A PROJECT REPORT ON RATIO ANALYSIS FORGENERAL MILLS INDIA PVT LTD. SUBMITTED BY GAURAV RAMESH DHAWANE SUBMITTED TO UNIVERSITY OF PUNE IN PARTIAL FULFILLMENT OF MASTER OF BUSINESS ADMINISTRATION JSPM’S JAYWANTRAO SAWANT COLLEGE OF ENGINEERING HADAPSAR, PUNE 2007-2009

The creditors or suppliers extend short term credit to the concern. If the current assets

are quite sufficient to meet current liabilities then the creditors will not hesitate inextending credit facilities. Current & acid-test ratios will give an idea about the

financial position of the concern.

D) Utility to Employees:-

The employees are also interested in the financial position of the concern

especially profitability. Their wage increases & fringe benefits are elated to the

volume of profits earned by the concern. Various profitability ratios relating to gross

profits, operating profit, net profit, etc. enable employee to put forward their view

points for the increase of wages & other benefits.

E) Utility to Government:-

Government is interested to know the overall strength of the industry.

Government may base its future policies on the basis of industrial information

available from various units. The ratios may be used as indicators of overall financialstrength of public as well as private sector.

F) Tax Audit Requirements:-

Section 44 AB was inserted in the Income Tax Act by the Finance Act, 1984.under this

section every assessed engaged in any business & having turnover or gross receipts

exceeding Rs. 40 lak is required to get the accounts audited by a chartered accountant &

submit the tax audit report before the due date for filing the return under Section 139(1).

This ratio indicates whether your investment in the business is adequately proportionate

to your sales volume. It may also uncover potential credit or management problems,

usually called "overtrading" and "under trading."

Overtrading, or excessive sales volume transacted on a thin margin of investment, presents a potential problem with creditors. Overtrading can come from considerable

management skill, but outside creditors must furnish more funds to carry on daily

operations.

Under trading is usually caused by management's poor use of investment money and their

general lack of ingenuity, skill or aggressiveness.

This ratio, which uncovers management's ability to function in competitive situations

while not excluding intangible assets, is inconclusive if studied by itself. But when

viewed alongside, Working Capital to Total Assets, Retained Earnings to Total Assets,and EBIT to Total Assets, it can confirm whether your business is in imminent danger.

Equity to Debt

Market Value of Common + Preferred Stock

= Equity to Debt RatioTotal Current + Long-Term Debt

This ratio shows you by how much your business's assets can decline in value before it

The Times Interest Earned Ratio shows how many times earnings will cover fixed-

interest payments on long-term debt.

• Leverage Ratios

This group of ratios calculates the proportionate contributions of owners and creditors toa business, sometimes a point of contention between the two parties. Creditors like

owners to participate to secure their margin of safety, while management enjoys the

greater opportunities for risk shifting and multiplying return on equity that debt offers.

Note: Although leverage can magnify earnings, it exaggerates losses.

Equity Ratio

Common Shareholders' Equity= Equity Ratio

Total Capital Employed

The ratio of common stockholders' equity (including earned surplus) to total capital of the

business shows how much of the total capitalization actually comes from the owners.

The study is made on the basis of secondary data. The annual by the firms were of greathelp collection the necessary information. In addition to this, the personal of “GENERALMILLS INDIA PVT LTD” were very co-operative in forwarding the necessaryinformation as and when required.

Tools for data collection

Data require for this project is mainly tow type’s i.e. primary data & secondary data and Ialso use the Graphs in analysis of ratio which help to understand to every one.

Primary Data: -

Those are collected fresh and the time and this happens to be original in character.The primary data were collected through personal ineraction with the manager andofficial of the frim.

Secondary Data: -

Secondary data means data is already available i.e. they refer the data which havealready been collected and analyzed by someone else, then he has to look into varioussources form whose he can obtain them, usually the publications technical trade

journal books, Magazines and Net and Reports of company etc.

