32

Gaining Lives With Our Gaining Lives With Our Unique PBM Capabilities Jon Roberts Executive Vice President & President, CVS/caremark

Gaining Lives With OurGaining Lives With Our Unique PBM Capabilities

Jon RobertsExecutive Vice President & President, CVS/caremark

Agenda

Performance HighlightsPerformance HighlightsPerformance Highlights

Pharmacy Trends and Cost Management

Performance Highlights

Programs

Well Positioned to Grow in Evolving Health Care Environment

2©2014 CVS Health

Delivering on Our Promises with Strong PBM PerformancePBM Performance

Net Revenue($, billions)

Operating Profit($, billions)

76.2

98.213.6%CAGR13.6%CAGR

3.1

3.814.6%CAGR14.6%CAGR

58.9 2.2

3.1

2011 2013 2015E 2011 2013 2015E

3©2014 CVS Health

Notes:1. 2013 excludes Provigil.2. 2015 reflects midpoint of guidance ranges.

2015 Gross New Business of $6.6 Billion

$1.3billion

$6.6billion$2.1

$3.2billion

State of Florida

billion

Government & Union EmployerHealth Plan

4©2014 CVS Health

Notes:1. As of 12/4/14.2. Gross Wins excludes Medicare Part D SilverScript individual products.

Net New Client Business of $3.2 Billionwith 96% Retentionwith 96% Retention

Revenues($, billions) 75% of client non-

renewals due to 6.6 1.8

0.8

acquisition and retirees

3.20.8

Business Not Renewed

Gross New Business

Acquired Moved to Exchange (Primarily Retirees)

Other Net New Business

4 million members implemented in 2014 … clients highly satisfied

Business (Primarily Retirees)

Notes:1. As of 12/4/14.2 Net New Client Business excludes Medicare Part D SilverScript individual products

5©2014 CVS Health

2. Net New Client Business excludes Medicare Part D SilverScript individual products.3. Client retention rate is defined as: 1 less (projected 2015 lost revenues from known terminations occurring after January 1, 2014,

divided by estimated 2015 PBM revenues) expressed as a percentage. Both terminations and PBM revenues exclude the individual PDP business.

How We Win: Compete on Price, Differentiate with Service and CapabilitiesService and Capabilities

Advanced Formulary Adherence

Programs

Network StrategiesPreferred Network,

MaintenanceExclusive Specialty y

Strategies ProgramsMaintenance Choice®

Specialty

6©2014 CVS Health

Aetna: Continuing to Expand Our Partnership

Aetna Medicare Business

Coventry Commercial and Medicaidus ess a d ed ca d

Q1 2015 Q1 2016 2017

Coventry M diMedicare

Maintenance Choice® and Pharmacy Advisor® continue to expand

7©2014 CVS Health

Note:1. Aetna Medicare Business lives are moving to the CVS/caremark platform in Q1 of 2015.

