member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Contents

1 Executive summary 1

2 Scope and approach 4 2.1 KPMG’s engagement 4 2.1.1 Gas resource base in Australia 4 2.1.2 Factors influencing the commercialisation of gas in Australia 4 2.1.3 Domestic gas market 4 2.1.4 Integration with LNG export markets 5 2.1.5 Carbon and renewable energy policy implications 5 2.1.6 Impact of potential interventionist policies 5 2.1.7 Outlook for the Australian natural gas market 5 2.2 Report structure 5

4 Factors affecting gas field commercialisation 48 4.1 Land rights and access 48 4.2 Multiple land use classifications 48 4.3 Capital investment constraints 49 4.4 Infrastructure and labour availability 49

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

4.5 Geology and geography 49 4.6 CSG water management 50 4.7 Ramp-up gas 51 4.8 Scale 52 4.9 Environmental regulation 52 4.10 Approvals time 52 4.11 Technology 53

5 Australia’s LNG export markets 54 5.1 Introduction 54 5.1.1 Trade flows 54 5.1.2 Pricing 56 5.1.3 Production 58 5.2 LNG demand base 60 5.2.1 Japan 62 5.2.2 South Korea 62 5.2.3 China 63 5.2.4 India 63 5.3 LNG rivals 63 5.3.1 Qatar 64 5.3.2 Malaysia 64 5.3.3 Indonesia 65 5.3.4 Papua New Guinea 65 5.3.5 Other 65 5.4 Existing LNG projects in Australia 66 5.4.1 Operational 66 5.4.2 Under construction 66 5.5 Proposed LNG projects 67

6 The role of gas in a carbon constrained economy 78 6.1 CPRS 78 6.2 Enhanced RET 79 6.3 Clean Energy Initiative 81 6.4 Issues for the LNG industry 81

7 Factors impacting the domestic gas supply market 83 7.1 Co-dependence on LNG exports 83 7.2 Joint marketing 83 7.3 Vertical integration 84 7.4 Price transparency 84 7.5 Acreage management 85 7.6 Pipeline policy and regulation 86 7.6.1 Gas quality specifications 86 7.6.2 Pipeline regulations 86

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

7.6.3 Approvals process 86

8 Gas market efficiency 87 8.1 National Gas Bulletin Board 87 8.2 Short Term Trading Market 88 8.3 National Gas Market Operator 89 8.4 Impact of interventionist policies on market efficiency 90

9 Gas policy initiatives 91 9.1 Mandatory domestic gas reservation 91 9.2 Retention leases 91 9.3 Royalty reductions or holidays 91 9.4 Broadening of gas quality specifications 92 9.5 Taxation reform to assist small exploration companies 92 9.6 Provision of infrastructure supporting exploration and development 92

10 Outlook for the Australian natural gas market 93 10.1 Short term outlook 93 10.2 Medium term outlook 93 10.3 Long term outlook 94

A Australia’s gas resource base 96 A.1 Conventional gas 96 A.2 Coal Seam Gas (CSG) 105

B Long term and medium term LNG contracts in force in 2008 (duration > 4 yrs) 109

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Disclaimer Inherent Limitations

This report has been prepared as outlined in Section 2.1 and Section 2.2. The services provided in connection with this engagement comprise an advisory engagement, which is not subject to assurance or other standards issued by the Australian Auditing and Assurance Standards Board and, consequently no opinions or conclusions intended to convey assurance have been expressed.

References to ‘review’ throughout this report have not been used in the context of a review in accordance with assurance and other standards issued by the Australian Auditing and Assurance Standards Board.

Any estimates or projections of future economic performance are impacted by numerous factors that may influence the various components of the estimates or projections, and are inherently indeterminable whether considered in isolation or in conflux. Although KPMG exercises reasonable care when making forecasts or predictions, factors in the process, such as market behaviour, are inherently uncertain. As such, future events may not unfold as expected and actual results achieved for the forecast periods covered will vary from the information presented. Any estimates or projections will only take into account information available to KPMG up to the date of the deliverable and so findings may be affected by new information. Accordingly, we do not warrant or guarantee that any outcome presented in this report will be achieved. Further, events may have occurred since we prepared this report which may impact on it and its findings.

No warranty of completeness, accuracy or reliability is given in relation to the statements and representations made by, and the information and documentation provided by market participants consulted as part of the engagement.

KPMG have indicated within this report the sources of the information provided. We have not sought to independently verify those sources unless otherwise noted within the report.

KPMG is under no obligation in any circumstance to update this report, in either oral or written form, for events occurring after the report has been issued in final form.

The findings in this report have been formed on the above basis.

Third Party Reliance This report is solely for the purpose set out in Section 2.1 and Section 2.2 of this report and for APPEA’s information, and is not to be used for any other purpose.

This report has been prepared at the request of APPEA in accordance with the terms of KPMG’s Engagement Letter with APPEA, dated 18 September 2009. Other than our responsibility to APPEA, neither KPMG nor any member or employee of KPMG undertakes responsibility arising in any way from reliance placed by a third party on this report. Any reliance placed is that party's sole responsibility.

We understand that this report may be made available on the APPEA website. Third parties who access this report are not a party to our Engagement Letter with APPEA and, accordingly, may not place reliance of this report.

KPMG shall not be liable for any losses, claims, expenses, actions, demands, damages, liabilities or any other proceedings arising out of any reliance by a third party on this report.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

1 Executive summary KPMG have been engaged by the Australian Petroleum Production & Exploration Association (APPEA) to undertake a study of the natural gas market in Australia, its structure, efficiency and future outlook. The purpose of the report is to assist APPEA in establishing a current base of information to communicate with its stakeholders.

The topics covered in this Gas Market Report include:

• an overview of Australian gas reserves and resources;

• the nature and structure of the Australian natural gas market;

• factors affecting the commercialisation of domestic gas resources (including those for Liquefied Natural Gas (LNG) export);

• the impact of the gas export market on the efficient operation of the domestic gas market;

• analysis of potential impacts of interventionist policies aimed at domestic gas volume/price control; and

• an outlook for the Australian gas market.

Gas production in Australia services both domestic gas demand (56%) and the export LNG markets (44%).1 While coal is the predominant fuel in Australia, the use of natural gas has accelerated at a rate greater than that of coal (average consumption of gas has increased by an average of 3.5% pa, compared to 2.4% pa for coal). The strong growth to date has been driven by sustained population growth, strong economic growth, alongside its competitiveness as a fuel source and governmental policies to encourage its uptake.2 The outlook is furthermore positive, as gas is projected to be the fastest growing fossil fuel over the period to 2029-30.3 Primary gas consumption is projected to rise by 3.4% per year, its share of primary energy consumption projected to rise to 33% by 2029-30.4 This forecast growth in demand is driven primarily by the electricity sector, as the share of gas fired generation (GFG) in the energy mix is projected to increase considerably over the medium to long term, reflecting the shift to less carbon intensive fuels in a carbon constrained environment.5

While Australia accounted for 2% of world gas reserves and production in 2008, it is the world’s six largest LNG exporter, accounting for 9% of the world’s LNG trade in 2008.6 Since 2006-07, gas exports have increased by 12%. By 2029-30, LNG exports are projected to reach 109 Mt (from 14.4 Mt in 2007-08), reflecting an average annual growth rate over the outlook period of 9.5%.7

1 Australian Energy Regulator, State of the Energy Market 2009, at 226. 2 Geoscience Australia and ABARE, Australian Energy Resource Assessment, Canberra, 2010, at 102. 3 Ibid at 2 at 121. 4 Ibid. 5 Ibid at 2 at 121 and 122. 6 Ibid at 2 at 83. 7 Ibid at 2 at 122.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Production of LNG is projected to increase its share of total Australian gas production to 70% by 2029-30.8

There are two types of gas production: conventional and unconventional. Unconventional gas production typically includes coal seam gas (CSG), tight and shale gas. However, no tight or shale gas is currently produced in Australia.9 Accordingly, for the purposes of this report, only conventional gas and CSG is discussed. Conventional gas contributes 92% of Australia’s gas production, with the remainder consisting of CSG production. Australian gas production is projected to reach 8505 PJ (7.7 Tcf) in 2029-30, with CSG projected to account for 29% of this total.10 CSG is set to contribute to a greater proportion of the gas market, as the burgeoning LNG industry in Queensland (QLD) continues to gain momentum.

In order to inform the Gas Market Report, KPMG undertook a targeted industry consultation, alongside a desktop analysis of the Australian gas market. The industry consultation was conducted by way of one-on-one discussions with a cross section of gas market participants. The industry consultation facilitated the identification of common themes in industry views and the reasons supporting those views. The recurrent themes from the desktop research undertaken and the targeted industry consultation include the following:

• Australia has no shortage of gas resources, across each of the east, west and Northern Territory (NT) markets.

