76

In the Middle East since Deloitte GCC Powers of Construction 2014 Are you ready for the recovery?

| Date post: | 28-Mar-2018 |

| Category: |

Documents |

| Upload: | vuongkhanh |

| View: | 217 times |

| Download: | 2 times |

In the MiddleEast since

Deloitte GCC Powers of Construction 2014Are you ready for therecovery?

2 | Deloitte GCC powers of construction 2012 | Five lessons to learn from

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 3

ContentsForeword

4

Interviews (Roots Group, Arabtec, Msheireb Properties, Qatar Rail)

Combatting fraud in theconstruction sector

34SMARTer constructionHow the GCC’s mega-projects needto learn post-2008

40

Is your schedule right?

50

Project controlsThe heart of the successful deliveryof any capital project

60

How do you keep track of theassets you built once operational?A question of value

68

Infrastructure and socialinfrastructure spend and thechallenges around these projects

30

Plan, plan and plan againAre you a market leader or follower?

46

What does good look like ineffective project delivery?

56

Capital offenceThe need for discipline in Middle

Eastern energy and resources projects

64

4 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

If we consider the fundamentals of the constructionindustry, it is certainly easy to conclude that there is a lot of positive sentiment and more recently positivedevelopments in awarding some mega and socialinfrastructure projects across key markets. Governments’spending is creating a positive comeback forconstruction, but as we all know this is dependent on oil revenues which need to be maintained above a break-even margin to allow the spending to continue.The mass social infrastructure spends are a main priorityfor most governments as a measure to curb anypotential negative government sentiment and instabilitywhich could have occurred as a knock-on effect of thesurrounding turmoil the wider region has encounteredover the past couple of years.

While oil prices provide healthy margins, strongpopulation growth continues, and many major eventsdraw nearer and long-term plans for developmentstrategies to take shape, we will see the constructionindustry confident of growth for the foreseeable future.The GCC construction industry is now valued at overUS$1.3T, with US$935B in execution including long-termmegaprojects, US$81B out to tender, US$211B in designphases and US$136B under study according to MEED.These are levels which are getting close to the pre-globalrecession years. The construction industry thereforeseems to be out of the recession and into recoverymode. The big question is: “Are you ready for theconstruction recovery?”

Looking backOver the last year the optimism within the GCCconstruction market has risen considerably and rightly so.The GCC saw US$70B worth of construction projectscompleted in 2013 with this number predicted to rise toUS$83.5B in the current year according to Ventures ME.Residential developments accounted for just over 43% oftotal completed projects, which is expected due to theregion’s rapid population growth and thus thegovernments’ increased social infrastructure spends. TheUAE and the KSA ranked in the top two positions for allsectors apart from education and healthcare whereQatar held the top spot in both.

During 2013, Dubai saw over 500 building projectslaunched, which is a massive number for one city alone.This number also does not take into account Expo 2020which was only announced in late November 2013.Since the celebrations of Dubai winning Expo 2020, wehave seen renewed confidence in the already improvingconstruction industry. In a market that relies uponconfidence and optimism, this is the much neededstimulus to create momentum for a renewed“development and economic cycle.” The largest everExpo site is set to be built in the Jebel Ali (DWC) area at a total cost of between US$2B to US$4B. The secondaryinfrastructure spend will be upwards of US$8B, and willinclude construction opportunities in the transport,hospitality, retail and commercial sectors.

Dubai’s Roads and Transport Authority (RTA) hasannounced that it will fast-track a US$1.36B expansionof the Dubai Metro’s Red Line to connect to the DubaiWorld Central. Emaar Properties announced that it hassigned a memorandum of understanding with DubaiWorld Central to develop a massive (13.63 million sqm)golf centered residential estate adjacent to the areasurrounding the Expo 2020 site. These are the first ofmany announcements regarding large-scale projectsbeing planned in the wake of the Expo win. Tourism andHospitality have been the key focus for the legacy afterExpo, as we see Emirates Airlines grow from strength tostrength and more GCC residents continue to invest inthe UAE as a safe haven.

With all this extra infrastructure spend, jobs will begenerated with some estimates claiming 30% of thepotential 300,000 jobs created by Expo 2020 is expectedto be in the construction sector alone. The governmenthas also announced that all new and existingconstruction projects are going to be fast-tracked to beready for 2020. The demand for skills and resources willof course increase and we would hope that a well-planned and phased development strategy will preventthe price for these resources and for talent frombecoming disproportionately expensive.

Meanwhile in Saudi Arabia 2013, yielded the largest evervalue of construction contracts awarded during a

ForewordReview and outlook

Cynthia CorbyPartnerConstruction Industry LeaderDeloitte Middle East

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 5

calendar year. This was largely due to the US$22.5Bawarded in three separate contracts on the Riyadh MetroProject. Because of this, transportation accounted for thelargest proportion of contracts awarded in terms of valuewith power coming in a distant second. This clearlyshows that the Saudi government still considers capitalexpenditure to be a major priority.

Looking forwardLooking to 2014 and further ahead it seems likegovernment-led initiatives will continue to drive growthin the GCC construction sector as regional governmentscontinue to focus on social infrastructure projects. Therail industry alone in the GCC could create 50,000 jobswith most nations creating or upgrading their railnetworks. These consist of the multi-nationinterconnected railway network along with metro andtram projects of which there are many, including theRiyadh Metro project, Etihad Rail, Qatar Rail and theupgrades to the Dubai metro.

According to a survey performed by Pinsent Masons,90% of companies perceived greater optimism in themarket in 2013, with 77% reporting a healthier orderbook for the next 12 months relative to the previous yearand 40% expecting their order books to increase by over10%. This emphasizes the optimism currently in themarket, but with mass optimism there needs to becaution, as we have all learnt from the past.

UAEThe UAE is seeing renewed development, with the pick-up in the Dubai real estate and tourism markets set to bereinforced by Dubai winning the right to host Expo 2020.Figures from the Department of Economic Developmentreveal the GDP of Dubai will grow 4.7% in 2014, withthe main drivers of the economy being tourism, trade,transportation and real estate. The UAE market is ontrack to reach the levels of investment last seen beforethe recession; it is also good to see that there areUS$12B of previously stalled projects within the countrywhich have now resumed construction. Looking forwardto Expo 2020 and the anticipated spend mentionedpreviously, the government has now installed a charge

which will be applicable to guests staying in all types ofholiday accommodation. The revenue received from this“tourism levy” will be used by the government to financeits significant capital expenditure.

Abu Dhabi is set to be transformed by US$100B worth of construction projects, which include housing,education, transport and other developments. As statedby Fahad Al Raqbani, director general of Abu DhabiCouncil for Economic Development, “These projects willemphasize the economic competitiveness of the Emirate,empower the role of the private sector and sustain thelocal economy’s growth in a manner that will lead toaccomplishing the objectives of the economic vision2030.”

The UAE is seeing reneweddevelopment, with the pick-up in theDubai real estate and tourism marketsset to be reinforced by Dubai winningthe right to host Expo 2020

