14

North American Markets: Oil, Gas, Electricity The Trilateral Commission, North American Regional Meeting November 2, 2010 Hal Kvisle Former President and CEO, TransCanada Corporation

| Date post: | 28-May-2018 |

| Category: |

Documents |

| Upload: | nguyenkien |

| View: | 217 times |

| Download: | 0 times |

North American Markets: Oil, Gas, Electricity

The Trilateral Commission, North American Regional Meeting

November 2, 2010

Hal Kvisle Former President and CEO, TransCanada Corporation

Forward-Looking Information

This presentation may contain certain information that is forward looking and is subject to

important risks and uncertainties. The words "anticipate", "expect", "may", "should",

"estimate", "project", "outlook", "forecast" or other similar words are used to identify such

forward-looking information. All forward-looking statements reflect TransCanada’s beliefs

and assumptions based on information available at the time the statements were made.

Actual results or events may differ from those predicted in these forward-looking statements.

Factors which could cause actual results or events to differ materially from current

expectations include, among other things, the ability of TransCanada to successfully

implement its strategic initiatives and whether such strategic initiatives will yield the

expected benefits, the operating performance of the Company’s pipeline and energy assets,

the availability and price of energy commodities, regulatory processes and decisions, changes

in environmental and other laws and regulations, competitive factors in the pipeline and

energy industry sectors, construction and completion of capital projects, labour, equipment

and material costs, access to capital markets, interest and currency exchange rates,

technological developments and the current economic conditions in North America. By its

nature, such forward-looking information is subject to various risks and uncertainties, which

could cause TransCanada's actual results and experience to differ materially from the

anticipated results or expectations expressed. Additional information on these and other

factors is available in the reports filed by TransCanada with Canadian securities regulators

and with the U.S. Securities and Exchange Commission. Readers are cautioned not to place

undue reliance on this forward-looking information, which is given as of the date it is

expressed in this presentation or otherwise, and to not use future-oriented information or

financial outlooks for anything other than their intended purpose. TransCanada undertakes

no obligation to update publicly or revise any forward-looking information, whether as a

result of new information, future events or otherwise, except as required by law.

