1

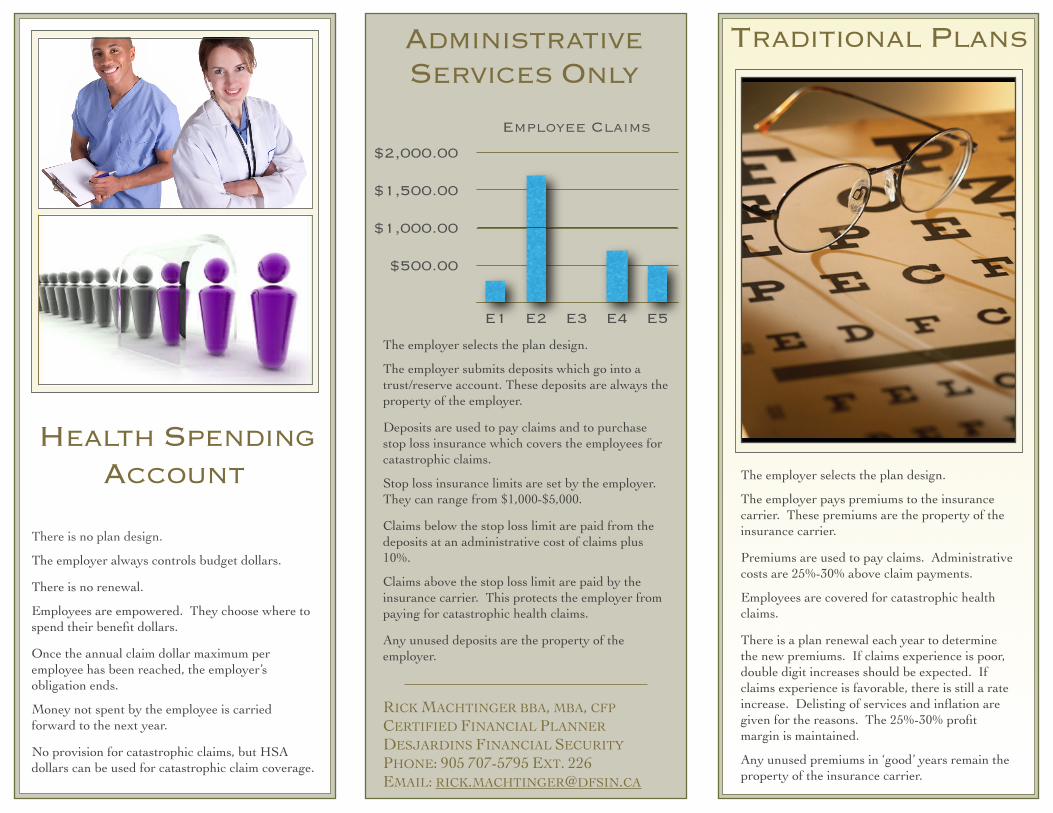

The employer selects the plan design. The employer pays premiums to the insurance carrier. These premiums are the property of the insurance carrier. Premiums are used to pay claims. Administrative costs are 25%-30% above claim payments. Employees are covered for catastrophic health claims. There is a plan renewal each year to determine the new premiums. If claims experience is poor, double digit increases should be expected. If claims experience is favorable, there is still a rate increase. Delisting of services and inflation are given for the reasons. The 25%-30% profit margin is maintained. Any unused premiums in ‘good’ years remain the property of the insurance carrier. TRADITIONAL PLANS There is no plan design. The employer always controls budget dollars. There is no renewal. Employees are empowered. They choose where to spend their benefit dollars. Once the annual claim dollar maximum per employee has been reached, the employer’s obligation ends. Money not spent by the employee is carried forward to the next year. No provision for catastrophic claims, but HSA dollars can be used for catastrophic claim coverage. The employer selects the plan design. The employer submits deposits which go into a trust/reserve account. These deposits are always the property of the employer. Deposits are used to pay claims and to purchase stop loss insurance which covers the employees for catastrophic claims. Stop loss insurance limits are set by the employer. They can range from $1,000-$5,000. Claims below the stop loss limit are paid from the deposits at an administrative cost of claims plus 10%. Claims above the stop loss limit are paid by the insurance carrier. This protects the employer from paying for catastrophic health claims. Any unused deposits are the property of the employer. RICK MACHTINGER BBA, MBA, CFP CERTIFIED FINANCIAL PLANNER DESJARDINS FINANCIAL SECURITY PHONE: 905 707-5795 EXT. 226 EMAIL: RICK.MACHTINGER@DFSIN.CA $500.00 $1,000.00 $1,500.00 $2,000.00 E1 E2 E3 E4 E5 Employee Claims ADMINISTRATIVE SERVICES ONLY HEALTH SPENDING ACCOUNT