20

IEA 2019. All rights reserved. Oslo – 22 October 2019 Peter Fraser, Gas, Coal and Power Markets Division Gas 2019 market report

IEA 2019. All rights reserved.

Oslo – 22 October 2019

Peter Fraser, Gas, Coal and Power Markets Division

Gas 2019 market report

2018 was another golden year for natural gas

Gas demand jumped by 4.6% in 2018, accounting for nearly half of overall demand growth. The United States and China led the growth.

Average annual change in global primary energy demand, 2010-18

100

200

300

2010-16 2017 2018

Mtoe

Energy demand

Natural gas

China

United

States

- 40 - 20 0 20 40 60 80 100 120 140 160 180

Japan

Russia

Europe

Other Eurasia

South and Central America

Other North America

Africa

India

United States

Other Asia Pacific

Middle East

China

bcm

Fast growing Asian markets drive future gas demand

World natural gas consumption growth for selected countries and regions, 2018-24

China accounts for over 40% of global gas consumption growth. All sectors contribute to growth, with industry taking the lead in most markets.

- 40 - 20 0 20 40 60 80 100 120 140 160 180

Japan

Russia

Europe

Other Eurasia

South and Central America

Other North America

Africa

India

United States

Other Asia Pacific

Middle East

China

bcm

Industry

Power generation

Buildings & Other sectors

- 40 - 20 0 20 40 60 80 100 120 140 160 180

Japan

Russia

Europe

Other Eurasia

South and Central America

Other North America

Africa

India

United States

Other Asia Pacific

Middle East

China

bcm

Industry Other sectors

bcm

LNG emerges as an alternative marine fuel

The growth in LNG as a marine fuel is supported by two main segments – cruise and container ships –which account for 80% of expected consumption by 2024.

LNG consumption for maritime shipping by main segment, 2018-24

0

2

4

6

8

2018 2019 2020 2021 2022 2023 2024

bcm

Other

Cruise ships

Container ships

The United States leads production and exports growth

The United States and China account for over half of total production increment to 2024. US and Eurasian exports dominate LNG and pipeline trade growth.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Exports

Production

United States China Middle East

Russia Other Eurasia Egypt

Australia Other Africa South and Central America

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Exports

Production

United States China Middle East

Russia Other Eurasia Egypt

Australia Other Africa South and Central America

United States China

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Exports

Production

United States China Middle East

Russia Other Eurasia Egypt

Australia Other Africa South and Central America

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Exports

Production

United States China Middle East

Russia Other Eurasia Egypt

Australia Other Africa South and Central America

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Exports

Production

United States China Middle East

Russia Other Eurasia Egypt

Australia Other Africa South and Central America

Contributors to natural gas production and export growth, 2018-24

US natural gas production reaches 1 tcm mark by 2024

Associated shale strongly contributes to short-term production growth up to takeaway infrastructure limits and then slows with lesser LTO growth.

Natural gas production, United States, 2014-24

0

500

1 000

2014 2016 2018 2020 2022 2024

bcm

Other sources

Dry shale - other

Dry shale - Appalachia

Associated shale - other

Associated shale - Permian

Domestic consumption

Global gas trade is rising rapidly, driven by Asian demand

European imports have increased attracted by low prices.

LNG imports, quarterly (2015-19)

0

20

40

60

80

100

120

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2015 2016 2017 2018 2019

bcm

Japan and Korea China Other Asia Europe Other regions Annual average

The United States and China become #1 LNG seller & buyer in 2024

Fast growing Asian economies and Europe account for over 95% of the increase in LNG imports. US exports surge while Australia reaches a plateau and Qatar prepares for expansion*.

World LNG trade for a selection of importers and exporters, 2014-24

0

20

40

60

80

100

120

2014 2016 2018 2020 2022 2024

bcm

China Japan Europe India

0

20

40

60

80

100

120

2014 2016 2018 2020 2022 2024

United States Australia Qatar Russia

LNG Imports LNG Exports

* Considering operating liquefaction plants, projects under construction or with FID as of early June 2019

Northwest Europe supply gap increases…

Import requirements of Northwest Europe (2005-24)

Decreasing Groningen production will increase the region’s import dependence.

