GE Oil & Gas Claudi Santiago President & CEO This document contains "forward-looking statements" - that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance, and often contain words such as "expects," "anticipates," "intends," "plans," "believes," "seeks," or "will." Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties which could adversely or positively affect our future results include: the behavior of financial markets, including fluctuations in interest rates and commodity prices; strategic actions, including dispositions; future integration of acquired businesses; future financial performance of major industries which we serve, including, without limitation, the air and rail transportation, energy generation, media, real estate and healthcare industries; unanticipated loss development in our insurance businesses; and numerous other matters of national, regional and global scale, including those of a political, economic, business, competitive and regulatory nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.

Transcript

GEOil & Gas

Claudi SantiagoPresident & CEO

This document contains "forward-looking statements" - that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance, and often contain words such as "expects," "anticipates," "intends," "plans," "believes," "seeks," or "will." Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties which could adversely or positively affect our future results include: the behavior of financial markets, including fluctuations in interest rates and commodity prices; strategic actions, including dispositions; future integration of acquired businesses; future financial performance of major industries which we serve, including, without limitation, the air and rail transportation, energy generation, media, real estate and healthcare industries; unanticipated loss development in our insurance businesses; and numerous other matters of national, regional and global scale, including those of a political, economic, business, competitive and regulatory nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.

1 /GE Confidential and Proprietary Information /

May 10, 2006

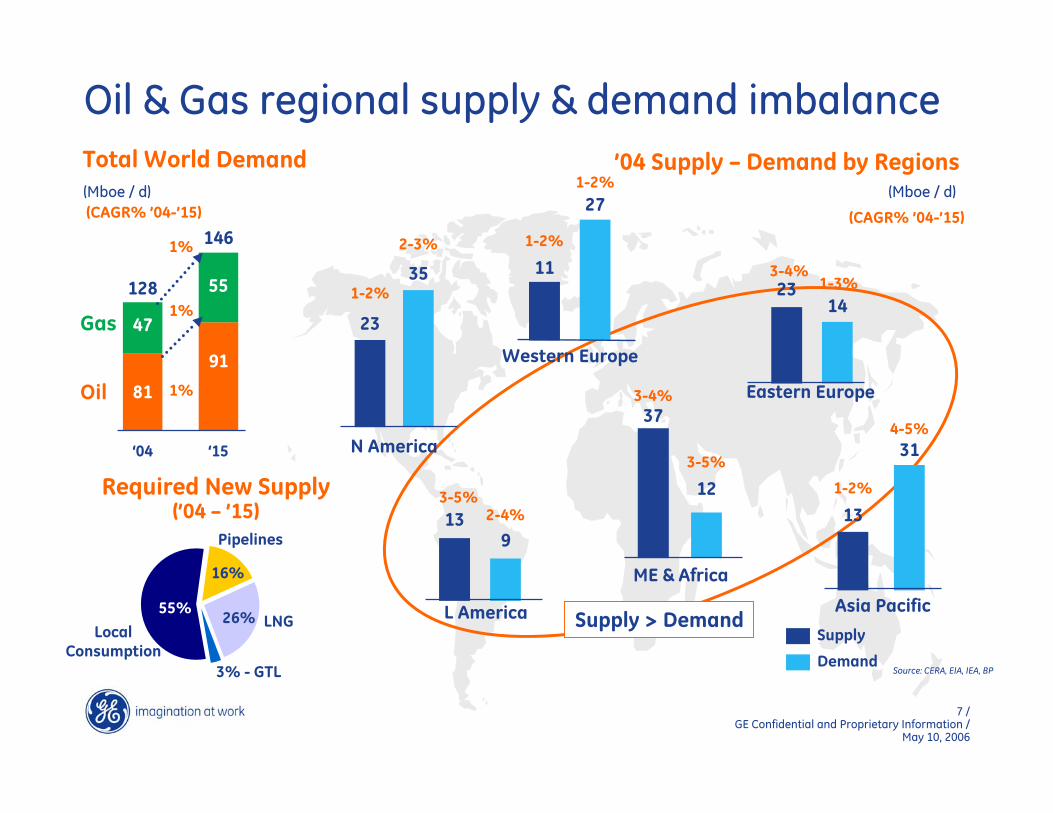

Oil & Gas Industry

Off-shore Platform

LNG … Liquefied Natural Gas

Compression Trains

Pipelines … “iPigs”

Refinery

2 /GE Confidential and Proprietary Information /

May 10, 2006

Building a Growth Platform

Nuovo Pignone

Acquisition

$1.3

'94

Oil & GasIndustry

Focus

$1.7

'00

GlobalizedFootprint

$2.7

'02

$2.2

'01

Created aTechnologyAdvantage

'97

Developeda Service

Model

$1.5

'03

AdjacentSegment

Entry

$3.1

'04

CoreOrganic

Expansion

$3.6

‘05

BecamePart of

GE Infra-structure

$4.2

($B orders)

3 /GE Confidential and Proprietary Information /

May 10, 2006

Service evolution

65%35%

‘06~$5.0

($B orders)

10%

‘97

$1.5

90%Units

Service

4 /GE Confidential and Proprietary Information /

May 10, 2006

Global presence

15%RoW

20%USA

25%Europe+

~$5.0

40%ME&A

19%36%

32%

$3.6

13%

$1.7

27% 16%

12%45%

Europe+

‘06‘04‘00

($B Orders)

RoW

ME&A USA

5 /GE Confidential and Proprietary Information /

May 10, 2006

Oil & Gas part of GE Infrastructure … for Good Reasons