28

Getting the Community Involved in Dealing with Current Financial Realities May 17, 2012 Mohsin Dada CFP® CFO North Shore School District 112, Highland Park, IL

Getting the Community Involved in Dealing with Current Financial Realities

May 17, 2012

Mohsin Dada CFP®CFO

North Shore School District 112, Highland Park, IL

Objectives

Create Awareness of our available Financial Resources

Think of ways to Balance the District Budget, while maintaining the current level of services to our students

Address Significant Financial Impacts

Obtain Philosophical Agreement as to Budget Approach

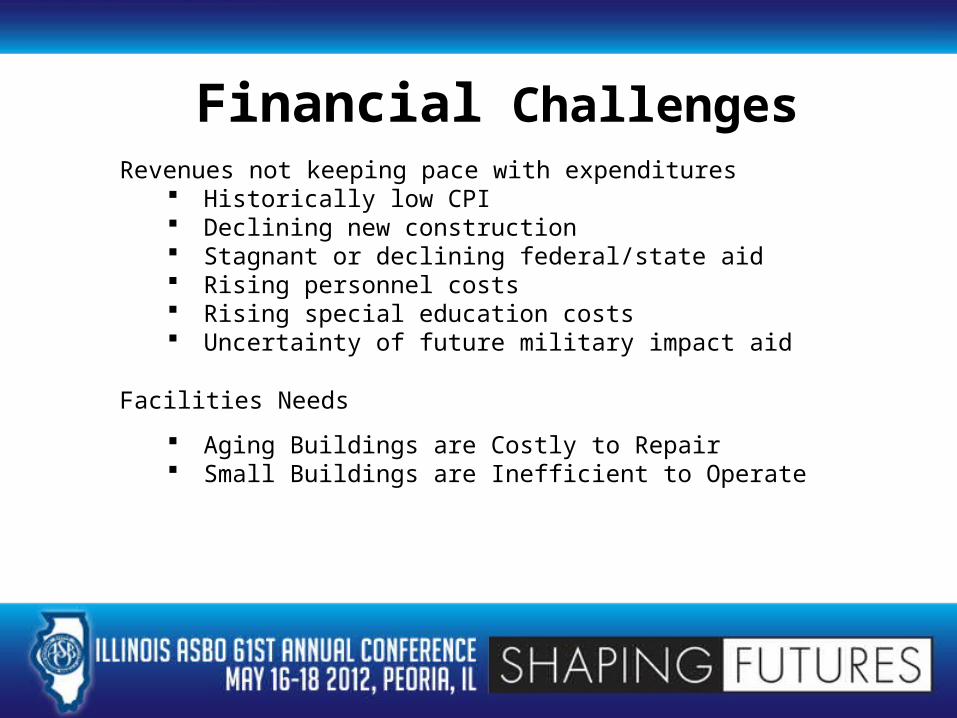

Financial ChallengesRevenues not keeping pace with expenditures

Historically low CPI Declining new construction Stagnant or declining federal/state aid Rising personnel costs Rising special education costs Uncertainty of future military impact aid

Facilities Needs

Aging Buildings are Costly to Repair Small Buildings are Inefficient to Operate

North Shore School District 112Revenue by Type – FY12

School Year Annual ExtraordinaryReimbursement Per Pupil

Annual Special EdPersonnel Reimbursement

1978-79 $2,000 Per Year $6,250 (Certified)

$2,500 (Non-Certified)

Proration rate assumed at 100% Proration rate assumed at 100%

1986-87 $2,000 Per Year $8,000 (Certified)

$2,800 (Non-Certified)

Proration rate assumed at 100% Proration rate assumed at 100%

1990-91 $2,000 Per Year $8,000 (Certified)

$2,800 (Non-Certified)

Actual Reimbursement: $1,973

ProrationRate: 100%

Proration Rate: 98.63%

1996-97 $2,000 Per Year $8,000 (Certified)

$2,800 (Non-Certified)

Actual

Actual Reimbursement: $1,734 $6,448 (Certified)

$2,327 (Non-Certified)

Proration rate: 86.71% Proration rate: 83.10%

2008 onwards The Reimbursement is no $9,000 (Certified)longer based on Special Education $3,500 (Non-Certified)

services and is calculatedas a % of regular education enrollment.

