239

April 2015 Georgian National Investment Agency Chemical Sector Research

April 2015

Georgian National Investment Agency

Chemical Sector Research

Group 24.1Production of Main Chemicals

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 3

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

DISCLAIMER

Our findings, observations and/or recommendations are those that we could reasonably derive from the procedures or scope of services performed. The specific procedures performed were agreed with Georgian National Investment Agency (the Client) and were performed by us as set forth in the Report.

Our work was carried out solely based on the publicly available research data.

We have indicated within our Report the sources of the information presented and have satisfied ourselves, so far as possible, that the information presented in our Report is consistent with other information which was made available to us inthe course of our work in accordance with the terms of the Contract. We have not, however, sought to establish the reliability of the sources by reference to other evidence.

All recommendations, provided to you with/in this Report that refer to the future have some limitations in the sense that they are based on the assumptions valid on the issuance date. These assumptions could change with time, after the date of this Report issuance, and so could lose their value.

References to 'KPMG Analysis' in this Report indicate only that we have (where specified) undertaken certain analytical activities on the underlying data to arrive at the information presented; we do not accept responsibility for the underlying data.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 4

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Table of Contents

Abbreviations 5Glossary of terms 6Industrial gases 7Pigments and other coloring matter 62Mineral Fertilizer and nitrogen compounds 102Other basic organic chemicals 155

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 5

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Abbreviations

AMD Armenian Dram

AG Aktiengesellschaft - corporation limited by share ownership

ASEAN Association of Southeast Asian Nations

AZN Azerbaijani Manat

bbl Barrel

BP British Petroleum

BVBA Private limited liability company

CAGR Compound Annual Growth Rate

CCPIA China Crop Protection Industry Association

CFR Cost and Freight

CIA Central Intelligence Agency

CIS Commonwealth of Independent States

COGS Cost of Goods Sold

EBIT Earnings Before Interest and Tax

EU European Union

EUR Euros

etc Et cetera

FAO Food And Agriculture Organization of the United Nations

FAT Free Agricultural Tax

FOB Free on board

FX Foreign exchange

GMO Genetically Modified Organisms

GmbHGesellschaft mit beschränkter Haftung, stands for company with limited liability

HAP Hazardous air pollutant

IFA International Fertilizer Industry Association

Inc. Incorporation

ITC International Trade Center

ITCI International Tax Competitiveness Index

K/mt Kilo metric ton

kg Kilogram, measurement unit of weight

m.t. Metric ton

m3 Cubic meter

MMBtu one million British Thermal UnitsLLC Limited Liability Company

LOA Lubricating oil additives

Ltd. Limited Company

N/A Not available

NAFTA North American Free Trade Agreement

nes Not elsewhere stated

NSSRA National Statistic Service of the Republic of Armenia

OECD Organization for Economic Co-operation and Development

OPEC Organization of the Petroleum Exporting Countries

o/t Other

p.a. Per annum

P/E Ratio of Price to Equity

PAG Polyalkylene glycol

PTA Purefied Terephthalic Acid

R&D Research and Development

s.a.r.l.Société à responsabilité limitée, it is a private limited liability corporate entity that exists in

s.r.l. The legal title of limited liability company

s.r.o.The legal title of a private limited company in Czech and Slovak.

Sp.z.o.o. The legal title of a private limited company in Poland.

t ton, measurement unit of weightUAH Ukrainian Hryvnia

UK United Kingdom

USA United States of America

VAT Value Added Tax

VOC Volatile Organic Compounds

WACC Weighted average cost of capital

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 6

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Glossary of terms

b.o.e.Barrel of oil equivalent, is a unit of energy based on the approximate energy released by burning one barrel

Bar The bar is a metric (but not SI (International System of Units)) unit of pressure

°C Celsius, temperature measurement unit

Current Ratio Is calculated as current assets divided by current liabilities

EBIT margin Is calculated as earnings before interest and tax divided by total sales

Inventory Turnover Is calculated as total sales divided by inventory

NACENomenclature of Economic Activities, is the European statistical classification of economic activities

Net Income Margin Is calculated as net income divided by total revenue

Rare gases Helium, neon, argon, krypton, xenon and radon are called rare gases

Return on Assets Is calculated as net income divided by total assets

S.A.Type of corporation in countries that mostly employ civil law, it is equivalent to public limited company in common law jurisdictions

SG&A margin Is calculated as sales, general and administrative expenses divided by total sales

Total Asset Turnover Is calculated as total sales divided by total assets

Industrial Gases

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 8

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

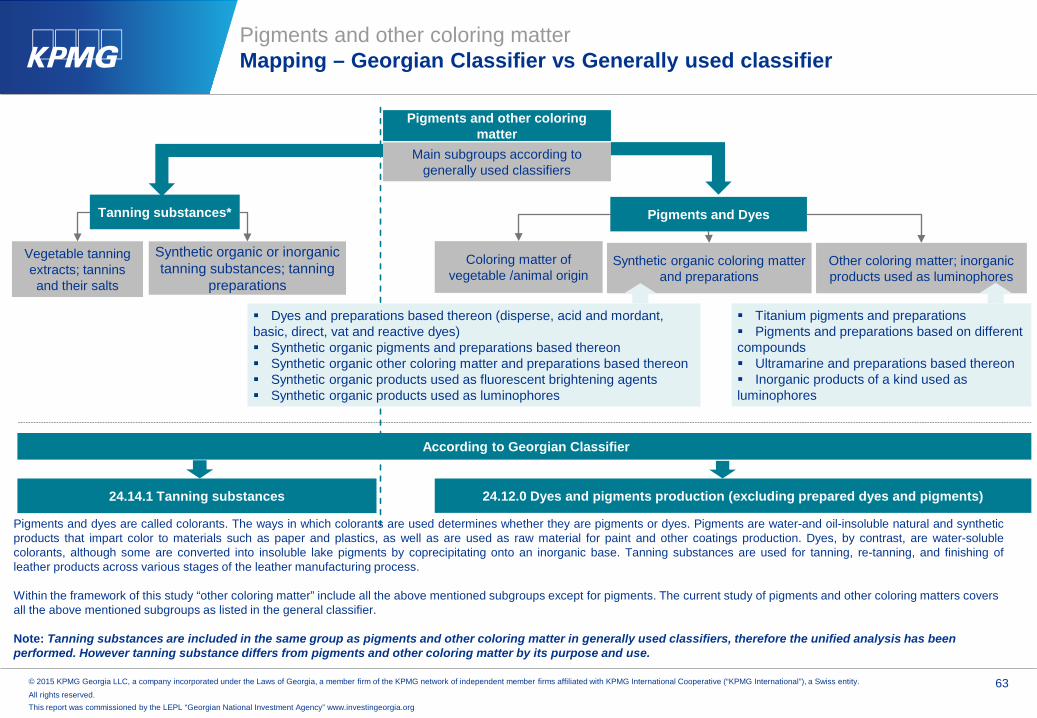

Industrial gasesMapping – Georgian Classifier via Generally used classifiers

In Georgian National Classifier SEK 001-2004 Sub Group 24.11 includes the following sections

Industrial gases

Elementary gases

- Argon- Chlorine- Fluorine- Helium- Hydrogen- Krypton- Neon- Nitrogen- Oxygen- Radon- Xenon

- Carbon dioxide- Helium- Krypton- Neon- Nitrogen- Radon- Xenon

Inorganic compounds; liquid air; compressed air; amalgams o/t of precious metals*

Generally used classification

Classification of Industrial gases under research

Industrial gases are used in various industries including health care, automotive, manufacturing, semiconductor, food andbeverages, chemical, electricity and metal industries.

Liquid and compressed

air

Cooling agent (refrigerant),

acetylene

Industrial gas mixtures Inert gases Safety

(insulating) gases

Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons,Unsaturated acyclic hydrocarbons

1. Mixtures of industrial gases presented in the report2. industrial gases obtained as co-products or by-products of other operations, such as;- Anhydrous ammonia- Ethylene- Ethylene oxide- Hydrogen fluoride- Hydrogen chloride- Trimethylamine- Methylamine- Sulphur dioxide - Nitrous oxide

- Ammonia- Argon- Carbon dioxide- Chlorine- Nitrogen- Nitrous oxide- Neon- Helium- Hydrogen

Note: Due to classification of available data, the inorganic compounds, amalgams, which are not industrial gases, are also included in the research, but the trade share of the whole group in the trade of industrial gases is less than 1%

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 9

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMapping – Georgian Classifier via Generally used classifiers (continued)

Our analysis has been performed based on the general classifier and as per the above mapping. Our analysis includes allthe mentioned industrial gases. The selected industrial gases are widely consumed worldwide and are produced by themajor big four companies (Linde, Air Liquide, Praxair and Air products) of the sector. Due to the chemical properties of thecorresponding gas, the same gas may be included in more than one group of the Georgian classifier, for instance radon isboth an elementary gas and an inert gas.

Due to the data representation differences (for acetylene, liquid and compressed air and nitrous oxide, the data is availableonly for chemical groups including those gases, not per individual type) the report classifies the mentioned industrial gasesinto two groups

1. Main industrial gases, which include

Anhydrous ammonia

Rare gases (excl. argon), which includes

helium, neon, krypton, radon and xenon

Argon

Oxygen

Nitrogen

Oxirane (ethylene oxide)

Ethylene

Sulphur dioxide

Chlorine

Hydrogen

Hydrogen fluoride

(hydrofluoric acid)

Methylamine, di- or trimethylamine and their salts*

Carbon dioxide

Hydrogen chloride

(hydrochloric acid)

Note: In the classification used the methylamine and di-or trimethylamine salts are also included in the group, however salts are not considered as industrial gases

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 10

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMapping – Georgian Classifier via Generally used classifiers (continued)

Unsaturated acyclic hydrocarbons, which includes acetylene

Fluorine; bromine, which includes fluorine

Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons

Inorganic compounds nes; liquid air; compressed air; amalgams o/t of precious metals, which includes liquid andcompressed air

Inorganic oxygen compounds of non-metals nes, which includes nitrous oxide

While using the term “industrial gases” it is considered that the data for both groups are included in the analyses.

2. Basic chemicals including industrial gases, which include

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 11

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

The industry is highly dominated by the global gas big four companies which account for approximately 71% of the industry’s global market

Industrial gasesGeneral overview

Due to their chemical properties, such as reactivity, inertness, and coldness, industrial gases are widely used in process industries such as Oil and Gas, Chemicals, Power, Mining, Metals, Pharmaceuticals, Food, Electronics, and Aerospace.

The industrial gas industry is highly consolidated with only four major players that have global reach. In 2013 combined, Linde, Air Liquide, Praxair and Air Products comprise around an estimated 71% of the global industrial gas market. For the same date the cumulative sales of the big four companies of the sector totaled to USD 61 billion, thus the total market size of the industrial gases can be estimated to be equal to around USD 85.9 billion.

It is estimated that the total market size of the big four companies will reach to USD 71 billion in 2016, growing by the CAGR equal to 5.6% in the period of 2010-2016. In 2013 Air Liquide lost 0.66% of its market share while Linde increased its market share by 0.36% thus becoming the leader of the big four by its market size, exceeding the Air Liquide’s market size by 9.4%. For the period of 2010-2013 Linde was the only company among the big four companies that had a stable growth of its market share, while all the big four companies have estimated stable growth of their market size for the periodof 2014-2016.

