We are delighted to release this white paper "Future cities: the choices that we make today" as knowledge partner for the 7th International Conference on Real Estate organised by the Confederation of Indian Industry (CII) here in New Delhi.

The white paper is second in the series of collaboration between Grant Thornton India and CII that began in 2009-10. It strives to map industry opinions and interpretation of the established urban governance practices in India.

The white paper is based on an online and interview-based survey, and presents a mix of quantitative and qualitative analysis.

Key highlights

• efficient urban planning and governance the key to sustain growth momentum

• collaboration between and within the public and private sectors an imperative

• marriage of the infrastructure and real estate sectors to ensure planned development

• new formats such as hospotels and low cost budget housing to be introduced

The year 2011 ushered a new decade of opportunities for the Indian real estate sector. After one and a half years of gradual consolidation, real estate in India has covered its own comfortable ground, and is positioned at the right threshold to take a quantum leap in years to come.

Though, during the downturn, the Indian real estate sector was significantly affected. With the help of cumulative Gross Domestic Product (GDP) growth and a rebounding economy, Indian real estate has been able to stand again and has emerged at one of the topmost positions in real estate sector in Asia, after China.

According to the data released by the Department of Industrial Policy and Promotion (DIPP), housing and real estate sector including cineplex, multiplex, integrated townships and commercial complexes etc, attracted a cumulative foreign direct investment (FDI) worth US$9,405 million from April 2000 to January 2011 wherein the sector witnessed FDIamounting to US$1,048 million during April-January 2010-11.

Focus has especially been on the various metros like Delhi and NCR, Mumbai & Kolkata for developing projects ranging from residential, retail to commercial complexes. As per the report of the Technical Group on Estimation of Housing Shortage, an estimated shortage of 26.53 million houses during the Eleventh Five Year Plan (2007-12) provides a big investment opportunity for private players.

Complimenting the huge potential available in the sector, the favorable policies of the Indian government have also been one of the major contributors to accommodate and accelerate private investments in the infrastructure sector. These include sector specific policies, providing incentives and tax holidays to attract private investments, permission of 100% FDI in the infrastructure sector, special provision of Viability Gap Funding (VGF) and Public Private Participation (PPP) approach.

Vijay K ThadaniChairman, CII – Northern RegionCEO, NIIT Ltd

Vishesh ChandiokNational Managing PartnerGrant Thornton India

To enable the stakeholders to have a clear perspective of the macro environment surrounding this sector, a survey was conducted by our Knowledge Partner – Grant Thornton India. The results of the survey are included in this white paper, which also presents broad themes for discussion in this Conference - planning, governance, finance and infrastructure including technology and green initiatives.

CII has been actively engaged with the real estate sector addressing their key issues relating to policy matter and developing a roadmap to leverage the growth potential of this sector. To build further impetus for the sector, CII organises various focused interactions, seminars, conferences and expositions to provide an ideal platform for deliberations, and showcase business outlook for various stakeholders. 7th International Conference on Real Estate: Realty 2011 is another step forward in this direction.

We convey our sincere thanks to all the respondents associated with the survey for their tremendous support and valuable inputs. We hope that you would find this white paper insightful and enriching.

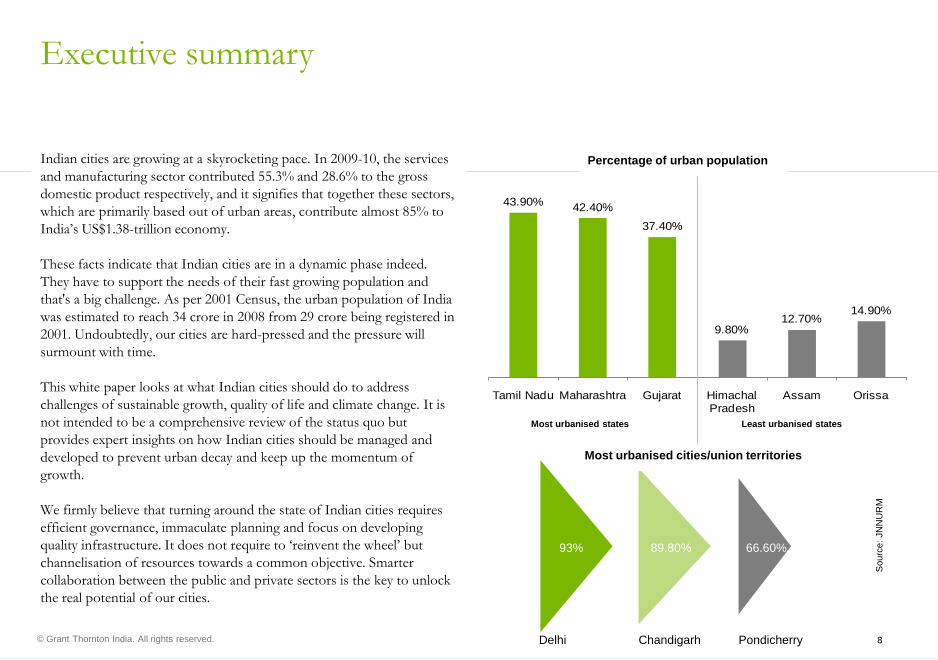

Indian cities are growing at a skyrocketing pace. In 2009-10, the services and manufacturing sector contributed 55.3% and 28.6% to the gross domestic product respectively, and it signifies that together these sectors, which are primarily based out of urban areas, contribute almost 85% to India’s US$1.38-trillion economy.

These facts indicate that Indian cities are in a dynamic phase indeed. They have to support the needs of their fast growing population and that's a big challenge. As per 2001 Census, the urban population of India was estimated to reach 34 crore in 2008 from 29 crore being registered in 2001. Undoubtedly, our cities are hard-pressed and the pressure will surmount with time.

This white paper looks at what Indian cities should do to address challenges of sustainable growth, quality of life and climate change. It is not intended to be a comprehensive review of the status quo but provides expert insights on how Indian cities should be managed and developed to prevent urban decay and keep up the momentum of growth.

We firmly believe that turning around the state of Indian cities requires efficient governance, immaculate planning and focus on developing quality infrastructure. It does not require to ‘reinvent the wheel’ but channelisation of resources towards a common objective. Smarter collaboration between the public and private sectors is the key to unlock the real potential of our cities.

While the government is expected to act as an enabler –rationalising policies, promoting corporate-style city governance and curbing corruption, the private sector should take charge of developing cities in their own right.

Collaboration within the sectors ought to be promoted. By far, the core sectors of infrastructure and real estate in India have grown in a disjointed way, which is identical to other countries, which have experienced a dynamic phase of high growth.

However, to advance it to the next stage, defragmentation of resources spread across industries is more of a necessity than choice.

Five key aspects that are critical for ensuring brighter future of the Indian real estate sector and Indian cities at large:

• planning• governance• infrastructure• finance • green technology

The degree of collaboration between infrastructure and real estate sectors will define the future course.

A snapshot:A snapshot: i f d linfrastructure and real estate

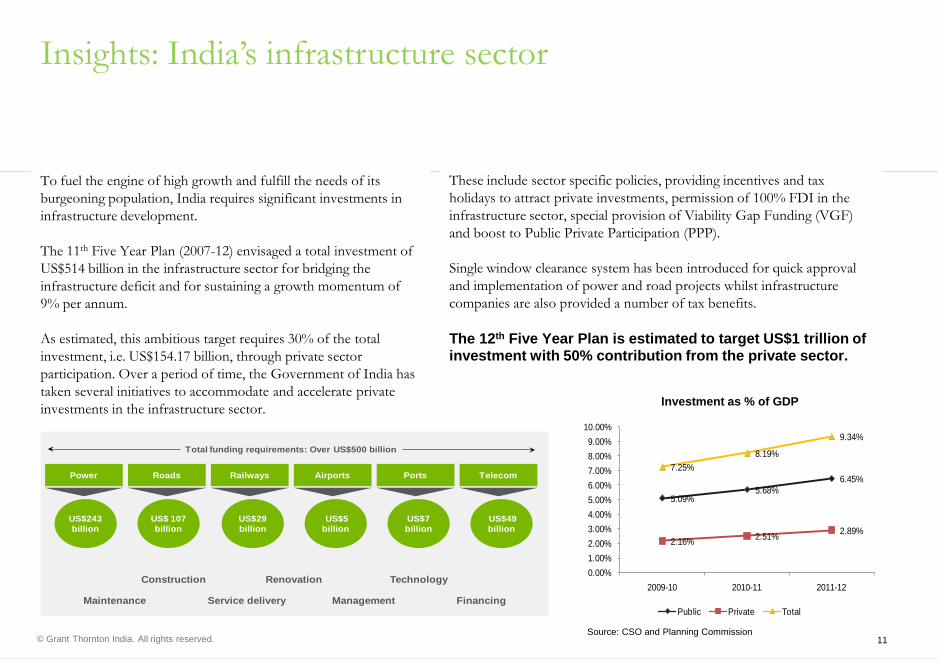

To fuel the engine of high growth and fulfill the needs of its burgeoning population, India requires significant investments in infrastructure development.

The 11th Five Year Plan (2007-12) envisaged a total investment of US$514 billion in the infrastructure sector for bridging the infrastructure deficit and for sustaining a growth momentum of 9% per annum.

As estimated, this ambitious target requires 30% of the total investment, i.e. US$154.17 billion, through private sector participation. Over a period of time, the Government of India has taken several initiatives to accommodate and accelerate private investments in the infrastructure sector.

These include sector specific policies, providing incentives and tax holidays to attract private investments, permission of 100% FDI in the infrastructure sector, special provision of Viability Gap Funding (VGF) and boost to Public Private Participation (PPP).

Single window clearance system has been introduced for quick approval and implementation of power and road projects whilst infrastructure companies are also provided a number of tax benefits.

The 12th Five Year Plan is estimated to target US$1 trillion of investment with 50% contribution from the private sector.

