA (CMD, Alembic Ltd.)

Shri Hasmukhlal S. Parikh Independent & Non-

executive Director CA

Dr. Amritlal C. Shah Independent & Non-

executive Director M.A., Ph.D. (Economics)

Other Key Management Personnel

Shri Hemendra C. Shah Chief Financial Officer

Shri U. V. Phani Kumar Chief Executive Officer -

MHE Division

Shri V B Kalyankar Chief Executive Officer -

Gear Division

Shri Paresh M. Shukla Company Secretary and

Compliance Officer

ELECON ENGINEERING CO. LTD.

17 www.careratings.com

EQUIGRADE

Material Handling Equipment (MHE) Industry

MHE industry forms part of the capital goods industry. The industry can be broadly divided into:

• Material handling systems comprising bulk material handling and unit load handling

• Ash handling systems.

The equipments manufactured include bulk, powder and other solids handling systems for coal, ash and other raw

materials and finished products such as cement. The material handling equipment includes belt conveying systems,

pneumatic conveying systems, crushing and screening equipment, coal/ore/ash handling plants and associated

equipment such as stackers, reclaimers, ship loaders/unloaders, wagon tipplers and feeders which cater to the needs

of the core industries such as power, cement, port, mining, fertilizers and steel. Hence the growth of MHE industry

is linked to the growth in the said core industries.

According to CARE Research, the core industries are expected to grow at a healthy rate of 9 – 10 per cent per

annum through the next five years on the back of both buoyant industrial capex plans as well as humungous

investments by the Government in infrastructure sector. Rising household income levels translate into growing

demand for consumer goods, which in turn drive the growth of the capital goods / core industries. Buoyancy in the

core industries would facilitate the growth in order book for the MHE industry.

The level of competition in Indian MHE industry is relatively high. Furthermore, the Indian companies face

competition from foreign companies as well. Rising commodity prices in the light of recovery in the global

economy is also a challenge for the MHE industry.

Industrial Gear Industry

The industrial gears industry also forms part of the capital goods industry. Manufacturing of gears and gearboxes

involves high precision machining and accurate assembly as mechanical power is to be transmitted noiselessly and

without losses. There are different types and sizes of gears such as helical gears, worm gears, spiral gears, etc. The

products find application in almost all manufacturing industries including cement, steel, sugar, elevators, fertilizer,

plastic, rubber, wind energy, etc. as well as the MHE industry. On the back of buoyant outlook for the Indian

manufacturing as well as MHE industry, the prospects remain bright for the Indian gear industry.

The level of competition in Indian industrial gear industry is relatively high. Furthermore, the Indian companies

face competition from foreign companies, especially from China. The rising commodity prices are a challenge for

the gear industry as well.

SNAPSHOT OF THE INDUSTRY

ELECON ENGINEERING CO. LTD.

