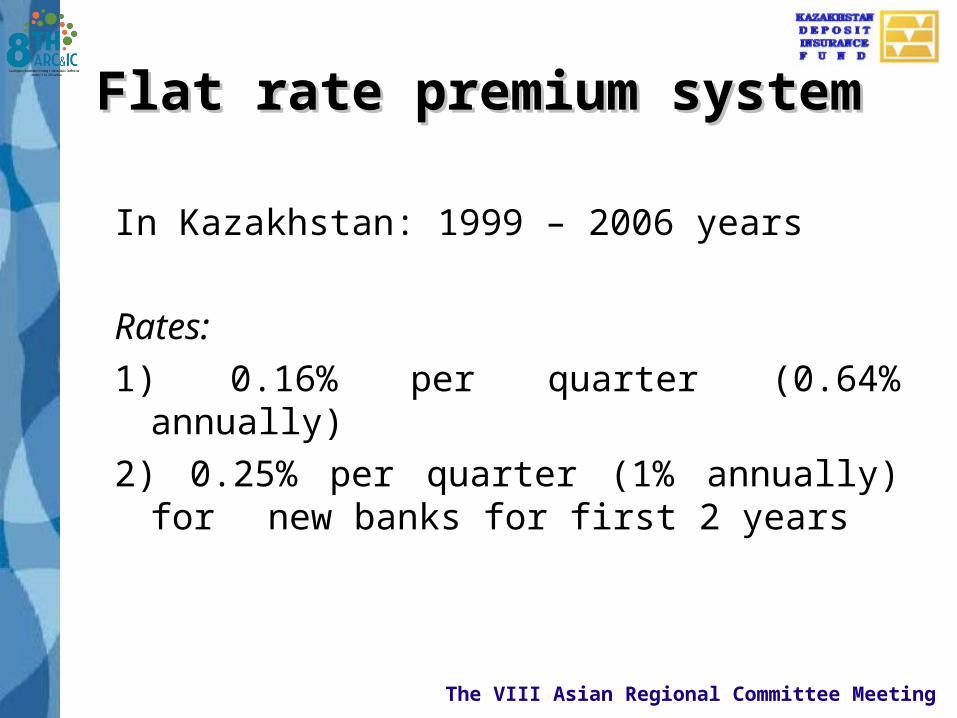

FUNDING FUNDING sources, mechanisms and sources, mechanisms and critical issues critical issues . . Experience of Experience of the KDIF the KDIF Presented by Mrs. Bakhyt Mazhenova Chair, KDIF

1. keeps track of their financial positions and any events with negative potentiality

2. inspects correctness and comprehensiveness of depositors’ records in the banks’ software