• SOURCES OF COLLECTION OF DATA:-

1. Staff of the GENERAL MILLS INDIA PVT LTD

2. Magazines and Net

3. Journal Books of GENERAL MILLS INDIA PVT LTD

4. Annual General Report of 2002-03, 2003-04, 2005-06 and 2006-07

Loss for the year before one off items 331,666,031 236,026,814

Goodwill written off 6a 151,512,500

Settlement of dispute 18 16,014,908

Net loss for the year 331,666,031 403,554,222 195,729,145 225,407,658

Balance in profit & loss A/c brought forward 1,082,729,953 1,414,395,984 165,690,233 363,880,780

Add: Non compete fees written off 6b 137,050,000

Less: Provision for fringe benefit tax 2,461,402 5,887,310

Net loss for the year after taxation 198,190,547 231,294,968Balance in profit & loss A/c carriedforward 1,414,395,984 1,955,000,206 363,880,780 595,175,748

• Current Ratio = Current Assets, Loans & Advances / CurrentLiabilities & Provision

Particulars 2007 2006 2004 2003

Current Assets 1,324,070,612 397,044,641 389,682,651 250,963,563

Current Liabilities 754,597,707 260,502,889 404,911,677 564,228,419

Current Ratio 1.75 1.52 0.96 0.44

00.20.40.60.8

11.21.41.61.8

RATIO

2007 2006 2004 2003

YEAR

Cureent Ratio

Cureent Ratio

• Interpretation:

As a conventional rule, a current ratio of 2:1 or even 1.5:1 is considered satisfactory. Thesolvency ratio indicates ability of a concern to meet its total liabilities out of its totalassets. In the 2007 the position is good i.e. 1.75, in the year 2006, 2004 and 2003 the ratioare 1.52, 0.96 and 0.44 respectively.