www.careratings.com 18

EQUIGRADE

Consolidated Income Statement

(Rs. Crore) FY08 FY09 FY10 FY11 P FY12 P FY13 P

Total Income 836 965 1,071 1,274 1,648 1,895

EBITDA 140 159 174 203 252 299

Depreciation and amortisation 14 22 33 29 35 39

EBIT 126 136 141 174 216 261

Interest 27 48 51 53 63 72

PBT 99 88 90 121 153 189

Ordinary PAT (After minority interest) 67 57 66 89 107 132

PAT (After minority interest) 67 57 66 89 107 132

Fully Diluted Earnings Per Share* (Rs.) 7.2 6.2 7.1 9.6 11.5 14.2

Dividend, including tax 16 16 16 16 22 27

* Calculated based on ordinary PAT on Current Face Value of Rs. 2/- per share

Consolidated Balance Sheet

(Rs. Crore) FY08 FY09 FY10 FY11 P FY12 P FY13 P

Net worth (incl. Minority Interest) 236 274 324 371 456 561

Debt 409 592 522 691 715 799

Deferred Liabilities / (Assets) 17 33 40 42 44 47

Capital Employed 662 899 885 1,104 1,216 1,407

Net Fixed Assets, incl. Capital WIP 193 311 362 390 465 555

Investments 9 11 6 6 6 6

Loans and Advances 57 75 55 65 84 97

Inventory 253 401 315 419 497 561

Receivables 492 472 518 684 754 867

Cash and Cash Equivalents 8 61 39 25 34 39

Current Assets, Loans and Advances 810 1,008 926 1,193 1,368 1,563

Less: Current Liabilities and Provisions 350 432 409 485 623 716

Total Assets 662 899 885 1,104 1,216 1,407

Ratios based on Consolidated Financials

FY08 FY09 FY10 FY11 P FY12 P FY13 P

Growth in Operating Income 14.7% 15.4% 11.0% 19.0% 29.4% 15.0%

Growth in EBITDA 18.6% 13.1% 9.9% 16.7% 23.7% 19.0%

Growth in PAT 22.4% -14.5% 15.2% 34.0% 20.8% 23.2%

Growth in EPS 18.7% -14.5% 15.2% 34.0% 20.8% 23.2%

EBITDA Margin 16.8% 16.4% 16.3% 16.0% 15.3% 15.8%

PAT Margin 8.0% 6.0% 6.2% 7.0% 6.5% 7.0%

RoCE 21.9% 17.5% 15.8% 17.5% 18.7% 19.9%

RoE 31.8% 22.6% 22.2% 25.5% 25.9% 25.9%

Net Debt-Equity (times) 1.7 1.9 1.5 1.8 1.5 1.4

Interest Coverage (times) 5.1 3.3 3.4 3.9 4.0 4.2

Current Ratio (times) 2.3 2.3 2.3 2.5 2.2 2.2

Inventory Days 110 152 107 120 110 108

Receivable Days 215 178 176 196 167 167

Price / Earnings (P/E) Ratio 9.6 7.2 5.9 4.8

Price / Book Value(P/BV) Ratio

2.0 1.7 1.4 1.1

Enterprise Value (EV)/EBITDA 7.5 6.4 5.2 4.3

Source: Company, CARE Equity Research

FINANCIAL STATISTICS

ELECON ENGINEERING CO. LTD.

19 www.careratings.com

EQUIGRADE

CARE Equigrade Grid (CEG)

Through CEG, CARE Equity Research addresses two critical factors considered by an investor while investing in a

particular company’s equity shares:

1. Fundamentals: Whether the company is fundamentally sound with respect to its business, its financial position, its

management and its prospects.

2. Valuation: What is the Current Intrinsic Value (CIV) of the stock and how it compares vis-a-vis its Current

Market Price (CMP)

These factors are answered assigning quantitative grades to both these parameters. CEG is the snapshot of

‘Fundamental Grade’ and ‘Valuation Grade’ assigned by CARE Equity Research.

Fundamental Grade

This grade represents how sound the company is fundamentally, vis-à-vis other listed companies in India. This grade

captures:

1. Business Fundamentals and Prospects

2. Financial Soundness

3. Management Quality

4. Corporate Governance Practices

The grade is assigned on a five-point scale as under:

CARE Fundamental Grade Evaluation

5/5 Strong Fundamentals

4/5 Very Good Fundamentals

3/5 Good Fundamentals

2/5 Modest Fundamentals

1/5 Weak Fundamentals

Valuation Grade

This grade represents the potential value in the company’s equity share for the investor over a 1 year period. The

Current Intrinsic Value (CIV) or the price arrived by CARE Equity Research on fundamental basis is compared with

the current market price (CMP) of the stock and the grade is assigned based on the gap between CIV and CMP of the

stock.

EXPLANATION OF GRADES

ELECON ENGINEERING CO. LTD.

www.careratings.com 20

EQUIGRADE

The grade is assigned on a five-point scale as under:

CARE Valuation Grade Evaluation

5/5 Considerable Upside Potential

(>25% from CMP)

4/5 Moderate Upside Potential

(10-25% from CMP)

3/5 Fairly Priced

(+/- 10% from CMP)

2/5 Moderate Downside Potential

(Negative 10-25 from CMP)

1/5 Considerable Downside Potential

(<25% from CMP)

Grading determination is a matter of experienced and holistic judgment, based on relevant quantitative and qualitative factors of

the company in relation to other listed companies.

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there exists no conflict of

interest that can bias the grading recommendation of the company.

This report has been sponsored by the company.

DISLCLAIMER

This report is prepared by CARE Research, a division of Credit Analysis & REsearch Limited [CARE]. CARE Research has taken

utmost care to ensure accuracy and objectivity while developing this report based on information available in public domain or from

sources considered reliable. However, neither the accuracy nor completeness of information contained in this report is guaranteed.

