Page 1

Garment Market Survey Report

Macro Industry, Consumer and Distribution Survey results and recommendations

Prepared by: ADS Network, Next to Spinney’s Supermarket, 16th street, Wazir Akbar Khan, Kabul- Afghanistan

Page 2

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 1 of 68

Table of Contents 1. Executive Summary and Key conclusions: ............................................................................................ 4

2. Objective of the Project ........................................................................................................................ 6

3. The research Methodology adopted .................................................................................................... 6

4. The Garments industry overview .......................................................................................................... 6

5. Consumer Research Key Findings: ........................................................................................................ 9

5.1 Respondent Age Profile: ............................................................................................................... 9

5.2 Marital Status profile: ................................................................................................................... 9

5.3 Ethnic Profile: .............................................................................................................................. 10

5.4 Respondents by profession: ........................................................................................................ 11

5.5 Average family size of the respondents: ..................................................................................... 12

5.6 Literacy profile of respondents: .................................................................................................. 12

5.7 Most recent Garment purchase: ................................................................................................. 13

5.8 Most recently purchased Fabric: ................................................................................................ 14

5.9 Time since last garment was purchased: .................................................................................... 14

5.10 Time since last Fabric was purchased: ........................................................................................ 15

5.11 Most preferred place for buying garments and fabrics: ............................................................. 16

5.12 Buying habit for garments: ......................................................................................................... 16

5.13 Buying habit for Fabrics: ............................................................................................................. 17

5.14 Frequency of purchase of garments and fabrics: ....................................................................... 18

5.15 If garment purchased for Special Occasions, what special occasions: ................................... 19

5.16 Budget kept for buying garments/fabrics: .................................................................................. 19

5.17 Frequency of purchase of wedding clothing: .............................................................................. 19

5.18 Budget for Eid/Nawroz/Winter/Summer shopping: ................................................................... 20

5.19 Fabric stitching behavior: ............................................................................................................ 21

5.20 Influencing factors when buying garments: ............................................................................... 23

5.21 Consumer buying preferences: ................................................................................................... 24

5.22 Style preference by Season: ........................................................................................................ 25

5.23 Style preference for Special occasions/Working clothes/Home clothes .................................... 26

5.24 Key decision maker for clothes purchase in the family .............................................................. 27

5.25 Children’s clothes buying behavior: ............................................................................................ 27

5.26 The most important factor when buying a Fabric: ..................................................................... 29

Page 3

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 2 of 68

5.27 Multi Dimension scaling for garments- consumer attitudes towards garments: ....................... 30

5.28 Concept card test: SET-A ............................................................................................................. 32

5.29 Concept Card test- Set-B: ............................................................................................................ 35

6. Consumer Research Key Findings by Segment ................................................................................... 37

6.1 Segment wise Age Distribution: .................................................................................................. 37

6.2 Segment wise marital status and ethnic grouping: .................................................................... 38

6.3 Other Demographic patterns by segment: ................................................................................. 38

6.4 Most recently purchased Garments and Fabrics: ....................................................................... 41

6.5 Time since last purchase of garments and fabrics: ..................................................................... 42

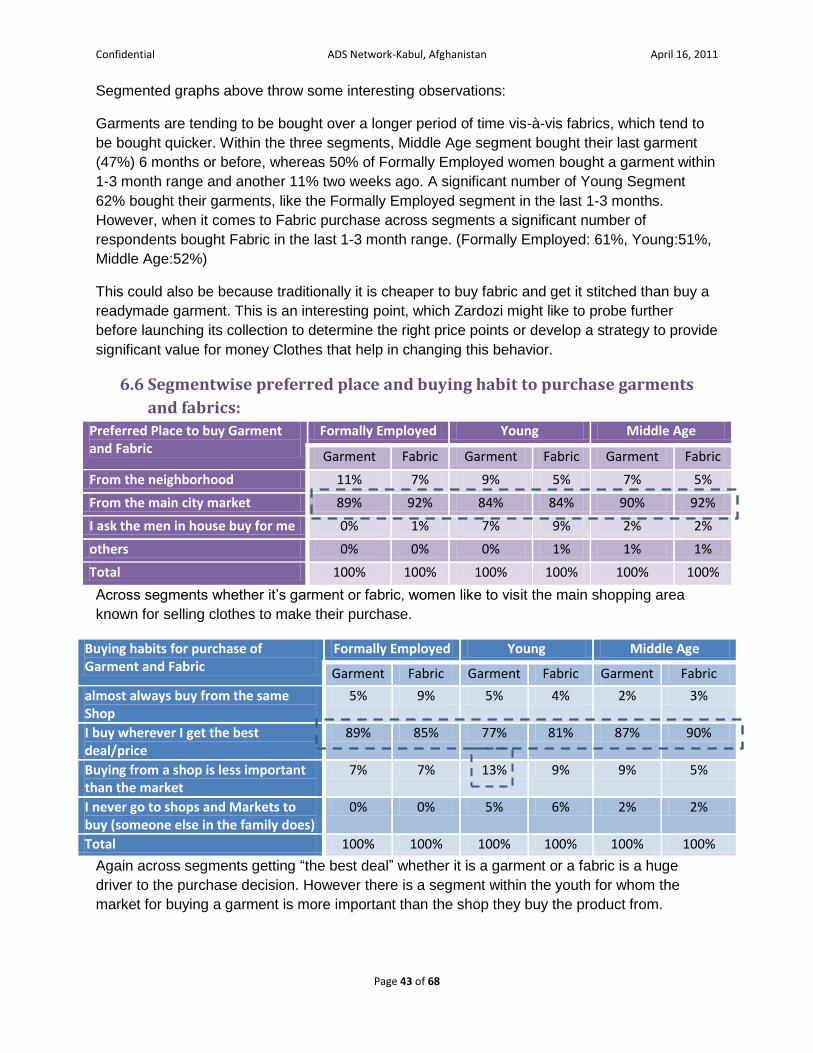

6.6 Segmentwise preferred place and buying habit to purchase garments and fabrics: ................. 43

6.7 Perceived frequency of purchase of garments: .......................................................................... 44

6.8 Perceived frequency of purchase for garments:......................................................................... 45

6.9 Budget for purchase of Garments and Fabric: ............................................................................ 46

6.10 Segmentwise Budget for purchase of clothes during Eid/Nawroz: ............................................ 47

6.11 Budget kept for Summer and Winter clothes: ............................................................................ 48

6.12 Fabric Stitching behavior: ........................................................................................................... 48

6.13 Purchase intent and influences for buying clothes: .................................................................... 50

6.14 Style preferences during winters and summers: ........................................................................ 51

6.15 Style preferences segmentwise for Weddings: .......................................................................... 52

6.16 Style preference while working or going to school: ................................................................... 53

6.17 Style preference when at home: ................................................................................................ 53

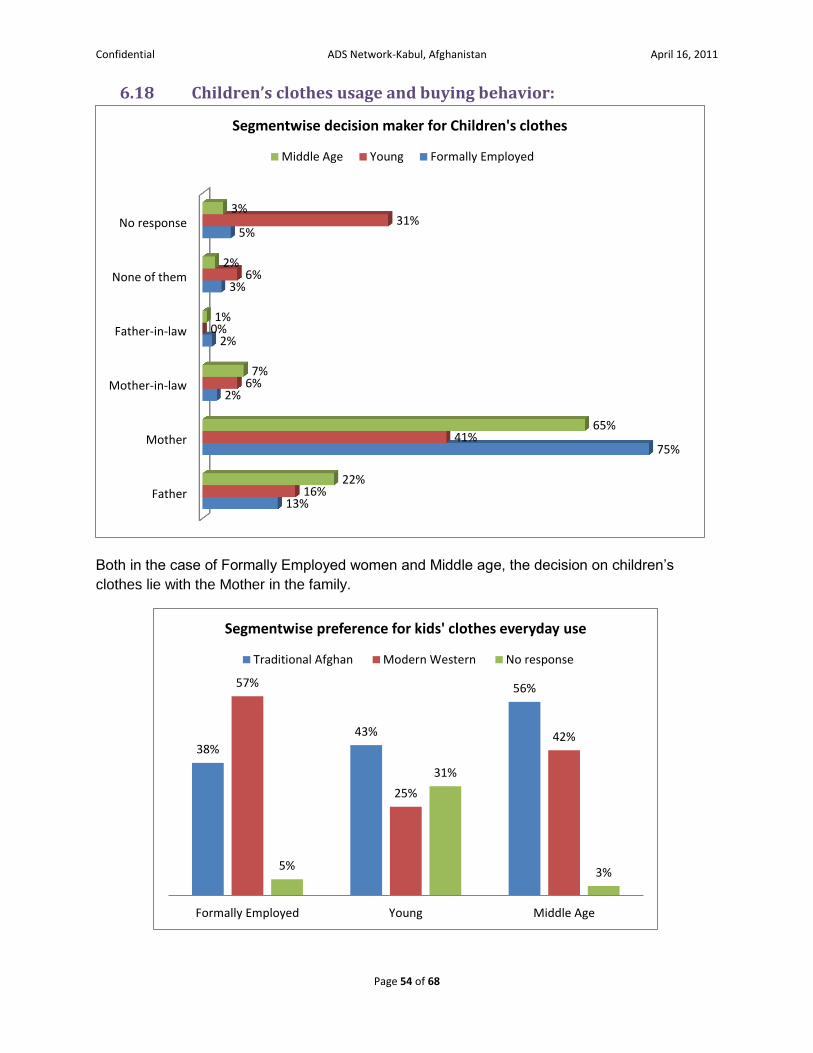

6.18 Children’s clothes usage and buying behavior: .......................................................................... 54

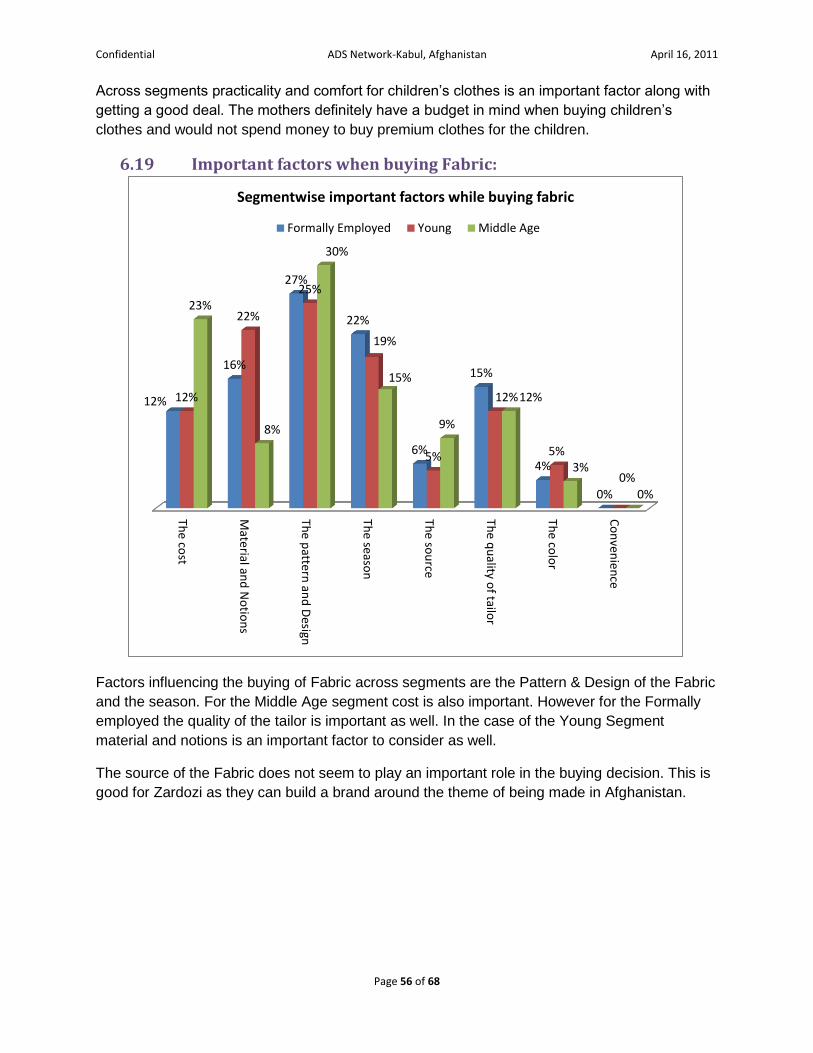

6.19 Important factors when buying Fabric: ...................................................................................... 56

6.20 Segmentwise Multi Dimension scaling for garments- consumer attitudes towards garments: 57

6.21 Segmentwise Concept Card test- Set-A: ..................................................................................... 58

6.22 Concept Card test for Set-B: ....................................................................................................... 59

7. Retailer/Wholesaler/Distribution Survey Key Findings: ..................................................................... 62