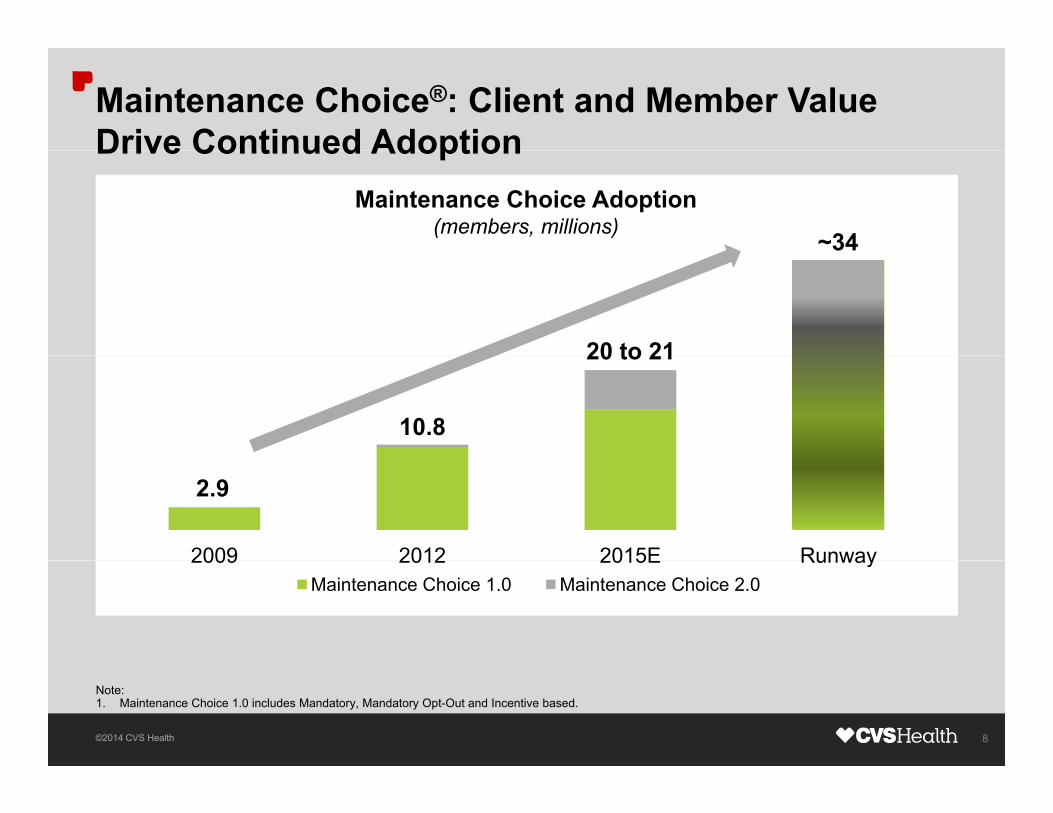

Maintenance Choice®: Client and Member Value Drive Continued AdoptionDrive Continued Adoption

~34

Maintenance Choice Adoption(members, millions)

20 to 21

10.8

20 to 21

2009 2012 2015E Runway

2.9

2009 2012 2015E RunwayMaintenance Choice 1.0 Maintenance Choice 2.0

8©2014 CVS Health

Note:1. Maintenance Choice 1.0 includes Mandatory, Mandatory Opt-Out and Incentive based.

Specialty ConnectTM: Like Maintenance Choice®, Only CVS Health Can OfferOnly CVS Health Can Offer

Choose Where to Send / Bring Prescription

Choose Preferred Delivery Location

Counseling From Therapy-specific

CareTeamsg p Delivery Location CareTeams

CVS/specialty Home / Location of Choice

CVS/pharmacy CVS/pharmacyFull Integration With

CVS/specialty

~75,000 patients served … half choose the retail pick-up option

9©2014 CVS Health

Pharmacy Advisor® Serves All Our Lines of Business

• Successfully d l d

Cumulative Counseling Interventions(millions)

9 9 deployed across Commercial, Medicare and Medicaid

7.2

9.9

Medicaid

• Delivering value in Medicare on

3.8

in Medicare on Clinical Star Measures

Q4'11 Q4'12 Q4'13 Q3'14

1.3

Q4 11 Q4 12 Q4 13 Q3 14

Retail Call Center

10©2014 CVS Health

Note:1. PBM: Commercial, Medicare, Medicaid and Exchanges.

CVS/minuteclinic Savings Strategy Continues to GrowGrow

• ~14 fold increase in member Client Adoption

(members, thousands)

lives enrolled in three years

• Launched capability to 1,200

14,500

adjudicate CVS/minuteclinicservices through PBM benefit~14X

• Significant opportunity to grow lives with CVS/minuteclinicremains

23910888

1.2 million total implemented and committed lives to date

2015201420132012 Runway

11©2014 CVS Health

Note:1. CVS Caremark Product Team master client pipeline tracking. Based on implemented plans thru 2014.

