33

Hitachi Capital (UK) PLC Vehicle Solutions Hitachi Capital Vehicle Solutions December 2017 Future of Fuel Report

Hitachi Capital (UK) PLCVehicle Solutions

Hitachi Capital Vehicle Solutions

December 2017

Future of Fuel Report

ForewordWe know that clean air is on the agenda. This year, the Government has been particularly proactive in moving towards legislation to tackle the UK’s pollution problem, with Clean Air Zones set to be introduced in 29 local authorities across England and similar moves being made in Scotland and Wales. In Oxford, the City and County Councils are proposing to create the world’s first Zero Emission Zone. Pressure on businesses to be green has never been greater.

For the automotive industry, technology and cost have long been the limiters on adding pace to the uptake of environmentally friendly vehicles. That is changing, but it appears that we are on the tipping point. The UK government has moved against diesel vehicles with the introduction of tax rises for diesel motorists, while London has now stepped up congestion charges to a new, more expensive ‘T-charge’ for some drivers.

What does it mean for vehicle finance? As readers will discover in this report, there are still a great many concerns from fleet owners about the future, such as work that needs to be done on improving infrastructure, or on the technology of alternatively-fuelled vehicles in general. Addressing those concerns is something that, as a vehicle solutions provider, we look to do through our conversations with the fleet managers that we meet every day.

We’ve been struck by the positive feedback from key figures in the fleet industry, such as Nissan, CNG Fuels, TfL and Cadent. Their opinions in the following pages shed real light on the immediate opportunities with green fuel.

Infrastructure is improving, and going green can save businesses huge amounts of money. Our research has found that, if every van and HGV was powered by electricity, approximately £14 billion could be saved on fuel costs. This is a staggering sum that could then go into other crucial areas such as innovation, jobs, expansion or new kit – the options are many.

If businesses take a long-term decision when it comes to investing in their fleet, it could save significant amounts of time and money. The same can be said for other areas of business, where finance is providing opportunities to invest in green, cost-saving technologies across the board.

For anyone involved in the motor industry, this is a very exciting time, with manufacturers and technologists bringing incredible new ideas to the market constantly. Businesses need to be on the journey to a greener future, and we’re looking forward to working with partners and customers to help them achieve it.

Jon LawesManaging Director, Hitachi Capital Vehicle Solutions

©Hitachi Capital (UK) PLC. 2017. All rights reserved.i

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Commentary by Professor Jonatan PinkseThe opportunity to advance the development and prevalence of alternatively-fueled vehicles (AFVs) has never been greater than it is now. Though technologies such as electrically powered vehicles are not necessarily new, this is the first time that AFVs have received such a great deal of support across the board.

In addition to positive incentives such as subsidies, a significant window of opportunity has opened due to the Government’s increasing focus on policies designed to gradually phase out vehicles with an internal combustion engine.

The future of diesel cars in particular is looking increasingly uncertain, with its toxicity put into sharp focus by the recent Volkswagen scandal, where the company cheated emissions tests and covered up dangerously high levels of pollution. Moves by the Government, such as its intention to ban the sale of petrol and diesel cars by 2040, have also dampened public opinion of the fuel.

It is not just the UK that is beginning to take action, either. France is mirroring the UK’s own target, with a ban to take effect from 2040 – except in Paris, which has brought its target forward to 2030. Similarly, Copenhagen plans to ban all diesel cars as early as 2019.

The bad press for traditional fuels underlines the tremendous opportunity for AFVs to rise in popularity, and their potential to overhaul existing car fleets.

There are drawbacks, such as lingering technological barriers, the limited range of electric vehicles or the current lack of charging infrastructure, for example.

However, the advantages even now far outweigh the disadvantages. My own research has demonstrated that providers of AFVs can begin to overcome many of the initial barriers to adoption by innovating their business models, and particularly their value proposition. Rather than just offering vehicles as a product, the introduction of AFVs allows firms to provide new solutions for mobility in a much broader sense, championing mobility as a service.

Recognising the potential of AFVs as a key component of business strategy, rather than just a method of greening fleets, will be crucial for businesses as we move towards the scrapping of internal combustion engines. With the emergence of innovations such as vehicle-to-everything (V2X) and other connecting technologies, AFVs should not be seen merely as a means of reducing pollution and mitigating climate change – important as this may be. In reality, they are helping in the journey towards making all vehicles smarter and safer.

The key here is that in doing so, businesses will be able to change consumer perceptions of such technol-ogies, demonstrating their value as a green service and simultaneously overcoming the problems inherent with new, disruptive technologies.

This is an exciting moment for AFVs. We are only seeing the tip of the iceberg in terms of the innovation and benefits they are set to bring to businesses and consumers alike in the future.

Jonatan Pinkse is Professor of Strategy, Innovation and Entrepreneurship at the Manchester Institute of Innovation Research, part of Alliance Manchester Business School, University of Manchester.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.ii

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Hitachi Capital Vehicle Solutions Future of Fuel Report 2017This report by Hitachi Capital Vehicle Solutions is ideal for fleet managers who want to:

• Discover what other professionals are thinking. Our survey of fleet managers delivers unprecedented insight into their thinking about alternatively-fuelled vehicles. What are they doing already? What do they intend to do in future? And why? The answers could influence your own plans.

• Understand the available options. The types and models of AFVs are multiplying all the time, from elec-tric saloon cars to gas-powered trucks. This report explains the benefits and drawbacks of each, helping you to decide which AFVs are best suited to your organisation.

• Be up-to-date with the latest legislation. Whether it’s the Government’s Air Quality Plan or London’s Ultra-Low Emission Zone, legislators are currently doing a lot to encourage the uptake of AFVs. Our clear explanations are designed to guide you through this changing landscape.

The information, materials and opinions contained in this report are for general information purposes only. They are not intended to constitute legal or other professional advice, and should not be relied on or treated as a substitute for specific advice relevant to particular circumstances.

All images subject to copyright. The views expressed in this paper are those of Hitachi Capital Vehicle Solutions. Whilst every effort has been made to ensure the accuracy of the information within this document, it is offered as guidance only. Hitachi Capital (UK) PLC does not accept any responsibility for any loss which may arise from reliance on informa-tion or materials in this document.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.iii

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

IntroductionAlternatively-fuelled vehicles (AFVs) are now a feature of British roads. According to the Society of Motor Manufac-turers and Traders (SMMT), 58,657 alternatively-fuelled cars were registered in the first six months of this year, which is 280% higher than four years ago. That’s an astonishing level of growth by any standards.

And that growth is only going to continue. Having barely survived a General Election, Theresa May’s Government recently published its Air Quality Plan (AQP). This plan explicitly aims to replace old, dirty vehicles with cleaner alternatives. Its headline proposal – a total ban on the sale of diesel and petrol cars in the UK by 2040 – is indicative of the direction of travel.

The AQP and various other policies are discussed later on, but the main purpose of this report is to communicate the views of commercial fleets. Hitachi Capital Vehicle Solutions conducted a survey to discover what fleet profes-sionals think about AFVs, and many of the results were heartening. A full 62% of fleets now contain AFVs of some kind. Given that fleets account for over half of all new car sales, this is a great boon for the environment – and for the country as a whole.

It also reflects the growing viability of greener motoring. Manufacturers have played their part in making AFVs make sense for fleets, by creating vehicles that are more powerful, more practical and less costly than they were in the past. Even before the AQP, politicians were doing their bit too. There is now a broad range of government incentives in place to encourage the uptake of cleaner vehicles. No wonder 42% of fleets intend to add more AFVs to their ranks within the next two years.

However, it’s not an entirely happy story. 73% of our respondents feel that the Government could – and should – still be doing more. They are concerned, in particular, about infrastructure. Are there enough charge points for electric vehicles (EVs)? Where are the filling stations for Compressed Natural Gas (CNG) and biodiesel? As we say in our recommendations at the end of this report, these are questions that shouldn’t be ignored.

But even with these uncertainties, we are optimistic. The future is a cleaner place – and, judging by our survey, fleet operators and drivers will do a lot to get us there.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.1

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

ContributorsSuzanne PhillipsNational Fleet ConsultantE: [email protected] Phillips is National Fleet Consultant at Hitachi Capital Vehicle Solutions. A qualified Accountant with over 11 years’ worth of fleet experience, her role includes portfolio evaluation, business strategy development, and consultancy in areas such as funding and taxation.

James BlighNational Sales ManagerSpecialist Asset SolutionsM: 07825 341301E: [email protected] from a farming background, James started his career at Goodyear GB, working in HGV and specialist plant and agriculture markets. Over the past 27 years, James has worked at Dawson Group, Via GTI and BNP Paribas Lease Group. James works in the Specialist Asset Solutions team at Hitachi Capital Vehicle Solutions, focusing on HGV and specialist plant leasing.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.2

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Contents and main findings

1. The rise of AFVsThe number of alternatively-fuelled car registrations has risen by 280% over the last four years. Many of these have found their way into fleets. 62% of fleets contain AFVs.