3. starts consultations with Regulators

The VIII Asian Regional Committee Meeting

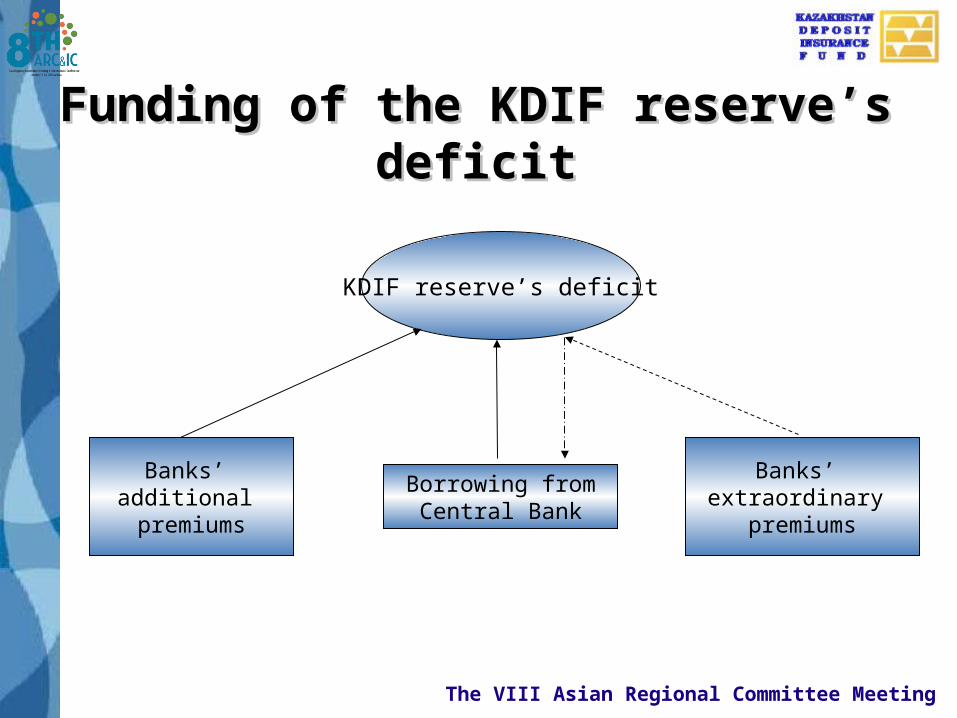

Is it always possible in the Is it always possible in the practice to cover reserve’ practice to cover reserve’ deficit by member-banks’ deficit by member-banks’

extra premiums?extra premiums?

The VIII Asian Regional Committee Meeting

Case studyCase study

• «Valut-Tranzit Bank» JSC – big regional bank failed in 2007 (number of guaranteed depositors exceeded 200,000 persons)

• In two cases out of three the KDIF’ reserve deficit was financed by its Sole Shareholder – the National Bank of Kazakhstan

It has established a precedent

The VIII Asian Regional Committee Meeting

Lesson learnedLesson learned

In practice it is complicated to implement theoretically attractive scheme on covering a reserve’ deficit by member-banks as market would always try to impose whole responsibility for bank’ failure on Regulator

The VIII Asian Regional Committee Meeting

The Kazakhstani DIS in crisisThe Kazakhstani DIS in crisis

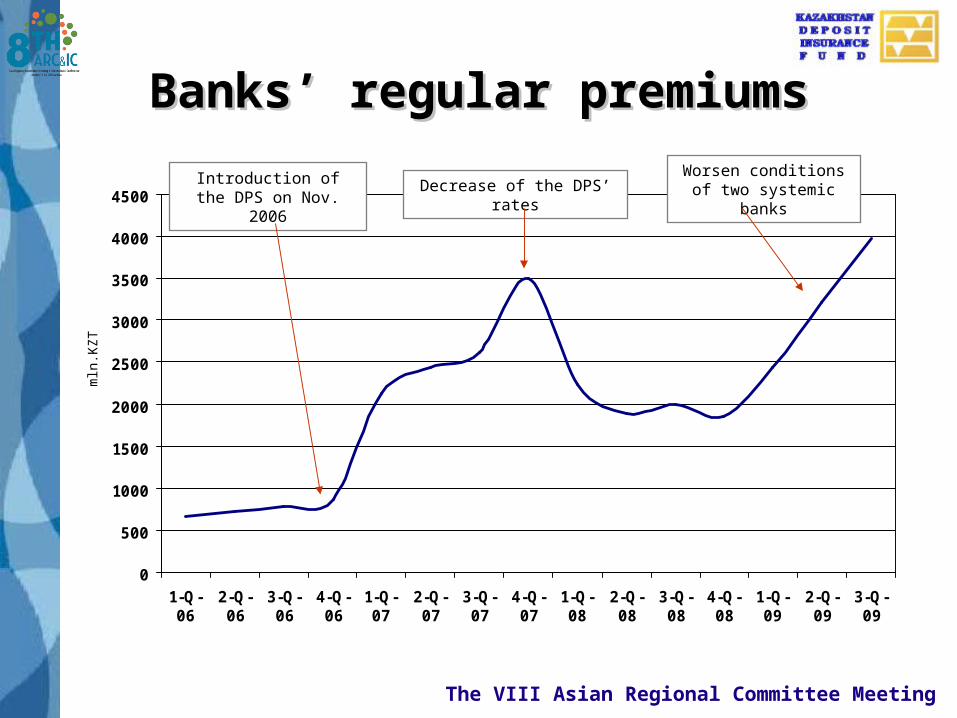

1. The coverage amount was increased more than 7 times – from 700 thousand KZT (≈4.7 ths.$) up to 5 million KZT (≈34 ths.$) the KDIF’ potential financial burden increased by 60%

