25

General Principles of Financial Planning

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | juan-greenhow |

| View: | 224 times |

| Download: | 6 times |

General Principles of Financial Planning

Topic 1: Financial Planning Process

• Learning Objectives (a) Diagram the personal financial planning process

as defined by the CFP Board’s Job Task Domains and Financial Planning Practice Standards.

(b) Recognize unethical practices in the financial planning profession based on the CFP Board Standards of Professional Conduct.

Topic 1: Financial Planning Process

• Purpose and benefits • Six step process • Responsibilities • Financial planning methodology • Ethical issues • Assessing risk tolerance

Topic 1: Purpose and Benefits of the Financial Planning Process

• Purpose – To prepare a road map for clients to follow in

accomplishing their financial objectives • Benefits – To derive various solutions toward the

accomplishment of significant goals and the satisfactory resolution of client issues

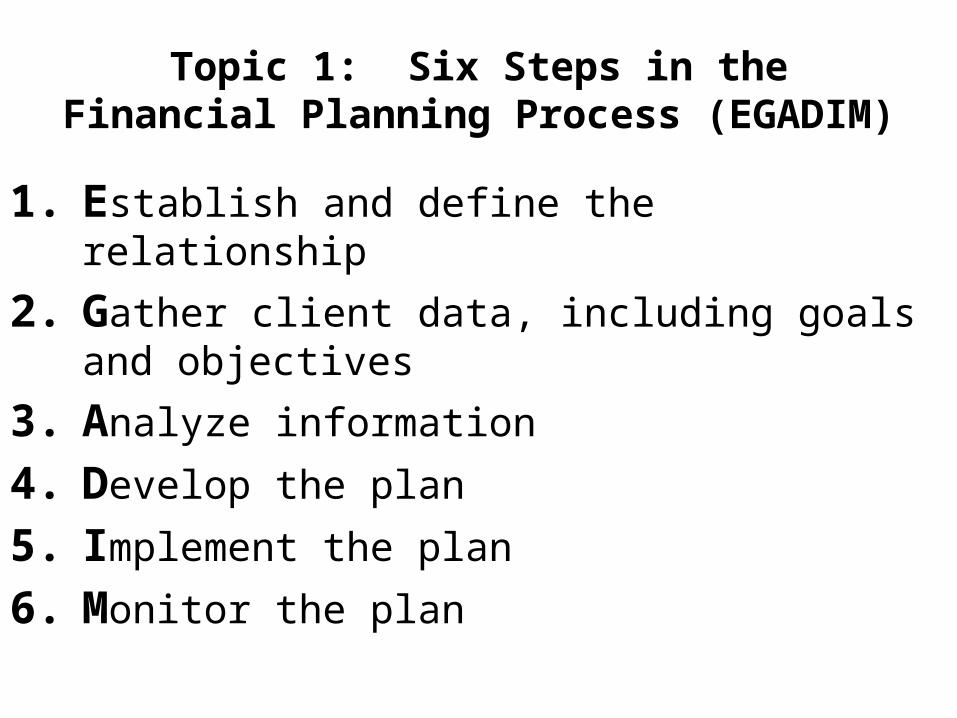

Topic 1: Six Steps in the Financial Planning Process (EGADIM)

1. Establish and define the relationship

2. Gather client data, including goals and objectives

3. Analyze information

4. Develop the plan

5. Implement the plan

6. Monitor the plan

Topic 1 Step 1: Establishing the Client-Planner Relationship

• Among the topics to be addressed in this step are: – Identifying the services that will be provided – Describing how the planner will be compensated – Identifying the specific responsibilities of both the

planner and the client – Deciding on the time frame of the engagement – Discussing any other matters needed to define or

limit the engagement’s scope

Topic 1: Factors Used to Determine if a Planner is Practicing Financial Planning

• Four factors used by CFP Board to determine if a planner is practicing financial planning or the material elements of financial planning – Client’s understanding and intent – Comprehensiveness of data-gathering – Breadth and depth of recommendations – Degree to which multiple subject areas are

involved

Topic 1: Rule 1.3

• If the services include financial planning or the material elements of the financial planning process, the certificant or the certificant’s employer shall enter into a written agreement governing the financial planning services (“Agreement”). The Agreement shall specify: – The parties to the Agreement – The date of the Agreement and its duration – How and on what terms each party can terminate the

Agreement – The services to be provided as part of the Agreement

Topic 1: Rule 2.2 • A certificant shall disclose to a prospective client or client

the following information: – Description of compensation, including the terms under which the

certificant or certificant’s employer may receive any other sources of compensation and what those payments are based on

– Conflicts of interest – Material information that could reasonably be expected to affect

the client’s decision to engage the certificant, including information about the certificant’s areas of expertise

– Contact information for certificant and employer – If the services include financial planning or the material elements

of financial planning, these disclosures must be in writing

• The certificant shall timely disclose to the client any material changes to the above information

Topic 1 Step 2: Establishing the Client’s Goals and Objectives and Gathering Information