2. Electric and hybridElectrics and hybrids are the most familiar types of AFV on our roads. They are the most prevalent among fleets too. 22% contain electric vehicles, and 46% contain hybrids.

3. GasOnly 4% of fleets contain a vehicle fuelled by CNG. But that low proportion doesn’t mean that gas isn’t useful. It is increasingly attractive for hauliers whose vehicles can’t be powered by electricity.

4. BiodieselDiesel has got a bad name recently, but not all diesels are created equal. 82% of the UK’s biodiesel comes from used cooking oil, making it a particularly environmentally-friendly fuel.

5. Fleet thinking82% of fleet professionals believe that it is important for fleets to move towards AFVs. This is what many of them are doing: 42% of fleets plan to add new AFVs in the next two years. However, 28% of respondents said that their organisation should be doing more.

6. The obstaclesFleet managers name infrastructure and vehicle costs as the biggest obstacles in the way of AFVs. But they have other concerns too, including electric vehicle range, and the availability of suitable gas and biodiesel vehicles.

7. The policyClean Air Zones are among the latest policies designed to encourage the uptake of AFVs, and 65% of fleet professionals believe that they will work. However, there’s scepticism about the Government’s actions more generally. 73% say that more needs to be done to meet emissions targets.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.3

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

1. The rise of AFVsClimate change is one of the great concerns of our age. It has prompted governments around the world to work to reduce carbon dioxide (CO2) emissions, and companies have followed suit. Going green is now one of the most important aspects of corporate social responsibility.

Transport has been a major focus of these efforts. Cars and other vehicles are responsible for a quarter of the UK’s greenhouse gas emissions, so making them cleaner is essential. Manufacturers have recognised this and have made great strides towards improving fuel efficiency. The average new petrol car is now 36% cleaner than it was a decade ago.

But improving existing fossil fuel vehicles isn’t the whole solution. Manufacturers have also been working on low-carbon alternatives, powered by everything from hydrogen to vegetable oil. Indeed, Volvo recently announced that it will not make any pure petrol or diesel cars after 2018. Governments have also introduced various policies to encourage the uptake of AFVs. These vehicles and these policies are detailed throughout this report.

The shift towards AFVs has been made more urgent by recent concerns about diesel. It was once thought that diesel vehicles were a cleaner option than petrol ones, as they generally produce less CO2. However, scientists and policymakers have become increasingly worried about the other pollutants, such as nitrogen oxides (NOx), that diesel engines emit. These pollutants are particularly harmful for people.

When it comes to CO2 and NOx emissions, there are differences between different forms of AFV. But AFVs are, on the whole, much cleaner than their traditional counterparts. All trends are moving in their direction.

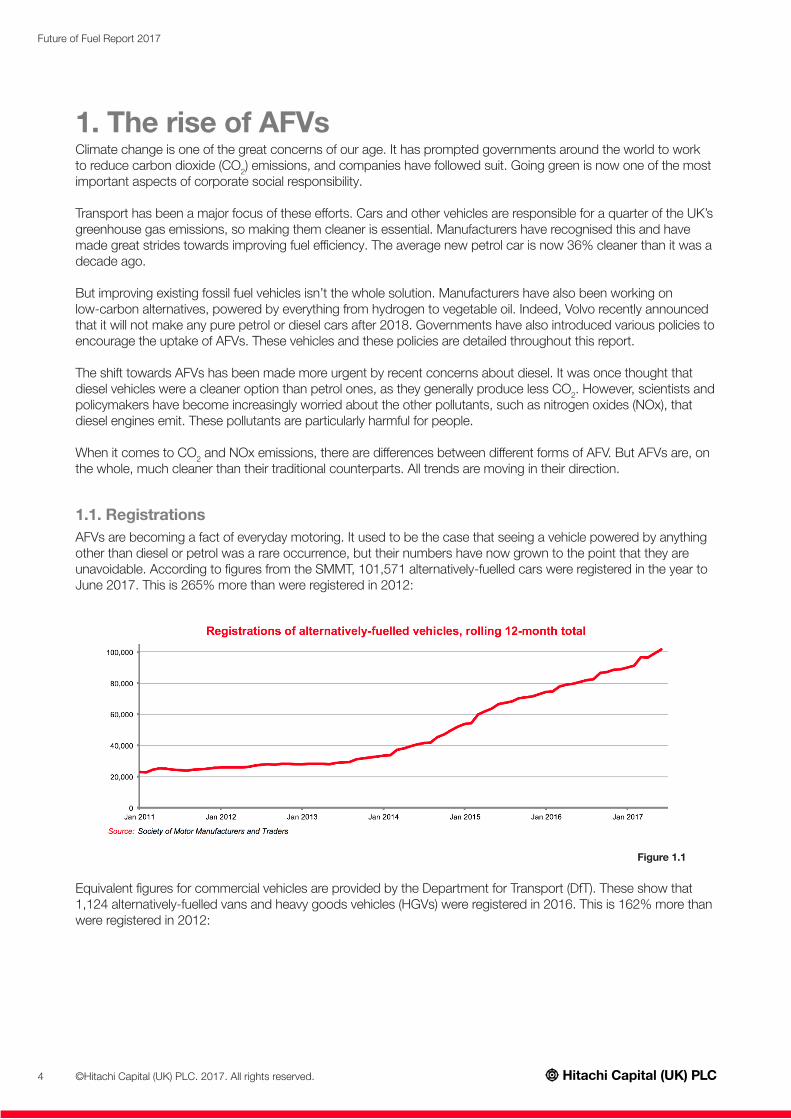

1.1. RegistrationsAFVs are becoming a fact of everyday motoring. It used to be the case that seeing a vehicle powered by anything other than diesel or petrol was a rare occurrence, but their numbers have now grown to the point that they are unavoidable. According to figures from the SMMT, 101,571 alternatively-fuelled cars were registered in the year to June 2017. This is 265% more than were registered in 2012:

Figure 1.1

Equivalent figures for commercial vehicles are provided by the Department for Transport (DfT). These show that 1,124 alternatively-fuelled vans and heavy goods vehicles (HGVs) were registered in 2016. This is 162% more than were registered in 2012:

©Hitachi Capital (UK) PLC. 2017. All rights reserved.4

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Figure 1.2

1.2. Fleet take-upThese trends are borne out by Hitachi Capital Vehicle Solutions’ survey of fleet professionals. A remarkable 62% now have alternatively-fuelled vehicles in their fleets.

Hybrid electric vehicles are the most popular form of AFV in the fleets we questioned. 46% of fleets currently use them, while 22% contain electric vehicles. Other forms of alternative fuel are currently less prevalent. 7% of fleets use biodiesel, 4% pure Compressed Natural Gas (CNG), 3% dual-fuel CNG, and 3% Liquefied Natural Gas (LNG).

Figure 1.3

Each type of alternative fuel, along with their benefits and challenges, will be explored in subsequent chapters.

1.3. AFVs in EuropeThe rise is happening across Europe, too. Figures from the International Council on Clean Transportation show that 4% of all new cars registered in the European Union (EU) in 2015 were AFVs, up from just 0.3% in 2005. That 4% was made up of: 1.5% Hybrid Electric Vehicles (HEVs), 1.5% natural gas vehicles, 0.6% Plug-in Hybrid Vehicles (PHEVs), and 0.4% Battery Electric Vehicles (BEVs) or Hydrogen Fuel Cell Vehicles (FCVs).

Two EU countries stand out as having particularly large numbers of AFVs: Italy and the Netherlands. In each of these countries, AFVs accounted for 13% of all new cars in 2015. In Italy, this is due to a high number of natural gas vehicles, while the Netherlands has far more PHEVs than the rest of Europe.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.5

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Figure 1.4

As a result, the Netherlands has done more than most other European countries when it comes to reducing CO2 emissions from transport. Average CO2 emissions of new cars in the Netherlands fell by 40% from 2005 to 2015, compared to the 25% fall achieved by the rest of the EU in the same period.

Beyond the EU, Norway is the clear leader in AFVs. 17% of all new cars registered there in 2015 were BEVs or FCVs, 5.3% were PHEVs and 7.1% were HEVs.

Whilst trends in the UK are encouraging, this shows that we could still go a lot further.

1.4 Future technologiesFor the most part, this report is about today’s AFVs and the policies around them. However, the automotive industry is moving so quickly that the future cannot be ignored. Here are some of the technological developments to look out for in coming years:

Better batteriesBroadly speaking, advances in battery technology are being made in two ways: efficiency and space. Lithium-oxygen batteries are an example of the former – they could be between 5 and 15 times more efficient than the lithium-ion batteries that currently power electric vehicles. The work of the German research group Fraunhofer is an example of the latter – they are developing new ways of stacking batteries that should enable more to be fitted within a car.

Wireless chargingThe idea of using inductive technology to charge electric vehicles wirelessly, as they drive along the road, is not a new one. Trials have been performed around the world, including in the UK, whilst some countries have gone even further. South Korea already has several wirelessly-charged bus routes. Israel is planning to open its own – a half-mile route in Tel Aviv – next year. The question is not whether wireless charging is possible, but whether it can be introduced cost-effectively across large areas.