• There is no need for interventionist policies to be introduced by Governments to reserve domestic gas supply or control its price. Market forces suffice to establish the equilibrium between domestic and LNG supply at the respective prices. Domestic gas reservation policies distort the market and discourage investment.

• The QLD Government’s decision to set aside future gas fields for domestic supply if needed (rejecting the option to require a percentage of gas from all fields to contribute to domestic supply) is supported by industry. Further, the QLD Government’s decision was consistent with the findings of KPMG Econtech’s critique and economic analysis on the impact of the proposed policies, which found that mandatory gas volume reservation would diminish the consumer welfare that could be derived from the creation of a 28Mtpa LNG industry in the Gladstone region.

• Buyers and sellers are now opting to contract gas supply for shorter periods (3-5 years as opposed to typical 15 year terms) for ‘brownfield’ and mature supply projects. However, for ‘greenfield’ projects, long-term contracts are still more applicable in order to secure investment.

• Pipeline contracts are generally long-term in comparison to contracts from mature supply projects. The alignment of contract terms would go a long way to standardise contracts and remove any inherent market frictions.

East coast, west coast and the Northern Territory gas markets are distinct and will remain that way until WA’s market matures. Lack of transparency in the gas market has been raised by some

8 Ibid at 2 at 122. 9 Ibid at 2 at 85. 10 Ibid at 2 at 86.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

participants as a potential impediment. The lack of standardisation across the market, including fungibility of contracts, also acts as a potential barrier to trade. Joint ventures are often needed to secure investment in illiquid non-transparent markets, particularly for foundation contracts. WA could benefit from a Gas Market Bulletin Board, but it is too premature for a gas Short Term Trading Market.

• The Federal Government’s proposed Carbon Pollution Reduction Scheme (CPRS) is given qualified support by surveyed industry participants. Increasing costs of abatement and the risk of diminishing investment capital are concerns. The CPRS is potentially beneficial for domestic gas market development, as it will make gas more competitive with coal as a fuel source once carbon costs are accounted for. Industry has expressed a desire for further clarity surrounding permit allocation arrangements for the LNG industry.

• The Enhanced Renewable Energy Target (RET) scheme creates an unequal playing field in the electricity market, at the expense of the contribution from gas-fired generation (GFG). The carbon price should dictate when renewable technologies are commercially viable, without the need for the RET. While the enhanced RET may act to remove up to 20% of potential market opportunities for GFG, it will nonetheless foster gas as the fuel of choice for backing up the wind farm Power Purchase Agreements (PPAs) vulnerable to the intermittent nature of wind.

• In Western Australia, after the Reindeer and Macedon gas projects are brought online, offshore gas fields will be predominantly underpinned by LNG projects. Domestic supply will depend on the existence of the export LNG market.

• The terms of retention leases can affect the timing of supply of gas to domestic markets, though changes to legislation governing such acreage management is not considered desirable from a gas producer’s perspective. Infrastructure inadequacies, including gas quality specifications for pipelines, can restrict domestic supply, as can development approval processes, which can be overly onerous on time. Tightening the rules surrounding the issue of retention leases could also act as a deterrent to investment in Australia. Royalty reductions and holidays for tight gas operators would be a desirable intervention measure, as would taxation reform for small exploration companies.

This Report provides an overview of Australia’s domestic gas market and the challenges, opportunities and dynamics that it currently faces in light of its increasing integration with the Global market for LNG and the Australian electricity market. Further, the findings in this Report provide context for understanding how the current Australian gas market can operate efficiently, and an outlook going forward.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

2 Scope and approach

2.1 KPMG’s engagement KPMG has been engaged by APPEA to prepare a report on the natural gas market in Australia. The study encompasses:

• an overview of Australia’s natural gas resource base;

• factors affecting its commercialisation;

• the domestic gas market (and regional differences within);

• the export LNG industry;

• the influence of pending and legislated climate change policies on gas market dynamics;

• the impact of the gas export market on the efficient operation of the domestic gas market;

• potential impacts of interventionist policies aimed at domestic gas volume/price control; and

• outlook for the Australian natural gas market.

2.1.1 Gas resource base in Australia A desktop review of the Australian domestic gas market was conducted in order to compile a snapshot of Australia’s existing natural gas resource base. The basins with known gas reserves were identified using publicly available sources of information, and these were then categorised according to the type of natural gas being extracted – that is, conventional gas or coal seam gas (CSG). The geographic location of the basins, their area covered, total reserve estimate and key fields and projects belonging to each basin were then described.

2.1.2 Factors influencing the commercialisation of gas in Australia Industry consultation was conducted in order to inform the report on the factors influencing commercialisation of gas in Australia. Topics explored include land rights and access, multiple land use classifications, capital investment constraints, infrastructure and labour availability, geology and geography, and the management of waste water and ramp-up gas.

2.1.3 Domestic gas market An overview of the domestic gas market was compiled using a combination of available market information and anecdotal evidence collected from industry consultations, incorporating descriptions of significant features and trends in each of the regional markets comprising the national market,

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

including the east coast, west coast and Northern Territory market. Commentary focuses on market developments on the supply side, gas infrastructure, GFG and gas retailing.

2.1.4 Integration with LNG export markets An overview of the global LNG industry and international LNG demand and supply centres was undertaken using available market information and input from industry feedback. The existing LNG suppliers operating in Australia are described, and an analysis of prospective and committed Australian LNG projects was undertaken.

2.1.5 Carbon and renewable energy policy implications The impacts of the Federal Government’s climate change policies, specifically the expanded Renewable Energy Target (RET) and the proposed Carbon Pollution Reduction Scheme (CPRS), on gas market dynamics are discussed. Industry views are also included in the commentary.

2.1.6 Impact of potential interventionist policies Several potential interventionist policies aimed at domestic gas price/volume control are reviewed in order to identify what could be expected as likely outcomes. Consultation with industry was a key component of the research to inform this section of the report.

2.1.7 Outlook for the Australian natural gas market An outlook for the Australian gas market was developed, largely driven from industry feedback, and analysis of information gathered. This included views on the direction of the Australian natural gas supply and demand balance, alongside its anticipated price path.

2.2 Report structure Chapter 3 presents Australia’s gas basins, categorising them according to their specific gas resource type. Their size, key fields and key projects (existing and expected) are explored. It also reviews the Australian gas market structure. Each of the three distinct markets operating within Australia – the east coast, west coast and Northern Territory markets – are individually described. Commentary surrounding the supply base, gas transport infrastructure, GFG and retailing in each region is provided. It includes recent developments affecting and potential issues facing each market.

Chapter 4 reviews the factors affecting gas field commercialisation. It is predominantly informed by feedback received from KPMG’s targeted industry consultation.

Chapter 5 reviews Australia’s existing and anticipated involvement in the global LNG industry. It gives an overview of the role of LNG in the global landscape and the main LNG demand and supply centres in the international market. It then looks at Australia’s existing LNG projects, and new projects on the horizon.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Chapter 6 is an overview of the role of gas in a carbon constrained economy. It presents the existing policy instruments that have been used in order to implement the Government’s climate change goals and the expected impact of these instruments on the domestic gas and LNG export markets.

Chapter 7 presents potential identified barriers to supply of domestic gas in Australia. Competition with LNG export markets is also explored.

Chapter 8 addresses issues surrounding the efficiency of the Australian gas market and outlines any identified impediments to this end.

Chapter 9 presents analysis surrounding interventionist strategies being considered by the government, aimed at domestic volume/price control.

Chapter 10 presents a short term, medium term and long term outlook for the Australian gas market.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3 Australia’s gas market

3.1 Overview Natural gas serves a wide and increasingly important role in Australia’s economy. Besides being a key domestic energy source, electricity generation fuel and feedstock for international LNG projects, it is a:

• significant and expanding contributor to export earnings and economic growth;

• significant contributor to the petroleum sector’s $8 billion per year tax and royalty payments made to the government.11

• stimulant for regional investment and development.

