FUNDS FLOW STATEMENT INTRODUCTION The basic financial statements i.e., the Balance Sheet and Profit & Loss A/c or Income Statement of business reveals the net effect of various transactions on operational and financial position of the company. The balance sheet gives a summary of the assets & liabilities of an undertaking at a particular point of time. There are many transactions that take place in an undertaking and which do not operate Profit & Loss A/c. Thus another statement has to be prepared to show the change in Assets & Liabilities from the end of one period of time to the end of another period of time. The statement is called a statement of changes in financial position or a Funds Flow Statement. The Funds Flow Statement is a statement which shown the movement of funds and is a report of financial operations of business undertaking. In simple words it is a statement of source and application of funds. MEANING & CONCEPT OF FUNDS The term “Fund” has been defined and interpreted differing by different experts. Broadly the term fund refers to all the 1

Transcript

FUNDS FLOW STATEMENT

INTRODUCTION

The basic financial statements i.e., the Balance Sheet and Profit & Loss A/c or Income

Statement of business reveals the net effect of various transactions on operational and financial

position of the company. The balance sheet gives a summary of the assets & liabilities of an

undertaking at a particular point of time.

There are many transactions that take place in an undertaking and which do not operate

Profit & Loss A/c. Thus another statement has to be prepared to show the change in Assets &

Liabilities from the end of one period of time to the end of another period of time. The statement

is called a statement of changes in financial position or a Funds Flow Statement.

The Funds Flow Statement is a statement which shown the movement of funds and is a

report of financial operations of business undertaking. In simple words it is a statement of

source and application of funds.

MEANING & CONCEPT OF FUNDS

The term “Fund” has been defined and interpreted differing by different experts. Broadly

the term fund refers to all the financial resource of the company on the other extreme fund has

been understood as cash only. The most acceptance meaning of the “fund” is “working capital”.

Working Capital is excess of current assents over current liability. The term fund has a

variety of meaning.

A) CASH FUND OR NARROW SENSE

In a narrow sense, funds mean only cash. ‘Cash flow statement portrays net effect of

various business transactions cash into account receipts & disbursement of cash.

1

The concept of preparing funds from statement is not accepted, as there are many such

transactions that do not affect cash but represent the flow of fund.

For Ex:

Purchase of furniture on credit does not affect cash but there is flow of fund.

B) CAPITAL FUND (or) BROADER SENSE

Here funds means all financial resources used in business, whether in the form of men,

money, material, machine & others.

C). NET WORKING CAPITAL (or) POPULAR SENSE

Networking capital means differences between current assets & liabilities. A fund

generally refers to cash or cash equipment or to working capital.

In any business we cannot under estimate the flow of funds from two operations. The

business runs with funds but the organization knows how to flow of funds.

The Funds Flow Statement is concerned with sources and applications of organization.

Statement of changes in working capital shows the increase or decrease in the working

capital.

“Funds from Operations” statement shows how much funds from operations.

Funds Flow Statement

In every concern, the funds flow in form different sources and similarly funds are

invested in various sources of investment. It is continuous process. The study and control of this

funds-flow process (i.e., the uses and sources of funds) is the main objective of financial

management to assess the soundness and the solvency of the enterprise.

2

The funds-flow-statement is a report on financial operations changes, flow or

movements during the period. It is a statement which shows the sources an application of funds

or it shows how the activities of a business are financed in a particulate period. In other words,

such a statement shows how the financial resources have been used during a particular period of

time. It is, thus, a historical statement showing sources and application of funds between the two

dates designed especially to analyses the changes in the financial conditions of an enterprise. In

the words of Fouke, it is-

“A statement of Sources and Application of Funds is a technical device designed to analyses

the changes in the financial condition of business enterprises between two dates.”

Funds Flow Statement is not an income statement. Income statement shows the items of

income and expenditure of a particular period, but the Funds flow statement is an operating

statement as it summaries the financial activities for a period of time. It covers all movements

that involve an actual exchange of assets.