Autonomous vehiclesIt’s not necessary for autonomous vehicles to be AFVs, but many of those in development are. For example, Waymo – formerly Google’s self-driving division – has recently moved to Chrysler Pacifica hybrids for testing its technology. Tesla has also confirmed that its latest electric cars are all fitted with the necessary hardware for full autonomous driving, pending a software update in future.

New alternativesOther alternative fuels, such as biobutanol, already exist. Scientists are likely to develop more in future. These alternatives will struggle to be noticed in a marketplace that is increasingly electric – but, as recent automotive history has shown, nothing should be dismissed prematurely.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.6

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

2. Electric and hybridElectric and hybrid vehicles are the most familiar and prevalent types of AFVs, particularly among car and van drivers. They are all powered by electricity; although to differing extents and in different ways, depending on their type. The main types of electric and hybrid vehicle are:

2.1. A typologyHybrid Electric VehicleThis is a vehicle powered by a traditional internal combustion engine (ICE) – either petrol or diesel – as well as an electric battery. The battery is charged using excess energy from the ICE, as well as by reclaiming the car’s kinetic energy when it brakes. The use of electricity allows a hybrid to achieve much better fuel economy, and therefore lower emissions, than a traditional ICE vehicle.

The most popular HEV in Britain is the Toyota Prius – a petrol-electric hybrid. It can do 94 miles per gallon (mpg), compared to 52mpg for the average new petrol car, and produces just 70 grams of CO2 per kilometre (g CO2/km), compared to 124g CO2/km for the average new petrol car. Similarly, the Hyundai Ioniq HEV can manage around 80mpg and emits 79g CO2/km.

Battery Electric VehicleThis is a vehicle powered entirely by an electric battery, which is charged by plugging it in. They emit no CO2, although CO2 is of course emitted producing the electricity that charges them.

The most popular BEV in the UK is the Nissan LEAF, which can travel up to 235 miles on a single charge. Others can go even further before needing to be recharged: the Renault Zoe has a range of 250 miles, while for the Tesla Model S 75 it’s 300 miles.

There are also Battery Electric vans. The Nissan e-NV200 Van, the Renault Kangoo Z.E. and the Peugeot Partner Electric can all travel up to 106 miles on a single charge. The newly-announced e-NV200 with a 40kWh battery is reported to have a range of up to 173 miles between charges.

Plug-in Hybrid Electric VehicleThis is a vehicle that has both an ICE and a plug-in electric battery. At any time, it can be running on the battery alone, on the ICE alone, or on a combination of the two like a HEV.

The UK’s most popular model is the Mitsubishi Outlander PHEV, which can travel 166mpg and emits 41g CO2/km. The next most popular PHEV is the Mercedes-Benz C 350 e, which can do 135mpg and emits 48g CO2/km.

This category also includes ‘range extended’ versions of BEVs such as the BMW i3 REx. These are BEVs fitted with an additional, small petrol engine to generate electricity when the battery’s charge is too low. The i3’s range extender increases its range on a single charge from 125 miles to 206 miles using the petrol engine.

Our consultants say…‘Plug-in hybrids provide a gentle entry to the world of electric vehicles for many fleets and their employees. To maximise their financial benefits, an accurate journey analysis needs to be completed alongside a full cost-of-ownership analysis.’

‘The days of fleet operators using vehicles that run on one fuel type have passed. Fleet managers will, in future, operate a mixed range of AFVs to meet the operational demands of their businesses.’ – Colin Marriott, Fleet Consultant

‘There are few better ways for a company to demonstrate its commitment to the environment than turning up to meetings in an electric car. It can make a big positive impression.’ – Karl Anders, National EV and Public Sector Manager, Nissan

©Hitachi Capital (UK) PLC. 2017. All rights reserved.7

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Hydrogen Fuel Cell VehicleThis is an electric vehicle that uses a hydrogen fuel cell, instead of a battery, to generate electricity. FCVs emit no CO2 – only water – although most of their hydrogen comes from natural gas, and CO2 is emitted in the production process. They generally have lower overall energy efficiency than BEVs, but a much greater range. Refilling a hydrogen tank also takes much less time than recharging a battery.

Only two FCVs are currently available in the UK: the Hyundai ix35 FCEV and the Toyota Mirai. The Honda Clarity is also due to go on sale this year. All three models can travel more than 300 miles on a single tank of hydrogen.

Some vans and even HGVs have been converted to dual-fuel vehicles, running on both diesel and hydrogen.

2.2. Registrations of electric and hybrid cars

Figure 2.1

Hybrid cars are the most popular form of AFV. 61,791 were registered in the year to June 2017, representing 61% of all new AFV registrations. Almost all (98%) of these were petrol-electric hybrids, and registrations of diesel-electric hybrids have fallen by 37% in the last year.

27,066 PHEVs were registered in the year to June, up 17% on the previous 12 months. For BEVs, the number was 12,691 – a 21% increase.

2.3. Electric HGVsThe power and weight of batteries has been an impediment to the development of electric HGVs. However, this situation is changing and more electric HGVs are coming onto the road. Mercedes, Tesla and the British company Tevva are among those who have recently announced their own models. In fact, Tevva isn’t just building its own battery-powered trucks – it already converts existing ones to run on electricity. Their technology has already been trialled successfully. The 7.5-tonne Tevva demo-truck can travel 100 miles with zero emissions, and has the potential for 300 miles with a range extender.

2.4. Survey findingsCars and vans are by far the most popular form of electric vehicle. 13% of fleets in our survey include electric cars, and 9% contain electric vans. By contrast, just 2% use electric specialist vehicles, and only 1% have electric HGVs.

Even where electric cars and vans are used, they rarely make up a large proportion of the fleet. In just 3% of fleets are more than 10% of cars electric, and in just 1% are more than 10% of vans electric.

13% of fleets contain electric cars.42% of fleets contain

hybrid cars.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.8

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Almost all hybrid electric vehicles in fleets are cars. 42% of fleets surveyed contain hybrid cars, whereas only 3% contain hybrid vans and just 1% have hybrid HGVs or specialist vehicles.

In 13% of fleets, more than 10% of cars are hybrids. However, hybrids make up a majority of cars in just 2% of fleets.

Our consultants say…‘There are so many different factors affecting the overall cost of AFVs – from acquisition costs to maintenance and fuel costs – that working it all out can be challenging for fleets. A good fleet data supplier, such as Hitachi Capital Vehicle Solutions, can provide a benchmark cost-per-mile that can be used to evaluate the potential benefits of each type of AFV.’

How we helped British Gas go electric

British Gas came to Hitachi Capital Vehicle Solutions with a challenge. They wanted to reduce the emissions of their van fleet whilst saving money and maintaining safety and reliability. Together, we explored the potential of electric vans. This began with us reaching out to the manufacturer Nissan. They delivered ten hand-built, pre-production prototypes from Japan that had been modified to meet the needs of British Gas. This was the first time that any manufacturer had given a leasing company and its client access to pre-pro-duction vehicles. These vehicles were put through a rigorous pilot. Drivers were selected and then provided with home charging points, special training and 24-hour telephone support. Their feedback, along with the data from various tests and inspections, led us to make further improvements. For example, white noise generators were added so that pedestrians could hear the vans at low speed. Alongside this, Hitachi Capital Vehicle Solutions developed a ‘total cost of ownership’ model to show that the vans weren’t just road-effective but cost-effective too.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.9

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

3. GasVehicles can be powered by gas – either natural gas (which predominantly consists of methane, and can come either liquefied or compressed) or Liquefied Petroleum Gas (LPG, which is mostly propane).

Petrol cars can be converted to run on gas, and most are dual-fuel: they can be powered by either gas or petrol. Engines have also been developed to allow HGVs to run on gas. These can either be pure LPG, LNG or CNG vehicles, or dual-fuel HGVs that run on both gas and diesel.

Gas vehicles generally emit less CO2 than their petrol equivalents, and although they also emit methane, their total greenhouse gas emissions are less than petrol and roughly equivalent to diesel. They emit less NOx and other air pollutants than diesel, however, making them cleaner than traditional fuels overall.

3.1. Bio-CNGWhereas natural gas traditionally came from the ground like oil, it can also be produced from food and other waste. When compressed, this renewable biomethane is known as Bio-CNG and can be used to power any kind of vehicle.

The environmental benefits of Bio-CNG are much greater than for other gas vehicles, as the waste used to produce the fuel would otherwise decompose and emit methane. Vehicles that run on Bio-CNG do emit CO2, but this has a much lower global warming potential than the methane that is avoided.

Currently, around 120 HGVs in the UK run on Bio-CNG or a dual-fuel combination of Bio-CNG and diesel – and that number is growing rapidly.

3.2. Survey resultsOur survey reveals that relatively few fleets currently use natural gas. Just 4% contain pure CNG vehicles, while 3% have dual-fuel CNG vehicles and 3% have ones that run on LNG.

Those fleets that do use gas generally use it to power HGVs and specialist vehicles, rather than cars and vans. 3% of fleets run the majority of their HGVs on gas.