• Establishing goals and objectives – Quantify specific financial goals in dollar terms and

within definite time frames – General aspirations must be specified in detail – Rank the objectives according to the client’s

priorities – Examine the objectives with due regard to the

client’s limited resources and other constraints

Topic 1: Typical Information Gathered • Assets - FMV, basis, date acquired, and related debts • Liabilities - Debts, alimony and support • Life insurance - Policy amounts, beneficiary designations, and

premium payments • Income - Wages, salary and other income • Expenditures - Current budget, savings and investments • Investments - Risk-tolerance and investment objectives • Estate planning - Wills, trusts, gifts, inheritances, and impact of

future earnings • Retirement planning - Retirement age, travel goals, and part-time

consulting • Miscellaneous - Disability income, medical expenses, education,

and hobbies

Class Exercise • The following list contains common data-gathering questions. Brainstorm ways to

change the wording of each question to encourage the client to offer qualitative details. In other words, turn the closed-end question into an open-end question.

• 1) How much life insurance do you have? • 2) Do you have long-term care insurance? • 3) Do you have a will? • 4) Who is the beneficiary on your retirement accounts and life insurance

policies? • 5) Do you have a retirement plan at work? • 6) Do you have an IRA? • 7) What kinds of investments have you owned in the past? • 8) What is the purpose of the money in this account? • 9) At what age do you plan to retire? • 10) What are your financial goals? • 11) Are there any “special needs” children or grandchildren in your family?

Topic 1: Problems With Gathering Information

• If the planner has made reasonable effort to obtain pertinent information from the client but the client has failed to provide the information, the planner may need to: – Redefine the scope of the engagement to exclude

the area for which there is missing information – Terminate the engagement

Topic 1 – Step 3: Steps for Analyzing and Evaluating the Information Gathered

• Review – Financial statements – Cash flow statements – Insurance policies – Wills – Trusts – Buy-sell agreements

• Analyze the information – To determine the strengths and weaknesses in the client’s financial

position • Evaluate

– The client’s objectives in view of available resources – The economic conditions as they relate to future resources and cash flow

for the client

Topic 1 Step 4: Developing the Plan

• Identify the strategies and products available for achieving the client’s objectives – Educate the client as to the alternatives and

advantages and disadvantages of each alternative, including maintaining the status quo

• Select the most appropriate strategies and products from those available – Provide additional disclosures based on product

recommendations

Topic 1 Step 5: Implementing the Plan

• Work closely with other professionals to carry out the financial plan designed for the client

• Define what the planner will do and when, and what the client will do and when

Topic 1 Step 6: Monitoring the Plan

• Periodically review the plan to determine the significance of any changes in: – Federal tax laws – Economic conditions – Available investment techniques – Client’s goals and objectives

• If new areas of planning arise that were not part of the original scope of the engagement, the planner and client will need to go back to step 1 and redefine the scope of the engagement

Topic 1: Responsibilities

• Typically, the financial planner is responsible for all six steps in the financial planning process

• The client will be responsible for: – Providing all of the necessary information – Reviewing the recommended plan – Some of the implementation – Monitoring the plan

Topic 1: Financial Planning Methodology

• Single-purpose view – A single financial product or service can be considered

financial planning • Multiple-purpose view

– Financial planning must deal with a broad range of financial concerns, such as investments, insurance, and taxes

• Comprehensive view – True financial planning must cover all of the client’s financial

concerns and goals • Purist view

– Comprehensive planning done in a single client engagement (with ongoing monitoring), on a fee-only basis

Topic 1: Ethical Issues

• The difference between compliance and ethics – Compliance is upholding the law – Ethics is doing what is morally correct rather than

merely doing what is legally acceptable • CFP Board’s Code of Ethics and Professional

Responsibility will be discussed in detail in Topics 76 - 78

Topic 1, Part 2: Assessing Risk Tolerance

• Four life situations involving risk – Monetary – Physical – Social – Ethical

• Planners should not assume monetary risk tolerance based on a client being risk tolerant in other areas

Characteristics of Risk Averters versus Risk Takers

Risk Averter Risk Taker Perceive risk as danger Perceive risk as opportunity Tend to overestimate risk Tend to underestimate risk Prefer low variability of possible Prefer high variability of results possible results Focus on worst-case scenario Focus on best-case scenario Tend to be pessimistic Tend to be optimistic Tend to like structure Tend to prefer ambiguity Tend to dislike change Tend to enjoy change Prefer certainty Prefer uncertainty

Demographics and Risk Tolerance

Tendency to be LESS risk tolerant Tendency to be MORE risk tolerant Inherited wealth Earned wealth Lower degree of formal education Higher degree of formal educationFirst-born children Later-born children Married with dependents Single Work in public sector Work in private sector Nonprofessional Professional Same job for long time Changes jobs often Lower-level managers Upper-level managers Compensated by salary Compensated by commission

Investment Risk Tolerance

• Understanding the trade-off between risk and return • Perceived risk is the individual’s interpretation of a risky

situation • Bounded rationality – There are limits on how rationally human beings can act in

many situations • Risk tolerance versus risk capacity – Risk tolerance = the amount of risk a client is willing to take on – Risk capacity = the amount of risk the client can afford to take

on • Use of risk tolerance questionnaires

•End of Topic 1