7.1 Numbers of years the respondents have been in business: ....................................................... 62

7.2 Type of business, Annual turnover estimates and size of staff kept: ......................................... 63

7.3 Source cities and countries for Garments and Fabric purchases by Channel intermediaries: ... 64

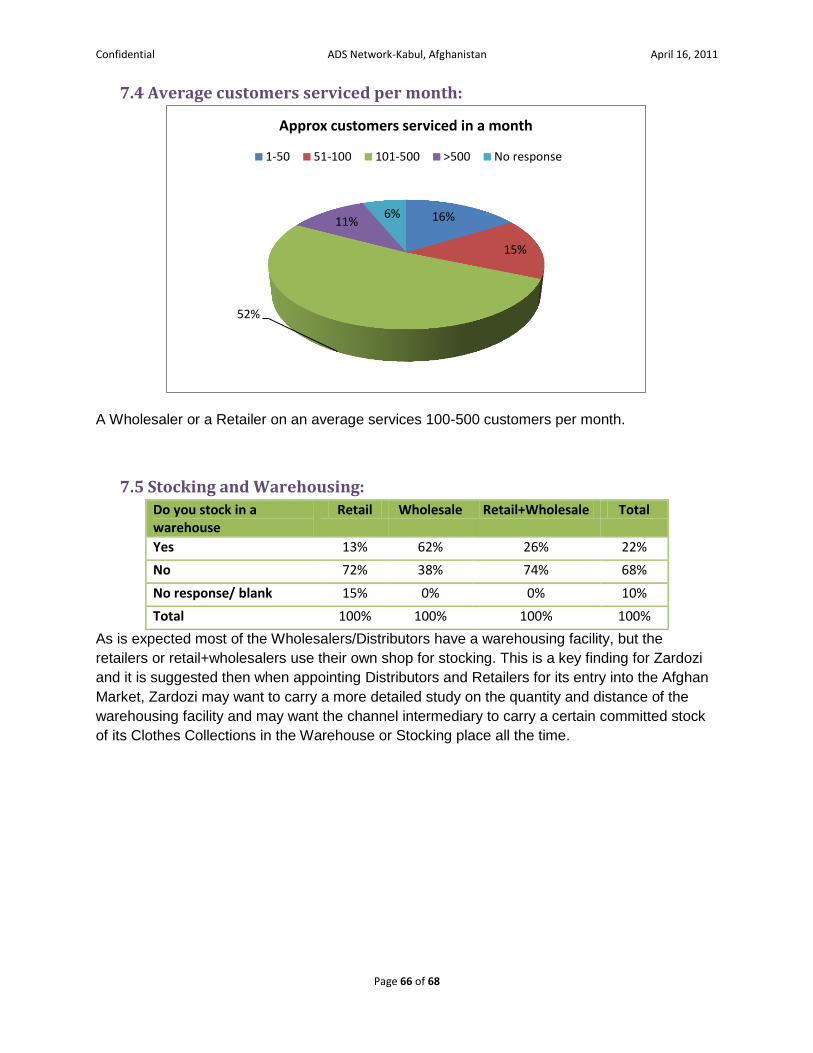

7.4 Average customers serviced per month: .................................................................................... 66

7.5 Stocking and Warehousing: ........................................................................................................ 66

Page 4

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 3 of 68

7.6 Fast moving Garments and Fabrics in the channel: .................................................................... 67

Page 5

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 4 of 68

1. Executive Summary and Key conclusions: 1.1 According to the mandate of the project, ADS Network was given the task to carry out a

comprehensive industry, consumer and trade research that will help the client Zardozi to

make plans to enter the domestic Afghan Market.

1.2 The Garments/fabrics imports market is estimated to be US$122.45 Million for the year

2009/10. With the Afghan GDP ranked no.6 in the top 10 fastest growing GDPs at 8.9%,

this market size is likely to double in the next five years, which makes it an ideal time for

Zardozi to look at entering the domestic Afghan market.

1.3 To understand the garments and fabric business a consumer survey was conducted. It

was conducted in Kabul, Jalalabad and Mazar-e-Sharif. The three segments that were

surveyed were- Young Women below 30, Formally Employed Women over 30, Middle

Age Women over 30 not employed.

1.4 Amongst the most recently purchased garments, respondents said that they purchased

either traditional event’s wear (mostly in Kabul) or winter wear, which had the

seasonality factor because the survey was conducted in winters. The most recently

purchased fabric was Bakhmal, this material was also amongst the fastest selling in the

Distribution survey.

1.5 The consumers tend to buy Fabrics more often than garments, where the purchase

cycle tends to be longer.

1.6 The main market in the city is the place for consumers to buy their garments and

fabrics. The Afghan consumer, whether buying Fabrics or Garments is always looking to

get a good deal. Therefore pricing the Zardozi domestic collection becomes a key

success parameter.

1.7 The Formally Employed and Young Segment tend to purchase garments more

frequently than the Middle Age segment. This coupled with the fact that these two

segments spend more on their purchases than the Middle Age segment makes them

the best two segments for Zardozi to target for their collection. Across segments buying

garments on special occasions is important, especially for Weddings and family get -

togethers.

1.8 We can see that across segments, there is tendency to spend low during Eid, however

when it comes to Nawroz, there is a tendency to spend extra money to buy new clothes.

This is a very important point to consider by Zardozi, they should have a Nawroz

collection by the time next Nawroz is celebrated.

1.9 There is very limited stitching done by women from home or by themselves, an

overwhelming majority gets fabric stitched by tailors, paying the tailors in the range of

Afa.251-750 .

1.10 While Budget is an important criterion for selecting clothes across all segments,

the Formally Employed and Young segment, tend to also get influenced by their

discussions with friends and the style/color/design that catches their eye while

shopping. However in the case of the Middle Age segment, the budget and best deals

are the most significant influencing factors.

Page 6

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 5 of 68

1.11 While the Formally Employed segment prefers to wear Western style outfits in

winters, in summers across all segments the preference is for Punjabi suits. These are

two clear indicators for Zardozi to design its style for the two seasons.

1.12 While the Formally Employed and Young segment prefers Western Style with

light or no embroidery for weddings, the Middle Age segment prefers the more

traditional Afghan style.

1.13 Across all segments, women are the biggest decision makers when it comes to

purchase of clothes, the men do not have any say in this matter. Even for a child’s

clothes purchase the choices are made by the mother.

1.14 Formally Employed women (57%) preferred western style clothes for kids for

their everyday use, while 56% Middle age women preferred Traditional Afghan style.

However across segments women preferred Western Clothes for kids during special

occasions. The Afghan mothers are pretty rational decision makers when it comes to

buying clothes for their kids. They would have a budget in mind, look for the best deals

and practical/comfortable clothes for the kids, rather than go to any length to purchase

clothes.

1.15 Factors influencing the buying of Fabric across segments are the Pattern &

Design of the Fabric and the season. For the Middle Age segment cost is also

important. However for the Formally employed the quality of the tailor is important as

well. In the case of the Young Segment material and notions is an important factor to

consider as well. The source of the Fabric does not seem to play an important role in

the buying decision. This is good for Zardozi as they can build a brand around the

theme of being made in Afghanistan.

1.16 It is recommended for Zardozi, that when launching its Clothes Collection for the

Afghan market, the company should position its collection as providing Afghan women

the confidence and comfort and making them look pretty. These are relevant

dimensions especially for the Formally Employed and Young segment, which should be

the first two segments it should target.

1.17 In the concept card test the Formally Employed and Young segment preferred

the more modern looks of the Punjabi Suits and Coats, whereas the Middle Age

segment preferred the more tone-down Korti Daman style. The Maxi style is not

preferred by any segment.

1.18 The Survey also yielded possible price points at which Zardozi should introduce

its Domestic collection.

1.19 The Distribution Survey was conducted across 210 respondents. 59% of the

channel intermediaries have been in the business from 1-10 years, showing the time

since new government started.

1.20 The Average staff size, whether it is a Retail Outlet or Wholesale Company is

from 1-4.

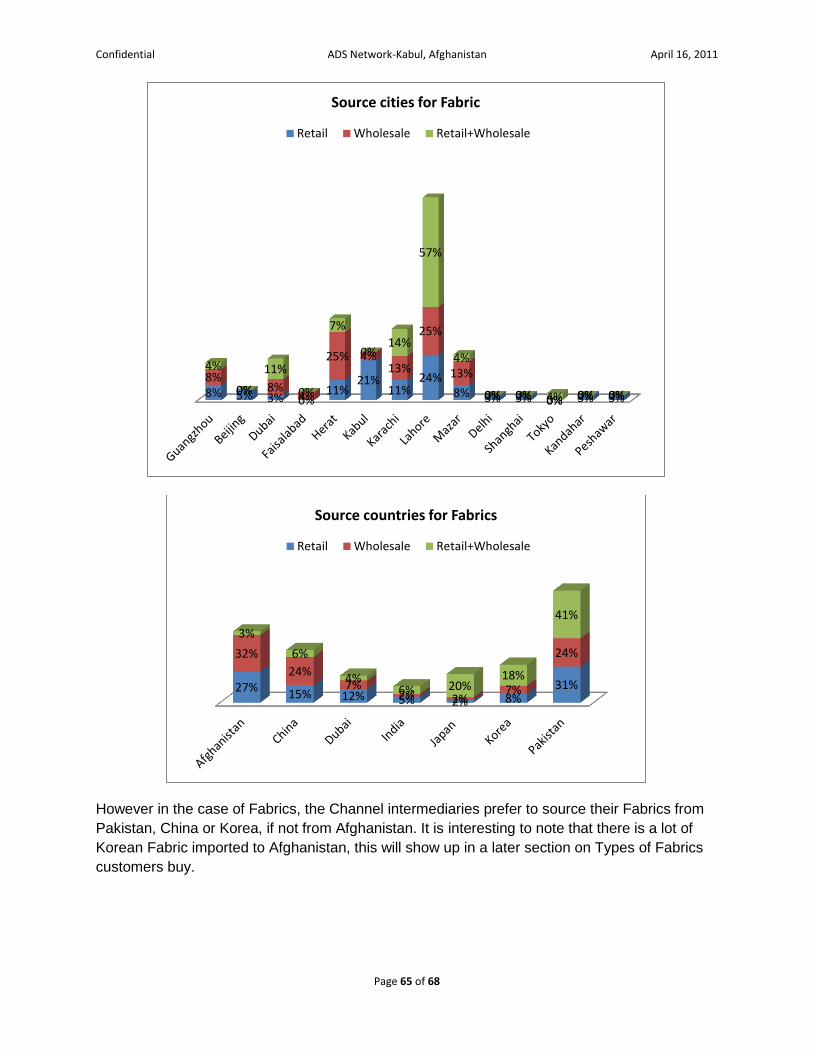

1.21 It is interesting to note that while most of garments are sourced from with

Afghanistan, either Kabul or Mazar, India and China are the big markets from where

garments are imported. But when it comes to fabrics, Pakistan is the country from

where most fabrics are imported. This could also be because the survey left out Herat

which gets imports from Iran as well.

Page 7

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 6 of 68

1.22 The fast moving garments according to the trade are- Anarkalis and Punjabi

Suits. Sharara is also popular. Amongst Fabrics it’s the Bakhmal and velvet that are the

fast moving items. Quality and Fashion are the predominant reasons for these fabrics

and garments to be fast moving.

2. Objective of the Project Zardozi wanted ADS Network to carry out a complete Industry study for the Garments and

Fabric business in Afghanistan. The results of this study and the subsequent recommendations

will be used as an input for Zardozi’s plan to enter the domestic Afghan Market.

3. The research Methodology adopted ADS Network carried out telephonic and personal interviews with industry experts. Secondary

Data was obtained from various sources including the Central Statistical Organization of

Afghanistan on the macro economic factors influencing the garments and fabrics business in

Afghanistan. Client inputs were taken to assess the marketplace.

The research methodology adopted was to carry out two surveys, a. Consumer Survey to

understand women’s and children’s garments and consumer buying behavior, attitudes and

testing of their garments likes and dislikes. b. Distribution survey, conducted amongst, Retailers,

wholesalers and tailors to understand the business dynamics and assess the estimated size of

the trade for fabrics and garments.

The Consumer Survey: was carried out in Kabul, Jalalabad and Mazar-e-Sharif, the three

important markets being considered by Zardozi to launch with their Domestic collection. The

respondents were segmented into- Formally Employed women above 30, Middle Aged women

not working above 30 and young women below 30.

The total Sample size was 500 respondents in the three cities.

The Distribution Survey: was carried out in Kabul city with a total sample size of 200

distribution intermediaries.

In both the surveys the research tool was a close ended questionnaire.

4. The Garments industry overview The Macroeconomic overview of Afghanistan is very positive. Afghanistan has shown rapid

strides in growth since the last 10 years. As per the IMF 2010 World Economic Outlook the GDP

of Afghanistan was estimated to have grown by 9.79%.

Year Gross domestic product based on purchasing-power-parity (PPP) valuation

of country GDP (billion $)

Per cent Change

2002 $11.17

Page 8

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 7 of 68

2003 $13.14 17.61%

2004 $13.67 4.06%

2005 $15.72 14.98%

2006 $17.57 11.75%

2007 $20.65 17.56%

2008 $21.81 5.61%

2009 $26.98 23.67%

2010 $29.62 9.79%

The government of Afghanistan has undertaken the goal as per its ANDS and MDG Strategy to

improve the GDP per capita of Afghanistan from its current level of US$500 per annum to

US$510, However at the rate at which the Afghan GDP is going, by 2015 the GDP per capita for

Afghanistan would be close to US$1,000. Coupled with the growth in GDP per capita and real

GDP, it estimated that the garment segment will expand and double in size in the next 5 years

as per industry sources. Zardozi with its first mover advantage in the marketplace could become

the dominant player and hold a large chunk of this market.

Of the total garments and fabric imports reported, a staggering 89% share is that of Fabric

imports. The remaining 11% is for imports of Garments for all segments. This is not surprising

however, when we look at the traditional Afghan wear for men being always stitched by tailors,

the same can be said for most of the women’s and children’s wear.

Although the CSO Statistical yearbook 2010, reports the figures as per their data collected from

formal sources, however it is obvious that there is a larger portion of the Garment’s market that

goes unreported through informal sources. However, since Zardozi plans to introduce a

Garment’s collection in the domestic market it should look to target a share of the reported

garments Market.