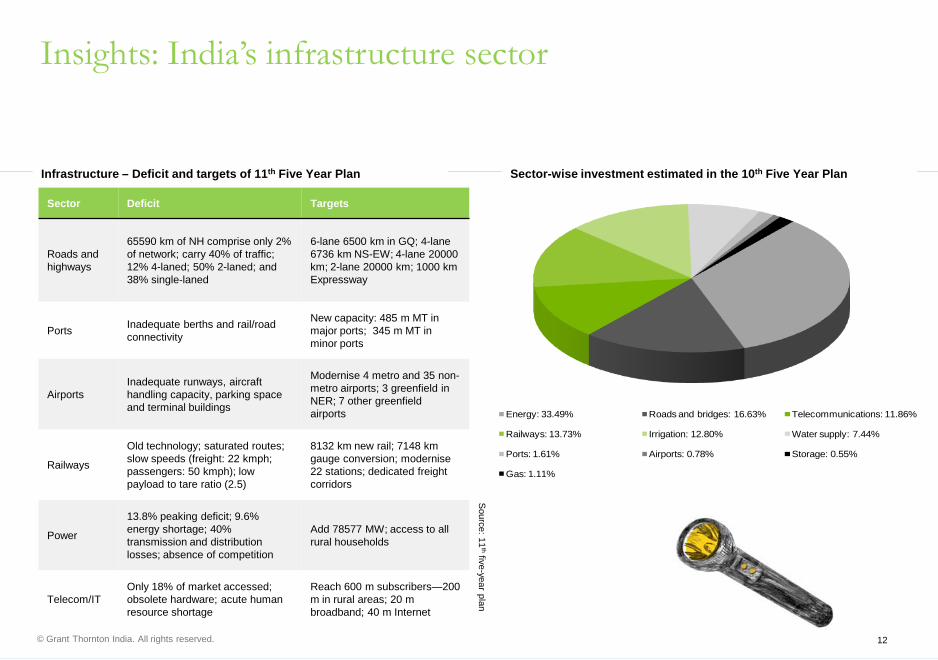

65590 km of NH comprise only 2% of network; carry 40% of traffic; 12% 4-laned; 50% 2-laned; and 38% single-laned

6-lane 6500 km in GQ; 4-lane 6736 km NS-EW; 4-lane 20000 km; 2-lane 20000 km; 1000 km Expressway

Ports Inadequate berths and rail/road connectivity

New capacity: 485 m MT in major ports; 345 m MT in minor ports

AirportsInadequate runways, aircraft handling capacity, parking space and terminal buildings

Modernise 4 metro and 35 non-metro airports; 3 greenfield in NER; 7 other greenfieldairports

Railways

Old technology; saturated routes; slow speeds (freight: 22 kmph; passengers: 50 kmph); lowpayload to tare ratio (2.5)

8132 km new rail; 7148 km gauge conversion; modernise22 stations; dedicated freight corridors

Power

13.8% peaking deficit; 9.6% energy shortage; 40% transmission and distribution losses; absence of competition

Add 78577 MW; access to all rural households

Telecom/ITOnly 18% of market accessed; obsolete hardware; acute human resource shortage

Reach 600 m subscribers—200 m in rural areas; 20 m broadband; 40 m Internet

Infrastructure – Deficit and targets of 11th Five Year Plan Sector-wise investment estimated in the 10th Five Year Plan

Energy: 33.49% Roads and bridges: 16.63% Telecommunications: 11.86%

Railways: 13.73% Irrigation: 12.80% Water supply: 7.44%

Ports: 1.61% Airports: 0.78% Storage: 0.55%

Gas: 1.11%

Insights: India’s real estate sector

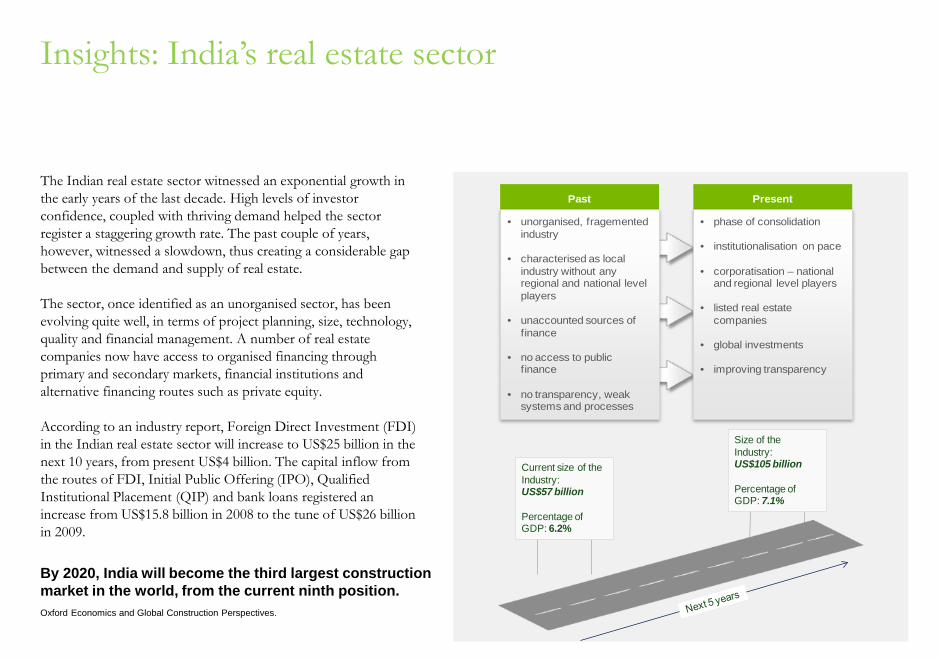

The Indian real estate sector witnessed an exponential growth in the early years of the last decade. High levels of investor confidence, coupled with thriving demand helped the sector register a staggering growth rate. The past couple of years, however, witnessed a slowdown, thus creating a considerable gap between the demand and supply of real estate.

The sector, once identified as an unorganised sector, has been evolving quite well, in terms of project planning, size, technology, quality and financial management. A number of real estate companies now have access to organised financing through primary and secondary markets, financial institutions and alternative financing routes such as private equity.

According to an industry report, Foreign Direct Investment (FDI) in the Indian real estate sector will increase to US$25 billion in the next 10 years, from present US$4 billion. The capital inflow from the routes of FDI, Initial Public Offering (IPO), Qualified Institutional Placement (QIP) and bank loans registered an increase from US$15.8 billion in 2008 to the tune of US$26 billion in 2009.

By 2020, India will become the third largest construction market in the world, from the current ninth position.Oxford Economics and Global Construction Perspectives.

Current size of the Industry:US$57 billion

Percentage of GDP: 6.2%

Size of the Industry:US$105 billion

Percentage of GDP: 7.1%

Past

• unorganised, fragemented industry

• characterised as local industry without any regional and national level players

• unaccounted sources of finance

• no access to public finance

• no transparency, weak systems and processes

Present

• phase of consolidation

• institutionalisation on pace

• corporatisation – national and regional level players

Transparency on customer services has also improved vis-à-vis delivery schedules, information sharing on issues and after sales. We also cannot ignore the positive developments on the fronts of policy reforms and the increasing recognition of real estate as an infrastructure service driving the economic growth engine of the country.

With so many positive signs, the sector has gained in a short period of time, the concern in the present perspective, however, arises as how to deal with the challenges posed by multi-pronged pressures on the front of regulatory environment, planning governance and finance.

There is an opportunity of high growth, yet again, in the approaching times, and a planned and strategic approach will help seize this opportunity, at an optimum level.

Data source: The United Nations and Capital Line

India’s real estate sector structure

Office Residential Retail Hospitality

• primarily driven by services sector,mainly IT/ITeS and financial services

• over 7000 listed companies

• more than 730,000 private companies

• rising demand for plug-and-play offices

• 40 cities with over one million population

• 85 cities with more than half-a-million population

• 379 million people to move to urban areas from rural areas

• huge shortage of housing units

• demand for affordable housing

• top 20 cities generate over 30% of India’s disposable income

• household income growth at 11.2% from 2004 to 2007 in these cities

• opening market for global retail majors

• riding on the back of US$36 billion travel & tourism industry

• double-digit growth in the foreign tourist arrivals in 2010

• Incredible India campaign attracted 4.93 million foreign tourists till November 2010

• domestic business and leisure travel on rise

Tier I cities: Mumbai, Delhi, Bangalore, Chennai, Kolkata

Tier II cities: Hyderabad, Pune, Ahmedabad, Chandigarh, among others

Tier III cities: Jaipur, Nagpur, Indore, Bhopal, among others

The Indian real estate sector has been witnessing some significant changes for the last couple of years and there is clearly a very strong momentum to bring major shifts with respect to planning, governance and finance. In order to realise the ambition of bringing the Indian real estate sector at par with the global real estate sector, a coordinated effort and focus is required from each of the key stakeholders of the sector.

• developers - need to be more transparent in sharing information- technology will be the catalyst – use of technology can take this sector to a different level

• government- needs to streamline the approval process and make it more objective- real estate and infrastructure sector should be closely integrated- introduce reforms by providing additional benefits/ incentives- real estate bill should be enforced at the earliest

• financers- need to have relatively liberal policies when it comes to lending to real estate and infrastructure

companies- utilisation of funds should be closely monitored - create deterrents for non-compliance of lending norms

The following sections would discuss the aforementioned aspects in a detailed manner.

David JonesPartner and Practice Leader – Real estate Walker, Chandiok & Co

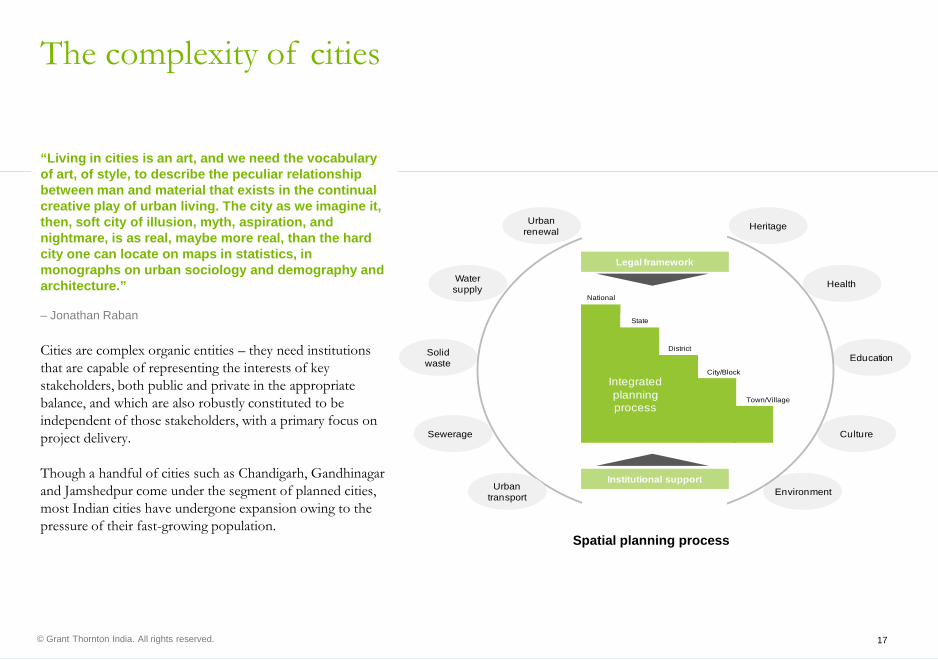

“Living in cities is an art, and we need the vocabulary of art, of style, to describe the peculiar relationship between man and material that exists in the continual creative play of urban living. The city as we imagine it, then, soft city of illusion, myth, aspiration, and nightmare, is as real, maybe more real, than the hard city one can locate on maps in statistics, in monographs on urban sociology and demography and architecture.”

– Jonathan Raban

Cities are complex organic entities – they need institutions that are capable of representing the interests of key stakeholders, both public and private in the appropriate balance, and which are also robustly constituted to be independent of those stakeholders, with a primary focus on project delivery.

Though a handful of cities such as Chandigarh, Gandhinagarand Jamshedpur come under the segment of planned cities, most Indian cities have undergone expansion owing to the pressure of their fast-growing population.