STATE SPECIAL EDUCATION REIMBURSEMENTS

Property tax levy is capped at CPI plus any new property growth

• Low CPI in last 3 years: average 1.43%• Nominal new property growth• Declining Equalized Assessed Valuation (total

property wealth of district) Interest Earnings < 1% No growth in state or federal funding

Factors Affecting Revenues As of December 2011

• Average CPI Increase, Last Three Years: 1.43%• Historic CPI Average 2.50%• Average New Construction, Last Three Years: .89%

FY12 0.35% (estimated)FY11 0.94%FY10 1.39%

• 8 Year New Construction Average: 1.43%

• Investment earnings at Historic Lows

Factors Affecting RevenuesProperty Taxes Capped at CPI Plus New Construction

As of December 2011

Factors Affecting RevenuesProperty Taxes Capped at CPI Plus New Construction

• Average CPI Increase, Last Four Years: 1.83%

• Historic CPI Average (Since 1992) 2.53%

• Average New Construction, Last Three Years: .93%FY12 0.46% FY11 0.94%FY10 1.39%

• 10 Year New Construction Average: 1.43%

• Investment earnings at Historic Lows

Factors Affecting RevenuesFiscal Year 2012 General State Aid

Amount of GSA per studentNumber of School Districts in the state 865

Foundation Level 625 $429 - $6,119Alternative Method 171 $219 - $428Flat Level 69 $218

General State Aid provides unrestricted grants-in-aid to school districts in an equitable manner.It is distributed in inverse proportion to local fiscal capacity, as measured by property tax wealth per student.North Shore School Dist 112 is relatively a wealthy school district in comparison to most school districts in the stateand is in the Flat Level of $218 per student.

State Categorical Reimbursements

10 YEARS OF DEFICIT - SURPLUS SPENDINGOur Financial History

FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 (es-timated)

-$5,000,000

-$4,000,000

-$3,000,000

-$2,000,000

-$1,000,000

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

729,040

-3,753,364 -1,381,418 -4,227,304 -3,835,041

3,542,599

-203,103 -679,886 -1,247,999 -1,346,185

Operating Surplus or Deficit after adjustment from Bond Proceeds, Capital Leases and Transfers

Operating Fund Projections with Fund Balance Target

Operating Funds – Education, Operations & Maintenance, Transportation, Illinois Municipal Retirement Fund, Tort and Working Cash

Aggregate View - Projection Summary

$3,209,975

($5,708,495)

$10,232,637

$15,652,151

$19,784,226

$22,942,981

($10,000,000)

($5,000,000)

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

2012 2013 2014 2015 2016 2017

FY-End Balances 25% of Expenditures

North Shore School District 112Expenditures by Type – FY12

Salaries and benefits account for close to 70% of budget– Salaries have risen by more than CPI– Medical insurance rates have risen by an average 9.34% in

past 3 years

Unfunded government mandates– Special Ed Costs– Transportation costs– ELL, NCLB, RtI