0

50

100

150

200

250

300

350bcm

import requirements demand production

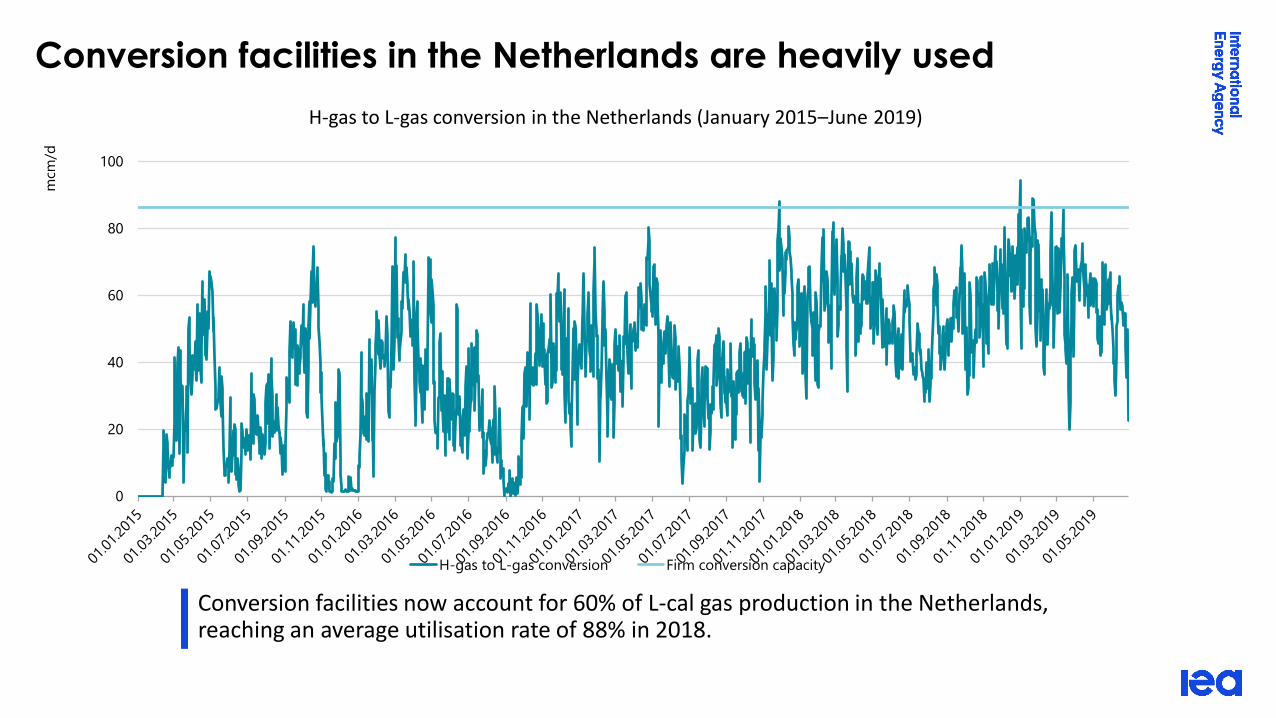

Conversion facilities in the Netherlands are heavily used

Conversion facilities now account for 60% of L-cal gas production in the Netherlands, reaching an average utilisation rate of 88% in 2018.

H-gas to L-gas conversion in the Netherlands (January 2015–June 2019)

0

20

40

60

80

100

mcm

/d

H-gas to L-gas conversion Firm conversion capacity

0

1

2

3

4

5

6

7

2013201420152016201720182019

bcm

Russian imports (German entries)