‘CNG can be used for any vehicle: passenger cars, vans, trucks, buses, refuse vehicles or anything else, really. In theory, any vehicle that runs on petrol or diesel could, today, run on gas.’ – Philip Fjeld, CEO, CNG Fuels

‘There’s been an expansion in the availability of gas vehicles. Run on biomethane, these vehicles can offer substantial greenhouse gas savings.’ – Fergus Worthy, Project Manager for Freight & Fleet, Transport for London (TfL)

‘We set Hitachi Capital Vehicle Solutions the challenge of creating a vehicle powered by our own product, gas. They delivered the world’s first Mercedes Antos that runs on CNG and diesel. We’re delighted with the fuel savings and emissions reductions that resulted from it – and have now ordered more for our fleet.’ – David XXXX, XXXX, Cadent

3%of fleets use gas for the majority

of their HGVs.

‘Vehicles powered by Bio-CNG offer tremendous air quality benefits and lower fuel costs. They are also 50% quieter than diesel vehicles, and can cut CO2 emissions by more than 80%.’ – Philip Fjeld

©Hitachi Capital (UK) PLC. 2017. All rights reserved.10

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

4. BiodieselVegetable oil and animal fats are used to power vehicles, in the form of biodiesel.

Biodiesel is usually blended with normal petroleum diesel: for example, ‘B10’ is a blend of 10% biodiesel and 90% petroleum diesel. Blends with a low proportion of biodiesel can be used in standard diesel engines without modifi-cation, but vehicles may require modifications to run on purer forms of biodiesel.

4.1. The environmental benefitsAlthough it produces CO2 when combusted, biodiesel is better for the environment than traditional fossil fuels because the plants used in its production also absorb CO2 – so its life-cycle emissions are lower.

On average, switching from fossil fuels to biodiesel reduces greenhouse gas emissions by 85%.

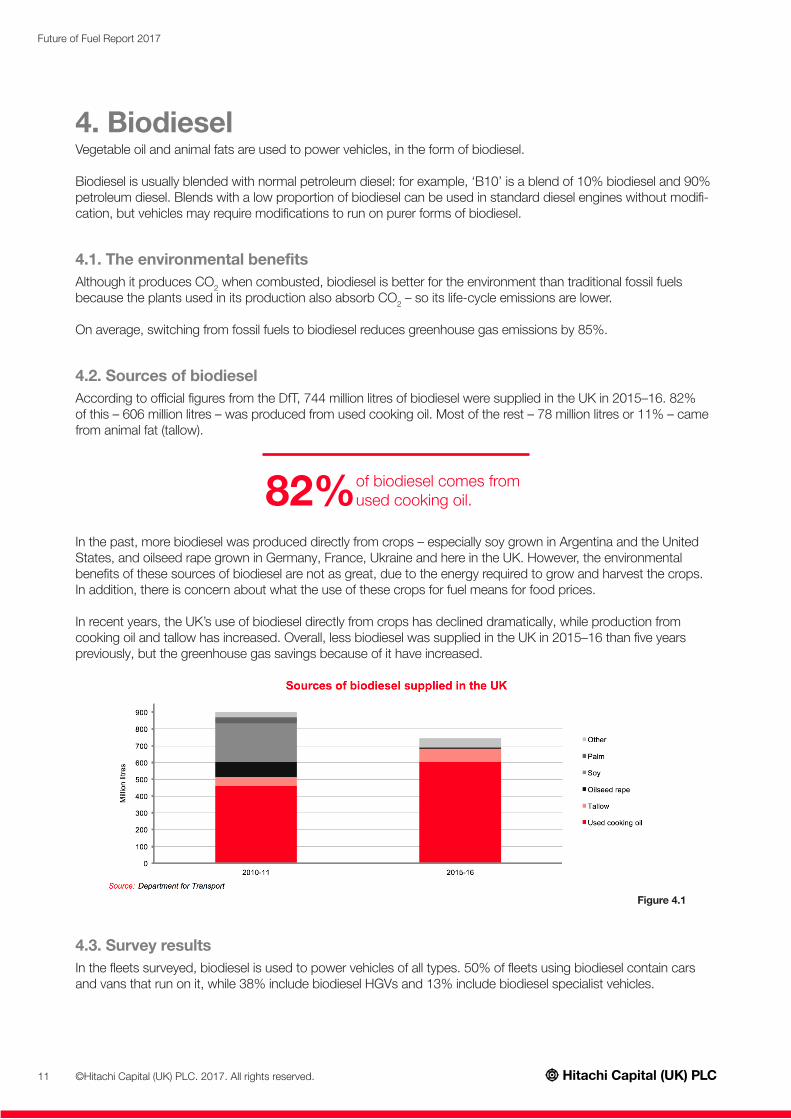

4.2. Sources of biodieselAccording to official figures from the DfT, 744 million litres of biodiesel were supplied in the UK in 2015–16. 82% of this – 606 million litres – was produced from used cooking oil. Most of the rest – 78 million litres or 11% – came from animal fat (tallow).

In the past, more biodiesel was produced directly from crops – especially soy grown in Argentina and the United States, and oilseed rape grown in Germany, France, Ukraine and here in the UK. However, the environmental benefits of these sources of biodiesel are not as great, due to the energy required to grow and harvest the crops. In addition, there is concern about what the use of these crops for fuel means for food prices.

In recent years, the UK’s use of biodiesel directly from crops has declined dramatically, while production from cooking oil and tallow has increased. Overall, less biodiesel was supplied in the UK in 2015–16 than five years previously, but the greenhouse gas savings because of it have increased.

Figure 4.1

4.3. Survey resultsIn the fleets surveyed, biodiesel is used to power vehicles of all types. 50% of fleets using biodiesel contain cars and vans that run on it, while 38% include biodiesel HGVs and 13% include biodiesel specialist vehicles.

82%of biodiesel comes from used cooking oil.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.11

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

5. Fleet thinkingOur survey reveals that fleet professionals understand the important role alternative fuels have to play. Most of them are researching alternatives to petrol and diesel for their vehicles, and a large number plan to add more AFVs to their fleets in the coming months and years. However, only a minority believe that their organisation is doing enough in this area, and many say they should be doing more.

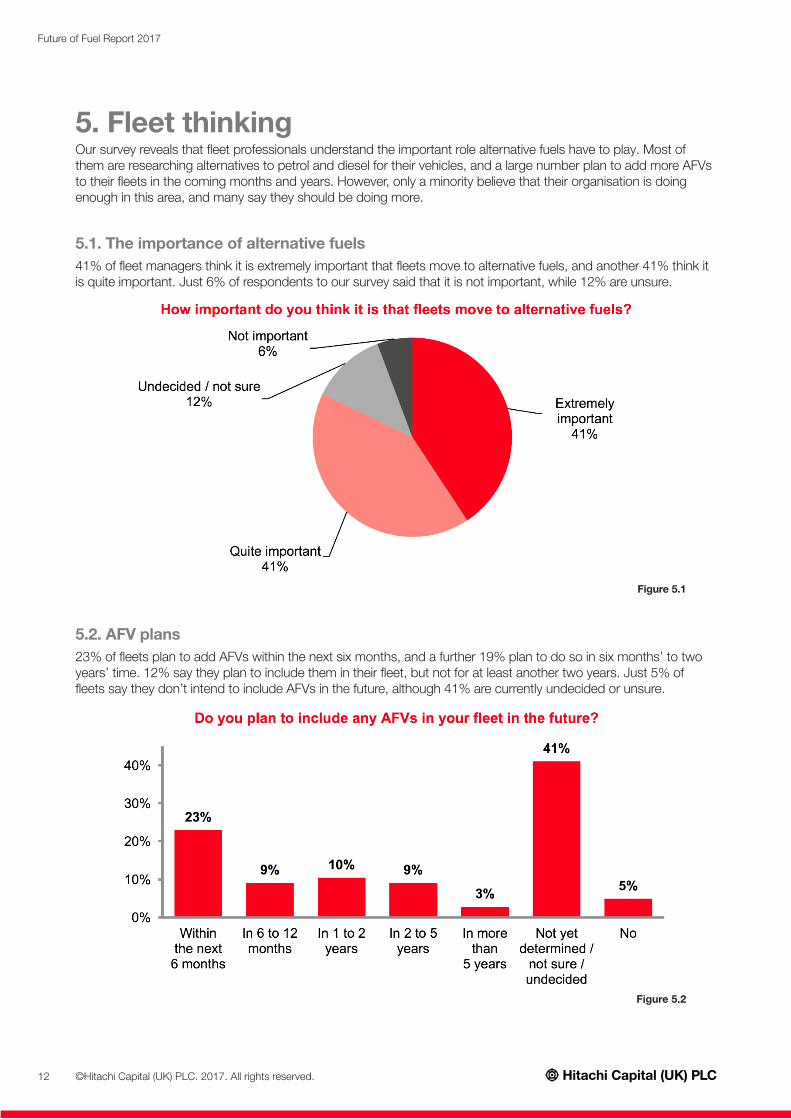

5.1. The importance of alternative fuels41% of fleet managers think it is extremely important that fleets move to alternative fuels, and another 41% think it is quite important. Just 6% of respondents to our survey said that it is not important, while 12% are unsure.