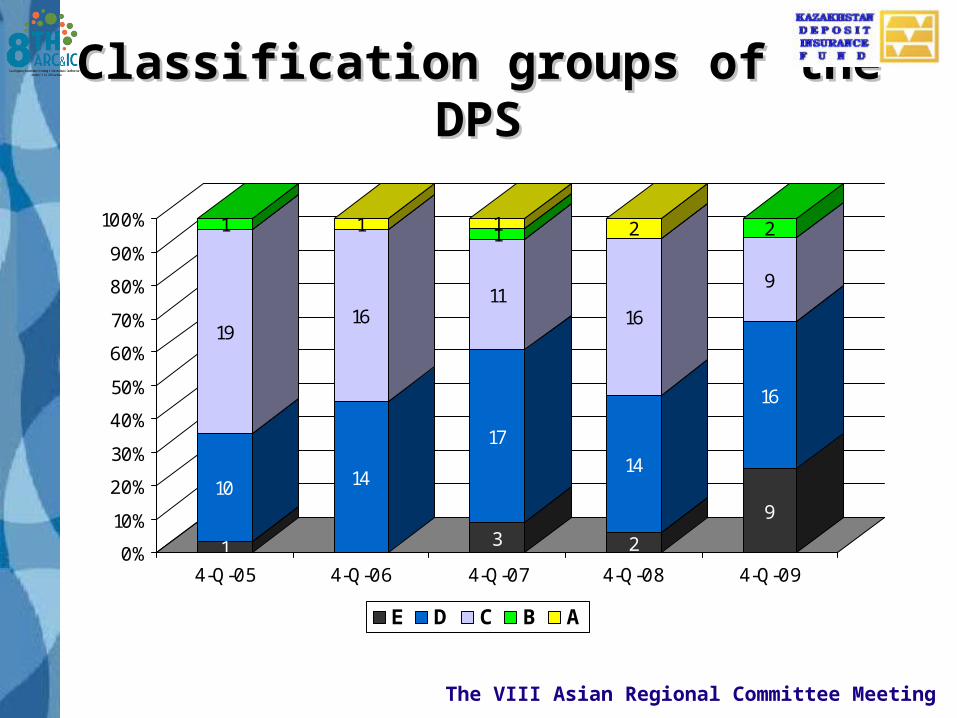

2. The financial positions and soundness of the banks, especially big ones, significantly deteriorated (since middle of 2009 two systemic banks are in the worse group – “E”)

The VIII Asian Regional Committee Meeting

Classification groups of the Classification groups of the DPSDPS

1

10

19

1

14

16

1

3

17

11

11

2

14

16

2

9

16

9

2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

4-Q-05 4-Q-06 4-Q-07 4-Q-08 4-Q-09

E D C B A

The VIII Asian Regional Committee Meeting

user

поменяй расцветку (более контрастную), а то рядом стоящие группы сливаются между собой. + добавь данные по количеству банков в каждой группе

The The KazakhstaniKazakhstani DIS in DIS in crisis crisis

3. The Kazakhstani banking sector is highly concentrated – 5 largest banks holds about 75% of total amount of retail deposits as well as total amount of the banks’ assets

The VIII Asian Regional Committee Meeting

Outcomes for the KDIFOutcomes for the KDIF

• The main portion of the premiums to the KDIF paid by mentioned 5 banks

• In case of the failure of some of these banks the reserve deficit might be significant

• The mechanism of reserve deficit’s financing by member-banks extra premiums in crisis environment is not applicable