Ukrainian transit Belarus transit Nord Stream

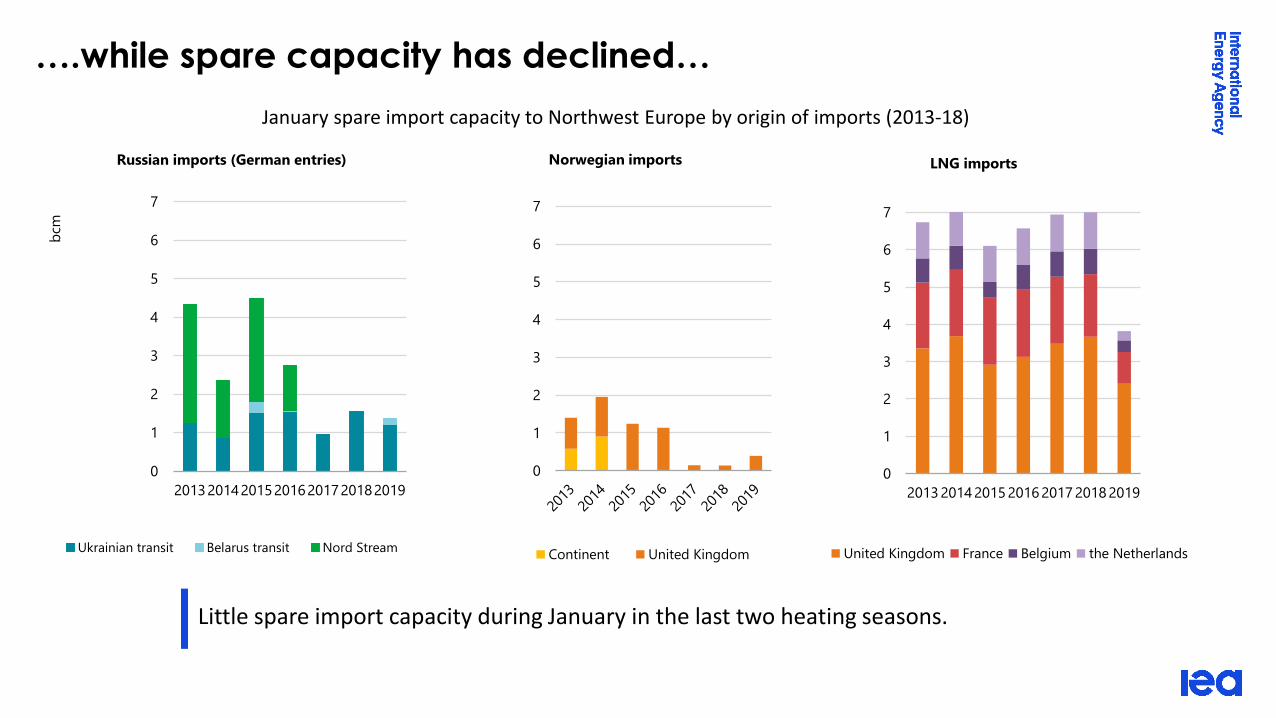

….while spare capacity has declined…

Little spare import capacity during January in the last two heating seasons.

January spare import capacity to Northwest Europe by origin of imports (2013-18)

0

1

2

3

4

5

6

7

Norwegian imports

Continent United Kingdom

0

1

2

3

4

5

6

7

2013 2014 2015 2016 2017 2018 2019

LNG imports

United Kingdom France Belgium the Netherlands

…in a transforming energy system

Northwest Europe could face even greater need for gas on cold, calm winter evenings as nuclear and coal are reduced suggesting more investment in flexible downstream infrastructure is needed.