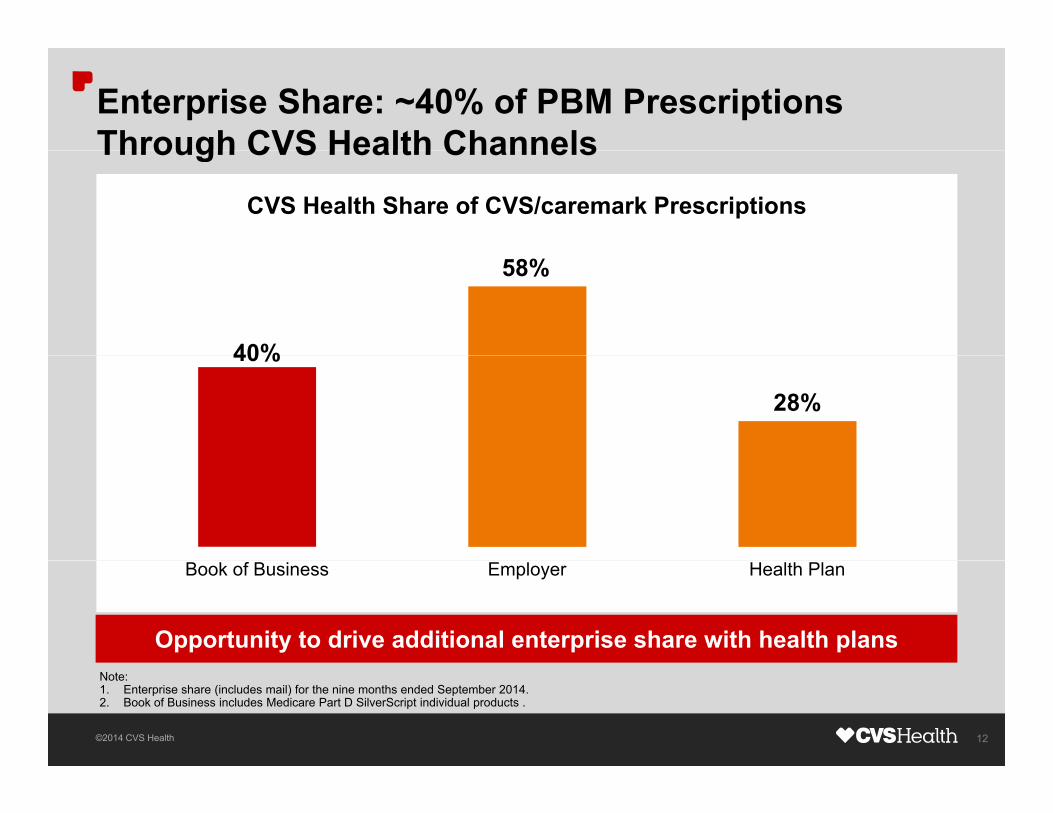

Enterprise Share: ~40% of PBM Prescriptions Through CVS Health ChannelsThrough CVS Health Channels

CVS Health Share of CVS/caremark Prescriptions

40%

58%

40%

28%

Book of Business Employer Health Plan

Opportunity to drive additional enterprise share with health plans

12©2014 CVS Health

Note:1. Enterprise share (includes mail) for the nine months ended September 2014.2. Book of Business includes Medicare Part D SilverScript individual products .

Agenda

Performance HighlightsPerformance Highlights

Pharmacy Trends and Cost Management Pharmacy Trends and Cost Management Programs

Well Positioned to Grow in Evolving Health Care

Programs

Environment

13©2014 CVS Health

Fewer New Generics to Mitigate Trend: Spend Management Programs Increase in ImportanceManagement Programs Increase in Importance

Total Brand Market Sales of Expected Generic Launches($, billions)

35.0

24.4

14.7 16.5

24.4

12.3

5.8

2012 2013 2014E 2015E 2016E 2017E

Note:1 2013 d i i l d ll t l l h

14©2014 CVS Health

1. 2013 and prior includes all actual launches.2. 2014E forward includes all actual and expected generic launches in total brand numbers.3. Forward-looking information assumes no “at risk” launches.Source: Total brand market sales estimates represent 12 months of sales as reported in the IMS Health NSP file.

Specialty is Growing in Absolute Dollarsand Percent of Total Spendand Percent of Total Spend

Total Industry Specialty Spend($, billions)

235

127

179

235

17%CAGR

92CAGR

2012 2014E 2016E 2018E SpecialtyPercent

30% 38% 45% 50%

Pharmacy spend Infused oncologyMedical spend

Percentof TotalDrug

Spend

15©2014 CVS Health

Source: NHE, Artemetrix, CVS/caremark internal analysis, 2013.