Figure 5.1

5.2. AFV plans23% of fleets plan to add AFVs within the next six months, and a further 19% plan to do so in six months’ to two years’ time. 12% say they plan to include them in their fleet, but not for at least another two years. Just 5% of fleets say they don’t intend to include AFVs in the future, although 41% are currently undecided or unsure.

Figure 5.2

82%of fleet professionals

believe that alternative fuels are important for the future.

42%of fleets plan to add new AFVs

in the next two years.

28%of respondents say their

organisations should be doing more to move to AFVs.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.12

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

The majority (55%) of organisations planning to add AFVs in the next six months already have some in their fleets. Nevertheless, more than a quarter of fleets without any AFVs at the moment do plan to add some within the next six months.

5.3. The steps fleets are taking30% of fleet managers say that their organisation is taking adequate steps towards AFVs, but 28% say they should be doing more. Just 10% say they see no advantage in AFVs and so are not taking them up, but 15% say other pressures on their business are more important.

Figure 5.3

5.4. Research into alternative fuelsAlmost all (95%) of those fleet professionals who say their organisations ‘should be doing more’ are researching AFVs. Most of this research is around alternative fuels for cars and vans, though, with relatively little for HGVs and specialist vehicles. 64% of respondents are researching alternatively-fuelled cars, and 56% alternatively-fuelled vans.

Figure 5.4

Only 15% are researching alternative fuels for HGVs and just 3% are doing the same for specialist vehicles.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.13

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

6. The obstaclesWhat difficulties do fleets face when adopting alternative fuels? What obstacles are preventing more organisations from making the switch? Our survey found that infrastructure and vehicle costs are concerns for fleet professionals in relation to all types of AFV, but it also revealed certain problems particular to each fuel.

The first section of this chapter sets out the survey results, and subsequent sections consider each of the three biggest obstacles to the take-up of AFVs.

6.1. Survey findings

Figure 6.1 The most frequently-mentioned concern about adopting electric and hybrid vehicles is range – cited by 62% of those fleet managers who are not currently planning to use more AFVs in the coming months and years.

Figure 6.2

Infrastructure is a significant concern for many fleets when considering switching to AFVs. 38% of respondents cite it as a barrier to adopting electric and hybrid vehicles, 51% say it’s preventing them choosing CNG and LNG vehicles, and 42% say it’s a problem for biodiesel vehicles.

‘TfL will install 150 rapid charge points by the end of 2018 and at least 300 by 2020. This will help alleviate concerns over range and infrastructure.’ – Fergus Worthy

‘A lot of it is psychological: people think that they need a much longer range than they actually do, and they worry about going somewhere without a charge point. As ranges increase, that’s becoming less of a problem, but those worries are still a barrier to take-up.’ – Karl Anders

©Hitachi Capital (UK) PLC. 2017. All rights reserved.14

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Vehicle cost is another major barrier to the uptake of AFVs. It’s cited by 52% of respondents in relation to electric and hybrid vehicles, 45% in relation to CNG and LNG, and 36% in relation to biodiesel.

The availability of suitable vehicles – or lack thereof – is preventing many fleet managers from switching to gas or biodiesel. However, this is less of a concern when it comes to electric and hybrid vehicles.

Figure 6.3

6.2. RangeWhile not an issue for vehicles that run on gas or biodiesel, range is the most prominent concern for fleet profes-sionals when it comes to electric and hybrid vehicles. This is nothing new. So-called ‘range anxiety’ is a fear that manufacturers have long been attempting to combat.

In recent years, advances in battery technology have greatly extended the distance that battery electric vehicles can drive on a single charge. Most models of battery electric car can now manage 100 miles or more before needing to be plugged in.

Given that the average car journey is just 9 miles long, and 98% of trips cover less than 50 miles, these ranges are more than adequate for most drivers, most of the time. However, for fleets whose drivers regularly undertake longer journeys, PHEVs or FCVs offer longer ranges.

6.3. InfrastructureInfrastructure was cited as an obstacle most often in relation to CNG and LNG. However, it was also mentioned by significant numbers of fleet professionals in relation to all other types of AFV: electric, hybrid and biodiesel.

Most fleets with HGVs running on CNG fill them up at their depots. This may require significant investment for large fleets, and is unlikely to be a practical option for small ones.

However, CNG Fuels has also opened public filling stations, including one in Leyland that is the first to be connected to the high-pressure gas grid. It opened in March 2016, and can refuel 500 lorries a day. More such filling stations are planned for the coming years, making CNG a realistic option for more fleets.

For fleets that are adding BEVs and PHEVs, the Government’s Workplace Charging Scheme offers vouchers worth £300 for each of the first 20 charging sockets businesses install. In his Autumn Statement in November 2016, Philip Hammond introduced extra support for businesses installing charge points, in the form of a new 100% First-Year Allowance available until April 2019.

In Autumn Budget 2017, the Chancellor also established a new £400 million Charging Investment Infrastructure Fund.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.15

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

There are now more than 13,000 public charge points around the UK’s road network. 2,300 of these are rapid chargers capable of bringing a battery up to 80% charge in just 30 minutes, and at least one of these can be found at 96% of motorway service stations. Many public charge points do require users to subscribe to their provider, though fees are relatively low, and sometimes free.

The Government plans boost the number of charge points further by giving itself the power to require motorway service stations and other large fuel retailers to install charge points. This measure forms part of the Automated and Electric Vehicles Bill, which is currently working its way through Parliament.

The number of public hydrogen filling stations is also growing. There are currently only around a dozen of them, mostly in London and the South East. More are due to open, though, including on existing petrol station forecourts.

Figure 6.4

6.4. Vehicle costThe higher sticker price associated with all types of AFV is an understandable concern for many fleet professionals. CNG trucks, for example, can cost £25,000–£30,000 more than their diesel counterparts. However, costs are coming down – particularly in the case of electric and hybrid vehicles – as the technology develops and larger numbers are manufactured.

And the upfront cost is only one element of a vehicle’s whole life costs. Fleets should also consider fuel costs, tax implications and Government grants – all of which argue in favour of AFVs.

The prices of petrol and diesel rose sharply during 2016 – by 15% and 13% respectively – making alternative fuels even more attractive by comparison. Electricity is not subject to fuel duty and costs only about 2 pence per mile for cars, compared to 10 to 12p for petrol or diesel. Meanwhile, Bio-CNG is around 40% cheaper than diesel. Research by Hitachi Capital Vehicle Solutions has found that, if every van and HGV was powered by electricity, businesses could save an estimated £14 billion on fuel costs.

The Government has introduced a number of incentives for low-emission vehicles, such as the Plug-in Car Grant for electric vehicles and lower Vehicle Excise Duty (VED) and Company Car Tax (CCT) rates for cleaner cars. These are explained in more detail in the following chapter.

Our consultants say…‘Using an experienced and knowledgeable supply partner to calculate real-world running costs is critical to understanding the actual total cost of ownership through the vehicle’s lifecycle. Through our work with British Gas and others, Hitachi Capital Vehicle Solutions has gained a thorough understanding of these costs for every fuel and asset type, and every part of the country.

‘It is important to remember that both journey type and driving style affect the relative costs of AFVs. Using data from driver questionnaires and telematics, Hitachi Capital Vehicle Solutions’ experts can help organisa-tions to choose the right vehicle for the right journey and driver.

‘Driver training is a fundamental part of improving fuel consumption, reducing both costs and emissions. Telematics can also be used to plan jobs and route more efficiently, thereby reducing operational mileage.’

‘Even for conventional vehicles, fleets should base their decisions on total cost of ownership rather than upfront cost. Many alternatively-fuelled vehicles are cheaper to run than a diesel equivalent, so the total of cost ownership can be attractive.’ – Fergus Worthy

©Hitachi Capital (UK) PLC. 2017. All rights reserved.16

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

7. Government policyPolicymakers at both local and national levels have introduced a range of measures to combat climate change and tackle air pollution. Many of these are designed to incentivise greener motoring, either by placing extra charges on dirtier vehicles or by reducing the cost of cleaner ones.

7.1. Air Quality PlanThe Government’s latest AQP has been a long time coming. In fact, the story of its publication stretches back to 2011. That’s when the Coalition Government released a plan in response to the UK breaching its EU-mandated NO2 limits the previous year. (See section 7.4 for more information about these limits.) However, the environ-mental group ClientEarth argued that this plan was insufficient, and, in 2015, the Supreme Court agreed with them. The Government was ordered by the Court to draw up a new plan.

This second plan was published by the new Conservative Government in December 2015, but it too met with disapproval. ClientEarth successfully challenged it in the High Court, and the Government was told to produce the draft for a third plan by 24 April 2017, and then the finished document by 31 July 2017. Theresa May and her ministers tried to have these deadlines extended – on the grounds that the Government had to enter a period of silence, or ‘purdah’, ahead of the snap election – but their appeal was denied. The final plan would have to be published by 31 July.

