26

Gemtek : A Leader in Wireless Broadband Access Kevin Yang Exec. Board & Spokesperson Gemtek Technology Co., Ltd. Date: Mar., 2011 2011 Outlook

Gemtek :

A Leader in Wireless Broadband Access

Kevin Yang

Exec. Board & Spokesperson

Gemtek Technology Co., Ltd.

Date: Mar., 2011

2011 Outlook

• Gemtek in a nutshell

• 2010 review

• Product and business strategies

• 2011 drivers, outlook and sales distribution

Agenda Agenda Agenda

Headquartered at Hsinchu Industrial Park, Total Employee: ≈ 4,500 (TWN: 1200; China: 3300)

• R&D and Engineering: ≒ 20%

• Production & QC: ≒ 50%

• Sales, Financial, Adm.: ≒ 30%

Capital: NT$2.84B (US$97.9 Million)

Market Cap: ≈ US$353 Million (Feb. 2011)

Production Capacity3 SMT Lines, 12 DIP Lines, 45 Assembly Lines and 15 Packing Lines

Corporate Facts

120

250

400 393

502542

668

559

713

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008 2009 2010

Million dollars (USD)

Annual Sales

TAIWAN

Shanghai

SUZHOU

Hong Kong

Hsinchu

KuShan

Czech Site

Plant Size: 172,000 SQF

Hsinchu Headquarter

Floor Space: 162,000 SQFLand Area: 215,000 SQF

Suzhou Plant

Prod. Floor: 66,000 SQF Land Area: 150,000 SQF

Facilities

Sites Certified for:ISO 9001, ISO 14001

OHSAS 18001, TL9000, C-TPAT

KunShan Plant

Plant Size: 330,000 SQF

Czech RepublicPrague

Votice

Changshu

Chang-Shu site

Floor Space: 441,160 SQFLand Area: 1,635,520 SQF

● Production pilot run June , 2010.

● Mass Production July . 2010.

● 30-50% capacity boost for new products & new customers

Global Facilities Expansion

As of September 30, 2009 As of September 30, 2010

Sales Revenue (k) 13,098,761 14,703,852

Gross Margin (k) 1,644,778 1,645,260

Gross Margin (%) 12.56% 11.19%

Operating Income (k) 608,444 178,023

Operating Profit (%) 4.65% 1.21%

Net Profit After Tax (k) 448,125 315,120

EPS after tax 1.76 1.27

Units: NT$ Thousands; Consolidated

*Stock based on 284Million shares

’10 Q3 Financial Performance

Cash & Equiv 2,266,127 1,598,139

Total Current Assets 7,034,140 13,098,282

A/R 2,911,311 6,025,316

Inventory 1,544,237 3,055,823

Net PPE 3,956,674 4,062,431

L/T Investment 1,514,849 1,021,741

Total Assets 12,852,724 1 8,661,994

L/T Debts 417,291 38 8,584

Total Liabilities 5,476,796 11,566,756

Shareholder Equities 7,305,219 7,095,238

2009200920092009200920092009200920102010201020102010201020102010

Ending September 30Ending September 30Ending September 30Ending September 30Ending September 30Ending September 30Ending September 30Ending September 30In NT$000In NT$000’’

Source: Gemtek

Balance SheetBalance Sheet

’10 Q3 B.S.