Pharmacy spend Infused oncologyMedical spend

Return of Double-digit Trend Requires Tighter Cost Controls

Payor Trend

Cost Controls

10 3%10.3%

3.8%

0.1%

2012 2013 2014E

16©2014 CVS Health

Source: 2014 - Enterprise Analytics as of Q314; excludes compounds due to client-specific strategies.

Our Unique Set of Tools to Manage Trend

Managed Ad d S i ltF l

Traditional / Non-specialty Drugs

Specialty DrugsIn Pharmacy

Specialty Drugs In Medical

Managed, Advanced, Value Advanced Specialty

30- and 90-day Retail, Mail, Maintenance Choice Preferred, Exclusive and Infusion Networks

Formulary

Networks ,

Prior Authorization, Retrospective review

Cross-Benefit Clinical Guideline Management and PA

Utilization Management

Site of Care Transition Management with Coram Nurses

Prior Authorization Pharmacy Benefit Medical Benefits Claims

Site Of Care

Claims Prior Authorization, Retrospective Review

Pharmacy BenefitClaims Edits Edits with Novologix

Technology

Pharmacy Advisor® CareTeam including Pharmacist, Accordant and Coram Nurses

Claims Editing

Care Coordination

17©2014 CVS Health

Coordination

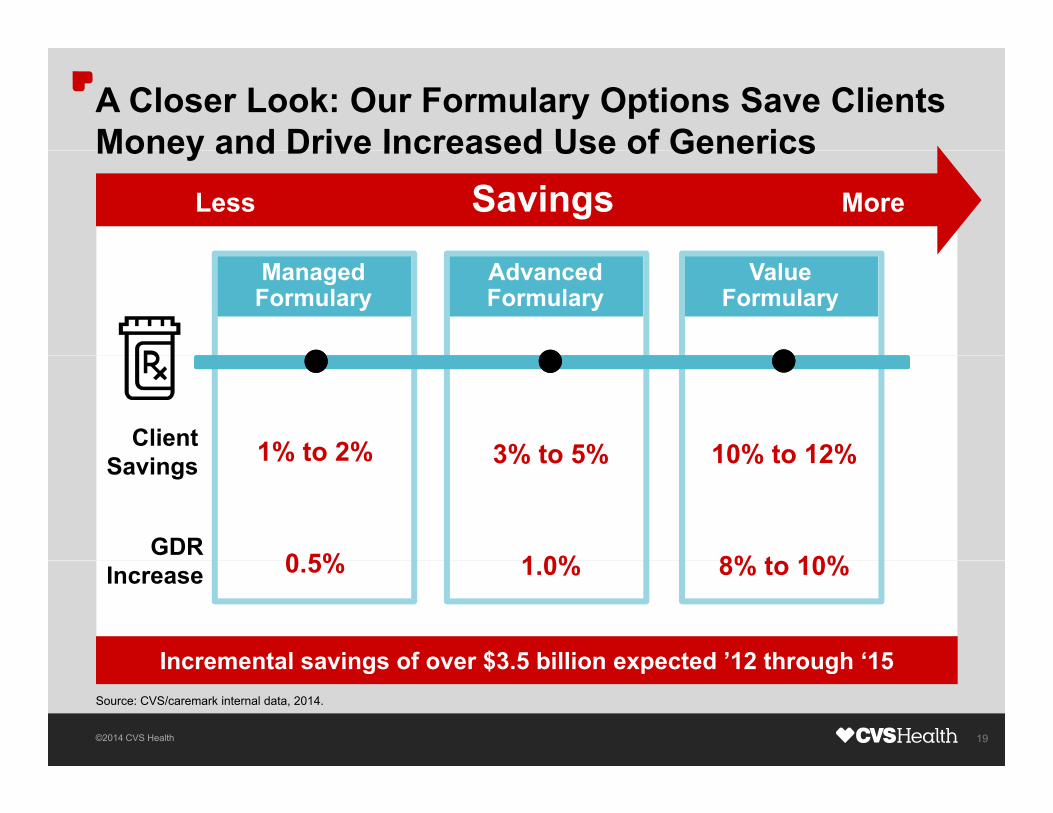

A Closer Look: Our Formulary Options Save Clients Money and Drive Increased Use of GenericsMoney and Drive Increased Use of Generics

Managed Formulary

CVS/caremark led industry with introduction of strategy to exclude certain branded drugs from formulary

• Approach delivers savings to clients and their members

• Improved rebates on formulary brandsImproved rebates on formulary brands

• Increased penetration of generics

Have excluded more drugs to date than other traditional PBMs

Incremental savings of over $3 5 billion expected ’12 through ‘15

18©2014 CVS Health

Source: CVS/caremark internal data, 2014.