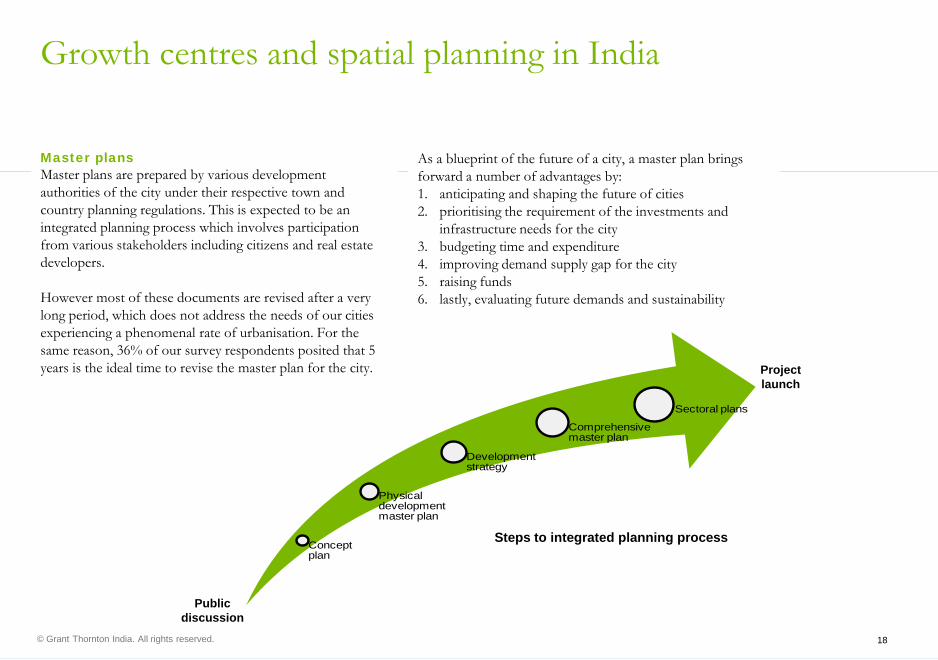

Master plansMaster plans are prepared by various development authorities of the city under their respective town and country planning regulations. This is expected to be an integrated planning process which involves participation from various stakeholders including citizens and real estate developers.

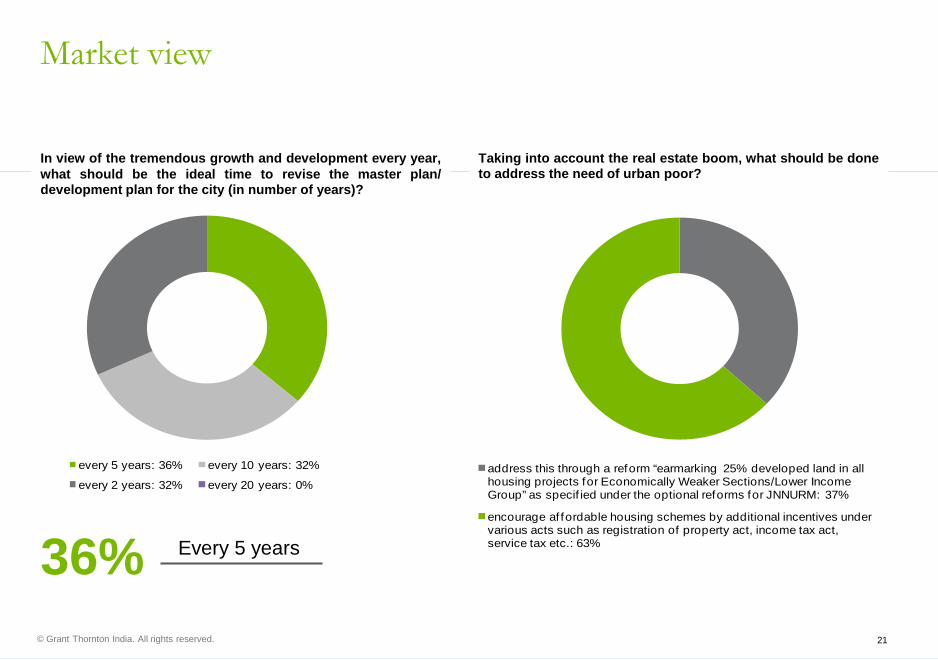

However most of these documents are revised after a very long period, which does not address the needs of our cities experiencing a phenomenal rate of urbanisation. For the same reason, 36% of our survey respondents posited that 5 years is the ideal time to revise the master plan for the city.

As a blueprint of the future of a city, a master plan brings forward a number of advantages by:1. anticipating and shaping the future of cities2. prioritising the requirement of the investments and

infrastructure needs for the city3. budgeting time and expenditure4. improving demand supply gap for the city5. raising funds6. lastly, evaluating future demands and sustainability

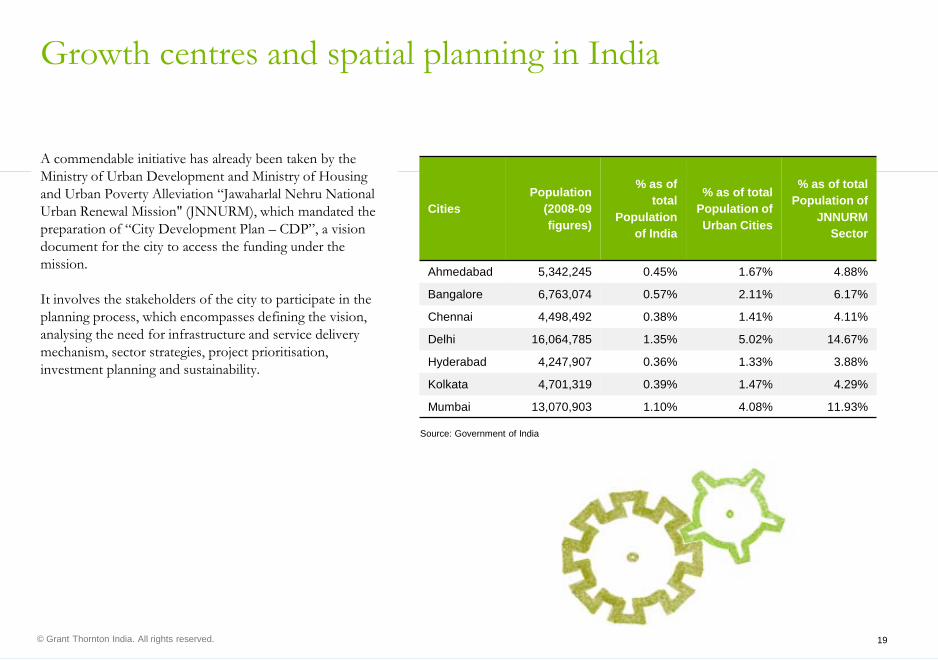

A commendable initiative has already been taken by the Ministry of Urban Development and Ministry of Housing and Urban Poverty Alleviation “Jawaharlal Nehru National Urban Renewal Mission" (JNNURM), which mandated the preparation of “City Development Plan – CDP”, a vision document for the city to access the funding under the mission.

It involves the stakeholders of the city to participate in the planning process, which encompasses defining the vision, analysing the need for infrastructure and service delivery mechanism, sector strategies, project prioritisation, investment planning and sustainability.

Government reforms73rd and 74th Constitutional Amendment Act (CAA) Aimed at bringing a sea change in the rural and urban governance, the 73rd and 74th constitutional amendments were historic legislations.

The amendments facilitated a decentralised governance structure comprising of duly elected representatives of people and encourages greater participation of all the stakeholders, particularly women, scheduled caste, scheduled tribe and members of the backward communities, in urban governance and management.

This remarkable move also ensures that adequate resources are made available to the local bodies. Immediately after the said legislation was enacted, the state governments went ahead with appropriate amendments in the state legislation to bring them in tune with the CAA.

In the urban sectors the Municipal Acts underwent changes to include the provisions of 74th CAA, the state governments took steps to transfer the functions included in the 12th schedule besides constituting the State Finance Commissions and the Election Commissions.

Under 74 CAA, 12th schedule specifies transfer of below specified functions:1. urban planning function including town planning2. regulation of land use and construction of buildings 3. planning for socio economic and social development

This was to strengthen the urban local bodies and make them accountable for the service delivery in their cities. For decades urban development authorities have been involved in the planning exercise except cities like Ahmedabad where corporations are also being involved in the planning process.

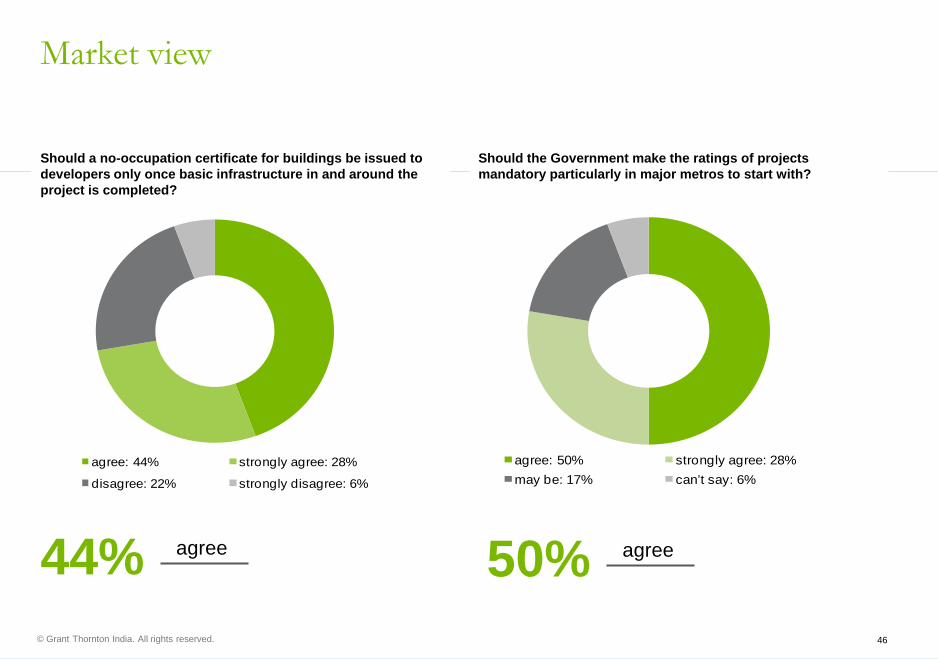

In view of the tremendous growth and development every year,what should be the ideal time to revise the master plan/development plan for the city (in number of years)?

Taking into account the real estate boom, what should be doneto address the need of urban poor?

address this through a reform “earmarking 25% developed land in all housing projects for Economically Weaker Sections/Lower Income Group” as specif ied under the optional reforms for JNNURM: 37%

encourage af fordable housing schemes by additional incentives under various acts such as registration of property act, income tax act, service tax etc.: 63%

Towns adjoining metropolitan cities in India have been successful in decongesting larger cities, controlling population migration and providing better quality of life. However, most satellite towns or twin cities in the country have grown organically. A planned development of these urban areas can help improve the scenario in a faster and better manner.

Satellite townsSatellite towns are smaller municipalities that may be planned adjacent to the major city which in turn forms a part of the metropolitan area. Satellite towns are different from suburbs and subdivisions in the sense that they have separate urban local body from the parent city (the mega/metropolis). These towns have their own independent urbanised area and are considered to be the part of the urbanised area of a large city.

The emergence of Gurgaon, Noida, Faridabad and Ghaziabad around New Delhi is the prime example of satellite towns in the Northern India. Considering the potential of satellite towns in decongesting larger cities, the government has now taken a welcome move of developing satellite towns, thereby converting natural urban sprawl into urban development.

About seven mega satellite towns around the mega cities of India viz. Delhi, Mumbai, Kolkata, Chennai, Bangalore, Hyderabad and Ahmedabad have been planned to be developed under a pilot project of the ministry of urban development and the project will be extended to other larger cities as well.

Twin citiesTwin cities refer to cities that are in geographic proximity. They are so close that they grow into each other. Twin cities often have their own defined limits and are separated by a natural border or barrier. Moreover, these cities can have their own governing structure i.e. they can either have two separate municipal corporations running the cities or both the cities being run by a single municipal corporation.

Where twin cities differ from satellite townships is in the fact that satellite cities are miniature metro areas on the fringes of larger ones and are separated from the larger center by a substantial belt of rural territory, while twin cities may be fully integrated in physical form.