And so it was. The new AQP was released on 26 July 2017. Its most prominent proposal was a total ban on the sale of new diesel and petrol vehicles by 2040 – however, this probably sounds more radical than it actually is. 2040 is, after all, 23 years away. If manufacturers and consumers continue to buy into AFVs as they have been doing, then petrol and diesel cars could be superseded before that date, anyway. A de facto ‘ban’ might come into force ahead of a de jure one.

Aside from the ban, the AQP’s main proposal was an expansion of Clean Air Zones (CAZs). We discuss these fully in section 7.2, below, although it is worth noting now that CAZs will largely be the responsibility of local authorities. Their introduction, as well as the policies that will apply within them, may well differ from area to area.

A number of other policies were mooted ahead of the publication of the AQP. One of these was a scrappage scheme that would help diesel motorists move from their current vehicles to cleaner alternatives. However, on its publication, the AQP neither confirmed nor denied the policy. Instead, a scrappage scheme – along with other compensatory measures, such as discounted bus travel – will be put up for consultation in the autumn.

The AQP was similarly inconclusive about the possibility of further tax hikes for diesel vehicles, advising readers to wait for Autumn Budget 2017. That Budget revealed that, as of April 2018, diesel cars will be subject to both higher first-year VED rates and a 4-percentage-point supplement to CCT. Exemptions were made for cleaner diesel cars and all vans.

Our consultants say…‘Organisations must prepare for the impact of the Air Quality Plan, with several cities already planning to restrict older diesel vehicles from entering their Clean Air Zones, or charge them to do so. Working with a fleet partner to understand how Clean Air Zones will affect costs and asset utilisation is a good place to start.’

7.2. Clean Air ZonesA form of CAZ already exists, although it doesn’t go by that name. Most of Greater London has been a ‘Low Emission Zone’ since 2008. Vans larger than 1,205kg that do not meet Euro 3 emissions standards face a £100-a-day charge to drive within it, whilst lorries over 3,500kg that do not meet Euro IV must pay £200 a day.

Mayor of London Sadiq Khan introduced a new ‘T-Charge’ in October 2017. Vehicles that do not meet Euro 4 emission standards will have to pay £10 a day extra to drive in the existing congestion charge zone in central London.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.17

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

In April 2019, that area will become an Ultra-Low Emission Zone (ULEZ). Diesel vehicles that do not meet Euro 6 emission standards will have to pay to drive in the zone, as well as petrol vehicles that don’t meet the Euro 4 standards. The charge will rise to £12.50 a day for cars, vans and motorbikes, while buses, coaches and HGVs will face a £100-a-day charge.

Khan is already looking to go further than his current ULEZ proposals. His recent Draft Transport Strategy – which has also been put forward for consultation – includes an ambition for London to have a zero-emission transport system by 2050. This could involve the introduction of a Zero Emission Zone.

To some extent, the national Government wants London’s lead to be followed elsewhere. One of the major proposals in the AQP was a roll-out of CAZs in the 29 areas with the worst air pollution problems, including Manchester, Birmingham and Leeds. The Government will order the corresponding local authorities to implement new measures to reduce harmful emissions, but will leave it up to each council to decide the specific mix of policies that will apply in its area.

The 29 councils will have to reveal their CAZ plans by the end of 2018. These could include cutting emissions from public transport, such as by retrofitting buses, as well as reducing congestion by improving road layouts, changing speed bumps and reprogramming traffic lights. The Government has announced a new £255 million ‘Implemen-tation Fund’ to help councils draw up and deliver their plans.

However, the Government isn’t eager to see London-style charges within these CAZs. As the AQP puts it: ‘the UK government believes that if a local authority can identify measures other than charging zones that are at least as effective at reducing NO2, those measures should be preferred as long as the local authority can demonstrate that this will deliver compliance as quickly as a charging Clean Air Zone.’

43% of fleet managers think the rollout of London’s ULEZ and other Clean Air Zones is a good idea. 28% regard it as inconvenient but necessary, while just 9% say it’s a bad idea. 15% say it doesn’t affect their organisation.

Figure 7.1

65%of fleet managers say

Clean Air Zones will make them more likely to use AFVs.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.18

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

25% of fleet managers say that hearing about the proposed rollout of Clean Air Zones makes them a lot more likely to use AFVs, while 40% say it makes them a little more likely to do so. Meanwhile, 34% say it will have no impact on their decisions.

Figure 7.2

Our consultants say…‘“Inconvenient but necessary” sums up the fleet industry’s reaction to Clean Air Zones. Hitachi Capital Vehicle Solutions has been working with our customers for many years to prepare them for the introduction of these zones, and is well-placed to help organisations to rapidly integrate these changes into their fleet policies.’

7.3. Greenhouse gas emission targetsThe UK’s efforts to reduce CO2 emissions are governed by the Climate Change Act of 2008. This introduced a specific target: the country’s greenhouse gas emissions should be 80% below their 1990 levels by 2050.

So, how are we doing? A snapshot of the data suggests that considerable progress is being made. According to provisional figures from the Department for Business, Energy & Industrial Strategy, the UK’s greenhouse gas emissions in 2016 totalled 466 million tonnes CO2 equivalent (MtCO2e) – 42% below the 1990 baseline.

However, other data is less encouraging. For example, emissions from the transport sector have actually increased slightly since 1990 – by 0.5%. In 2016, transport accounted for 26% of all greenhouse gas emissions.

Figure 7.3

©Hitachi Capital (UK) PLC. 2017. All rights reserved.19

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

What’s more, progress may stall in future. As part of the 2008 Act, the Government introduced legally-binding ‘carbon budgets’ to cap total emissions across a series of five-year periods. In the first carbon budget period (2008 to 2012) emissions totalled 2,982 MtCO2e – 36 MtCO2e below the cap. The carbon budget for the second period (2013 to 2017) is 2,782 MtCO2e, and the UK is on course to meet it. However, current projections show emissions

in the fourth and fifth periods exceeding the carbon budgets set for those years (2023 to 2027 and 2028 to 2032).

These concerns match those of fleet managers. Only 10% think that the Government is doing enough to encourage the adoption of AFVs in order to meet its target for greenhouse gas emissions. 73% say it isn’t.

Figure 7.4

7.4. Air quality standardsCO2 isn’t the only emission subject to legal limits. The Air Quality Standards Regulations of 2010 wrote into British law the emission standards set across the European Union. They cover pollutants ranging from nitrogen dioxide (NO2) to lead, and require ministers to draw up AQPs wherever those standards are breached.

The UK has exceeded the limits for NO2 ever since they came into force on 1 January 2010, which explains the need for the new AQP, detailed in section 7.1.

7.5. Emissions testsSeptember 2017 saw the introduction of stricter testing regimes for new vehicles. The European Union’s Real Driving Emissions tests aim to reduce the difference between official emissions levels and those actually produced on the road, especially with regards to NOx. The Worldwide Harmonised Light Vehicles Test Procedure will replace the New European Driving Cycle tests for measuring CO2 and fuel consumption – again with the aim of more accurately capturing a vehicle’s real-world performance.

‘People affected by Clean Air Zones will be looking for cost effective and practical transport solutions. Operators will need the right fleet mix, including AFVs, to meet those demands.’ – Gerry Keaney, Chief Executive, BVRLA