3

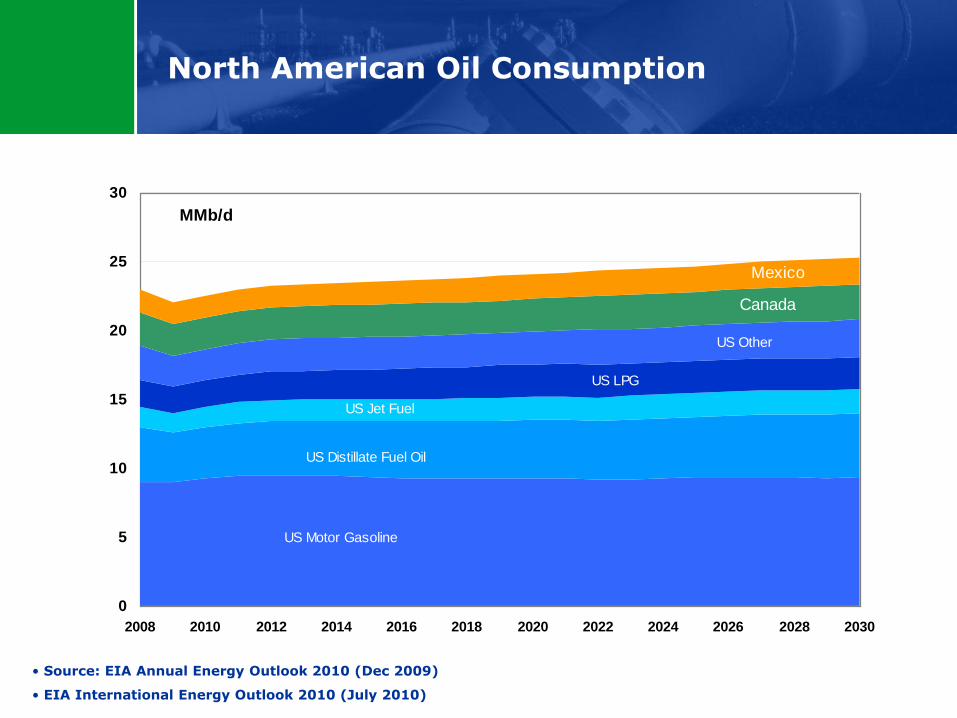

North American Oil Consumption

• Source: EIA Annual Energy Outlook 2010 (Dec 2009)

• EIA International Energy Outlook 2010 (July 2010)

US Motor Gasoline

US Distillate Fuel Oil

US Jet Fuel

US LPG

US Other

Canada

Mexico

0

5

10

15

20

25

30

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

MMb/d

4

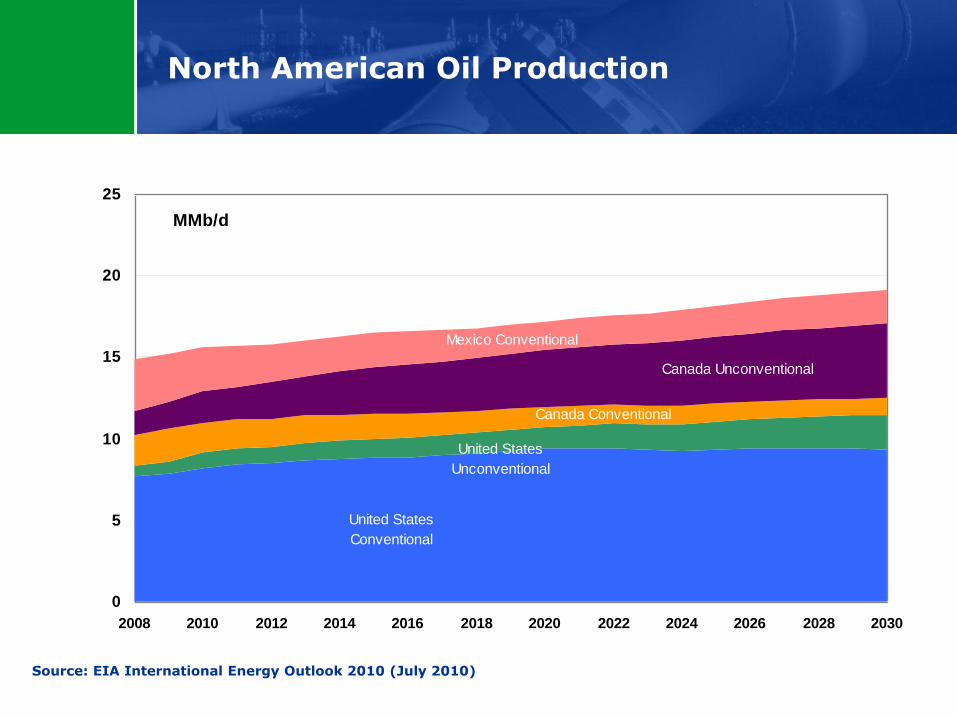

North American Oil Production

Source: EIA International Energy Outlook 2010 (July 2010)