So the reported Garment’s Market is pegged at US$122.45 Million for the year 2009/10. It is

recommended that Zardozi take this as the market size and for its projection take a 10% growth

rate on this base figure for projections in its business plans.

Page 9

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 8 of 68

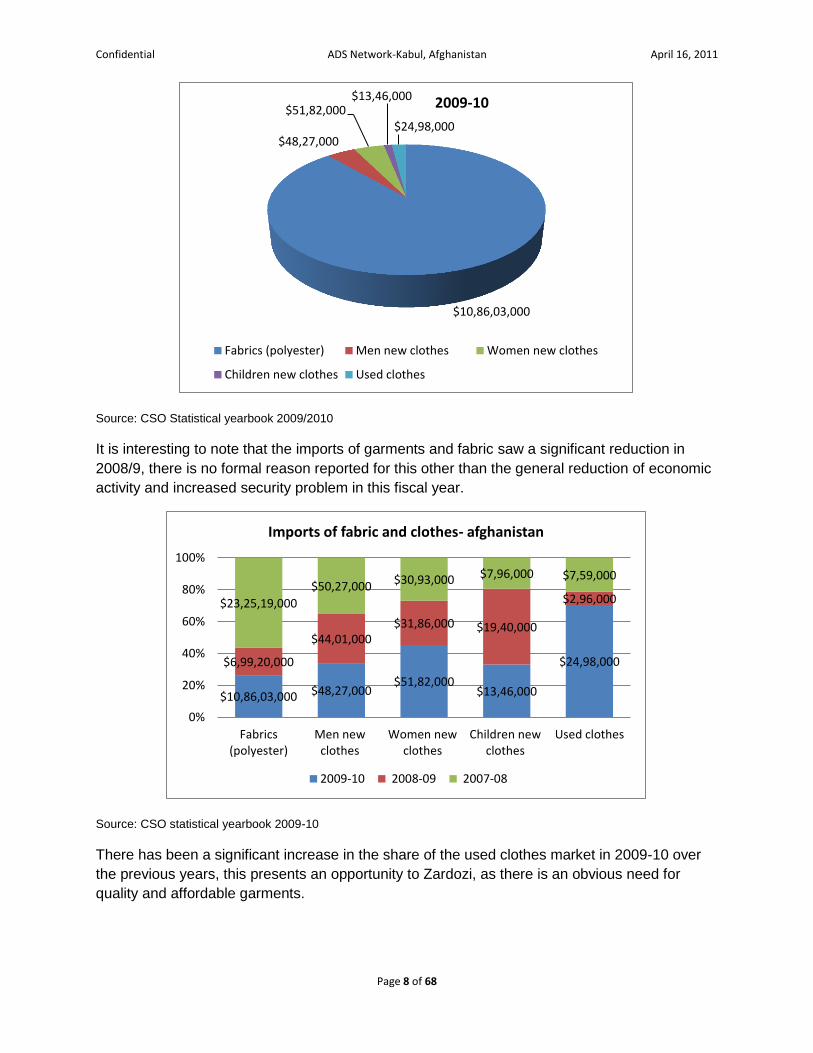

Source: CSO Statistical yearbook 2009/2010

It is interesting to note that the imports of garments and fabric saw a significant reduction in

2008/9, there is no formal reason reported for this other than the general reduction of economic

activity and increased security problem in this fiscal year.

Source: CSO statistical yearbook 2009-10

There has been a significant increase in the share of the used clothes market in 2009-10 over

the previous years, this presents an opportunity to Zardozi, as there is an obvious need for

quality and affordable garments.

$10,86,03,000

$48,27,000

$51,82,000 $13,46,000

$24,98,000

2009-10

Fabrics (polyester) Men new clothes Women new clothes

Children new clothes Used clothes

$10,86,03,000 $48,27,000 $51,82,000

$13,46,000

$24,98,000 $6,99,20,000

$44,01,000 $31,86,000 $19,40,000

$2,96,000 $23,25,19,000

$50,27,000 $30,93,000 $7,96,000 $7,59,000

0%

20%

40%

60%

80%

100%

Fabrics(polyester)

Men newclothes

Women newclothes

Children newclothes

Used clothes

Imports of fabric and clothes- afghanistan

2009-10 2008-09 2007-08

Page 10

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 9 of 68

5. Consumer Research Key Findings: The key findings are structured by Total Afghanistan data, Total Afghanistan split between the 3

segments. Region wise all segments, region wise individual segments.

Total Afghanistan Consumer Survey Findings:

5.1 Respondent Age Profile:

5.2 Marital Status profile:

Base Table for Marital Status profile:

Marital status Kabul Jalalabad Mazar Afghanistan

Married 62% 51% 57% 57%

Single 33% 39% 37% 36%

4% 9%

21%

18% 16%

16%

16%

Respondet Age profile: Afganistan

<18 18-20 21-25 26-30 31-35 36-40 >40

57%

36%

7% 0%

Afghanistan marital status profile

Married Single Divorce/Widow No response

Page 11

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 10 of 68

Divorce/Widow 6% 10% 5% 7%

No response 1% 0% 0% 0%

Total 100% 100% 100% 100%

5.3 Ethnic Profile:

Base Table for Ethnic profile:

Ethnic Group

Kabul Jalalabad Mazar Afghanistan

Pashtun 24% 46% 13% 27%

Tajik 63% 43% 73% 60%

Uzbek 7% 0% 4% 4%

Hazara 7% 2% 5% 5%

Others 0% 3% 3% 2%

Refused 0% 6% 1% 2%

Total 100% 100% 100% 100%

27%

60%

4% 5% 2% 2%

Afghanistan Ethnic Profile

Pashtun Tajik Uzbek Hazara Other Refused

Page 12

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 11 of 68

5.4 Respondents by profession:

Base table of respondents by profession:

Profession Kabul Jalalabad Mazar Afghanistan

Stay at Home 32% 52% 49% 43%

Employed 50% 35% 33% 41%

Student 19% 13% 17% 16%

Total 100% 100% 100% 100%

Of the 43% who stay at home, following is the break-down of how many work or do not work

from home:

Do you work from home Kabul Jalalabad Mazar Afghanistan

Yes 90% 72% 49% 69%

No 0% 27% 50% 27%

Refused 10% 1% 1% 4%

Total 100% 100% 100% 100%

Of the 41% formally employed, following is the break-down of the kind of organizations the

respondents work in:

Employed Kabul Jalalabad Mazar Afghanistan

NGOs/UN 12% 19% 12% 14%

Government 76% 70% 86% 77%

Private Companies 12% 8% 2% 8%

No response 0% 4% 0% 1%

Total 100% 100% 100% 100%

Of the 16% Students, following is the profile of their current education levels:

43%

41%

16%

Afghanistan: respondents by profession

Stay at home Employed Student

Page 13

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 12 of 68

Students Kabul Jalalabad Mazar Afghanistan

High School 14% 95% 81% 54%

In college 76% 5% 19% 41%

No response 11% 0% 0% 5%

Total 100% 100% 100% 100%

5.5 Average family size of the respondents:

Base table for average family size:

Family size Kabul Jalalabad Mazar Afghanistan

One-two 0% 1% 7% 3%

three-five 25% 37% 26% 29%

six-eight 39% 36% 35% 37%

More than eight 37% 25% 32% 32%

Total 100% 100% 100% 100%

It is interesting to note that the family size reported in Jalalabad tends to be smaller than in

Kabul or Mazar.

5.6 Literacy profile of respondents:

2% 29%

37%

32%

Afghanistan: average Family size

One-two three-five

six-eight More than eight

0%

5%

10%

15%

20%

25%

30%

35%

NoFormal

education

1 to 6grade

7 to 9grade

10 to 12grade

University Refused NoResponse

1%

7% 8%

32%

27% 24%

1%

Afghanistan literacy profile

Page 14

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 13 of 68

As per the base table below the high rate of refusal to answer this question came mainly from

Jalalabad:

Literacy levels Kabul Jalalabad Mazar Afghanistan

No Formal education 3% 1% 0% 1%

1 to 6 grade 6% 3% 13% 7%

7 to 9 grade 10% 4% 11% 8%

10 to 12 grade 37% 35% 22% 32%

University 28% 23% 31% 27%

Refused 18% 35% 23% 24%

No Response 0% 1% 1% 1%

Total 100% 100% 100% 100%

5.7 Most recent Garment purchase:

As per the base table, it is interesting to note that while in Kabul the most recently purchased garments

were for events, but in Mazar and Jalalabad, it was winter wear, which is obvious since the survey was

conducted in January/ February period. However the affluence in Kabul can be seen from the fact that

more % respondents in Kabul purchased events wear than the national average:

Garment Recently purchased Kabul Jalalabad Mazar Afghanistan

Traditional event's wear 61% 38% 53% 52%

Summer Every day wear 3% 2% 3% 3%

0%

10%

20%

30%

40%

50%

60% 52%

3%

21%

2%

17%

5% 0%

Afghanistan: Garment most recently purchased

Page 15

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 14 of 68

Winter Every day wear 10% 34% 23% 21%

Summer Office/Professional wear 0% 7% 1% 2%

Winter Office/Professional wear 23% 10% 15% 17%

Girl's traditional clothing (Eid, Nawroz, weddings) 4% 9% 4% 5%

Any other 0% 1% 0% 0%

Total 100% 100% 100% 100%

5.8 Most recently purchased Fabric:

Bakhmal and Pashme seem to be the most popular Fabrics purchased for stitching garments.

5.9 Time since last garment was purchased:

0%

5%

10%

15%

20%

25%

30%

14% 11%

27%

22%

2% 1% 3% 1%

6% 6%

2% 1% 1% 1% 0% 0% 0% 3%

Afghanistan: latest Fabric purchased

0%

5%

10%

15%

20%

25%

30%

1 week ago 2 weeksago

1 monthago

3 monthsago

6 monthsago

1 year agoor more

5%

11%

25% 27%

13%

20%

Afghanistan: Time since last garment was purchased

Page 16

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 15 of 68

On an average 52% of the respondents purchased their last garment between 1 to 3 months

ago.

Base table for the time since last garment was purchased:

Time since last Garment purchased Kabul Jalalabad Mazar Afghanistan

1 week ago 4% 5% 7% 5%

2 weeks ago 10% 13% 10% 11%

1 month ago 24% 20% 31% 25%

3 months ago 25% 27% 29% 27%

6 months ago 10% 20% 11% 13%

1 year ago or more 28% 16% 13% 20%

Total 100% 100% 100% 100%

5.10 Time since last Fabric was purchased:

Like in the case of garment purchase, the average time for purchase of fabric is also between 1

to 3 months.

Base table for time since last Fabric was purchased:

Time since last fabric purchased Kabul Jalalabad Mazar Afghanistan

1 week ago 3% 9% 12% 7%

2 weeks ago 10% 18% 11% 12%

1 month ago 35% 25% 28% 30%

3 months ago 34% 10% 30% 25%

6 months ago 14% 27% 10% 17%

1 year ago or more 6% 12% 9% 8%

No response 0% 0% 1% 0%

Total 100% 100% 100% 100%

0%

5%

10%

15%

20%

25%

30%

1 weekago

2 weeksago

1 monthago

3months

ago

6months

ago

1 yearago ormore

Noresponse

7%

12%

30%

25%

17%

8%

0%

Afghanistan: last time fabric purchased

Page 17

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 16 of 68

Again in the case of Jalalabad, the average time of 1-3 months is less than the National

average.

5.11 Most preferred place for buying garments and fabrics:

Preferred place to purchase Garments Kabul Jalalabad Mazar Afghanistan

From the neighborhood shop 16% 9% 1% 9%

From the main city market 84% 83% 98% 88%

I ask the men in house buy for me 0% 7% 1% 2%

others 1% 1% 0% 0%

Total 100% 100% 100% 100%

Preferred place to buy Fabric Kabul Jalalabad Mazar Afghanistan

From the neighborhood 10% 5% 1% 6%

From the main city market 87% 85% 97% 90%

I ask the men in house buy for me 0% 7% 1% 3%

others 3% 2% 0% 2%

Total 100% 100% 100% 100%

In both the cases for buying garments and fabrics, the respondents prefer to buy them from the

Main City market. Therefore it is important that the Zardozi Collection be present in all the Main

markets where it plans to launch, preferably with high visibility large retail outlets.

5.12 Buying habit for garments:

An overwhelming majority of respondents purchased garments where they got the best deal or

price, indicating a value for money buyer.

Base table indicates this trend across the cities:

4%

85%

9% 2%

Afghanistan: Buying habit for garments

almost always buy from the same Shop

I buy wherever I get the best deal/price

Buying from a shop is less important than the market

I never go to shops and Markets to buy (someone else in the family does)

Page 18

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 17 of 68

Buying habit for garments Kabul Jalalabad Mazar Afghanistan

almost always buy from the same Shop 4% 3% 4% 4%

I buy wherever I get the best deal/price 93% 78% 81% 85%

Buying from a shop is less important than the market

4% 12% 14% 9%

I never go to shops and Markets to buy (someone else in the family does)

0% 7% 1% 2%

Total 100% 100% 100% 100%

5.13 Buying habit for Fabrics:

Just as in the case with garments, in the case of fabrics as well, the buyer is looking for value

for money deals. However unlike garments, in Kabul there is a slight tendency to buy fabric from

a shop regularly visited:

Buying habit for Fabrics Kabul Jalalabad Mazar Afghanistan

almost always buy from the same Shop 10% 4% 1% 5%

I buy wherever I get the best deal/price 88% 77% 89% 85%

Buying from a shop is less important than the market

3% 13% 8% 7%

I never go to shops and Markets to buy (someone else in the family does)

1% 6% 1% 2%

Total 100% 100% 100% 100%

6%

85%

7% 2%

Afghanistan: Buying habit for Fabrics

almost always buy from the same Shop

I buy wherever I get the best deal/price

Buying from a shop is less important than the market

I never go to shops and Markets to buy (someone else in the family does)

Page 19

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 18 of 68

5.14 Frequency of purchase of garments and fabrics:

It is interesting to note that while answering the question about last garment and fabric

purchased the respondents average was between 1 to 3 months. However, a large percentage

while answering the question on frequency of purchase of garments said that they bought

garments for special occasions, whereas percentage who bought Fabrics for special occasions

were relatively less. This shows an interesting behavior pattern, where women tend to buy

garments for special occasions, but would rather buy Fabric and stitch for daily wear.