14,541 15,579

17,266 18,820 18,888

20,024 21,355

15,241 16,336

17,318 17,204 17,695 18,521

19,457

11,431 12,715 12,683 13,475 14,120

15,300 16,639

10,199 11,393 10,684 11,503 11,996 12,708

13,663

9.0%

3.4%

5.3%

2.8%

6.1%

6.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

-

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014E 2015E 2016E

Annual sales of big four companies, USD million

Linde Air Liquide Praxair Air products Growth rate of the total salesSource: Jefferies, company dataNote: FX rate used 1 EUR = 1.13 USD

Estimated values

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 12

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

In 2014 the emerging markets accounted for 34% of the global industrial gas market

Industrial gasesMarket overview

Source: Societe Generale, Cross Asset Research, 25 September 2014

Source: Capital IQ

Key ratios for industrial gas industryAs of 26 January 2015Net Income Margin % 4.4%Total Asset Turnover 0.6xCurrent Ratio 1.4xInventory turnover 9.5xAverage Days Sales Outstanding 68.7Total Debt/Equity 61.3%Total liabilities/Total Assets 50.1%Net Income, 2 Year Growth % (1.0%)Gross Profit, 1 Year Growth % 1.3%Cash from Operations, 1 Year Growth % 4.8%

Source: Societe Generale, Cross Asset Research, 25 September 2014

According to the Societe Generale cross assetresearch, most end markets of the industrial gases arequite cyclical, nevertheless the industrial gas majors arenot widely influenced by the pricing cycles of theircustomers due to the signed pricing contracts.

The industry has become increasingly global, as growth in emerging markets has been around twice the rate of that in major western markets.

According to the Synopsis of Chemicals report dated 25 September 2014, in 2014 the emerging markets accounted for the following shares in the corresponding big four companies’ market sizes; Air Liquide (22%),Linde (36%), Air products (38%), Praxair (38%). For the same date the emerging markets accounted for the 34% of the global market size of the industrial gas sector.

10%

10%

3%

5%

7%

11%26%

28%

Geographic breakdown of the market, 2013

Developing Asia

China

C/E Europe

Africa/ME/Other

S/C America

Japan

W. Europe

US/Canada

25%

1%

13%

10%9%

13%

8%

13%

8%

Global gases industry by end-market (%), 2013

Manufacturing

Glass

Metals

Healthcare

Food and beverages

Energy

Electronics

Chemicals

Other

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 13

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

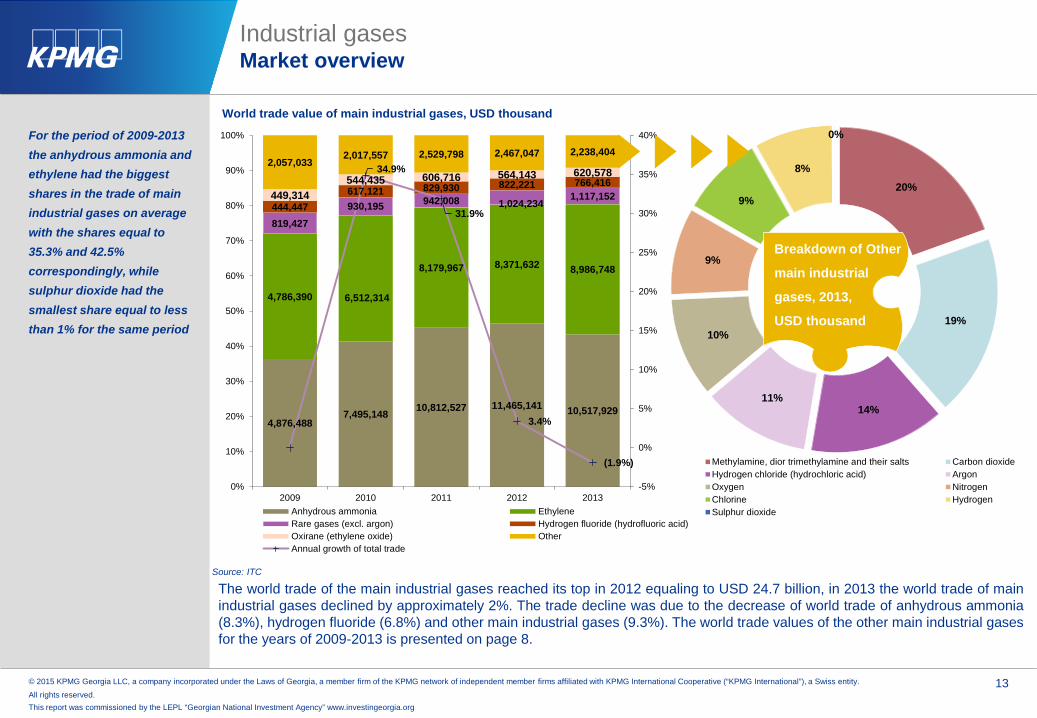

4,876,488 7,495,148 10,812,527 11,465,141 10,517,929

4,786,390 6,512,314

8,179,967 8,371,632 8,986,748

819,427 930,195 942,008 1,024,234

1,117,152 444,447

617,121 829,930 822,221 766,416 449,314

544,435 606,716 564,143 620,578 2,057,033

2,017,557 2,529,798 2,467,047 2,238,404 34.9%

31.9%

3.4%

(1.9%)

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013

World trade value of main industrial gases, USD thousand

Anhydrous ammonia EthyleneRare gases (excl. argon) Hydrogen fluoride (hydrofluoric acid)Oxirane (ethylene oxide) OtherAnnual growth of total trade

20%

19%

14%11%

10%

9%

9%

8%

0%

Methylamine, dior trimethylamine and their salts Carbon dioxideHydrogen chloride (hydrochloric acid) ArgonOxygen NitrogenChlorine HydrogenSulphur dioxide

For the period of 2009-2013 the anhydrous ammonia and ethylene had the biggest shares in the trade of main industrial gases on average with the shares equal to 35.3% and 42.5% correspondingly, while sulphur dioxide had the smallest share equal to less than 1% for the same period

Industrial gasesMarket overview

Source: ITC

The world trade of the main industrial gases reached its top in 2012 equaling to USD 24.7 billion, in 2013 the world trade of mainindustrial gases declined by approximately 2%. The trade decline was due to the decrease of world trade of anhydrous ammonia(8.3%), hydrogen fluoride (6.8%) and other main industrial gases (9.3%). The world trade values of the other main industrial gasesfor the years of 2009-2013 is presented on page 8.

Breakdown of Other

main industrial

gases, 2013,

USD thousand

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 14

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

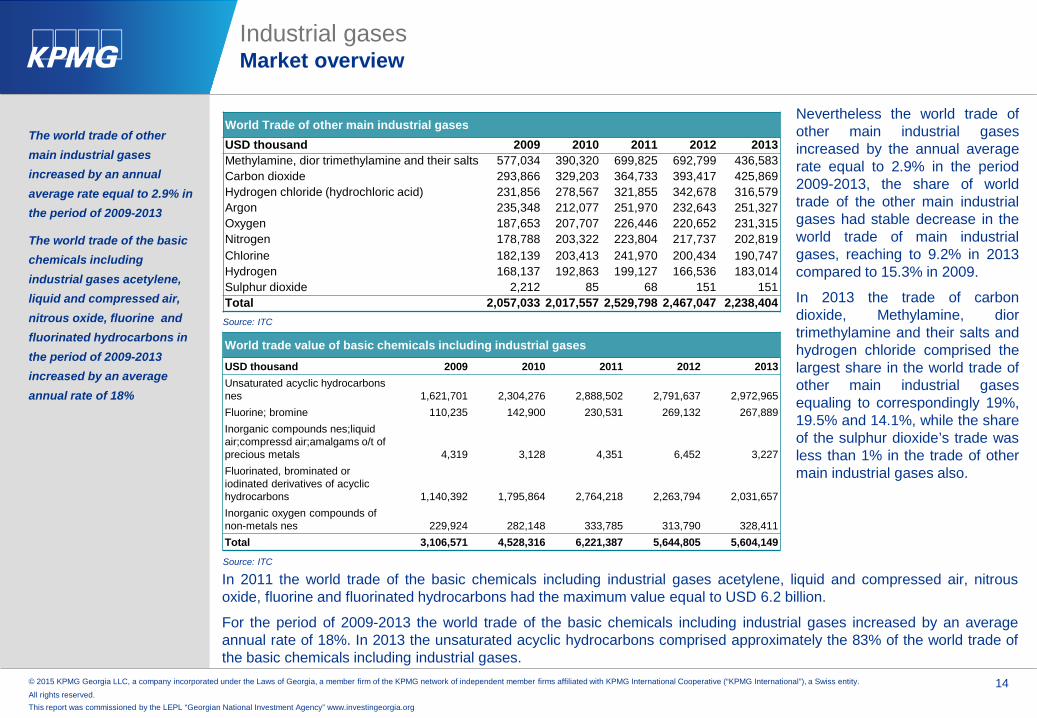

The world trade of other main industrial gases increased by an annual average rate equal to 2.9% in the period of 2009-2013

The world trade of the basic chemicals including industrial gases acetylene, liquid and compressed air, nitrous oxide, fluorine and fluorinated hydrocarbons in the period of 2009-2013 increased by an average annual rate of 18%

Industrial gasesMarket overview

Source: ITC

Nevertheless the world trade ofother main industrial gasesincreased by the annual averagerate equal to 2.9% in the period2009-2013, the share of worldtrade of the other main industrialgases had stable decrease in theworld trade of main industrialgases, reaching to 9.2% in 2013compared to 15.3% in 2009.

In 2013 the trade of carbondioxide, Methylamine, diortrimethylamine and their salts andhydrogen chloride comprised thelargest share in the world trade ofother main industrial gasesequaling to correspondingly 19%,19.5% and 14.1%, while the shareof the sulphur dioxide’s trade wasless than 1% in the trade of othermain industrial gases also.

World Trade of other main industrial gasesUSD thousand 2009 2010 2011 2012 2013Methylamine, dior trimethylamine and their salts 577,034 390,320 699,825 692,799 436,583Carbon dioxide 293,866 329,203 364,733 393,417 425,869Hydrogen chloride (hydrochloric acid) 231,856 278,567 321,855 342,678 316,579Argon 235,348 212,077 251,970 232,643 251,327Oxygen 187,653 207,707 226,446 220,652 231,315Nitrogen 178,788 203,322 223,804 217,737 202,819Chlorine 182,139 203,413 241,970 200,434 190,747Hydrogen 168,137 192,863 199,127 166,536 183,014Sulphur dioxide 2,212 85 68 151 151Total 2,057,033 2,017,557 2,529,798 2,467,047 2,238,404

Source: ITC

In 2011 the world trade of the basic chemicals including industrial gases acetylene, liquid and compressed air, nitrousoxide, fluorine and fluorinated hydrocarbons had the maximum value equal to USD 6.2 billion.

For the period of 2009-2013 the world trade of the basic chemicals including industrial gases increased by an averageannual rate of 18%. In 2013 the unsaturated acyclic hydrocarbons comprised approximately the 83% of the world trade ofthe basic chemicals including industrial gases.