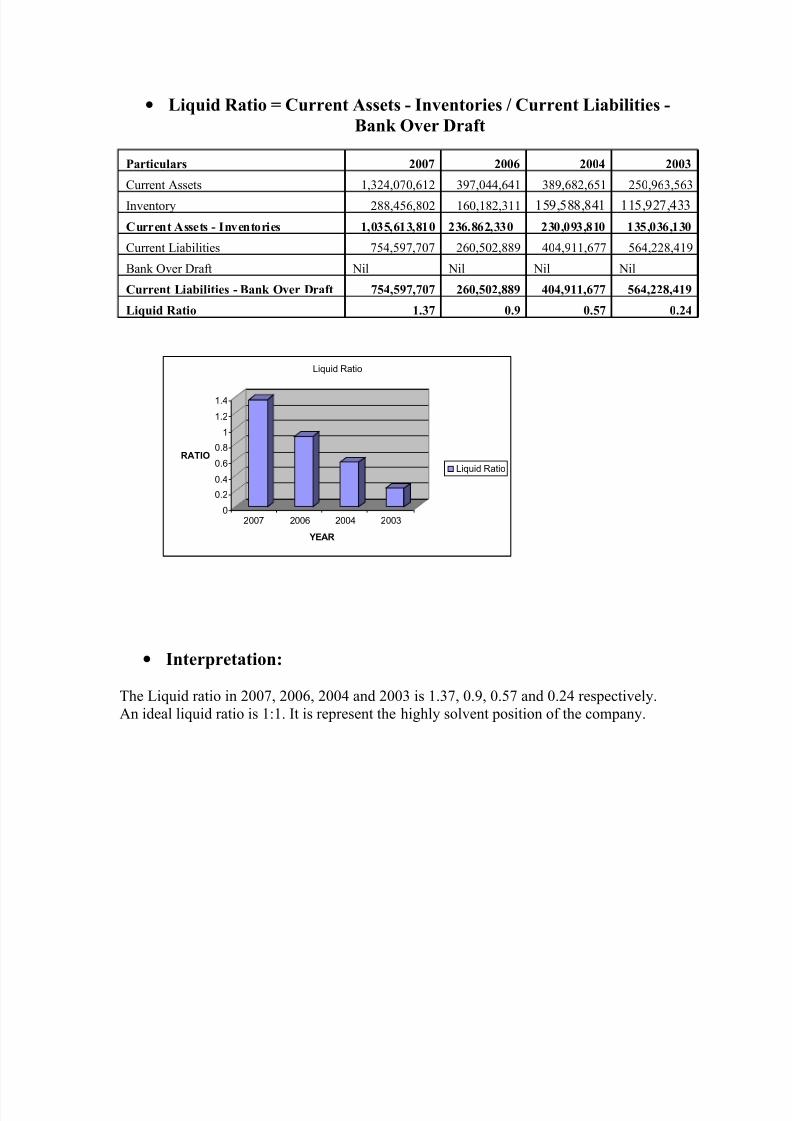

Current Assets - Inventories 1,035,613,810 236.862,330 230,093,810 135,036,130

Current Liabilities 754,597,707 260,502,889 404,911,677 564,228,419

Bank Over Draft Nil Nil Nil Nil

Current Liabilities - Bank Over Draft 754,597,707 260,502,889 404,911,677 564,228,419

Liquid Ratio 1.37 0.9 0.57 0.24

0

0.2

0.4

0.6

0.8

1

1.2

1.4

RATIO

2007 2006 2004 2003

YEAR

Liquid Ratio

Liquid Ratio

• Interpretation:

The Liquid ratio in 2007, 2006, 2004 and 2003 is 1.37, 0.9, 0.57 and 0.24 respectively.An ideal liquid ratio is 1:1. It is represent the highly solvent position of the company.

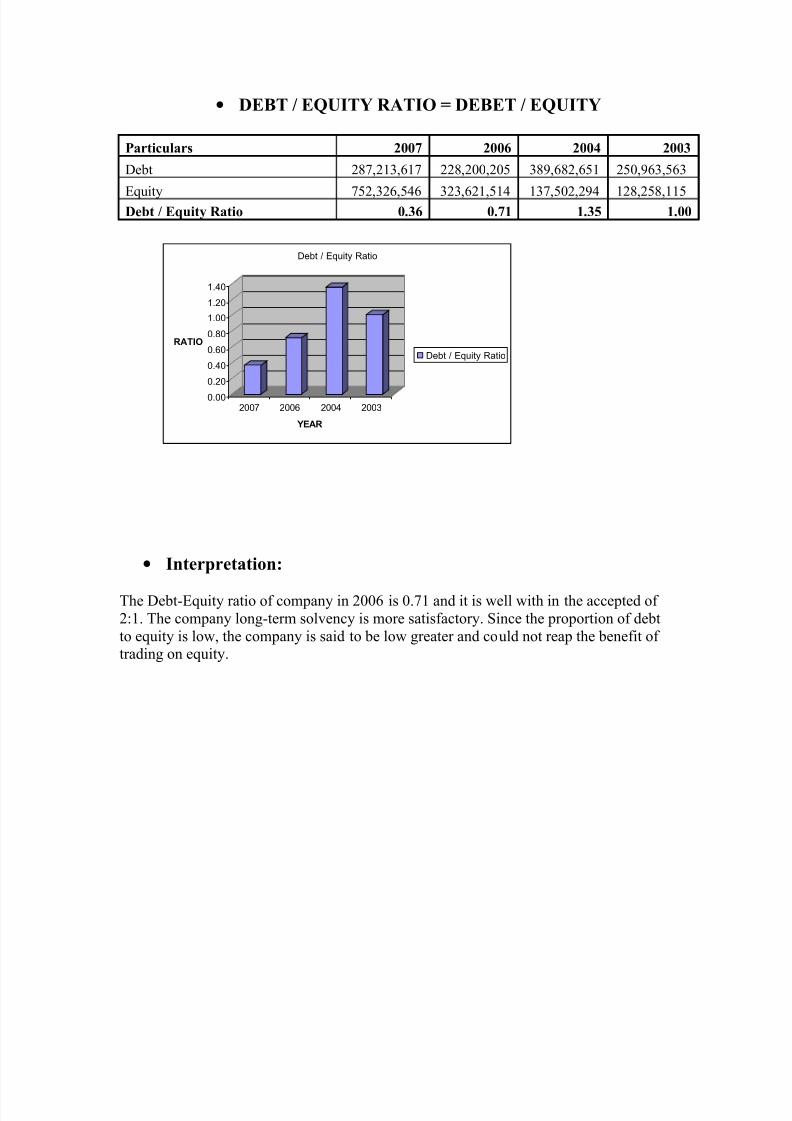

The Debt-Equity ratio of company in 2006 is 0.71 and it is well with in the accepted of 2:1. The company long-term solvency is more satisfactory. Since the proportion of debtto equity is low, the company is said to be low greater and could not reap the benefit of trading on equity.

• Inventory Turnover Ratio = Cost of Goods Sold / AverageInventory

Particulars 2007 2006 2004 2003Cost of Goods Sold 1,076,253,832 756,065,488 569,265,804 466,637,879Average Inventory 175,501,199 142,956,404 116,531,601 71,411,326Inventory Turnover Ratio 6.13 5.29 4.89 6.53

0

1

2

3

4

5

6

7

RATIO

2007 2006 2004 2003

YEAR

Inventory Turnover Rat io

Inventory Turnover Rat io

• Interpretation:

The company is having low inventory turnover ratio, and the company’s working capitalmight be tied up in financing inventory. The Inventory Turnover ratio in 2007 and 2006is 6.13 and 5.29 respectively.

Inventory ratio in the 2007, 2006, 2004 and 2003 is 21.79%, 40.34%, 39.41% and46.19%. There is clear indication that 40% of current assets are locked up in the forminventory.

Cost of Goods Sold 1,600,841,511 1,158,793,028 941,448,759 749,643,176Gross Profit Ratio 32.78 34.75 39.53 37.75

05

1015

2025303540

RATIO

2007 2006 2004 2003

YEAR

Gross Profit Ratio

Gross Profit Ratio

• Interpretation:

The ratio measures the gross profit margin on the total net sales made by the company. In2007, 2006, 2004 and 2003 the gross profit ratio is 32.78%, 34.75%, 39.53% and 37.75respectively.

• Operating Ratio = Cost of Goods Sold + Operating Expenses /Sales * 100

Particulars 2007 2006 2004 2003Cost of Goods Sold 1,076,253,832 756,065,488 569,265,804 466,637,879Operating Expenses 574,896,657 451,363,513 456,543,879 465,529,996Sales 1,600,841,511 1,158,793,028 941,448,759 749,643,176Operating Ratio 103.14 104.2 108.96 124.34

0

20

40

60

80

100120

140

RATIO

2007 2006 2004 2003

YEAR

Operating Ratio

Operating Ratio

• Interpretation:

The Operating ratio is very high. This is not good for company. The operating ratio in2007, 2006, 2004 and 2003 is 103.14, 104.2, 108.96 and 124.34 repectively.

Number of factors should be taken into consideration before reaching a conclusion aboutshort-term and long-term financial position and performance of the concern.

Some of the factors are

Type of business carried on.Type of product manufacture.Reputation of the concern.Type of assets available to invest.Type of funds brought in for working.

The company is integrated specialized manufacturing food production. For systematiclong rang planning will serve vital and dynamic document, which will guide GeneralMills India Pvt Ltd. In the years to make a profit, and further to improve the service to thespecialized food products as well as customers, the food production will be exported tosome of the most discerning markets of the world.

General Mills India Pvt Ltd faces its future nit with apprehension but with full confidenceand in process serve, its owner, the government, its customer, its employees and itssuppliers by effectively fulfilling the role that has been assigned to it.

Following are the limitions which were faced on the project.

Limitation of primary data

Managers executive of a company are not ready to share confidential information aboutcertain financial issue. Official are bound by some rules and regulation of company sothey are not able.

Confidential financial information cannot be disclosedOfficial of a company cannot be disclosed confidential financial information.

Other

The study is limited to “GENERAL MILLS PVT LTD” and the findings need notapply in a similar sense to other similar firms.

The data available are based on annul reports.

The time was very limited and hence one could not probe as deep into the problem as one would have linked to.

The objective was to collect as much as possible having no access to other recordsof the company except the published statements, the interpretation of the resultsmight not be perfect and accurate.

The company should maintain the current ratio for the years by proper maintaining current assets and current liabilities.

The company should properly utilize its liquid assets by employing it in better technologies. Which may increase the efficiency and quality of the products?

The company should reduce cost of production and also operating cost, whichmay ultimately increase the profits of the company.

The company should improve our competitiveness through improved materialutilization and reduced process cost.

The company should increase there efficiencies of net working capital and tomaintain adequate level of working capital.