United States

Conventional

United States

Unconventional

Canada Conventional

Canada Unconventional

Mexico Conventional

0

5

10

15

20

25

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

MMb/d

5

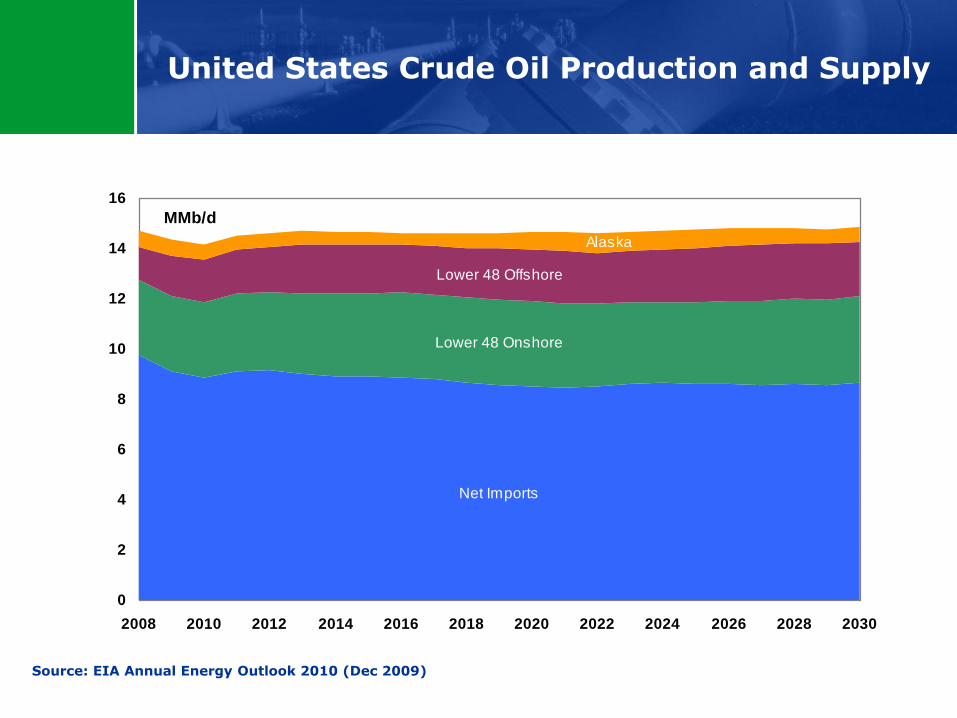

United States Crude Oil Production and Supply

Source: EIA Annual Energy Outlook 2010 (Dec 2009)