1%

7%

25%

20% 14%

33%

Afghanistan: frequency of purchase of garments

Evey weeek Once a month

Once in 3 months Once in 6 months

Once a year Definitly on special occassions

0% 12%

30%

37%

8% 13%

Afghanistan: frequency of purchase of fabrics

Evey weeek Once a month

Once in 3 months Once in 6 months

Once a year Definitly on special occassions

Page 20

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 19 of 68

5.15 If garment purchased for Special Occasions, what special

occasions:

What special occasion is Garment purchased

Kabul Jalalabad Mazar Afghanistan

Nawroz 0% 11% 0% 2%

Eid 15% 20% 12% 15%

To go to family weddings 80% 63% 51% 67%

When going on holidays 4% 0% 2% 2%

others 0% 3% 35% 12%

No response/ 1% 3% 0% 1%

Total 100% 100% 100% 100%

Of the 33% respondents who purchased garments for special occasions, a large percentage

(67%) purchased a garment for weddings. This could be a potential area for Zardozi to look

into while developing their Clothes Collection.

5.16 Budget kept for buying garments/fabrics:

There is a tendency to keep a higher budget for garments vis- a- vis fabrics, however a lot of

respondents really don’t have a budget in mind when they go for shopping of garments or

fabrics.

5.17 Frequency of purchase of wedding clothing:

Frequency of Purchase of New clothing for weddings

Kabul Jalalabad Mazar Afghanistan

Rarely 7% 1% 24% 10%

Occasionally 64% 70% 41% 59%

Don’t know/ care

budget of<Afa 1,000

budget of<Afa 2,000

budget of<Afa 5,000

budget of<Afa 7,500

budget of<Afa

10,000

exceedsAFA

10,000

Noresponse

35%

25% 29%

5% 5% 2% 1% 0%

51%

33%

8% 6% 1% 0% 0% 0%

Budget kept for buying garments/fabrics: Afghanistan

Garments Fabrics

Page 21

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 20 of 68

Often 12% 21% 18% 16%

Every wedding 17% 9% 17% 15%

No response 1% 0% 0% 0%

While purchase of new garments is mostly for special occasions like Weddings, however the

frequency of purchase of new clothing is occasional, very few respondents purchase new

clothing for every wedding.

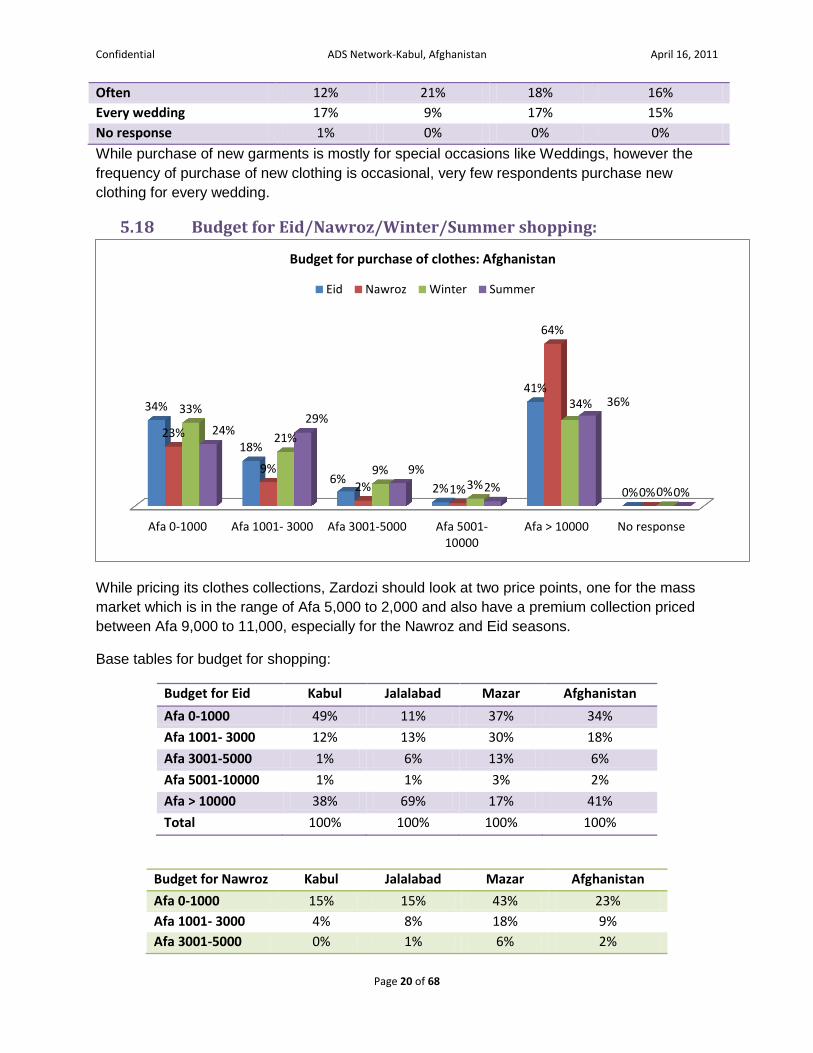

5.18 Budget for Eid/Nawroz/Winter/Summer shopping:

While pricing its clothes collections, Zardozi should look at two price points, one for the mass

market which is in the range of Afa 5,000 to 2,000 and also have a premium collection priced

between Afa 9,000 to 11,000, especially for the Nawroz and Eid seasons.

Base tables for budget for shopping:

Budget for Eid Kabul Jalalabad Mazar Afghanistan

Afa 0-1000 49% 11% 37% 34%

Afa 1001- 3000 12% 13% 30% 18%

Afa 3001-5000 1% 6% 13% 6%

Afa 5001-10000 1% 1% 3% 2%

Afa > 10000 38% 69% 17% 41%

Total 100% 100% 100% 100%

Budget for Nawroz Kabul Jalalabad Mazar Afghanistan

Afa 0-1000 15% 15% 43% 23%

Afa 1001- 3000 4% 8% 18% 9%

Afa 3001-5000 0% 1% 6% 2%

Afa 0-1000 Afa 1001- 3000 Afa 3001-5000 Afa 5001-10000

Afa > 10000 No response

34%

18%

6% 2%

41%

0%

23%

9%

2% 1%

64%

0%

33%

21%

9% 3%

34%

0%

24% 29%

9%

2%

36%

0%

Budget for purchase of clothes: Afghanistan

Eid Nawroz Winter Summer

Page 22

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 21 of 68

Afa 5001-10000 0% 0% 4% 1%

Afa > 10000 82% 75% 29% 64%

Total 100% 100% 100% 100%

Budget for Winter Clothes

Kabul Jalalabad Mazar Afghanistan

Afa 0-1000 56% 15% 20% 33%

Afa 1001- 3000 12% 19% 37% 21%

Afa 3001-5000 1% 14% 14% 9%

Afa 5001-10000 0% 1% 9% 3%

Afa > 10000 32% 50% 21% 34%

No response 1% 0% 0% 0%

Total 100% 100% 100% 100%

Budget for summer clothes

Kabul Jalalabad Mazar Afghanistan

Afa 0-1000 35% 14% 21% 24%

Afa 1001- 3000 35% 23% 28% 29%

Afa 3001-5000 7% 11% 10% 9%

Afa 5001-10000 0% 1% 5% 2%

Afa > 10000 24% 51% 36% 36%

Total 100% 100% 100% 100%

5.19 Fabric stitching behavior:

Fabric stitched by self Kabul Jalalabad Mazar Afghanistan

Yes 20% 20% 23% 21%

No 81% 79% 77% 79%

No response 0% 1% 0% 0%

Total 100% 100% 100% 100%

Overwhelming 79% respondents get their fabrics stitched by someone other than themselves.

Who stitches the Fabric Kabul Jalalabad Mazar Afghanistan

My tailor 78% 94% 83% 84%

Someone in the family 22% 5% 17% 15%

No response 0% 1% 0% 0%

Total 100% 100% 100% 100%

84% respondents get their Fabrics stitched by a tailor. When entering the Afghan market

Zardozi could look at creating special Retail outlets, where women can buy the garment and get

Page 23

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 22 of 68

it stitched from the Retail outlet itself as one of its possible innovations, apart from a ready-

made garment collection.

Prices for stitching Fabric

Kabul Jalalabad Mazar Afghanistan

I pay about Afa 100 0% 3% 2% 1%

Between Afa 101-250 19% 22% 24% 22%

251-500 58% 39% 47% 49%

501-750 21% 22% 18% 20%

751- 1000 2% 13% 1% 5%

>1000 1% 1% 7% 3%

Total 100% 100% 100% 100%

Time take to stitch

Kabul Jalalabad Mazar Afghanistan

1 day 0% 0% 1% 0%

2 days 2% 13% 3% 6%

1 week 56% 71% 67% 64%

1 month 41% 16% 23% 28%

No response 2% 0% 5% 2%

Total 100% 100% 100% 100%

The table above shows that the average time to stitch a cloth from fabric is 1 week. Again, to

point out, Zardozi could innovate with certain Retail Outlets, where a customer can buy a fabric

and stitch a garment within a day or two.

Of those who knew how to stitch (21%), following table illustrates where they learnt the skill:

Who taught stitching Kabul Jalalabad Mazar Afghanistan

My mother 44% 27% 29% 34%

My grandmother 3% 7% 0% 3%

Someone amongst my relatives 13% 30% 46% 29%

I taught myself 21% 23% 14% 19%

I learnt it formally in an NGO 18% 7% 9% 12%

No response 3% 7% 3% 4%

Total 100% 100% 100% 100%

Those respondents (12%) who learnt the skill of stitching learnt it either at Bagh-e-Zanana or

National Solidarity NGO.

Page 24

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 23 of 68

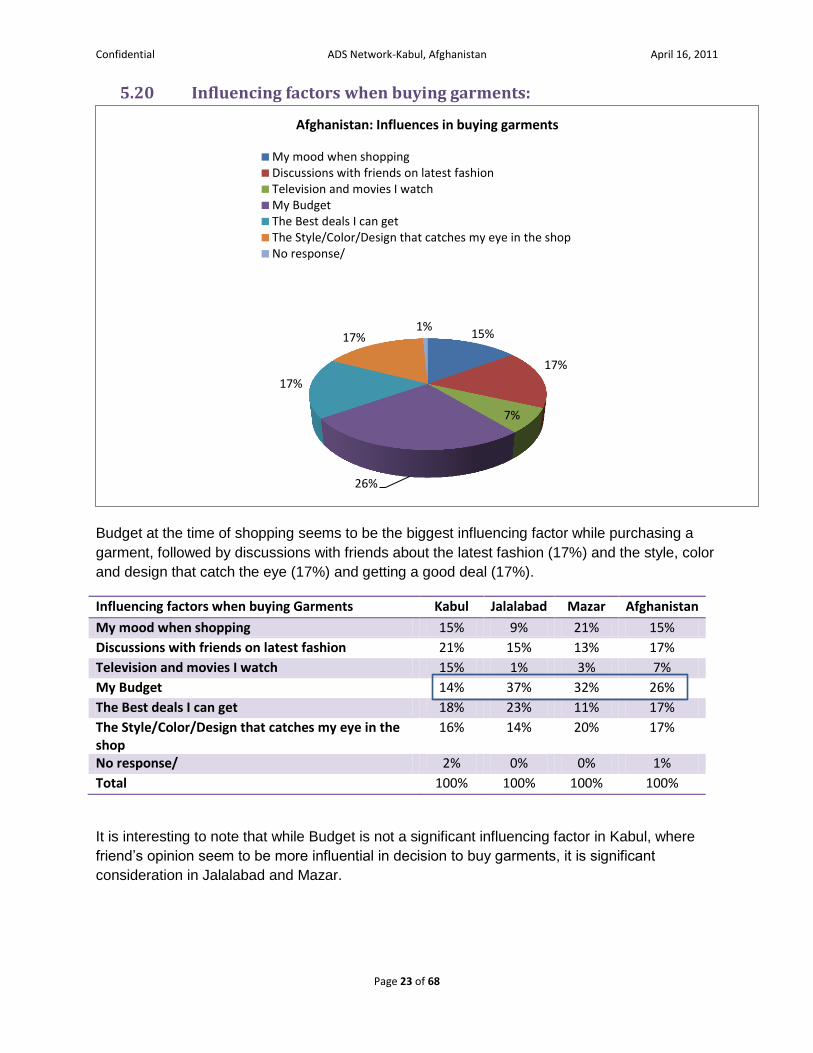

5.20 Influencing factors when buying garments:

Budget at the time of shopping seems to be the biggest influencing factor while purchasing a

garment, followed by discussions with friends about the latest fashion (17%) and the style, color

and design that catch the eye (17%) and getting a good deal (17%).

