196

Gianni Amisano Carlo Giannini Topics in Structural VAR Econometrics 2nd edition

| Date post: | 17-May-2018 |

| Category: |

Documents |

| Upload: | nguyenkien |

| View: | 215 times |

| Download: | 1 times |

Gianni Amisano Carlo Giannini Topics in Structural VAR Econometrics 2nd edition

iv

Gianni Amisano Carlo Giannini Dipartimento di Dipartimento di Economia Scienze Economiche Politica e Metodi Quantitativi Università di Brescia Università di Pavia Via Porcellaga, 21, via S. Felice, 5 25121 Brescia, Italy 27100, Pavia, Italy [email protected] [email protected]

v

To Anne, Vittoria and Andrea

vi

vii

Foreword In recent years a growing interest in the structural VAR approach

(SVAR) has followed the path-breaking works by Blanchard and Watson (1986), Bernanke (1986) and Sims (1986), especially in the U.S. applied macroeconometric literature. The approach can be used in two different, partially overlapping, directions: the interpretation of business cycle fluctuations of a small number of significant macroeconomic variables and the identification of the effects of different policies.

SVAR literature shows a common feature: the attempt to "organise", in a "structural" theoretical sense, instantaneous correlations among the relevant variables. In non-structural VAR modelling, instead, correlations are normally hidden in the variance-covariance matrix of the VAR model innovations.

VAR analysis tries to isolate ("identify") a set of independent shocks by means of a number of meaningful theoretical restrictions. The shocks can be regarded as the ultimate source of stochastic variation of the vector of variables which can all be seen as potentially endogenous.

Looking at the development of SVAR literature we felt that it still lacked a formal general framework which could embrace the several types of models so far proposed for identification and estimation.

This is the second edition of the book, which originally appeared as number 381 of the Springer series "Lecture notes in Economics and Mathematical Systems". The author of the first edition was Carlo Giannini.

The second edition is a revised and augmented version of the first one, where the additional parts focus on a series of issues and developments in the econometric literature, and are motivated by the many questions addressed to the author of the first edition by different researchers. These issues were developed and discussed within a research group including Rocco Mosconi (Dipartimento di Economia e Produzione, Politecnico di Milano), Mario Seghelini (Research Unit, Deutsche Bank, Milan) and the two authors of this second edition.

In our view, it is very difficult to attribute most of the new parts of the book specifically to any of the two co-authors. Nevertheless,

viii

the absolute majority of the new parts originate from the contribution of the new co-author, who has largely benefited from the material and the results contained in his Ph.D. thesis.

The second edition of this book is justified, beside the fact that the first one was sold out, by the many developments in VAR econometrics, especially in cointegration analysis, which rendered the previous edition of the book inadequate, since it just contained some summary indications in that respect. We felt that it was necessary to discuss all the methodological and practical issues connected to the application of the Structural VAR framework to cointegrated settings.

Moreover, we had to take into account the problem raised in a series of papers by Marco Lippi, Lucrezia Reichlin and Danny Quah, and related to the existence of non fundamental representations. In this book we discuss at length the relevance of this problem, in the light of the existing literature, and we present a new method, based on the estimation of VARMA models, of checking whether the validity of the dynamic simulations obtained from a structural model is affected by the relevance of non fundamental representations. Nevertheless, we believe that on this problem other work will be necessary. Appendix D of the first edition has been eliminated from the second edition. This appendix contained the description of two RATS (written by Antonio Lanzarotti and Mario Seghelini) performing the estimation and the dynamic simulation of Structural VAR models. These two procedures, now available at the ESTIMA WWW site (http://estima.com), were not immediately applicable to the analysis of cointegrated systems. For this reason, they have been modified by Gianni Amisano and Mario Seghelini and they are now incorporated as a Structural VAR Analysis menu of the menu driven RATS computer package MALCOLM (MAximum Likelihood analysis of COintegrated Linear Models), written by Rocco Mosconi1 (see Mosconi, 1996) and designed to perform VAR and Structural VAR analysis in possibly cointegrated systems. Most of

ix

the computations described in chapter 9 of this book were performed by using the MALCOLM package. MALCOLM will be available on the Internet at the following URL: http://vega.unive.it/~alex/GRETA/MALCOLM..

The general structure of the second edition of this book is as

follows. Chapter 1 introduces the main concepts of VAR analysis. Following Rothenberg (1971, 1973), chapters 2, 3 and 4 develop

a methodological framework for three types of models (models K, C and AB) which encompass all the different models used in the applied literature. In fact, looking at a selected choice of recent SVAR applied papers one can see the following correspondence with regard to the categorisation put forward in this book: Blanchard and Watson (1986) is an example of K-model; Blanchard and Quah (1989) and Shapiro and Watson are examples of C-models; Bernanke (1986) and Blanchard (1989) are examples of AB-models.

We have also tried to generalise the identification and the estimation set-up by using the most general type of linear constraints available for the representation of beliefs on the organisation of instantaneous responses of the endogenous variables to "exogenous" independent shocks.

Building on Lütkepohl (1989, 1990), chapter 5 contains calculations of the asymptotic distributions of impulse response functions and of forecast error variance decompositions. In this chapter, we also describe the possibility of using bootstrapping or Monte Carlo integration techniques. Section 5.3 was written by Antonio Lanzarotti.

Chapter 6 includes deals with the treatment of deterministic components, long run constraints in a stationary context, and gives a detailed account of how to use Structural VAR analysis in the presence of (possibly) cointegrated series: In order to do that it was necessary to discuss at length the inferential and modelling issues arising in the presence of cointegration.

