13

Georgian Tourism Industry Overview 2012 Georgian National Tourism Administration 4 Sanapiro St; Tbilisi 0105, Georgia; Tel: (+995 32) 243699; Email: [email protected]

Georgian Tourism Industry Overview

2012

Georgian National Tourism Administration 4 Sanapiro St; Tbilisi 0105, Georgia; Tel: (+995 32) 243699; Email: [email protected]

1

Georgian Tourism Industry Overview

1. Executive Summary

Travel and tourism is one of the largest and fastest-growing

service industries globally. In 2011, the share of tourism in

world GDP amounted to 9% or a value of over

US$6 trillion. The sector employed over 255 million people

worldwide, which is 8.7% of global employment. The Travel

and tourism industry is expected to grow by an average of

4% annually, reaching 10% of global GDP or US$10 trillion.

The number of international arrivals increased by 4.6% in

2011 and reached the record number of 980 million.

UNWTO expects growth to maintain its steady rate at about

3.3% until 2030.

International traveler arrivals have been growing rapidly in

Georgia as well. In 2011, the number of international

travelers reached 2 822 363, representing 39 % growth.

According to the recently updated information the number

of international travelers was 4 389 256 in 2012,

demonstrating 56% increase over previous year. The growth

in the Georgian tourism industry has been faster than that

of the world. This trend is observed in the share of Georgia

of international visitor arrivals that has increased from

0.12% in 2007 to 0.29% in 2011. The statistics for the last

three years demonstrate that the highest number of arrivals

fall in July and August. Turkey, Azerbaijan and Armenia

occupy the top three places by number of visitors, together

accounting for approximately 76% of total international

arrivals.

Currently, the seaside region of Ajara and the capital Tbilisi

dominate the Georgian hotel market. There are in total

1051 accommodation units with total capacity of 34 751

beds throughout the country. Ajara region boasts the

largest number of bed-places. Hotels account for 63% of the

bed capacity, followed by Guest Houses and Family Houses

with 16% each. With increasing number of visitors,

medium-term demand is already outstripping current

supply. Consequently, it is expected that supply of

accommodation units will increase considerably to keep

pace with demand.

The aviation market in Georgia has demonstrated

considerable growth in the last few years. Until 2003, the

market was not open to competition being a monopoly of

different business groups. However, in recent period

various steps have been taken towards liberalization, which

brought about a rapid increase in the number of flights and

passengers. Major airlines operating in Georgia are:

Georgian Airways, Turkish Airlines, Lufthansa, BMI, Czech

Airlines, China Southern Airlines, Qatar Airways, Alitalia,

AZAl, Air Baltic, LOT, Air Astana, Belavia, Ukraine

International Airlines, Aerosvit, Estonian Air, Pegasus, Fly

Dubai, Fly Georgia, etc.

Development of tourism stands high in the priorities of the

Georgian government. To spur sector growth, various

incentives are being offered to investors; among them are

the Hotel Investment Initiative and Free Tourist Zones to

name but a few.

Against the backdrop of global economic crisis, the

Georgian tourism industry continues to grow. The outlook

for the industry is highly optimistic. It is forecast that the

industry will create more jobs and generate more income in

the years to come.

2

2. Sector Overview

2.1 Global Trends

Travel and tourism is one of the largest and fastest-growing

service industries globally. In 2011, the share of tourism in

world GDP amounted to 9% or a value of over US$6 trillion.

The travel and tourism industry is expected to grow by an

average of 4% annually, reaching 10% of global GDP or

US$10 trillion. The sector employed over 255 million people

worldwide, which is 8.7% of global employment. By 2022

the number of jobs generated by the industry is expected to

grow to 328 million, or 1 in every 10 jobs in the world.1

The number of international arrivals world-wide increased

by 4.6% in 2011 and reached the record number of 980

million. UNWTO expects growth to maintain its steady rate

at about 3.3% till 2030.2

Figure 1: International arrivals

More than a half (51%) of total international visitors come

to Europe. Accordingly, European countries took top places

in the rankings. France occupied the first place with 79.5

million travelers followed by the USA and China.3

1 World Travel & Tourism Council, 2012. Travel & Tourism

Economic Impact. 2 UNWTO World Tourism Barometer, January 2012. Advance

Release. 3 UNWTO World Tourism Barometer, January 2012. Advance

Release.

Figure 2: International Arrivals: Top 10 countries

International tourist receipts grew by 3.8% and exceeded

US$ 1 trillion for the first time. The amount of international

tourist receipts had an increasing trend between 2007 and

2011, except in 2009, when the amount dropped to 852.4

Figure 3: International tourism receipts (million USD)

2011 is considered to be one of the most challenging years

ever experienced by the global travel and tourism industry.

However, according to the latest research of the World

Travel and Tourism Council, despite political instability,

economic ambiguity and natural disasters, the industry’s

4 UNWTO World Tourism Barometer, January 2012. Advance

Release.

899918

882

939

980

2007 2008 2009 2010 2011

Source:UNWTO World Tourism Barometer

79,5

62,357,3 56,7

46,1

29,3 29,3 28,424,7 23,4

Source:UNWTO World Tourism Barometer

856940

852926

1030

2007 2008 2009 2010 2011

Source:UNWTO World Tourism Barometer

3

contribution to world GDP grew by nearly 3% to US$2

trillion and directly generated 1.2 million new jobs. This was

supported by a 3% increase in visitor exports to US$1.2

trillion, with almost 3% growth in capital investment, which

rose to over US$ 0.7 trillion. Despite the fact that, the

macroeconomic environment still remains challenging,

research suggests that the contribution of tourism to global

GDP and employment in the future will increase. In

particular, research projects growth in household incomes

not only in large emerging economies (Brazil, Russia, India

and China), but also in the rest of Southeast Asia and Latin

America. Furthermore, increasing international trade

especially from emerging markets will boost business travel

demand. To summarize, according to research, growth in

travel and tourism’s direct contribution to GDP will remain

stable at 3% in 2012. In addition, the industry is expected to

generate directly over 2 million new jobs, with a 2%

increase in visitor exports and 3.5% growth in investment

over the year.5

2.2 Tourism in Georgia

2.2.1 General Overview

Georgia boasts rich natural and cultural resources. With a

territory of only 69.700 square kilometers, Georgia is almost

unique among the world’s nations for biodiversity. To find

subtropical marshes, semi deserts, lofty alpine zones and

snowy peaks - all within a hundred kilometers of each

other-is rare indeed. Georgia is home to more than 12 000

historical and cultural monuments, four out of which are

included in the list of UNESCO World Heritage Sites: 1.

Mtskheta - the ancient capital of Georgia,

2. Bagrati Cathedral (XI century), 3. Gelati Monastery in

Kutaisi (XI century), 4. Ushguli Village in Svaneti (located at

5 World Travel & Tourism Council, 2012. Travel & Tourism

Economic Impact

2 300 m above sea level, this is the highest settlement in

Europe). Georgia offers lots of possibilities to travelers of

different types. Tourists arriving to Georgia for a relaxing

holiday can opt for spending time at 103 resorts or visiting

springs of mineral waters (around 2400) or simply go to the

seaside. Lovers of nature will be interested in exploring 8

national parks and 31 protected areas throughout Georgia.

The winter resorts of Gudauri, Bakuriani and Mestia offer

skiers and holidaymakers an extraordinary winter and

summer vacation.

International tourist arrivals to Georgia have been growing

rapidly over the last years. In 2011, their number reached

2 822 363, representing 39 % growth. According to the

recently updated information the number of international

travelers was 4 389 256 in 2012, demonstrating 56%

increase over previous year.

Figure 4: Georgia: International arrivals

The growth in the Georgian tourism industry has been

faster than that of the world. This trend is observed in the

share of Georgia in international visitor arrivals that has

increased from 0.12% in 2007 to 0.29% in 2011.

560 021

763 231

1 051 7491 290 108

1 500 049

2 031 717

2 822 363

4 389 256

2005 2006 2007 2008 2009 2010 2011 2012

Source: The Ministry of Internal Affairs

4

Figure 5: Share of Georgia in international visitor arrivals

The comparison of growth rates of the world and Georgia

shows that in the last five years tourist arrivals in Georgia

increased considerably faster than in the whole world. Even

in 2008, during the world financial crisis when arrivals

worldwide fell by 4 %, the number of international visitors

to Georgia increased by 16%. In addition, Georgia showed

the highest relative increase of 39% in 2011 among the

emerging destinations.6

The statistics for the last three years demonstrate that the

highest number of arrivals fall in July and August.

Figure 6: Georgia: International arrivals by months

The majority, 86% of all arrivals, come from neighboring

countries Armenia, Azerbaijan, Russia and Turkey; only 14%

of visitors are from other countries.

6 UNWTO Tourism Highlights 2012 Edition

Figure 7: Arrivals: Neighboring Countries vs. World

Turkey, Azerbaijan and Armenia occupy the top three places

by number of visitors, together accounting for

approximately 76% of total international arrivals.

As for growth rate, out of the top ten countries, Iran,

Kazakhstan, Russia and Armenia have shown the most rapid

increase in visitor numbers over the last three years: 511%,

236%, 118% and 99% respectively.

Figure 8: International arrivals: Top 10 countries

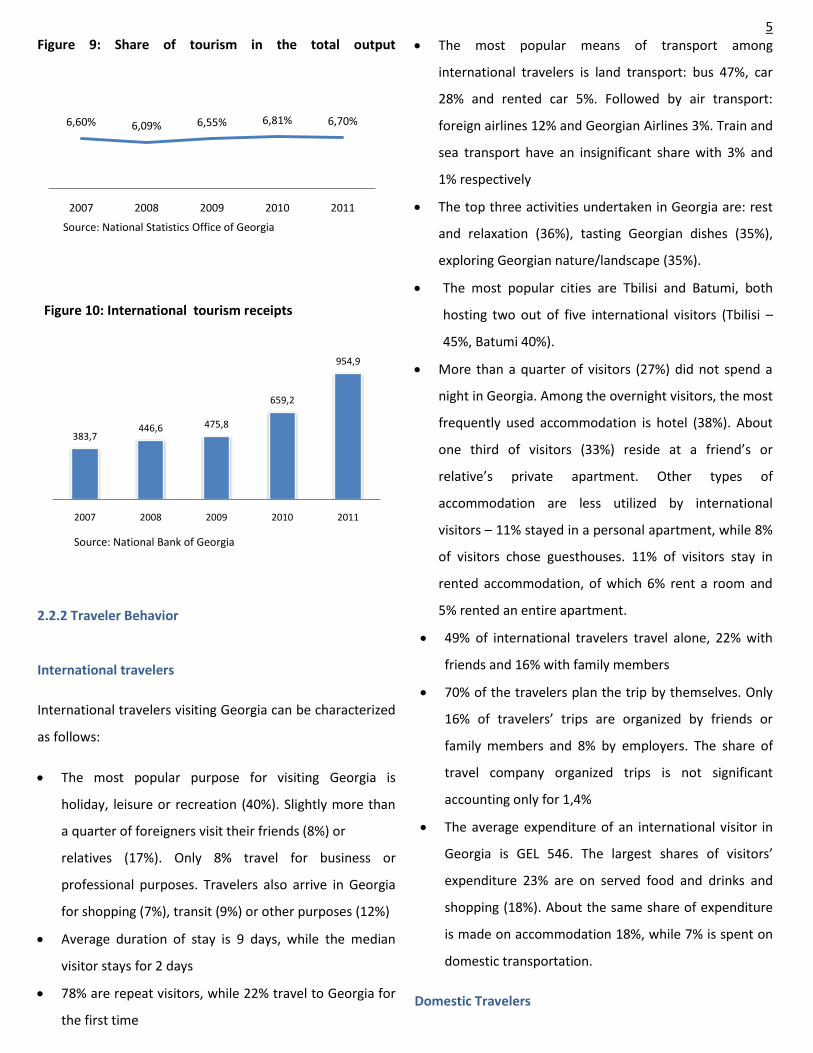

International tourism receipts also demonstrated an

increasing trend reaching almost USD 938 297 000 in 2011.

Although the share of tourism in total output decreased in

2008 as a result of world financial crisis, since then it has

showed significant growth accounting for more than 7% of

total output.

0,12% 0,14%0,17%

0,22%

0,29%

2007 2008 2009 2010 2011

Source: The Ministry of Internal Affairs

0

50000

100000

150000

200000

250000

300000

350000

400000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2009

2010

2011

Source: The Ministry of Internal Affairs

0.2 %

0.2 %

1 %

3 %

9.4 %

86.1 %

0.1 %

Others

Africa

Middle East

America

Asia and the Pacific

Europe

Neighbouring Countries

Source: The Ministry of Internal Affairs

0 100 000 200 000 300 000 400 000 500 000 600 000 700 000 800 000

Kazakh…

Germany

USA

Israel

Ukraine

Iran

Russia

Armenia

Azerbai…

Turkey

2009

2010

2011

Source: The Ministry of Internal Affairs

5

Figure 9: Share of tourism in the total output

Figure 10: International tourism receipts

2.2.2 Traveler Behavior

International travelers

International travelers visiting Georgia can be characterized

as follows:

The most popular purpose for visiting Georgia is

holiday, leisure or recreation (40%). Slightly more than

a quarter of foreigners visit their friends (8%) or

relatives (17%). Only 8% travel for business or

professional purposes. Travelers also arrive in Georgia

for shopping (7%), transit (9%) or other purposes (12%)

Average duration of stay is 9 days, while the median

visitor stays for 2 days

78% are repeat visitors, while 22% travel to Georgia for

the first time

The most popular means of transport among

international travelers is land transport: bus 47%, car

28% and rented car 5%. Followed by air transport:

foreign airlines 12% and Georgian Airlines 3%. Train and

sea transport have an insignificant share with 3% and

1% respectively

The top three activities undertaken in Georgia are: rest

and relaxation (36%), tasting Georgian dishes (35%),

exploring Georgian nature/landscape (35%).

The most popular cities are Tbilisi and Batumi, both

hosting two out of five international visitors (Tbilisi –

45%, Batumi 40%).

More than a quarter of visitors (27%) did not spend a

night in Georgia. Among the overnight visitors, the most

frequently used accommodation is hotel (38%). About

one third of visitors (33%) reside at a friend’s or

relative’s private apartment. Other types of

accommodation are less utilized by international

visitors – 11% stayed in a personal apartment, while 8%

of visitors chose guesthouses. 11% of visitors stay in

rented accommodation, of which 6% rent a room and

5% rented an entire apartment.

49% of international travelers travel alone, 22% with

friends and 16% with family members

70% of the travelers plan the trip by themselves. Only

16% of travelers’ trips are organized by friends or

family members and 8% by employers. The share of

travel company organized trips is not significant

accounting only for 1,4%

The average expenditure of an international visitor in

Georgia is GEL 546. The largest shares of visitors’

expenditure 23% are on served food and drinks and

shopping (18%). About the same share of expenditure

is made on accommodation 18%, while 7% is spent on

domestic transportation.

Domestic Travelers

6,60% 6,09% 6,55% 6,81% 6,70%

2007 2008 2009 2010 2011

Source: National Statistics Office of Georgia

383,7446,6 475,8

659,2

954,9

2007 2008 2009 2010 2011

Source: National Bank of Georgia

6

The travel patterns of domestic travelers differ slightly from

those of international ones:

The most common purpose of travel among Georgians

is visiting friends or relatives 44%, rather than going

for holiday, leisure or recreation (16%). Nearly every

tenth visit is related to health or medical care, 12%

travel for shopping and just 3% travel on business or a

professional trip

Average duration of stay is 2 days

20% of domestic visitors travel only once, while the

other 80% are regular travelers

Bus or minibus is the most common means of

transportation for domestic travelers. 55% use a bus at

some point in their trip, followed by private vehicle

34%. Smaller portions of Georgians use train and

rented car: 6% and 4% respectively

Main activities during domestic trips are rest and

relaxation (30%), shopping (22%) and exploring

Georgia’s Nature/Scenery/Landscape (9%)

The top three most visited places are: Tbilisi (27%),

Kutaisi (9%) and Batumi (7%)

40% of domestic travelers do not stay overnight. Out

of those staying - 55% choose private accommodation

of a friend or relative, 17% private houses/apartments

and 11% secondary residences

Domestic travelers typically travel alone (44%) or with

close family members (36%). Less than one quarter

(23%) of visitors travel with extended family members,

friends, co-workers, etc

About 68% of visitors organize their trips by themselves

and 28% rely on family members and friends. Very few

visits are organized by employers (8%) or travel

companies (0.02%).

2.2.2 The Hotel Market

Currently, the seaside region of Ajara and the capital, Tbilisi,

dominate the Georgian hotel market. There are in total

1051 accommodation units with a total capacity of 34 751

beds. Ajara region boasts the largest number of bed-places.

Hotels account for 63% of the bed capacity, followed by

Guest Houses and Family Houses with 16% each. With

increasing number of visitors, medium-term demand is

already outstripping current supply. Consequently, it is

expected that the supply of accommodation units will

increase considerably to keep pace with demand.

Tbilisi boasts several international brand hotels: Radisson

Blue Iveria, Tbilisi Marriott, Courtyard Marriot, Sheraton

Metekhi Palace, Holiday Inn and Citadines. Several other

international chains are expanding in the city as well. As

regards Batumi, Sheraton and Radisson Blue hotels have

recently opened there. Major hotel projects under

construction are the following: Kempinski, Hilton, Holiday

Inn, Ritz-Carlton, Marriott to name but a few.

A number of brand hotels are starting operation in the spa

resorts of Georgia as well.

Figure 11: Number of Accommodation Units

263

151

132

126

111

85

67

56

31

16

13

Adjara

Samtskhe-Javakheti

Kakheti

Tbilisi

Samegrelo-Upper Svaneti

Mtskheta-Mtianeti

Imereti

Guria

Racha-Lechkhumi

Lower Kartli

Inner Kartli

Source: Georgian National Tourism Administration

7

Figure 12: Bed Capacity by Regions

Figure 13: Bed capacity by types

2.2.3 The Aviation Market

The aviation market in Georgia has demonstrated

considerable growth in the last few years. Until 2003, the

market was not open to competition being a monopoly of

different business groups. However, after the Rose

Revolution, various steps have been taken to liberalize the

market, which has resulted in a rapid increase in the

number of flights and passengers. The government of

Georgia is planning to transform the country into a regional

transportation hub. Several significant steps were

undertaken to this end: the introduction of an Open Sky

Policy, the integration of Georgia into the European

Common Aviation Area (ECAA) and the development of

modern airport network.

Open Sky Policy

In 2005 Georgia announced an Open Sky Policy, which is

considered as a liberal approach to support free

competition and attract foreign airlines to the Georgian

aviation market. The Introduction of the Open Sky Policy

facilitated entrance of the world’s largest airlines to the

Georgian civil aviation market, notably Lufthansa, Turkish

Airlines, China Southern Airlines, Fly Dubai, LOT Polish

Airlines, Air Baltic, Estonian Air, Air Astana, ATA Air, Aerosvit

Ukrainian Airlines, Qatar Airways Alitalia, UTair Ukraine

Airlines and Aegean Airlines.

Georgia’s Integration into the European Common

Aviation Area

The Common Aviation Area Agreement between the

European Union and Georgia was signed on December 2,

2010 in Brussels, Belgium. The Agreement aims to open

respective markets and integrate Georgia into a wider

European Common Aviation Area (ECAA), as well as to

harmonize the country’s legislation with the European one.

Other Projects

EU funded Twinning project aimed at assisting Georgia in

the harmonization of regulations on civil aviation safety

and air carrier licensing with those of the EU (launched

in 2011);

Preferential conditions for domestic flight operators

were developed;

10266

5723

5326

2797

2746

2574

2006

1956

767

410

180

Adjara

Samtskhe-Javakheti

Tbilisi

Guria

Imereti

Mtskheta-Mtianeti

Kakheti

Samegrelo-Upper Svaneti

Racha-Lechkhumi

Lower Kartli

Inner Kartli

Source: Georgian National Tourism Administration

22012

5373 55121008 220 255 279 92

Source: Georgian National Tourism Administration

8

A ‘Proposal for Low Cost Carriers’ was elaborated to

facilitate entrance of Low Cost Carriers to the Georgian

aviation market;

In 2010, the International Air Transport Association

(IATA) made a decision to establish the Billing and

Settlement Plan Georgia (BSP). This system simplifies

and supports selling, calculation and transfer procedures

for the agencies accredited by IATA;

Successful steps were taken to improve national civil

aviation legislation, particularly:

• Drafting of a new air law was initiated;

• Operating regulations were developed and issued

for the domains of Personnel Licensing (PEL),

Operations (OPS), and Airworthiness of aircraft (AIR);

• A Surveillance programme in the domains of the

PEL, OPS, and AIR has been structured;

• Licensing, certifications, authorizations and

approvals were upgraded.

The Georgian Air Navigation Service Provider –

‘Sakaeronavigatsia’ Ltd, responsible for air traffic

management in Georgia, has implemented several

projects focused on Air Traffic Control Systems, Radio

Location, renovation of Illumination and Technical

Equipment.

Planned Activities

Gradual harmonization of Georgia’s aviation legislation

with European standards and implementation of EU

aviation rules in aviation safety, security, environment,

consumer protection, air traffic management, economic

regulation, competition issues, and social aspects

Acceleration of the process of accession to the European

Organization for the Safety of Air Navigation

(EUROCONTROL)

Supporting the establishment of the BSP Georgia.

Infrastructural Projects

Two international and one domestic airports are operating

in Georgia complying fully with International Civil Aviation

Organization (ICAO) standards. Tbilisi and Batumi

International Airports are run by a Turkish company - TAV

Airports Holding Co. They started operation in February and

May of 2007 respectively. Mestia Airport (Queen Tamar

Airport) was officially opened in 2011. The capacity of

Tbilisi and Batumi International Airports is 2000 and 300

passengers/hour respectively. As regards Mestia

International Airport, its capacity is 100 passengers/hour .

The Construction works of Kopitnari International Airport

(Kutaisi) was finished in September, 2012. The opening

was marked by the launching of flights by low-cost carrier

Wizz Air from Kutaisi to Kiev. The company is the third LCC

in the Georgian market after Pegasus and FlyDubai.

Another significant step forward will be the opening of Poti

International Airport which will become a hub for regional

and international transportation.

Figure 14: Tbilisi international Airport: Passengers and

Flights

565909 614516713565

702073

821860

1057046

5070

5835

63625951

7837

9081

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

-100000

100000

300000

500000

700000

900000

1100000

2006 2007 2008 2009 2010 2011

Passengers Flights

Source: The Ministry of Economy and Sustainable Development of Georgia

9

Figure 15: Batumi international Airport: Passengers and

Flights

Figure 16: Kutaisi International Airport: Passengers and

Flights

Airlines

In 2012, new player Qatar Airways entered the market by

opening the route Baku - Tbilisi. Qatar is the first of the

major Gulf carriers to serve Georgia and is the second

Middle Eastern carrier in Georgia after FlyDubai. Qatar

Airways opens up new faster connections to passengers

travelling between Georgia and Africa, the Middle East or

Asia. In addition to new airways, existing companies

increased their number of flights within the recent period.

In June 2012, Air Astana increased Almaty-Tbilisi flights

from three to four times per week. The company plans to

add flights to Astana-Tbilisi routes as well. Growing

interest towards Tbilisi has influenced the plans of Air

Astana to create its Central Asian network here, providing

connections through its Almaty and Astana hubs.

China Southern Airlines also recently increased Urumqi-

Tbilisi flights from two to three times a week. The carrier

is using Urumqi as a transit hub for its fast expanding

network in central Asia and Eastern Europe.

Recently, new domestic airline Fly Georgia has entered

Georgian market. New company Air Caucasus also plans to

start operation. These Airlines are deemed to be

competitors for Georgian Airlines and will significantly

increase international capacity in Tbilisi.

Another airline showing increasing interest in Georgia is

AirBaltic, which serves the Riga-Tbilisi route three times a

week and is considering offering four weekly flights.

Figure 18: Tbilisi International Airport

39795

7927767984

88101

133306

484

699

538

916

1446

-100

100

300

500

700

900

1100

1300

1500

-6000

14000

34000

54000

74000

94000

114000

134000

2006 2007 2008 2009 2010 2011

Passengers Flights

Source: The Ministry of Economy and Sustainable Development of Georgia

28679

15379

84187221

4340

325

199

10974

47 0

50

100

150

200

250

300

350

400

450

500

0

5000

10000

15000

20000

25000

30000

2006 2007 2008 2009 2010 2011

Passengers Flights

Source: The Ministry of Economy and Sustainable Development of Georgia

18%

82%

Domestic Airlines

International Airlines

Source: The Ministry of Economy and Sustainable Development of Georgia

10

This year is going to be quite challenging for Georgia’s

aviation industry as new airlines are entering the market,

while others are expressing greater interest and increasing

flight frequencies on various routes. Though some coming

increases are seasonal, more successes are yet to come,

as the country is making important steps forward with its

plan to become the transportation hub of the region.7

Major airlines operating in Georgia are:

Georgian Airways, Turkish Airlines, Lufthansa, BMI, Czech

Airlines, China Southern Airlines, Qatar Airways, Alitalia,

AZAl, Air Baltic, LOT, Air Astana, Belavia, Ukraine

International Airlines, Aerosvit, Estonian Air , Pegasus, Fly

Dubai, Fly Georgia, ATA airlines, SCAT, Ural Airlines, Arkia

Israel Airlines, S7, Aegean Airlines.

Figure 17: Tbilisi International Airport: Share of airlines

7 CAPA, Centre for Aviation, 2012. Georgia’s aviation market

expanding with Government interest. Available at: http://centreforaviation.com/analysis/georgias-aviation-market-expanding-with-government-interest-76705

2.2.4 Government Incentives

The Georgian government has declared tourism and hotel

industry development to be a high priority. Various

investment initiatives have been proposed to spur the

sector’s growth, among them are:

The Hotel Investment initiative giving investors the

opportunity to enter the Georgian market in an

immediately competitive position by offering the

following benefits:

Access to prime real estate locations through

privatization

Privatized property acquisition through a direct

sale

Significant discounts on current market value for

privatized properties

Land plots, Greenfield projects, and properties

with suitable buildings for Brownfield projects

Preferential terms from municipalities, such as

Tbilisi and the regional centers

Free Tourist Zones giving investors special privileges in

Kobuleti and Anaklia/Zugdidi. Investors making

investments of USD 1-3 mln in Kobuleti are offered the

following:

Free Land

Free Hotel Master Plan

Free casino license for hotel capacity over

100 rooms

Exemption from profit and property taxes for 15

years

Fully provided engineering utility networks and

corresponding outdoor infrastructure

18,3%

13,5%

12,8%

9,7%

6,6%5,9%

5,4%5,0%

4,3% 4,1% 4,0%

2,0%

8,3%

Source: The Ministry of Economy and Sustainable Development of Georgia

11

After the successful initiation of Kobuleti, the

Anaklia/Zugdidi Free Tourist Zone was established. The

Special package for investors here is as follows:

Free land

Free Hotel Master Plan

Full engineering utility networks (water,

electricity, gas)

Exemption from profit and property taxes for 15

years

Mineral water pipe supply for the new resort

Free casino license for hotel capacity over 80

rooms

Georgian citizenship for foreign investors

In addition to the current possibilities of entering the

market through joint ventures and acquisitions, there are

many opportunities for investors to enter not only as

hotel owners, but also as hotel operators. For example,

there are many individual Georgian hotels that are

currently interested in working with an international

operator as a way to increase revenues and occupancy

rates.

For hotel owners, considering the supply gaps that

currently exist, the market is open to any form of new

investment. Not only do hotel investors have access to

prime real estate locations, but they can work with the

Georgian Government and municipalities like Tbilisi to

negotiate preferential terms.

2.3 Sector Outlook

Against the backdrop of global economic crisis, The

Georgian tourism industry continues to grow. The outlook

for the industry is highly optimistic. It is forecast that the

industry will create more jobs and generate more income

in the years to come. The number of arrivals to Georgia is

expected to increase substantially thanks to various steps

taken by the Government in general and the Georgian

National Tourism Administration in particular.

Among the actions taken by the GNTA towards increasing

the number of travelers in the country are development

of tourism infrastructure, facilitation of international

travel, improvement of service quality, large-scale

marketing campaigns, targeting new markets and tourist

product development.

Development of tourist infrastructure stands high on the

priorities of government. Major reconstruction works

related to tourism are underway.

Significant steps were taken towards travel facilitation and

visa relaxation. Georgia has no visa policy with around 87

countries. Among them are citizens of the United States,

Canada and the European Union member states, who can

enter Georgia solely on the basis of an Identity Card.

Travelers from most other countries are issued visas on

arrival.

Another significant issue is service quality enhancement

which is achieved through intensive trainings for the

representatives of the tourism and hospitality industry

throughout Georgia.

Marketing undoubtedly plays a vital role in tourism

growth. Activities undertaken by GNTA cover promotional

campaigns in domestic and international markets, press

and FAM trips, participation in international travel-fairs,

production of print materials, social media marketing, etc.

Choosing the right markets is undoubtedly an integral part

of marketing. While maintaining existing markets, GNTA

12

concentrates on tapping into new countries, among them

are new emerging economies with immense potential.

Making the most of Georgia’s rich natural and cultural

resources by offering new tourist products provides

increased possibilities for targeting travelers of different

tastes. GNTA efforts focus on the development of

different types of tourism such as MICE, wine, eco,

adventure to name but a few.

It should be mentioned that at all stages of tourism

development particular attention is paid to the issue of

sustainability. Preserving the environment and ensuring

the sustainable use of resources for future generations

are of paramount significance.

2.3.1 Long-term perspective

European Youth Olympic Festival 2015

On November 26-27, in Belgrade, the 39th General

Assembly of European Olympic Committees chose the

Georgian Capital to host the Youth Olympic Festival in

2015. Over 4 000 athletes from 49 European countries will

participate in the Festival taking place in Tbilisi. The

sporting infrastructure of the city will be renovated

according to the European standards and an “Athletes

Village” will be built. For this single event the city of Tbilisi

is expected to host more then 10, 000 visitors, of which

approximately 5,000 will require 3-star hotel

accommodation and about 200 visitors will need 5-star

hotel accommodation, all within Tbilisi. Considering the

fact that there are only 5011 bed-places in Tbilisi

(including Guest Houses and Family Houses), there is an

immediate need for new hotel investment to fill the gap in

supply. This festival represents a good opportunity for the

country to showcase its rich tourism potential.

UEFA Super Cup 2015

The UEFA Executive Committee has given Tbilisi the

opportunity to host a mega sport event, the UEFA Super

Cup. The UEFA Super Cup is an annual football match

between the winners of the Champions League and the

Europe League. The game will be held at the newly

renovated Mikheil Meshki Stadium. This event will gather

football fans from all over the world

.