Emerging Accountable Care Models: Paradigm Shift from Volume to Value Shelley Price, MS, FHIMSS Director, Payer and Life Sciences, HIMSS DISCLAIMER: The views and opinions expressed in this presentation are those of the author and do not necessarily represent official policy or position of HIMSS. @SPriceHIMSS | #GovHIT

Transcript

Emerging Accountable Care Models: Paradigm Shift from Volume to ValueShelley Price, MS, FHIMSSDirector, Payer and Life Sciences, HIMSS

DISCLAIMER: The views and opinions expressed in this presentation are those of the author and do not necessarily represent official policy or position of HIMSS.

• Understand trends and drivers in healthcare reform from a volume-based system to a value-based system in both the private and public sectors

• Recognize and connect the common themes, issues and challenges between Population Health, new Payment Models, and Accountable Care Organizations

• Learn about new partnerships and efforts toward collaborative, accountable care

• Gain knowledge of the role of data and health IT in driving toward transformation through population health and new payment and delivery models

Agenda

• Healthcare Reform: Why and How

– Driving toward transformation through population health and new payment and delivery models

• Themes, Issues and Challenges

– Population Health

– Payment Models

– Accountable Care Organizations

• Case Studies

• Data and HIT

• HIMSS Resources

• Take-aways

• Questions

Healthcare Reform

Volume to Value

Disease/Acute Care to Wellness/Chronic Disease Mgt

• Trends

• Drivers

Triple Aim

Market competition

ACA

Public outcry

How Do We Get There?

Population Health

Enabler: New Payment and

Delivery Models

Sample Vehicle: ACOs

Pt 1. Population Health Management

• Definition: Public health vs. population health “…from a public health perspective, populations are defined by

geography of a community (e.g., city, county, regional, state, or national levels); and

from the perspective of the delivery system (individual providers, groups of providers, insurers, and health delivery systems), population health connotes a "panel" of patients served by the organization.”

• CMS for new payment models, private payers, State Medicaid

– Data venues:

• public health, HIEs, payers, Enterprise

– Data users:

• Researchers, analysts, consultants

PHM: Issues – Needs & Challenges

• Starting up

– C-Suite: How do I begin? Where do I begin? Sure it’s the way of the future…but I am overwhelmed with (go-live, ICD-10, reporting, et al); how can I start in on this?

• Lack of a business plan

• Project management problem

• Available technology ‘toolkits’

– Many ‘solutions’

– Is it right for me? How do I use it?

• Data

– Access

– Architecture

– Timeliness

• Funding

– Initial investment cost; maintenance for activities; limited alternative payment models

• Staffing

– New skills needed (e.g. PHIM, analytics)

– Staffing shortages

Pt 2: Payment Models

• Enabler to Change

– Reimbursement incentivizes action

– Need financial framework to support health/healthcare change

• Drivers: Triple Aim

– Public Outcry

– Public Policy

• ACA

• Pending SGR reform

– Healthcare market competition

• Providers

• Payers

• IT vendors

Triple Aim

Market competition

ACA

Public outcry

Pt 2: Payment Models

• Examples of Models

FFS

DRG

Bundled payments

VBPVBID

P4P

Gain-sharing

PCMH/ACOs

Global payments

What’s the HIT component?

– Benchmarking

– Outcomes analysis and allocation

– Quality measure reporting

– Analytics

– Risk-sharing

Pt 3: Accountable Care OrganizationsYou’ve Seen One, Then You’ve Seen One

• What | Who | How?

– In general……

• What / Definition / Purpose:

– A group of defined providers working collaboratively, connectively, within a risk-baring structure to improve quality, heath outcomes, and costs of a defined patient population

• Who / Stakeholders:

– Primary: Large hospital systems, large group practices, small-group practices, primary care providers, payers (public and private), IT solution vendors

• Costs and Savings (3 years)– Total savings: $470M (Federal) – Bonuses to ACOs: $1.31B – Penalties from ACOs: $20M– Average ACO startup cost incl 1st yr operating: $.58M

Federal Programs Today (MSSP)

1. April 10, 2012: 27 selected

– Est. 375,000 beneficiaries, 10,000 physicians, 10 hospitals, 13-smaller physician-driven

organizations in 18 States

2. July 9, 2012: 89 selected

– Est. 1.2 million beneficiaries in 40 States and Washington, D.C.