World trade value of basic chemicals including industrial gases

USD thousand 2009 2010 2011 2012 2013Unsaturated acyclic hydrocarbons nes 1,621,701 2,304,276 2,888,502 2,791,637 2,972,965Fluorine; bromine 110,235 142,900 230,531 269,132 267,889Inorganic compounds nes;liquidair;compressd air;amalgams o/t of precious metals 4,319 3,128 4,351 6,452 3,227Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons 1,140,392 1,795,864 2,764,218 2,263,794 2,031,657Inorganic oxygen compounds of non-metals nes 229,924 282,148 333,785 313,790 328,411Total 3,106,571 4,528,316 6,221,387 5,644,805 5,604,149

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 15

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

For the period of 2009-2013 Armenia, Georgia and Azerbaijan had insignificant shares in the regional export of both main industrial gases and basic chemicals including industrial gases

Industrial gasesMarket overview

Source: ITC Source: ITC

Source: ITC Source: ITC

The main importing countries of the main industrial gases in the region in 2013 were Turkey, Ukraine and Russiacomprising correspondingly 74%, 18.8% and 5.6% of the region import in 2013. In 2013 Russia was the main importingcountry of the basic chemicals including industrial gases in the region with the regional share of 88%

The exporting countries of the main industrial gases in the region in 2013 were Russia, Ukraine and Turkey comprising70.1%, 27.9% and 2.1% of the region export in 2013 respectively.

In 2013 Russia, Turkey and Ukraine were the main exporting countries of the basic chemicals including industrial gases inthe region with the regional shares of 70.9%, 21.4% and 7.4% correspondingly. Georgia had a share of export equal to0.3%.

Regional Import value of main industrial gases

USD thousand 2009 2010 2011 2012 2013Russia 13,897 12,214 18,468 24,910 28,353Ukraine 28,262 21,903 23,961 19,717 95,490Georgia 743 1,010 897 1,491 2,338Armenia 830 667 904 1,123 914Turkey 246,794 350,712 475,596 400,732 375,715Azerbaijan 1,532 2,297 4,762 4,181 4,921Total 292,058 388,803 524,588 452,154 507,731

Regional export value of main industrial gases

USD thousand 2009 2010 2011 2012 2013Russia 707,783 803,556 1,661,871 1,564,896 1,649,853Ukraine 117,383 406,500 633,815 668,917 656,263Georgia 234 425 642 513 333Armenia 8 1 13 - -Turkey 20,576 26,101 85,526 108,683 48,515Azerbaijan 35 25 - 4 -Total 846,019 1,236,608 2,381,867 2,343,013 2,354,964

Regional Import value of basic chemicals including industrial gases

USD thousand 2009 2010 2011 2012 2013Russia 20,520 39,980 51,595 56,197 52,754Ukraine 1,167 2,092 10,601 7,574 6,370Georgia 176 400 789 1,032 383Armenia 33 45 182 258 105Turkey 15,405 25,193 44,721 31,395 31,022Azerbaijan 69 55 416 164 293Total 37,370 67,765 108,304 96,620 90,927

Regional export value of basic chemicals including industrial gases

USD thousand 2009 2010 2011 2012 2013Russia 16,076 12,783 12,173 10,867 14,086Ukraine 1,259 3,005 2,860 1,638 1,472Georgia 23 1 - - 55Armenia 7 - 5 6 3Turkey 1,102 3,046 4,469 2,695 4,260Azerbaijan - - - - -Total 18,467 18,835 19,507 15,206 19,876

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 16

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

55,48953,951

57,830

60,913

64,600

(2.8%)

7.2% 5.3% 6.1%

(4.0%)

(2.0%)

-

2.0%

4.0%

6.0%

8.0%

48,000

50,000

52,000

54,000

56,000

58,000

60,000

62,000

64,000

66,000

2008 2009 2010 2011 2012

Global consumption of industrial gases, USD million

global consumption volume growth rate

39%

32%

24%

5%

Global consumption of industrial gases by geography segmentation USD million, 2012

Asia-Pacific

Europe

Americas

Middle East & Africa

The compound annual growth rate of consumption in the period 2012–2017 is predicted to be 8%

Industrial gasesMarket overview

Source: Marketline Industry Profile, 2013Source: Marketline Industry Profile, 2013

The global industrial gases market has produced stable and good growth in recent years, after covering from contractionthat occurred in 2009. The market is expected to continue this trend through to the end of the forecast period in 2017.

In 2012 (the latest available data at the date of conducting research) Asia-Pacific accounted for 39.2% (USD 25.3 billion),Europe accounted for 31.6% (USD 20.4 billion), Americas accounted for 24% (USD 15.8 billion) and Middle East andAfrica accounted for 5% (USD 3.1 billion) of the global industrial gases consumption.

The global industrial gases consumption grew by 6.1% in 2012 to reach a value of USD 64,600 million.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 17

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

81,464

88,246

95,1138.3%

7.8%

7.5%7.6%7.7%7.8%7.9%8.0%8.1%8.2%8.3%8.4%

70,000

75,000

80,000

85,000

90,000

95,000

100,000

2015 2016 2017

Global consumption forecast of industrial gases, 2015-2017, USD million

global consumption forecast growth rate

In 2017 the global consumption of industrial gases will increase by 47.2% compared to 2012

Industrial gasesMarket overview

Source: Marketline Industry Profile, 2013

Main consuming countries for industrial gases areBelgium, Germany and France.

Below are presented the annual productionvolumes of the main industrial gases whichcomprise the 90.8% in the world trade of the mainindustrial gases. The annual production volume isalso presented which is presented in the basicchemicals including industrial gases and isincluded in the group called fluorine, bromine.The total trade of the fluorine bromine and themain industrial gases presented below comprisethe 80% of the total world trade of industrialgases.

In 2017, the global consumption of industrialgases is forecasted to have a value of USD95,113.1 million, an increase of 47.2% since2012.

Ammonia: Ammonia is being increasingly made in countries which have low cost sources of natural gas and coal(China and Russia account for ca 40%). The largest plants produce about 3000 tones a day and there are plans tobuild plants that produce 4000-5000 tones a day, which would mean that the total world output could be managed with100 such units. The annual world production volumes of ammonia is equal to 140 million tones, from which Europeaccounts for 16 million tones, North America 15 million tones, US 8 million tones, Asia 74 million tones, Russia 12.5million tones and Middle east 13 million tones.

Chlorine: The annual world production of chlorine is equal to 56 million tones, from which Europe accounts for 16million tones and North America 11 million tones.

Fluorine: The annual world production of fluorine is equal to 20 thousand tones, from which Europe accounts for 9thousand tones.

Hydrogen: The annual world production of hydrogen is equal to 50 million tones.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 18

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

The global annual production volume for industrial gases can be estimated to equal 310 million tones

Industrial gasesMarket overview

Hydrogen fluoride: The annual world production volumes of hydrogen fluoride is equal to 1 million tones, from whichEurope accounts for 240 thousand tones.

Rare gases: The annual world production of rare gases is equal to 704,510 tones, from which helium accounts for 4500tones, neon 1 tone, argon 700,000 tones, krypton 8 tones and xenon 0.6 tone.

Given that the world trade of the above mentioned industrial gases comprise the 80% of the world trade of industrialgases, the global annual production volume for industrial gases can be estimated to equal 310 million tones.

According to the big four companies’ (Linde, Air Liquide, Praxair and Air products) company reports for the period of2010-2013 the world production value of industrial gases comprised 19,929 USD million.

According to the Helvea Baader Bank Group Equity Research Sector Report, the industrial gases companies havecurrently only a capacity utilization of 75% and there is optimizing potential. Thus the world capacity of industrial gasproduction can be estimated to equal to 414 million tones with the production value of 26,572 USD million.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 19

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesRaw materials

Raw major materials include:

Sulphuric acid

Ammonium nitrate

Nitrites; nitrates

Fluorspar

Sulphur

Potassium chloride

Calcium carbide

Methanol

Natural gas (liquefied and in gaseous state)

Magnesium chloride

Sodium Chloride,

Ethyl alcohol,

Hydroxylamine

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 20

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

The industrial gas industry differs from many other industries because its raw materials are primarily extracted from the atmosphere.The approximate volume

percentages of the main ingredients of the dry air are as follows:

78.1% nitrogen,

20.9% oxygen,

0.9 % argon,

carbon dioxide, neon, helium, krypton, hydrogen and xenon account for less one 1% of the dry air

Industrial gasesProduction chain

Air separation as the production chain of nitrogen, oxygen and rare gases including argon

Air intake1

Preliminary purification

2

Air is a mixture of nitrogen and oxygen. This accountsfor 99 %. The remainder consists of argon, carbon dioxide and other rare gases. Oxygen, nitrogen, argon, as well as the raregases neon, xenon and krypton are obtained fromthe air by the method of low temperature rectification.

1

Before the air is separated into its gaseous components, unwanted ingredients must be removed. These are filtered out,chemically absorbed of surfaces or frozen out.

2

Compression3

The air that has been sucked in is compressed at apressure of around 6 bar. Heat is created as a result(this effect is familiar from the bicycle pump).

3

The compressed air is first cooled down to a temperatureof minus 180°C. As it expands in the separationcolumns, it cools down still further (reversed bicyclepump effect). As a result it liquefies to some extent(the temperature being lower than the boiling point).

Preliminary cooling

4

4

Cooling and separating

By means of the separation column, the air is separated into its components. This is a purely physical process, not involving any chemical reactions. The liquid mixture of products trickles down to meet the rising stream of gas. The liquid collects on the trays of the column, and is penetrated by the vapor bubbles from beneath. Here it is oxygen preeminently, with its higher boiling point (-183 degrees C), which condenses out of the stream of gas. The drops of liquid, on the other hand, give rise for preference to evaporating nitrogen, with its lower boiling point of -196°C.Gaseous nitrogen collects, in consequence, at the top of the separation column, while liquid oxygen collects at the bottom of the column. The oxygen at the bottom is vaporized, while nitrogen in liquid form is introduced at the top of the column. This process is continued as long as is required to reach the desired level of purity.

5

5

With a view to obtaining the rare gases, the separation column of the air separation unit is equipped with additional aggregates for raw argon, a neon/helium mixture and a krypton/xenon mixture. These mixtures must be purified still further. In a modern air separationunit with a production capacity of 45,000 cubic meters of oxygen per hour, 1700 cubic meters of argonper hour and 91 cubic meters of rare gases (neon, krypton and xenon) per hour can be recovered.Of these, 60 to 85 % can be obtained in the form of high purity gases.

Rare gas recovery6

Compression7

The gas products oxygen and nitrogen are fed into a pipeline network at a pressure of 40 bar.

7

Filling8

6

Liquid oxygen, nitrogen and argon are filled into cryogenic tanks or road tankers or compressed to 300 bar, vaporized and filled into steel cylinders.

8

Source: Messer report: This is how air separation works

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 21

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Natural gas

Production chain for main industrial gases not produced by air separation

Main raw materials, key ratios for 2013

Chemical operationsAdditional industrial gases (besides the ones obtained by air separation) are obtained as co-products or by-products of other operations. Depending on what kind of industrial gas is produced, the chemical operations may vary, such as electrolysis, liquefaction and stripping, steam reforming, combustion, oxidation, smelter operations, etc.