Influencing factors when buying Garments Kabul Jalalabad Mazar Afghanistan

My mood when shopping 15% 9% 21% 15%

Discussions with friends on latest fashion 21% 15% 13% 17%

Television and movies I watch 15% 1% 3% 7%

My Budget 14% 37% 32% 26%

The Best deals I can get 18% 23% 11% 17%

The Style/Color/Design that catches my eye in the shop

16% 14% 20% 17%

No response/ 2% 0% 0% 1%

Total 100% 100% 100% 100%

It is interesting to note that while Budget is not a significant influencing factor in Kabul, where

friend’s opinion seem to be more influential in decision to buy garments, it is significant

consideration in Jalalabad and Mazar.

15%

17%

7%

26%

17%

17% 1%

Afghanistan: Influences in buying garments

My mood when shoppingDiscussions with friends on latest fashionTelevision and movies I watchMy BudgetThe Best deals I can getThe Style/Color/Design that catches my eye in the shopNo response/

Page 25

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 24 of 68

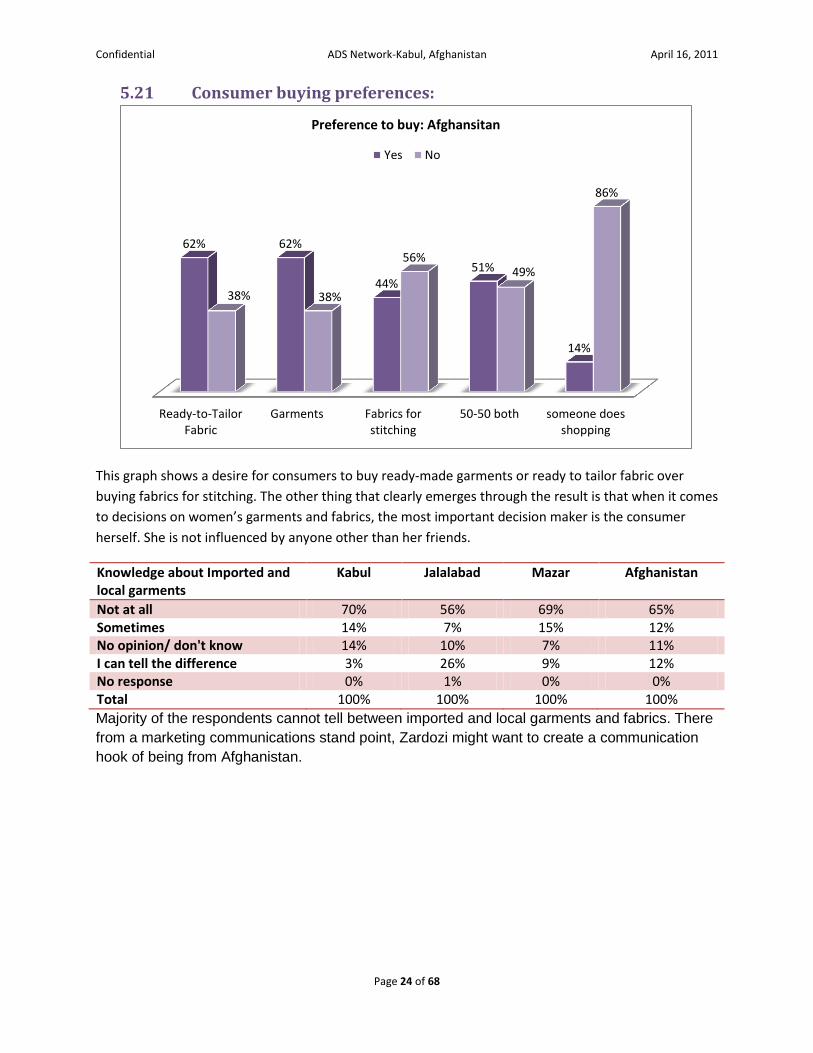

5.21 Consumer buying preferences:

This graph shows a desire for consumers to buy ready-made garments or ready to tailor fabric over

buying fabrics for stitching. The other thing that clearly emerges through the result is that when it comes

to decisions on women’s garments and fabrics, the most important decision maker is the consumer

herself. She is not influenced by anyone other than her friends.

Knowledge about Imported and local garments

Kabul Jalalabad Mazar Afghanistan

Not at all 70% 56% 69% 65% Sometimes 14% 7% 15% 12% No opinion/ don't know 14% 10% 7% 11% I can tell the difference 3% 26% 9% 12% No response 0% 1% 0% 0% Total 100% 100% 100% 100%

Majority of the respondents cannot tell between imported and local garments and fabrics. There

from a marketing communications stand point, Zardozi might want to create a communication

hook of being from Afghanistan.

Ready-to-TailorFabric

Garments Fabrics forstitching

50-50 both someone doesshopping

62% 62%

44% 51%

14%

38% 38%

56% 49%

86%

Preference to buy: Afghansitan

Yes No

Page 26

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 25 of 68

5.22 Style preference by Season:

While in winters the clothing style does not really matter, there is a clear preference for Punjabi

Suits during summers. This could also be because; summer-time Afghan families like to do

picnics and other outdoor activities. Zardozi should have a big summer collection influenced by

the Punjabi Suit style.

Base tables for Style preferences in winters and summers:

Style preference winter Kabul Jalalabad Mazar Afghanistan

Traditional afghan clothes 3% 16% 25% 14%

Western style clothes 43% 3% 37% 29%

Punjabi Suits 20% 28% 15% 21%

Doesn't matter 35% 53% 22% 36%

Total 100% 100% 100% 100%

Style preferences for summers

Kabul Jalalabad Mazar Afghanistan

Traditional afghan clothes 6% 7% 14% 9%

Western style clothes 8% 1% 13% 7%

Punjabi Suits 76% 81% 60% 73%

Doesn't matter 11% 10% 13% 11%

Total 100% 100% 100% 100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Traditional afghanclothes

Western styleclothes

Punjabi Suits Doesn't matter

14%

29% 21%

36%

9% 7%

73%

11%

Afghanistan: Style preference by season

Winter Summer

Page 27

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 26 of 68

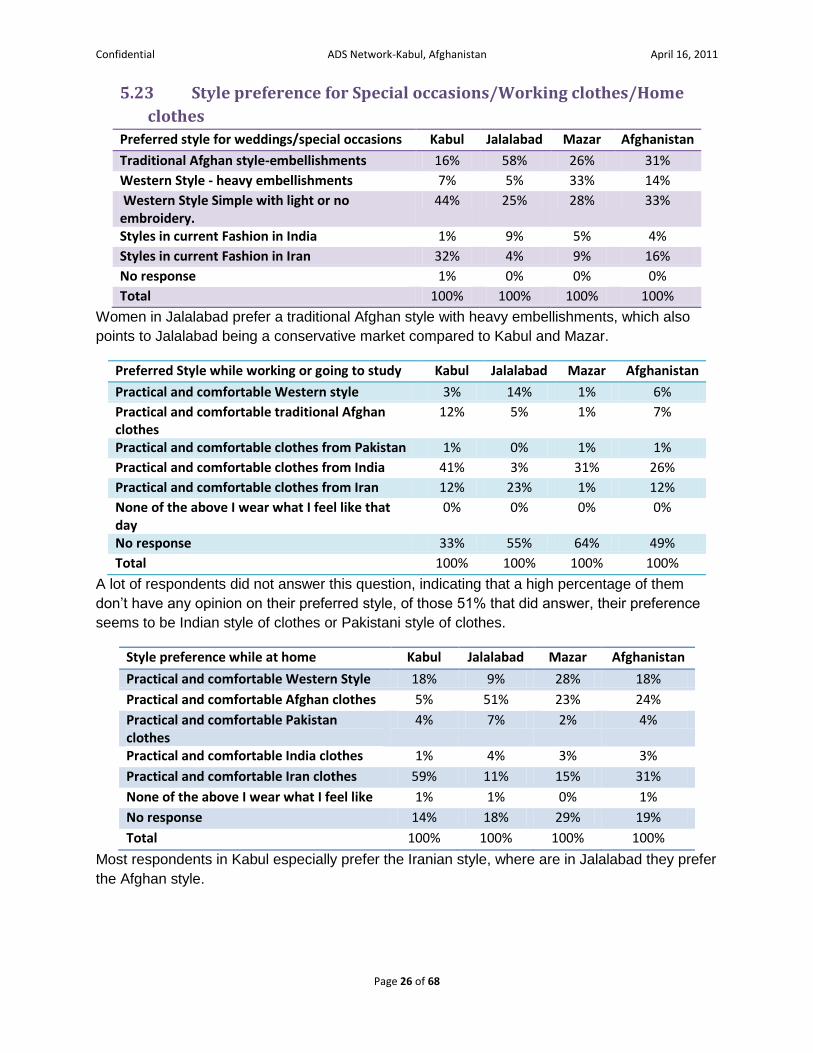

5.23 Style preference for Special occasions/Working clothes/Home

clothes

Preferred style for weddings/special occasions Kabul Jalalabad Mazar Afghanistan

Traditional Afghan style-embellishments 16% 58% 26% 31%

Western Style - heavy embellishments 7% 5% 33% 14%

Western Style Simple with light or no embroidery.

44% 25% 28% 33%

Styles in current Fashion in India 1% 9% 5% 4%

Styles in current Fashion in Iran 32% 4% 9% 16%

No response 1% 0% 0% 0%

Total 100% 100% 100% 100%

Women in Jalalabad prefer a traditional Afghan style with heavy embellishments, which also

points to Jalalabad being a conservative market compared to Kabul and Mazar.

Preferred Style while working or going to study Kabul Jalalabad Mazar Afghanistan

Practical and comfortable Western style 3% 14% 1% 6%

Practical and comfortable traditional Afghan clothes

12% 5% 1% 7%

Practical and comfortable clothes from Pakistan 1% 0% 1% 1%

Practical and comfortable clothes from India 41% 3% 31% 26%

Practical and comfortable clothes from Iran 12% 23% 1% 12%

None of the above I wear what I feel like that day

0% 0% 0% 0%

No response 33% 55% 64% 49%

Total 100% 100% 100% 100%

A lot of respondents did not answer this question, indicating that a high percentage of them

don’t have any opinion on their preferred style, of those 51% that did answer, their preference

seems to be Indian style of clothes or Pakistani style of clothes.

Style preference while at home Kabul Jalalabad Mazar Afghanistan

Practical and comfortable Western Style 18% 9% 28% 18%

Practical and comfortable Afghan clothes 5% 51% 23% 24%

Practical and comfortable Pakistan clothes

4% 7% 2% 4%

Practical and comfortable India clothes 1% 4% 3% 3%

Practical and comfortable Iran clothes 59% 11% 15% 31%

None of the above I wear what I feel like 1% 1% 0% 1%

No response 14% 18% 29% 19%

Total 100% 100% 100% 100%

Most respondents in Kabul especially prefer the Iranian style, where are in Jalalabad they prefer

the Afghan style.

Page 28

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 27 of 68

5.24 Key decision maker for clothes purchase in the family

In cases where the family is a joint family, the key decision maker tends to be the mother, when

it comes to buying clothes for the kids.

Base table:

Key Decision maker while buying clothes in the family for kids

Kabul Jalalabad Mazar Afghanistan

Father 10% 17% 29% 17%

Mother 77% 61% 52% 65%

Mother-in-law 3% 11% 2% 5%

Father-in-law 2% 0% 0% 1%

None of them 1% 3% 5% 3%

No response 7% 8% 12% 8%

Total 100% 100% 100% 100%

5.25 Children’s clothes buying behavior:

Type of clothes preferred for Kids

Kabul Jalalabad Mazar Afghanistan

Traditional Afghan 34% 68% 44% 47%

Modern Western 60% 24% 45% 45%

No response 6% 8% 12% 8%

Total 100% 100% 100% 100%

17%

65%

5% 1% 3%

8%

0%

10%

20%

30%

40%

50%

60%

70%

Key Decision maker in family while buying clothes for kids: Afghansitan

Page 29

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 28 of 68

Traditional Afghan clothes are preferred more in Jalalabad, where as in Kabul modern western

clothes are preferred. In Mazar, there is an equal split between the two.

Type of clothes preferred for Kids during special occasions

Kabul Jalalabad Mazar Afghanistan

Traditional Afghan 13% 54% 19% 27%

Modern Western 80% 38% 69% 65%

No response 7% 8% 12% 8%

Total 100% 100% 100% 100%

During special occasions both in Mazar and Kabul western clothes are preferred, whereas in

Jalalabad it is the traditional Afghan clothes that are preferred.

On the important considerations while buying Children’s clothes, four dimensions were taken.

The ideal score is 5 for Agree Completely. From the above radar map, we can see that comfort

and practicality are the most important dimensions for parents while buying children’s clothes.

Again to underscore the price sensitivity of the market, the fourth dimension of “Budget being

not important” a lot of people’s opinion is that it is important. Zardozi is recommended to do

special focus groups and trials while making the Children’s clothes collections to test these two

dimensions along with the appropriate price points to cater to.

2.79

4.45

4.30

2.77 0.00

1.00

2.00

3.00

4.00

5.00Importance of Budget

Comfort & pacticality

Best Deals

The right clothes

Important considerations when buying Children's clothes

Kabul Jalalabad Mazar Afghanistan

Page 30

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 29 of 68

5.26 The most important factor when buying a Fabric:

The pattern and design, followed by the season are the two most important factors while buying

a Fabric.