Satellite townships evolve as a result of the population from the larger metropolitan areas migrating to these areas in search of better and more affordable living amenities with the core still being the larger metropolitan area. Satellite townships are sometimes listed as part of the larger metro area, and sometimes listed as totally independent. In terms of governance, satellite townships have their own municipal councils established to take care of day to day running of the city.

Twin cities have multiple centers of equal importance and it is the inter-dependence between these multiple centers which gives rise to this concept. An example of this can be resource sharing between twin cities in terms of industrial development with one city being the industrial hub and the other city being a resource provider for the industry in terms of power, workforce and raw materials.

Examples of twin cities in India

• Chandigarh and Mohali• Kolkata and Howrah• Hyderabad and Secunderabad• Pune and Pimpri Chinchwad• Bhubaneswar and Cuttack• Hubli and Dharwad

• focus on appropriate town planning including topics related to affordable housing, scalability, satellite cities, vertical or horizontal growth, zoning laws etc

• provision of adequate resources to local bodies

• participation of citizens and real estate developers in city planning and development projects

• development of well-planned satellite towns to decongest metropolitans and prevent urban decay

Management and governance: turning liabilities into assets

India has been witnessing a very high rate of urbanisation. The economic base of the nation has already shifted to the urban centers through expanding industries, trade, commerce and services. With cities emerging as the engines of economic growth, India is bound to experience an unprecedented shift of human settlements to the cities.

This urban explosion is expected to create a need for investments in the social and economic functions of the cities to ensure the cities deliver a quality of life that can enable people to become national assets.

The graduation of number of urban centers from lower population size categories to bigger cities has resulted in a top heavy structure of urban population in India. A sizeable part of the country has reached levels of urbanisation which are much higher than the national average. Some of the states like Tamil Nadu and Maharashtra are now close to the half-way mark and states like Gujarat and Karnataka are substantially urbanised. Amongst the smaller ones, Delhi, Mizoram, and Goa are predominantly urban.

Lopsided urbanisation has led to degradation of the environment and the overall quality of life. Some of the key parameters that need to be taken into account to assess the current situation in the Indian cities are water supply, private transportation, sewage, solid waste, rail based transit and affordable housing creation.

The current performance of India’s cities is poor across key indicators and hence there is a strong need for effective urban governance for sustained growth.The need of the hour is to discover resources to fulfill requirements of maintaining and augmenting infrastructure, responding strongly to the urbanisation, safeguarding environment and yet retaining competitive edge. It is evident that if cities fail to deal constructively with these factors, it will undermine the sustainability of cities.

A phenomenal 72% survey respondents voiced their opinion that public participation and feedback should be ensured in order to improve city governance.

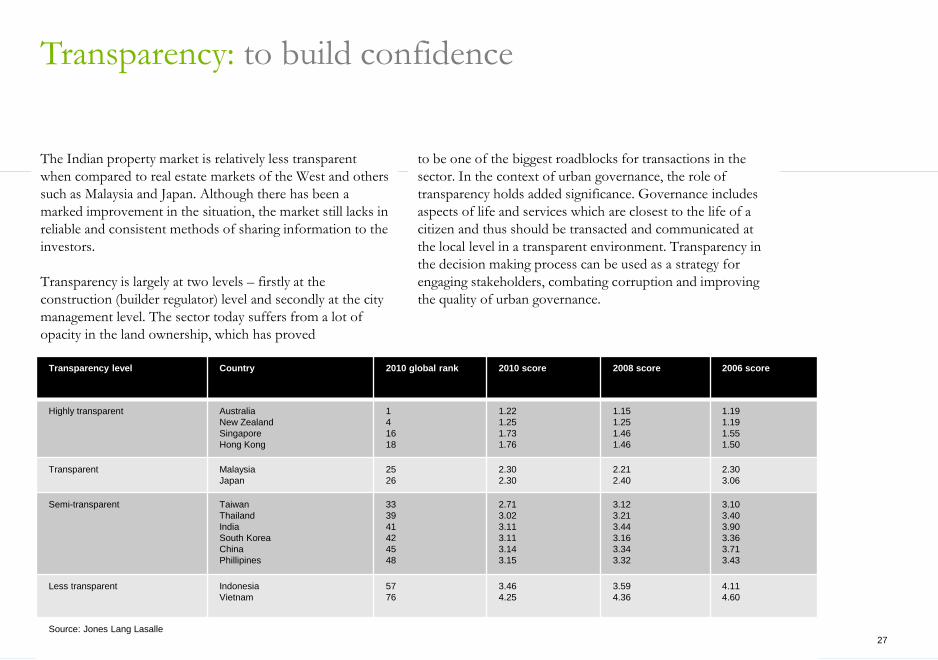

The Indian property market is relatively less transparent when compared to real estate markets of the West and others such as Malaysia and Japan. Although there has been a marked improvement in the situation, the market still lacks in reliable and consistent methods of sharing information to the investors.

Transparency is largely at two levels – firstly at the construction (builder regulator) level and secondly at the city management level. The sector today suffers from a lot of opacity in the land ownership, which has proved

to be one of the biggest roadblocks for transactions in the sector. In the context of urban governance, the role of transparency holds added significance. Governance includes aspects of life and services which are closest to the life of a citizen and thus should be transacted and communicated at the local level in a transparent environment. Transparency in the decision making process can be used as a strategy for engaging stakeholders, combating corruption and improving the quality of urban governance.

Transparency level Country 2010 global rank 2010 score 2008 score 2006 score

Highly transparent AustraliaNew ZealandSingaporeHong Kong

Direct and clear accountability: key to good governance

The accountability of local authorities to their citizens is fundamental to good governance. Choices that cities make on leadership and management are a vital component of effective governance. A successful model of governance empowers the local leaders and holds them accountable. Countries like Britain and China have created empowered bodies to set policies and execute operations. The large cities of these countries have empowered mayors with long tenures and clear accountability for the city’s performance.

Currently, cities in India function under the authority of archaic and bureaucratic departments due to which there is visible lack of accountability. Some of the cities in India have already been learning from their Western counterparts. Kolkata’s modified mayor-commissioner model stands as a good example of reforms in municipal structures.

Having directly elected mayors to lead the metropolitan authorities would be a desirable step towards bringing in more accountability. Also, the relative roles of metropolitan and municipal structures in the country should be clearly defined for the successful management of large cities.

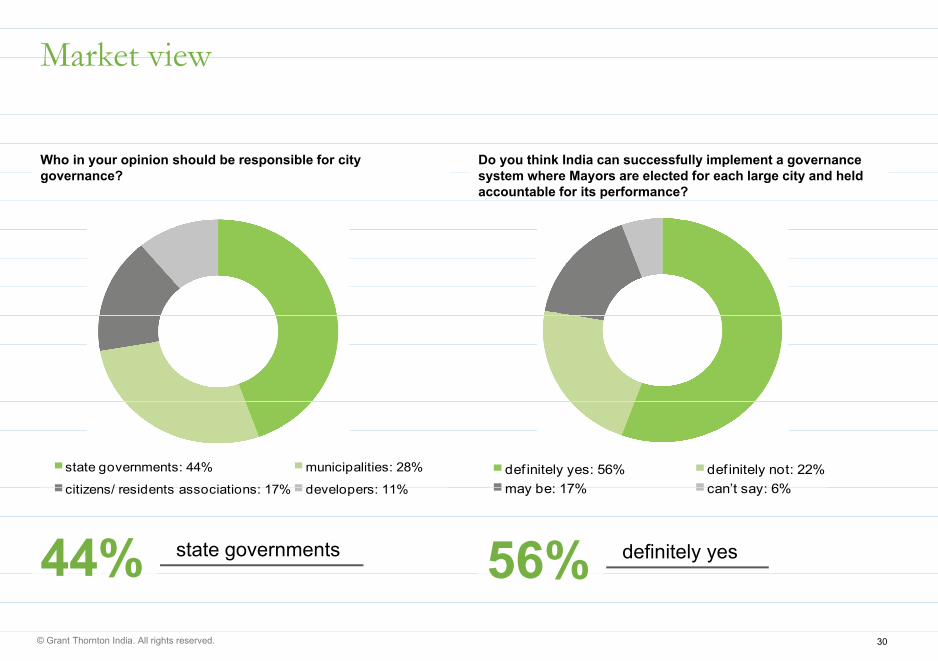

More than half of our survey respondents (56%) said that India can successfully implement a governance system where Mayors are elected for each large city and held accountable for its performance.

The country should also now move to corporate agencies (BEST, Mumbai’s bus and electricity agency, for instance) that have specialised skills and the ability to take decisions quickly and judiciously.

Performance-driven systems should be created which would firstly define and lay down metrics to measure performance. These systems should hold people accountable for their performance, but only after giving them control over the resources needed to do their job. Mechanisms must also be there to suitably reward good performance and improve poor performance.

Market viewMarket view

Who in your opinion should be responsible for city ?

Do you think India can successfully implement a governance t h M l t d f h l it d h ldgovernance? system where Mayors are elected for each large city and held

accountable for its performance?

state governments: 44% municipalities: 28%

citizens/ residents associations: 17% developers: 11%def initely yes: 56% def initely not: 22%may be: 17% can’t say: 6%citizens/ residents associations: 17% developers: 11% may be: 17% can t say: 6%

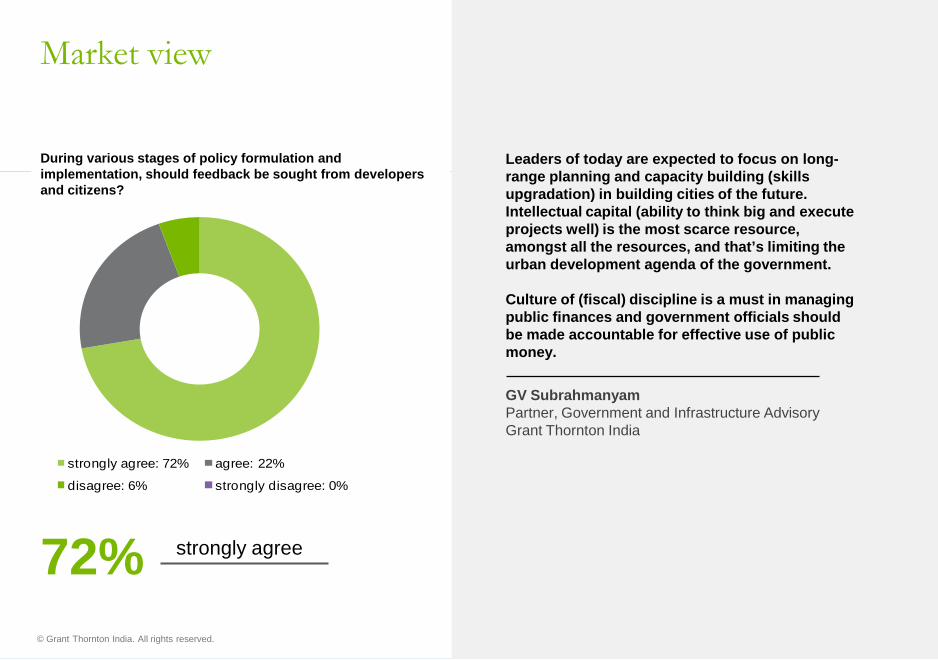

During various stages of policy formulation and implementation, should feedback be sought from developers and citizens?

strongly agree: 72% agree: 22%

disagree: 6% strongly disagree: 0%

72% strongly agree

Leaders of today are expected to focus on long-range planning and capacity building (skills upgradation) in building cities of the future. Intellectual capital (ability to think big and execute projects well) is the most scarce resource, amongst all the resources, and that’s limiting the urban development agenda of the government.