Industrial gases

Ammonia

AmmoniasP/E 27.5xReturn on Assets % 2.4%Gross Margin % 56.4%SG&A Margin % 49.2%EBIT Margin % 3.1%Net Income Margin % 1.7%

Chlorine

Alkalis And Chlorine*P/E 26.2xReturn on Assets % N/AGross Margin % 38.0%SG&A Margin % 17.5%EBIT Margin % 8.1%Net Income Margin % 5.8%

Ethyl alcohol, methanol

AlcoholP/E 10.2xReturn on Assets % 5.0%Gross Margin % 9.8%SG&A Margin % 2.7%EBIT Margin % 7.1%Net Income Margin % 5.9%

Nitrogen

NitrogenP/E 19.8xReturn on Assets % 5.1%Gross Margin % 36.8%SG&A Margin % 20.3%EBIT Margin % 10.5%Net Income Margin % 6.8%

Salts

SaltsP/E 19.1xReturn on Assets % 2%Gross Margin % 22.9%SG&A Margin % 15.8%EBIT Margin % 5.9%Net Income Margin % (0.2%)

Oxygen

OxygenP/E 19.8xReturn on Assets % 5.1%Gross Margin % 36.8%SG&A Margin % 20.3%EBIT Margin % 10.5%Net Income Margin % 6.8%

Industrial gasesProduction chain (continued)

Sulphur

SulphurP/E 5xReturn on Assets % 5.9%Gross Margin % 32.3%SG&A Margin % 17%EBIT Margin % 10%Net Income Margin % 5.8%

Crude petroleum and natural gas P/E 14.8xReturn on Assets % 3%Gross Margin % 7.7%SG&A Margin % 4.8%EBIT Margin % 2.6%Net Income Margin % 1.9%

Industrial gasesP/E 19.9xReturn on Assets % 5.2%Gross Margin % 25.1%SG&A Margin % 16%EBIT Margin % 6.7%Net Income Margin % 4.3%

Source: (1) Cap IQ(2) Linde: Gases and Applications

Note: * Ratios for alkalis and chlorine are provided for February 2015 (data for 2013 is not available)

According to the Morgan Stanley research variable costs are primarily energy-related, either for the electricity used in the separation of atmospheric gases, or the purchase of natural gas for hydrogen extraction. The core businesses are asset-intensive, so capex/depreciation is a real expense, and maintenance capex can run 3-5% of revenue. Transportation fleets for merchant and packaged gas networks are also a major component of expense.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 22

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

The main price drivers are:

Cost of raw materials (mainly natural gas and energy for fulfilling different chemical processes),

Transportation costs of the industrial gases

Labor costs

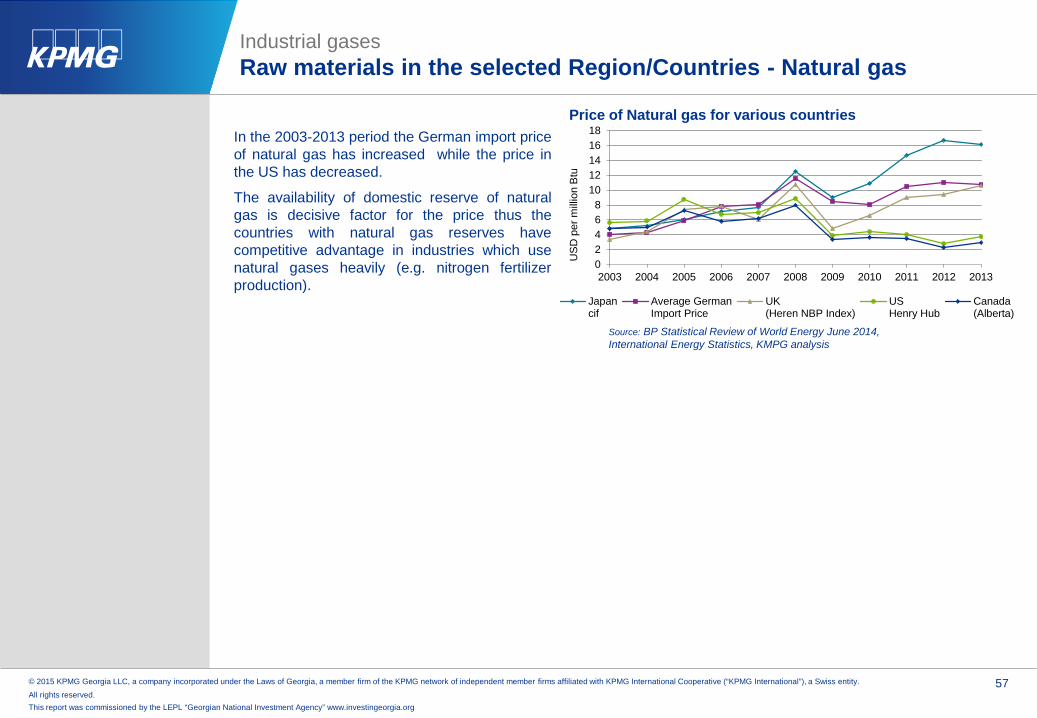

Industrial gasesPrice analysis

Prices, per unit of industrial gas, 2013

USD/ton Armenia Georgia Ukraine Turkey Azerbaijan Central Asia EURare gases (excl. argon) 61,500 29,231 43,494 49,476 38,625 11,826 24,376Carbon dioxide N/A 460 159 12,600 412 420 173Chlorine 1,088 764 271 611 941 685 265Ethylene N/A N/A 1,658 1,434 N/A N/A 1,463Hydrogen chloride (hydrochloric acid) 471 336 545 459 275 294 90Hydrogen fluoride (hydrofluoric acid) 1,500 N/A 1,504 1,296 N/A 4,373 1,980Methylamine, dior trimethylamine and their salts 1,500 N/A 2,570 1,251 N/A N/A 1,682Oxirane (ethylene oxide) N/A N/A 1,224 3,109 N/A 6,929 1,653Anhydrous ammonia 786 553 481 510 690 385 550Sulphur dioxide N/A N/A N/A N/A N/A N/A N/AHydrogen N/A N/A N/A N/A 2,880 2,350 1,709Oxygen 16,000 427 168 4,606 7,250 216 127Nitrogen N/A 31,000 134 25,000 1,588 459 N/AArgon 2,552 1,509 4,000 436 514 987 354Unsaturated acyclic hydrocarbons nes 18,000 2,000 2,134 7,000 7,000 2,600 1,750Fluorine; bromine N/A N/A N/A 39,667 N/A 885 1,807Inorganic compounds nes;liquidair;compressd air;amalgams o/t of precious metals N/A N/A N/A N/A N/A N/A N/AFluorinated, brominated or iodinated derivatives of acyclic hydrocarbons 11,500 4,246 5,107 4,633 6,483 6,130 5,810Inorganic oxygen compounds of non-metals nes 18,000 4,200 894 4,919 3,080 4,358 772Source: ITC

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 23

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Importer Countries

Global Top 20 Importer countries by value

EU (28 including Turkey)Top 20 Importer countries by value

CIS countries and Ukraine Import by value

Country Import Value (USD, thousands) Country Import Value

(USD, thousands) Country Import Value (USD, thousands)

1United States of

America 3,997,056 1 Belgium 3,178,043 1 Ukraine 95,4902 Belgium 3,178,043 2 Germany 1,439,535 2 Belarus 49,5793 China 2,602,501 3 France 1,002,580 3 Russian Federation 28,3534 Germany 1,439,535 4 Netherlands 692,951 4 Kazakhstan 21,5525 Korea, Republic of 1,130,318 5 Spain 653,562 5 Azerbaijan 4,9216 India 1,108,197 6 United Kingdom 578,547 6 Republic of Moldova 1,3947 France 1,002,580 7 Turkey 375,715 7 Armenia 9148 Indonesia 995,272 8 Italy 298,230 8 Kyrgyzstan 8669 Taipei, Chinese 859,544 9 Sweden 295,902 9 Uzbekistan 816

10 Netherlands 692,951 10 Finland 229,040 10 Tajikistan 72711 Spain 653,562 11 Czech Republic 130,95412 United Kingdom 578,547 12 Portugal 122,54313 Japan 431,628 13 Lithuania 95,27214 Morocco 406,339 14 Romania 92,22815 Turkey 375,715 15 Slovakia 72,59416 Thailand 366,337 16 Austria 66,30817 Italy 298,230 17 Denmark 49,31818 Sweden 295,902 18 Hungary 41,16919 Norway 285,753 19 Poland 38,35520 Finland 229,040 20 Ireland 18,243 Source: ITC

Note: In 2013 Georgian import of main industrial gases was USD 2,338 thousand.

Main Industrial gases, 2013

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 24

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Importer Countries

Global Top 20 Importer countries by value

EU (28 including Turkey)Top 20 Importer countries by value

CIS countries and Ukraine Import by value

Country Import Value (USD, thousands) Country Import Value

(USD, thousands) Country Import Value (USD, thousands)

1United States of

America 878,784 1 Belgium 679,010 1 Russian Federation 52,7542 Belgium 679,010 2 Netherlands 412,030 2 Ukraine 6,3703 Netherlands 412,030 3 France 327,732 3 Kazakhstan 3,9574 France 327,732 4 Germany 200,502 4 Belarus 3,3785 China 261,119 5 United Kingdom 184,363 5 Azerbaijan 2936 India 235,547 6 Italy 146,843 6 Uzbekistan 2797 Thailand 217,741 7 Spain 112,611 7 Republic of Moldova 1648 Canada 216,445 8 Austria 37,377 8 Armenia 1059 Korea, Republic of 208,311 9 Turkey 31,022 9 Kyrgyzstan 90

10 Germany 200,502 10 Czech Republic 23,832 10 Tajikistan 311 Japan 186,539 11 Poland 14,78212 United Kingdom 184,363 12 Sweden 14,01813 Italy 146,843 13 Hungary 13,65114 Singapore 144,877 14 Portugal 10,95215 Spain 112,611 15 Ireland 8,61316 Mexico 112,541 16 Finland 7,38017 Brazil 98,598 17 Slovakia 6,41118 Taipei, Chinese 95,643 18 Denmark 5,54219 Saudi Arabia 71,198 19 Greece 5,26520 Malaysia 67,847 20 Romania 4,036 Source: ITC

Note: In 2013 Georgian import of basic chemicals including main industrial gases was USD 383 thousand.

Basic chemicals including industrial gases, 2013

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 25

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Exporter Countries

Global Top 20 Exporter countries by value

EU (28 including Turkey)Top 20 Exporter countries by value

CIS countries and Ukraine Export by value

Country Export Value (USD, thousands) Country Export Value

(USD, thousands) Country Export Value (USD, thousands)

1 Trinidad and Tobago 2,347,886 1 Netherlands 1,895,802 1 Russian Federation 1,649,8532 Netherlands 1,895,802 2 United Kingdom 1,328,261 2 Ukraine 656,2633 Russian Federation 1,649,853 3 Germany 1,214,370 3 Kazakhstan 12,4234 Korea, Republic of 1,501,132 4 France 634,601 4 Uzbekistan 6,4275 United Kingdom 1,328,261 5 Belgium 532,628 5 Belarus 6306 Germany 1,214,370 6 Ireland 196,677 6 Kyrgyzstan 497 Japan 1,183,015 7 Italy 179,102 7 Tajikistan 198 Saudi Arabia 1,124,582 8 Poland 147,100 8 Republic of Moldova 189 Canada 1,107,889 9 Spain 145,246 9 Azerbaijan -

10United States of

America 809,934 10 Finland 128,700 Armenia -11 Ukraine 656,263 11 Portugal 122,72012 France 634,601 12 Czech Republic 77,86613 Belgium 532,628 13 Hungary 58,19414 Malaysia 407,261 14 Estonia 50,665

15United Arab

Emirates 395,454 15 Turkey 48,51516 Indonesia 377,119 16 Austria 41,53317 Australia 374,442 17 Sweden 38,24418 Algeria 329,650 18 Slovakia 13,06819 China 322,961 19 Romania 11,781

20Iran (Islamic Republic of) 282,583 20 Slovenia 8,811

Source: ITC

Note: In 2013 Georgian export of main industrial gases was USD 333 thousand.