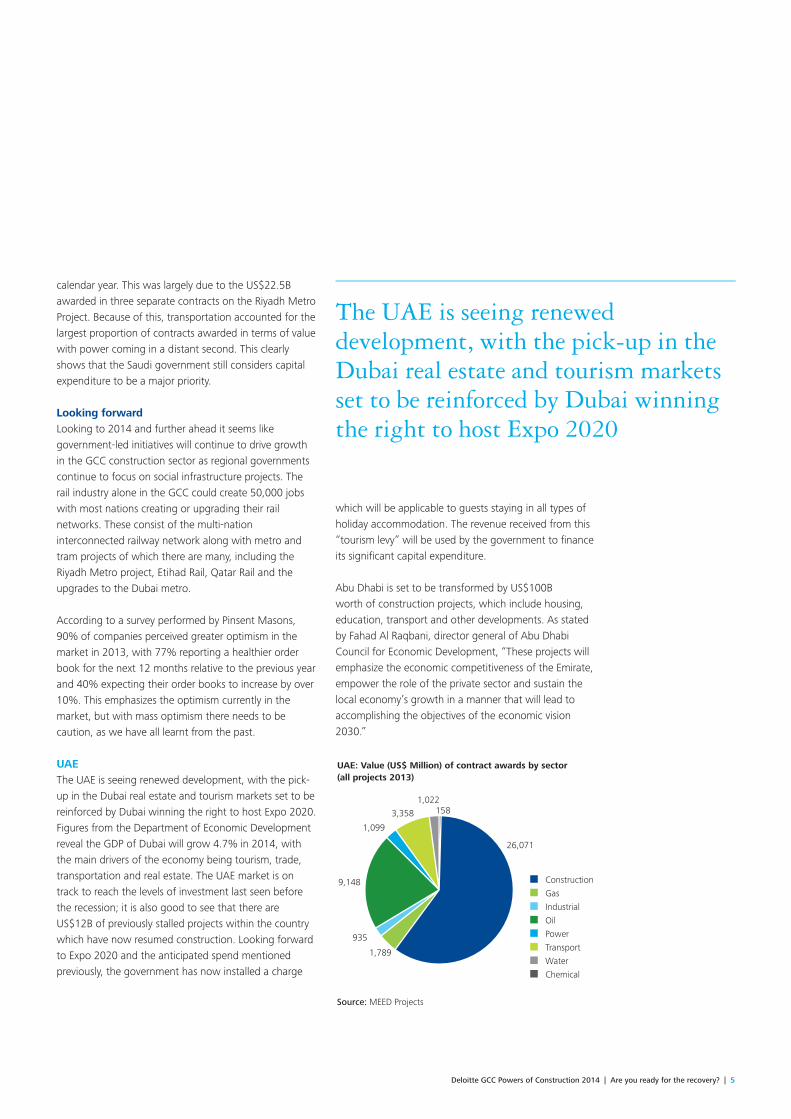

UAE: Value (US$ Million) of contract awards by sector (all projects 2013)

1581,022

3,358

1,099

9,148

935

1,789

26,071

Construction

Gas

Industrial

Oil

Power

Transport

Water

Chemical

Source: MEED Projects

6 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

According to Jones Lang LaSalle, around 22,000 newhomes were completed in Abu Dhabi in the last threemonths of 2013 with another 22,000 expected to behanded over this year. In the transport sector, US$2.9Bwill be invested in developing a 131km metro system inAbu Dhabi to accelerate the flow of traffic and keeppace with the growing population. The other big railproject is Etihad Rail, the US$10.8B scheme that will linkDubai, Abu Dhabi and the northern emirates, and theports of Khalifa and Jebel Ali. Etihad Rail will eventuallylink up with the planned 2,177km-long GCC railway.There will also be 246km of new major roads, includinga 62km highway connecting Dubai and Abu Dhabi,scheduled for completion in 2017.

There are, however, a few potential challenges for theconstruction industry within the UAE. These include the impact of the increased competition within themarketplace from international contractors trying to gettheir piece of the construction pie, and this could have anegative effect on the local contractor’s bottom line as itdoesn’t look like the pie is growing at the same rate asthe influx of added competition. Another risk is the lackof available skilled labor as Qatar, KSA and UAE competefor these resources – all potentially impacting profitabilityand potentially also quality due to the lack of resources.

KSAAccording to MEED Projects, KSA still leads the way inthe region with over US$1T of projects either planned orunderway. The residential sector accounts for just under30% of that market spend, while healthcare comes insecond at 20% and education at 10%. This again showsthat the social infrastructure spend by the Kingdom is a

main priority. A large proportion of the high-valueconstruction contracts awarded in the Kingdom in thelast three years have been in the transport sector,particularly aviation and rail. These include the KingAbdulaziz International Airport in Jeddah and the RiyadhMetro Project. The Kingdom is also set to award furthersubstantial contracts in the transport sector over the nextfive years, with project management contracts tenderedfor both the US$7B Saudi Landbridge rail project and theestimated US$10B expansion of Riyadh’s King KhalidInternational Airport.

The Kingdom also needs 2 million new homes by theend of 2014 to keep up with a population that’squadrupled over 40 years. In March 2011, King Abdullahbin Abdulaziz al-Saud pledged to invest US$70B inbuilding new homes for Saudi nationals. Last year, theKingdom’s Housing Ministry commissioned US$1.1B of housing projects in seven cities including Jeddah,Dammam and Tabuk as part of King Abdullah’s initiativeto construct 500,000 homes.

The biggest concern in KSA due to the massive scale ofconstruction is the reality of input cost inflation and thepossibility of project delays because of the lack ofavailability of resources including construction materialsand labor. Most of the region’s cement industries arealready operating at full capacity, with sizeable clinkerimports being seen in Saudi Arabia. Another labor issueis the implementation of the Saudization (Nitaqat)program, which we saw heavily enforced at the end oflast year and which could see up to 2 million* leave theKingdom. Unsurprisingly, this has had a disproportionateeffect on the construction industry, mainly because ofshortages of local unskilled labor and through higherinput costs.

QatarIn Qatar, the government is preparing to spend in excessof US$70B, mainly on infrastructure and transport butalso on hotels and stadia, in anticipation of the 2022FIFA World Cup and Qatar Vision 2030. The Minister ofFinance allocated US$24B to key projects, an increase of16% from 2013/14; this is also the biggest infrastructurebudget in the country’s history. The Finance Minister also

According to MEED Projects, KSAstill leads the way in the region withover US$1T of projects either plannedor underway

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 7

mentioned that he expects spending on projects to reachUS$182B over the next five years. BMI also has a positiveoutlook and expects the infrastructure sector in Qatar tocontinue to have double digit growth over the comingyear.

Qatar, in common with the other GCC powerhouses,continues to focus on improving its social infrastructure.Funds have also been set aside for completing theHamad International Airport, the New Doha Port Project,the rail and metro projects, and the roads program. Amajor part of the spending will be on the Qatar Railproject, which is expected to cost around US$45B tobuild.

Lusail City has started receiving its first residentsfollowing the completion of the bulk of its infrastructureand the town will be fully ready at the end of 2014according to Qatari Diar. When completed, it is designedto have over 200,000 people living within it and have avalue of around US$45B.

Again the major cause for concern is the risingconstruction costs, from materials to labor. The Qatarigovernment is aiming to keep these costs in check bytaking a hands-on approach. It is looking to regulatecommodities by creating a single buying source toimport into the country run by a government subsidiarywhich will then sell on to the contractors. Meanwhile,the government has attempted to increase the supply ofcertain commodities by raising production levels withinthe country again by creating government subsidiarieswhich own these commodities and can stockpile thembefore prices escalate.

Rest of the GCCWork is picking up in Kuwait and Bahrain, both of whichhave had their own problems over the last few years, butit is Oman that is the one to watch outside UAE, KSAand Qatar looking forward. Oman has budgeted forcontinued strong spending on its infrastructure andtourism sectors. The country announced US$15.5B ofspending on rail at the end of 2013 as well as theconstruction of a new town in Duqm.

Among the pan-GCC projects, the GCC rail network is byfar the largest project with a combined value close toUS$200B. Construction of the network, which will linkOman in the south to Kuwait in the north through theUAE, Qatar, Bahrain and Saudi Arabia, is scheduled to becompleted by 2018. Meanwhile, the contract for a newcauseway linking Saudi Arabia and Bahrain is scheduledto be completed in 2014. When completed, these shouldassist in regional and international trade, with the use ofa world-class logistics network connecting all GCCnations.

So make sure you are ready for the upturn and do notforget the lessons of the past – conduct feasibility studiesto support the business case for the spend, and controlthe costs through efficient and effective design to ensurethe assets that will be built to provide a sensible returnon investment for the end users. It is only in so doingthat we can create a sustainable market place withworld-class infrastructure and social infrastructure tosupport the local populations.

* http://www.theguardian.com/world/2013/nov/29/saudi-arabia-foreign-labour-crackdown-migrants

GCC: Value of projects 2014 to 2020 (all sectors)

Water

Industrial

Source: MEED Projects

Transport

Gas

Power

Construction

Oil

Chemical

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

0

Val

ue (U

S$ M

illio

n)

Bahrain Oman Kuwait Qatar SaudiArabia

UAE Dubai Abu Dhabi

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 9

Msheireb PropertiesinterviewDevelopingcommunities whichencourage socialinteraction, respect forculture and achievesustainable livingMsheireb Properties is a real estate company and asubsidiary of Qatar Foundation. The company wasestablished as a commercial venture to support theFoundation’s aims and the Qatar National Vision 2030that aims to develop Qatar into an advanced societycapable of sustaining its development and providing ahigh standard of living for all of its people. Its mission isto change the way people think about urban living andimprove their overall quality of life, through innovationsthat encourage social interaction, respect for culture,and greater care for the environment. MsheirebProperties spent three years researching Qatariarchitecture and numerous approaches to urbanplanning all over the world with the most respectedexperts in the industry – in order to realize anarchitectural language rooted in the best of the pastthat may be preserved for and by future generations.