Culture of (fiscal) discipline is a must in managing public finances and government officials should be made accountable for effective use of public money.

GV SubrahmanyamPartner, Government and Infrastructure AdvisoryGrant Thornton India

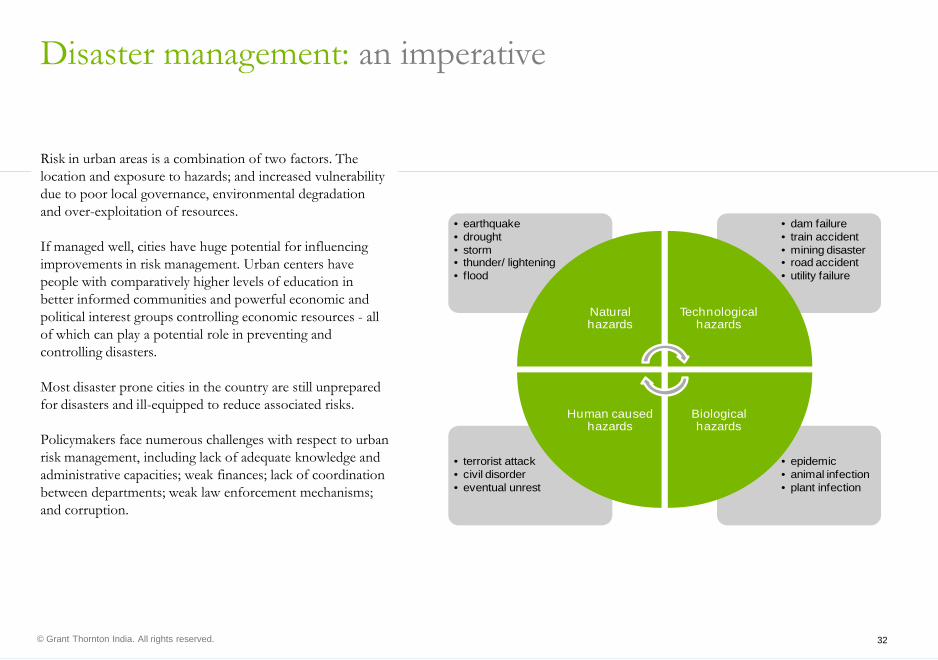

Risk in urban areas is a combination of two factors. The location and exposure to hazards; and increased vulnerability due to poor local governance, environmental degradation and over-exploitation of resources.

If managed well, cities have huge potential for influencing improvements in risk management. Urban centers have people with comparatively higher levels of education in better informed communities and powerful economic and political interest groups controlling economic resources - all of which can play a potential role in preventing and controlling disasters.

Most disaster prone cities in the country are still unprepared for disasters and ill-equipped to reduce associated risks.

Policymakers face numerous challenges with respect to urban risk management, including lack of adequate knowledge and administrative capacities; weak finances; lack of coordination between departments; weak law enforcement mechanisms; and corruption.

Our survey reveals the state of disaster management in our cities. 33% of the respondents believed that disaster management services are non-existent and 39% said that they are hardly present.

A proactive approach to the identification and resolution of issues around urban governance, transparency, accountability and disaster management, with the involvement of all the key stakeholders will ensure that the growth of Indian cities and the real estate sector happens in a planned, structured manner which is beneficial for its inhabitants.

are non existent: 33% hardly present: 39%

present but in-appropriate: 28%

39% hardly present

What is the status of disaster management services available in urban cities?

Technology can be a game changer for the real estate sector and can enable high growth. Using technology in urban planning, maintaining property records, providing online citizen services will lead to efficient and transparent governance. Technology also helps in Disaster Management for our cities. Usage of Green Technology, recycling and waste management will create self-sustaining cities of the future.

Suresh KumarPartner, IT AdvisoryGrant Thornton India

Key aspects

I h ll• a detailed review of city governance and management

and the need to bring in accountability

In a nutshell

• greater clarity and ease in understanding regulations and guidelines

• provide singular approval authority or clearance corridors

• simplify regulations and avoid multi-regulatory bodies. Create mechanisms to monitor and enforce regulationsregulations

• develop more responsive disaster management systems

Despite becoming the second fastest growing economy and the fourth largest economy of the world, India continues to face large gaps in the demand and supply of essential social and economic infrastructure and services.

Rapidly growing economy, increasing industrial activity, burgeoning population pressure, and all-round economic and social development have led to greater demand for better quality and coverage of water and sanitation services, sewerage and drainage systems, solid-waste management, roads and seaports, and power supply. Increased demand has put the existing infrastructure under tremendous pressure and far outstripped its supply.

Where are the gaps?India needs to grow at 9-plus per cent on a sustained basis if it has to lift the masses out of poverty. And the distance between reality and the country's ambition of a sustained high growth rate requires huge investments in physical infrastructure. Take power, for instance. Almost every state has power shutdowns of four to eight hours and the gap between demand and supply is over 15,000 MW.

The delays caused due to dismal roads are estimated to cost the economy nearly 1 per cent of its GDP. Every year India loses Rs 70,000 crore as agricultural produce rots in the fields and on the way to markets because of poor connectivity.

How to bridge those gaps?India requires to develop quality infrastructure with considerable speed, however, there has been cases of under-utilisation of funds and this has made policymakers and planners think hard. The consensus is that the Government must create a pipeline of bankable projects to keep the flow of funds going. The Government should use the India Infrastructure Finance Company Limited (IIFCL) corpus to create a shelf of bankable projects that can be picked up by developers for delivery on time.

The other solution is a stronger long-term debt financing system to support its vast infrastructure financing requirements. Infrastructure projects have a typically long gestation period and need long-term debt. No fund has till now addressed this core need. There is an asset liability mismatch in the banking system. Banks are borrowing for shorter term but end up lending to projects with a maturity of 10-15 years.

The real deep pockets which can fund long-term debt financing are pension funds, insurance companies and provident funds but they need to get the regulatory approvals to invest in infrastructure.

The Government has now put the creation of a separate infrastructure debt fund on the fast track. A Standing Committee on Infrastructure Finance under the chairmanship of the finance secretary has had four stakeholders meetings with insurance companies, equity fund managers, pension and superannuation funds.

While there are ways of making infrastructure funds deliver, the question now is to find the will. Regulatory procedures, delays in project implementation and cost escalations are also impediments to the financial viability of projects.

While infrastructure financing has grown substantially, there is little long-term financing available for infrastructure.

Infrastructure Finance CompaniesThe RBI introduced a special category of Non-Banking Finance Companies (NBFCs), called Infrastructure Finance Companies (IFCs). To qualify as an IFC, over 75% of its total assets should comprise infrastructure assets.

IFCs would benefit from a lower risk weight on their bank borrowings (from a flat 100% to as low as 20% for AAA rated borrowers), higher permissible bank borrowing (up to 20% of bank’s net worth as against 15% for an NBFC), access to external commercial borrowings (up to 50% of owned funds on an automatic basis) and relaxation in their single party/group exposure norms on both debt and equity.

Altogether this should enable a highly rated IFC to raise more funds, of longer tenor and lower cost, and lend more to infrastructure companies. Two key steps were taken to expand the corporate debt market. First, the bonds were imparted more liquidity by allowing repoability of corporate debt instruments with certain minimum requirements. Second, greater transparency was imparted by making the reporting and settlement of transactions through an exchange mechanism mandatory.

Further, to promote greater bank finance to infrastructure, RBI announced various measures in its Annual Monetary Policy Statement in April 2010. First, banks’ provisioning requirements for unsecured sub- standard exposure has been reduced from 20% to 15%.

Second, non-SLR bonds issued by companies engaged in infrastructure activities, with minimum residual maturity of 7 years, could be invested as “held to maturity” and therefore not be subject to mark-to-market requirements. This measure is aimed at incentivising banks to invest in long-term bonds issued by infrastructure companies.

Further, RBI has facilitated lending to the infrastructure sector by allowing annuities and toll collection rights in case of Build Operate Transfer (BOT) type projects as tangible security for the purpose of secured bank loans.

The government also approved the takeout financing norms for IIFCL by allowing it to buy a part of the banks’ loans. This step is aimed at freeing up banks’ capital for financing new projects and addressing their asset liability mismatch concern.

IIFCL is expected to provide takeout finance of about Rs. 25,000 crore in the next three years. Finally, to channel long-term savings from retail investors to infrastructure, the Union Budget announced personal income tax relief of up to Rs. 20,000 for investment in long-term infrastructure bonds issued by companies engaged in the infrastructure sector.

These bonds would be notified by the Central Government. The tax relief of Rs 20,000 would be over and above the existing limit of Rs. 1 lakh on tax savings.

India plans to double its infrastructure spending to US$1 trillion in the five year period starting 2012. Prima facie the figure looks astronomical and one may visualise the tremendous impact on the infrastructure growth. However the infrastructure projects in India have an infamous history of missed deadlines, red tape and massive cost overruns.

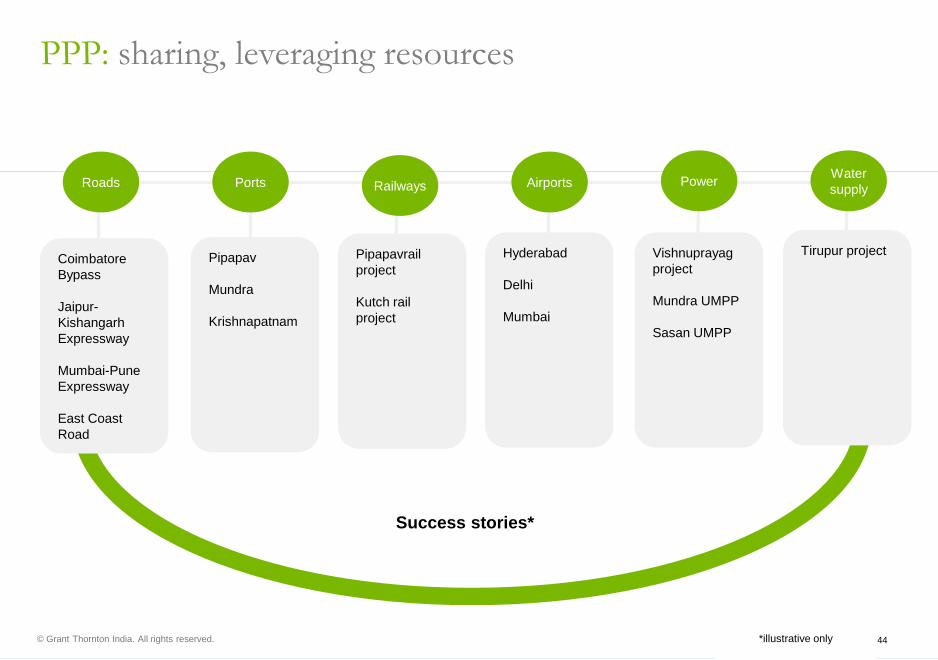

Taking this constraint into consideration and looking at the economy growing over 8.5 per cent every year and a fast urbanising population of 1.2 billion, Indian infrastructure projects need innovative financing models and modern technologies. One such innovative model is Public Private Partnership (PPP).

There is no doubt that there are significant opportunities in India’s infrastructure sector. As we have seen with telecom and, to some extent with power and roads, infrastructure can provide investors with a platform to expand and leverage on the growth of Indian economy. The government is keen to nurture profitable partnerships with the private sector to bridge the investment and the knowledge gaps within infrastructure.