CARE Research operates independently of ratings division and this report does not contain any confidential information obtained by

ratings division, which they may have obtained in the regular course of operations. Opinions expressed herein are our current

opinions as on the date of this report.

CARE’s valuation of the security is mainly based on company specific fundamental factors. Equity prices are affected by both

fundamental factors as well as market factors such as – liquidity, sentiment, broad market direction etc. The impact of market factors

can distort the price of the security thereby deviating from the intrinsic value for extended period of time. This report should not be

construed as recommendation to buy, sell or hold a security or any advice or any solicitation, whatsoever. It is also not a comment on

the suitability of the investment to the reader. The subscriber / user assumes the entire risk of any use made of this report or data

herein. CARE specifically states that it or any of its divisions or employees have no financial liabilities whatsoever to the subscribers /

users of this report. This report is for personal information only of the authorised recipient in India only. This report or part of it

should not be reproduced or redistributed or communicated directly or indirectly in any form to any other person, especially outside

India or published or copied for any purpose.

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express Highway, Somaiya

Hospital Road, Sion East, Mumbai – 400 022.

CARE Research is not responsible for any errors or omissions in analysis/inferences/views or for results obtained from the use of

information contained in this report and especially states that CARE (including all divisions) has no financial liability whatsoever to

the user of this product. This report is for the information of the intended recipients only and no part of this report may be published

or reproduced in any form or manner without prior written permission of CARE Research.

ELECON ENGINEERING CO. LTD.

21 www.careratings.com

EQUIGRADE

Credit Analysis & REsearch Ltd. (CARE) is a full service rating company that offers a wide range of rating and grading services

across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in line with the best international

practices.

CARE Research

CARE Research is an independent research division of CARE Ratings, a full service rating company. CARE Research is

involved in preparing detailed industry research reports with 5 year demand and 2 year profitability outlook on the industry

besides providing comprehensive trend analysis and the current state of the industry. CARE Research also offers research that

is customised to client requirements. CARE Research currently offers reports on more than 21 industries that include Cement,

Steel, Aluminium, Construction, Shipping, Ship-building, Commercial Vehicles, Two-Wheelers, Tyres, Auto Components,

Pipes, Natural Gas, Retail, Sugar, etc. CARE Research now offers independent research of equities through its product

‘EQUIGRADE’.

CREDIT ANALYSIS & RESEARCH LTD

HEAD OFFICE |Mr. P. N. Satheeskumar | Cell: +91-9820416004 | Tel: +91-22-6754 3555 | E-mail:

4th Floor, Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai - 400 022 |

Tel: +91-022- 6754 3456 | E-mail: [email protected] | Fax: +91-022- 6754 3457

KOLKATA | Mr. Sukanta Nag | Cell: +91-98311 70075 | Tel: +91-33- 2283 1800/ 1803, 2280 8472 |

E- mail: [email protected] | 3rd Flr., Prasad Chambers (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata -700 071

CHENNAI | Mr. V Pradeep Kumar | Cell: +91 9840754521 | Tel: +91-44-2849 7812/2849 0811 | Fax: +91-44-2849 0876 |

Email: [email protected] | Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769, Anna Salai, Chennai - 600 002

AHMEDABAD | Mr. Mehul Pandya | Cell: +91-98242 56265 | Tel: +91-79-40265656 | Fax: +91-79-40265657 |

E-mail:[email protected] | 32, Titanium, Prahaladnagar Corporate Road, Satellite, Ahmedabad - 380 015.

NEW DELHI | Ms. Swati Agrawal | Cell: +91-98117 45677 | Tel: +91- 11- 2331 8701/ 2371 6199 |

E-mail: [email protected] | 3rd Floor, B -47, Inner Circle, Near Plaza Cinema, Connaught Place, New Delhi - 110 001.

BANGALORE | Mr. G. Sundara Vathanan | Cell: +91 98860 24430 | Tel:+91-80-2211 7140 |

E-mail: [email protected] | Unit No. 8, I floor, Commander's Place, No. 6, Raja Ram Mohan Roy Road,

(Opp. P F Office), Richmond Circle, Bangalore - 560 025.

HYDERABAD | Mr. Ashwini Kumar Jani | Cell: +91-91766 47599 | Tel: +91-40-40102030 |

E-mail: [email protected] | 401, Ashoka Scintilla | 3-6-520, Himayat Nagar | Hyderabad - 500 029

ABOUT CARE