Repair and Maintenance of Aging Facilities

Factors Affecting Expenditures

Salaries by Staff Type

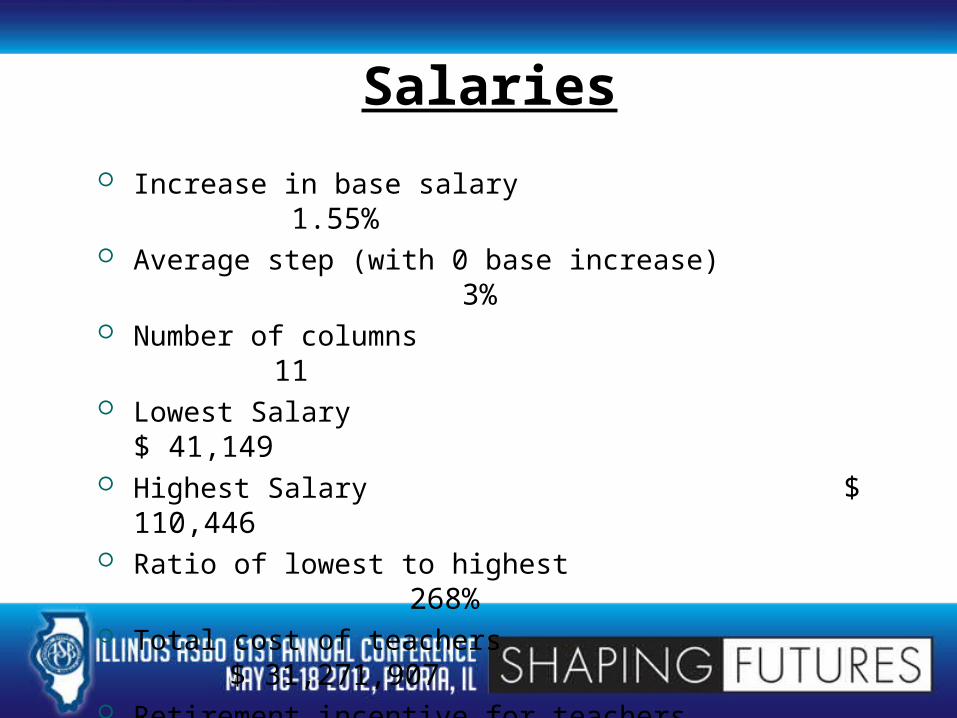

Salaries Increase in base salary

1.55% Average step (with 0 base increase)

3% Number of columns

11 Lowest Salary

$ 41,149 Highest Salary

$ 110,446 Ratio of lowest to highest

268% Total cost of teachers

$ 31,271,907 Retirement incentive for teachers

6% Number of teachers on retirement incentive

30

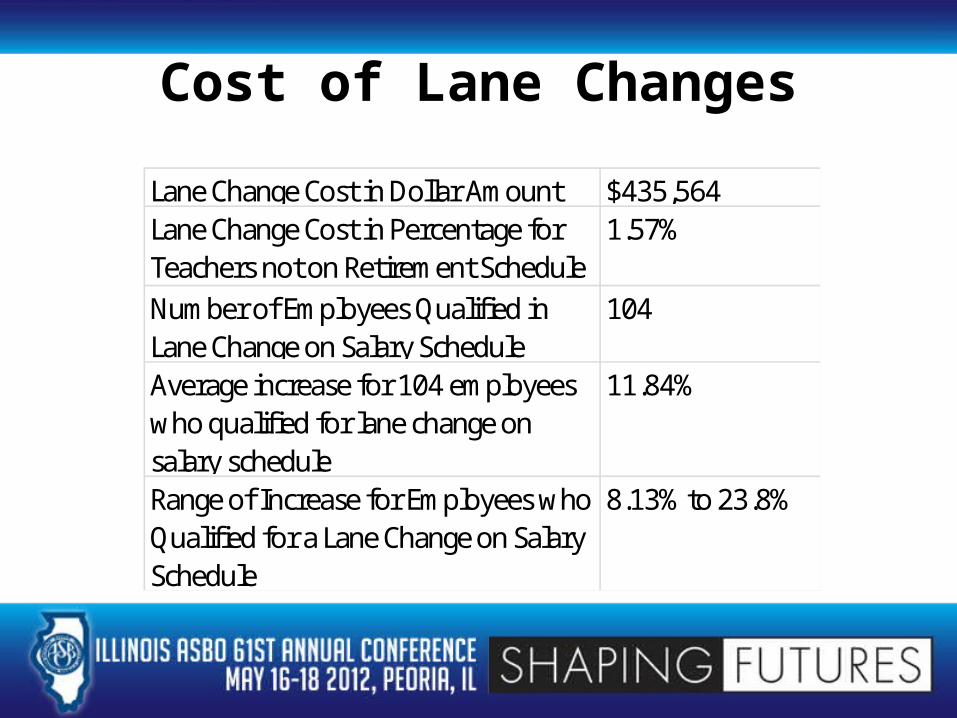

Cost of Lane Changes

Lane Change Cost in Dollar Amount $435,564 Lane Change Cost in Percentage for Teachers not on Retirement Schedule

1.57%

Number of Employees Qualified in Lane Change on Salary Schedule

104

Average increase for 104 employees who qualified for lane change on salary schedule

11.84%

Range of Increase for Employees who Qualified for a Lane Change on Salary Schedule

8.13% to 23.8%

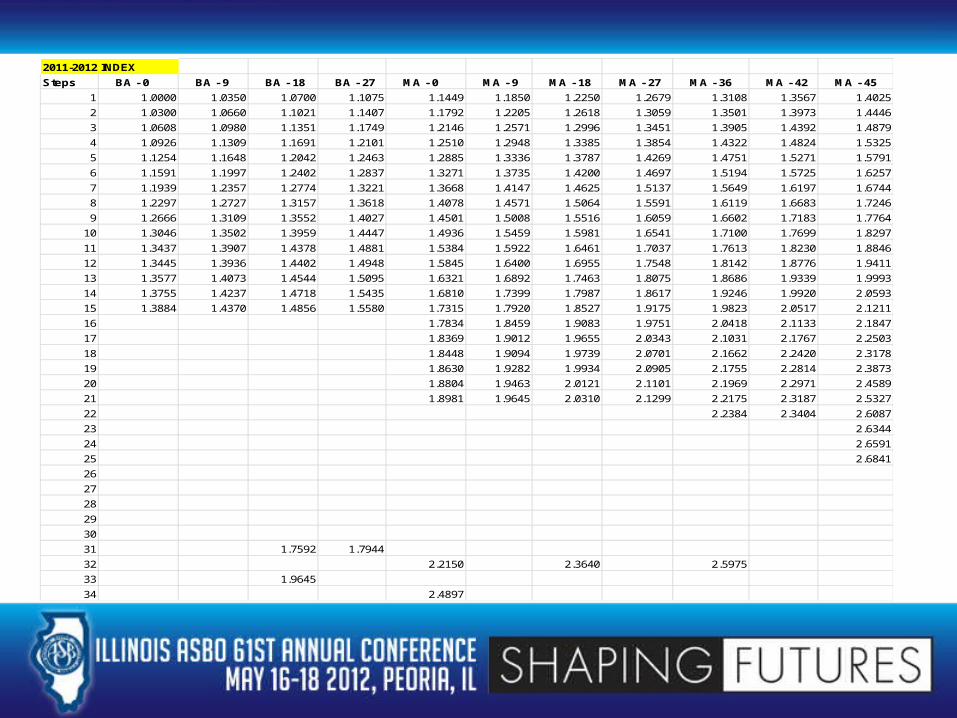

2011-2012 INDEXSteps BA - 0 BA - 9 BA - 18 BA - 27 MA - 0 MA - 9 MA - 18 MA - 27 MA - 36 MA - 42 MA - 45

1 1.0000 1.0350 1.0700 1.1075 1.1449 1.1850 1.2250 1.2679 1.3108 1.3567 1.40252 1.0300 1.0660 1.1021 1.1407 1.1792 1.2205 1.2618 1.3059 1.3501 1.3973 1.44463 1.0608 1.0980 1.1351 1.1749 1.2146 1.2571 1.2996 1.3451 1.3905 1.4392 1.48794 1.0926 1.1309 1.1691 1.2101 1.2510 1.2948 1.3385 1.3854 1.4322 1.4824 1.53255 1.1254 1.1648 1.2042 1.2463 1.2885 1.3336 1.3787 1.4269 1.4751 1.5271 1.57916 1.1591 1.1997 1.2402 1.2837 1.3271 1.3735 1.4200 1.4697 1.5194 1.5725 1.62577 1.1939 1.2357 1.2774 1.3221 1.3668 1.4147 1.4625 1.5137 1.5649 1.6197 1.67448 1.2297 1.2727 1.3157 1.3618 1.4078 1.4571 1.5064 1.5591 1.6119 1.6683 1.72469 1.2666 1.3109 1.3552 1.4027 1.4501 1.5008 1.5516 1.6059 1.6602 1.7183 1.7764

10 1.3046 1.3502 1.3959 1.4447 1.4936 1.5459 1.5981 1.6541 1.7100 1.7699 1.829711 1.3437 1.3907 1.4378 1.4881 1.5384 1.5922 1.6461 1.7037 1.7613 1.8230 1.884612 1.3445 1.3936 1.4402 1.4948 1.5845 1.6400 1.6955 1.7548 1.8142 1.8776 1.941113 1.3577 1.4073 1.4544 1.5095 1.6321 1.6892 1.7463 1.8075 1.8686 1.9339 1.999314 1.3755 1.4237 1.4718 1.5435 1.6810 1.7399 1.7987 1.8617 1.9246 1.9920 2.059315 1.3884 1.4370 1.4856 1.5580 1.7315 1.7920 1.8527 1.9175 1.9823 2.0517 2.121116 1.7834 1.8459 1.9083 1.9751 2.0418 2.1133 2.184717 1.8369 1.9012 1.9655 2.0343 2.1031 2.1767 2.250318 1.8448 1.9094 1.9739 2.0701 2.1662 2.2420 2.317819 1.8630 1.9282 1.9934 2.0905 2.1755 2.2814 2.387320 1.8804 1.9463 2.0121 2.1101 2.1969 2.2971 2.458921 1.8981 1.9645 2.0310 2.1299 2.2175 2.3187 2.532722 2.2384 2.3404 2.608723 2.634424 2.659125 2.684126 27 28 29 30 31 1.7592 1.7944 32 2.2150 2.3640 2.5975 33 1.9645 34 2.4897

Medical Insurance Costs

TYPETOTAL ANNUAL PREMIUM

PAID BY EMPLOYEE

PPO Single $8,532.00 - $8,532.00 (100%)HMO Single $5,208.00 - $5,208.00 (100%)DIFFERENCE $3,324.00 - $3,324.00

PPO Family $23,172.00 $11,388.00 $11,784.00HMO Family $14,124.00 $6,132.00 $7,992.00DIFFERENCE $9,048.00 $5,256.00 $3,792.00

PAID BY EMPLOYER

HMO/PPO Participation Ratio By Category 2011 All Employees

HMO PPO TOTAL

SINGLE 87 438 525% by Category 16.6% 83.4% 100.0%

FAMILY 44 54 98% by Category 44.9% 55.1% 100.0%

TOTAL 131 492 623% by Category 21.0% 79.0% 100.0%

Health Care Trend Rate History

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%

2003

2004

2005

2006

2007

2008

2009

2010

2011

Year

Rates

PPO

HMO

10.7% (Projected)10.5% (Projected)

10.7%10.5%

10.7%

10.7%

10.4%

10.6%

11.2%10.9%

12.4%12.2%

13.0%13.2%

14.2%14.1%

15.7%16.4%

Source: Aon Consulting 2010 Health Care Trend Survey

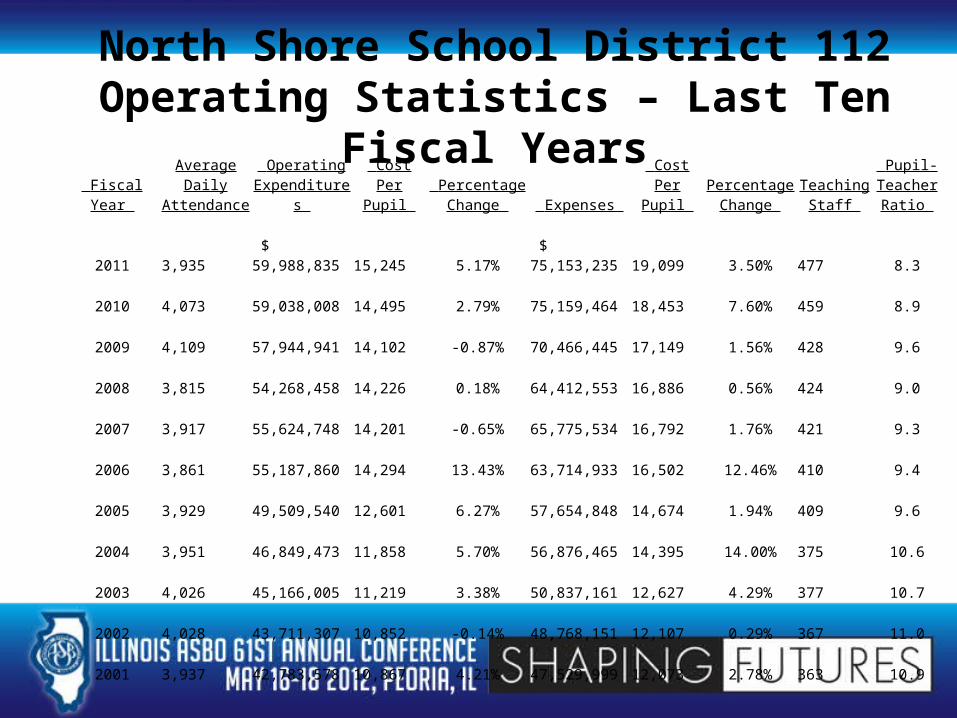

North Shore School District 112Operating Statistics – Last Ten Fiscal Years

Fiscal Year Average Daily

Attendance Operating

Expenditures Cost Per

Pupil Percentage

Change Expenses Cost Per

Pupil Percentage

Change Teaching

Staff

Pupil-Teacher Ratio

2011 3,935 $ 59,988,835 15,245 5.17% $ 75,153,235 19,099 3.50% 477 8.3

2010 4,073 59,038,008 14,495 2.79% 75,159,464 18,453 7.60% 459 8.9

2009 4,109 57,944,941 14,102 -0.87% 70,466,445 17,149 1.56% 428 9.6

2008 3,815 54,268,458 14,226 0.18% 64,412,553 16,886 0.56% 424 9.0

2007 3,917 55,624,748 14,201 -0.65% 65,775,534 16,792 1.76% 421 9.3

2006 3,861 55,187,860 14,294 13.43% 63,714,933 16,502 12.46% 410 9.4

2005 3,929 49,509,540 12,601 6.27% 57,654,848 14,674 1.94% 409 9.6

2004 3,951 46,849,473 11,858 5.70% 56,876,465 14,395 14.00% 375 10.6

2003 4,026 45,166,005 11,219 3.38% 50,837,161 12,627 4.29% 377 10.7

2002 4,028 43,711,307 10,852 -0.14% 48,768,151 12,107 0.29% 367 11.0

2001 3,937 42,783,578 10,867 4.21% 47,529,999 12,073 2.78% 363 10.9

North Shore School District 112Current Situation

Compounding Effect of Expenditures Exceeding Revenues

North Shore School District 112Summary of Major Expenditures Assumptions

No Shift of Pension Obligation to the local Board of Education from the State of Illinois Pension Rate for Employer to stay at 0.58% THIS (TRS Health) Employer Rate 0.66% TRS Federal Fund pension rate 25.12% Health Insurance increase 10% Dental Insurance increase 6% Enrollment no significant change Staffing no change No significant change in Impact Aid Retirees FY13 – 5, FY14 – 6, FY 15 – 9, FY 16 – 0 New hire replacement BA-Step 6 $48,435

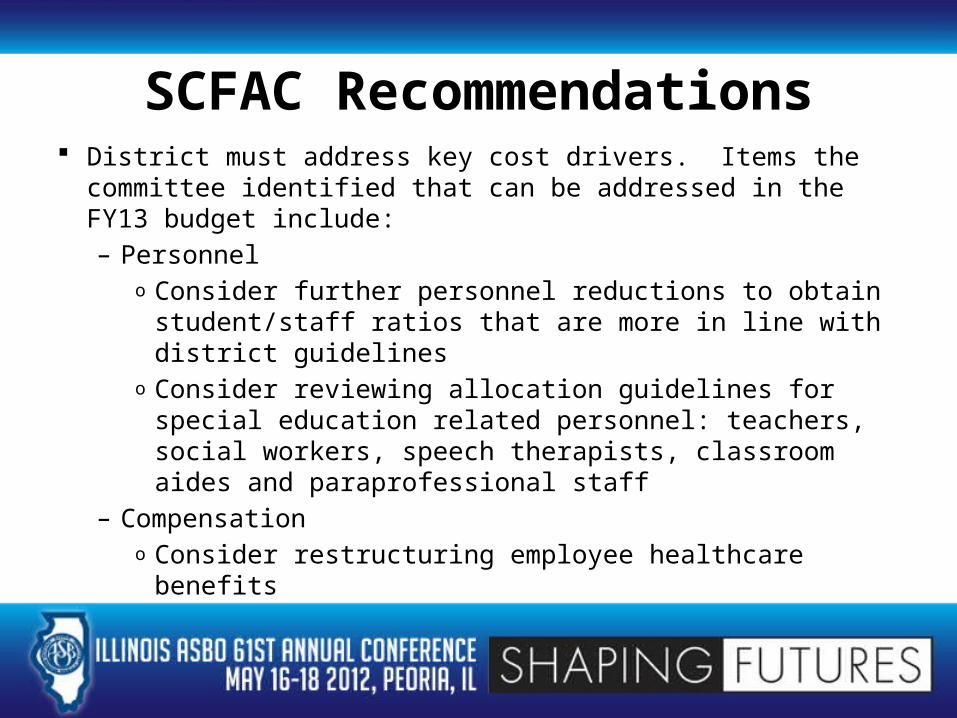

SCFAC Recommendations District must address key cost drivers. Items the committee

identified that can be addressed in the FY13 budget include:– Personnel

o Consider further personnel reductions to obtain student/staff ratios that are more in line with district guidelines

o Consider reviewing allocation guidelines for special education related personnel: teachers, social workers, speech therapists, classroom aides and paraprofessional staff

– Compensationo Consider restructuring employee healthcare benefits

Strong reserve balance Strong tax base Good financial

management Low debt level /

Capacity for additional debt

Valuable real estate assets

Strong credit rating High tax collection

rates High revenue per

student Engaged community

perceives high value

Financial Strengths

ANY QUESTIONS???