Gas has increasingly become the marginal fuel for electricity generation, leading to the increasing convergence of Australian gas and electricity markets. Forty-four percent of Australia’s gas production is exported. In 2009-10, Australian LNG exports are forecast to increase by 13%.12 Natural gas is the third largest source of Australia’s primary energy consumption (behind coal and petroleum products).13 While coal is Australia’s largest energy commodity export, the use of natural gas in Australia has accelerated at a rate greater than that of coal (average consumption has increased by an average of 3.5% pa, compared to 2.4% pa for coal).14

The Australian gas market can be broadly divided into three regions: east coast, west coast and the Northern Territory (NT). These markets are geographically isolated from one another, making transmission and distribution of gas between markets uneconomic at present.15 As a result, all gas is either consumed within each market or exported as LNG.16 The east coast is Australia’s largest gas market, and the most advanced in terms of its interconnectedness and price transparency. The electricity generation and residential sectors are the largest consumers of gas in the east coast market.17 The west coast accounts for around 57% of Australia’s gas production, and accounts for around 41% of Australia’s gas consumption.18 The electricity generation and manufacturing sectors account for the majority of gas consumption in the west coast market.19 The NT market is the smallest producer and consumer of gas in Australia.20

The west coast and NT markets support Australia’s two operational LNG developments: North West Shelf Venture (NWS Venture) and Darwin LNG, which have been supplying LNG to Asian markets for twenty years and three years respectively. The NWS Venture has also supplied domestic gas to WA for 25 years, accounting for 65% of the state’s gas supply. This highlights the potential for LNG to successfully supply not only export markets but local markets as well. 11 Belinda Robinson, CEDA Oil & Gas Industry Update (Conference), 5 November 2009. 12 ABARE, Australian Commodities, Vol 16 No. 14, December quarter 2009 at 662. 13 ABARE, Energy in Australia, Department of Energy, Resources and Tourism, 2009 at 47. 14 Ibid. 15 Ibid at 2 at 104. 16 Ibid. 17 Ibid at 2 at 105. 18 Ibid. 19 Ibid. 20 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3.1.1 Resources, reserves and production Geoscience Australia defines petroleum resources (which includes natural gas) to include only those natural concentrations of petroleum from which economic extraction of a part is feasible within the range of technology and prices likely to be seen within the next 20 to 25 years.21 Australia has abundant gas resources. According to the State of the Energy Market Report 2009, Australia has over 200,000 PJ (190 Tcf) of gas resources – making it one of the largest endowments in the Asia Pacific region.22 CSIRO estimates that CSG resources in Queensland (alone) are between 150,000 PJ (143 Tcf) and 500,000 PJ (476 Tcf), averaging around 250 Tcf.23 Sedimentary basins located (mostly) offshore from WA in Commonwealth waters currently hold more than 80% of Australia’s discovered natural gas resources. The proved and probable (2P) reserves (those with at least a 50% cumulative probability of existence24) within this resource base account for approximately 60,257 PJ (57 Tcf).25

Australia’s gas production total for the year to June 2009 was approximately 1780 PJ (including LNG exports).26 In 2009-10, Australia’s gas production is forecast to increase by 10%.27 The number of developed and producing fields has almost doubled over the past decade. Currently there are 67 producing fields in the WA region. Not surprisingly, Western Australia is also Australia’s largest producer of gas (66% of national production in 2007-08 (1141 PJ)), followed by Victoria (at 20% (312 PJ)). Gas production in WA has been growing at an average annual rate of 6.8% (over the past seven years), compared to 3.2% in Victoria. There are two primary sources of natural gas in Australia: conventional gas and coal seam gas. At present, with a share of 92%, Australian gas production is dominated by conventional gas.

Around 96% of Australia’s conventional gas production is sourced from the three petroleum basins: the Carnarvon Basin (WA), the Gippsland Basin (offshore Victoria) and the Cooper-Eromanga Basin (central Australia). The Carnarvon Basin in WA is set to become an even bigger contributor with the recent approval of the Gorgon Gas Project – the Greater Gorgon resource is the largest undeveloped gas resource under common control in Australia. Other basins contributing to conventional gas production are the Perth, Browse and Bonaparte Basins (WA), Otway and Bass Basins (Victoria) and the Amadeus Basin (NT).

While CSG currently constitutes only 8% of total natural gas production in Australia28, it is the fastest growing gas production sector29 and its contribution is set to escalate with the successful development of QLD’s burgeoning CSG to LNG industry. In the five years to 2008, 2P (proved and probable) CSG reserves increased at a rate of about 46% per year, significantly increasing resource life.30 Currently, QLD and NSW are the only two states in Australia producing CSG. CSG accounted for almost 23% of gas produced in eastern Australia in the year to June 2009.31 It contributes around 21 Geoscience Australia, http://www.ga.gov.au/resources/publications/oil-gas-resources-australia-2008/glossary.jsp, last accessed 22 January 2010. 22 Ibid at 1 at 28. 23 Dr. Abouna Saghafi, CSIRO Energy Technology, Enhanced Coal Bed Methane (ECBM) and CO2 storage in Australian coals, 2007 at 10. 24 Geoscience Australia, http://www.ga.gov.au/resources/publications/oil-gas-resources-australia-2008/glossary.jsp, last accessed on 22 January 2010. 25 Ibid at 1 at 226. 26 Ibid. 27 ABARE, Australian Commodities, Vol 16 No. 4, December quarter 2009, at 660. 28 Ibid at 1 at 226. 29 Ibid at 1 at 229. 30 Ibid at 2 at 98. 31 Ibid at 1 at 229.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

90% of QLD’s total natural gas production (sourced from the Bowen and Surat Basins) and meets over 70% of the QLD market demand.32 The entirety of NSW’s gas production (albeit marginal in size) is CSG sourced (from the Gunnedah Basin).

The Joint Petroleum Development Area (JPDA) is also a substantial source of production. The JPDA was established by the Timor Sea Treaty between Timor-Leste and Australia in 2002. It demarcates an area of the Timor Sea located between Australia and Timor-Leste that has overlapping territorial claims by the two countries. The Timor Sea Treaty provisionally gives 90% of the tax revenues from petroleum production from within the JPDA to Timor-Leste and 10% to Australia. Concerning natural gas, there are two projects lying within the JPDA:

• The Bayu-Undan liquids and gas development; and

• The Greater Sunrise gas project (gas reserve estimate of 8.3 Tcf, about three times that of Bayu Undan)

Figure 3.1 shows the location of Australia’s gas reserves. Table 3.1 provides the size of the reserves, their production volumes and the percentage they contribute to domestic sales in 2009 (excluding the JPDA). Figure 3.2 shows a summary of Australian gas production per region, including the JPDA. Figure 3.3 shows the market shares of domestic gas production per gas basin as it stood in 2008 (as the close indicator of 2009 positioning).

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Figure 3.1: Location of Australia's gas reserves, 2009

Notes: Production data for year ended 30 June 2009. Reserves at June 2009. Source: State of the Energy Market 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.1: Natural gas reserves and production in Australia, 2009

Gas Basin Production (Year to June 2009) Proved and Probable Reserves (June 2009)2 PJ Percentage of Domestic Sales PJ Percentage of Domestic Sales

Conventional Natural Gas Western Australia Carnarvon 332 32.2 28739 47.7 Perth 7 0.7 21 0 Northern Territory Amadeus 19 1.9 181 0.3 Bonaparte 0 0 1638 2.7 Eastern Australia Cooper (SA-QLD) 124 12.4 1084 1.8 Gippsland (VIC) 230 23 5625 9.3 Otway (VIC) 116 11.6 1291 2.1 Bass (VIC) 18 1.8 287 0.5 Surat-Bowen (QLD) 16 1.6 212 0.4 Total conventional natural gas 852 85 39079 64.9 Coal Seam Gas Surat-Bowen (QLD) 143 14.3 19726 32.7 Sydney (NSW) 5 0.5 1452 2.4 Total coal seam gas 148 14.8 21178 35.1 Domestic Totals 1000 100 60257 100 Liquefied Natural Gas (Exports) Carnarvon (WA) 766 Bonaparte (NT) 14 Total liquefied natural gas 780 Total production 1780 Notes: 1. Conventional natural gas reserves include liquefied natural gas and ethane 2. Proved reserves are those for which geological and engineering analysis suggests at least a 90 per cent probability of commercial recovery. 3. Probable reserves are those for which geological and engineering analysis suggests at least a 50 per cent probability of commercial recovery. Source: State of the Energy Market 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Figure 3.2: Australian gas production by region (including JPDA), 2008

TAS, 2%

SA, 4%

QLD, 5%

JPDA, 9%

VIC, 22%

NT, 2%

WA, 56%

Source: Oil & Gas in Australia, October 2008

Figure 3.3: Market shares in domestic gas production, by basin, 2008

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3.1.2 Wholesale pricing Australian wholesale gas prices have historically been low by international standards.33 They have also been relatively stable, bound by provisions in long term supply contracts out of the Cooper and Gippsland basins and the North West Shelf fields.34 While gas in the United States and Europe closely follows the oil price, natural gas in Australia has traditionally been used as a substitute for coal in coal-fired electricity generation. Australian gas prices have therefore effectively been capped by Australia’s low cost coal prices.35 Given gas price transparency is very low throughout Australia (except in Victoria where a Short Term Trading Market exists), precise pricing information is not widely available. In 2005, estimates for wholesale gas prices on the east coast ranged between $2.90 to $3.15 per gigajoule.36 Between 2005 and 2008, there has been upward pressure on gas prices due to various factors including: • Substantial increases in costs associated with gas exploration, development and production.