Incremental savings of over $3.5 billion expected 12 through 15

A Closer Look: Our Formulary Options Save Clients Money and Drive Increased Use of GenericsMoney and Drive Increased Use of Generics

Less Savings More

Managed Formulary

Advanced Formulary

Value Formulary

1% to 2% 10% to 12%3% to 5%ClientS i 1% to 2%

0 5%

10% to 12%

8% t 10%

3% to 5%

1 0%

Savings

GDR 0.5% 8% to 10%1.0%Increase

Incremental savings of over $3 5 billion expected ’12 through ‘15

19©2014 CVS Health

Source: CVS/caremark internal data, 2014.

Incremental savings of over $3.5 billion expected 12 through 15

A Closer Look: Our Network Options Offer Savings and Choiceand Choice

Less Savings More

Retail 90 Maintenance Choice®

2.0Maintenance Choice®

1.0

90-dayNetwork

30 day

National Advanced ChoiceTM Exclusive Choice

68,000h i

50,000h i

19,000h i30-day

Networkpharmacies pharmacies pharmacies

20©2014 CVS Health

Agenda

Performance HighlightsPerformance Highlights

Pharmacy Trends and Cost Management Programs

Well Positioned to Grow in Evolving Health Care Well Positioned to Grow in Evolving Health Care Environment Environment

21©2014 CVS Health

Evolving Health Care Environment: Consumer is at the CenterConsumer is at the Center

3X150% 3Xexpected covered lives by 2018

%growth in CDH enrollment

10K 40+%CONSUMERS

10K people per day turning 65

40+% projected increase in lives from 65 2013

22©2014 CVS Health

Source: CDH - Employer Health Benefits Survey 2014; Exchanges - CBO 2014 beginning with 2013 enrollment; Medicaid – Avalere 2014; Medicare: Pew Research Center.