Main Industrial gases, 2013

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 26

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Exporter Countries

Global Top 20 Exporter countries by value

EU (28 including Turkey)Top 20 Exporter countries by value

CIS countries and Ukraine Export by value

Country Export Value (USD, thousands) Country Export Value

(USD, thousands) Country Export Value (USD, thousands)

1United States of America 1,216,971 1 Belgium 668,741 1 Russian Federation 14,086

2 China 722,224 2 United Kingdom 237,844 2 Ukraine 1,4723 Belgium 668,741 3 Netherlands 219,581 3 Belarus 5424 South Africa 431,874 4 France 156,522 4 Armenia 35 United Kingdom 237,844 5 Germany 111,397 5 Kyrgyzstan 26 Netherlands 219,581 6 Spain 85,845 6 Kazakhstan 27 Japan 211,113 7 Italy 39,292 7 Tajikistan 08 Canada 206,106 8 Austria 35,417 8 Republic of Moldova 09 France 156,522 9 Estonia 19,294 9 Azerbaijan 0

10 Saudi Arabia 144,706 10 Czech Republic 16,972 10 Uzbekistan 011 Israel 139,946 11 Hungary 14,82412 Brazil 133,652 12 Portugal 9,52113 Germany 111,397 13 Sweden 7,00014 Spain 85,845 14 Finland 6,734

15United Arab Emirates 79,210 15 Denmark 4,591

16 Singapore 71,946 16 Turkey 4,26017 Jordan 57,017 17 Poland 4,12218 Italy 39,292 18 Slovakia 3,91119 Taipei, Chinese 39,014 19 Slovenia 2,04320 Austria 35,417 20 Lithuania 1,407

Source: ITC

Basic chemicals including industrial gases, 2013

Note: In 2013 Georgian export of basic chemicals including main industrial gases was USD55 thousand.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 27

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

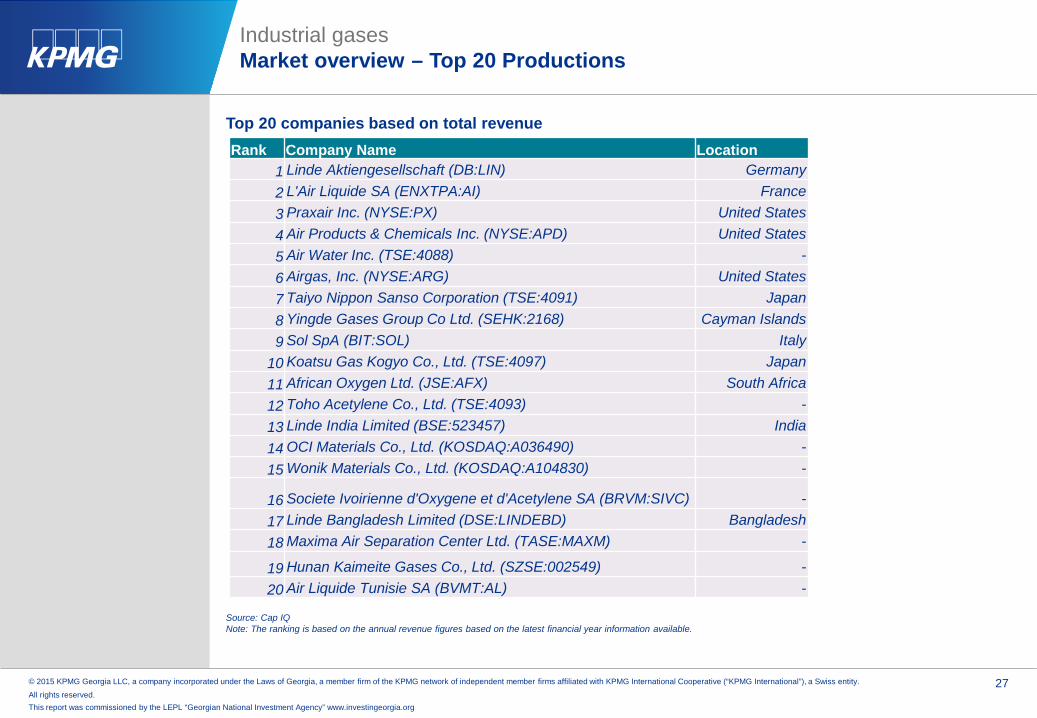

Industrial gasesMarket overview – Top 20 Productions

Top 20 companies based on total revenue Rank Company Name Location

1 Linde Aktiengesellschaft (DB:LIN) Germany2 L'Air Liquide SA (ENXTPA:AI) France3 Praxair Inc. (NYSE:PX) United States4 Air Products & Chemicals Inc. (NYSE:APD) United States5 Air Water Inc. (TSE:4088) -6 Airgas, Inc. (NYSE:ARG) United States7 Taiyo Nippon Sanso Corporation (TSE:4091) Japan8 Yingde Gases Group Co Ltd. (SEHK:2168) Cayman Islands9 Sol SpA (BIT:SOL) Italy

10 Koatsu Gas Kogyo Co., Ltd. (TSE:4097) Japan11 African Oxygen Ltd. (JSE:AFX) South Africa12 Toho Acetylene Co., Ltd. (TSE:4093) -13 Linde India Limited (BSE:523457) India14 OCI Materials Co., Ltd. (KOSDAQ:A036490) -15 Wonik Materials Co., Ltd. (KOSDAQ:A104830) -

16 Societe Ivoirienne d'Oxygene et d'Acetylene SA (BRVM:SIVC) -17 Linde Bangladesh Limited (DSE:LINDEBD) Bangladesh18 Maxima Air Separation Center Ltd. (TASE:MAXM) -

19 Hunan Kaimeite Gases Co., Ltd. (SZSE:002549) -20 Air Liquide Tunisie SA (BVMT:AL) -

Source: Cap IQNote: The ranking is based on the annual revenue figures based on the latest financial year information available.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 28

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Importer companies

Top 20 anhydrous ammonia importer companies based on number of product or service categories traded Rank Company Name Location

1 Univar France2 Coger France3 Mash Traders United Arab Emirates4 Chemlink LLC United Arab Emirates5 Cadilhac Morocco6 Simar, S.A. Spain7 Produits Chimiques Maghreb Morocco8 CRISTIAN GRUP S.R.L. Romania9 Merck (Schweiz) AG Switzerland

10 Linegal Chemicals Sp. z o.o. Poland11 BRENNTAG S.R.L. Romania12 Compagnie de Produits Chimiques du Maroc Morocco13 Kresry NV Belgium14 Brenntag Nordic AS Norway15 Eltachem Maroc s.a.r.l. Morocco16 IMPAG AG Switzerland17 Baum-Lux Russian Federation18 Univar AB Sweden19 Univar Oy Finland20 Chemia-Lublin SA Przedsiebiorstwo Handlowe Poland

Source: ITCNote: The top companies are illustrated for those industrial gases which have considerable share in the world trade

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 29

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Importer companies

Top 20 ethylene importer companies based on number of product or service categories traded Rank Company Name Location

1 Univar France2 Mash Traders United Arab Emirates3 Chemlink LLC United Arab Emirates4 Simar, S.A. Spain5 CRISTIAN GRUP S.R.L. Romania6 Kemat Belgium Polybutenes SA-NV Belgium7 IMPAG AG Switzerland8 Poisson Saint Eloi France9 VWR International BVBA Belgium

10 Acros Organics BVBA Belgium11 Diemer, S.L. Spain12 Rit-Chem Co Inc United States of America13 Radiation Dynamics, Inc. United States of America14 Merck Oy Finland15 Kodox, S.L. Spain16 The National Chemical Co Ltd Ireland17 HELM AG Germany18 Emirates Industrial Gases Co LLC United Arab Emirates19 AIR PRODUCTS Sp. z o.o. Poland20 HELM AG Germany

Source: ITCNote: The top companies are illustrated for those industrial gases which have considerable share in the world trade

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 30

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Exporter companies

Top 20 anhydrous ammonia exporter companies based on number of product or service categories traded Rank Company Name Location

1 Univar France2 Coger France3 Mash Traders United Arab Emirates4 Chemlink LLC United Arab Emirates5 Simar, S.A. Spain6 Produits Chimiques Maghreb Morocco7 Denies NV-SA Belgium8 Linegal Chemicals Sp. z o.o. Poland9 Sophyc France

10 Compagnie de Produits Chimiques du Maroc Morocco11 Kresry NV Belgium12 Univar Oy Finland13 Chemia-Lublin SA Przedsiebiorstwo Handlowe Poland14 Russtail Trade Company Russian Federation15 H.C.I. Chemicals Nederland BV Netherlands16 Brenntag Nordic Oy Finland17 Metrac NV Belgium18 Chemikolor SA Przedsiebiorstwo Uslugowo-Handlowe Poland19 Algol Chemicals ApS Denmark20 Algol Chemicals Oy Finland

Source: ITCNote: The top companies are illustrated for those industrial gases which have considerable share in the world trade

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 31

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesMarket overview – Top 20 Exporter companies

Top 20 ethylene exporter companies based on number of product or service categories traded Rank Company Name Location

1 Univar France2 Mash Traders United Arab Emirates3 Chemlink LLC United Arab Emirates4 Simar, S.A. Spain5 Denies NV-SA Belgium6 DuPont Performance Elastomers, LLC United States of America7 Kemat Belgium Polybutenes SA-NV Belgium8 Dow Chemical Company United States of America9 Sophyc France

10 Anti-Seize Technology United States of America11 Dedert Corp. United States of America12 Dow Chemical Canada Inc. Canada13 Poisson Saint Eloi France14 VWR International BVBA Belgium15 Timminco Limited Canada16 ANGUS Chemical Co. United States of America17 Chemfil Canada Limited Canada18 Bio Chambers Incorporated Canada19 Acros Organics BVBA Belgium20 Methanex Corporation Canada

Source: ITCNote: The top companies are illustrated for those industrial gases which have considerable share in the world trade

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 32

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

In 2014 Georgia was mainly importing industrial gases from Turkey (52%) and the import value was equal to USD 1 million. The mostly imported industrial gas in 2013 was anhydrous ammonia.