The VIII Asian Regional Committee Meeting

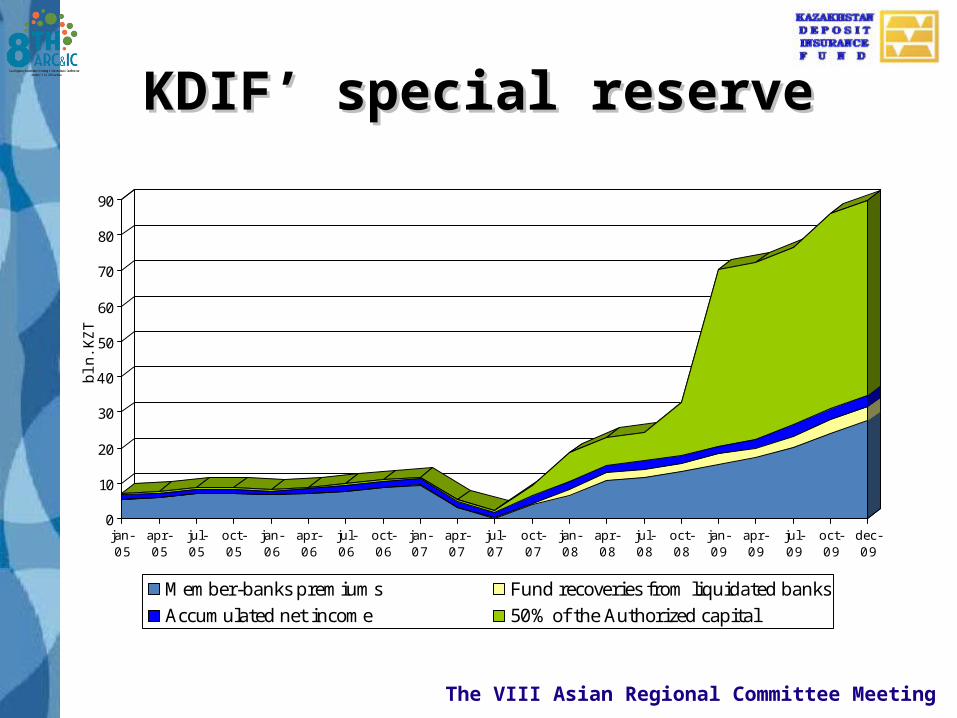

State’ financial support of the State’ financial support of the DIDI

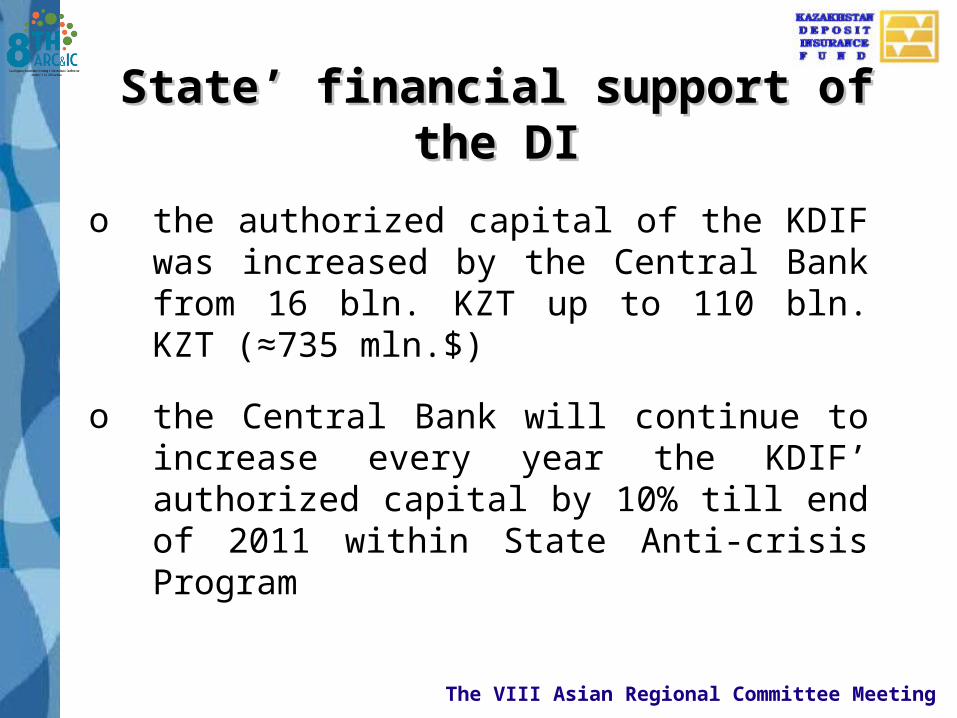

o the authorized capital of the KDIF was increased by the Central Bank from 16 bln. KZT up to 110 bln. KZT (≈735 mln.$)

o the Central Bank will continue to increase every year the KDIF’ authorized capital by 10% till end of 2011 within State Anti-crisis Program

The VIII Asian Regional Committee Meeting

Thank you forThank you foryour attentionyour attention