Base table:

Most important factor while buying Fabric

Kabul Jalalabad Mazar Afghanistan

The cost 12% 29% 7% 15%

Material and Notions 13% 15% 19% 15%

The pattern and design 23% 17% 43% 27%

The season 24% 15% 15% 19%

The source 9% 5% 4% 6%

The quality of tailor 16% 14% 9% 13%

The color 5% 5% 2% 4%

Convenience 0% 0% 0% 0%

Total 100% 100% 100% 100%

16%

15%

27%

19%

6%

13% 4% 0%

Afghanistan: Most important factor when buying a fabric

The cost Material and Notions The pattern and design

The season The source The quality of tailor

The color Convenience

Page 31

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 30 of 68

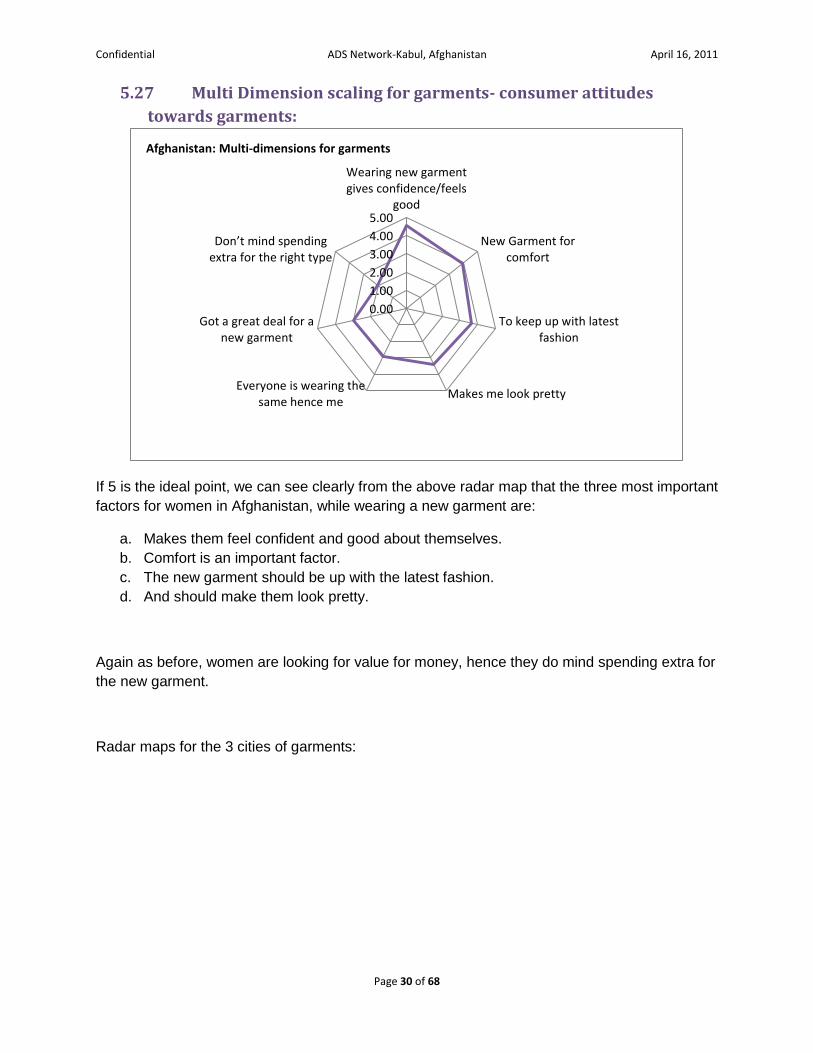

5.27 Multi Dimension scaling for garments- consumer attitudes

towards garments:

If 5 is the ideal point, we can see clearly from the above radar map that the three most important

factors for women in Afghanistan, while wearing a new garment are:

a. Makes them feel confident and good about themselves.

b. Comfort is an important factor.

c. The new garment should be up with the latest fashion.

d. And should make them look pretty.

Again as before, women are looking for value for money, hence they do mind spending extra for

the new garment.

Radar maps for the 3 cities of garments:

0.00

1.00

2.00

3.00

4.00

5.00

Wearing new garmentgives confidence/feels

good

New Garment forcomfort

To keep up with latestfashion

Makes me look prettyEveryone is wearing the

same hence me

Got a great deal for anew garment

Don’t mind spending extra for the right type

Afghanistan: Multi-dimensions for garments

Page 32

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 31 of 68

0.00

1.00

2.00

3.00

4.00

5.00

Wearing newgarment gives

confidence/feels…

New Garment forcomfort

To keep up withlatest fashion

Makes me lookpretty

Everyone is wearingthe same hence me

Got a great deal fora new garment

Don’t mind spending extra for

the right type

Kabul

0.00

1.00

2.00

3.00

4.00

5.00

Wearing newgarment gives…

New Garment forcomfort

To keep up withlatest fashion

Makes me lookpretty

Everyone is wearingthe same hence me

Got a great deal fora new garment

Don’t mind spending extra for …

Jalalabad

Page 33

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 32 of 68

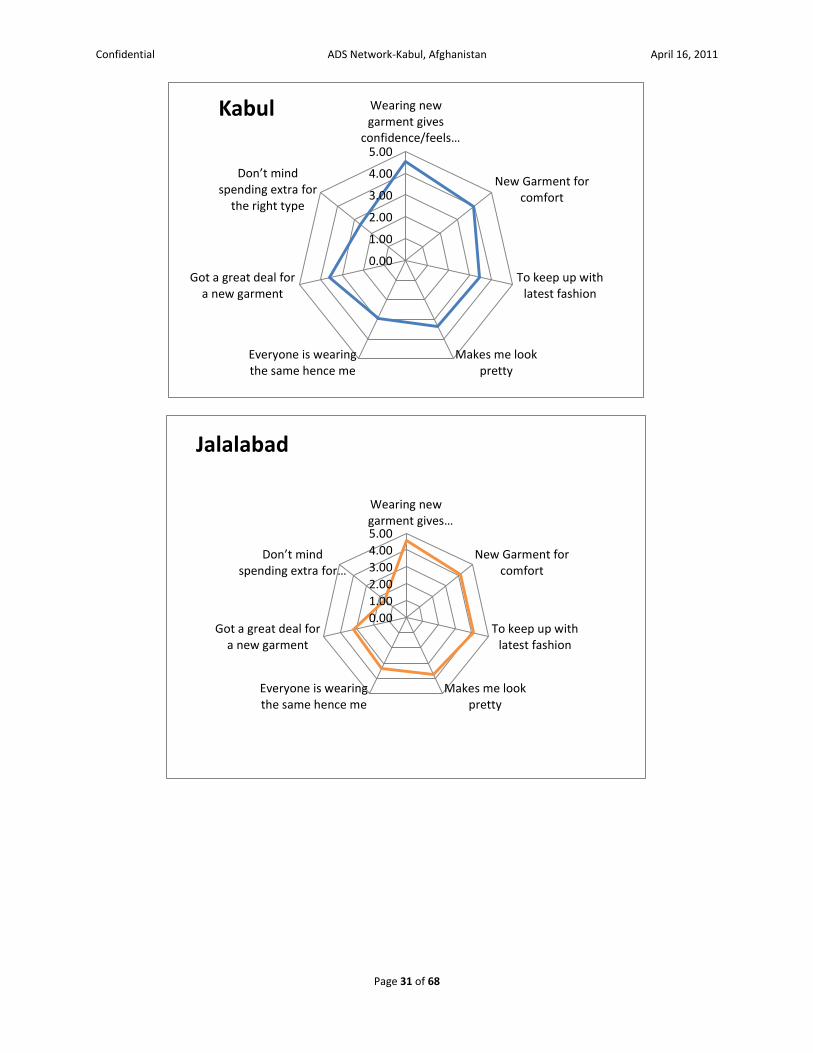

As we can see, in Kabul, the women do have a tendency to look for good deals when buying a

new garment, more than the national average. Not so in Mazar and Jalalabad.

5.28 Concept card test: SET-A

Respondents were shown the following concept cards to take their opinions in SET-A:

0.00

1.00

2.00

3.00

4.00

5.00

Wearing newgarment gives

confidence/feels…

New Garment forcomfort

To keep up withlatest fashion

Makes me lookpretty

Everyone is wearingthe same hence me

Got a great deal fora new garment

Don’t mind spending extra for

the right type

Mazar

4.54

4.27

3.97

4.29

3.77

3.71

4.01

3.82

3.92

3.34

3.69

3.68

Kabul

Jalalabad

Mazar

Afghanistan

1 1.5 2 2.5 3 3.5 4 4.5 5

1: I love the Design, 2: I just like it, 3:Doesn't impress me, 4:I dislike it, 5: I totally dislike it.

Set-A: Concept Card results

Pic-3

Pic-2

Pic-1

Page 34

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 33 of 68

SET-A PIC-1

Set-A PIC-2

Page 35

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 34 of 68

Set-A PIC-3

PIC-1 was the most popular in all the cities, except for Mazar, where Pic-2 was favored.

Following tables illustrate the price points the respondents were willing to pay for each of the

Pics in the Set-A shown above:

0%10%20%30%40%50%60%70%80%90%

88%

10% 2% 0%

78%

18%

3% 0%

88%

8% 4% 0%

Afghanistan: price points to pay for concept card style

Pic-1 Pic-2 Pic-3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Afa 1000- 2000

Afa 2001-5000

Afa 5001-10000

Noresponse

93%

6% 1% 0%

92%

7% 1% 0%

97%

1% 2% 0%

Mazar: Price points to pay for concept card style

Pic-1 Pic-2 Pic-3

Page 36

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 35 of 68

It is interesting to note here, that while for Pic-1: the coat the price range customers are willing

to pay is between Afa 1,000- 2,000 range, for the Korti Daman, there is a certain percentage,

especially in Kabul (31%) who are willing to pay between Afa 2,000- 5,000.

While in Mazar a lot of people liked the Korti Daman, however they are not willing to pay more

than Afa.2,000 for the same. It is suggested that with a good marketing and quality product

Zardozi can price the Coat (Pic-1) and Shirt (Pic-3) around the Afa.2,500 price range and the

Korti Daman at around Afa.4,000 range.

5.29 Concept Card test- Set-B: In the Concept Card Set-B following were the pictures shown to the respondents to take their

view on the dimensions of cut, style, overall look, contemporary look, like/dislike of the pictures:

Set-B PIC-1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Afa 1000- 2000

Afa2001-5000

Afa5001-10000

Noresponse

91%

9% 1% 0%

83%

13% 3% 1%

83%

11% 5% 1%

Jalalabad:price points to pay for concept card style

Pic-1 Pic-2 Pic-3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Afa 1000- 2000