Industrial gasesGeorgia - industrial gas import

Source: ITC

Industrial gas import structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) 98 178 36 131 296Carbon dioxide 10 34 64 138 295Chlorine 424 549 390 398 489Ethylene - - - - -Hydrogen chloride (hydrochloric acid) 158 188 250 106 125Hydrogen fluoride (hydrofluoric acid) - 3 7 2 5Methylamine, dior trimethylamine and their salts - - - - -Oxirane (ethylene oxide) - - - - -Anhydrous ammonia - - - 578 876Sulphur dioxide - - - - -Hydrogen - - 14 12 14Oxygen 4 1 8 36 41Nitrogen 12 17 7 10 31Argon 37 40 121 80 166Total 743 1,010 897 1,491 2,338Unsaturated acyclic hydrocarbons nes - - 1 3 2Fluorine; bromine - - - - -Inorganic compounds nes;liquidair;compressd air;amalgams o/tof precious metals - - - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons 173 391 774 967 276Inorganic oxygen compounds of non-metals nes 3 9 14 62 105Total 176 400 789 1,032 383

Source: ITC

Source: ITC

1,010 897

1,491

2,338

1,711

400

789

1,032

383 300

-

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014

Import of industrial gases in 2009 - 2014, USD thousand

Import of main industrial gases Import of basic chemicals including industrial gases

52%

9%

1%

6%

2%1%

3%

5%

12%

2%7%

Industrial gas importer structure by countries, 2014

Turkey

United Arab Emirates

United Kingdom

Ukraine

Germany

Estonia

Russian Federation

India

Iran (Islamic Republic of)

Armenia

Other

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 33

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

425

642

513

333395

1 - -55

-0

100

200

300

400

500

600

700

2010 2011 2012 2013 2014

Export of industrial gases in 2010 - 2014, USD thousand

Export of main industrial gases Export of basic chemicals including industrial gases

In 2013 the total export of industrial gases was equal to USD 388 thousand

In 2014 Georgia was mainly exporting industrial gases to Azerbaijan (88%) and the export value was equal to USD 353 thousand. The mostly exported industrial gas in 2013 was carbon dioxide

Industrial gasesGeorgia - industrial gas export

Source: ITC

Industrial gas export structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) 5 - - - -Carbon dioxide 48 128 235 226 259Anhydrous ammonia 181 286 371 241 65Chlorine - 3 0 0 1Ethylene - - - - -Hydrogen chloride (hydrochloric acid) - 6 22 27 8Hydrogen fluoride (hydrofluoric acid) - - - - -Methylamine, dior trimethylamine and their salts - - - - -Oxirane (ethylene oxide) - - - - -Sulphur dioxide - - - - -Hydrogen - - - - -Oxygen - - 11 - -Nitrogen - 1 3 - -Argon - 1 - 19 -Total 234 425 642 513 333Unsaturated acyclic hydrocarbons nes - - - - -Fluorine; bromine - - - - -Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals - - - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons - - - - 3Inorganic oxygen compounds of non-metals nes 23 1 - - 52Total 23 1 - - 55

88%

12%

Industrial gas export structure by countries, 2014

Azerbaijan Armenia

Source: ITC

Source: ITC

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 34

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

In 2013 the total production of oxygen and carbon dioxide increased by 2.9%, while the total consumption of the same gases increased by 5.7% for the same period

Industrial gasesGeorgia - industrial gas production and consumption

Due to insignificant level of industrial gas production in Georgia, the National statistical office of Georgia does notprovide information regarding all the industrial gas production volumes and only data for the production volumes ofoxygen and carbon dioxide is available for the period of 2012-2014 September.

8,977 9,344

7,038

9,372 9,538

7,009

-

2,000

4,000

6,000

8,000

10,000

12,000

2012 2013 2014 January-September

Production of industrial gases, tons

Oxygen Carbon dioxide

9,167

9,536

8,452

9,096

7,800

8,000

8,200

8,400

8,600

8,800

9,000

9,200

9,400

9,600

9,800

2012 2013

Consumption of industrial gases, tons

Oxygen Carbon dioxide

Source: National statistical office of Georgia Source: National statistical office of Georgia, KPMG calculations

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 35

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

In 2013 Armenia was mainly importing industrial gases from Iran (43%) and the import value was equal to USD 438 thousand. The mostly imported industrial gas in 2013 was chlorine.

Industrial gasesArmenia - industrial gas import

Source: ITC

Source: ITC

Source: ITC

Industrial gas import structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) 30 82 32 70 123Carbon dioxide 3 32 26 11 7Chlorine 279 286 312 367 285Ethylene - - - 4 -Hydrogen chloride (hydrochloric acid) 57 69 208 201 168Hydrogen fluoride (hydrofluoric acid) 16 2 4 8 6Methylamine, dior trimethylamine and their salts 3 2 - - 3Oxirane (ethylene oxide) 9 8 - 5 4Anhydrous ammonia 60 48 163 197 33Sulphur dioxide - - - - -Hydrogen - 1 1 - -Oxygen 5 5 23 88 16Nitrogen 5 2 27 4 1Argon 363 130 108 168 268Total 830 667 904 1,123 914Unsaturated acyclic hydrocarbons nes 16 5 19 102 18Fluorine; bromine - - - - -Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals - - - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons 13 26 132 52 69Inorganic oxygen compounds of non-metals nes 4 14 31 104 18Total 33 45 182 258 105

830

667

904

1,123

914

33 45

182258

105

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013

Import of industrial gases in 2009 - 2013, USD thousand

Import of main industrial gases Import of basic chemicals including industrial gases

4%4%

9%

6%

18%

43%

3%

4%

9%

Industrial gas importer structure by countries, 2013

Poland

United Arab Emirates

Ukraine

Russian Federation

Germany

Iran (Islamic Republic of)

Georgia

Turkey

Other

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 36

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

Industrial gasesArmenia - industrial gas export

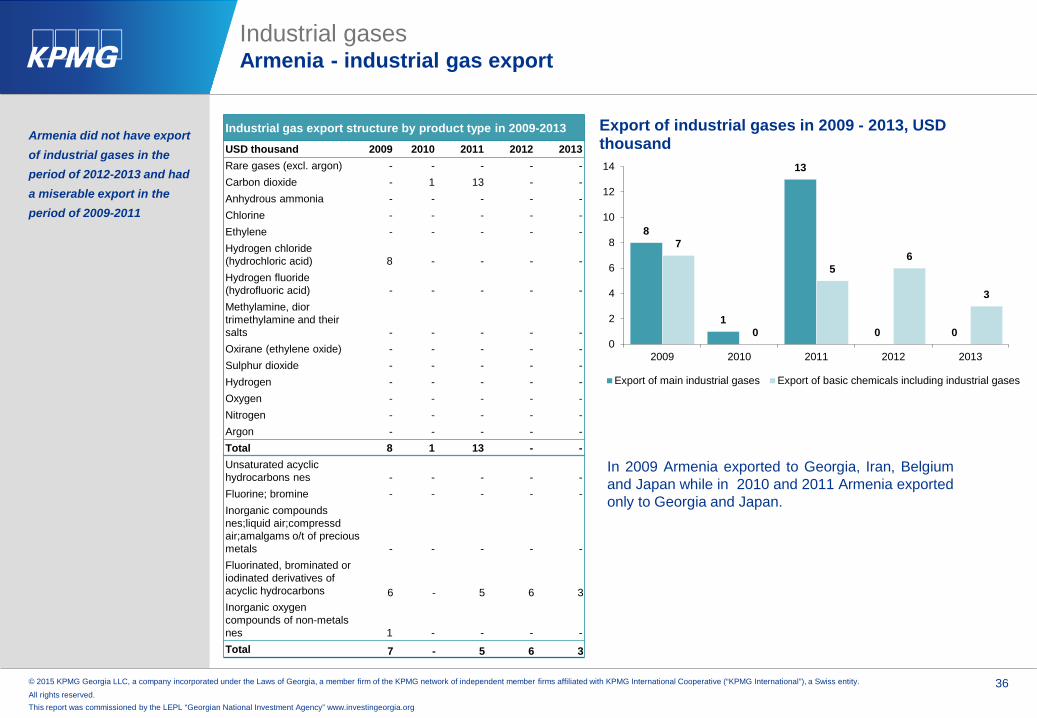

Industrial gas export structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) - - - - -Carbon dioxide - 1 13 - -Anhydrous ammonia - - - - -Chlorine - - - - -Ethylene - - - - -Hydrogen chloride (hydrochloric acid) 8 - - - -Hydrogen fluoride (hydrofluoric acid) - - - - -Methylamine, dior trimethylamine and their salts - - - - -Oxirane (ethylene oxide) - - - - -Sulphur dioxide - - - - -Hydrogen - - - - -Oxygen - - - - -Nitrogen - - - - -Argon - - - - -Total 8 1 13 - -Unsaturated acyclic hydrocarbons nes - - - - -Fluorine; bromine - - - - -Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals - - - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons 6 - 5 6 3Inorganic oxygen compounds of non-metals nes 1 - - - -Total 7 - 5 6 3

Armenia did not have export of industrial gases in the period of 2012-2013 and had a miserable export in the period of 2009-2011

In 2009 Armenia exported to Georgia, Iran, Belgiumand Japan while in 2010 and 2011 Armenia exportedonly to Georgia and Japan.

8

1

13

0 0

7

0

5 6

3

0

2

4

6

8

10

12

14

2009 2010 2011 2012 2013

Export of industrial gases in 2009 - 2013, USD thousand

Export of main industrial gases Export of basic chemicals including industrial gases

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 37

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

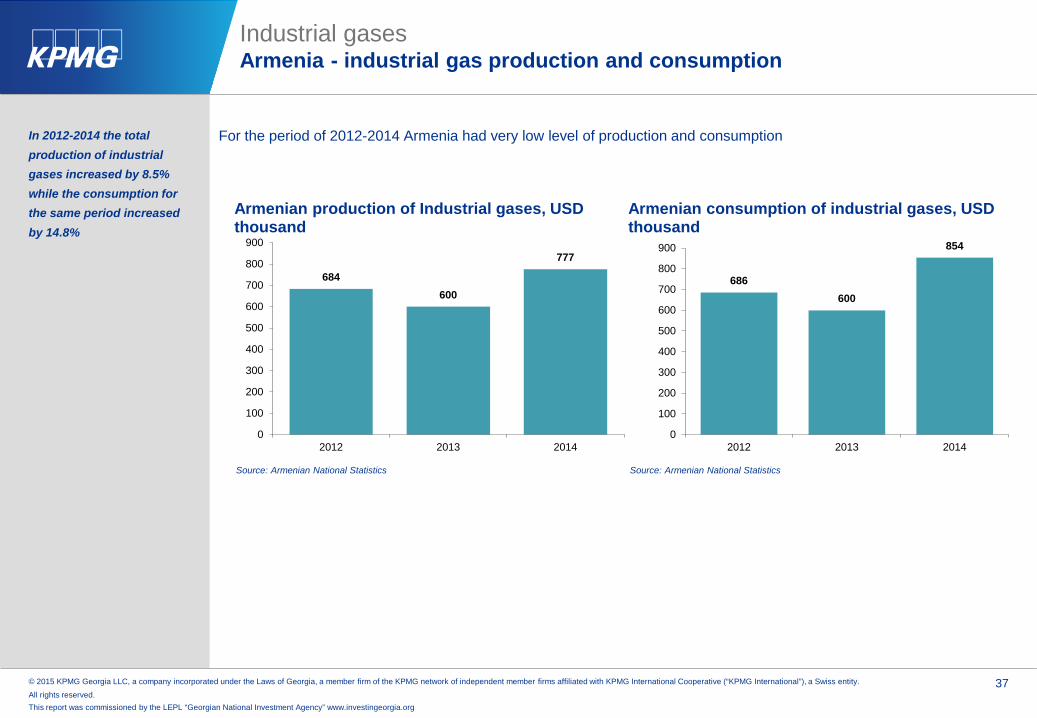

In 2012-2014 the total production of industrial gases increased by 8.5% while the consumption for the same period increased by 14.8%

Industrial gasesArmenia - industrial gas production and consumption

For the period of 2012-2014 Armenia had very low level of production and consumption