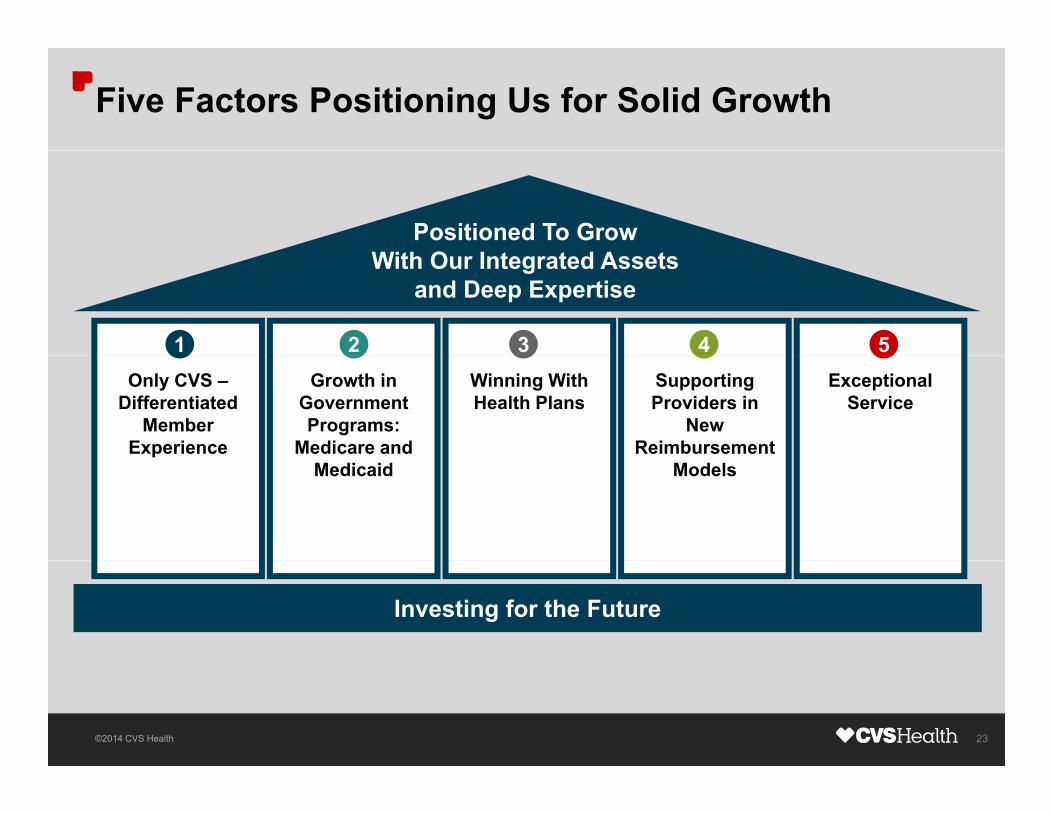

Five Factors Positioning Us for Solid Growth

Positioned To GrowWith O I t t d A t

1 2 3 4 5

With Our Integrated Assets and Deep Expertise

Supporting Providers in

New Reimbursement

Winning With Health Plans

Growth in Government Programs:

Medicare and

Only CVS –Differentiated

Member Experience

Exceptional Service

ModelsMedicaid

Investing for the Future

23©2014 CVS Health

Only CVS – Differentiated Member Experience: Helps Members Better Manage Health and Costs

1

Helps Members Better Manage Health and Costs CVS Retail Pharmacist

CVS/minuteclinicNurse

CVS/specialty CareCall Center CVS/specialty Care Team

Call Center Pharmacist

Infusion NurseBenefit Opportunity

Specialist

Digital Tools

24©2014 CVS Health

Growth in Government Programs: Medicare Growth Through SilverScript and Our Health Plan Partners

2

Through SilverScript and Our Health Plan PartnersMedicare Members By PBM

(millions)SilverScript Choice

and SilverScript Plus

CVS Health

Express Scripts

OptumRx

7.2

6 9

8.4• Competitively priced

• Zero deductible and

Catamaran

Humana

CVS Health 6.9

6.3

3.9

Zero deductible and low premium

• Personalized

Prime

Cigna 1.6

1.5

marketing

Envision

MedImpact

Captive PDP Captive MAPD NonCaptive

0.7

0.4

25©2014 CVS Health

p p p

Source: CMS (Membership figures as of October 3, 2014)