3. Jan 10, 2013: 106 selected

– 47 States, PR, and DC are now served

– Increasing trend toward physician-led practices (approx half of new group)

• serving <10,000 beneficiaries each; approx 20 percent CHCs, rural health clinics and

CAH

4. Dec 23, 2013: 123 selected

– Est. 1.5 million additional beneficiaries

– Focus on underserved: 1 in 5 ACOs include CHCs, rural health clinics, and CAH that serve

– Physician Group Practice Transition Demonstration

• January 2012: 6 organizations

• All Told: more than 5.3 million beneficiaries through nearly 400 organizations in all states except Delaware are receiving care from providers participating in CMS initiatives

4 million Medicare beneficiaries having care coordinated by 220 MSSP and 32 Pioneers ACOs(Geographic Distribution of ACO Population)

21Source: Centers for Medicare & Medicaid

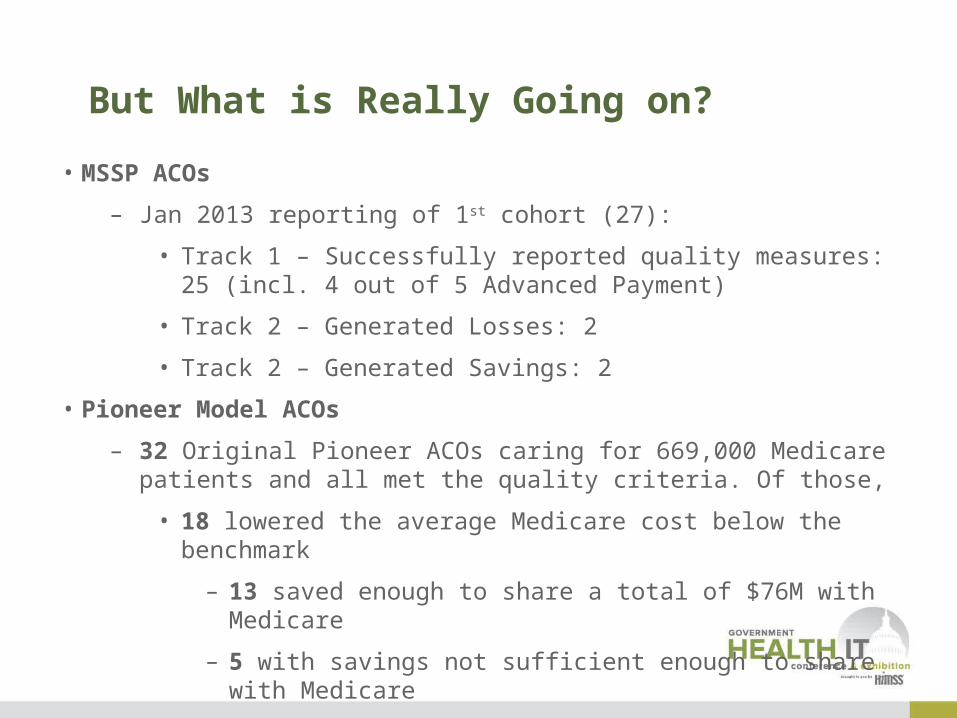

But What is Really Going on?

• MSSP ACOs

– Jan 2013 reporting of 1st cohort (27):

• Track 1 – Successfully reported quality measures: 25 (incl. 4 out of 5 Advanced Payment)

• Track 2 – Generated Losses: 2

• Track 2 – Generated Savings: 2

• Pioneer Model ACOs

– 32 Original Pioneer ACOs caring for 669,000 Medicare patients and all met the quality criteria. Of those,

• 18 lowered the average Medicare cost below the benchmark

– 13 saved enough to share a total of $76M with Medicare

– 5 with savings not sufficient enough to share with Medicare

Payer-Provider Collaboration• Provider partners are diverse• Payer-involvement varies from

o TPA/MSOo First-payer status (temporary

exclusivity)o True collaborative partner

Single-Provider ACO• Tends to be original entity (Billings

Clinic, Sharp Healthcare)• More likely to be looking to develop in-

house competency (unless existing)• Decision making mechanism is less

likely to see change*

Insurer-Led ACO• More likely to be a physician group

(physician problems)• Insurer likely to retain formulary decisions

Multiple-Provider ACO• High likelihood of separate governing

structures (unless M/A in the works)• Decisions may be joint but purchases are

along original lines (hospital/physician group)