73%of fleet professionals say the Government must do more to support AFVs

©Hitachi Capital (UK) PLC. 2017. All rights reserved.20

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

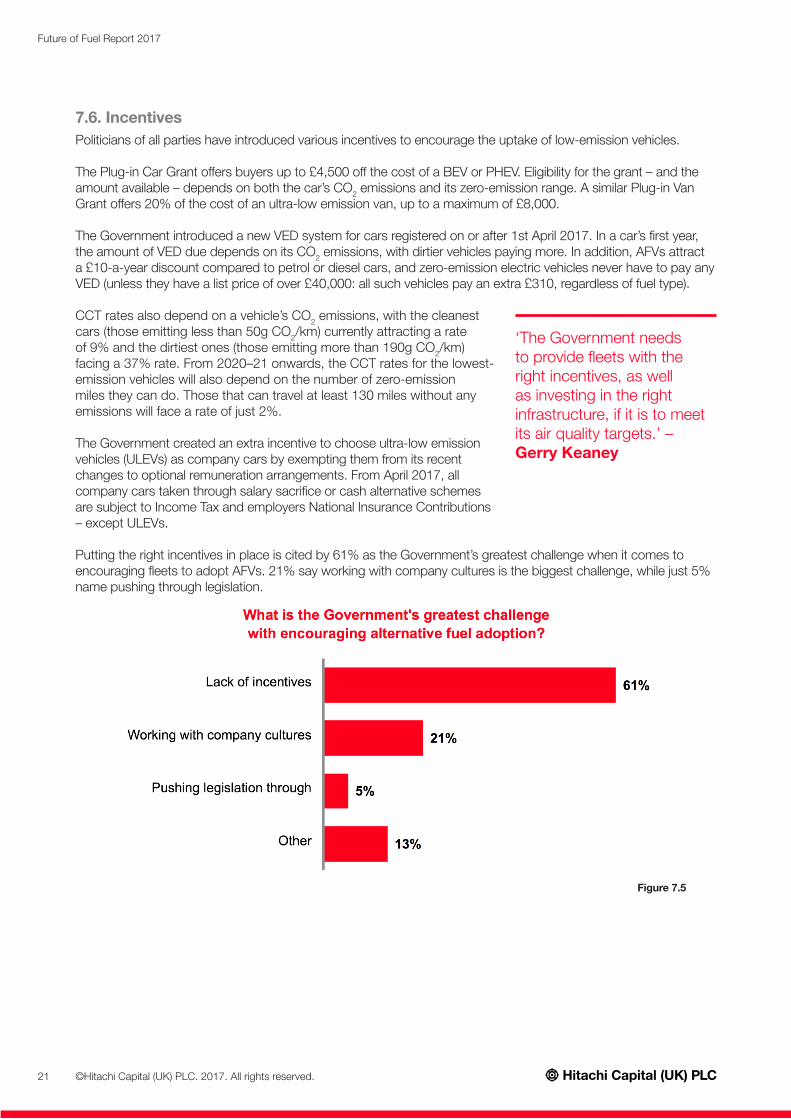

7.6. IncentivesPoliticians of all parties have introduced various incentives to encourage the uptake of low-emission vehicles.

The Plug-in Car Grant offers buyers up to £4,500 off the cost of a BEV or PHEV. Eligibility for the grant – and the amount available – depends on both the car’s CO2 emissions and its zero-emission range. A similar Plug-in Van Grant offers 20% of the cost of an ultra-low emission van, up to a maximum of £8,000.

The Government introduced a new VED system for cars registered on or after 1st April 2017. In a car’s first year, the amount of VED due depends on its CO2 emissions, with dirtier vehicles paying more. In addition, AFVs attract a £10-a-year discount compared to petrol or diesel cars, and zero-emission electric vehicles never have to pay any VED (unless they have a list price of over £40,000: all such vehicles pay an extra £310, regardless of fuel type).

CCT rates also depend on a vehicle’s CO2 emissions, with the cleanest cars (those emitting less than 50g CO2/km) currently attracting a rate of 9% and the dirtiest ones (those emitting more than 190g CO2/km) facing a 37% rate. From 2020–21 onwards, the CCT rates for the lowest-emission vehicles will also depend on the number of zero-emission miles they can do. Those that can travel at least 130 miles without any emissions will face a rate of just 2%.

The Government created an extra incentive to choose ultra-low emission vehicles (ULEVs) as company cars by exempting them from its recent changes to optional remuneration arrangements. From April 2017, all company cars taken through salary sacrifice or cash alternative schemes are subject to Income Tax and employers National Insurance Contributions – except ULEVs.

Putting the right incentives in place is cited by 61% as the Government’s greatest challenge when it comes to encouraging fleets to adopt AFVs. 21% say working with company cultures is the biggest challenge, while just 5% name pushing through legislation.

Figure 7.5

‘The Government needs to provide fleets with the right incentives, as well as investing in the right infrastructure, if it is to meet its air quality targets.’ – Gerry Keaney

©Hitachi Capital (UK) PLC. 2017. All rights reserved.21

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Conclusion and recommendations

1. The rise of AFVs will continue.The overall market share of AFVs may not seem particularly large when compared to petrol or diesel cars – but, crucially, it’s growing at a faster rate than either of those. In the past year alone, AFVs have gone from representing 3.2% to 4.2% of all new car registrations. As manufacturers increase both the quality and quantity of available models, and as politicians continue to incentivise their uptake, these numbers are certain to grow further. Fleets will be an important driver of this growth: 62% already include AFVs, and 42% plan to add more in the next two years.

2. Electricity isn’t the only alternative fuel. When it comes to the future of motoring, electric and hybrid vehicles have come to dominate the conversation. This is, in large part, a reflection of their prevalence: 22% of fleets now contain electric vehicles and 46% contain hybrids. But other alternative fuels are available. Fuels such as CNG or biodiesel may indeed be better options for HGVs and specialist vehicles. Policymakers and fleet operators cannot afford to ignore these alternatives and their benefits, both financial and environmental.

3. Clean Air Zones will work.London is introducing its ULEZ in 2019. Other cities will follow with similar Clean Air Zones. These are designed not just to penalise the dirtiest vehicles, but to incentivise cleaner alternatives. Will this work? Our survey suggests that it will. 65% of respondents say that the introduction of Clean Air Zones makes them more likely to use AFVs in their fleets. What’s more, many will do so enthusiastically. Only 28% of fleet professionals think that, whilst necessary, these proposals are ‘inconvenient’. A full 43% believe they are unequivocally a ‘good idea’.

4. The Government should invest in infrastructure.Fleet professionals are clear: the Government needs to do more to encourage the uptake of AFVs if it wants to meet its ambitious emissions targets. There are already a lot of tax incentives and grants in place, but perhaps not enough policy around infrastructure. Concerns about charge points are preventing some fleets from going electric, yet there are many more charge points than there are filling stations for CNG and biodiesel. The Government would be wise to invest in all of these facilities as part of his programme of infrastructure spending.

5. Fleets need to review their policies.Fleet managers aren’t just calling on politicians to act. 28% think that their own organisations should be doing more to adopt AFVs. The truth is that any fleet stands to gain by moving to greener alternatives, although the nature of that move will differ from fleet to fleet. Leasing companies such as Hitachi Capital Vehicle Solutions are on hand to help you with these considerations. By reviewing every aspect of your fleet policy, you can make the technologies of the future work for you.

To discover how we help fleets operate more effectively, efficiently and safely, visit our website: www.hitachicapitalvehiclesolutions.co.uk/future-of-fuel-report

©Hitachi Capital (UK) PLC. 2017. All rights reserved.22

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

MethodologyHitachi Capital Vehicle Solutions commissioned Shape the Future to survey fleet professionals in the UK, assessing their attitudes towards alternative fuels.

Fieldwork took place between 30 January and 15 March 2017, using an online survey on the Survey Mechanics platform.

149 respondents took part in the survey, including 48 fleet managers.

The table below provides some background statistics on these respondents and their fleets.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.23

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

The estimation that switching to electric vans and HGVs could save businesses approximately £14 billion a year uses the following assumptions:

• Annual vehicle miles are the same as 2016 figures from HYPERLINK “https://www.gov.uk/government/statis-tical-data-sets/tra01-traffic-by-road-class-and-region-miles” DfT Road Traffic Statistics (49.1 billion for vans, 16.6 billion for HGVs. These figures are for Great Britain).

• Average petrol and diesel consumption rates per mile are the same as for 2015, as calculated from HYPERLINK “https://www.gov.uk/government/statistical-data-sets/env01-fuel-consumption” DfT Transport Energy and environment statistics, HYPERLINK “https://www.gov.uk/government/statistical-data-sets/tra01-traffic-by-road-class-and-region-miles” DfT Road Traffic Statistics and HYPERLINK “https://www.gov.uk/government/statistics/digest-of-united-kingdom-energy-statistics-dukes-2016-main-chapters-and-annexes” BEIS Digest of UK Energy Statistics 2016.

• Average petrol and diesel prices are the same as the average figure for 27/11/2017 from HYPERLINK “https://www.gov.uk/government/statistical-data-sets/oil-and-petroleum-products-weekly-statistics” BEIS Weekly road fuel prices (120.1p per litre for petrol, 123.8p per litre for diesel – inc VAT).

• Electric vans achieve the same electricity consumption rate per mile as that stated by HYPERLINK “https://www.nissan.co.uk/vehicles/new-vehicles/e-nv200/charging-range.html” Nissan for the e-NV200 (106 miles on a single charge of its 24kWh battery).

• Electric HGVs achieve the same electricity consumption rate per mile as that stated by HYPERLINK “https://www.daimler.com/innovation/case/electric/efuso-2.html” Daimler for the E-FUSO Vision One (350km on a single charge of its 300kWh battery).

• Average electricity costs per kWh are the same as 2017 Q2 figure for non-domestic consumers (including the Climate Change Levy) from HYPERLINK “https://www.gov.uk/government/statistical-data-sets/gas-and-elec-tricity-prices-in-the-non-domestic-sector” BEIS Quarterly Energy Prices (10.64p per kWh – exc VAT).

• VAT is included (at 20%).