Infrastructure calls for huge investments and while returns are high, it requires investors willing to accept long gestation periods. Infrastructure development is also a function of continuous and speedy adaptation to technology. This would not be possible without quality manpower and heavy investment. Thus it is clear that the way ahead is through well defined and innovative PPPs.

PPP refers to a contractual arrangement between a government agency and a private sector entity that allows for greater private sector participation in the delivery of public infrastructure projects through concession agreements. In comparison with the traditional models, the private sector in the PPP model assumes a greater role in planning, financing, design, construction, operation and maintenance of public facilities.

PPPs represent partnerships inaction with huge stakes for both the public sector and private sector agencies to succeed collectively. It is important that the public and private sector work together, keeping the project and outcomes in focus rather than maximising their own interests, and collaborate for mutually enduring value. PPPs represent a new way of doing business, and not about command and control. Ultimately, the project partners need to remember that PPPsare not about finance, they are also about improving the quality and efficiency of public services.

The Approach Paper to the Eleventh Plan states that “One has to reach out to the private sector, and private savings, and to the other mechanisms available in the market today to raise funds".

The National Development Council (NDC) has passed a resolution which mentions that “increased private participation has now become a necessity” to mobilise the resources needed for infrastructure expansion and upgradation. The Approach Paper to the Eleventh Plan has called for aggressive promotion of private partnership in infrastructure development.

Public Private Partnership (PPP): sharing, leveraging resources

Globally, governments are increasingly constrained in mobilising the required financial and technical resources and the executive capacity to cope with the rising demand for water supply, sewerage, drainage, electricity supply, and solid-waste management. Rapid economic growth, growing urban population, increasing rural–urban migration, and all-round social and economic development have compounded the pressure on the existing infrastructure, and increased the demand–supply gap in most of the developing world.

Countries and governments, especially in the developing world, are experiencing increasing pressure from their citizens, civil society organisations, and the media to provide accessible and affordable infrastructure and basic services. While the infrastructure gap is rising, government budgetary resources are increasingly constrained in financing this deficit.

The pressure has also come from the international pact on Millennium Development Goals (MDGs), under which the progress of the country is measured and monitored in terms of access to safe drinking water, sanitation, health etc.

Rising costs of maintaining and operating existing assets, inability to increase revenue and cut costs and waste, and rising constraints on budgets and borrowing, do not allow governments to make the required investments in upgrading or rehabilitating the existing infrastructure or creating new infrastructure.

The political economy of infrastructure shortages, constrained public resources, and rising pressure from citizens and civil society have combined to push governments and policymakers to explore new ways of financing and managing these services.

Governments have been pushed to exploring new and innovative financing methods in which private sector investment can be attracted through a mutually beneficial arrangement.

Since neither the public sector nor the private sector can meet the financial requirements for infrastructure in isolation, the PPP model has come to represent a logical, viable, and necessary option for them to work together.

The emergence of PPPs is seen as a sustainable financing and institutional mechanism with the potential of bridging the infrastructure gap. PPPs primarily represent value for money in public procurement and efficient operation.

Apart from enabling private investment flows, PPPs also deliver efficiency gains and enhanced impact of the investments. Efficient use of resources, availability of modern technology, better project design and implementation, and improved operations are some of the benefits which are not readily available for a public sector project, in many instances.

PPP projects also lead to faster implementation, reduced lifecycle costs, and optimal risk allocation. Private management also increases accountability and incentivises performance and maintenance of required service standards. Finally, PPPs result in improved delivery of public services and also promote public sector reforms.

The foremost benefit of adopting the PPP route is the ability to access capital funding from the private sector, considering that funding is getting increasingly limited from public sector budgets.

Thus, PPPs allow governments to overcome their budgetary and borrowing constraints and raise finance for high-priority public infrastructure projects. Essentially, governments are able to use private finance through PPPs to build infrastructure projects that would previously have been built by the public sector using public sector finance. PPP projects also leverage public capital by converting capital expenditure into flow-of-service payments.

The high degree of economic externality of public infrastructure, and the commercial and socio-economic risks involved in developing and operating them, has made it difficult to appropriate returns from infrastructure investments.

The long gestation period of infrastructure projects also requires sustainable financial and operational capacity. Therefore, there is increasing reluctance in both the public and private sectors to absorb all the costs and assume all the risks of building and operating these assets alone. Since the private sector assumes the risk of nonperformance of assets and realises its returns if the assets perform, the PPP process involves a full-scale risk appraisal. This results in better cost estimation and better investment decisions.

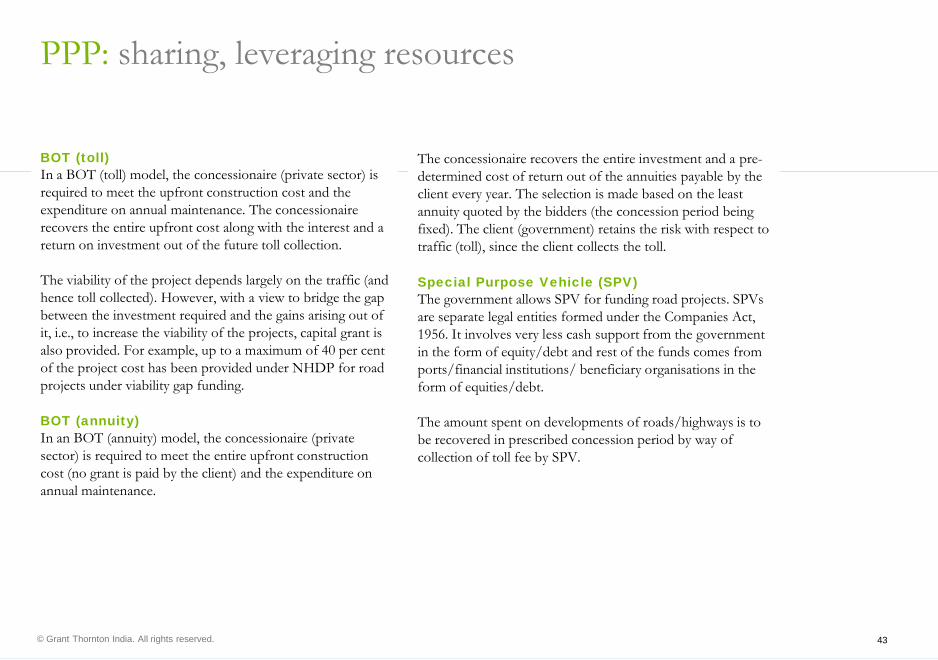

BOT (toll)In a BOT (toll) model, the concessionaire (private sector) is required to meet the upfront construction cost and the expenditure on annual maintenance. The concessionaire recovers the entire upfront cost along with the interest and a return on investment out of the future toll collection.

The viability of the project depends largely on the traffic (and hence toll collected). However, with a view to bridge the gap between the investment required and the gains arising out of it, i.e., to increase the viability of the projects, capital grant is also provided. For example, up to a maximum of 40 per cent of the project cost has been provided under NHDP for road projects under viability gap funding.

BOT (annuity) In an BOT (annuity) model, the concessionaire (private sector) is required to meet the entire upfront construction cost (no grant is paid by the client) and the expenditure on annual maintenance.

The concessionaire recovers the entire investment and a pre-determined cost of return out of the annuities payable by the client every year. The selection is made based on the least annuity quoted by the bidders (the concession period being fixed). The client (government) retains the risk with respect to traffic (toll), since the client collects the toll.

Special Purpose Vehicle (SPV) The government allows SPV for funding road projects. SPVs are separate legal entities formed under the Companies Act, 1956. It involves very less cash support from the government in the form of equity/debt and rest of the funds comes from ports/financial institutions/ beneficiary organisations in the form of equities/debt.

The amount spent on developments of roads/highways is to be recovered in prescribed concession period by way of collection of toll fee by SPV.

Proper allocation of risksEffective PPP models involve sensible ascertainment of roles and fair sharing of responsibilities, costs, and risks between the public and private sectors. Optimal, not maximum, assignment of risk is the principle that needs to be adopted.

Provide adequate protection for lendersPPP design and documentation should provide adequate protection to debt service against non-commercial risks related to force majeure, regulatory changes, contract termination etc.

Avoid renegotiation and midway changes to save costs and delaysA concession agreement should be structured in such a manner as to cover all possible causes of later adjustments, leaving a minimum room for renegotiation.

A key lesson learnt from international experiences is that governments often get over enthusiastic to get private sector participation by offering excessively concessional terms to the project company.

Full and clear support by governmentSupport for the PPP programme and for specific PPP projects has to come from the highest political level of government. A strong political will is essential in overcoming resistance, and needs to be seen as a clear signal of the government’s intention to meet its contractual commitments.

Proactive public communication and stakeholder managementMany PPPs have failed due to strong opposition from the local community, media, and other stakeholders. Feedback and consultations with citizens, labour unions, relevant government agencies, private investors, civil society organisations, and media will ensure support, client focus, and improved overall coordination of the project.

• plan for tangible infrastructure such as roads, water, energy, transportation/ use of solar energy, waste management, recreation, healthcare and education

• incentives and schemes that will provide the necessary push to these sectors

The real estate sector in India has emerged as a significant driver of economic growth in the last decade, rather than being a derivative of the global upturn seen till end 2008. In terms of GDP contribution, the sector has grown from 4.5% in 2007 to 5% in 2009.

Expansion in sources of capital has been a critical catalyst in the sector’s progression towards a more organised play with closer linkages to the macro economic conditions of the country. The sector received capital flows of around US$26 billion in 2009.

However, the sector started facing acute capital scarcity towards the end of 2008 with a slowdown in absorption, increase in home loans rates, declining internal accruals, commercial bank’s cautious approach and expensive FDI/mezzanine funds.

The overall credit situation worsened by the global economic downturn led to the entry of real estate on the ‘negative’ list of the already limited universe of institutional investors.

While alternatives for institutional funding have expanded considerably in the last 5 years, the domestic real estate industry continues to be at a nascent stage when compared to mature markets.

Considering the emerging business environment and investor expectations, real estate companies are expected to take a proactive approach and drive demand by introducing new formats that are missing in the market.

Concepts such as hospotels, which combine services of hospital and hotel, for instance, could be a potential driver. At the same time, affordable housing is slated to be one of the most powerful engines of growth for the sector.

Missing formats and asset classesThe Indian real estate industry is poised to emerge as one of the most preferred investment destinations for global realty and investment firms. There are few anticipated, albeit unexplored potential opportunities, which are likely to ensure sustained growth of the Indian realty sector in the medium to long term.

These engines for growth would act as a catalyst for real estate development across the country. Some of these opportunities which are expected to further drive the demand for real estate development include the following:

• logistics & warehousing infrastructure• healthcare infrastructure• low-cost budget housing• hospotels: combining the services of a hospital and a

hotel

Logistics & warehousing infrastructureWarehousing is one of the main segments of the logistics sector growing the fastest at a rate of around 40 per cent. One of the important industries contributing to this high growth in warehousing is the retail sector.

Healthcare infrastructureGrowing at a compound annual growth rate of 16 per cent, the Indian healthcare sector is expected to grow to about US$50.2 billion and US$78.6 billion by the year 2011 and year 2016 respectively.

The healthcare infrastructure market in the country is expected to grow at 14.5 per cent over the next few years. The total investment required to reach the optimum target of 1.85 beds per thousand populations would be US$77.9billion out of which US$69.7 billion is expected to come from the private sector.

Low cost budgetingAs per the Working Committee of the 11th Plan (2007-12) the total shortage of dwelling units at the beginning of Eleventh Plan Period was 24.7 million. As per the estimates by National Housing Bank (NHB), going forward, the gap of housing unit shortage would further widen to about 45 million units during the Eleventh Plan (2007– 2012) period.