Net Imports

Lower 48 Onshore

Lower 48 Offshore

Alaska

0

2

4

6

8

10

12

14

16

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

MMb/d

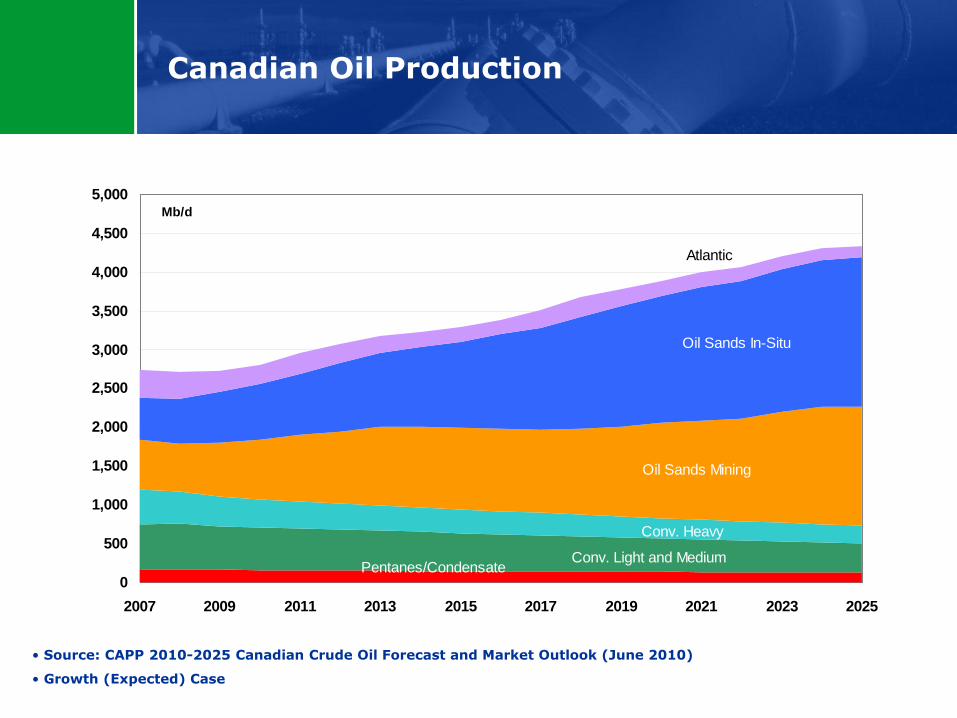

Pentanes/CondensateConv. Light and Medium

Conv. Heavy

Oil Sands Mining

Oil Sands In-Situ

Atlantic

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

Mb/d

6

Canadian Oil Production

• Source: CAPP 2010-2025 Canadian Crude Oil Forecast and Market Outlook (June 2010)