Northwest Europe’s changing gas flexibility landscape

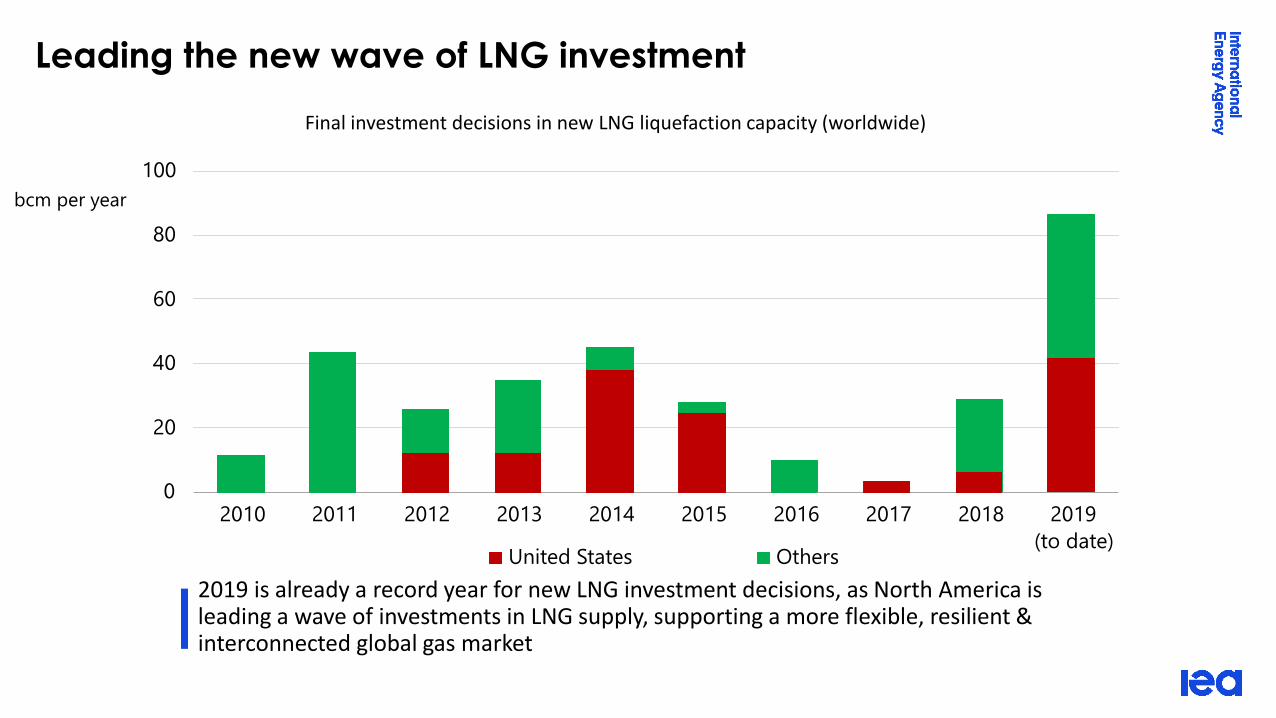

Leading the new wave of LNG investment

Final investment decisions in new LNG liquefaction capacity (worldwide)

2019 is already a record year for new LNG investment decisions, as North America is leading a wave of investments in LNG supply, supporting a more flexible, resilient & interconnected global gas market

0

20

40

60

80

100

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(to date)

bcm per year

United States Others

Equity-lifting model gaining popularity

FID-enabling contracts by signing year and structuring model (2014-19)

Equity-lifting has recently facilitated the FID taken on projects such as LNG Canada,Greater Tortue FLNG, Golden Pass LNG, and Arctic LNG 2.

0

10

20

30

40

50

60

70

2014 2015 2016 2017 2018 2019

bcm

Other structures Equity lifting

LNG

Canada

…to a rapidly transforming Asian market

Evolution of Asian LNG buyers types (2010-2024)

Emerging Asian buyers driving future LNG demand growth see LNG as a component oftheir gas supply portfolio.

0% 20% 40% 60% 80% 100%

2024

Share of LNG in gas supply

Emerging buyers Traditional buyers Emerging buyers Traditional buyers

*size of the bubbles indicates annual LNG imports

-20%

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

LT c

on

tract

s in

LN

G s

up

ply

Share of LNG in gas supply

2010

Towards a global convergence of natural gas prices?

Gas markets in major regions are closing the price gap thanks to the development of global LNG trade. The Asian spot market still faces a higher degree of price volatility.

Evolution of natural gas spot market prices, 2014-19

0

2

4

6

8

10

12

14

16

18

20Ja

n-1

4

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Ap

r-15

Jul-

15

Oct

-15

Jan

-16

Ap

r-16

Jul-

16

Oct

-16

Jan

-17

Ap

r-17

Jul-

17

Oct

-17

Jan

-18

Ap

r-18

Jul-

18

Oct

-18

Jan

-19

Ap

r-19

Jul-

19

USD

/MB

tu

Europe (TTF) North America (Henry Hub) Asia (Asian LNG spot)

All markets are not (yet) equal when it comes to end users

The influence of market pricing on end users’ prices remains currently limited for most Asian markets.