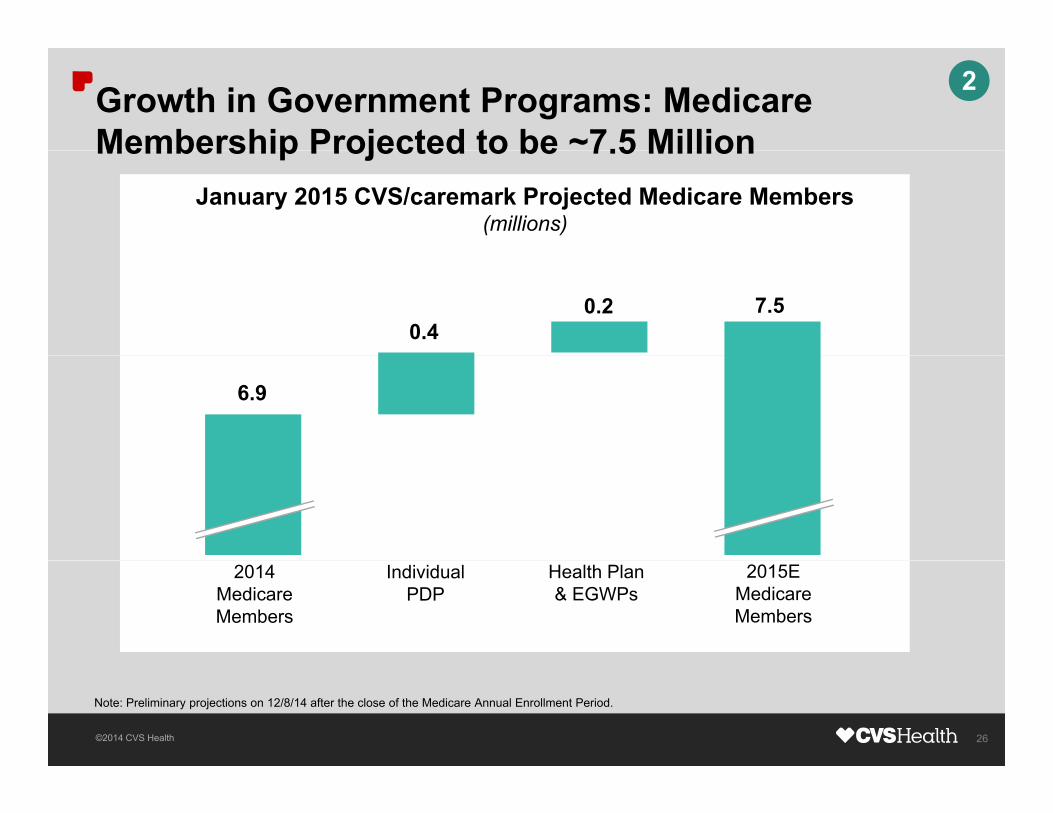

Growth in Government Programs: Medicare Membership Projected to be ~7.5 Million

2

Membership Projected to be 7.5 MillionJanuary 2015 CVS/caremark Projected Medicare Members

(millions)

0.47.50.2

6.9

2015E Medicare Members

Health Plan & EGWPs

Individual PDP

2014 Medicare Members

26©2014 CVS Health

Note: Preliminary projections on 12/8/14 after the close of the Medicare Annual Enrollment Period.

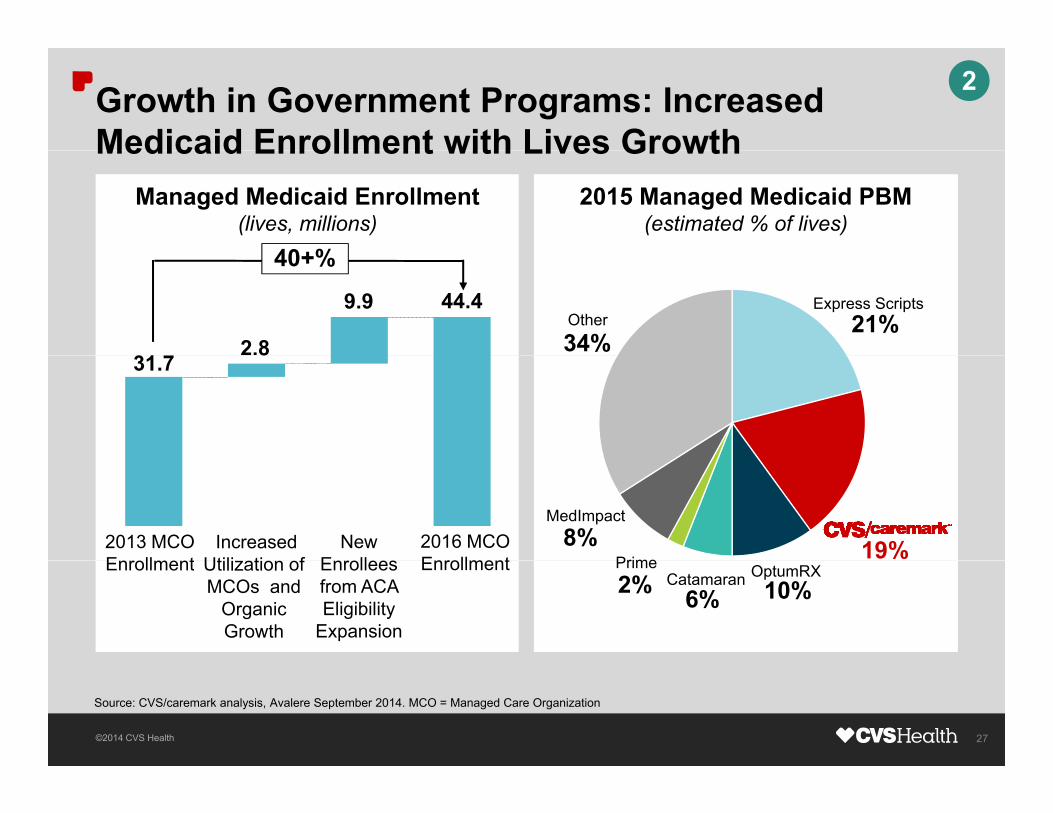

Growth in Government Programs: Increased Medicaid Enrollment with Lives Growth

2

Medicaid Enrollment with Lives Growth2015 Managed Medicaid PBM

(estimated % of lives)Managed Medicaid Enrollment

(lives, millions)