• Higher oil prices have pushed up international gas prices which has flowed into Australian LNG exports. This has put upward pressure on WA’s domestic gas prices (given its sizeable LNG export capacity) and has heightened east coast price expectations (given its potential LNG export capacity).

• Drought conditions in eastern Australia in 2007 increased the demand for GFG, which escalated gas prices.

• Market participants began factoring the projected effects of the CPRS into demand projections and pricing on long term gas contracts.37

In 2008 and 2009, weaker economic growth (domestically and internationally) softened demand for natural gas and eased price pressure.38 Figure 3.4 shows indicative price data for the period 2005 to 2009 for domestic gas and LNG exports in Australia. Commentary on the pricing patterns on the east versus west coast is provided in detail in Section 3.2.2 and 3.2.3.

33 Ibid at 1 at 244. 34 Ibid at 1 at 244 and Ibid at 2 at 106. 35 Ibid. 36 Australian Energy Regulator, State of the Energy Market 2008, at 243. 37 Ibid at 1 at 244. 38 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Figure 3.4: Indicative wholesale natural gas prices

Notes: 1. Prices for the second quarter of the year (April-June). 2. Data for Producers A, B, C and D are average company realisations for specific Australian gas producers. Source: State of the Energy Market 2009

3.1.3 Pipelines

Australia’s gas transmission pipeline system has almost trebled in length since the early 1990s, and around $4 billion has been invested or committed to new transmission pipelines and expansions since 2000.39 A large portion of this investment has been in long-haul cross border pipelines that have introduced new sources of supply and improved the security of gas supply on the east coast. The interconnected nature of the eastern jurisdictions has not only widened the gas supply options available, it has also created a more competitive landscape for gas producers, pipeline operators and gas retailers.

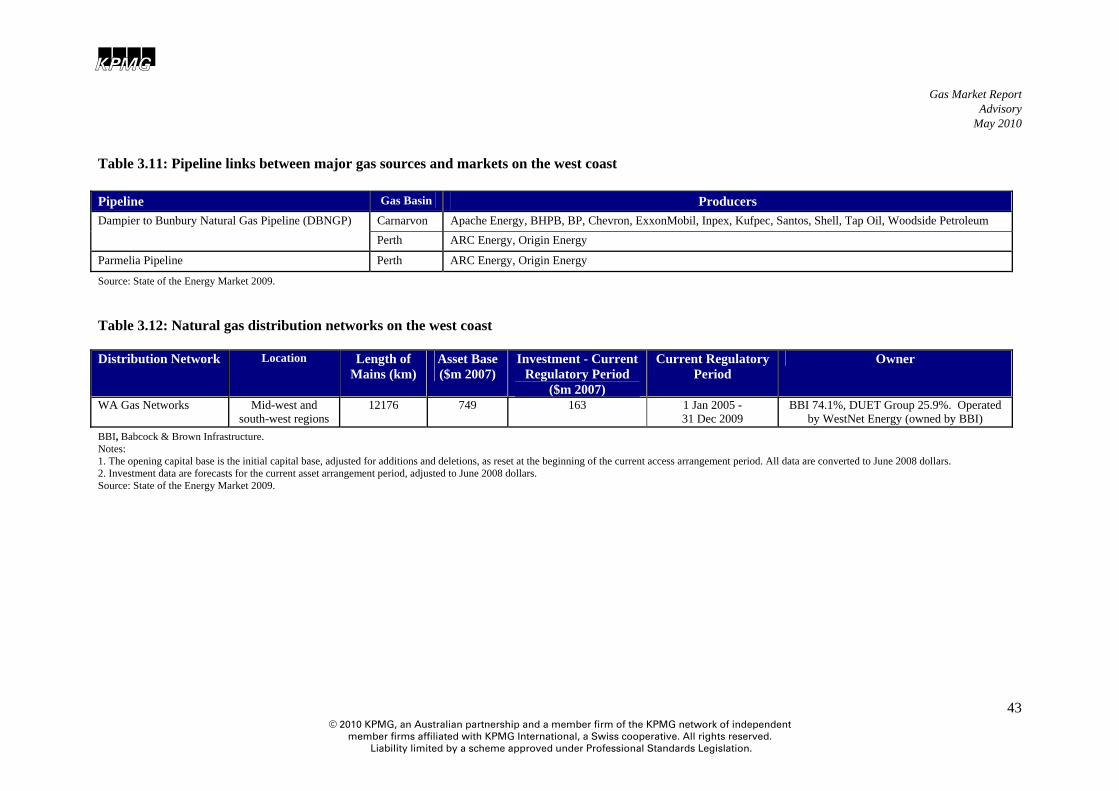

Transmission pipelines in Western Australia and the Northern Territory are not interconnected with other jurisdictions. WA is serviced by three main pipelines: the Dampier to Bunbury Pipeline (DBNGP) (holds the significant position of suppling the south west of WA), Goldfields Pipeline and the Parmelia Pipeline. There has been sizeable investment in WA pipelines in the past ten years, including expansion of the DBNGP and new pipelines to supply gas to the mining and resources sector.40 In NT, the Amadeus Basin to Darwin Pipeline transports gas from the Mereenie and Palm Valley gas fields.

In general it is cheaper to transport gas into Sydney, Canberra and Adelaide from the Cooper Basin than it is from the Victorian coastal basins.41 Tariffs for interruptible services are typically 30% higher than that of firm transportation charges. However, they are paid on the actual quantities shipped rather than on reserved capacity.42 Transmission through the high pressure transmission system is the smallest contributor to delivered costs for residential consumers in Australia’s capital

39 Ibid at 1 at 254. 40 Ibid at 1 at 255. 41 Ibid at 1 at 272. 42 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

cities. Transmission charges range from 2% of delivered gas in Adelaide and Melbourne, to 7% in Perth.43

Figure 3.5 shows Australia’s major gas transmission pipelines. Figure 3.5: Australia's major gas transmission pipelines

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Gas distribution networks in Australia deliver over 370 petajoules of gas per year and have a combined valuation of over $8 billion.44 The total length of Australia’s gas distribution networks expanded from approximately 67,000 kilometres in 1997 to over 82,000 kilometres in 2009.45 Natural gas is now reticulated to most Australian capital cities, major regional areas and towns. Investment to augment and expand the networks is forecast at about $2 billion in the current access arrangement periods (typically five years).46 The investments are relatively small and stable over time compared to gas transmission capital projects, whose investment cycles are often ‘lumpy’.

The major gas distribution networks in Australia are privately owned, with South Australia, Victoria, Western Australia and Queensland having privatised their state-owned networks in 1993, 1997, 2000 and 2006 respectively.47 The construction of new transmission pipelines provides opportunities to develop new distribution networks, which otherwise tend to focus on roll-out and upgrade projects. Distribution charges for metering and transport often represent the most significant component of retail gas prices for small gas users (up to 60%).48

Figure 3.6 shows the location of Australia’s gas distribution networks.

44 Ibid at 1 at 276. 45 Ibid. 46 Ibid. 47 Ibid. 48 Ibid at 1 at 275.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Figure 3.6: Australia’s gas distribution networks

Source: State of the Energy Market 2009

The regulatory framework underpinning gas transmission and distribution in Australia has increasingly gained focus as the rate of project commercialisation supersedes the current capabilities of gas transport infrastructure. The Australian Energy Regulator (AER) is responsible for the economic regulation of covered natural gas transmission and distribution pipelines in all states and territories (except WA). It also enforces the national gas law and national gas rules in all jurisdictions, and regulates retail markets (other than retail pricing) in all states (except WA and NT). The AER is responsible for setting the rate of return on investments made in gas networks.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3.1.4 Gas-fired generation About 200 large electricity generators operate in the National Electricity Market (NEM) jurisdictions in eastern and southern Australia.49 Of the registered NEM generation capacity, about 20% is GFG.50 However, given its positioning as intermediate and peaking plant generators, GFG supplies only about 8% of the electricity output.51 Black and brown coal account for around 60% of the registered NEM capacity, yet supply 85% of the output, given their positioning as predominantly baseload generators. Hydroelectric generation accounts for 17%, but has less than 6% of the output.52 In WA, around 60% of installed generation capacity is fuelled by natural gas, and 35% by coal.53 In SA and NT, electricity generation is also mainly fuelled by natural gas.54 The majority of committed and proposed investments in Australian generation capacity involve GFG (2200 MW out of total 2650 MW of committed capacity)55, which is an indication of the industry’s anticipation of the Federal Government’s climate change policies.56 Currently, coal is the lowest cost fuel sources for electricity generation in Australia, followed by gas. However, due to its lower carbon intensity, gas is well placed to become more cost competitive against coal, should the Government’s proposed Carbon Pollution Reduction Scheme (CPRS) be enacted. However, the expanded Renewable Energy Target (RET) does erode the benefits of the CPRS for the gas industry, by forcing renewable energy supply against market forces. The impact of the CPRS and enhanced RET are discussed in more detail in Chapter 6. Most of the committed GFG projects are expected to be commissioned by the end of 2010. Table 3.2 shows the GFG projects that were completed in the twelve month period to October 2009. Figure 3.7 shows the location and fuel type of Australian generation projects in advanced stages of development (the size of the GFG projects is also indicated). Table 3.3 shows the NEM’s committed investment generation projects as at June 2009. Table 3.4 lists the major generation development projects proposed for the NEM, showing that the bulk of proposed capacity occurs in NSW (possibly because the region is the highest net importer in the NEM) and Queensland.57