New income tax regimeThe new income tax slabs introduced by the Government of India will reduce the tax burden for 60% of the taxpayers in the country. It is hoped that the resulting higher levels of disposable income would translate into greater consumption levels for products ranging from durable goods to real estate.

Besides policies and regulations, the GoI has also provided income tax incentives depending upon the nature of project. Affordable housing projects (including slum redevelopment and rehabilitation projects) approved before March 31, 2008 are eligible for profit-linked incentives under Section 80-IB (10) of the Income Tax Act.

The tax incentive is 100 per cent of profits earned from the business of developing and building specified housing projects subject to certain conditions.

Over 46% of the total plan outlay (Rs 173,552 crore) has been allotted for infrastructure development during 2010-11. Furthermore, an additional Rs 20,000 in tax savings will be allowed for taxpayers who invest in infrastructure bonds, a policy move which will further infuse funds into infrastructure development in India.

Reaffirming SEZsIt was decided during FY2009-10 that only investment-linked incentives would be provided while profit-linked incentives would be done away with. The Government is yet to clarifying issues pertaining to this. However, the removal of an anomaly in Section 10AA of the SEZ Act for estimating export profits and the Finance Minister’s reaffirmation on the importance of special economic zones (SEZ) will help the real estate industry in taking forward its SEZ plans across the country.

Urban development allocation up by 75%The Budget 2010 increased the allocation for urban development to Rs 5,400 crore which includes Rs 1,270 crorefor slum redevelopment and Rs 1,000 crore for housing and urban poverty alleviation.

Interest subvention scheme on housing loans extendedThe one percent interest subvention scheme introduced during the FY2009-10 Budget has been extended for another year for housing loans of up to Rs 1 million with property value of less than Rs 2 million. This will continue to boost demand in India’s affordable housing market.

Project completion period extended from 4 years to 5yearsReal estate developers, many of whom have struggled to complete projects due to the credit crunch can benefit from this extension as, under section 80-IB, they would be eligible for tax benefits within 5 years from the date of approval of their projects from local authorities. A 100% tax deduction on profits from housing projects was previously available within 4 years only.

Increased housing unit sizeBudget 2010 increased the permissible built up area (BUA) of individual housing unit from 2% of the total BUA or 2,000 sq ft to 3% of the total BUA or 5,000 sq ft whichever is higher. This has the potential to positively impact the luxury housing market.

ECB to be made available for cold storageGreater access to cheaper funds through external commercial borrowings (ECBs) may help the development of quality cold storage facilities in the country, potentially benefiting the Indian logistic industry and driving demand for warehousing space. Currently, 25-30% of perishable food items in India are lost due to spoilage as India lacks quality cold storage facilities.

5 additional mega food park projectsThis would take the total number of food parks in the country to 27 and drive ample real estate development opportunities in the precincts of these new food parks.

Investment linked tax incentive scheme to hotel industryStarting April 2010, a 100% deduction on capital expenditure (excluding land, goodwill, and financial instrument) has been proposed for 2 star hotels and above. This initiative would spur a supply-side boost to the hotel industry across India.

Increase in excise duty from 8% to 10%Costs of material input such as cement will increase and drive up the cost of construction for real estate development.

Hardening of interest ratesThe government intends to gradually roll back the stimulus packages in tandem with tighter monetary policies by the RBI. As such, bond yields are expected to harden in the short term and be in the range of 7.75-8.25% during FY2010-11. A likely hike in interest rates would result in higher home loan rates and higher cost of funds for real estate development, both of which would dampen the recovery of the real estate sector.

The Government’s clear emphasis on infrastructure development, its shift towards fiscal prudence and an effort towards lessening the burden on taxpayers are initiatives that will bode well for India’s real estate industry and its economy as a whole.

The US is the master of pooled finance. Its bond markets, being mature and dynamic have a considerable depth and tradability for long-term finance. The US treasury rate usually acts as the true arbiter for the same. A number of municipalities have raised pool finance in bonds, through participation certificates, since the 1980s.

Their experience is therefore worth looking at, as the arbiter of pooled finance in India. In the US, the private initiatives started in 1960s. Since then, laws have been passed in almost every area to allow the private sector to participate. Even so, there was a substantial resistance in the '60s and '70s until budgetary realities forced a sizeable change, as far as roads, healthcare, power and educational institutions were concerned.

Privatisation went to the extent where even trading in power was encouraged. Many varied instruments came up to take care of the financing aspects.

The stock markets freely quoted utility companies and so equity financing was not an issue. Pooled finance against certificates of participation came up in many urban centers. These certificates were traded and re-traded many times. Institutional loans were not an issue, as end user charges were freely available. Therefore, federal grants were kept to a minimum. This elaboration serves as a model as to how it works in the most developed country.

Private sector participation in infrastructure, both in the development of new projects and in the acquisition of privatised public sector monopolies, offers many potential benefits. Competition generally improves the supply and quality of infrastructure service, thus boosting local standards of living.

In addition, the participation of the private sector in infrastructure allows governments to devote more of their public funds to pressing social problems or to the development of projects that are unattractive to private investors.

Private Financial Institutions (PFI) initiatives in BritainBritain has made significant progress in the management of enterprises through private finance initiatives. Since late 1980s, it is often argued that the PFI provides additional investment for the public sector and enables projects to proceed which would not otherwise have been possible. In this case, the investment may be done directly or indirectly.

Essential features of PFI• capital investment projects (for the public sector) are

financed as well as constructed by a private company, and then leased back to the public sector over a predetermined period (generally 25 to 30 years), and that generally the private company provides a range of services associated with the capital project (e.g., maintenance)

• PFI involves not only alternative sources of finance for public investment but also services related to the capital

• the PFI appeared to be a way of drawing on alternative sources of finance in such a manner which would not increase the (reported) budget deficit

• under the PFI, the concerned company borrows at a higher rate of interest which is reflected in the price it charges to the government, but the company bears the risks associated with the operation and maintenance of the investment project.

Malaysia initially followed the traditional methods of financing, i.e., through the government grant and international loans, supported by government guarantee etc. However, in the 90s, the Malaysian Government drew up an ambitious plan for expansion of the private sector.

In 16 years, i.e., from 1983-1999, more than 200 projects came up which had a reasonable degree of privatisation. Most of these projects either made break even or profit. This attracted the interest of the world, and Malaysia became a model for the developing countries. The Malaysian Government also encouraged the ingress and egress of their senior staff to go to the private sector on three and five year deputations.

These staff members often came back with massive experience on how to structure a commercially viable deal. This highlights a very important issue-the relative lack of know-how of senior state officials on how to make a deal commercially viable.

This is due to a lack of understanding from the investors' point of view that can be rectified with real

work experience of the sector. This issue cannot be underestimated in spite of the mass of technical reasons that is given for the relative failure of the private sector in infrastructure.

In addition to this, the Malaysian Government made very effective use of guarantees and funding as "last mile coverage". In short, when all the structuring was done and a little "juice" was required to sweeten the deal, the state often came forward with the sweetener. This approach made the best use of limited government funds.

There is no doubt that this helped in accomplishing a number of projects. The sweetener could be in the form of state guarantees full or partial, bank guarantees, part funding, or any other form of comfort to get the private investor and international community to pump in the funds.

The Malaysian methods have been replicated either fully or partially by many other developing countries. China has also made very effective use of the partial guarantees to attract substantial FDI. Their forte has been joint ventures and successful pilot projects. All of these provide effective models for them to follow.

China has some well-established principles for attracting funds for infrastructure, which have stood the test of time. For example: • they generally raise debt in the local market through the

banking system, varying around 17% on average • equity is raised by means of joint ventures and

international issues. Joint venture tends to have 51% government participation. Foreigners seem to be generally happy with 49% which allows them significant say in the management of the company

Any new and innovative idea is readily accepted and first tried on a small scale, which is implemented quickly and readily. If it works, then it is expanded on a large scale. This is where India could learn from China. India, being a democratic country, tends to take a lot of time implementing a project.

If the project could first be tried on a small scale (say in select municipalities and panchayats where the decision-making is absolutely from the ground level), then this would encourage the shareholders and stakeholders that something was indeed happening.

Offices would be set up and the commitment starts. Any errors/problems could be quickly rectified so that the large projects would not suffer from major operational deficiencies. All this is absolutely essential to get the right stakeholder/financier inland to see the actual color of his money.

Growing real estate needs supported by strong macroeconomic fundamentals will necessitate additional amount of liquidity into the system. Encouraging small investors to invest and mopping up large sums through Real Estate Investment Trusts (REITs) and Real Estate Mutual Funds (REMFs) is essential. This will facilitate the much-needed supply of funds for the real estate sector to provide housing to 1.2 billion people at the rate of providing almost 10 million units annually. SEBI has already issued draft REMF regulations in 2008, but will have to accelerate the roll-out after careful considerations.

Granting infrastructure status to some of the critical priority projects in the real estate sector is vital for the sector's growth as building integrated townships, mass housing colonies, special residential zone etc are more or less the same as building large-scale infrastructure facilities. If it is accomplished, banks could extend loans to the industry on similar norms as they adopt for infrastructure companies. This will also attract investments from foreign investors. Needless to mention, such projects should also be provided tax incentives as are eligible to the infrastructure projects.

Apart from these reforms measures, there are several other measures that the Government can consider taking on a priority basis to support the sector in maximising its growth. Single window clearance should be introduced at the earliest, while eliminating the need for environmental clearances, if the plan is as per zonal requirements.

Finally, if the government were to make affordable housing a success story, the developers should be provided incentives in the form of land at concessional rates along with other tax incentives, provision of surrounding infrastructure, loans at concessional rates to the buyers and the like.

The three land-mark legislations staring at the door step of the economy–Direct Taxes Code 2010, GST and IFRS–will change the rules of the game and hence these legislations should be crafted as also implemented carefully.

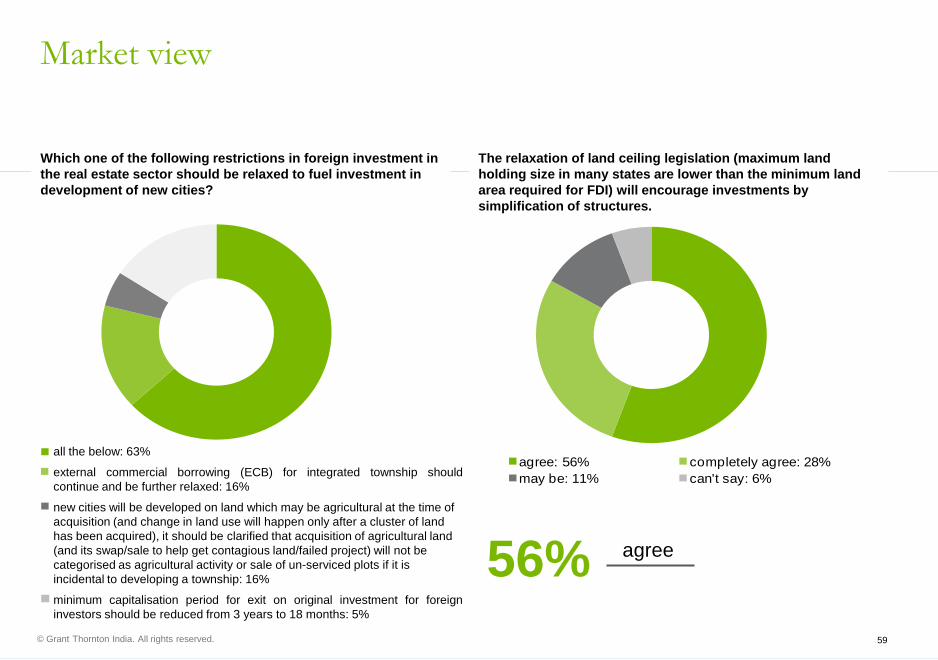

Which one of the following restrictions in foreign investment in the real estate sector should be relaxed to fuel investment in development of new cities?