Various titles are used for this statement such as 'Statement of sources and Application of

Funds', 'Summary of Financial operations,' 'Changes in Financial Position', 'Fund received and

Disbursed', 'Funds Generated and Expended', Changes in Working Capital”, “Statement of Fund'

etc. Title of Funds Flow Statement has been modified from time to time. Really it is very

difficult to find a short time for such statement which carries much to the readers regarding its

contents and functions.

A new interpretation of the term 'funds, has now been adopted as to include assets or

financial resourceful which do not flow through the working capital accounts. It seems to be the

most suitable meaning fort the term 'funds' but the most commonly used interpretation of the

term 'funds' is 'working capital'

Distinction Between funds Flow Statement and Balance Sheet

There is also a difference between meaning, purpose and importance of Funds Flow

Statement and Balance Sheet although both are prepared with the same accounting data.

3

A summary of main points of differences between these two is give below:-

a) Balance sheet is a statement showing the financial position of the concern on a particular

date. The asset side portrays the development of resources in various types of properties a

liabilities side indicates the manner in which these resources are obtained. It shows all

assets and liabilities whether current or fixed, tangible or intangible etc., while Funds

Flow Statement shows the changes in current assets an current liabilities during a

particular period of time.

b) Balance Sheet shows the total financial position on a particular date and in this way, it is

of a historical nature and therefore, its utility is very limited for the management. On the

other hand, Funds Flow Statement is a comparative statement of assets and liabilities and

depicts the changes in working capital during the period of two Balance sheets.

c) Funds Flow Statement is an analysis and control device for the management.

Management can ensure the long term on the short term solvency of the firm by studying

the internal funds flow cycles. It is a modern technique of knowing the inflows and

outflows of funds during a particular period. Balance Sheet represents the balance of

various assets and liabilities and does not present analysis of any kind.

d) There are two views of h financial position of the firm-long term a short-term. Short-

term financial position means the technical solvency of the firm in the near future while

on the other hand, long-term financial position means future financial structure of the

firm. Both are inter-relate but there is a differences in their analysis. The short-term view

of the financial position of the firm ca not is had from the Balance Sheet.

Distinction between funds flow statement and cash flow statement

We have fully explained the meaning and importance of both the statements-Funds Flow

a Cash Flow statements.

A distinction between these two statements may be briefed as under:-

(I) Funds Flow Statement am concerned with all items constituting funds (Working

4

Capital) for the business while Cash Flow Statement deals only with cash transactions. In

other words, a transaction affecting working capital other than cash will affect Funds

statement, and not the Cash Flow Statement.

(ii) In Funds Flow Statement, net increase or decrease in working capital is recorded

while in Cash Flow Statement; individual item involving cash is taken into account.

(iii) Funds Flow statement is started with the opening cash balance and closed with the

closing cash balance records only cash transactions.

(iv) Cash Flow Statement is started with the opening cash balance and closed with ht

closing cash balance while there a no opening or closing balances in Funds Flow

Statement.

A fund flow statement, better known as a cash flow statement, is an important document

in the accounting world. A fund flow statement shows a company's inflows and outflows of

funds. It is used to show investors, stakeholders or owners where the company's money came

from and where it went.

RULE

The flow of funds occurs when a transaction changes on one hand a non-current A/c and

on the other a current A/c and Vice-versa. According to working capital concept of funds the

term “Flow o Funds” return to movement of funds in working capital.

If any transaction results in increase in working capital.It is said to be a “source” or

“inflow of funds” and if it results in decrease of working capital, it is said to be “application” or

“out flow of funds”.

CURRENT ASSETS

Current Assets are those assets, which in the ordinary course of business can be or will be

converted into cash within a short period of normally one accounting year.

5

CURRENT LIABILITIES

Current liabilities are those liabilities which are intended to be paid in ordinary course of

business with in short period of normally one accounting year out of the current assets or the

income of the business.