10 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

The company is guided by the progressive vision of HerHighness Sheikha Moza bint Nasser. Her Highnessestablished the company with a mandate to address agap in the architectural history of Qatar and rediscover a unique form of Qatari urban development. MsheirebProperties aims to understand and implement how thebest of the past and modern, innovative technologiesand thinking can blend to create a new architecturallanguage in Qatar that is unique to the region.

The company’s name, Msheireb, means ‘a place to drinkwater’ (in Arabic) and is the historical name of thedowntown area of Doha.

We spoke with the Chief Executive Officer of MsheirebProperties, Eng. Abdulla Hassan Al–Mehshadi, whoshared his views on their vision, new projects and thefuture of development in Qatar.

Msheireb Downtown Doha is the flagship developmentof Msheireb Properties that aims to revive, regenerateand conserve the historical downtown of the Qataricapital, Doha. The US$5.5B project was launched in2010 in partnership with global industry leaders andexperts, to align the architectural learnings of the pastwith the latest in eco-friendly technologies that paystribute to Qatar’s tradition and embraces the future. Torealize a language that is relevant, enriching and trulyQatari.

Msheireb Downtown Doha (“MDD”) will be the first ofits kind complete smart city in the region, incorporatingstate-of-the-art technologies to create a better livingenvironment for all. It will feature extensive retail outletsincluding a mall, designed to transform the area into anunparalleled retail, leisure and entertainment hub. TheGalleria is a closed, air-conditioned shopping mall whichwill comprise approximately 100 stores set across fourlevels of shopping and entertainment space. Spanningapproximately 48,000 square meters of gross leasablespace, the Galleria forms a major part of the retailoffering at MDD. The Galleria will comprise an anchorsupermarket on the lower ground floor, a multi-retailspace and a six-screen cinema. The mall will also featurea dedicated entertainment zone for young audiences,involving both educational and physical activities wherechildren of all ages will be entertained in a safe andfriendly environment. MDD is set to create a locationwhere all sections of the population can enjoythemselves; the development features a variety of otherretail offerings which will not only attract visitors andtourists, but will also serve the thriving communitywhich will soon be living and working in MDD. Sikkat Al Wadi, the development’s largest pedestrian street,running the entire length of Downtown Doha will alsoprovide a wide range of shopping options, includingflagship stores in addition to fashion boutiques,restaurants, and cafes. With a special focus on features

“The Msheireb project creates a true tangible link between vernacular, tradition and thefuture of construction in the Region. The way in which Msheireb took on board theunderstanding of historical placement of buildings and façade designs to create passivecooled environments is a testament to the Qatari vision to deliver in excellence. The needsof a modern mixed use development often has no place for the culture of the past, butMsheireb has shown that the vernacular past of the likes of Souq Waqif can be translateddirectly into the modern context of a mixed use city and create a successful fusion betweenthe old and the new and set a precedence of sustainable excellence that has been seen as acatalyst for sincere design. It is truly a remarkable effort by Qatar and the Msheireb Team”

Nigel Eckersall

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 11

that add to the safety and convenience of all includingthe disabled, the project has been designed toaccommodate the entire community.

Unique to the Msheireb development is its blend ofcasual and high street shopping, stylish plazas andcommunity spaces. It will also host the region`s largestshaded open-air square, Al Baraha, a family destinationwith restaurants and cafes featuring events and largescale shows, with special cooling devices ‘cool pools’, to refresh visitors at the hottest times of the year.Pedestrian friendly access from the main streets of thecity and an underpass connection to Souk Waqif willfurther enhance the shopping experience making it afun and enjoyable trip for all.

Mr Al– Mehshadi confirmed that for Msheireb Propertiesthe key priority and the definitive target is to make surethat project phases One through Three are completedby 2016. Thirty percent of the project will be completeby the end of 2014. Discussing the usual challenges ofmanaging changes in a project this vast, we asked MrAl–Mehshadi how he has controlled the design changesand variations to the plans to ensure these do notdisrupt or delay the project significantly. He replied that their “focus was to ensure that the designs werecomplete and therefore any changes that occur are only those that are vital due to technological or criticalchanges required in the project and as such they haveminimized the changes which could disrupt the workplan and affect overall schedules.”

Complementing this array of exceptional retail offeringswill be the project’s efficiently planned infrastructureand transport system. Host to Qatar’s largest metrostation, Msheireb has an integrated road networkconnecting the Downtown area to the rest of the city.Retail will greatly benefit from parking provisions ofwhich there will be 11,000 spaces within three to fiveunderground basement levels, spanning the entire

length of the development, a first of its kind allowingthe public to move freely across this vast car park spacefrom one end of the development to the others. Tomaximize the use of space, MDD plans to install anumber of power stations underground and it recentlyenergized a 66KV power plant, which is another first forQatar. All utilities are completed as planned to date withthe District Cooling Plant commissioned as well.

The photovoltaic* solar system in MDD is an advancedPV system installed in buildings within phase 1A of theproject. The installation of the solar panels reflectsMsheireb Properties’ ongoing commitment tosustainable development in line with Qatar’s NationalVision for 2030. The roof-mounted photovoltaicmodules will supply a portion of the electricity needs of the buildings within Phase 1 of this landmarkdevelopment.

Adopting advanced clean technology such as solarenergy in addition to traditional methods of climatemanagement is a hallmark of the Msheireb projectwhich, on completion, will have one of the largestconcentrations of LEED-certified (US Green BuildingCouncil) buildings in the world. “When MDD iscomplete, the project will comprise 5,200 solar panelsacross a total of 8,400 square meters of onsite energyproduction in the form of both electricity and hot water.

Adopting advanced clean technologysuch as solar energy in addition totraditional methods of climatemanagement is a hallmark of theMsheireb project

*Photovoltaics (PV) is a method of generating electrical power by converting solar radiation into direct current electricity using semiconductorsthat exhibit the photovoltaic effect.

12 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

Each year, the solar PV system will reduce totalgreenhouse gas emissions by 568 metric tons which isequivalent to 241,000 liters of gasoline consumed”,commented Al–Mehshadi.

The six consortiums currently building MDD have beenspecifically chosen by Msheireb after a thoroughassessment of the contractors’ expertise, financialstability and technical capability, which was extensivelyinvestigated by Msheireb prior to finalizing the tenderprocess. An important aspect of each consortium’s bidwas an assessment of the consortium’s deepunderstanding of how to operate in Qatar, a criticalsuccess factor for the winning bids. Msheireb alsoinsisted on all consortiums being a combination of alocal Qatar contractor and an international contractor.This helped ensure that the consortium represented asymbiotic relationship where knowledge transfer is key,helping local contractors learn international processesand systems that will benefit the Qatari constructionindustry, while the international contractors learn thenuances of the construction sector within Qatar. “A newmeasure put in place by the Government of Qatar was arequirement for each entity in the consortium to sign a100% performance bond, not the usual performance

bond signed by all and shared as a joint liability – hereeach consortium partner takes a 100% performancebond risk for the total project value. This is a progressivestep in challenging the local contractors to ‘step up’ tothe same level as their international counterparts, with asignificant risk then acting as the incentive to ensurecooperation between the consortium parties to deliveron budget and on schedule. This was a strategic moveby the Government to offer international contractors acertain level of comfort and assurance in expecting thelocal contractors to be fully committed to the project,financially and otherwise.”

Looking at the medium-term horizon, Mr Al– Mehshadiconfirms that there will be an influx of internationalcontractors and consultants, and that the concerns over Qatar’s vast development requirements have beenmitigated by a significant investment in planning forQatar’s construction boom. Among the concerns is thelarge demand for labor, both skilled and unskilled, as the development in Qatar gains momentum andincreases in the lead-up to the FIFA World Cup 2022and Qatar Vision 2030. He says that the authorities areproactively exploring various options to be able to easethe requirements and restrictions around visas to helpaddress the potential lack of labor in the future. At thepeak of construction at MDD there will be 45,000construction workers on site.

A further concern was around the roads, ports andairports being ready and available to cope with therequirements that this vast construction phase willdemand. “There are regular meetings held between all these stakeholders to ensure that the port and thefirst phase of the airport will be ready when these initial projects will peak to cope with the sourcingrequirements and getting the required materials to the projects on time.”

Among the concerns is the largedemand for labor, both skilled andunskilled, as the development in Qatargains momentum and increases in thelead-up to the FIFA World Cup 2022and Qatar Vision 2030

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 13

As with every construction boom, the cost of materialsis a concern, specifically around the cost escalation ofthe primary commodities. As such the Qatar Governmenthas created two additional cement companies and alsoQatar Steel, which will create a single source fordistributors to buy from and hence control the cost ofthese primary commodities; in the long term, this will ensure that a viable ROI is generated on theseinvestments.