Afa2001-5000

Afa5001-10000

Noresponse

83%

15%

3% 0%

65%

31%

5% 0%

84%

11% 6%

0%

Kabul: price points to pay for concept card style

Pic-1 Pic-2 Pic-3

Page 37

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 36 of 68

Set-B Pic-2

Set-B PIC-3

Page 38

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 37 of 68

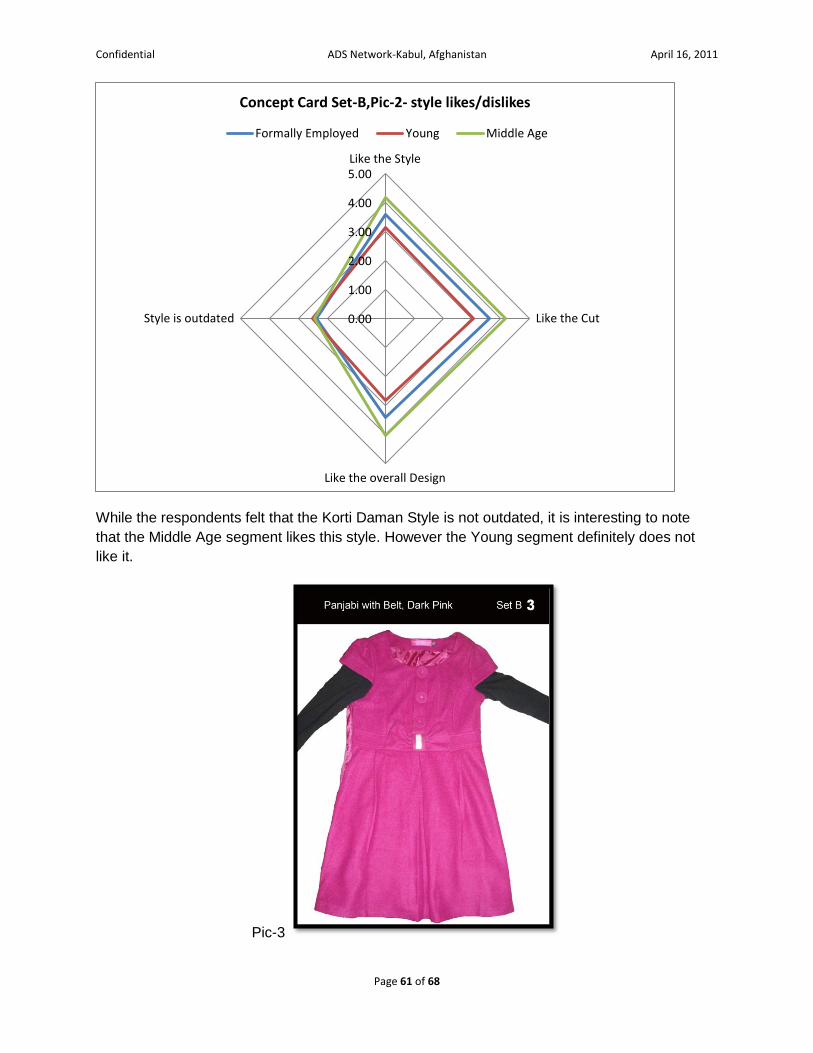

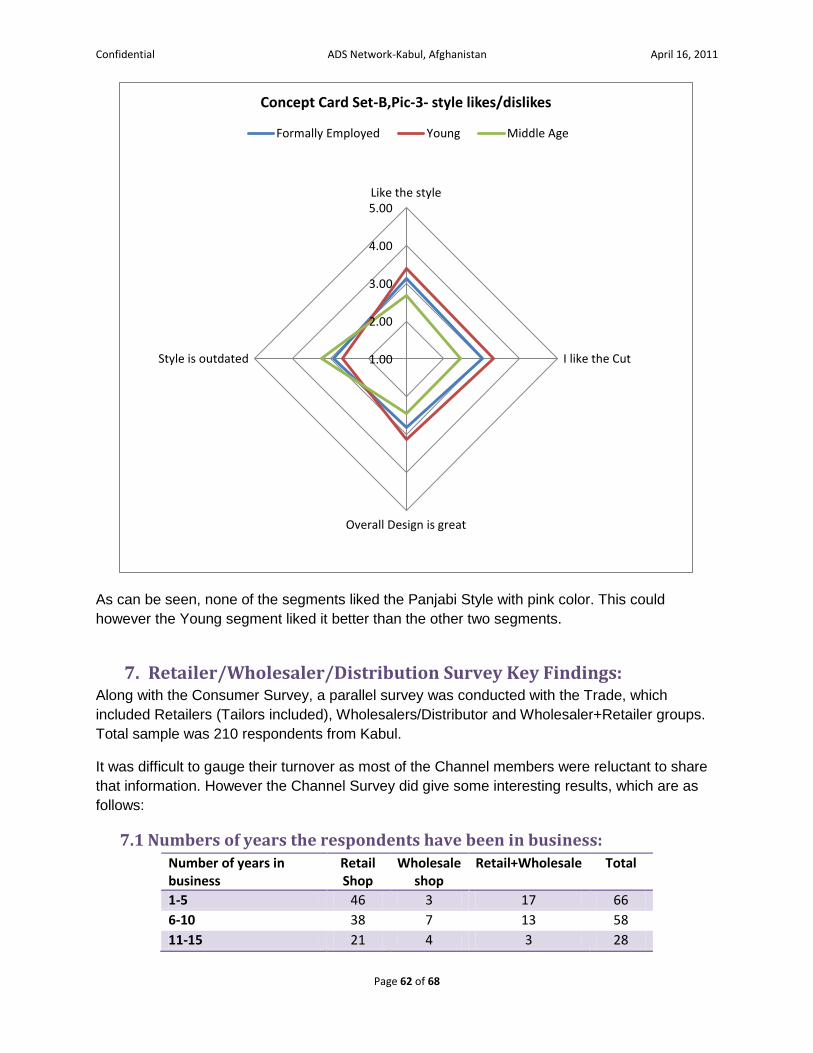

It is interesting to note that Pic-2, which is the Korti Daman was liked by the respondents, where are Pic-

1 Maxi skirt was not liked at all with high points for the dimension “will never wear this” and “style is

outdated’.

6. Consumer Research Key Findings by Segment The main aim in this section is the find out consumer behavior trends and attitudes by

segments. As per research plan, the 3 significant Women segment that were researched were,

Formally Employed women, Young women (students or staying at home), and Middle Age

women over the age of 30 years mostly not working or working from home. The key results are

as follows:

6.1 Segment wise Age Distribution: The respondents’ age grouping is as follows:

0.00

1.00

2.00

3.00

4.00

5.00Like the style

Like the cut

Like theoverall design

Style isoutdated

will neverwear this

Afghanistan: Concept Card set-B dimensions comparison

Set-B: Pic-1

Set-B: Pic-2

Set-B: Pic-3

1% 2%

22% 27%

21% 14% 15%

11%

28%

41%

18%

1% 1% 0% 1% 0% 0% 5%

25%

34% 35%

<18 18-20 21-25 26-30 31-35 36-40 >40

Segment wise Age Distribution

Formally Employed Young Middle age

Page 39

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 38 of 68

From the above chart we can see that the Formally Employed segment is well distributed in the

over 30 age group as per the research brief, the same pattern follows for the Middle age group.

Young women were taken to be 30 years or less.

6.2 Segment wise marital status and ethnic grouping:

6.3 Other Demographic patterns by segment: Profession:

Profession Formally Employed

Young Middle Age

Total

I stay at home 0 65 150 215

I am employed 200 3 0 203

59%

37%

4% 0%

32%

66%

1% 1%

80%

4% 16%

0%

Segmentwise Marital status

Formally Working Young Middle Age

27%

60%

4% 7%

2% 2%

32%

54%

4% 3% 3% 4%

23%

67%

4% 4% 2% 1%

Pashtun Tajik Uzbek Hazara Others Refused

Segmentwise Ethnic grouping

Formally Employed Young Middle Age

Page 40

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 39 of 68

I am a student 0 82 0 82

Total 200 150 150 500

Nature of Formally Employed women’s work:

Family Size by segment:

It is interesting to note that 75% of Middle age Segment has a large family size- 6 people or

above, where as 72% of Formally Employed Segment has family size less than 6. This patterns

also reflects in the Education profile shown in the graph below. However when referring to the

point 5.6 page 9 of this report, the regional literacy profile is fairly consistent across the cities,

therefor the assumption of Kabul being bigger than the other two cities, therefore having more

14%

77%

8% 1%

Formally Employed women's nature of employment

NGOs/ UN Government Private companies No response

0% 10% 20% 30% 40% 50%

1-2

3-5

6-8

>8

3%

31%

41%

26%

4%

31%

35%

29%

1%

24%

33%

42%

Segmentwise family size

Middle Age Young Fomally Employed

Page 41

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 40 of 68

formally employed or literate women does not hold good. The family size and literacy levels

between Middle-Age and Formally Employed are a significant insight for Zardozi.

A large percent of Middle Age segment refused to tell their education level (we can safely

assume that these are illiterate women who don’t want to reveal that they don’t have any formal

education), where as those that did reveal only 2% went up till university vis-à-vis 51% of

Formally Employed segment.

The Family size and Literacy profile of the women is significant to Zardozi, as the most attractive

segment for them to launch their domestic Clothes collection becomes Formally Employed

Women Segment, who have smaller Family Size, therefore higher disposable income and

higher education level, therefore the ability to be early adopters in the Product Life Cycle.

0% 10% 20% 30% 40% 50% 60%

No formal Education

1 to 6 Grade

7-9 Grade

10-12 Grade

University

Refused

No response

1%

2%

2%

44%

51%

2%

0%

1%

6%

13%

37%

21%

21%

2%

3%

15%

12%

11%

2%

58%

0%

Literacy levels by segment

Middle Age Young Formally Employed

Page 42

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 41 of 68

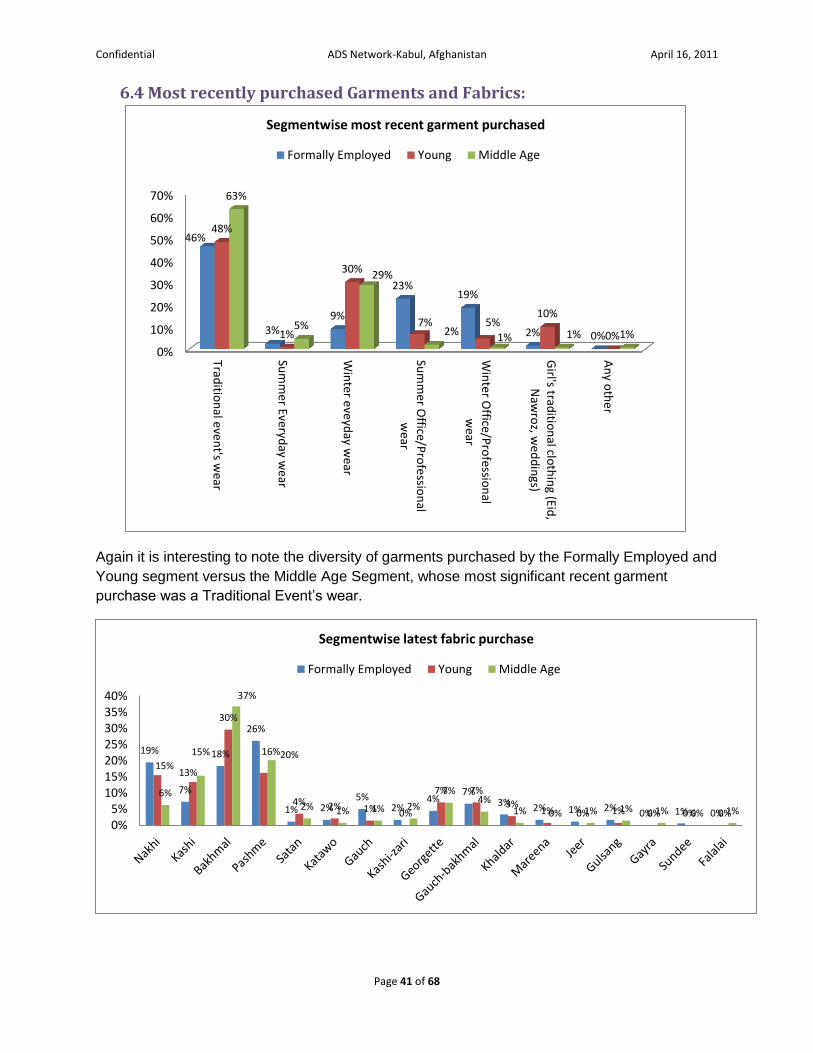

6.4 Most recently purchased Garments and Fabrics:

Again it is interesting to note the diversity of garments purchased by the Formally Employed and

Young segment versus the Middle Age Segment, whose most significant recent garment

purchase was a Traditional Event’s wear.

0%

10%

20%

30%

40%

50%

60%

70%

Traditio

nal e

ven

t's wear

Sum

me

r Everyday w

ear

Win

ter eve

yday w

ear

Sum

me

r Office/P

rofe

ssion

alw

ear

Win

ter Office/P

rofessio

nal

wear

Girl's trad

ition

al cloth

ing (Eid

,N

awro

z, we

dd

ings)

An

y oth

er

46%

3% 9%

23% 19%

2% 0%

48%

1%

30%

7% 5% 10%

0%

63%

5%

29%

2% 1% 1% 1%

Segmentwise most recent garment purchased

Formally Employed Young Middle Age

19%

7%

18%

26%

1% 2% 5%

2% 4%

7% 3%

2% 1% 2% 0% 1% 0%

15% 13%

30%

16%

4% 2% 1% 0%

7% 7%

3% 1% 0% 1% 0% 0% 0%

6%

15%

37%

20%

2% 1% 1% 2%

7% 4%

1% 0% 1% 1% 1% 0% 1%

0%5%

10%15%20%25%30%35%40%

Segmentwise latest fabric purchase

Formally Employed Young Middle Age

Page 43

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 42 of 68

The Formally Employed segment tends to buy more diverse range of Fabrics- Nakhi, Kashi,

Bakhmal and Pashme and so do the Young segment. In the case of the Middle Age segment,

they preferred to buy Bakhmal more than any other fabric.

6.5 Time since last purchase of garments and fabrics:

8% 11%

25% 25%

10%

23%

0%

9% 10%

34% 27%

15%

7% 0%

0%

10%

20%

30%

40%

1 weekago

2 weeksago

1 monthago

3 monthsago

6 monthsago

1 yearago ormore

Noresponse

Formally Employed segment

Time since last garment purchase Time since last Fabric Purchase

5%

13%

31% 31%

12% 9%

0% 7%

15%

29% 22%

18%

9%

0% 0%

10%

20%

30%

40%

1 weekago

2 weeksago

1 monthago

3 monthsago

6 monthsago

1 yearago ormore

Noresponse

Young Segment

Time since last garment purchase Time since last Fabric Purchase

1%

9%

18%

25%

19%

28%

0%

6%

13%

25% 27%

18%

11%

1% 0%

5%

10%

15%

20%

25%

30%

1 weekago

2 weeksago

1 monthago

3 monthsago

6 monthsago

1 yearago ormore

Noresponse

Middle age segment

Time since last garment purchase Time since last Fabric Purchase

Page 44

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 43 of 68

Segmented graphs above throw some interesting observations:

Garments are tending to be bought over a longer period of time vis-à-vis fabrics, which tend to

be bought quicker. Within the three segments, Middle Age segment bought their last garment

(47%) 6 months or before, whereas 50% of Formally Employed women bought a garment within

1-3 month range and another 11% two weeks ago. A significant number of Young Segment

62% bought their garments, like the Formally Employed segment in the last 1-3 months.

However, when it comes to Fabric purchase across segments a significant number of

respondents bought Fabric in the last 1-3 month range. (Formally Employed: 61%, Young:51%,

Middle Age:52%)

This could also be because traditionally it is cheaper to buy fabric and get it stitched than buy a

readymade garment. This is an interesting point, which Zardozi might like to probe further

before launching its collection to determine the right price points or develop a strategy to provide

significant value for money Clothes that help in changing this behavior.

6.6 Segmentwise preferred place and buying habit to purchase garments

and fabrics:

Preferred Place to buy Garment and Fabric

Formally Employed Young Middle Age

Garment Fabric Garment Fabric Garment Fabric

From the neighborhood 11% 7% 9% 5% 7% 5%

From the main city market 89% 92% 84% 84% 90% 92%

I ask the men in house buy for me 0% 1% 7% 9% 2% 2%

others 0% 0% 0% 1% 1% 1%

Total 100% 100% 100% 100% 100% 100%

Across segments whether it’s garment or fabric, women like to visit the main shopping area

known for selling clothes to make their purchase.