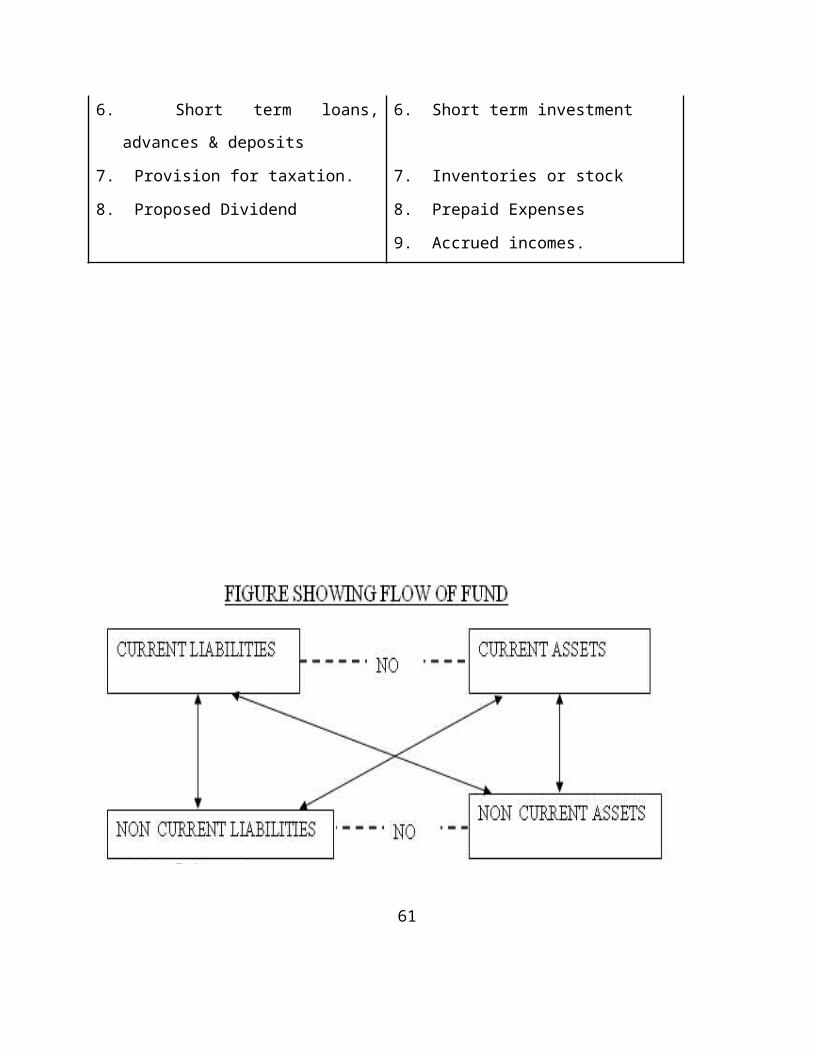

Differences between current liabilities & current assets

CURRENT LIABILITIES CURRENT ASSETS

1. Bills Payable 1. Cash in Hand

2. Sundry Creditors 2. Cash at Bank

3. Accrued or O/s Expenses 3. Bills Receivable

4. Dividends Payable 4. Sundry Debtors or A/c’s receivable

5. Bank Overdraft 5. Short term loans & advances

6. Short term loans, advances & deposits 6. Short term investment

7. Provision for taxation. 7. Inventories or stock

8. Proposed Dividend 8. Prepaid Expenses

9. Accrued incomes.

6

MEANING & DEFINITION OF FUNDS FLOW STATEMENT

Funds Flow Statement is a method by which we study changes in the financial position of

business enterprise beginning & ending financial statement dates. It is a statement showing

sources & uses of funds for a period of time.

FOUIKE DEFINES

“A statement of sources & application of funds is technical devices designed to analyses

the changes in the financial condition of business enterprise between two dates’

ANTHONY DEFINES

“The Funds Flow Statement describes the sources from which additional funds were

derived and the use to which these sources were put.

7

NEED AND IMPORTENCE OF STUDY

Many business owners disregard the importance of Funds flow statements because they

unwittingly believe that their current financial standing can be construed from other financial

reports and projections. Unfortunately, however, a Funds flow statement is necessary to

adequately assess the incoming and outgoing flow of Funds and other resources in a business.

Not only will a business owner with a Funds flow system be more aware of his or her

financial standing, but it will also help investors to make educated decisions on future

investments. A business with regular and reliable Funds flow statements shows more economic

solvency, and is more attractive to investors.

A Funds flow statement documents the incoming and outgoing Funds in plain terms.

Future sales and sales made for credit (unless they have been paid off) are not included in the

funds flow statement, and most of the data will come from core operations. Payables and

receivables should be expressly defined, as should depreciation of product value and inventory

that has not yet been moved.

This will allow a business owner to compare past periods with the current financial

standing and determine whether your receivables have increased or decreased.

This can also help to track your investments next to your receivables and payables. Are

your investments increasing or decreasing in value? And has your inventory moved at a steady

pace? New or expanding businesses can expect to see a decrease in Funds flow, but this doesn’t

mean that the business is going under. More stables businesses should see a steadily increase in

Funds flow over a period of several months or years.

There are typically five different sections in a Funds flow statement, though large

businesses might have more complex Funds flow systems as required.

Lesser consumption of cement for M-20 grade concrete and above

Faster DE shuttering of form work

Reduced construction time

Primo Concrete Cement - Concrete Redefined

Primo - The success story In 2008 Zuari Cement launched its high-strength cement under the 32

brand name 'Primo Concrete Cement' in Bangalore City. 'Primo' improves the density of the

concrete matrix and increases the durability of the concrete, making it an immediate hit

among construction and infrastructure projects undertaken in and around Bangalore. Recently

Primo was also launched in Kochi and Chennai. An extensive marketing and distribution

network across south India concretes Zuari Cement's success story.

New products, on the line of the extremely successful 'Primo' launch, will play a

significant role in key markets.

Primo Concrete Cement - Concrete Redefined

Primo concrete cement is high quality cement prepared from the finest raw material. Owing

to optimum water demand, it contributes to a very low co-efficient of permeability of the

concrete prepared. This improves the density of the concrete matrix and increases the durability

of the concrete. Primo is a high performance cement far exceeding the coal requirement of IS

12269-1987. It is this very durability that translates into long-lasting residential and commercial

constructions of a wide variety, such as dams, canals, highways, roads and flyovers.

Higher compressive strength

Better soundness

Lesser consumption of cement for M-20 Concrete grade

and above

Faster DE shuttering of form work

Reduced construction time

Italcementi GroupItalcementi Group at a glance

With an annual production capacity of approximately 70 million tons of cement,

Italcementi Group is the world’s fifth largest cement producer.

33

The Parent Company, Italcementi Spa., is one of Italy’s 10 largest industrial companies

and is included in FTSE/MIB Index of the Italian Stock Exchange.

Italcementi Group’s companies combine the expertise, knowhow and cultures of 22

countries in 4 Continents boasting an industrial network of 59 cement plants, 15 grinding centers,

5 terminals, 373 concrete batching units and 92 aggregates quarries.

In 2009 the Group had sales amounting to over 5 billion Euros.

Italcementi, founded in 1864, achieved important international status with the take-over

of Cements François in 1992

Following a period of re-organization and integration that culminates in the

adoption of a single corporate identity for all Group subsidiaries, the newly-born Italcementi

Group began to diversify geographically through a series of acquisitions in emerging countries

such as Bulgaria, Morocco, Kazakhstan, Thailand and India, as well as operating in North

America. As part of the plan to further enhance its presence in the Mediterranean area, in 2005

the Group boosted its investments in Egypt becoming the market leader

In 2006 Italcementi acquired full control of the activities in India and signed an

agreement to strengthen its position in Kazakhstan while, in 2007, it further strengthened its

presence in Asia and the Middle East through the operations in China, Kuwait, Saudi Arabia.

As a member of the World Business Council for Sustainable Development (WBCSD)

Italcementi Group has signed the Cement Sustainability Initiative’s Agenda for Action, the first

formal commitment that binds a number of world cement industry leaders to an action plan that

aims at satisfying present-day needs at the same time as safeguarding the requirements of future

generations.

To further confirm its commitment on these issues, the Group has taken over the co-

Chairmanship of the Cement Sustainability Initiative for the period 2011-2012. Moreover,

Italcementi has been included in “The Sustainability Yearbook 2012” the most comprehensive

publication on corporate sustainability released yearly by SAM (Sustainable Asset

Management).

34

FUNDS FLOW STATEMENT

INTRODUCTION

The basic financial statements i.e., the Balance Sheet and Profit & Loss A/c or Income

Statement of business reveals the net effect of various transactions on operational and financial

position of the company. The balance sheet gives a summary of the assets & liabilities of an

undertaking at a particular point of time.

There are many transactions that take place in an undertaking and which do not operate

Profit & Loss A/c. Thus another statement has to be prepared to show the change in Assets &

Liabilities from the end of one period of time to the end of another period of time. The statement

is called a statement of changes in financial position or a Funds Flow Statement.

The Funds Flow Statement is a statement which shown the movement of funds and is a

report of financial operations of business undertaking. In simple words it is a statement of

source and application of funds.

MEANING & CONCEPT OF FUNDS

The term “Fund” has been defined and interpreted differing by different experts. Broadly

the term fund refers to all the financial resource of the company on the other extreme fund has

been understood as cash only. The most acceptance meaning of the “fund” is “working capital”.

Working Capital is excess of current assents over current liability. The term fund has a

variety of meaning.

A) CASH FUND OR NARROW SENSE

In a narrow sense, funds mean only cash. ‘Cash flow statement portrays net effect of

various business transactions cash into account receipts & disbursement of cash.

35

The concept of preparing funds from statement is not accepted, as there are many such

transactions that do not affect cash but represent the flow of fund.

For Ex:

Purchase of furniture on credit does not affect cash but there is flow of fund.

B) CAPITAL FUND (or) BROADER SENSE

Here funds means all financial resources used in business, whether in the form of men,

money, material, machine & others.

C). NET WORKING CAPITAL (or) POPULAR SENSE

Networking capital means differences between current assets & liabilities. A fund

generally refers to cash or cash equipment or to working capital.

In any business we cannot under estimate the flow of funds from two operations. The

business runs with funds but the organization knows how to flow of funds.

The Funds Flow Statement is concerned with sources and applications of organization.

Statement of changes in working capital shows the increase or decrease in the working

capital.

“Funds from Operations” statement shows how much funds from operations.

Funds Flow Statement

In every concern, the funds flow in form different sources and similarly funds are

invested in various sources of investment. It is continuous process. The study and control of this

funds-flow process (i.e., the uses and sources of funds) is the main objective of financial

management to assess the soundness and the solvency of the enterprise.

36

The funds-flow-statement is a report on financial operations changes, flow or

movements during the period. It is a statement which shows the sources an application of funds

or it shows how the activities of a business are financed in a particulate period. In other words,

such a statement shows how the financial resources have been used during a particular period of

time. It is, thus, a historical statement showing sources and application of funds between the two

dates designed especially to analyses the changes in the financial conditions of an enterprise. In

the words of Fouke, it is-

“A statement of Sources and Application of Funds is a technical device designed to analyses

the changes in the financial condition of business enterprises between two dates.”

Funds Flow Statement is not an income statement. Income statement shows the items of

income and expenditure of a particular period, but the Funds flow statement is an operating

statement as it summaries the financial activities for a period of time. It covers all movements

that involve an actual exchange of assets.

Various titles are used for this statement such as 'Statement of sources and Application of

Funds', 'Summary of Financial operations,' 'Changes in Financial Position', 'Fund received and

Disbursed', 'Funds Generated and Expended', Changes in Working Capital”, “Statement of Fund'

etc. Title of Funds Flow Statement has been modified from time to time. Really it is very

difficult to find a short time for such statement which carries much to the readers regarding its

contents and functions.

A new interpretation of the term 'funds, has now been adopted as to include assets or

financial resourceful which do not flow through the working capital accounts. It seems to be the

most suitable meaning fort the term 'funds' but the most commonly used interpretation of the

term 'funds' is 'working capital'

Distinction Between funds Flow Statement and Balance Sheet

There is also a difference between meaning, purpose and importance of Funds Flow

Statement and Balance Sheet although both are prepared with the same accounting data.

37

A summary of main points of differences between these two is give below:-

e) Balance sheet is a statement showing the financial position of the concern on a particular

date. The asset side portrays the development of resources in various types of properties a

liabilities side indicates the manner in which these resources are obtained. It shows all

assets and liabilities whether current or fixed, tangible or intangible etc., while Funds

Flow Statement shows the changes in current assets an current liabilities during a

particular period of time.

f) Balance Sheet shows the total financial position on a particular date and in this way, it is

of a historical nature and therefore, its utility is very limited for the management. On the

other hand, Funds Flow Statement is a comparative statement of assets and liabilities and

depicts the changes in working capital during the period of two Balance sheets.

g) Funds Flow Statement is an analysis and control device for the management.

Management can ensure the long term on the short term solvency of the firm by studying

the internal funds flow cycles. It is a modern technique of knowing the inflows and

outflows of funds during a particular period. Balance Sheet represents the balance of

various assets and liabilities and does not present analysis of any kind.

h) There are two views of h financial position of the firm-long term a short-term. Short-

term financial position means the technical solvency of the firm in the near future while

on the other hand, long-term financial position means future financial structure of the

firm. Both are inter-relate but there is a differences in their analysis. The short-term view

of the financial position of the firm ca not is had from the Balance Sheet.

Distinction between funds flow statement and cash flow statement

We have fully explained the meaning and importance of both the statements-Funds Flow

a Cash Flow statements.

A distinction between these two statements may be briefed as under:-

(I) Funds Flow Statement am concerned with all items constituting funds (Working

38

Capital) for the business while Cash Flow Statement deals only with cash transactions. In

other words, a transaction affecting working capital other than cash will affect Funds

statement, and not the Cash Flow Statement.

(ii) In Funds Flow Statement, net increase or decrease in working capital is recorded

while in Cash Flow Statement; individual item involving cash is taken into account.

(iii) Funds Flow statement is started with the opening cash balance and closed with the

closing cash balance records only cash transactions.

(iv) Cash Flow Statement is started with the opening cash balance and closed with ht

closing cash balance while there a no opening or closing balances in Funds Flow

Statement.

A fund flow statement, better known as a cash flow statement, is an important document

in the accounting world. A fund flow statement shows a company's inflows and outflows of

funds. It is used to show investors, stakeholders or owners where the company's money came

from and where it went.

RULE

The flow of funds occurs when a transaction changes on one hand a non-current A/c and

on the other a current A/c and Vice-versa. According to working capital concept of funds the

term “Flow o Funds” return to movement of funds in working capital.

If any transaction results in increase in working capital.It is said to be a “source” or

“inflow of funds” and if it results in decrease of working capital, it is said to be “application” or

“out flow of funds”.

CURRENT ASSETS

Current Assets are those assets, which in the ordinary course of business can be or will be

converted into cash within a short period of normally one accounting year.

39

CURRENT LIABILITIES

Current liabilities are those liabilities which are intended to be paid in ordinary course of

business with in short period of normally one accounting year out of the current assets or the

income of the business.

Differences between current liabilities & current assets

CURRENT LIABILITIES CURRENT ASSETS

1. Bills Payable 1. Cash in Hand

2. Sundry Creditors 2. Cash at Bank

3. Accrued or O/s Expenses 3. Bills Receivable

4. Dividends Payable 4. Sundry Debtors or A/c’s receivable

5. Bank Overdraft 5. Short term loans & advances

6. Short term loans, advances & deposits 6. Short term investment

7. Provision for taxation. 7. Inventories or stock

8. Proposed Dividend 8. Prepaid Expenses

9. Accrued incomes.

40

MEANING & DEFINITION OF FUNDS FLOW STATEMENT

Funds Flow Statement is a method by which we study changes in the financial position of

business enterprise beginning & ending financial statement dates. It is a statement showing

sources & uses of funds for a period of time.