• Growth (Expected) Case

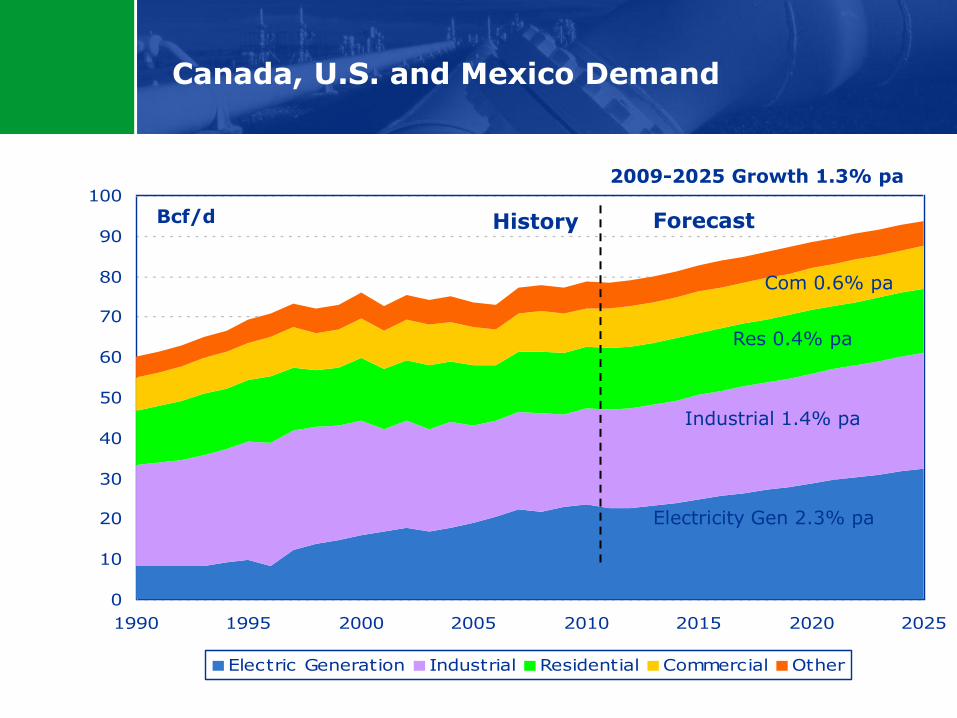

Canada, U.S. and Mexico Demand

0

10

20

30

40

50

60

70

80

90

100

1990 1995 2000 2005 2010 2015 2020 2025

Electric Generation Industrial Residential Commercial Other

Bcf/d History Forecast

2009-2025 Growth 1.3% pa

Industrial 1.4% pa

Electricity Gen 2.3% pa

Res 0.4% pa

Com 0.6% pa

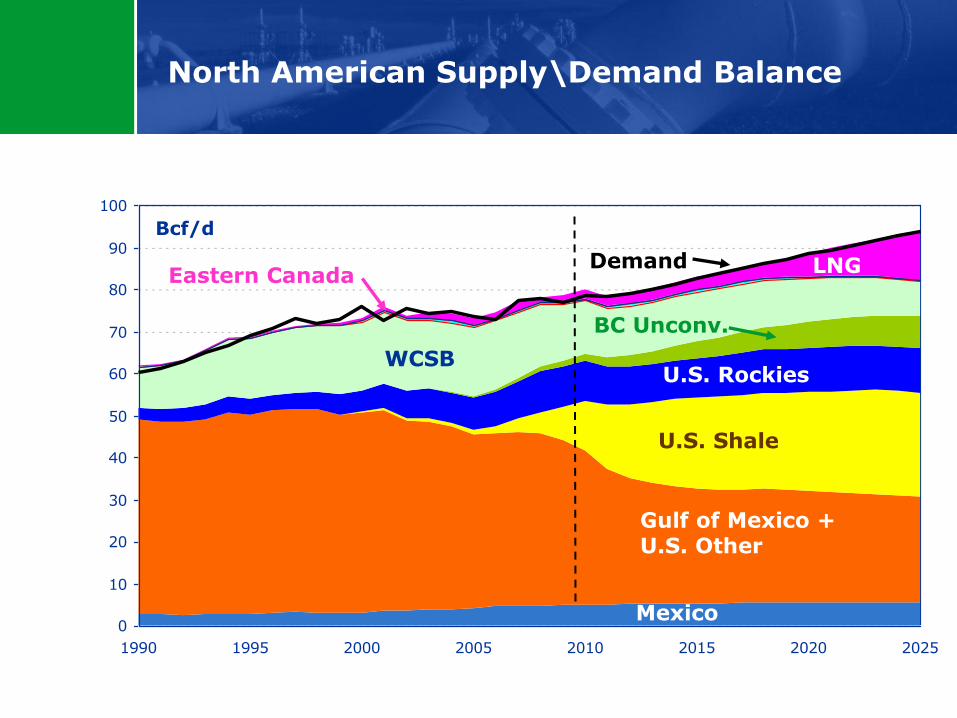

North American Supply\Demand Balance

0

10

20

30

40

50

60

70

80

90

100

1990 1995 2000 2005 2010 2015 2020 2025

Gulf of Mexico + U.S. Other

WCSB U.S. Rockies

Eastern Canada

Bcf/d

LNG

Mexico

Demand

History Forecast

U.S. Shale

BC Unconv.