Asian spot LNG price and domestic prices for a selection of Asian importing countries (2015-19)

0

2

4

6

8

10

12

14

16

USD

/MB

tu Asian LNG spot

China - average city

gate price

Japan - LNG contract

India - domestic gas

price

Pakistan - compound

average price

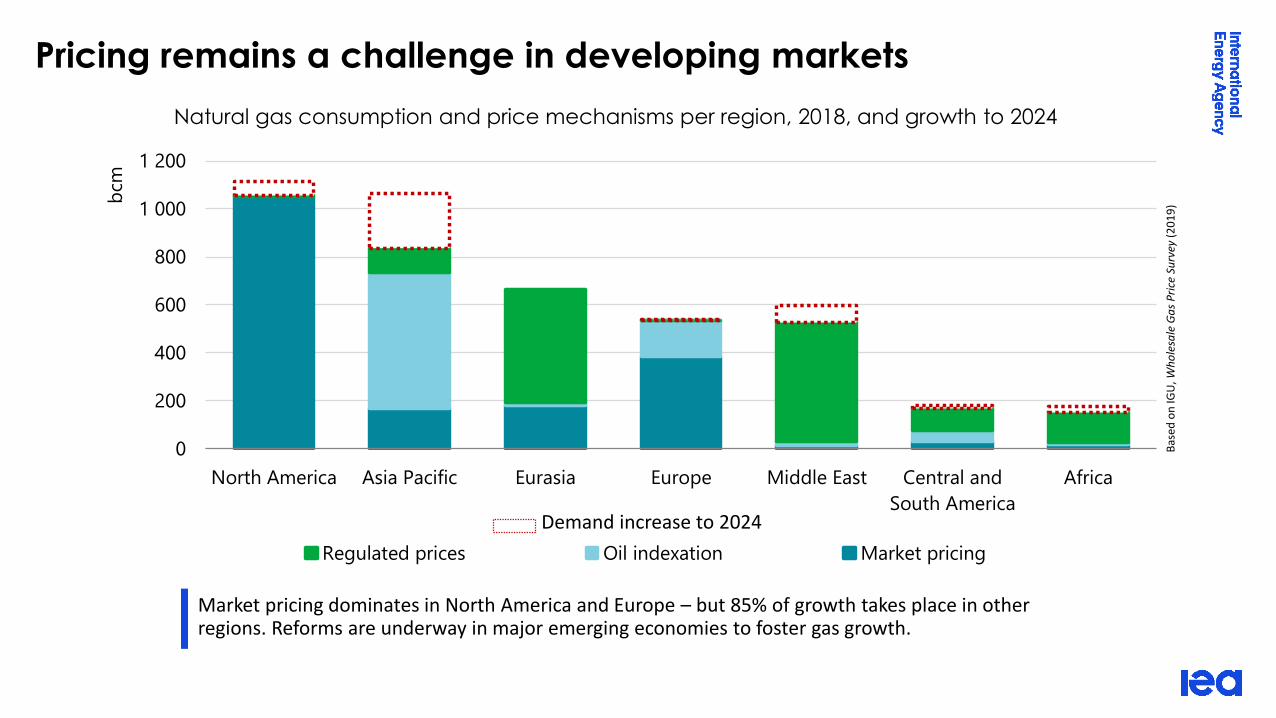

Pricing remains a challenge in developing markets

Market pricing dominates in North America and Europe – but 85% of growth takes place in other regions. Reforms are underway in major emerging economies to foster gas growth.

Natural gas consumption and price mechanisms per region, 2018, and growth to 2024

0

200

400

600

800

1 000

1 200

North America Asia Pacific Eurasia Europe Middle East Central and

South America

Africa

bcm

Regulated prices Oil indexation Market pricing

0

200

400

600

800

1 000

1 200

North America Asia Pacific Eurasia Europe Middle East Central and

South America

Africa

bcm

Regulated prices Oil indexation Market pricing

Demand increase to 2024

Bas

ed o

n IG

U, W

ho

lesa

le G

as

Pri

ce S

urv

ey(2

01

9)

Conclusions

• Natural gas demand will continue to grow in the medium-term, driven by emerging Asian economies – and led

by China.

• Although production increases in many regions, most of additional exports will come from US LNG and Eurasian

pipeline.

• LNG trade remains the main driver of gas market globalisation, and a major source of incremental supply for

Asia and Europe.

• This growth is supported by a rebound in investment.

• Market prices are converging as global LNG trade expands, and the share of market-driven pricing is increasing

in all regions.

• Current gas reforms in major emerging economies are a prerequisite to ensure competitive pricing and

sustainable growth in the longer term.