All these measures should give International playersconfidence to operate in Qatar and look at it as apromising and viable destination for conductingbusiness.

With Msheireb Downtown Doha, the company isdeveloping a blueprint for sustainable urbanregeneration, and believes in sharing the knowledge,experience and best practices to benefit the industry.MDD expects to fulfill its reputation to be a reliabledeveloper that delivers high quality, sustainable projectson time.

Abdulla Hassan Al-MehshadiChief Executive OfficerMsheireb Properties

Nigel EckersallSenior Design ManagerShapoorji Pallonji

Interviewed by:Cynthia CorbyPartnerConstruction Industry LeaderDeloitte Middle East

The Qatar Government has created twoadditional cement companies and alsoQatar Steel, which will create a singlesource for distributors to buy from andhence control the cost of these primarycommodities

Project factsheet

Project cost US$5.5B (QR 20B)

Land area 310,000 square metres (76 acres)

Project name Msheireb: means ‘a place to drink water’ in Arabic

Typology GFA (SqM) Percentage (%)

Commercial & governmental offices 280,000 36.8%

Retail 94,000 12.4%

Hotel 117,000 15.4%

Residential 222,000 29.2%

Community, cultural, school, mosques, museum

47,000 6.2%

Total 760,000 100.00%

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 15

Arabtec interviewA market overview:opportunities andchallengesArabtec Holding is the biggest listed constructioncontractor in the UAE which has just recorded a triple-digit growth rate (149%) in net income for 2013 and itsshares are at the highest level since August 2008. Wespeak to the Managing Director, Mr. Hassan Ismaik,about this rapidly expanding group, which hasundergone significant change since March 2013, aboutthe opportunities and challenges that lie ahead forArabtec and the construction industry.

The construction industry has seen a marked increase inlarge-scale projects in the GCC and wider Middle Eastregion recently. This can be attributed to a return ofconfidence following the economic downturn and anincrease in demand, particularly for residential andcommercial properties, mega infrastructure projects inroad, rail and aviation sectors, social infrastructure, and hydrocarbon infrastructure. There is increasedconfidence in the UAE economy, with the trade,logistics, tourism and retail sectors delivering increasedgrowth. This will be supported in the longer-term asDubai moves to deliver the Expo 2020 and as Abu Dhabi executes on its well-published multi-billion-dollarinvestment program to deliver the Abu Dhabi 2030 plan.

16 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

New Central Bank regulations, including the mortgagelimit of 85 percent of a first property’s value for UAEnationals and 75 percent for non-nationals, are part ofthe measures put in place by the UAE government toreduce the risk of a speculative bubble, giving long-termproperty investors and end-users greater comfort. Takingall this into account, it is evident that a number ofbusinesses have an optimistic view on the currentmarket backdrop which market participants view asexcellent prospects for growth, with continuedgovernment investment and commitment from theprivate sector.

With this positive outlook for the industry, ArabtecHoldings is diversifying its business through variouspartnerships and joint ventures in critical sectors in theindustry. The oil and gas sector will continue to growand we have made good progress on expanding intothis sector with acquisitions of subsidiaries such asTarget Engineering, which has extensive experience inthis area. We have also formed a joint venture withSamsung, enabling us to take on mega oil and gasprojects. This is part of our ongoing growth strategyinto other sectors, which includes infrastructure. Ourcredentials and capability in this regulated marketedhave been strengthened through the agreement tooperate a joint venture with GS Engineering andConstruction. This joint venture strengthens ourcapability in heavy infrastructure sectors, as well as oiland gas.

The Middle East construction market has a perception of being a difficult market to participate in, which isunjustly so. We have a longstanding track record in theregion, and our backlog has more than doubled in thelast 18 months. We understand what it takes tooperate in the region, and where we are looking tobuild other capabilities we partner with establishedglobal players to deliver complex projects to the highestpossible standard. The Middle East presents a wealth ofopportunities, particularly in light of the recent growthwitnessed in the GCC. This is why our growth strategycontinues to gain momentum in critical growth sectors,such as oil and gas and infrastructure.

In 2013, Arabtec set out its strategy for growth byexpanding its business in segments of the market thatcomplement its strong presence in the areas of high-risebuildings and airports. We are expanding our footprintin growth and complex higher-margin constructionsectors such as oil and gas, infrastructure and power. In order to achieve this, the group successfully raisedUS$650M through one of the Middle East’s largest everrights issues that was three times oversubscribed.Following on from the rights issue, two separate jointventure agreements were formed with SamsungEngineering and GS Engineering as mentioned above.These strategic joint ventures with Samsung and GSEngineering will enable us provide more high-quality,complex projects by enhancing our skills and expertise in all aspects of the construction process. We continuallylook for other potential joint venture partners to helpbuild our expertise in other areas.

The critical success factors for operating any jointventure in this region rely on Arabtec’s extensive localknowledge and firm links with stakeholders. The successof these joint ventures can also be measured by ourdiversification into new higher-margin sectors such as oiland gas, power, and infrastructure, increasing Arabtec’sskills and expertise whilst keeping our roots firmly inconstruction.

In order to strengthen its drive into new higher-marginsectors, Arabtec acquired the remaining stakes of twoother important subsidiaries, Target Engineering andEmirates Falcon Electromechanical Company (EFECO).

The critical success factors foroperating any joint venture in thisregion rely on Arabtec’s extensive local knowledge and firm links withstakeholders

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 17

Since the remaining stakes were acquired, bothcompanies have been awarded substantial contractsacross a number of projects. This demonstrates thevalue that Arabtec has been able to add since thetransactions.

Of course there are challenges that are unique to thisregion. The Middle East has many complex projects andthere is significant construction activity happeningacross the region. Scaling up the workforce to deliver on the project pipeline is one of the most interestingchallenges we have. Arabtec’s capabilities and know-how in delivering complex projects is proven and stemsfrom decades of experience and understanding – it ishow we transition this know-how to a larger work forceto deliver consistently on a much larger scale that willform a primary focus area for us.

To prepare for our growth we need talented people. Werecently announced that we will be hiring thousands ofpeople from across the UAE, GCC and MENA region.This drive will target particularly high caliber andambitious nationals who express a desire to contributeto their country’s growth and development by joiningArabtec. Arabtec Holding is fully focused on ensuring itmaintains a strong, enthusiastic workforce. As one ofthe higher payers in the construction industry in theUAE, Arabtec continues to ensure working conditionsare of the utmost high standard for its employees.Arabtec Holding’s growth and expansion relies onsourcing and retaining a world-class workforce. Arabtechas recently established a new HR division specificallyfor laborers. In addition, it has implemented newmeasures in order to raise the working and livingconditions for laborers.

Arabtec is very keen to increase its internationalpresence. The company has well-established operationsacross the GCC region and now operates further afieldin Egypt, Jordan, Kazakhstan, Syria, Saudi Arabia,Palestine and Russia. We are engaged in newopportunities in markets that include Iraq, Algeria andthe Balkans. We have announced our intention to open a regional headquarters in Belgrade, capital of Serbia, to drive Arabtec’s expansion into the Balkan region. Weexpect our regional headquarters will be operational in

Q2 2014, and will serve as a launch pad for Arabtec’splanned expansion in the wider Balkan region. Arabtecis already in advanced discussions with developersregarding projects in the Balkan region where there aresignificant opportunities for the group that are fully-aligned to our growth strategy.

Additionally, we are in the process of opening an office in the Iraqi capital, Baghdad, to capitalize on thecountry’s high potential, particularly in oil and gas andinfrastructure. The office will serve as a platform forexpansion by Arabtec Holding’s joint ventures andsubsidiaries, in what is expected to become the region’smost lucrative construction market. Arabtec is already inadvanced discussions with a number of clients in Iraq forlarge-scale projects in its target sectors. A major drivebehind Arabtec Construction’s expansion into Iraq is topave the way for our newly formed joint venture withSamsung Engineering and the soon to be completedjoint venture with GS Engineering and Construction totap the huge potential the Iraqi market presents in EPCand infrastructure sectors.

Arabtec is well placed to deliver on its internationalexpansion and will only undertake projects that arecommercially profitable and align with our growthstrategy. We are a strategic company and undertakeprojects when we know we have sufficient capital andconfirmation of funding from investors, as well as theability to recruit the necessary staff with the requisiteskills to deliver the project.