9

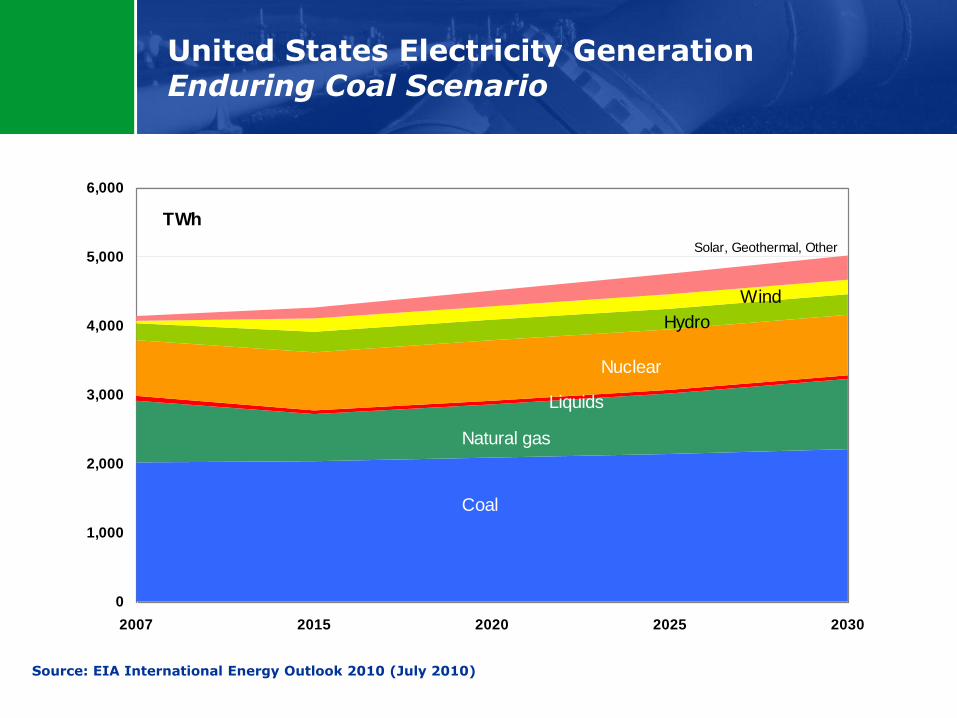

United States Electricity Generation Enduring Coal Scenario

Source: EIA International Energy Outlook 2010 (July 2010)

Coal

Natural gas

Liquids

Nuclear

Hydro

Wind

Solar, Geothermal, Other

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2015 2020 2025 2030

TWh

10

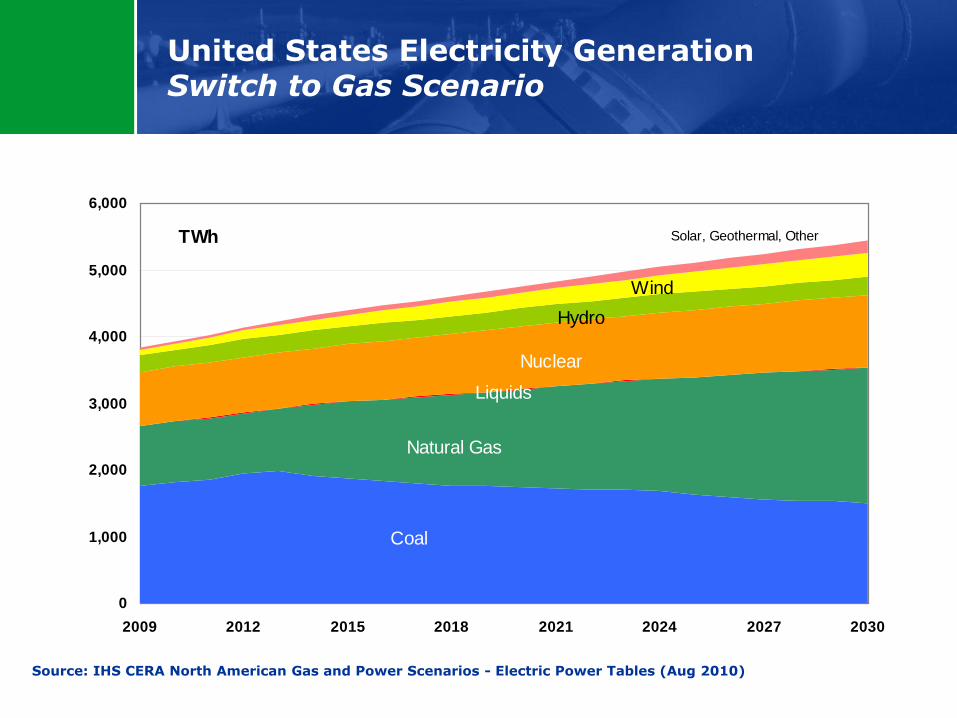

United States Electricity Generation Switch to Gas Scenario

Source: IHS CERA North American Gas and Power Scenarios - Electric Power Tables (Aug 2010)