Buying habits for purchase of Garment and Fabric

Formally Employed Young Middle Age

Garment Fabric Garment Fabric Garment Fabric

almost always buy from the same Shop

5% 9% 5% 4% 2% 3%

I buy wherever I get the best deal/price

89% 85% 77% 81% 87% 90%

Buying from a shop is less important than the market

7% 7% 13% 9% 9% 5%

I never go to shops and Markets to buy (someone else in the family does)

0% 0% 5% 6% 2% 2%

Total 100% 100% 100% 100% 100% 100%

Again across segments getting “the best deal” whether it is a garment or a fabric is a huge

driver to the purchase decision. However there is a segment within the youth for whom the

market for buying a garment is more important than the shop they buy the product from.

Page 45

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 44 of 68

6.7 Perceived frequency of purchase of garments:

If special occasions then which one

Formally Employed

Young Middle Age

Nawroz 2% 6% 1%

Eid 13% 16% 17%

To go to family wedding 74% 44% 72%

When going on holiday 5% 3% 0%

Others 6% 25% 10%

No response/ Blank 0% 6% 0%

Total 100% 100% 100%

Family Wedding and Family special occasions are the most important factors for purchase of a

garment. However amongst the young segment that is not the only reason to purchase new

garment.

1%

11%

27%

21%

9%

31%

1%

9%

31%

21%

17%

21%

0% 2%

17% 17% 17%

47%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Evey weeek Once amonth

Once in 3months

Once in 6months

Once a year Definitely onspecial

occasions

Segmentwise: frequency of purchase of garments

Formally Employed Young Middle Age

Page 46

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 45 of 68

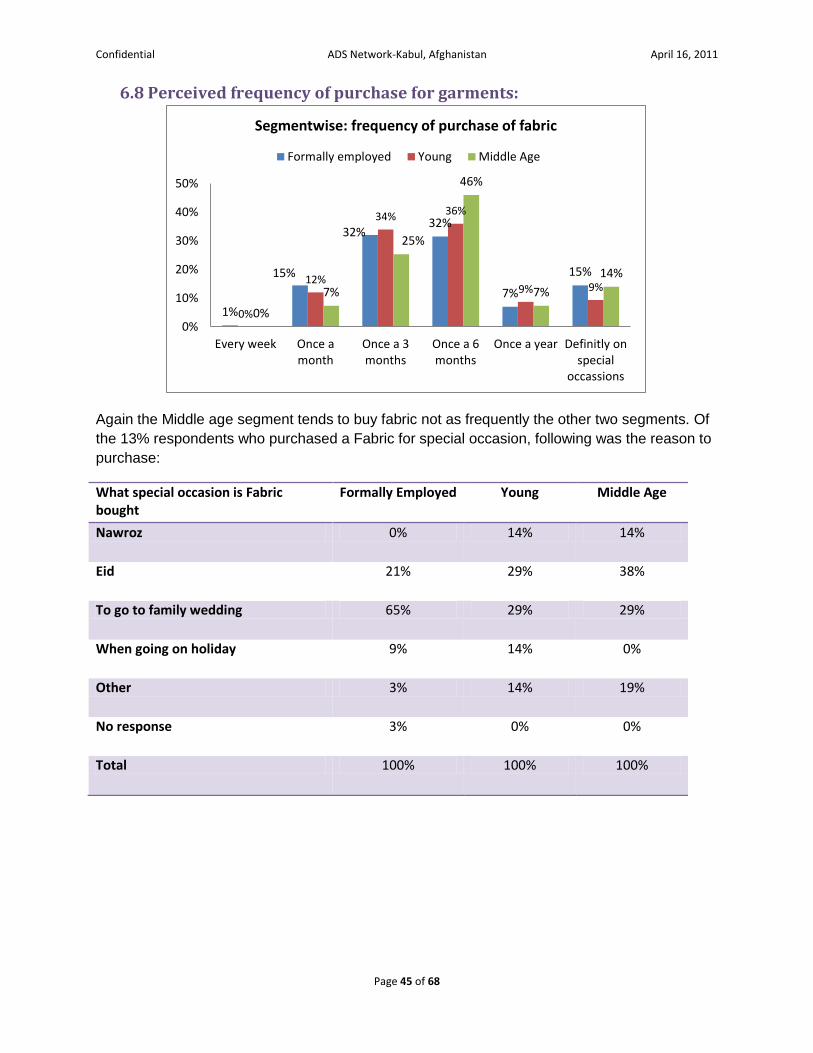

6.8 Perceived frequency of purchase for garments:

Again the Middle age segment tends to buy fabric not as frequently the other two segments. Of

the 13% respondents who purchased a Fabric for special occasion, following was the reason to

purchase:

What special occasion is Fabric bought

Formally Employed Young Middle Age

Nawroz 0% 14% 14%

Eid 21% 29% 38%

To go to family wedding 65% 29% 29%

When going on holiday 9% 14% 0%

Other 3% 14% 19%

No response 3% 0% 0%

Total 100% 100% 100%

1%

15%

32% 32%

7%

15%

0%

12%

34% 36%

9% 9%

0%

7%

25%

46%

7%

14%

0%

10%

20%

30%

40%

50%

Every week Once amonth

Once a 3months

Once a 6months

Once a year Definitly onspecial

occassions

Segmentwise: frequency of purchase of fabric

Formally employed Young Middle Age

Page 47

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 46 of 68

6.9 Budget for purchase of Garments and Fabric:

Across segments there is a tendency to keep a bigger budget for garments and a smaller

budget for Fabric.

0%5%

10%15%20%25%30%35%40%

Do

n’t kn

ow

, do

n’t

care

bu

dget o

f <A

fa1

,00

0

bu

dget o

f <A

fa2

,00

0

bu

dget o

f <A

fa5

,00

0

a bu

dge

t of <A

fa7

,50

0

a bu

dge

t of <A

fa1

0,0

00

My b

ud

get

defin

itely exceeds

AFA

10

,00

0

No

respo

nse

31% 27% 27%

5% 8%

2% 2% 0%

37% 17% 32%

7% 4% 2% 1% 1%

37%

30% 29%

3% 1% 1% 0% 0%

Budget for Garments

Formally Employed Young Middle Age

0%

10%

20%

30%

40%

50%

60%

Do

n’t kn

ow

, do

n’t care

bu

dget o

f <A

fa 1,0

00

bu

dget o

f <A

fa 2,0

00

bu

dge

t of <A

fa 5,0

00

a bu

dge

t of <A

fa 7,5

00

a bu

dge

t of <A

fa 10

,00

0

defin

itely exce

eds A

FA1

0,0

00

No

respo

nse

44% 39%

9% 8% 2% 0% 0% 0%

57%

29%

8% 4% 1% 0% 0% 1%

56%

31%

6% 6% 1% 0% 0% 0%

Budget for Fabric

Formally Employed Young Middle age

Page 48

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 47 of 68

6.10 Segmentwise Budget for purchase of clothes during Eid/Nawroz:

We can see that across segments, there is tendency to spend low during Eid, however when it comes to

Nawroz, there is a tendency to spend extra money to buy new clothes. This is a very important point to

consider by Zardozi, they should have a Nawroz collection by the time next Nawroz is celebrated.

34% 21%

8% 1%

37%

29%

20%

5% 3%

43%

39%

12%

4% 1%

45%

Afa 0-1000 Afa 1001- 3000 Afa 3001-5000 Afa 5001-10000 Afa > 10000

Budget for Eid clothes

Formally Employed Young Middle Age

17% 11% 2% 2%

69% 23% 11%

3% 1%

61%

32%

6% 1% 1%

60%

Afa 0-1000 Afa 1001- 3000 Afa 3001-5000 Afa 5001-10000 Afa > 10000

Budget for Nawroz

Formally Employed Young Middle Age

Page 49

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 48 of 68

6.11 Budget kept for Summer and Winter clothes:

It is interesting to note that the formally employed women tend to be more cost conscious when it

comes to buying summer or winter wear. Zardozi needs to look at two price ranges for its Summer and

Winter collection. One range should be from Afa-1,000 to Afa-4,000 and one premium range which is

from Afa- 9,000 and above.

6.12 Fabric Stitching behavior: If the Fabric is stitched by self or not-

38% 21%

10% 5% 27%

0%

25%

27%

10% 3%

35%

1%

35%

17%

7%

0%

42%

0%

Afa 0-1000 Afa 1001-3000

Afa 3001-5000

Afa 5001-10000

Afa > 10000 No Response

Budget kept for winter clothes

Formally Employed Young Middle Age

28% 33% 9% 4%

28%

0%

18% 29%

15% 1%

37%

0%

27%

24%

4%

1%

45%

0%

Afa 0-1000 Afa 1001-3000

Afa 3001-5000

Afa 5001-10000

Afa > 10000 No Response

Budget kept for Summer clothes

Formally Employed Young Middle Age

Page 50

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 49 of 68

Across segments the fabrics are stitched by Tailors.

Prices for stitching Fabric Formally Employed

Young Middle Age Total

I pay about Afa 100 1% 2% 2% 1%

Between Afa 101-250 16% 22% 30% 22%

251-500 46% 46% 54% 49%

501-750 26% 21% 11% 20%

751-1000 7% 7% 1% 5%

>1000 4% 3% 1% 3%

Formally Employed

Young

Middle Age

15%

21%

28%

85%

79%

71%

0%

0%

1%

Segmentwise: if Fabric stitched by self

No response No Yes

Formally Employed

Young

Middle Age

84%

86%

83%

16%

14%

16%

0%

0%

1%

Segmentwise: if fabric not stictched by self then who?

No response Someone in the family My tailor

Page 51

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 50 of 68

Total 100% 100% 100% 100%

The Formally Employed segment tends to pay more for stitching than the Middle Age segment.

Time taken to Stitch Formally Employed

Young Middle Age Total

1 day 1% 0% 0% 0%

2 days 5% 10% 3% 6%

1 week 68% 60% 63% 64%

1 month 26% 25% 32% 28%

No response/ Blank 1% 5% 1% 2%

Total 100% 100% 100% 100%

Average time taken for stitching is around 1 week.

Of the respondents who stitched the Fabric themselves, the skill was taught from the mother or

someone in the family. However there is a large section of Middle Age segment, which are self-

taught.

6.13 Purchase intent and influences for buying clothes:

Purchase intent for clothes Ready to tailor fabric

Buy Readymade

garment

Buy Fabric

and Stitch

50-50 both

Someone else buys

for me

Formally Employed Yes 73% 70% 34% 46% 5%

No 27% 30% 66% 55% 96%

Young Yes 63% 61% 40% 53% 22%

50%

3%

23% 17%

7% 0%

31%

6%

25%

6%

19% 13%

24%

0%

36% 31%

10%

0%

My mother My grandmother

Someoneamongst my

relation

I taughtmyself from

I learnt itformally

No response/Blank

Segmentwise: who taught stitiching

Formally Employed Young Middle Age

Page 52

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 51 of 68

No 37% 39% 59% 47% 78%

Middle Age Yes 47% 53% 61% 57% 18%

No 53% 47% 39% 43% 82%

Formally Employed women tend to go for either ready to tailor fabric or purchase garments,

whereas Middle Age segment prefers to buy fabric and get it stitched.

While Budget is an important criterion for selecting clothes across all segments, the Formally

Employed and Young segment, tend to also get influenced by their discussions with friends and

the style/color/design that catches their eye while shopping. However in the case of the Middle

Age segment, the budget and best deals are the most significant influencing factors.

6.14 Style preferences during winters and summers:

18% 18%

10%

20%

14%

20%

2%

12%

22%

10%

23%

15% 18%

0%

13% 11%

1%

37%

25%

11%

1% 0%

5%

10%

15%

20%

25%

30%

35%

40%

My m

oo

d w

he

n I go

sho

pp

ing

The

latest fashio

n th

at Id

iscuss w

ith frie

nd

s

Televisio

n an

d m

ovie

s Iw

atch

My B

ud

get

The

Be

st deals I can

get

The

Style/Co

lor/D

esign

that catch

es my eye in

the sh

op

No

respo

nse

Factors influencing purchase of clothes

Formally Employed Young Middle Age

Traditionalafghanclothes

Westernstyle clothes

Punjabi Suits Doesn'tmatter

8%

42%

18% 33%

10%

28% 21%

41% 25%

13% 25%

36%

Segmentwise style preference for winters

Formally Working Young Middle Age

Page 53

Confidential ADS Network-Kabul, Afghanistan April 16, 2011

Page 52 of 68

While the Formally Employed segment prefers to wear Western style outfits in Winters, in

summers across all segments the preference is for Punjabi suits. These are two clear indicators

for Zardozi to design its style for the two seasons.

6.15 Style preferences segmentwise for Weddings:

While the Formally Employed and Young segment prefers Western Style with light or no

embroidery for weddings, the Middle Age segment prefers the more traditional Afghan style.

Traditionalafghan clothes

Western styleclothes

Punjabi Suits Doesn't matter

6% 9%

76%

10% 3%

9%

75%

12% 18%

3%

66%

13%

Segmentwise style preference for summers

Formally Working Young Middle Age

0%5%

10%15%20%25%30%35%40%45%50%

Traditio

nal A

fghan

style-e

mb

ellish

men

ts

We

stern

Style - h

eavyem

bellish

men

ts

Western

Style Sim

ple

with

light o

r no

emb

roid

ery.

Styles in

curren

tFash

ion

in In

dia

Styles in

curren

tFash

ion

in Iran

No

respo

nse

20% 17%

37%

5%

22%

0%

30%