Sales Expansion for New Products and New Markets

RD Expansion for New Technologies

Structural Salary Adjustment

OPEX

Site Expansion Phase 2

SMT Line Expansion

Other Investments

CAPEXGM

NT$ Appreciation

Competitive Landscape

Product Life Cycle

Early-mover advantage

Self-Owned Capacity+

Cost-Down

Product Mix Shift

Expand OpMwith

Better Execution

Deliver Stronger P&L

Winning Strategies

� Expand New Customers Basis

� Provide Total Solutions

� Lead Product Innovation

What we have been doing amid & post the crisis —

Sustained Development of Business Winning Strategies

WANLAN

Application Processing

Media Processing

Wired

Wireless

ASSP

ConsumerElectronics Networking

Enterprise Networking

Green Life Networking

Wireless SystemsLocal Networking

Broadband Access

SeamlessCommunication

GreenLife

Entertainment& Social Effective

Work

Fast Access

EasyConnectivity

Product Vision

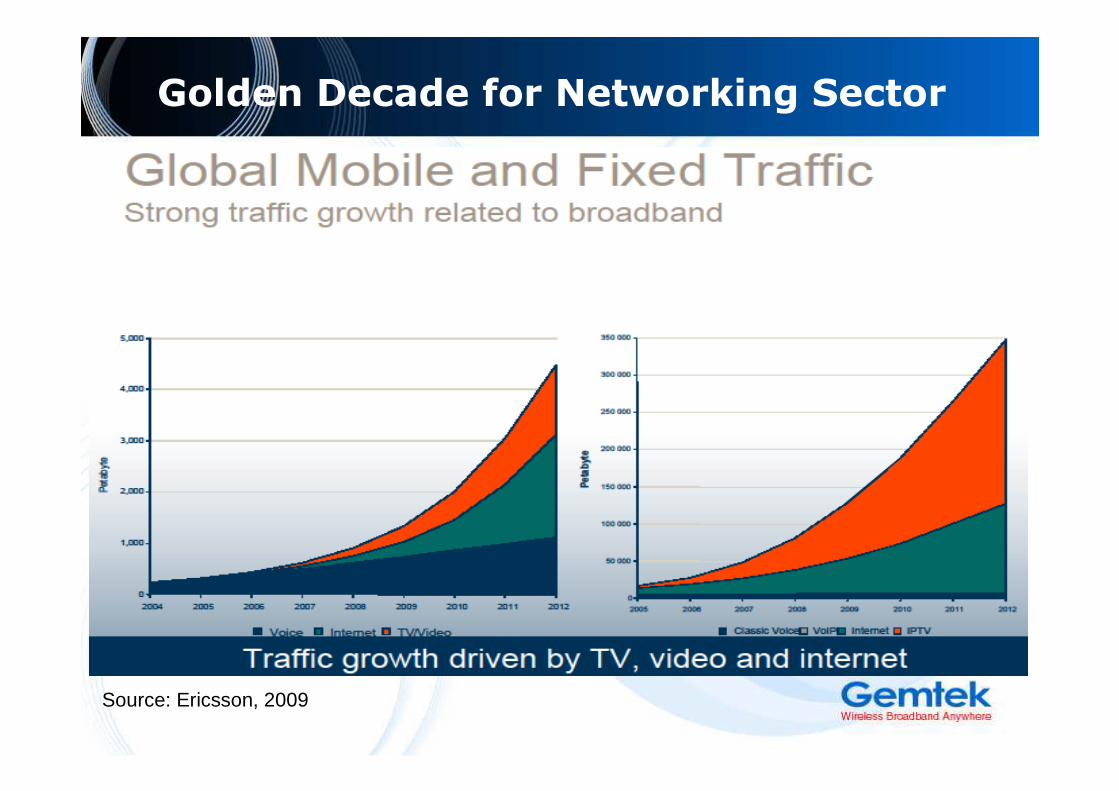

Source: Ericsson, 2009

Golden Decade for Networking Sector

SMB UTM

Femto

HomeNet

SmartGrid

Emerging

Current Mature

MID

DriveMarket Share

Cost Down

Differentiation

LTE

3G+Data

WiFi

Innovation

Add Customer Value

Invest Future

BackHaul

STB

GPON

DSL WiMAX

Tablet

20122011 2010

Innovator

Product Strategy Synergy to Emerge

WiMAX Femtocell

IPSTBMID

2011 Drivers

� Emerging countries will be a large market with positive market factors.

— Underlying demand remains healthy amid noises.

— Governmental broadband initiatives.

— Greenfield deployments just kiked off or awaiting in Indonesia, Philippine, Eastern-EU, and south Asia.

� Developed markets see WiMAX as a valuable auxiliary.

— WiMAX is one of the major “offload network” in broadband offering in developed countries.

— The only currently available broadband access solution with exiting networks.

— Fastest migration to LTE among all exsitingtechnologies.

— Long-awaited embedded devices arrived with increasing volume, signaling WiMAX ecosystem taking shape.

WiMAX Equipment Revenues (US$ million)

Source: Infonetics, 2010 Q1

Worldwide WiMAX Infrastructure: A Growth Story

Source: IEK, 2010

WiMAX Market Overview

Femtocell ecosystem is growing

Source: Airvana, Apr, 2010

Femtocell Volume fcst (,000 units)

Source: iSupply, 2010

� Commercially, the femtocell market has taken some strides forward recently, with a notable increase in live services numbers.