49 Ibid at 1 at 52. 50 Ibid at 1 at 55. 51 Ibid. 52 Ibid. 53 Ibid at 1 at 112. 54 Ibid at 1 at 59. 55 Ibid at 1 at 62. 56 Ibid at 36 at 67. 57 Ibid at 1 at 62.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.2: GFG developments completed between October 2008 – October 2009

Project Location Company Capacity (MW)

Capital Expenditure (A$m)

NewGenKwinana WA Babcock and Brown Power/ERM 330 400 Newman WA Babcock and Brown Power 37 90 Neerabup WA ANZ Infrastructure Services/ERM Power 320 425 Braemar 2 QLD ERM Power/Arrow Energy 450 546 Tallawarra Stage 1 NSW TRUenergy Tallawarra 400 350 Uranquinty NSW Origin Energy 640 700 Quarantine Expansion SA Origin Energy 120 86 Weddell Stage 2 NT Power and Water Corporation 43 N/A Tamar Valley TAS Aurora Energy 390 451

Source: ABARE, Electricity generation – Major development projects - April 2009 and October 2009 listings. Figure 3.7: Advanced electricity generation projects

Source: ABARE, Electricity generation – Major development projects - October 2009 listing.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.3: Committed investment projects in the NEM, June 2009

Developer Power Station Technology Capacity (MW)

Planned Commissioning Date

Queensland Queensland Gas Company Condamine CCGT 135 2009 - 10 Origin Energy Darling Downs CCGT 605 2010 Origin Energy Mount Stuart (extension) OCGT 127 2009 Rio Tinto Yarwun Cogen Gas cogeneration 152 2010 New South Wales Eraring Energy Eraring (extension) Coal fired 120 2010 – 11 Delta Electricity Colongra (units 2 – 4) OCGT 471 Victoria AGL Energy Bogong Hydro 140 2009 – 10 Origin Energy Mortlake OCGT 518 2010 Pacific Hydro Portland Wind 164 2009 – 10 South Australia International Power Port Lincoln OCGT 25 2010 Tasmania Aurora Energy Tamar Valley CCGT 196 2009

Note: Capacity is summer capacity for all generators Source: State of the Energy Market 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.4: Major proposed generation investment in the National Electricity Market, 2009 Developer Power Station Technology Capacity

(MW) Planned

Commissioning Date Queensland Origin Energy Spring Gully CCGT 1000 n/a ERM Energy Braemar 3 Gas 462 2012 ERM Energy Braemar 4 Gas 434 2013 CS Energy Swanbank F CCGT 380 2012 New South Wales Macquarie Generation Tomago Gas Turbine OCGT 500 n/a Eraring Energy Eraring upgrade Coal 60 2011 Eraring Energy Eraring upgrade Coal 60 2012 ERM Power Wellington (Unit 5) OCGT 280 2012 ERM Power Wellington (Units 1 - 4) OCGT 616 2011 AGL Energy Leaf's gully Gas 360 2012 Delta Electricity Mt Piper expansion Coal 600 2015-2016 Delta Electricity Bamarang CCGT 450 2012-2013 Delta Electricity Marulan Gas Turbine CCGT 420 2013-2014 Delta Electricity Marulan Gas Turbine OCGT 330 2013-2014 Delta Electricity Bamarang CCGT 330 2012-2013 International Power Parkes OCGT 150 n/a International Power Buronga OCGT 120 n/a Victoria Origin Energy Mortlake Stage 2 CCGT 470 n/a Santos Shaw River CCGT 500 2012 AGL Energy Tarrone Gas 500 2012 Solar system Solar System Victorian Solar

Energy Facility (Unit 2-51) Solar Concentrator 100 2012

Solar system Solar System Victorian Solar Energy Facility (Unit 52-77)

Solar Concentrator 54 2013

HRL Group and Harbin Power Engineering

IDGCC demonstration plant IDGCC 500 2013

South Australia Altona Resources Arkaringa IGCC 560 2014 International Power Pelican Point (Stage 2) Gas 300 n/a Strike Oil Kingston Coal 40 2015 Tasmania Gunns Bell Bay Pulp Mill power

plant Biomass 184 2012

Notes: 1. CCGT, combined cycle gas turbine; IDGCC, integrated drying and gasification combined cycle; OCGT, open cycle gas turbine 2. Excludes wind generation. Source: State of the Energy Market 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3.1.5 Gas retailing Gas retailing is the final component of the gas supply chain. All state and territory governments have introduced full retail contestability (FRC) for gas customers, which allows customers freedom of choice for selecting their gas supplier. In most jurisdictions there is at least one host retailer (whom are subject to various regulatory obligations), and new entrants. The major retail players in most jurisdictions are privately owned. On the east coast, AGL Energy, Origin Energy and TRUenergy are the largest retailers. Each has significant market share in Victoria and South Australia. AGL Energy is the largest gas retailer in NSW and jointly owns (with the ACT Government) the largest ACT retailer.58 AGL Energy acquired significant market share via the 2006-07 privatisation process, while Origin Energy was already established as a retailer in that state.59 In WA, Alinta (owned by Babcock and Brown Power) is the leading retailer and is the only retailer licensed to retail to customers consuming less than 0.l8 terajoules per year on the main distribution systems.60 NT Gas (owned by the APA Group) supplies a small quantity of gas to commercial and industrial customers in Darwin. Table 3.4 lists the active gas retailers for the small customer market. Table 3.5: Active gas retailers for the small customer market, May 2009 Retailer1 Ownership VIC NSW QLD SA TAS2 ACT WA

ActewAGL Retail ACT Government and AGL Energy AGL Energy AGL Energy Alinta Babcock & Brown Power Aurora Energy Tasmanian Government Australian Power & Gas Australian Power & Gas Country Energy NSW Government Energy Australia NSW Government Red Energy Snowy Hydro 3 Simply Energy International Power Tas Gas Retail Babcock & Brown Infrastructure Origin Energy Origin Energy TRUenergy CLP Group Victoria Electricity Infratil Active retailers 7 6 2 4 2 2 1 Approx market size ('000 000 customers)4 1.68 1.19 0.15 0.37 0.005 0.09 0.58 Host (incumbent retailer) New Entrant Notes: 1. Not all licensed retailers are listed. Some of the retailers listed only offer gas services as part of a gas and electricity contract. The list also excludes three small retailers (BRW Power Generation (Esperance), Dalby Town Council and Roma Town Council). 2. There is no host retailer in Tasmania as gas distribution and retail services have only been available for a short time and FRC existed from the market start. 3. Snowy Hydro is owned by the New South Wales Government (58%), the Victorian Government (29%) and the Australian Government (13%). 4. Customer numbers for Queensland, New South Wales and the ACT are estimates based on the number of distribution connection points. Source: State of the Energy Market 2009 58 Ibid at 1 at 295. 59 Ibid. 60 Ibid at 1 at 296.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

While all jurisdictions have introduced FRC, NSW, Victoria, SA and WA continue to regulate gas retail prices for small customers (the remaining states and territories do not). Wholesale gas costs and transportation charges account for the majority of retail gas prices.61 Retail operating costs and retail margins account for around 36% of retail prices in QLD and 22% in SA.62 Retail gas prices show significant variation for customers with different volume requirements and at different geographical locations. For small customers, distribution charges for metering and transport often represent the most significant component – up to 60% - of retail gas prices.63 However, regulatory arrangements governing the market, wholesale gas costs and industry scale also affect the retail prices. For businesses, the real price of gas has fallen by 10.6% since 1991, while for households it has increased by 28.6%.64 As shown in Figure 3.9, real household gas prices have increased since 1996 in all states except Victoria, however the pattern and rate of adjustment has varied.65 Customers in all states except QLD experienced real price increases from 2000-01 to 2008-09 of between 19.9% and 25.6%.66 Queensland prices were relatively stable from 2000-01 to 2004-05 but have since risen sharply.67 Figure 3.8: Real retail gas prices, July 1996 - March 2009 (forecasts based on 1998-99 prices)

Notes: The dashed lines are estimates based on inflating 1998-99 AGA data by the CPI series for gas and other household fuels for the capital city in that state. Source: State of the Energy Markets 2009

A high degree of vertical integration is a key feature of the Australian gas market, as gas retailers like Origin Energy and AGL increasingly look to gain exposure to all aspects of the gas supply chain – from securing gas acreage, to developing gas reserves, securing third party long term gas supply contracts, negotiating spot gas deals, building GFGs, forging LNG exporting projects and optimising gas placement opportunities between customers, GFGs and LNG projects.