Source: Armenian National Statistics Source: Armenian National Statistics

684600

777

0

100

200

300

400

500

600

700

800

900

2012 2013 2014

Armenian production of Industrial gases, USD thousand

686600

854

0

100

200

300

400

500

600

700

800

900

2012 2013 2014

Armenian consumption of industrial gases, USD thousand

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 38

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

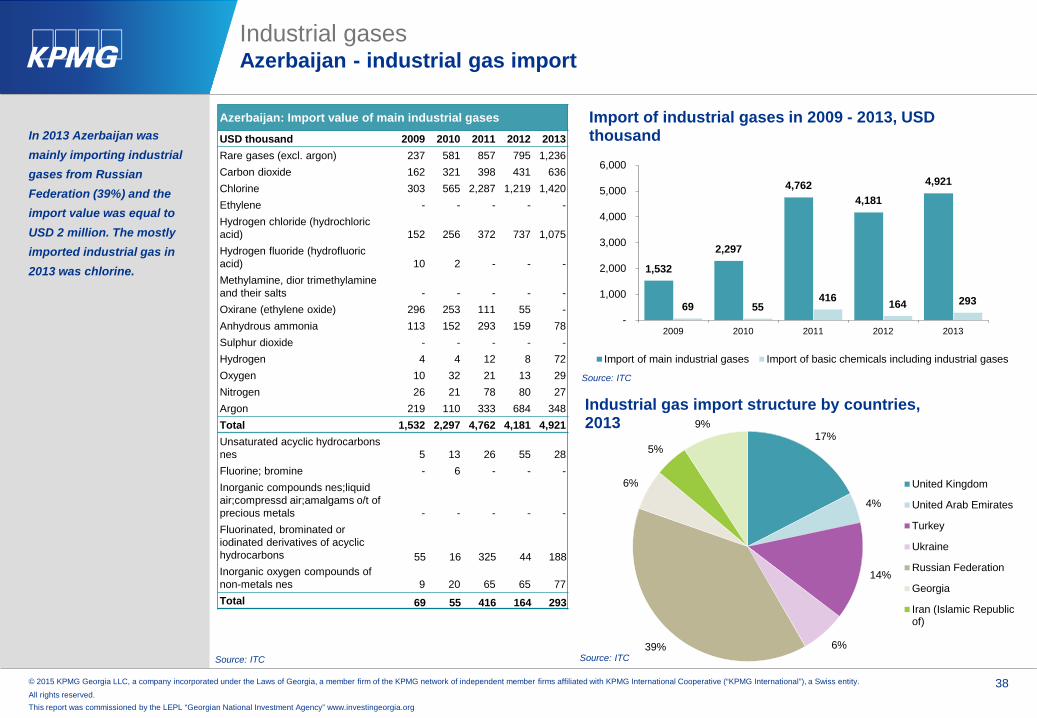

In 2013 Azerbaijan was mainly importing industrial gases from Russian Federation (39%) and the import value was equal to USD 2 million. The mostly imported industrial gas in 2013 was chlorine.

Industrial gasesAzerbaijan - industrial gas import

Source: ITC

1,532

2,297

4,762 4,181

4,921

69 55 416 164 293

-

1,000

2,000

3,000

4,000

5,000

6,000

2009 2010 2011 2012 2013

Import of industrial gases in 2009 - 2013, USD thousand

Import of main industrial gases Import of basic chemicals including industrial gases

Source: ITC

Source: ITC

Azerbaijan: Import value of main industrial gases

USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) 237 581 857 795 1,236Carbon dioxide 162 321 398 431 636Chlorine 303 565 2,287 1,219 1,420Ethylene - - - - -Hydrogen chloride (hydrochloric acid) 152 256 372 737 1,075Hydrogen fluoride (hydrofluoric acid) 10 2 - - -Methylamine, dior trimethylamine and their salts - - - - -Oxirane (ethylene oxide) 296 253 111 55 -Anhydrous ammonia 113 152 293 159 78Sulphur dioxide - - - - -Hydrogen 4 4 12 8 72Oxygen 10 32 21 13 29Nitrogen 26 21 78 80 27Argon 219 110 333 684 348Total 1,532 2,297 4,762 4,181 4,921Unsaturated acyclic hydrocarbons nes 5 13 26 55 28Fluorine; bromine - 6 - - -Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals - - - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons 55 16 325 44 188Inorganic oxygen compounds of non-metals nes 9 20 65 65 77Total 69 55 416 164 293

17%

4%

14%

6%39%

6%

5%

9%

Industrial gas import structure by countries, 2013

United Kingdom

United Arab Emirates

Turkey

Ukraine

Russian Federation

Georgia

Iran (Islamic Republicof)

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 39

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

In 2013 Azerbaijan didn’t export industrial gases

Industrial gasesAzerbaijan - industrial gas export

Source: ITC

Industrial gas export structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) - 25 - - -Carbon dioxide 1 - - - -Anhydrous ammonia - - - - -Chlorine 28 - - - -Ethylene - - - - -Hydrogen chloride (hydrochloric acid) - - - - -Hydrogen fluoride (hydrofluoric acid) - - - - -Methylamine, dior trimethylamine and their salts - - - - -Oxirane (ethylene oxide) - - - - -Sulphur dioxide - - - - -Hydrogen - - - - -Oxygen - - - - -Nitrogen 6 - - 4 -Argon - - - - -Total 35 25 - 4 -Unsaturated acyclic hydrocarbons nes - - - - -Fluorine; bromine - - - - -Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals - - - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons - - - - -Inorganic oxygen compounds of non-metals nes - - - - -Total - - - - -

35

25

0

4

00

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013

Export of main industrial gases, 2009-2013, USD thousand

Source: ITC

For the period of 2009-2013 Azerbaijan didn’t exportbasic chemicals including industrial gases.

In 2009 Azerbaijan exported only to Georgia, in 2010the country exported to France while in 2012Azerbaijan exported to United Kingdom.

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 40

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

In 2013 the production of industrial gases was 122 thousand tons

Industrial gasesAzerbaijan - industrial gas production and consumption

Source: State Statistical Committee of the Republic of Azerbaijan

The State Statistical Committee ofAzerbaijan provides information onproduction volumes of nitrogen, oxygen,liquid air, compressed air, chlorine,hydrogen chloride and ethylene. Both theimport and the export of ethylene is equalto zero, so the country’s consumption ofethylene is equal to the productionvolumes. For the period of 2009-2013 thetotal consumption of industrial gases(including ethylene) grew on overage by56%.

Nitrogen Oxygen Liquid air,compressed air Chlorine Hydrogen chloride Ethylene

2009 17,365 3,934 6,017 3,946 3,300 -2010 19,736 1,985 6,064 2,658 3,300 55,0082011 25,385 3,417 7,939 5,630 4,200 77,5752012 24,175 17,080 7 87 100 69,1572013 21,422 13,744 8,591 - - 78,469

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

Production of Industrial gases, 2009-2013, ton

2009

2010

2011

2012

2013

17,365 19,737 25,589 24,280 21,439

3,934 1,987

3,423

17,082 13,748 5,367 4,315 11,304

1,332 1,509 3,468 3,991 5,452 2,562 3,902

0%10%20%30%40%50%60%70%80%90%

100%

2009 2010 2011 2012 2013

Consumption of Industrial gases, 2009-2013, ton

Nitrogen Oxygen Chlorine Hydrogen chloride

Source: State Statistical Committee of the Republic of Azerbaijan, KPMG calculationsNote (2) liquid air, compressed air had different grouping in data sources, thus are not included in the consumption calculations

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 41

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

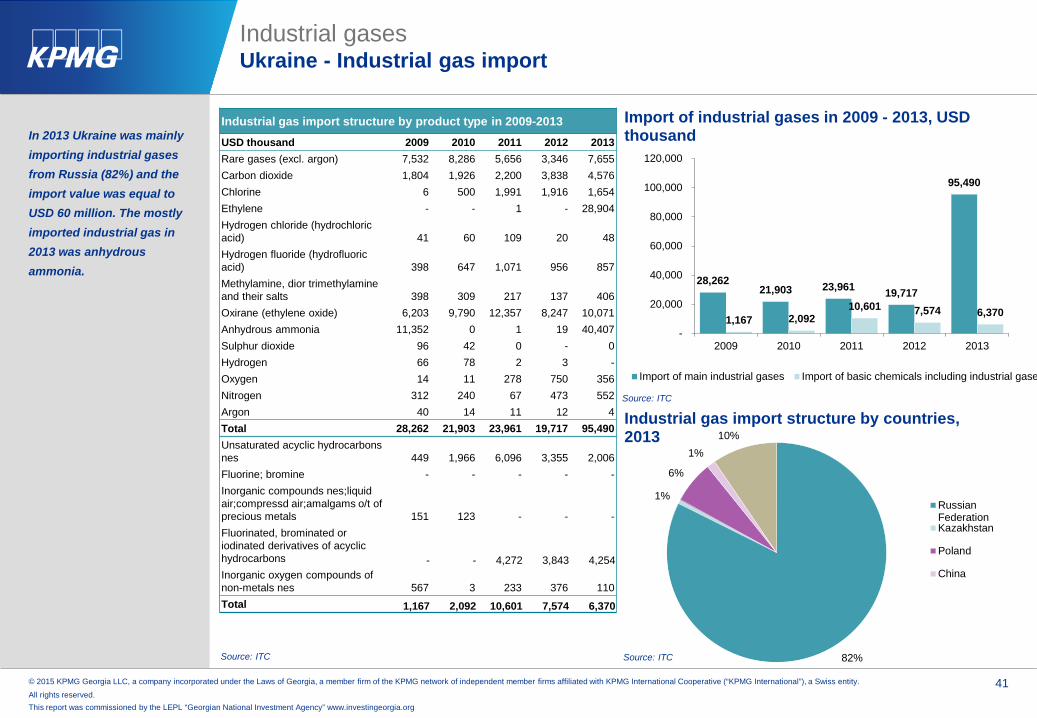

In 2013 Ukraine was mainly importing industrial gases from Russia (82%) and the import value was equal to USD 60 million. The mostly imported industrial gas in 2013 was anhydrous ammonia.

Industrial gasesUkraine - Industrial gas import

Source: ITC

Industrial gas import structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) 7,532 8,286 5,656 3,346 7,655Carbon dioxide 1,804 1,926 2,200 3,838 4,576Chlorine 6 500 1,991 1,916 1,654Ethylene - - 1 - 28,904Hydrogen chloride (hydrochloric acid) 41 60 109 20 48Hydrogen fluoride (hydrofluoric acid) 398 647 1,071 956 857Methylamine, dior trimethylamine and their salts 398 309 217 137 406Oxirane (ethylene oxide) 6,203 9,790 12,357 8,247 10,071Anhydrous ammonia 11,352 0 1 19 40,407Sulphur dioxide 96 42 0 - 0Hydrogen 66 78 2 3 -Oxygen 14 11 278 750 356Nitrogen 312 240 67 473 552Argon 40 14 11 12 4Total 28,262 21,903 23,961 19,717 95,490Unsaturated acyclic hydrocarbons nes 449 1,966 6,096 3,355 2,006Fluorine; bromine - - - - -Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals 151 123 - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons - - 4,272 3,843 4,254Inorganic oxygen compounds of non-metals nes 567 3 233 376 110Total 1,167 2,092 10,601 7,574 6,370

Source: ITC

Source: ITC

28,262 21,903 23,961 19,717

95,490

1,167 2,092 10,601 7,574 6,370

-

20,000

40,000

60,000

80,000

100,000

120,000

2009 2010 2011 2012 2013

Import of industrial gases in 2009 - 2013, USD thousand

Import of main industrial gases Import of basic chemicals including industrial gase

82%

1%

6%

1%10%

Industrial gas import structure by countries, 2013

RussianFederationKazakhstan

Poland

China

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 42

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

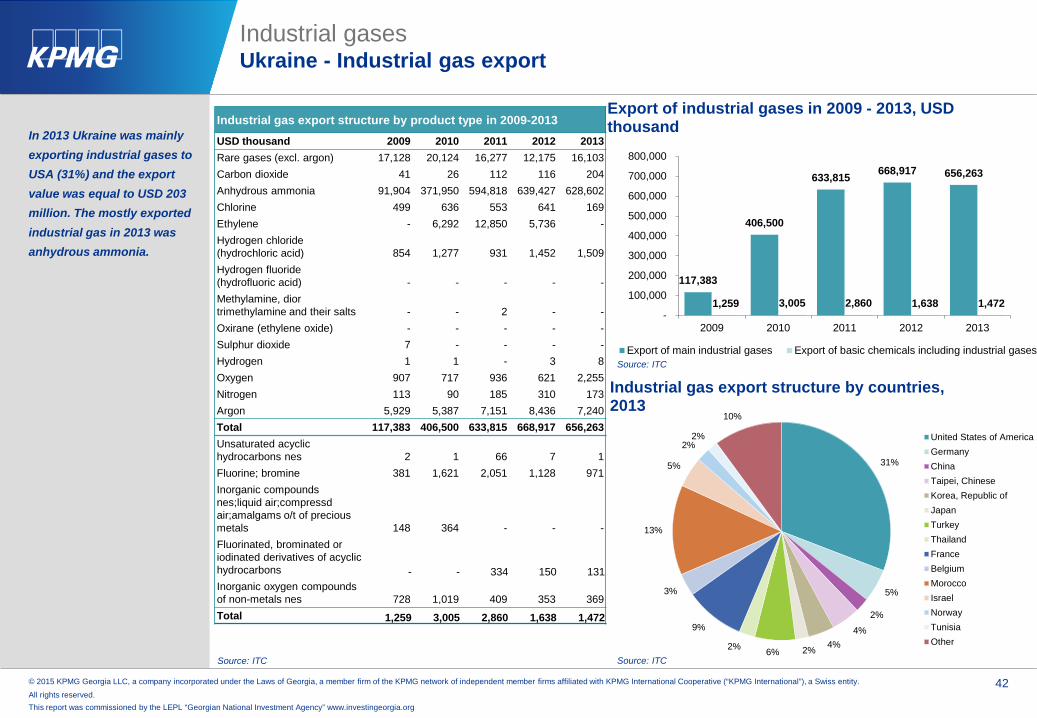

In 2013 Ukraine was mainly exporting industrial gases to USA (31%) and the export value was equal to USD 203 million. The mostly exported industrial gas in 2013 was anhydrous ammonia.

Industrial gasesUkraine - Industrial gas export

Source: ITC

Industrial gas export structure by product type in 2009-2013USD thousand 2009 2010 2011 2012 2013Rare gases (excl. argon) 17,128 20,124 16,277 12,175 16,103Carbon dioxide 41 26 112 116 204Anhydrous ammonia 91,904 371,950 594,818 639,427 628,602Chlorine 499 636 553 641 169Ethylene - 6,292 12,850 5,736 -Hydrogen chloride (hydrochloric acid) 854 1,277 931 1,452 1,509Hydrogen fluoride (hydrofluoric acid) - - - - -Methylamine, dior trimethylamine and their salts - - 2 - -Oxirane (ethylene oxide) - - - - -Sulphur dioxide 7 - - - -Hydrogen 1 1 - 3 8Oxygen 907 717 936 621 2,255Nitrogen 113 90 185 310 173Argon 5,929 5,387 7,151 8,436 7,240Total 117,383 406,500 633,815 668,917 656,263Unsaturated acyclic hydrocarbons nes 2 1 66 7 1Fluorine; bromine 381 1,621 2,051 1,128 971Inorganic compounds nes;liquid air;compressd air;amalgams o/t of precious metals 148 364 - - -Fluorinated, brominated or iodinated derivatives of acyclic hydrocarbons - - 334 150 131Inorganic oxygen compounds of non-metals nes 728 1,019 409 353 369Total 1,259 3,005 2,860 1,638 1,472

Source: ITC

Source: ITC

117,383

406,500

633,815 668,917 656,263

1,259 3,005 2,860 1,638 1,472 -

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2009 2010 2011 2012 2013

Export of industrial gases in 2009 - 2013, USD thousand

Export of main industrial gases Export of basic chemicals including industrial gases

31%

5%

2%

4%4%2%6%2%

9%

3%

13%

5%

2%2%

10%

Industrial gas export structure by countries, 2013

United States of AmericaGermanyChinaTaipei, ChineseKorea, Republic ofJapanTurkeyThailandFranceBelgiumMoroccoIsraelNorwayTunisiaOther

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 43

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

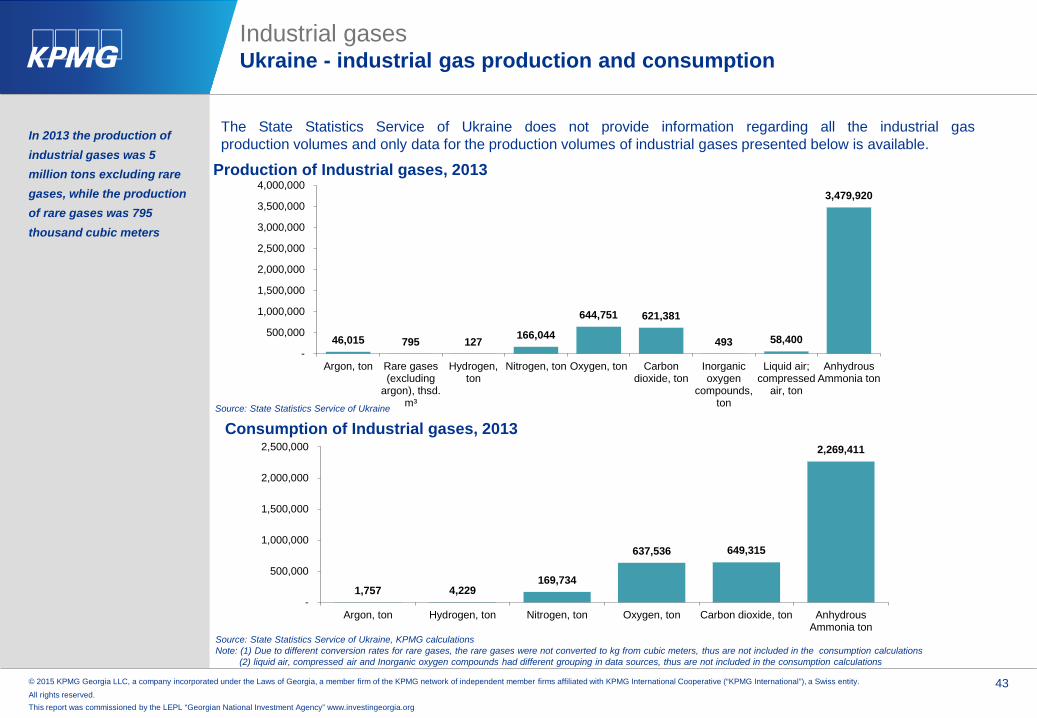

1,757 4,229 169,734

637,536 649,315

2,269,411

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Argon, ton Hydrogen, ton Nitrogen, ton Oxygen, ton Carbon dioxide, ton AnhydrousAmmonia ton

Consumption of Industrial gases, 2013

46,015 795 127 166,044

644,751 621,381

493 58,400

3,479,920

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Argon, ton Rare gases(excluding

argon), thsd.m³

Hydrogen,ton

Nitrogen, ton Oxygen, ton Carbondioxide, ton

Inorganicoxygen

compounds,ton

Liquid air;compressed

air, ton

AnhydrousAmmonia ton

Production of Industrial gases, 2013

In 2013 the production of industrial gases was 5 million tons excluding rare gases, while the production of rare gases was 795 thousand cubic meters

Industrial gasesUkraine - industrial gas production and consumption

Source: State Statistics Service of Ukraine

The State Statistics Service of Ukraine does not provide information regarding all the industrial gasproduction volumes and only data for the production volumes of industrial gases presented below is available.

Source: State Statistics Service of Ukraine, KPMG calculationsNote: (1) Due to different conversion rates for rare gases, the rare gases were not converted to kg from cubic meters, thus are not included in the consumption calculations

(2) liquid air, compressed air and Inorganic oxygen compounds had different grouping in data sources, thus are not included in the consumption calculations

© 2015 KPMG Georgia LLC, a company incorporated under the Laws of Georgia, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. 44

This report was commissioned by the LEPL “Georgian National Investment Agency” www.investingeorgia.org

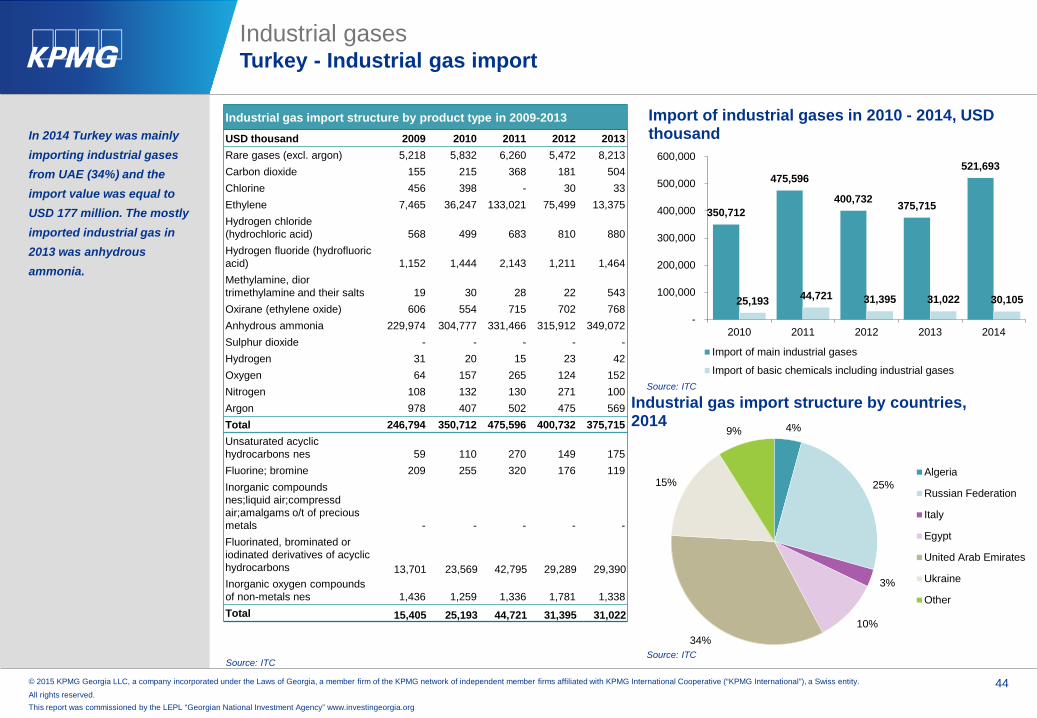

In 2014 Turkey was mainly importing industrial gases from UAE (34%) and the import value was equal to USD 177 million. The mostly imported industrial gas in 2013 was anhydrous ammonia.

Industrial gasesTurkey - Industrial gas import

Source: ITC