The GCC’s infrastructure sector is one of the key driversof long-term economic growth in the region. Over the

As one of the higher payers in theconstruction industry in the UAE,Arabtec continues to ensure workingconditions are of the utmost highstandard for its employees

18 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

next six years, over US$600B of investment is planned in infrastructure projects in the GCC, of which overUS$220B will be in rail infrastructure projects. Socialinfrastructure, such as hospitals and education facilities,as well as physical infrastructure such as airports, arevital for GCC countries to develop. Arabtec hasparticipated in this type of social infrastructure, such as the joint venture with Greece’s Terna S.A, to build the Aldara Hospital and Medical Center, a 105-bedhospital in the Saudi Arabian capital, Riyadh.

In addition Arabtec recently announced a joint venturethrough its subsidiary, EFECO, to carry out mechanical,electrical, and plumbing work at the new Abu DhabiInternational Airport Midfield Terminal Building (MTB).

Government investment is an indicator that the UAEcontinues to offer excellent prospects for growth. TheGovernment of Abu Dhabi announced in 2013 that ithas earmarked US$129B for infrastructure developmentbetween now and 2030 with US$8.1B ring-fenced fordevelopment for Expo 2020. Furthermore, DeutscheBank estimates that the addition of private sectorprojects could see as much as US$43B being spent in preparation for Expo 2020.

In Abu Dhabi, for example, tourism, infrastructure andreal estate will have the largest areas of growth. Arabteclooks forward to participating in development andconstruction for all these sectors.

We recently announced our largest ever contract interms of value and the largest in the real estate sector in the region for 36 mixed-use and residential towers forAabar Investments in Abu Dhabi and Dubai. Althoughthis is our largest project, we approach all our projects in the same way - with clearly defined deliverables andoutcome; this is essential in order for us to recruit theresources we need and maintain our reputation offinishing complex projects on time and in the most costeffective way. The project includes eight mixed-usetowers in the Tomouh City of Lights development in Abu Dhabi, with a total plot area of 900,000 sq.ft and abuilt area of 14,000,000 sq.ft. In addition, Arabtec willconstruct four mixed-use towers in the Reem Islanddevelopment.

We have reorganized our business extensively over the past 12 months to ensure that we are adequatelyprepared to scale up our business and take advantage of the many opportunities in the boom of the next fiveyears. Arabtec Holding is well positioned to deliver onthe various development and construction projects it has been awarded across all of its subsidiaries. Weunderwent a re-organization of our core businessactivities in 2013, which has meant we now havestronger governance and significantly enhanced systemsand processes. This has led to a number of strategicdecisions being taken, as well as building on ArabtecHolding’s existing reputation of delivering to a highstandard, and enhancing its skills and expertise throughnew partnerships. We see the vast amount of projectscoming on-line as a positive move and look forward tobeing a part of the delivery of these projects.

Over the years, Arabtec has proven its leading positionthrough a significant track record of delivering complexand challenging technical projects such as the BurjKhalifa and others. We are confident that our trackrecord in the Middle East and a well-thought outstrategy and good governance will help us deliver onour large backlog and on our growth strategy.

Hasan Abdullah IsmaikChief Executive OfficerArabtec Holding

Interviewed by:Cynthia CorbyPartnerConstruction Industry LeaderDeloitte Middle East

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 19

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 21

Roots Group interviewA view of the Saudiconstruction sectorfrom the materialsupply sideOusama Fansa, the CEO of the Roots Group, one of the region’s leading building materials suppliers, hasconfidence in the Kingdom of Saudi Arabia and theenduring strength of the construction sector there:“When I first arrived here 28 years ago I was told itwouldn’t last and I’ve been hearing the same every year since. Yes there are challenges and risks and thelandscape will continue to change, but what has been done here, particularly over the last five years, isimpressive and should give us confidence. I’ve beenwaiting 28 years for the end of the sector and I think Ihave a few more to wait yet.”

Like many forward-looking organizations in the sector,the Roots Group does not see the relative dominance ofgovernment in the construction sector as a never-endingsource of opportunity. “We’re not facing dropping off acliff here: the underlying demand for infrastructure andother investment is too great. We are expecting,however, a tapering off of the major programs in themedium term. Our role as leaders in the constructionsector and as key participants in the Kingdom’seconomy is to ensure that our own organizations aregeared up to reflect this. We have to be ready toreposition ourselves for the different demands of adifferent primary customer base.” Ousama is a strongadvocate for the local skills and expertise that he sees

22 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

evident in the Kingdom’s building materials supplyindustry. Outside of labor-intensive items such as carpetsand furniture, his goal for his Saudi manufacturingoperations is not to compete with Egyptian-sourcedmaterials, where price becomes the predominantconsideration. His own organization already exportssignificant amounts of material throughout the region,including North Africa. This reflects in part the growingappreciation of quality in procurement and specificationdecision-making – a theme he comes back to often.When pushed on what government could do tofacilitate the development of this sector, Ousama seesremoving the regulatory blockers and considering thefinancial incentives such as the FTZs used in the UAE aspotentially more impactful than the major permanentway freight lines, into which the Kingdom is investing.

Ousama retains confidence in the fundamentalrobustness of the Saudi market. He notes that theheadlines created by Expo 2020 and the soccer WorldCup coming to the region create an immediate focus on a deadline driven by events, albeit it with strongattention on the legacy investments this creates forthese countries. In contrast Saudi continues to focus onits longer-term plans to develop the country and theeconomic and social infrastructure required to meet theessentially demographic and resident-expectation drivendemands in the Kingdom.

Ousama is quick to note that the Saudi constructionindustry is far from without its challenges. Lack ofpredictability in project initiation and delays in paymentare well rehearsed themes in the Kingdom. Interestingly,Ousama’s view is that government clients probably getmore bad press in this regard than they deserve. Henotes that delays in payments in particular, notinfrequently between six and nine months, are often as a result of blockages that reside with the contractorsas opposed to the government. Those delays that are attributable to the client are often the result ofinexperienced staff or consultants not able or empoweredto approve work or procurements as they are bound byspecifications or procedures they are not able to adapt.

While Ousama embraces the employment of localnationals under the Saudization drive, he notes that for the sector this, and the associated cornerstones of government policy such as limiting visa availability,presents real challenges. The Roots Group as anorganization has been able to achieve 17% Saudizationof its staff in the Kingdom so far. Ousama notes,however, that he has been able to move this forwardprincipally in back-office functions. Here he has built astrong and highly regarded team of Saudi women to beresponsible for many functions including design. Forfront-line technical staff, in his own words, they havefurther to go with bringing Saudis into the workplace –a problem caused principally by the lack of appropriatelyskilled Saudi engineers, trade and technical people. Forconstruction firms, these roles are the core of the business and their impact includes wage inflation andskills shortages, putting at risk cost, quality and programcertainty. Ousama notes that these constraints come ata time when the sector is being asked to respond toprojects of a scale 10 or 20 times those they faced adecade ago. This creates, in his view, a fundamentalincompatibility between what the sector is being askedto deliver and a central, and to date relatively inflexible,national policy.

In contrast Saudi continues to focus onits longer-term plans to develop thecountry and the economic and socialinfrastructure required to meet theessentially demographic and resident-expectation driven demands in theKingdom

On the relative dominance in the market for majorprojects of the limited number of local contractors,Ousama notes that this in part reflects the commitmentand investment that these firms have made in theKingdom. This is both financial investment but also therole that they play directly in local materials andemployment markets. “Each of these firms is entwinedwithin Saudi Arabian society at multiple levels, fromcommunity up to national government – it is onlynatural that this is going to give them a presence andopportunities above other firms, top flight internationalorganizations or otherwise, who can view theirengagement in the Kingdom on a largely project byproject basis.” Ousama does bemoan the loss of manyof the high quality small to medium size contractors inSaudi. For many of these organizations the increasingcosts and complexity of business brought by regulationand greater requirements such as bonding (which hasboth a direct cost and lock-up facilities) has madeinvolvement in the sector untenable.