61 Ibid at 1 at 304. 62 Ibid. 63 Ibid at 1 at 275. 64 Ibid at 1 at 307. 65 Ibid. 66 Ibid. 67 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3.2 East coast

3.2.1 Suppliers The main suppliers of gas on the east coast are Origin Energy, British Gas (BG), Santos, Arrow Energy, BHP Billiton and ExxonMobil. Cooper and Gippsland dominated gas supply under long term (30 year) contracts. The market has now expanded and offers numerous sources of supply. The acceptance of CSG as a viable form of gas for commercial and retail customers and as a feedstock for GFGs and LNG trains has facilitated this step change in market structure.

The Gippsland Basin, which lies mostly offshore from the south east corner of Victoria, has great potential for bringing on-line new gas supplies for the east coast market. Production at the Longtom field started in October 2009. Kipper is currently Victoria’s largest known undeveloped gas resource, having estimated reserves of 620 Bcf.68 First gas production from the US$1.1 billion Kipper gas and condensate project is anticipated for 201169, with the field having an estimated lifespan of 15 years.70 Also in the Gippsland Basin, the Turrum field holds an estimated 1 Tcf of gas.71 The US$1.3 billion Turrum natural gas and condensate project is due for completion in 2011.72 Other fields in the Gippsland Basin expected to come online include Basker-Manta-Gummy and Sole.

Exploration at the Otway Basin (located off the south western corner of Victoria and the south east corner of South Australia) is mature onshore and immature offshore. Commercial gas discoveries include the offshore Thylacine and Geographe (combined raw gas reserves of approximately 950 Bcf)73, Minerva (301 Bcf)74 and Casino (280 Bcf)75 fields. Undeveloped gas discoveries include the La Bella (210 Bcf)76 and Henry (estimated 2P reserves of 150 PJ)77 fields. First gas production from the Henry field is expected during the first half of 2010.

Not all states have equal access to gas supplies. Unlike other mainland states, NSW does not have substantial indigenous gas production. It sources nearly all of its natural gas from interstate. NSW remains highly unexplored for natural gas compared to its neighbouring states, despite it being Australia’s largest source of gas demand. With QLD LNG plants expected to start shipping gas overseas in about 2014, some industry analysts argue it is critical that NSW act now to sure up a secure gas supply.

However, NSW has significant gas production potential. While the NSW CSG fields are yet to be proven commercial, this local supply has the potential to rapidly expand and reduce the need for

68 Department of Primary Industries, Oil and Gas Industry Activity, http://www.dpi.vic.gov.au/dpi/nrenmp.nsf/LinkView/4091419D117B5E654A2569B2002022F456D4D5E9AEF563E84A256A800011E5D6, 26 June 2009. 69 M. Lampard, ABARE, Minerals and energy: Major development projects – October 2009 listing, November 2009 at 8. 70 Ibid at 68. 71 Ibid. 72 Ibid at 60 at 8. 73 Woodside website, Otway, http://www.woodside.com.au/Our+Business/Production/Australia/Otway+Southern+Australia.htm. 74 Ibid at 68. 75 Ibid at 68. 76 Australian Government Department of Industry, Tourism and Resources, Release of Offshore Petroleum Exploration Areas Australia 2006 at 18. 77 Santos Website, Henry, http://www.santos.com/Content.aspx?p=343, 14 October 2009.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

interstate gas import in the future. NSW CSG proponents cite infrastructure and state regulations as the two biggest barriers holding back commercialisation of the reserves.

The prospect of a pipeline directly linking the CSG fields of QLD, Gunnedah and the Hunter Valley to major population centres in Sydney, Newcastle and Wollongong, is already having positive effects, with Santos initialising exploration at Gunnedah based on available transport infrastructure. This Queensland Hunter Gas Pipeline is discussed in more detail in Section 3.2.3.

Santos has the largest involvement with CSG in NSW. In June 2008 its Gunnedah tenements had the potential to contain 40 Tcf of CSG, more than that controlled by the NWS Venture. It has plans to drill 18 to 20 wells over the next 18 months in pursuit of proving up a preliminary resource. Santos has also considered LNG plants in Newcastle. While port constraints are a possible hurdle to this development, NSW gas may also be exported through QLD given sufficient transport capacity.

The Gloucester Basin is physically smaller than the other prospective coal seam gas basins in NSW and QLD, and therefore is unlikely to hold enough gas to support an LNG project on its own. However, it is large enough to support power stations and industrial users in the region.

As mentioned, NSW is considered to be a tougher operating environment than QLD. Approvals that may take up to one year in QLD, may take up to three in NSW. The NSW Government did launch the Exploration NSW initiative in 2000, which provided $30m of funding over seven years to promote minerals and petroleum exploration. It has been suggested this is a small proportion of what is needed.

3.2.2 Wholesale pricing Historically, wholesale gas prices on the east coast showed some evidence of rising prices.78 QLD prices in 2006 were in the range of $2.50 to $2.90/GJ, rising to around $4/GJ in 2008.79 However, EnergyQuest reported mixed outcomes in 2008-09.80 One QLD joint venture recorded average price realisations of $3.15/GJ in June quarter 2009.81

On the east coast generally, one major producer recorded average prices of around $3.46/GJ in June quarter 2009, compared with $3.12/GJ in the equivalent period of 2008.82 CSG prices in QLD were typically lower than conventional gas, however the onset of numerous CSG-LNG developments in QLD in the next few years may see wholesale gas prices rise in the longer term.83 In the short to medium term, EnergyQuest projects that domestic prices may ease during the lengthy ramp-up of LNG export capacity.84 During this period, increased supplies of gas will be available at relatively low domestic prices for domestic purposes such as power generation.85

78 Ibid at 36 at 244. 79 Ibid at 1 at 245. 80 Ibid. 81 Ibid. 82 Ibid. 83 Ibid. 84 Ibid. 85 Ibid at 1 at 36.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

The price listings of the Victorian spot market (which accounts for only 10-20% of the wholesale volumes traded in Victoria) can provide some comparisons to gas contract prices. However, the volatility that is observed in spot market prices (given prices can reach as high as the VoLL price of $800/GJ) means they are not necessarily indicative of underlying contract prices.

Until 2005, spot prices remained relatively stable (excluding the winter peaking demand profile). However, since then volatility has increased with substantially higher winter prices observed in 2006, 2007 and 2008 (spot prices peaked at $336/GJ on 17 July 2007).86 Spot price spikes which occurred in 2007 due to drought conditions, caused a shift to GFG and a corresponding increase in gas demand. Since then, however, spot prices have eased back towards trend levels.87 For June quarter 2009, Victorian spot prices averaged $2.68/GJ, down 19% on the previous year’s June quarter average.88 EnergyQuest reported that spot prices in June 2009 were below current contract prices.89 This outcome reflects a combination of factors:

• The expansion of the Victorian Transmission System via the Corio Loop development (completed in 2008) eased capacity constraints on the network, helping avoid winter price spikes.

• The easing of the drought in 2008, lead to reduced interstate demand for gas for electricity generation.

• A weaker economy and a relatively mild winter led to some easing of demand in 2009.90

3.2.3 Pipelines Gas transport in the east coast market is relatively more mature and interlinked than that of the west coast, however it services a greater demand base. There exists a significant interconnected network of transmission and distribution infrastructure, which is still progressively evolving to support the development of a competitive gas market. While cross border gas volume swaps between counterparties still remains a significant means of meeting gas demand on the east coast, significant investment has and will take place to enable greater deliveries of gas from QLD to the southern states, to pending LNG terminals near Gladstone, and to new GFGs that will potentially be built in response to the Federal Government’s climate change initiatives.