Coal

Natural Gas

Liquids

Nuclear

Hydro

Wind

Solar, Geothermal, Other

0

1,000

2,000

3,000

4,000

5,000

6,000

2009 2012 2015 2018 2021 2024 2027 2030

TWh

11

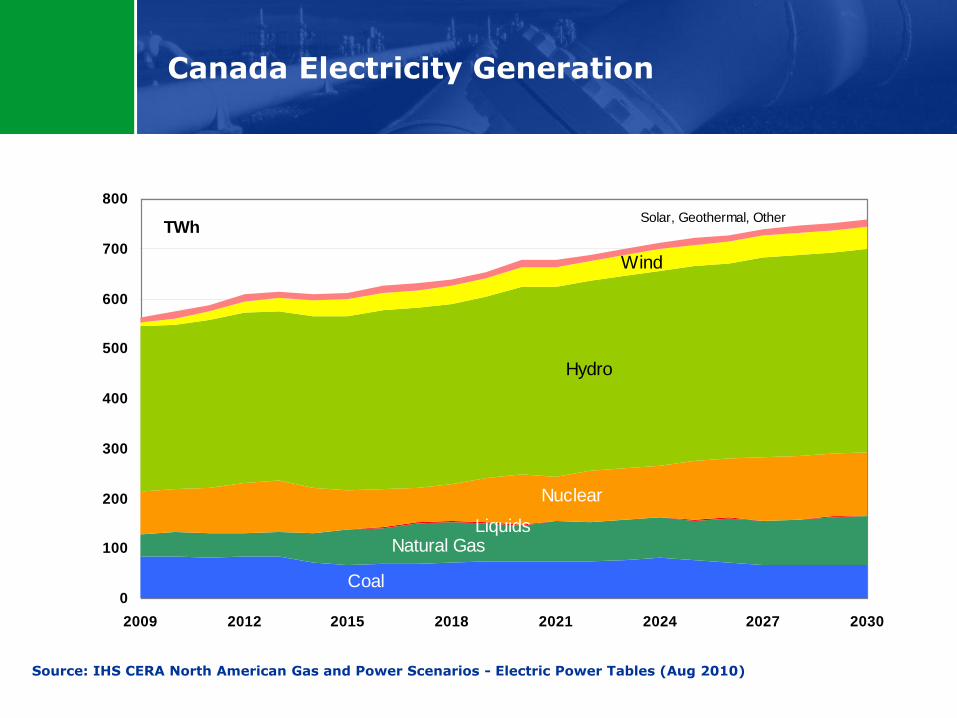

Canada Electricity Generation

Source: IHS CERA North American Gas and Power Scenarios - Electric Power Tables (Aug 2010)