On issues such as sustainability Ousama is generallypositive. While holistic LEED-type standards andmentality regarding design and construction are not yetthe norm, there is increasing awareness of sustainabilitystandards in specifying materials. Similarly whilehistorically any analytical consideration of whole lifecosts and long-term facility performance were verymuch secondary to the imperative to build, there isgrowing recognition of the criticality of this in thedesign and specification phases. This reflects an overalltrend that Ousama identifies in government contracting.Over the last five years there has been a consistentraising of the standards of many Saudi governmentclients. Organizations such as the Ministry of theInterior, Aramco, and the National Guard amongst manyare backing up progressive visions for their constructionprograms with strong in-house or embeddedengineering skills. This is being reflected in a progressiveincrease in the quality of work and materials specifiedand the rigor through which delivery is assessed. Inmany cases Ousama considers the standards as thehighest within the region. While there are still clearly

some variations in the standards achieved betweenclients, the overall trend is positive. Furthermore,Ousama sees the bar-raising effected by governmentclients as being reflected more widely now in the privatesector. As yet integrated supply chain management andthe specification of optimal materials based a structuredand holistic assessment are not the norm. They are,however, becoming more evident and as theconstruction sector begins to position itself for the post-government funding boom, Ousama Fansa is not alonein retaining cautious optimism.

Ousama FansaChief Executive OfficerRoots Group

Interviewed by:David BrazierDirectorInfrastructure & Capital ProjectsDeloitte CorporateFinance limited

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 23

The increasing costs and complexity ofbusiness brought by regulation andgreater requirements such as bondinghas made involvement in the sectoruntenable

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 25

Qatar Rail interviewTransforming Qatar’spublic transportationsystem to world-classlevelsQatar Railways Company (Qatar Rail) was established in2011 to design and implement an integrated world-classrailway system in the state of Qatar. Qatar Rail will bethe owner and manager of Qatar’s rail network and will be responsible for the design, construction,commissioning, operation and maintenance of theentire rail network and systems. Qatar Rail will consist of Metro, Long Distance and Light Rail Transit. We hearfrom Mr. Saad Ahmed Al Muhannadi, the ChiefExecutive Officer, who gives his insights and thoughtson the future of the transport sector within Qatar.

Qatar Rail was established to design, implement,operate and oversee the construction of a world-class,environment-friendly, technologically advanced andintegrated railway network in Qatar - making the latteramong the biggest railway projects in the world. Qatar’sintegrated railway network developmental programencompasses three vital projects: the Doha Metro, theLong Distance Passenger and Freight Rail, and the LightRail Transit project in the city of Lusail.

26 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

The Qatar National Vision aims to transform Qatar intoan advanced country by 2030, capable of sustaining itsown development and providing for a high standard ofliving for all its people for generations to come. Theplanned railway systems will support this vision. QatarRail will develop a world-class, efficient publictransportation system which will provide an attractiveand competitive alternative to private transport, capableof achieving a significant share.

Over the medium term the significant public investmentprogram should continue to drive growth. Theseinvestments are mainly related to the pioneeringinfrastructure projects to support the FIFA World Cup2022, the new sea port, the mega airport and the state-of-the-art railway network. There is also a keen focus onthe tourism industry. These investment projects willboost the non-hydrocarbon sector growth and facilitateeconomic diversification. The biggest challenge willsimply be the on-time delivery and completion of thesemajor projects we are undertaking. They require the set-up of huge infrastructure and the deployment ofadvanced technologies.

The Doha Metro network consists of four lines (Red,Gold, Green and Blue), extending to 354 kilometersacross the Greater Doha area, connecting the City’s two central points with larger commercial, residentialand dynamic areas in Downtown Doha, and operatingunderground in busy areas, and on and above theground levels in the suburbs. Moreover, the metronetwork will cover over 90 stations, serve Qatar’s twomillion people, most of whom are residing in Doha andsurrounding areas. The Doha Metro project will beconducted over two stages: the first, scheduled to becompleted in 2019, entails the set-up of 37 stationscovering 84 kilometers in total length. The project’ssecond phase, extending to 152 kilometers in totallength, and encompassing nearly 56 stations, will bedelivered by 2026.

Qatar Rail’s integrated railway network projectconstitutes not only one of the largest such initiatives inthe region, but more importantly, one that will work onconnecting the GCC’s railway infrastructures together,allowing for seamless and developed transport solutionsfor GCC residents commuting from one membercountry to the other.

Qatar’s railway network project will see a US$35Binvestment that includes plans to extend Qatar’srailways by 325 kilometers, and its rail networks tothose of other GCC countries. The investment fallsunder a wider vision of creating a united and integratedeconomic regional trade market through projects thatwill connect GCC countries via land and railwaytransport. The railway network project connecting GCCcountries will be equipped with the most advancedsystems, and extended to around 2,000 kilometers.

Qatar’s railway network project will seea US$35B investment that includesplans to extend Qatar’s railways by 325kilometers, and its rail networks tothose of other GCC countries

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 27

In this regard, Qatar Rail’s Long Distance Passenger and Freight Rail Project will consist of three differentcategories: a shuttle service for GCC transit passengersand travelers, transportation services for locals, andfreight transport services for international and domesticroutes.

Meanwhile, the Light Rail Transit project in the city ofLusail, which has already reached advanced stages, iscomposed of four lines extending to 30.5 kilometers intotal, a fleet of 34 trains, and 37 stations; more than 50 % of the structure, which is slated to be officiallydelivered by 2017, has been set up.

We are advancing at great speed with our projects, andwith the support of the groundbreaking technologieswe are employing, and the worldwide strategicpartnerships we have secured, we expect to rise to the challenge of delivering the projects as planned and scheduled.

An example of some of the partnerships Qatar Rail hascreated is in the opportunity to create the requisitetunnel boring machines required for the projects and weare very focused on continuing this trend. To achievethis we recently paid a visit to German manufacturer ofTunnel Boring Machines (TBM) HERRENKNECHT’s factoryheadquarters in Germany to learn about Lebretha, thefirst TBM manufactured for the Doha Metro project and slated to be delivered to Qatar in May 2014.HERRENKNECHT finalized the manufacturing of theLebretha TBM three weeks ahead of schedule. The 15TBMs that will be received by Qatar and deployed intothe Doha Metro projects rank among the best in theworld, having been tailor-designed for the State ofQatar’s geographic characteristics, nature, and areas.

We expect the next 12 months to bring about similarmilestones for our projects, and hopefully, similardeliveries that will be made ahead of schedule.

The priority is to successfully award the remainingdesign and build contracts in a timely manner and thento ensure that all contracts are managed as planned.This will be achieved through a well-structured bidderevaluation process and putting in place the prudentcontrols and management systems that will ensure thatall projects are performing as per plan. Managing theconstruction progress to ensure we deliver on time isparamount, which is why all our contracts are designand build to avoid any issues with incomplete designs at the time of construction.

Qatar Rail’s bidder selection is based on a combinationof technical and commercial criteria. A determination ismade that the technical solution proposed by a bidder is feasible, deliverable and robust, that it is based onreliable technologies, meets all minimum technicalrequirements set and that the costs and financialstructure are consistent with the technical solution. It isalso important to confirm that the bidding consortiummust come across as a cohesive entity rather than just acollection of companies put together purely for biddingpurposes.

Qatar Rail’s projects are aligned to the state’s NationalVision 2030, reflecting Qatar’s growing interest in majorinfrastructure projects; the integrated railway networkproject falls under the developmental and growth plansQatar is undertaking across various fields, including the

The 15 TBMs that will be received byQatar and deployed into the DohaMetro projects rank among the best inthe world

28 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

set-up of modern and efficient transport solutions. We,at Qatar Rail, are supporting the National Vision’s fouressential pillars: economic, social, human, andenvironmental development; Qatar Rail’s project willrevitalize growth across the state’s sectors contributingto its economy, creating economic and investmentopportunities, and being highly beneficial for thecountry’s environment through the reduction ofcongestion and carbon dioxide emissions.

The projects we will undertake will work in fullintegration to connect Qatar’s key areas with each otherand with their vital extensions – whereby, the DohaMetro will link the capital’s inner and outer areas suchas Lusail city, the New Doha International Airport, theEducation City, and the West Bay area.

We are also keen on having our projects make a positivedifference in the everyday lives of Qatari people, andbringing about a real shift for the State of Qatar, placingit among the world’s most developed and advancedcountries in the transport field, and equally rankingQatar Rail’s project among the most pioneering,ambitious, and innovative integrated railway projects in the region.

The State of Qatar will be undertaking several majorprojects pertaining to the hosting of the FIFA World Cup2022, and more importantly, in line with its NationalVision 2030. These projects require a slew of world-class

transport equipment and logistics solutions that arecapable of timely delivery; ones that we are heavilyinvesting in for all our projects and developments.

We are fully aware of the potential that a world-classproject like Qatar Rail has to offer. The mega projectwill act as a catalyst and provide an opportunity forQatar to promote the development of the private sector.

We have identified unique business opportunity clustersacross key industry sectors. These business opportunitieswill generate value for Qatar and are sustainable beyondthe construction of the rail network. Qatar Rail isworking with the business community and holdingroadshows to showcase these business opportunities,which can be captured both by Qatari entrepreneursand multinational companies.

Obviously there is significant pressure on us all to deliverquality on time to fulfill the Qatar 2030 Vision – this iswhy it is critical to evaluate and assess the longevity,reputation and technical expertise of all our partners.The Government is also assessing the need to createlaws which allow international companies to operatemore effectively in Qatar, which is very positive andcritical to achieve the end Goal!

Saad Ahmed AlMuhannadiChief Executive OfficerQatar Rail

Interviewed by:Cynthia CorbyPartnerConstruction Industry LeaderDeloitte Middle East

The State of Qatar will be undertakingseveral major projects pertaining to thehosting of the FIFA World Cup 2022,and more importantly, in line with itsNational Vision 2030

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 29

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 31

The projected level of investment in infrastructure acrossthe GCC states in the coming decade is enormous. The challenges for government and the private sectoralike in delivering the planned pipeline are significant.Large, time-critical and competing programs across theGCC will likely place pressure on the procurement of allinputs necessary for achieving a successful project, fromspecialist items of machinery such as TBMs and HVequipment, to labor (skilled and unskilled) and materials.This heightened demand not only places upwardpressure on prices, but also places delivery schedules atrisk. Port and logistics bottlenecks loom large in certainjurisdictions, further compounding these risks. Fundingis also likely to be a challenge. Aside from the Kingdomof Saudi Arabia, where credit is plentiful, debt maybecome scarce and the cost of debt, particularlycommercial bank debt, is likely to increase.

In this dynamic environment, ripe with opportunity, butreplete with risk, private market participants will need tomake astute decisions around the deployment of capitaland resources. These decisions are set to become evenmore challenging due to the resurgence of demand inother developed economies such as the United States,which may be perceived as providing a more establishedframework, and hence a safer haven, for capitalinvestment.

Infrastructure andsocial infrastructurespend and thechallenges aroundthese projects

32 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

With this in mind, we think it is possible to make somepredictions for infrastructure development in the MiddleEast, which may constitute useful sign-posts fordecision-makers:• Public Private Partnerships (PPP) will continue to beused extensively in the power, water and wastewatersectors. The GCC International Power Project (IPP)model is well established, with reasonably limitedjurisdictional variations. New IPP/IWPP markets such asDubai will provide good opportunities for developersand contractors familiar with that model;

• Beyond power and water, the favored procurementmethodology for infrastructure (that is not plant) willstill be direct procurement under fixed priceconstruction contracts based on the FIDIC suite ofdocuments. The procurement and delivery of theseprojects will continue to be managed extremelyaggressively by employers (both public and privatesector). Little ground will be given in response tocontractor requests for deviations during theprocurement process, and contractors will again beasked to stake considerable cash collateral to winprojects. Resilient and enterprising contractors may be able to increase profitability in the fixed priceenvironment if demand begins to outstrip supply;

• Some fairly large social infrastructure projects (notablyschools and health projects) will be delivered under aPPP availability payment model. Where the sponsorsare independent from the procuring entity, participantscould reasonably anticipate delays around projectclosings and higher than usual transaction costsconsistent with a fledgling, rather than mature,market. Furthermore, there may be a lack of fundingappetite for these projects, as there is less scope forexport credit support for non-plant based PPP;

• A resurgent real estate market in the UAE andelsewhere will provide government with theopportunity to subsidize the cost of PPP in the housingand accommodation sectors through the grant oflong-term leases, or the transfer of land plots, forprivate and commercial real estate development.While recent regulatory reform in the UAE has easedsome risks for investors in the sector, the currentinflationary signals in this market should leadcontractors to investigate the financial health of theproject sponsors in this sector (whether private orpublic) and to ensure that there are adequate non-realestate assets available from which to satisfy any debts;

• Elsewhere, user fees for most government-providedservices (such as roads or metro transport) willcontinue to be too low to support concession projectswith a significant element of revenue or patronagerisk. In a sense the GCC will avoid some of themistakes made elsewhere in relation to theformulation of such projects;

• There will be a trend towards more sustainable,greener and better maintained infrastructure,especially in the UAE. Renewable energy (solar/PV) willcome into its own as an important source of capacity.Specialist O&M contractors will play an increasinglyprominent role, particularly in the transport sectorwhere improvements in the operational efficiency ofmature infrastructure assets can be derived throughthe experience of private sector operators operatingacross a range of jurisdictions;

While recent regulatory reform in theUAE has eased some risks for investorsin the sector, the current inflationarysignals in this market should leadcontractors to investigate the financialhealth of the project sponsors in thissector

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 33

• GCC governments will continue their push for greaterinvolvement of their nationals in all aspects of thedelivery of infrastructure projects, as part of theirpolicies for achieving higher participation by GCCnationals in the private sector workplace overall.Private sector organizations that recognize this trendand which are able to seize upon it as an opportunity,rather than treating it as an obstacle to overcome, arelikely to achieve better outcomes;

• GCC governments will (astutely) take advantage ofliquidity sources in the Far East in particular by seekingcontractor-sourced finance for major "hard"infrastructure projects. Contractors will need to becareful to ensure that the portion of the outstandingcontract price representing principal becomes payablefrom a hard-coded date or that completion tests areachievable and documentation is unambiguous.Some contractors may view the contractor financemodel as closer to "business-as-usual" than appearson paper, given the historical need to self-finance theback-end of most projects in the GCC as a result ofthe culture of disputes that has developed in theregion, and the relatively poor payment record ofmost employers outside the NOCs and international oil majors; and

• GCC governments will continue to take a hard-nosedand sophisticated approach to major procurement.The increasing use of thinly capitalized procurementvehicles will mean that developers and contractors willneed to be alert to sources of recourse if projectsunravel. Political risk will need to be considered in thebroadest possible sense and not simply in the contextof state failure or blatant expropriation. The demandfor legal services relevant to the delivery ofinfrastructure projects in the public and private sectorwill rise as a result.

None of the above constitutes particularly new ororiginal thinking. While that may not satiate thoselooking for exponential economic growth through rapid

change, we think that it does reflect the fact that theGCC is becoming an increasingly mature market. Assuch, it will still provide excellent opportunities forprofitable growth as it has in the past, but with agreater focus on building economies which aresustainable and resilient. We are consistently surprisedby the clear thinking and foresight of the community ofleaders who, having now clearly established this regionas important for the rest of the world, are looking tobuild a lasting legacy for the benefit of their nationalpopulations.

Simon HarveyPartnerInfrastructure –Transactional Pinsent Masons

Bill SmithPartnerInfrastructure –DisputesPinsent Masons

Political risk will need to be consideredin the broadest possible sense and notsimply in the context of state failure orblatant expropriation

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 35

Combatting fraudin the constructionsectorA high-risk fraud environment is typified by heightenedpressure and opportunity. When these factors areconsidered on an industry basis, the construction sectorrates highly, particularly in the procurement cycle. Fromaward to execution, employees and external parties(agents, suppliers, and competitors) have significantopportunities to commit fraud.

In the Middle East, these risks are heightened by thesheer scale of capital projects, a propensity to cashdealings, the involvement of myriad connected parties,and a transient and low-paid workforce.

“Corruption can add up to 10% to the total cost ofdoing business globally, and up to 25% to the cost ofpublic procurement in developing countries.”

The absence of properly structured and executed fraudcontrols in construction projects acts as a vacuum intowhich fraud opportunity, and persons susceptible to thetemptations, are drawn together. In the below casestudies, you will see that the simplest of controls wouldhave prevented the fraud, or at the very least detected itmuch earlier.

36 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

Case study #1“A number of managers involved in the construction ofa major power project received large cash payments andgifts from colluding with vendors to award lucrativesupply contracts. Some of these same managers thenwent on to establish companies through proxies to actas agents in the supply of a wide range of materials tothe Plant. The syndicated nature of this scheme meantthat the segregation of controls of duties in theirprocesses was circumvented. The fraud took placeprogressively over a period of years. By the time awhistleblower came forward, the quantified leakageexceeded US$2M and involved 285 separate fraudincidents. The investigation discovered that there wasno active price checking outside of provided bids orexisting supply contracts. An examination of vendorregistrations and HR files would have identified thesuspicious links between suppliers and employees.”

Case study #2“Following allegations of misconduct involving thegeneral manager of a regionally-based constructioncompany, an investigation revealed a significantdiscrepancy between the quantity of high-value scrapmaterials that were removed from site and the

payments received for the scrap. The general managerwas found to have directed the sale of these materialsfor his own personal benefit. The schemes employedincluded the disposal of usable materials as scrap, saleof scrap below market value, and general theft anddiversion of scrap and consumable materials. Theposition of the individual allowed for the circumventionof internal controls, including diversion of staff fromtheir normal role, and placing undue pressure on-sitesecurity personnel to effect the movement of materialsfrom the sites without documentation. Calculated lossesexceeded US$1M; however, the true impact is likely tohave been significantly higher.”

Numbers do not tell the full storyThat last point in the above study is something thatreaders will see in many cases of fraud. This is quiteunderstandable, as these activities are mostly identified‘after the fact’ through investigations and post-construction audits. Full quantification of loss is asignificant exercise, and rarely do companies wish toinvest further funds to put a true number to the losswhen they have already weeded out the offendingpeople and practices. Only in circumstances where thereis a reasonable chance of recovery from the offendingparties or from insurers would such a detailedquantification be palatable.

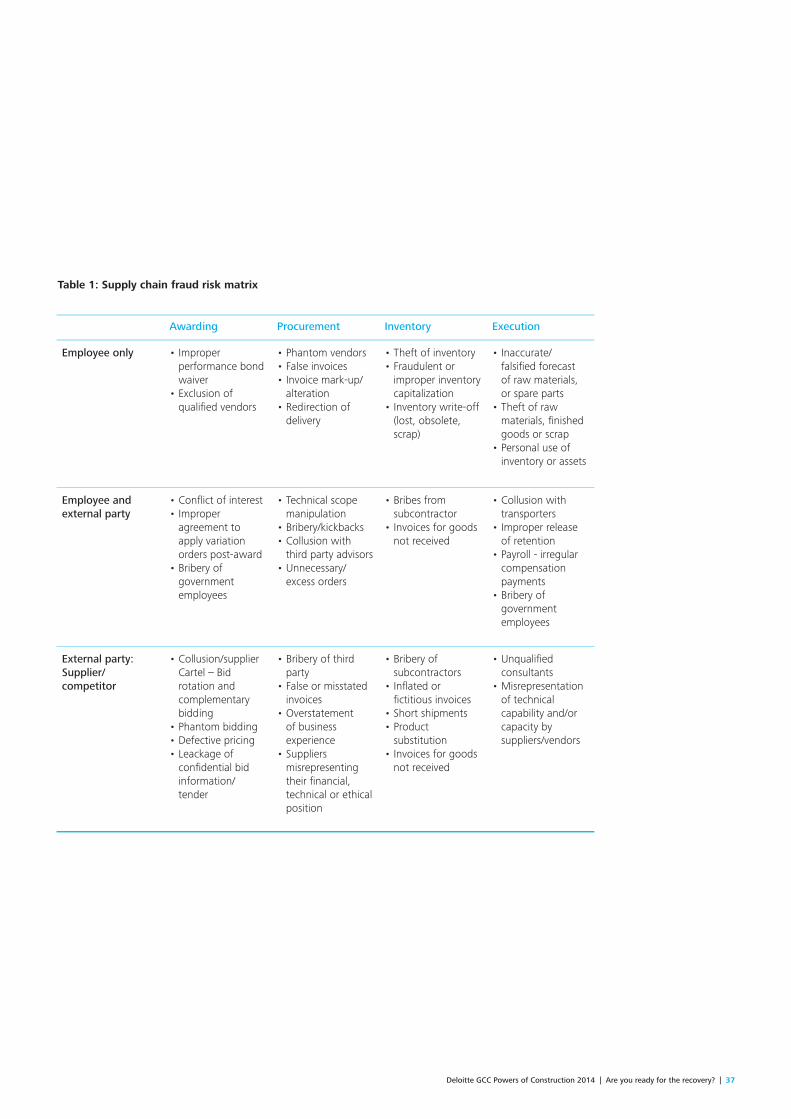

Fraud and supply chain integrity awarenessRegionally, much is being done to address the specter offraud, bribery, and corruption. Recent efforts in Oman,Saudi Arabia, and the UAE have placed companies onnotice that the ‘old’ ways of cornering business throughunder-the-table inducements are no longer acceptable.The recent spotlight has been on tendering andawarding. There are of course many other areasthroughout the four stages of the supply chain wherefraud and misconduct can occur. The following tablelists some of the fraud risks at each stage of the cycle,aligned against where that risk resides.

Recent efforts in Oman, Saudi Arabia,and the UAE have placed companieson notice that the ‘old’ ways ofcornering business through under-the-table inducements are no longeracceptable

Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery? | 37

Awarding Procurement Inventory Execution

Employee only • Improperperformance bondwaiver

• Exclusion ofqualified vendors

• Phantom vendors• False invoices• Invoice mark-up/alteration

• Redirection ofdelivery

• Theft of inventory• Fraudulent orimproper inventorycapitalization

• Inventory write-off(lost, obsolete,scrap)

• Inaccurate/falsified forecast of raw materials,or spare parts

• Theft of rawmaterials, finishedgoods or scrap

• Personal use ofinventory or assets

Employee andexternal party

• Conflict of interest• Improperagreement toapply variationorders post-award

• Bribery ofgovernmentemployees

• Technical scopemanipulation

• Bribery/kickbacks• Collusion withthird party advisors

• Unnecessary/excess orders

• Bribes fromsubcontractor

• Invoices for goodsnot received

• Collusion withtransporters

• Improper releaseof retention

• Payroll - irregularcompensationpayments

• Bribery ofgovernmentemployees

External party:Supplier/competitor

• Collusion/supplierCartel – Bidrotation andcomplementarybidding

• Phantom bidding• Defective pricing• Leackage ofconfidential bidinformation/tender

• Bribery of thirdparty

• False or misstatedinvoices

• Overstatement of businessexperience

• Suppliersmisrepresentingtheir financial,technical or ethicalposition

• Bribery ofsubcontractors

• Inflated orfictitious invoices

• Short shipments• Productsubstitution

• Invoices for goodsnot received

• Unqualifiedconsultants

• Misrepresentationof technicalcapability and/orcapacity bysuppliers/vendors

Table 1: Supply chain fraud risk matrix

38 | Deloitte GCC Powers of Construction 2014 | Are you ready for the recovery?

Fraud, in all its guises, has at its center a breach of trust.In a project environment, trust is essential due to thesegmented expertise that each party brings to the table.Accordingly, it is critical to ensure that the trust awardedis based on substance, and subjected to some level ofverification and cross-checking.

Prevention is better than cureThe most common of sayings – prevention is better thancure – is, however, a resounding truth when it comes tofraud. Too often, construction companies have beencaught out with an ‘eyes on the prize’ mentality, andhave neglected the core planning processes that mayidentify questions that need to be asked to other partiesin the project, while also neglecting to ensure that thesupply chain policies and procedures are clear,transparent, and properly segregated.

Whilst the risk of fraud can never be fully eliminated,companies can implement controls to mitigate thelikelihood of such risks occurring, and help detect themearlier to reduce the impact to the project, and to thecompany. Consider the following checklist forpreventing procurement fraud for example:1. Due diligence and background checks on partners/master contractors/sub-contractors. At a minimum,you should have confidence in the following factorsa. Capabilities to contracted tasksb. Financial stability and ultimate beneficiaries ofpayments

c. Reputation in the market2. Overt stance on fraud, bribery and corruption:a. Fraud Risk Management (FRM) frameworkb. ‘No bribes’ policyc. Business code of conduct, with specific conflict ofinterest and gifts and entertainment provisions

d. Whistleblowing facilitye. Fraud Response Plan (FRP)f. Ethics and fraud awareness training for your staffg. Supplier code of conduct for your suppliers,and their sub-contractors

h. Rotation policy on high risk parties (e.g. buyers)i. Enhanced employee screening for high riskpositions

j. ‘No bribery’ clause in all supplier agreementsk. Right to audit clauses in all supplier agreementsl. Debarment policy to exclude suppliers andcontractors that have participated in any illegalor unethical activities

3. Independent oversight to test and challenge yoursupply chain procedures and processes: a. Internal audit reviews b. Data mining to look for hidden red flags

The dynamic nature of construction projects shouldcompel continual vigilance throughout the life of theproject. Never lose sight of the fact that efficiency andperformance issues can at times be indicators that aparty is not being true and trustworthy in theirresponsibilities in the project. Robust and continualvigilance will greatly improve your chances of weedingout the fraudsters.

Neil HargreavesManaging DirectorForensic & DisputeServicesDeloitte CorporateFinance Limited

Stephen CroweDirector Forensic & DisputeServicesDeloitte CorporateFinance Limited