The relaxation of land ceiling legislation (maximum land holding size in many states are lower than the minimum land area required for FDI) will encourage investments by simplification of structures.

external commercial borrowing (ECB) for integrated township shouldcontinue and be further relaxed: 16%

new cities will be developed on land which may be agricultural at the time of acquisition (and change in land use will happen only after a cluster of land has been acquired), it should be clarified that acquisition of agricultural land (and its swap/sale to help get contagious land/failed project) will not be categorised as agricultural activity or sale of un-serviced plots if it is incidental to developing a township: 16%

minimum capitalisation period for exit on original investment for foreigninvestors should be reduced from 3 years to 18 months: 5%

56% agree

m

• understand the dynamics of financing a city’s development and growth plan

• identify incentives required to attract investors, businesses, home-owners and tourists

• evaluate current sources of finance available for a city and conduct a gap-analysis

• introduce new models and focus on affordable housing to keep up the momentum of growth

• review capital markets, financial instruments and tax/ duty structures to explore new sources of finance

Considering the changes in global climate, rising population, pollution, related regulations and also the commercial concerns vis-à-vis power crisis, running cost and pressure on urban infrastructure, green practices are all likely to surface up as a necessity rather than a matter of choice, in the next ten years.

Along with the environmental concerns, the most obvious objective of constructing green buildings would be to bring in energy efficiency practices, thus reducing the consumption of power and water, primarily. However, in the short term, real estate developers find the initial cost of deploying energy efficient systems as a major hindrance.

According to industry veterans, constructing a green building typically costs 25-35% more than the normal cost of construction. On the other hand, the cost benefit generated over the life of a green building far exceeds the initial cost of construction.

Nevertheless, there is a host of indirect benefits of constructing green buildings, in terms of better health, productivity, and of course, the brand equity for the developer.

The colour green has more positive connotations than negative. Green refers to environment, nature, spring, energy, health, harmony, life, growth, stability, money, wealth, etc. We build anything to thrive and survive. Why not strive to build green then? Not just real estate but more … Go green to save green.

Kenneth D. KhalkhoAssociate Director, CSR & SustainabilityBusiness Advisory Services, Grant Thornton India

Green construction will become the convention as more and more ecological regulations and laws supervising the industrial sector are mandated. The cities of the future will be completely self sustainable in terms of energy consumption, and architects will need to follow strict green design and construction criteria.

As a matter of fact, most of the technology for environment-friendly construction already exists and it is only a question of time until we see it being implemented on a regular basis.

General contractors too will need to reassess their approach to home improvement and remodeling, putting eco-friendly concepts of construction in use. For instance, recycling of old materials from the job site is completely easy to do with huge benefits to the environment in terms of waste control and reduction.

Real estate developers and general contractors only need to review and put in place the practices that are environment friendly and yet cost effective in the long term.

A vision of a clean, climatically stable planet has been envisaged since the industrial revolution. The need for power and energy to steer human life in the most natural and environment friendly way, is best achievable using green technology based resources.

The unlimited demand of energy to cater to human needs and the abundant availability of green resources combine to make “Greentech” and evergreen technology. Green technology or Clean Technology is emerging as one of the, if not the most important considerations for the realty sector all across the globe.

The industrial revolution that started 150 years ago brought advances but also marked the beginning of dangers down slope to the environment. Now is the time to start using technologies that can work harmoniously with the wonderful world we live in without compromising our quality of life.

Smart green design and construction is the way to go and general contractor and re-modelers as well as home owners are obligated to consider how to implement green construction technologies and products on every remodeling project, small or big!

Goals of green building – the next evolution in residential constructionFrom water-stingy toilets and electricity-sparing appliances, to flooring and siding made from sustainable materials, the housing industry is rolling out a trove of new, green products it hopes will lure homebuyers back into the market.

The tide toward green building that has taken hold in recent years remained unabated as the industry looks forward to better days, convinced that energy-efficient homes outfitted with sustainable materials will be coveted by future homebuyers.

People are interested in the things they can do to cut energy bills in the long run. And increasing competition between green-product suppliers is driving costs down, making it more affordable to build greener homes.

According to the United States Energy Information Administration, owners spend $107.9 billion annually on energy costs for commercial buildings.

In the last few years, we have seen a surge in the adoption of energy efficient technology implemented into buildings we live and work, in an effort to reduce costs and the buildings’ carbon footprint.

Building owners who have incorporated green technology into their buildings report a reduction in their monthly energy bills without having to sacrifice the comfort of the occupants. One example of a technology that has become cheaper is radiant floor systems, which function as heaters.

The main goal of green building is not just to be more friendly to the environment, but also be a healthier place to live for the home's occupants. In every aspect of a green home, non toxic or less toxic materials are employed. Green homes will also blend in better with their surroundings and use much less energy and water.

AdvantagesThere are many advantages to building and living in a green home. While there may be a bit more upfront cost, over the life of the home, the savings on energy costs alone would more than make up for any upfront costs. More cost savings will arise from energy efficiency, water efficiency, landscaping efficiency and materials efficiency. Also, for very sensitive homeowners, a green home will have used much less toxic or chemical based materials, making a green home much safer and healthier for the owner.

Green products in constructionWith the popularity of "green" products on the rise and the trend not looking to slow down anytime soon, construction products and building techniques that are friendly to the environment are seeing a rapid rise in sales.

Green practices can be incorporated from the very beginning of the building process. From the concrete masonry, beams, doors, windows, mechanical and electrical systems, moisture and heat protection,

finishes, appliances, pretty much for any aspect of building, there are green options and choices that can be made.

FlooringThere are many green types of flooring now available. Wood flooring made from wood that has been taken from old or disused buildings has gained more popularity, since this is a smart way to recycle. For new flooring products, green builders can now choose from green choices like cork, rubber and bamboo. New linoleum products are also now available that can be recycled and are less toxic than their predecessors.

CarpetCarpets are now available that are recyclable, use little or no toxic materials in manufacturing and are also lower in cost. Carpet tiles are a very green choice and are extremely easy to install and replace.

Not only is green home construction a hot area, green remodeling has also come to the forefront. Existing homeowners can now incorporate green building practices and materials when they are remodeling their homes. For example, in a typical kitchen remodel, the appliances are all replaced. In the case of a green home remodel, the appliances would all be replaced with energy star efficient appliances. Thus saving energy and money at the same time.

In the case of a bathroom remodel, simply replacing a toilet with a newer model toilet will save several gallons of water for each flush, which adds up to a significant water savings over time.

Whether you choose to use green practices to build or remodel for cost savings or environmental reasons, it's certain that green building is a trend that will only continue to grow.

Tax incentivesIn its annual budget, the Union government said it plans to levy a tax on the use of coal and use the money to start a national clean energy fund to back renewable energy projects. Besides, there are wind energy incentives, including a provision for 80% accelerated depreciation in the first year, a 10-year tax holiday, an income-tax waiver on power sold to utilities and favourable tariffs.

India offers several subsidies for solar power systems, such as solar lanterns and home lighting systems, and generation-based incentives of up to Rs12 per kilowatt-hour for power plants.

For small hydropower projects, there are concessions on customs duty, a 10-year tax holiday and other state-level incentives, including sales and electricity tax exemptions and preferential tariffs. Even general domestic private equity funds have been drawn to clean energy.

Ten Fifty B: San DiegoTen Fifty B is the tallest and greenest low income multi-family residential building on the West Coast and the first new structure in San Diego to earn LEED Gold certification.

The building features photovoltaic and solar thermal panels that create energy from the bright Southern California sunshine for use by the residents.

To conserve water, a necessity in this arid region of the country, each unit features efficient, low-flow water fixtures. More than 90 percent of the units have a view of the city and access to abundant natural light, reducing the amount of energy required during the day. The windows are also energy efficient, improving the temperature efficiency of the building. The mixed-use building features 229 apartments ranging in size from studio to three bedrooms, in addition to 14,000 square feet of retail space. Residents can mingle and relax in the landscaped outdoor common areas on the 7th and 9th Floors, above the base of the building.

Casa Dominguez: Los AngelesLocated on 3.58 acres in the Dominguez Hills area of Los Angeles, Casa Dominguez touts over 98,776 square feet of new construction space with 70 affordable one to four bedroom rental apartments and a Family Development Center. The development earned LEED Platinum certification in 2010 and has been recognised by the Southern California Association of Non Profit Housing with the Multi-Family Project of the Year.

Green elements of the development include the first commercial gray water irrigation system in LA County, an 84.87 kW (DC) solar energy system that will provide 100 percent of the energy for the common areas, high efficiency Low E windows, a ground source heat pump and California-friendly landscaping.

Each apartment unit has Energy Star Appliances in addition to low-VOC paints and floor coverings, recycled content carpets and low-flow water fixtures. Residents are given information and seminars to help them learn to save energy and take advantage of the green initiatives offered by the development.

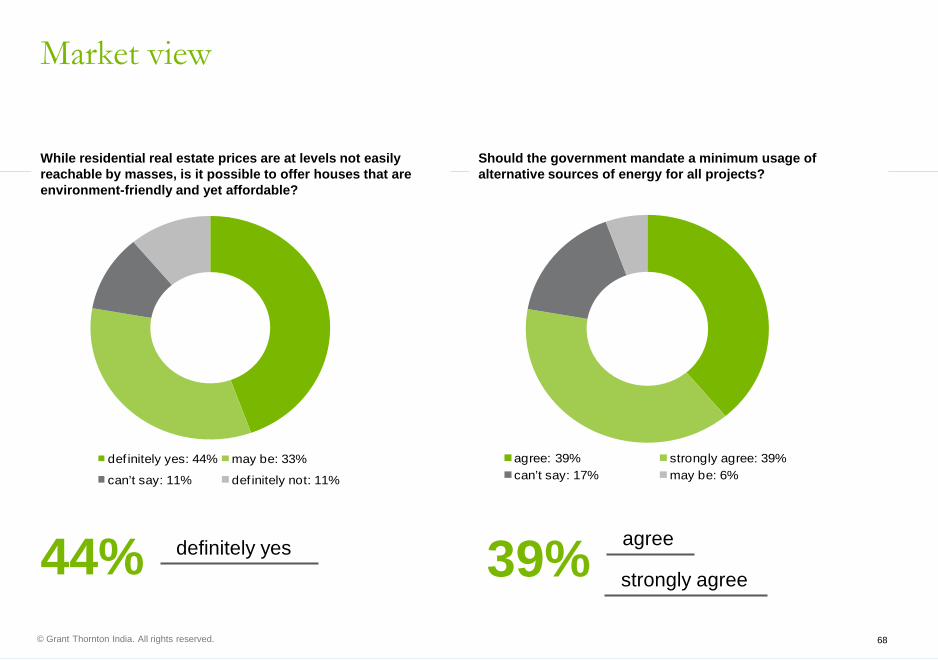

While residential real estate prices are at levels not easily reachable by masses, is it possible to offer houses that are environment-friendly and yet affordable?

Should the government mandate a minimum usage of alternative sources of energy for all projects?

def initely yes: 44% may be: 33%

can’t say: 11% def initely not: 11%