40+%

Express Scripts21%

34%Other

312.8

44.4

40+%

9.9

31.78

Prime

MedImpact8% 19%2016 MCO

EnrollmentNew

EnrolleesIncreased

Utili ti f2013 MCO Enrollment Prime

2% Catamaran6%

OptumRX10%

EnrollmentEnrollees from ACA Eligibility

Expansion

Utilization of MCOs and

Organic Growth

Enrollment

27©2014 CVS Health

Source: CVS/caremark analysis, Avalere September 2014. MCO = Managed Care Organization

Winning with Health Plans: $3.2 Billion Gross New Business and 30 Total Exchange Clients in 2015

3

Business and 30 Total Exchange Clients in 2015

Comprehensive services that meet needs for cost Unique PBM pcontrol, quality, enhanced capabilities

Holistic approach to manage specialty pharmacy

qModel

Comprehensive Holistic approach to manage specialty pharmacy across both pharmacy and medical benefits

pSpecialty Solutions

Enterprise services that create competitive advantage in the B2C environment

Member Access and Engagement

Line of business expertise to drive growth, compliance and innovation

Expertise in Government Programs

28©2014 CVS Health

Supporting Providers in New ReimbusementModels: Patient-centered Medical Home Example

4

Models: Patient centered Medical Home Example

CVS/caremarkCVS/pharmacy

Pharmacists provide counseling on adherence

and comprehensive medication review for

Adherence counseling and Electronic Health Record notification of patient non-adherence medication review for

vulnerable patientspatient non-adherence

and gaps in therapy

CVS/specialty

CareTeam pharmacist

CVS/minuteclinic

Support their patient management with Patient-centered

M di l Hp

and Accordant nurse serve as extension of

clinical team

programs such as diabetes counseling and

smoking cessation

Medical Home

29©2014 CVS Health

Supporting Providers in New ReimbusementModels: Patient-centered Medical Home Example

4

Models: Patient centered Medical Home Example

CVS/caremarkCVS/pharmacy

Pharmacists provide counseling on adherence

and comprehensive medication review for

Adherence counseling and Electronic Health Record notification of patient non-adherence medication review for

vulnerable patientspatient non-adherence

and gaps in therapy

CVS/specialty

CareTeam pharmacist

CVS/minuteclinic

Support their patient management with Patient-centered

M di l Hp

and Accordant nurse serve as extension of

clinical team

programs such as diabetes counseling and

smoking cessation

Medical Home

30©2014 CVS Health

Exceptional Service: We’re Raising the Bar toEnsure Continued Success

5

Ensure Continued Success

Continue to Evolve Service Culture

Invest inInfrastructure

Monitor Performance Service Culture Infrastructure

• Define success

• Make the metrics

Metrics

• Integrated delivery channels

• Holistic view of operational

• Make the metrics visible

• Reward achievement

• Automated benefit builder

• Artificial intelligence

performance

• Early detection of trends; avoidance of

in call centers

• Digital capabilities

escalated issues

• Speedy resolution

31©2014 CVS Health

Positioned for Today, Preparing for Tomorrow

Investments and Innovations address payor needsMade the Right Moves

Effectively engaging members and providersMade the Right Moves

Winning in the marketplace with integrated model

S l d ti titi i iStill Onl CVS Scale and expertise ensure competitive pricing

Differentiated offerings drive client retention and winsStill … Only CVS

Continue to expand unique breadth of capabilitiesLooking Ahead Continue to expand unique breadth of capabilities

Partnering with health plans to meet their needsLooking Ahead …

Continued Innovation

Unmatched capabilities to win in fast-growing sectors

Positioned for sustainable growth as market evolvesSustainable Growth

32©2014 CVS Health Gaining Lives With Our Unique PBM Capabilities