In the twelve months to October 2009, two gas pipeline projects were completed on the east coast. The Queensland to South Australia/New South Wales (QSN) Link was completed at an estimated cost of $165 million and connects the South Western Queensland Pipeline to the Moomba gas hub in north-east South Australia. Its transport capacity is 60 PJ/yr and it is a key lever in the transport of CSG produced in the Surat and Bowen Basins to be transported to the Moomba-Adelaide Pipeline (MAP), and the Moomba-Sydney Pipeline (MSP).91

Also completed in Queensland, at an estimated cost of $110 million, was the Berwyndale to Wallumbilla pipeline. Spanning 110km this pipeline connects the CSG fields around Berwyndale (located approximately 300km north-west of Brisbane) to the Wallumbilla gas hub.92

86 Ibid at 1 at 247. 87 Ibid at 36 at 245. 88 Ibid at 1 at 247. 89 Ibid. 90 Ibid. 91 A. Copeland, ABARE, Minerals and energy: Major development projects – April 2009 listing, May 2009 at 3. 92 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

There are also several natural gas pipelines at an advanced stage of development. In May 2009, Australian Pipeline Trust made the decision to proceed with the expansion of the Moomba to Sydney pipeline. The $90 million project is scheduled to be completed in 2010.93 SP AusNet is undertaking expansions to two of its pipelines: the Eastern Gas Pipeline (EGP) (which transports from Longford, Victoria to Wollongong) and the Queensland Gas Pipeline (QGP) (Wallumbilla to Gladstone). At an estimated cost of $41 million, the EGP expansion will increase capacity by 20 PJ/yr. At an estimated cost of $112 million, the QGP expansion will increase its capacity by 25 PJ/yr.94

Though still in planning phases, the Queensland Hunter Gas Pipeline (QHGP) is another key east coast infrastructure development. In April 2007, the QLD Government granted a pipeline licence for the QLD portion of the project. In February 2008, the NSW Government declared the project as critical infrastructure. In December 2008 the project was granted Federal Government approval. In February 2009, NSW approved their segment of the pipeline. The estimated capital cost of the project is $900m.95

If successful, the QHGP would be the third gas pipeline into NSW, delivering competitively priced gas from the Wallumbilla Gas hub in QLD to eastern Australia. It would initially free flow 85 PJ/year, however, with installation of compression, it could potentially increase gas flow to 160 PJ/year (NSW currently uses 200+ PJ/year).96 The importance of the QHGP lies in the fact that it could: • Provide much needed new gas pipeline capacity and reduce pressure on tariffs: the MSP and EGP

are nearing full delivery capacity, and the NSW transmission tariffs tripled in 2008 due to the capacity constraints with the MSP and EGP.

• Improve security of supply in the face of growing gas demand in NSW: by diversifying the supply sources and facilitating access to expanding gas reserves in QLD and NSW.

• Stimulate exploration and development of prospective gas reserves in northern and central NSW: including the commercialisation of the Gunnedah CSG field (estimated at 40 Tcf). The successful development of NSW CSG reserves could yield significant royalty revenue for the NSW Government.

• Facilitate the development of GFGs for base load power: NSW is in need of more generation capacity.

• Feed and facilitate potential LNG developments in the Hunter region. Table 3.5 lists the major gas transmission pipelines on the east coast, and their key physical and ownership characteristics. Table 3.6 shows the gas basins and producers that feed the major transmission pipelines. Table 3.7 shows the major gas distribution networks on the east coast, and their key physical and ownership features.

93 M. Lampard, ABARE, Minerals and energy: Major development projects – October 2009 listing, November 2009 at 9. 94 A Copeland, ABARE, Minerals and Energy: Major development projects – April 2009 listing, May 2009 at 9. 95 Queensland Hunter Gas Pipeline Website, http://www.qhgp.com.au/index.asp, accessed 18 November 2009. 96 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.6: Major transmission pipelines on the east coast

Pipeline Location Length (km)

Year Constructed

Capacity (TJ/D)

Covered? Valuation ($ million)

Current Access

Arrangement

Owner Operator

Queensland QSN Link (Ballera to Moomba interconnect) Qld-SA

(and NSW) 180 2009 212 No 165 (2009) n/a Epic Energy (Hastings) Epic Energy

South West Queensland Pipeline (Ballera to Wallumbilla)

Qld 756 1996 168 No n/a n/a Epic Energy (Hastings) Epic Energy

Roma (Wallumbilla) to Brisbane Qld 440 1969 208 Yes 296 (2006) 2007-2011 APA Group APA Group

Queensland Gas Pipeline (Wallumbilla to Gladstone)

Qld 629 1989-1991 79 No n/a n/a Jemena (Singapore Power International (Australia))

Jemena Asset Management

Carpentaria Pipeline (Ballera to Mount Isa) Qld 840 1998 117 Yes (light regulation)

n/a n/a APA Group APA Group

Wallumbilla to Darling Downs Pipeline Qld 205 2009 400 No 90 (2009) n/a Origin Energy Origin Energy

Berwyndale to Darling Downs Pipeline Qld 113 2009 No 70 (2009) n/a AGL Energy AGL Energy North Queensland Gas Pipeline Qld 391 2004 108 No 160 (2005) n/a Victorian Funds Management

Corporation AGL Energy, Arrow

Energy Dawson Valley Pipeline Qld 47 1996 30 Yes 8 (2007) 2007/2016 Anglo Coal (51%), Mitsui (49%) Anglo Coal New South Wales Moomba to Sydney Pipeline SA-NSW 2029 1974-1993 420 Partial 835 (2003) 2004-2009 APA Group APA Group

Eastern Gas Pipeline (Longford to Sydney) Vic-NSW 795 2000 250 No 450 (2000) n/a Jemena (Singapore Power International (Australia))

Jemena Asset Management

Central West (Marsden to Dubbo) Pipeline NSW 255 1998 10 Yes 28 (1999) 2000-2010 APA Group APA Group Central Ranges (Dubbo to Tamworth) Pipeline

NSW 300 2006 7 Yes 53 (2003) 2005-2019 APA Group Country Energy (NSW Govt)

Victoria Victorian Transmission System (GasNet) Vic 2035 1969-2008 1030 Yes 524 (2007) 2008-2012 APA Group APA Group/AEMO South Gippsland Natural Gas Pipeline Vic 250 2006-2010 No 50 (2007) n/a Multinet Gas Jemena Asset Management

VicHub Vic n/a 2003 150 (into Vic)

No n/a n/a Jemena (Singapore Power International (Australia))

Jemena Asset Management

South Australia SEA Gas Pipeline (Port Campbell to Adelaide)

Vic-SA 680 2003 314 No 500 (2003) n/a International Power, APA Group, and REST (equal shares)

APA Group

Moomba to Adelaide Pipeline SA 1185 1969 253 No 370 (2001) n/a Epic Energy (Hastings) Epic Energy

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Tasmania Tasmanian Gas Pipeline (Longford to Hobart) Vic-Tas 734 2002 129 No 440 (2005) n/a Babcock & Brown Infrastructure Jemena Asset Management

REST, Retail Employees Superannuation Trust Notes: 1. Covered pipelines are subject to regulatory arrangements under the National Gas Law. The Australian Energy Regulator (AER) covered pipelines outside Western Australia, where the Economic Regulation Authority is the transmission regulator. 2. For covered pipelines subject to full regulations, valuation refers to the opening capital base for the current regulatory period. For the Moomba to Sydney Pipeline, the Australian Competition Tribunal determined the valuation. For non-covered pipelines, listed valuations are estimated construction costs, subject to availability of data. 3. Coverage of the Moomba to Sydney Pipeline was partly revoked in 2003. The revoked portion runs from Moomba to the offtake point of the Central West Pipeline at Marsden. The covered portion became a light regulation pipeline in 2008 Source: State of the Energy Market 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.7: Pipeline links between major gas sources and markets on the east coast Pipeline Gas Basin Producers Brisbane Roma to Brisbane pipeline Surat-Bowen Mosaic, Origin Energy, Santos, Arrow Energy,

Mitsui, Molopo, BG Group Sydney and Canberra

Moomba to Sydney Pipeline (MSP) Cooper, Sydney Santos, Beach Petroleum, Origin Energy, AGL Energy, Sydney Gas

Adelaide Moomba to Adelaide Pipeline (MAP) Cooper Santos, Beach Petroleum, Origin Energy SEA Gas Pipeline Otway and Gippsland BHPB, ExxonMobil, Origin Energy, Santos

AWE, Beach Petroleum South West Queensland Pipeline / QSN Link

Darwin Amadeus Basin to Darwin Amadeus Magellan, Santos Bonaparte Pipeline Bonaparte ENI Tasmania Tasmanian Gas Pipeline Cooper (via MSP and NSW-Vic

Interconnect), Gippsland, Otway, Bass

Santos, Beach Petroleum, Origin Energy

Note: In some cases, it may only be possible to source gas from a particular basin using backhaul and swap arrangements. Source: State of the Energy Market 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.8: Natural gas distribution networks on the east coast

Distribution Network Location Length of Mains

(km)

Opening Capital Base (2008, $m)1

Investment - Current Regulatory Period

($m 2008)2

Current Regulatory

Period

Owner

New South Wales and ACT Jemena Gas Networks (NSW) Sydney, Newcastle/Central Coast and