Source: Leavitt Partners Center for Accountable Care Intelligence 2013

Innovation in the Commercial Marketplace

• Commercial Health Plans are engaging with Providers toward Accountable Care. Examples:

– Aetna

• Facilitating the clinical, financial, technological and cultural changes ; Aiding in implementing technology to unlock the power of evidence-based medicine and preventive care

– Example of results: 45% reduction in hospital admissions; 50% fewer patient hospital days; $600 annual savings per patient

– Cigna

• Strong focus on care coordinators and case managers

• 89 ‘collaboratives’ in 27 states

– covering 910,000 lives and

– through 36,000 providers

HIMSS Perspective

Pediatric ACOs

HIMSS TOWN HALL: Understanding the Particular Characteristics of Pediatric Populations and How They Could Impact Accountable Care Organizations

Presentation by Deb Wells, CHOP for the HIMSS ACO Task Force

April 4, 2014

Population Characteristics Compared

Healthy

Chronic Disease

High cost-high risk

Tier Adults Children

Highest cost patients

Multiple chronic conditions such as heart disease and diabetes. With better management patients can drop to the middle tier – often elderly

Rare and complex congenital or genetic diseases. Good management can keep them out of the ED and hospital but their conditions are generally life long

Chronic Disease

Large population with varying degrees of disease control, big opportunity for cost savings

Relatively small population with 1 or 2 chronic conditions such as asthma or ADHD

Healthy patients

Depending on who you ask 60-75% of patients

Most kids, with focus on prevention, growth & development

Meet the Family

School & Day Care

Community

Services

Dentist

Behavioral Health

Adoption & Foster

Care

Sports

Primary Care

Sub-Specialty

Care

Pharmacy Head

Start & Others

Long-term & Rehab

Home Care

Hospital

Minute Clinics

Pediatric Specialty

Unique ServicesSometimes the

Same for Routine Care Eye

Care

Summer Camp

Orthodontist

FamilyPatien

t

Key Issues• Kid’s unique medical needs and social environment necessitate care from

pediatric-trained physicians and child-specific community resources such as schools

• It is essential to select performance metrics that are meaningful to pediatrics and that accurately measure the quality of pediatric care

• Population characteristics and scarce sub-specialists require a regional vs local provider base

• Technology needs to include functionality to support pediatric care

• Children with medical complexity usually have many subspecialists and rely on community resources and will need special care throughout their lives

• The family is generally responsible for a child’s health care, rather than the patient him- or herself

• Federal leadership provided by Medicare is lacking in Medicaid, but states have begun working with providers to form Medicaid ACOs

• A largely healthy population means that a larger number of patients is needed to show significant cost savings

Influencing Quality and the Payer Relationship with C&BI

CASE STUDY by the C&BI Value Task ForceApril 4, 2014

Key Issues• Current coding and FFS program not

sufficient nor indicative of quality in complex obstetrics cases

• Hawaii Pacific Health and Hawaii Medical Service Association (BCBS) partnered on obstetrics program

• Contract tying reimbursement to outcomes synchronously achieved patient outcomes and fiscal objectives

• Results:

– State-of-the-art obstetrical service line

– Decrease in C-Section in low-risk deliveries

– Value-based payments: Increase to 15% of payments

– New contract: moving to 50% of payment value-based

Data and HIT

• Data warehousing• Healthcare data integration• Enterprise analytics• Predictive analytics• Population health

Financial Data

Clinical Data

Operational Data

Hope & promise….

and the challenge

Clinical & Business Intelligence – Turn Data into Action

“Defensive” Risk Management• Readmissions Management • Chronic Disease Detection • Inpatient Length of Stay Management • At Risk Population Detection • Hospital Acquired Condition Prevention

“Offensive” Risk Management• Chronic Care Management • Tailored Benefit Design • Wellness Program Management • Disease Detection & Early Intervention

PHM and ACO Common ChallengesSome common clinical analytics: