6

IGI|Life Funds Performance Report October 2017

IGI|Life

Funds Performance ReportOctober 2017

IGI Life Insurance Limited

July 2015

Source: SBP, PBS, Bloomberg

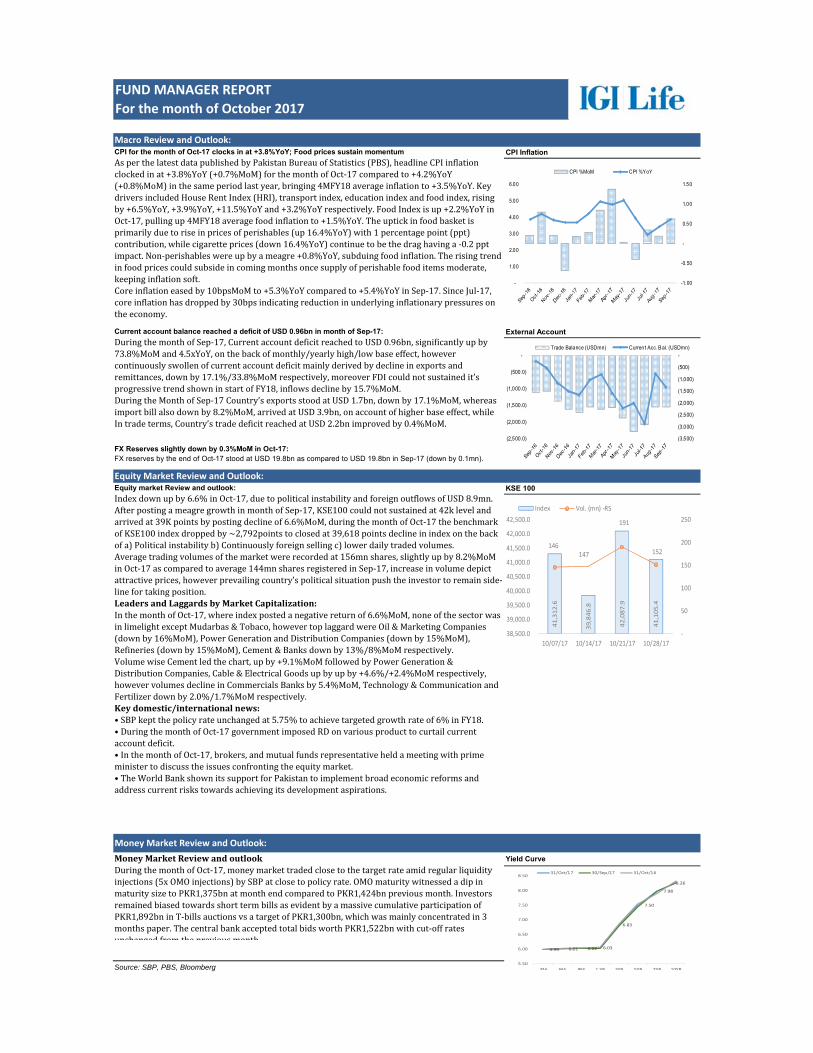

Equity Market Review and Outlook:

FUND MANAGER REPORT

For the month of October 2017

Macro Review and Outlook:CPI InflationCPI for the month of Oct-17 clocks in at +3.8%YoY; Food prices sustain momentum

AsperthelatestdatapublishedbyPakistanBureauofStatistics(PBS),headlineCPIinflationclockedinat+3.8%YoY(+0.7%MoM)forthemonthofOct‐17comparedto+4.2%YoY(+0.8%MoM)inthesameperiodlastyear,bringing4MFY18averageinflationto+3.5%YoY.KeydriversincludedHouseRentIndex(HRI),transportindex,educationindexandfoodindex,risingby+6.5%YoY,+3.9%YoY,+11.5%YoYand+3.2%YoYrespectively.FoodIndexisup+2.2%YoYinOct‐17,pullingup4MFY18averagefoodinflationto+1.5%YoY.Theuptickinfoodbasketisprimarilyduetoriseinpricesofperishables(up16.4%YoY)with1percentagepoint(ppt)contribution,whilecigaretteprices(down16.4%YoY)continuetobethedraghavinga‐0.2pptimpact.Non‐perishableswereupbyameagre+0.8%YoY,subduingfoodinflation.Therisingtrendinfoodpricescouldsubsideincomingmonthsoncesupplyofperishablefooditemsmoderate,keepinginflationsoft.Coreinflationeasedby10bpsMoMto+5.3%YoYcomparedto+5.4%YoYinSep‐17.SinceJul‐17,coreinflationhasdroppedby30bpsindicatingreductioninunderlyinginflationarypressuresontheeconomy.

External AccountCurrent account balance reached a deficit of USD 0.96bn in month of Sep-17:

DuringthemonthofSep‐17,CurrentaccountdeficitreachedtoUSD0.96bn,significantlyupby73.8%MoMand4.5xYoY,onthebackofmonthly/yearlyhigh/lowbaseeffect,howevercontinuouslyswollenofcurrentaccountdeficitmainlyderivedbydeclineinexportsandremittances,downby17.1%/33.8%MoMrespectively,moreoverFDIcouldnotsustainedit’sprogressivetrendshowninstartofFY18,inflowsdeclineby15.7%MoM.DuringtheMonthofSep‐17Country’sexportsstoodatUSD1.7bn,downby17.1%MoM,whereasimportbillalsodownby8.2%MoM,arrivedatUSD3.9bn,onaccountofhigherbaseeffect,whileIntradeterms,Country’stradedeficitreachedatUSD2.2bnimprovedby0.4%MoM.

FX Reserves slightly down by 0.3%MoM in Oct-17: FX reserves by the end of Oct-17 stood at USD 19.8bn as compared to USD 19.8bn in Sep-17 (down by 0.1mn).

Equity market Review and outlook:

Indexdownupby6.6%inOct‐17,duetopoliticalinstabilityandforeignoutflowsofUSD8.9mn.AfterpostingameagregrowthinmonthofSep‐17,KSE100couldnotsustainedat42klevelandarrivedat39Kpointsbypostingdeclineof6.6%MoM,duringthemonthofOct‐17thebenchmarkofKSE100indexdroppedby~2,792pointstoclosedat39,618pointsdeclineinindexonthebackofa)Politicalinstabilityb)Continuouslyforeignsellingc)lowerdailytradedvolumes.Averagetradingvolumesofthemarketwererecordedat156mnshares,slightlyupby8.2%MoMinOct‐17ascomparedtoaverage144mnsharesregisteredinSep‐17,increaseinvolumedepictattractiveprices,howeverprevailingcountry’spoliticalsituationpushtheinvestortoremainside‐linefortakingposition.LeadersandLaggardsbyMarketCapitalization:InthemonthofOct‐17,whereindexpostedanegativereturnof6.6%MoM,noneofthesectorwasinlimelightexceptMudarbas&Tobaco,howevertoplaggardwereOil&MarketingCompanies(downby16%MoM),PowerGenerationandDistributionCompanies(downby15%MoM),Refineries(downby15%MoM),Cement&Banksdownby13%/8%MoMrespectively.VolumewiseCementledthechart,upby+9.1%MoMfollowedbyPowerGeneration&DistributionCompanies,Cable&ElectricalGoodsupbyupby+4.6%/+2.4%MoMrespectively,howevervolumesdeclineinCommercialsBanksby5.4%MoM,Technology&CommunicationandFertilizerdownby2.0%/1.7%MoMrespectively.Keydomestic/internationalnews:•SBPkeptthepolicyrateunchangedat5.75%toachievetargetedgrowthrateof6%inFY18.•DuringthemonthofOct‐17governmentimposedRDonvariousproducttocurtailcurrentaccountdeficit.•InthemonthofOct‐17,brokers,andmutualfundsrepresentativeheldameetingwithprimeministertodiscusstheissuesconfrontingtheequitymarket.•TheWorldBankshownitssupportforPakistantoimplementbroadeconomicreformsandaddresscurrentriskstowardsachievingitsdevelopmentaspirations.

KSE 100

Money Market Review and Outlook:

Yield CurveMoneyMarketReviewandoutlookDuringthemonthofOct‐17,moneymarkettradedclosetothetargetrateamidregularliquidityinjections(5xOMOinjections)bySBPatclosetopolicyrate.OMOmaturitywitnessedadipinmaturitysizetoPKR1,375bnatmonthendcomparedtoPKR1,424bnpreviousmonth.InvestorsremainedbiasedtowardsshorttermbillsasevidentbyamassivecumulativeparticipationofPKR1,892bninT‐billsauctionsvsatargetofPKR1,300bn,whichwasmainlyconcentratedin3monthspaper.ThecentralbankacceptedtotalbidsworthPKR1,522bnwithcut‐offratesunchanged from the previous month

41,312.6

39,846.8

42,087.9

41,105.4

146 147

191

152

‐

50

100

150

200

250

38,500.0

39,000.0

39,500.0

40,000.0

40,500.0

41,000.0

41,500.0

42,000.0

42,500.0

10/07/17 10/14/17 10/21/17 10/28/17

Index Vol. (mn) ‐RS

(3,500)

(3,000)

(2,500)

(2,000)

(1,500)

(1,000)

(500)

-

(2,500.0)

(2,000.0)

(1,500.0)

(1,000.0)

(500.0)

-Trade Balance (USDmn) Current Acc. Bal. (USDmn)

-1.00

-0.50

-

0.50

1.00

1.50

-

1.00

2.00

3.00

4.00

5.00

6.00

CPI %MoM CPI %YoY

5.99 6.01 6.02 6.03

6.83

7.50

7.98

8.26

5.50

6.00

6.50

7.00

7.50

8.00

8.50

3M 6M 9M 1 YR 3YR 5YR 7YR 10YR

31/Oct/17 30/Sep/17 31/Oct/16

Strategy

Risk Profile

Pricing Mechanism

Pricing Days

Management Fee

Launch Date

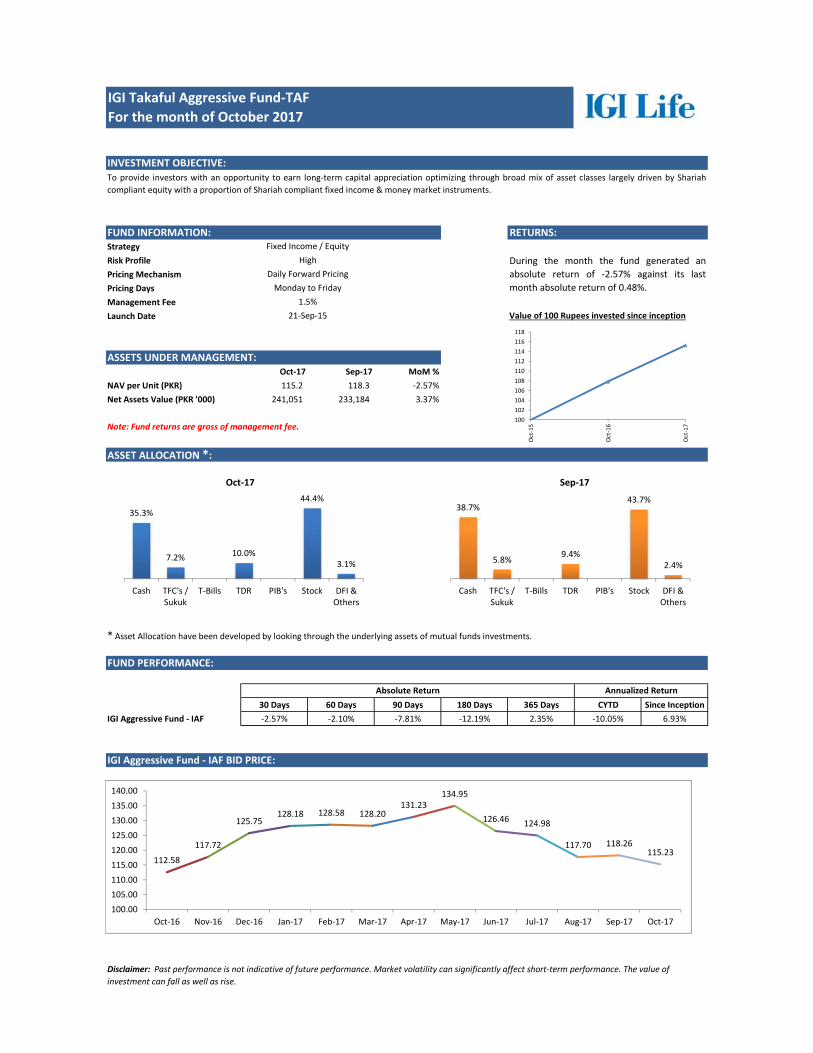

Oct‐17 Sep‐17 MoM %

NAV per Unit (PKR) 115.2 118.3 ‐2.57%

Net Assets Value (PKR '000) 241,051 233,184 3.37%

* Asset Allocation have been developed by looking through the underlying assets of mutual funds investments.

30 Days 60 Days 90 Days 180 Days 365 Days CYTD Since Inception

IGI Aggressive Fund ‐ IAF ‐2.57% ‐2.10% ‐7.81% ‐12.19% 2.35% ‐10.05% 6.93%

21‐Sep‐15 Value of 100 Rupees invested since inception

IGI Takaful Aggressive Fund‐TAF

For the month of October 2017

INVESTMENT OBJECTIVE:To provide investors with an opportunity to earn long‐term capital appreciation optimizing through broad mix of asset classes largely driven by Shariah

compliant equity with a proportion of Shariah compliant fixed income & money market instruments.

FUND INFORMATION: RETURNS:Fixed Income / Equity

High During the month the fund generated an

absolute return of ‐2.57% against its last

month absolute return of 0.48%.

Daily Forward Pricing

Monday to Friday

1.5%

Absolute Return Annualized Return

IGI Aggressive Fund ‐ IAF BID PRICE:

Disclaimer: Past performance is not indicative of future performance. Market volatility can significantly affect short‐term performance. The value of

investment can fall as well as rise.

ASSETS UNDER MANAGEMENT:

Note: Fund returns are gross of management fee.

ASSET ALLOCATION *:

Oct‐17 Sep‐17

FUND PERFORMANCE:

112.58

117.72

125.75128.18 128.58 128.20

131.23134.95

126.46 124.98

117.70 118.26115.23

100.00

105.00

110.00

115.00

120.00

125.00

130.00

135.00

140.00

Oct‐16 Nov‐16 Dec‐16 Jan‐17 Feb‐17 Mar‐17 Apr‐17 May‐17 Jun‐17 Jul‐17 Aug‐17 Sep‐17 Oct‐17

38.7%

5.8%9.4%

43.7%

2.4%

Cash TFC's /Sukuk

T‐Bills TDR PIB's Stock DFI &Others

35.3%

7.2% 10.0%

44.4%

3.1%

Cash TFC's /Sukuk

T‐Bills TDR PIB's Stock DFI &Others

100

102

104

106

108

110

112

114

116

118

Oct‐15

Oct‐16

Oct‐17

Strategy

Risk Profile

Pricing Mechanism

Pricing Days

Management Fee

Launch Date

Oct‐17 Sep‐17 MoM %

NAV per Unit (PKR) 111.9 113.4 ‐1.29%

Net Assets Value (PKR '000) 550,704 523,779 5.14%

* Asset Allocation have been developed by looking through the underlying assets of mutual funds investments.

30 Days 60 Days 90 Days 180 Days 365 Days CYTD Since Inception

IGI Balanced Fund ‐ IBF ‐1.29% ‐0.85% ‐4.70% ‐7.02% 3.09% ‐4.97% 5.48%

21‐Sep‐15 Value of 100 Rupees invested since inception

IGI Takaful Balanced Fund‐TBF

For the month of October 2017

INVESTMENT OBJECTIVE:The investment objective of the Fund is to earn competitive long term return by investing in mix of Shariah compliant equity, fixed income and money

market instruments. This fund is suited for investors with moderate risk tolerance.

FUND INFORMATION: RETURNS:Fixed Income / Equity

Moderate During the month the fund generated an

absolute return of ‐1.29% against its last

month absolute return of 0.44%.

Daily Forward Pricing

Monday to Friday

1.5%

Absolute Return Annualized Return

IGI Balanced Fund ‐ IBF BID PRICE:

Disclaimer: Past performance is not indicative of future performance. Market volatility can significantly affect short‐term performance. The value of

investment can fall as well as rise.

ASSETS UNDER MANAGEMENT:

Note: Fund returns are gross of management fee.

ASSET ALLOCATION *:

Oct‐17 Sep‐17

FUND PERFORMANCE:

49.4%

9.4%14.0%

24.1%

3.1%

Cash TFC's /Sukuk

T‐Bills TDR PIB's Stock DFI &Others

47.8%

10.9% 14.1%

24.0%

3.3%

Cash TFC's /Sukuk

T‐Bills TDR PIB's Stock DFI &Others

100

102

104

106

108

110

112

114

Oct‐15

Oct‐16

Oct‐17

108.59

112.04

116.78118.22 118.49 118.46

120.39122.68

118.22 117.47

112.91 113.41111.95

100.00

105.00

110.00

115.00

120.00

125.00

Oct‐16 Nov‐16 Dec‐16 Jan‐17 Feb‐17 Mar‐17 Apr‐17 May‐17 Jun‐17 Jul‐17 Aug‐17 Sep‐17 Oct‐17

Strategy

Risk Profile

Pricing Mechanism

Pricing Days

Management Fee

Launch Date

Oct‐17 Sep‐17 MoM %

NAV per Unit (PKR) 107.4 107.3 0.03%

Net Assets Value (PKR '000) 38,508 35,883 7.31%

* Asset Allocation have been developed by looking through the underlying assets of mutual funds investments.

30 Days 60 Days 90 Days 180 Days 365 Days CYTD Since Inception

IGI Conservative Fund ‐ ICF 0.03% 0.47% ‐0.54% ‐0.40% 1.76% 1.32% 3.41%

21‐Sep‐15 Value of 100 Rupees invested since inception

IGI Takaful Conservative Fund ‐ TCF

For the month of October 2017

INVESTMENT OBJECTIVE:To provide stable and competitive returns in line with the money markets exhibiting low volatility consistent with capital preservation by constructing a

liquid portfolio of low risk short term Shariah compliant investments yielding competitive returns.

FUND INFORMATION: RETURNS:Fixed Income

Low During the month the fund generated an

absolute return of 0.03% against its last month

absolute return of 0.44%.

Daily Forward Pricing

Monday to Friday

1.5%

Absolute Return Annualized Return

IGI Conservative Fund ‐ ICF BID PRICE:

Disclaimer: Past performance is not indicative of future performance. Market volatility can significantly affect short‐term performance. The value of

investment can fall as well as rise.

ASSETS UNDER MANAGEMENT:

Note: Fund returns are gross of management fee.

ASSET ALLOCATION *:

Oct‐17 Sep‐17

FUND PERFORMANCE:

56.3%

14.4%21.1%

4.2% 4.0%

Cash TFC's /Sukuk

T‐Bills TDR PIB's Stock DFI &Others

55.2%

16.6%20.6%

3.8% 3.8%

Cash TFC's /Sukuk

T‐Bills TDR PIB's Stock DFI &Others

100

101

102

103

104

105

106

107

108

Oct‐15

Oct‐16

Oct‐17

105.51105.86

106.19106.65 106.66

107.04

107.80

108.50

107.86 107.95

106.86107.33 107.36

104.00

105.00

106.00

107.00

108.00

109.00

Oct‐16 Nov‐16 Dec‐16 Jan‐17 Feb‐17 Mar‐17 Apr‐17 May‐17 Jun‐17 Jul‐17 Aug‐17 Sep‐17 Oct‐17