These calculations suggest that electricity is approximately 15.3 pence per mile cheaper than petrol/diesel for vans, and 37.5 pence per mile cheaper than diesel for HGVs. This implies that businesses could save approximately £13.7 billion a year by switching to electric vans and HGVs.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.24

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Sources and further readingFleet Insider: FY16/17 Mid-year ReviewHitachi Capital Vehicle Solutions

Fleet Insider: Industry Update February 2017Hitachi Capital Vehicle Solutions

New Car CO2 Report 2017Society of Motor Manufacturers and Traders, 2 March 2017

UK plan for tackling roadside nitrogen dioxide concentrationsDepartment for Environment, Food & Rural Affairs, 26 July 2017

‘Volvo Cars to go all electric’Volvo Car Group, 5 July 2017

‘New car market declines in June as demand stabilises over second quarter’The Society of Motor Manufacturers and Traders, 5 July 2017

June 2017 – EV registrationsThe Society of Motor Manufacturers and Traders, 5 July 2017

Vehicle Licensing Statistics: Quarter 1 (Jan - Mar) 2017Department for Transport, 15 June 2017

European Vehicle Market Statistics: Pocketbook 2016/17The International Council on Clean Transportation, 13 December 2016

‘Breakthrough battery tech could make electric cars more efficient’Ben Woods, Wired, 25 June 2016

‘1000 km range thanks to a new battery concept’Fraunhofer Institute for Ceramic Technologies and Systems IKTS, 2 May 2017

‘In South Korea, wireless charging powers electric buses’Keith Barry, Wired, 8 July 2013

‘Israel tests wireless charging roads for electric vehicles’Abigail Fagan, Scientific American, 11 May 2017

‘A first look at our Waymo fully self-driving Chrysler Pacifica Hybrid minivans’John Krafcik, Medium, 18 December 2016

‘All Tesla cars being produced now have full self-driving hardware’Tesla, 19 October 2016

Renewable Transport Fuel Obligation statistics: period 8 2015/16, report 6Department for Transport, 2 February 2017

Autumn Statement 2016HM Treasury, 23 November 2016

Spring Budget 2017HM Treasury, 8 March 2017

©Hitachi Capital (UK) PLC. 2017. All rights reserved.25

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Workplace Charging Scheme – Guidance Document for Applicants, Chargepoint Installers and ManufacturersOffice for Low Emission Vehicles, 3 November 2016

Charging point statistics 2017Zap-Map

Automated and Electric Vehicles Bill (Bill 112 2017-19)House of Commons, 18 October 2017

Weekly road fuel pricesDepartment for Business, Energy & Industrial Strategy

‘UK Supreme Court orders Government to take “immediate action” on air pollution’ClientEarth, 29 April 2015

Air quality in the UK: plan to reduce nitrogen dioxide emissionsDepartment for Environment, Food & Rural Affairs, 17 December 2015

‘ClientEarth wins air pollution case in High Court’Client Earth, 2 November 2016

‘Mayor plans to introduce Ultra Low Emission Zone in April 2019’Mayor of London, 4 April 2017

‘Mayor: £10 ‘Toxicity Charge’ for most polluting cars starts October 23’Mayor of London, 17 February 2017

Mayor’s Transport Strategy – Draft for public consultationMayor of London, 21 June 2017

Clean Air Zone FrameworkDepartment for Environment, Food & Rural Affairs, 5 May 2017

2016 UK Greenhouse Gas Emissions, Provisional FiguresDepartment for Business, Energy & Industrial Strategy, 30 March 2017

‘The plug-in car grant: a quick guide to what you need to know’Hitachi Capital Vehicle Solutions, 3 March 2017

‘The new system of Company Car Tax, explained’Hitachi Capital Vehicle Solutions, 21 December 2016

©Hitachi Capital (UK) PLC. 2017. All rights reserved.26

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

GlossaryAlternatively-fuelled vehicleA vehicle that runs on fuel other than petrol or diesel – such as electricity, solar power or biofuels – including hybrids.

Battery Electric VehicleA vehicle that is powered entirely by an electric battery. It is charged by being plugged in to a charge point.

Bio-CNGRenewable methane, produced from food and other waste and compressed, which can be used as a fuel.

BiobutanolButanol (a hydrocarbon) that is produced from crops and other biomass. It can be blended with petrol to power vehicles.

BiodieselDiesel produced from cooking oil, animal fat and crops. It is usually blended with normal petroleum diesel to power vehicles.

Charge pointA charging station for Battery Electric and Plug-in Hybrid Vehicles. Charge points come in three forms: standard, fast and rapid.

Clean Air ZoneAn area where targeted policies are implemented to reduce air pollution and improve air quality. These policies can include charging drivers to enter the Zone if their vehicles do not meet specified emission standards.

Company Car TaxA government tax on a car received by an employee as a benefit in addition to their salary.

Compressed Natural GasNatural gas that is compressed and used as a fuel.

Dual-fuelA dual-fuel (or ‘bi-fuel’) vehicle is one that can run on two different fuels – for example, Compressed Natural Gas and diesel.

Euro emission standardsThese set limits on exhaust emissions of carbon monoxide, nitrogen oxides and other pollutants for all new vehicles in the European Union. The latest standards – Euro 6 – apply to cars and small vans registered after 1 September 2015, and larger vans registered after 1 September 2016.

Fuel dutyA government tax on the sale of petrol, diesel and other motor fuels. The current rate for petrol and diesel is 57.95 pence per litre. Value Added Tax of 20% is also applied to the total cost of fuel including fuel duty.

Hybrid Electric VehicleA vehicle powered by both an internal combustion engine (whether petrol or diesel) and an electric battery. The battery is charged by the engine and by reclaiming energy under braking, rather than by being plugged in.

Hydrogen Fuel Cell VehicleAn electric vehicle that uses a hydrogen fuel cell, instead of a battery, to generate its electricity.

Kinetic energyThe energy a vehicle or other object has because of its motion. For any object of a given mass, the faster it is travelling, the greater its kinetic energy.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.27

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

Liquefied Natural GasNatural gas that has been converted to liquid form. It can be used as a fuel for vehicles.

Liquefied Petroleum GasA liquid mixture of propane and butane that can be used to fuel vehicles. Also known as ‘autogas’.

Natural gasA fossil fuel found in underground rock formations, oil fields and coal beds. It consists mostly of methane.

Optional remuneration arrangementAn arrangement where an employee gives up the right to an amount of earnings in return for a benefit, such as a company car. This could be a salary sacrifice scheme (where the employee gives up a portion of their salary in exchange for the benefit) or a cash alternative scheme (where the employee takes the benefit instead of a cash allowance).

Plug-in Car GrantA government grant towards the cost of a Battery Electric, Plug-in Hybrid or Hydrogen Fuel Cell car that meets specified eligibility criteria. To receive the Grant, a car must emit less than 75 grams of carbon dioxide per kilometre and be able to travel at least 10 miles with zero carbon dioxide emissions. The Grant is worth a maximum of £4,500.

Plug-in Hybrid Electric VehicleA vehicle powered by both an internal combustion engine and an electric battery. The battery is charged by being plugged in to a charge point.

Plug-in Van GrantA government grant towards the cost of a Battery Electric or Plug-in Hybrid van that meets specified eligibility criteria. To receive the Grant, a van must emit less than 75 grams of carbon dioxide per kilometre and be able to travel at least 10 miles with zero carbon dioxide emissions. The Grant is worth 20% of the purchase price of the van, up to a maximum of £8,000.

Ultra-low emission vehicleA vehicle that emits less than 75 grams of carbon dioxide per kilometre and can drive for at least 10 miles with no emissions.

Vehicle Excise DutyAn annual Government tax on cars used on the road, based on their fuel types and levels of carbon dioxide emissions.

©Hitachi Capital (UK) PLC. 2017. All rights reserved.28

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

AcronymsAFV Alternatively-fuelled vehicleBEV Battery Electric VehicleCCT Company Car TaxCNG Compressed Natural GasCO2 Carbon dioxideDfT Department for TransportEU European UnionEV Electric vehicleFCV Fuel Cell Vehicleg CO2/km Grams of carbon dioxide per kilometreHEV Hybrid Electric VehicleHGV Heavy goods vehicleICE Internal combustion engineLNG Liquefied Natural GasLPG Liquefied Petroleum Gasmpg Miles per gallonMtCO2e Million tonnes carbon dioxide equivalentNO2 Nitrogen dioxideNOx Oxides of nitrogenPHEV Plug-in Hybrid Electric VehicleSMMT Society of Motor Manufacturers and TradersUK United KingdomULEV Ultra-low emission vehicleULEZ Ultra-Low Emission ZoneVED Vehicle Excise Duty

Hitachi Capital Vehicle Solutions is a trading style of Hitachi Capital (UK) PLC. Authorised and regulated by the Financial Conduct Authority. Financial Services Register no. 704348. The register can be accessed through http://www.fca.org.uk

Registered Office: Hitachi Capital House, Thorpe Road, Staines-upon-Thames, Surrey, TW18 3HP. Registered in Cardiff under company no. 1630491

©Hitachi Capital (UK) PLC. 2017. All rights reserved.29

Future of Fuel Report 2017

Hitachi Capital (UK) PLC

![HITACHI CAPITAL CORPORATION HITACHI … the purposes of Directive 2004/39/EC ... HITACHI CAPITAL CORPORATION HITACHI CAPITAL (UK) PLC HITACHI CAPITAL AMERICA CORP. [[] [] ...](https://static.documents.pub/doc/80x56/5ad063b27f8b9a1d328e3da3/hitachi-capital-corporation-hitachi-the-purposes-of-directive-200439ec-.jpg)