FOUIKE DEFINES

“A statement of sources & application of funds is technical devices designed to analyses

the changes in the financial condition of business enterprise between two dates’

ANTHONY DEFINES

“The Funds Flow Statement describes the sources from which additional funds were

derived and the use to which these sources were put.

41

I.C.W.A IN GLOSSARY OF MANAGEMENT ACCOUNTING

TERMS DEFINES FUNDS FLOW STATEMENT

Funds Flow Statement as “a statement either prospective or retrospective setting out of

sources & application of the funds of an enterprise.

The purpose of statement is to indicate clearly the requirement of funds and how they are

proposed to be raised and efficient utilization & application of the same.

Funds Flow statement is called by various names such as sources and application of

funds, statement of changes in financial position, sources and uses of funds, summary of

financial operations, movement of working capital, movement of funds statement,

sources of increase and application of decrease etc…

USES, SIGNIFICANCE AND IMPORTANCE OF FUNDS FLOW STATEMENT

A Funds Flow Statement is an essential tool for the financial analysis and is of primary

importance to financial management. Now a day it is being widening used by the financial

analysis.

The basic purpose of funds flow statement is to reveal the changes in working capital on

2 balance sheets

42

DIFFERENCE BETWEEN FUNDS FLOW STATEMENT & CASH FLOW

STATEMENT

BASIS OF DIFFERENCE FUNDS FLOW STATEMENT CASH FLOW STATEMENT

1.Basis of concept It is based on a wider concept

Of funds, i.e., working capital.

It is based on a narrower concept of

funds, i.e., cash.

2. Basis of Accounting It is based on accrual basis of

accounting

It is based on cash basis of

accounting.

3. Schedule of changes in

working capital

Schedule of changes in working

capital is prepared to show the

changes in current assets and

Current liabilities.

No such Schedule of changes in

working

Capital is prepared.

4. Method of preparing Funds flow statement reveals

the sources and applications of

Funds. The net difference between

sources and applications of funds

represent net increase or decrease

In working capital.

It is prepared by classifying all

Cash inflows and outflows in terms of

operating, investing and financing

activities. The net difference

represents the net Increase or decrease

in Cash and cash equivalents.

A5. Basis of usefulness. It is useful in planning

intermediate and long term

Financing.

It is more useful for short-term

analysis and cash planning of the

business.

43

LIMITATIONS OF FUNDS FLOW STATEMENT

The funds flow statement has a number of uses; however, it has certain limitations also, which

are listed below.

1. It should be remembered that a funds flow statement is not a substitute of an income

statement or a balance sheet. It provides only some additions information as regards charges

in working capital.

2. Cannot reveal continuous changes.

3. It is not an original statement but simply is arrangement of data given in financial

statements.

44

4. It is essentially historic in nature and projected funds flow statement cannot be prepared with

much accuracy.

5. Change in cash is more important & relevant for financial management than the working

capital.

PROCEDURE FOR PREPARING A FUNDS FLOW STATEMENT

Funds flow Statement is a method by which we study changes in financial position of business

enterprise between beginning & ending financial statement dates. Hence the funds flow

statement is prepared by comparing two balance sheets and any of such other information

derived from the Accounts as may be needed

The preparation of funds flow statement consists of two parts.

A. Statement or schedule of changes in working capital.

B. Statement of sources & application of fund.

A.) STATEMENT OR SCHEDULE OF CHANGES IN W.C.

Working Capital means the excess of current assets over current liabilities.

Statement of changes in working capital is prepared to show the changes in

working capital between two balance sheet dates.

This statement is prepared with help of current assets and current liabilities

derived from two balance sheets.

Working capital = Current Assets – Current Liabilities

An increase in current assets increases W.C.

A decrease in current assets decreases W.C.

An increase in current liabilities decreased W.C.

A decrease in current liabilities increases W.C.

45

STATEMENT OF SCHEDULE OF CHANGES IN WORKING CAPITAL

ParticularsPrevious Year

Current Year

Effect of W.C.

IncreaseDecrease

Current Assets :Cash in Hand Xx Xx xxCash at Bank Xx Xx xxBills Receivable Xx Xx XxSundry Debtors Xx Xx XxTemporary investments Xx Xx xxStock / Inventions Xx Xx xxPrepaid Expenses Xx Xx xxAccrued Incomes Xx Xx XxTotal Current Assets Xxx XxxCurrent Liabilities :Bills Payable Xx xx xxSundry Creditors Xx xx XxOutstanding Expenses Xx xx XxBank Overdraft Xx xx xxShort term Advances Xx xx xxDividend Payable Xx xx XxProposed Dividend Xx xx XxProvision for Taxation Xx xx XxTotal Current Liabilities Xxx xxxWorking Capital (C.A. – C.L.) Xxx xxx

Net increase or decrease in W.C

Xxx Xxx

Xxxx xxxx xxxx Xxxx

46

STATEMENT OF SOURCES & APPLICATION OF FUNDS. :

Funds flow statement is a statement, which indicates various sources from which funds (W.C.)

have been obtained during a certain period and uses or applications to which these funds have

been put during that period.

Generally this statement is prepared in two formats.

a) T Form (or) An A/c Form (or) Self Balancing Type

b) Report Form.

a.) T FORMS AN ACCOUNT FORM

FUNDS FLOW STATEMENT

(For the year ended)

Sources Rs. Applications Rs.

Funds from operations Xx Funds lost in operations Xx

Issue of share capital Xx Redemption of preference share Xx

Issue of Debentures Xx Capital Xx

Raising of long term loans Xx Redemption of debentures Xx

Sale of non current (fixed)

assets

XxRepayment of long term loan

Xx

Non-trading receipts such as

dividends

Xx Purchase of long term

investments

Xx

Scale of long term investments Xx Non-trading payments Xx

Net decrease in working capital Xx Payment of Dividends Xx

47

Xx Payment of Tax Xx

Xx Net increase in working capital Xx

Xxx Xxx

REPORT FORM OF FUNDS FLOW STATEMENT

SOURCES OF FUNDS

Funds from Operation Xx

Issue of Share Capital Xx

Raising of long term loans Xx

Receipts from partly paid shares Xx

Sale of non-current (fixed) assets Xx

Non trading receipts, such as dividends Xx

Sale of investment (long term) Xx

Decrease in working capital Xx

Total Xxx

APPLICATION OR USES OF FUNDS :

Funds lost in operations Xx

Redemption of preference share capital Xx

Redemption of debentures Xx

Repayment of long term loans Xx

Purchase of non-current (fixed) assets Xx

Purchase of long term investments Xx

Non-trading payment Xx

Payment of dividends Xx

Payment of tax Xx

48

Increase in working capital Xx

Total Xxx

There are two methods of calculating funds from operation.

a. Funds from operation.

b. Adjusted Profit & Loss A/c

FUNDS FROM OPERATION

Closing Balance of Profit & Loss A/c Xxx

Add: Non-fund or Non-operating items Depreciation Xx

Loss on sale of fixed assets Xx

Under Writing Commission Xx

Discount on issue of shares & debentures Xx

Preliminary exp. Written off Xx

Deferred revenue expenses Xx

Goodwill Written off Xx

Patent or trade mark Xx

Provision for taxes Xx

Proposed Dividend Xx

Transfer to resume Xx

Provision for doubtful debts. Xx

Less: Non-operating Income Xx

Profit / Gain on sale of fixed assets Xx

Dividend Received Xx

Dividend Received Xx

Interest Received on Investments Xx

Profit on revaluation of assets Xx

49

Fund from operations Xxx

FUNDS FLOW STATEMENT IN ZUARI CEMENT INDUSTRIES LTD