Wollongong 23800 2300 542 1 July 2005 - 30

June 2010 Jemena (Singapore Power

International) Central Ranges System Tamworth 180 n/a n/a 2006-2019 APA Group Wagga Wagga distribution Wagga Wagga and surrounding areas 622 49 8 1 July 2005 - 30

June 2010 Country Energy (NSW Govt)

ActewAGL ACT, Palerang (Bungendore) and Queanbeyan

3604 266 66 1 July 2004 - 30 June 2010

ACTEW Corporation (ACT Govt) 50%; Jemena (Singapore Power International (Australia)) 50%

Victoria Multinet Melbourne's eastern and south-

eastern suburbs 9585 888 232 1 Jan 2008 - 31 Dec

2012 DUET Group 79.9%; BBI 20.1%

Envestra (Stratus) Melbourne, north-east and central Victoria, and Albury-Wadonga

region

9603 859 411 1 Jan 2008 - 31 Dec 2012

Envestra (Cheung Kong Infrastructure 18.5%, APA Group 30.6%)

SP Ausnet (Westar) Western Victoria 9284 955 342 1 Jan 2008 - 31 Dec 2012

SP AusNet (listed company: Singapore Power International 51%)

Queensland APT Allgas South of the Brisbane River 2605 362 141 1 July 2006 - 30

June 2011 APA Group

Envestra Brisbane, Gladstone and Rockhampton

2489 261 104 1 July 2006 - 30 June 2011

Envestra (Cheung Kong Infrastructure 18.5%, APA Group 30.6%)

South Australia Envestra Adelaide and surrounds 7477 942 213 1 July 2006 - 30

June 2011 Envestra (Cheung Kong Infrastructure

18.5%, APA Group 30.6%) Tasmania Tasmanian Gas Network Hobart, Launceston and other towns 730 1121 n/a Not regulated Tas Gas (BBI) Notes: 1. For Tasmania, the asset value is an estimated construction cost. For other networks, the asset value is the opening regulated asset base for the current regulatory period, adjusted to June 2008 dollars. 2. Investment data are forecasts for the current asset arrangement period, adjusted to June 2008 dollars. 3. National totals exclude the Northern Territory Source: State of the Energy Market 2009.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

3.2.4 Gas storage Gas storage facilities are limited on the east, however a large volume of storage is provided in the form of linepack (capacity within the gas pipelines). It is anticipated that more storage facilities will be built as demand for gas (especially for GFG) is forecast to increase.

There are two gas storage facilities in Victoria: the Iona Gas Plant and the Dandenong LNG storage facility. The Iona Gas storage facility is owned by TRUenergy and located near Port Campbell in southwest Victoria.97 The Iona facility is located in a depleted gas field originally used to supply the Western System, adjacent to the Otway Gas Plant currently under construction.98 This facility is connected to the VTS via the South West Pipeline to Melbourne.99 It is also connected to the SEA Gas Pipeline to provide flow to Adelaide.100

The Dandenong LNG storage facility is owned and operated by APA Group.101 It has a fully contracted capacity of around 0.7 PJ and provides peak shaving and security of supply services for the VTS.102 This facility injects gas into the VTS to meet peak winter demands as well as providing a truck loading service station for LNG tankers. The facility is not subject to regulation under the National Gas Code, and APA Group has no plans to change this situation at present.

3.2.5 Gas-fired generation GFG on the east coast has seen great growth in recent years, a result of the anticipation of a price on carbon (which heightens the attractiveness of gas as a fuel source over coal), and for its means as a channel for excess ramp-up gas from the CSG fields of QLD. Following the expected privatisation of NSW’s electricity generation assets, new GFG plants are expected, given NSW is forecast to be short baseload capacity in the near future. Gas is the most likely fuel choice, assuming the development of NSW’s CSG fields and adequate gas and electricity transmission capacity is in place.

In the six months to April 2009, ten electricity generation projects were completed, six of which were GFGs.103 Two of these were in NSW. With a 640MW capacity, the Uranquinty power station (located near Wagga Wagga in south-west NSW) is the largest of the six. The project had a capital expenditure bill of $700m. Stage 1 of the 400 MW Tallawarra power station (located around 100km south of Sydney) was completed. Origin Energy also completed the 120 MW expansion of its Quarantine power station, which is located in South Australia.104 In the six months to October 2009, no generation projects were completed.

97 TRUenergy Website, Iona Gas Plant, http://www.truenergy.com.au/Production/Iona/index.xhtml, last accessed 17 November 2009. 98 Ibid. 99 Ibid. 100 Ibid. 101 APA Group Website, Victoria, http://www.apa.com.au/our-business/gas-transmission-and-distribution/victoria.aspx, last accessed 17 November 2009. 102 Ibid. 103 A. Copeland, ABARE, Electricity Generation, Major development projects – April 2009 listing, May 2009 at 5. 104 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

There are also a number of advanced GFG projects on the east coast. Origin Energy has commenced construction on Stage 1 of the 550 MW Mortlake power station in Victoria. With a capital expenditure of $640m, it is scheduled for completion in 2010. Origin may also build a second 450MW unit at the complex at some future date.105

Origin Energy also has the Darling Downs project in Queensland, which has a capacity of 630MW, delivered at a capital cost of $951m. The project includes the construction of a pipeline to access CSG reserves in the area surrounding Roma and Chinchilla. It is scheduled to be completed in early 2010.106

Table 3.8 shows the existing and committed gas-fired power stations in each state belonging to the east coast market. Figure 3.10 shows registered generation capacity by state by fuel source.

105 A. Copeland, ABARE, Electricity Generation, Major development projects – April 2009 listing, May 2009 at 5. 106 Ibid.

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Table 3.9: Existing and committed gas-fired power stations in the east coast market

Station Type Configuration Registered capacity (MW)

New South Wales Colongra OCGT OCGT (4x166 MW) 664 Smithfield CCGT/Cogen OCGT (3x38 MW), Steam turbine (1x62 MW) 160 Tallawarra CCGT OCGT (1x260 MW), Steam turbine (1x160 MW) 435 Uranquinty OCGT OCGT (4x166 MW) 664 Queensland Barcaldine CCGT OCGT (1x37 MW), Steam turbine (1x18 MW) 55 Braemar OCGT OCGT (3x168 MW) 504 Braemar 2 OCGT OCGT (3x168 MW) 504 Condamine A CCGT OCGT (2x45 MW), Steam turbine (1x45 MW) 135 Darling Downs CCGT OCGT (3x120 MW), Steam turbine (1x270 MW) 630 Oakey OCGT OCGT (2x141 MW) 282 Roma GT OCGT OCGT (2x40 MW) 80 Swanbank E CCGT CCGT (1x385 MW) 385 Townsville CCGT OCGT (1x165 MW), Steam turbine (1x82 MW) 242 Yarwun Cogen OCGT (configuration as yet unknown) 160 South Australia Dry Creek GT OCGT OCGT (3x52 MW) 156 Ladbroke Grove OCGT OCGT (2x40 MW) 80 Mintaro GT OCGT OCGT (1x90 MW) 90 Osborne Cogen/CCGT OCGT (1x118 MW), Steam turbine (1x62 MW) 180 Pelican Point CCGT OCGT (2x160 MW), Steam turbine (1x158 MW) 478 Quarantine OCGT OCGT (4x24 MW; 1x120 MW) 216 Torrens Island A Steam turbine Steam turbine (4x120 MW) 480 Torrens Island B Steam turbine Steam turbine (4x200 MW) 800 Tasmania Bell Bay Steam turbine Steam turbine (2x120 MW) 240 Bell Bay Three OCGT OCGT (3x35 MW) 105 Tamar Valley OCGT OCGT OCGT (1x75 MW) 75 Tamar Valley OCGT OCGT (3x40 MW), Steam turbine (1x80 MW) 200 Victoria Bairnsdale OCGT OCGT (2x47 MW) 94 Jeeralang A OCGT OCGT (4x51 MW) 204 Jeeralang B OCGT OCGT (3x76 MW) 228 Laverton North OCGT OCGT (2x156 MW) 312 Mortlake OCGT OCGT (2x275 MW) 550 Newport Steam turbine Steam turbine (1x500 MW) 500 Somerton OCGT OCGT (4x40 MW) 160 Valley Power OCGT OCGT (6x50 MW) 300 Advanced proposals (both in VIC) Mortlake 2 CCGT Unknown 400 Spring Gully CCGT Unknown 1000

Source: ACIL Tasman, Fuel resource, new entry and generation costs in the NEM, 2009

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Liability limited by a scheme approved under Professional Standards Legislation.

Figure 3.9: Registered generation capacity by region by fuel source, 2009