— Lauched by AT&T & Vodafone in 2h ’09, StarHubin late ’08, and Japan’s KDDI, France’s Free & China Unicom have all committed to femtocell.

— The indoor coverage journey quickly turned into a data offload story.

� Femtocell unit prices is approaching a magic mark.

— Price comes down once adoption accelerates.

— Cheap flat rate broadband package bundling helps deliver FMC and other integrated CPE like functions.

0000

5000500050005000

10000100001000010000

15000150001500015000

20000200002000020000

25000250002500025000

30000300003000030000

35000350003500035000

40000400004000040000

2009200920092009 2010201020102010 2011201120112011 2012201220122012 2013201320132013

Femtocell Market Overview

Source: iSupply, March, 2010

� With demand skyrocketing, every player in the STB industry is throwing their elbows to get a share of the market.

— STB has transformed into a combination of residential gateway+ home networking+ STB.

— Telco operators hope to reduce churn and enhance “stickiness” by becoming the sole provider of bundled information and entertainment services within home, creating an entirely new home entertainment experience.

� Open platform, like Android, enables all embedded devices.

— Home gateways will be the hub of seamless communication & remote smart home controller (home Security, power consumption monitoring, alert system, and tracking etc)

IPTV Subscriber fcst (Million of subscribers)

IPTV Subscriber by region (Million of subscribers)

Source: iSupply, March, 2010

IPSTB Market Overview

Total Wireless Wide Area Networking Market fcst (,00 0 units)

Source: iSupply, 2Q, 2010

Tablet TAM & CAGR

Source: CLSA

� Everyone’s rushing to have tablets/MIDs ready for holiday season. Bigger screen and higher-end features enable new set of applications.

� Tablets or MIDs will also be major conduits for premium push services from telco operators.

� Corporate customers are also climbing on board this tablet/MID train.

MID Market Overview

Retail Market

• WiFi client and AP/Router revenue share percentage diluted as embedded& integrated devices take the lead.

• Wireless HDMI shipment to ramp up as new customers added in and new products coming through.

2011 Outlook

PC OEM (Modules)

• WiFi becomes the standard connectivity in mobile devices. 11n well placed to boom.

• WiFi+WiMAX dual mode module shipment expands as more notebook/netbook built-in.

• WiFi direct likely to increase application and trigger replacement cycle.

2011 Outlook

Telecom Products- Wired • Booming data demand generates wired IAD advancement.

• GPON product starts shipment to new customer.

• Technology upgrade as VDSL to begin replacing ADSL.

.

2011 Outlook

Telecom Products- Wireless • Overloading data traffic and fixed mobile convergence

continue to generate 3G femtocell demand throughout all markets. Shipment booms. New customers join.

• WiMAX footprint gain in emerging markets and some part of developed markets. High-end CPEs continue to have a niche share. Volume grows steadily.

• Close relationship with LTE chipset vendors. LTE small volume shipment starts.

2011 Outlook

Telecom Products- IPSTB• STB momentum still strong as carriers continue to focus

on triple/quadruple customized play to generate ARPU.

• Open platform, or smart TV, aims at telecom operators with highly customized functions.

2011 Outlook

Customized Mobile Devices• Highly customized mobile devices pushed for vertical

market and offer multi-media features that enhance digital home performances.

• Shipment starts to teleco/SI/content provider customers aimed at vertical markets.

2011 Outlook

IntegratedIntegratedIntegratedIntegratedProduc tsProduc tsProduc tsProduc ts40~45%40~45%40~45%40~45%

WiFiWiFiWiFiWiFiClientClientClientClient

ProductsProductsProductsProducts20~25%20~25%20~25%20~25%

Wimax Wimax Wimax Wimax~15%~15%~15%~15%

AP/RouterAP/RouterAP/RouterAP/Router15~20%15~20%15~20%15~20%

Integrated Products WiFi Client Products

Wimax AP/Router

IntegratedProducts

~50%

WiFi ClientProducts15~20%

Wimax~20%

AP/Router15~20%

Integrated Products WiFi Client Products

Wimax AP/Router

2010 Status 2011 Forecast

Sales Distribution Projection

Thank You