Coal

Natural GasLiquids

Nuclear

Hydro

Wind

Solar, Geothermal, Other

0

100

200

300

400

500

600

700

800

2009 2012 2015 2018 2021 2024 2027 2030

TWh

12

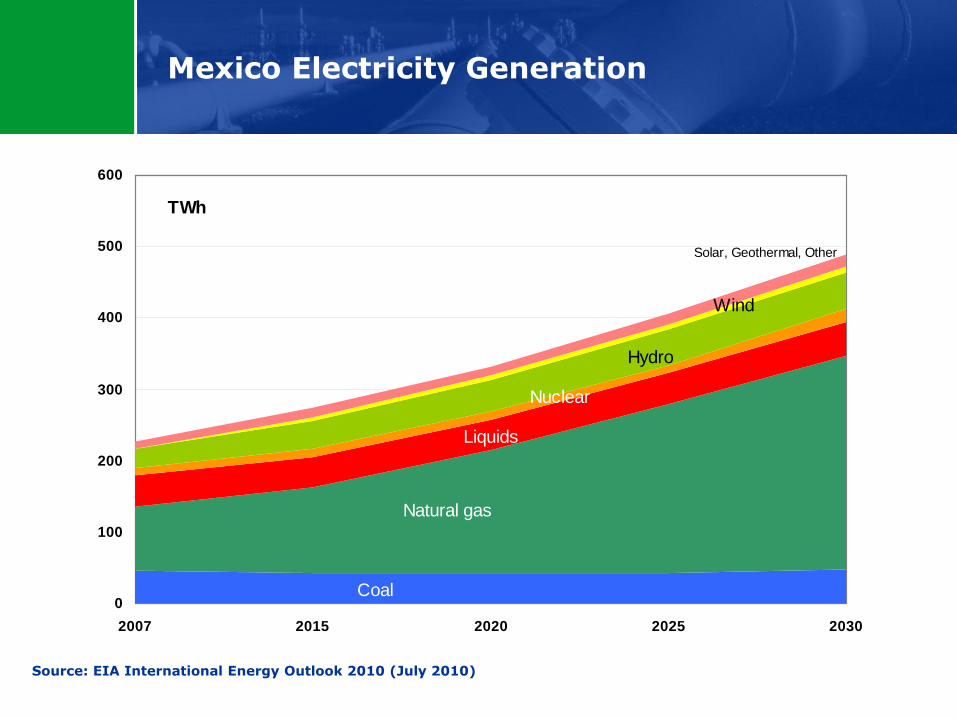

Mexico Electricity Generation

Source: EIA International Energy Outlook 2010 (July 2010)

Coal

Natural gas

Liquids

Nuclear

Hydro

Wind

Solar, Geothermal, Other

0

100

200

300

400

500

600

2007 2015 2020 2025 2030

TWh

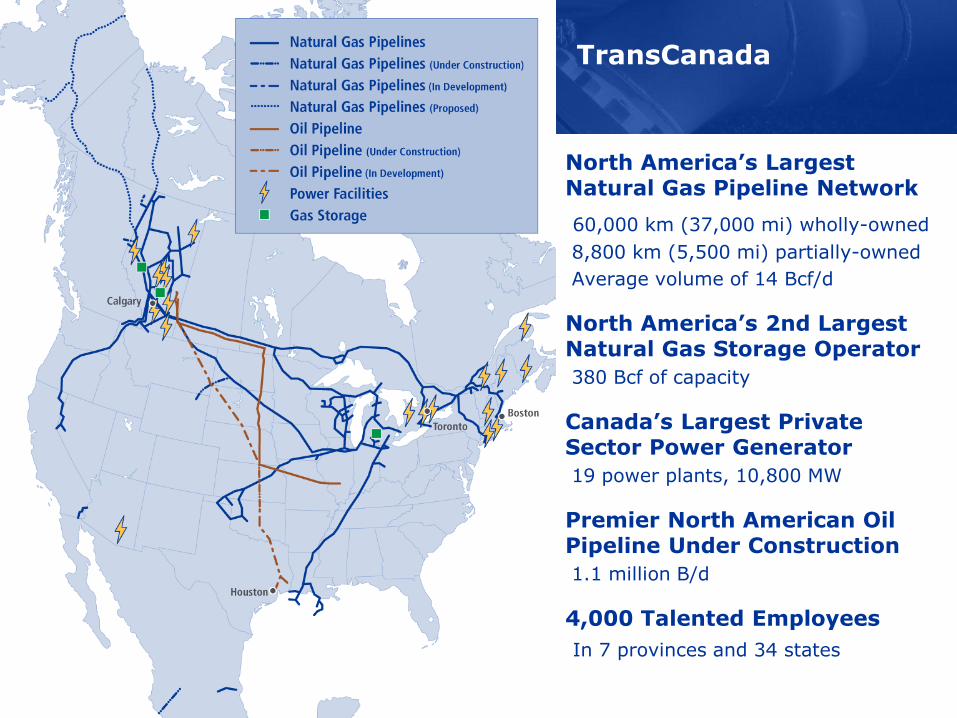

TransCanada

North America’s Largest Natural Gas Pipeline Network

60,000 km (37,000 mi) wholly-owned

8,800 km (5,500 mi) partially-owned

Average volume of 14 Bcf/d

North America’s 2nd Largest Natural Gas Storage Operator

380 Bcf of capacity

Canada’s Largest Private Sector Power Generator

19 power plants, 10,800 MW

Premier North American Oil Pipeline Under Construction

1.1 million B/d

4,000 Talented Employees

In 7 provinces and 34 states

Thank you

Hal Kvisle Former President and CEO TransCanada Corporation