In chapter 7 we explain how to use the dominance ordering and the likelihood dominance criteria introduced by Pollack and Wales (1991) as model selection devices in Structural VAR analysis, in order to choose among alternative structuralisations of the same unstructured VAR model.

x

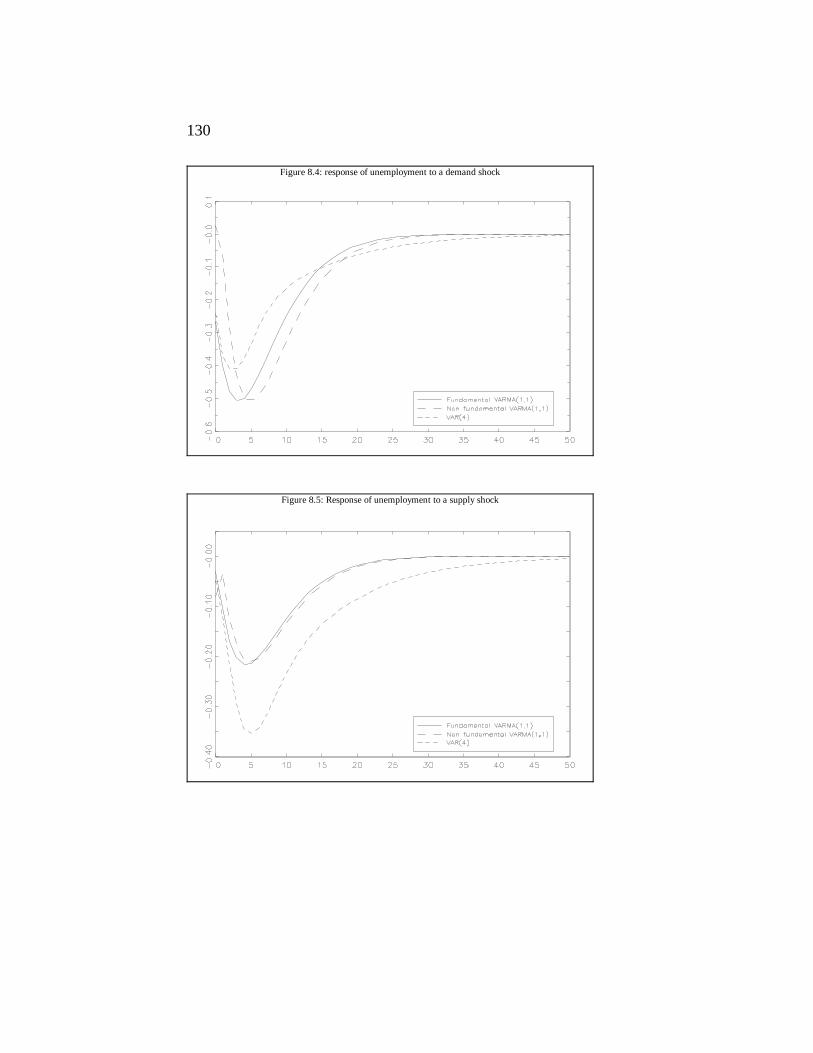

In chapter 8, we describe how to cope with the problems induced by the relevance of non fundamental representations.

Chapter 9 tries to offer deeper insights into SVAR modelling by providing the results of two applied exercises carried out on Italian data sets by using AB-models.

Annex 1 deals with the notion of structure in SVAR modelling, while Annex 2 contains our point of view on the meaning of each of the three types of models discussed in this book. We also try to suggest some criteria on which model to choose in different applications together with some general considerations on their overall working.

Appendix A briefly summarises rules and conventions of matrix differential calculus adopted in this monograph.

Appendix B contains the calculation of the first order conditions for the maximisation of the likelihood of the K-model and the corresponding Hessian matrix.

Appendix C has been written jointly by Antonio Lanzarotti and Mario Seghelini and it contains some examples of symbolic identification analysis for the K, C and AB models.

We wish to thank Fabio Canova, Lorenzo Cella, Riccardo Cristadoro, Carlo Favero, Jack Lucchetti, Massimiliano Serati, Ken Wallis and Sanjay Yadav for useful discussions, and Mario Faliva for providing useful algebraic references. We are also indebted to S. Calliari, J.D. Hamilton, M. Lippi, J.R. Magnus, H. Neudecker, R. Orsi, P.C.B. Phillips, D.S.G. Pollock, H.E. Reimers and to the unknown Springer referee, for their suggestions and encouragements after reading the first version.

Special thanks are due to Antonio Lanzarotti and Mario Seghelini, both for their contributions and for their suggestions. They have accompanied us through a journey started in a fog of confused ideas.

An important acknowledgement is due to the work of Rocco Mosconi. His superb econometric competence and programming skills are clearly witnessed by the quality of his MALCOLM package, which has been extensively used by the authors in order to apply the techniques documented in this book. Beside that, his scientific support has been crucial in different stages of our work.

xi

Finally, we want to thank our families, to which this book is dedicated.

The usual disclaimer obviously applies. Brescia and Pavia, August 1996.

Contents Foreword vii Chapter 1: From VAR models to Structural VAR models 1 1.1. Origins of VAR modelling 1 1.2. Basic concepts of VAR analysis 2 1.3. Efficient estimation: the BVAR approach 6 1.4. Uses of VAR models 10 1.4.1. Dynamic simulation 10 1.4.2. Unconditional and conditional forecasting 11 1.4.3. Granger causality 13 1.5. Different classes of Structural VAR models 15 1.6. The likelihood function for SVAR models 19 1.7. Structural VAR models vs. dynamic simultaneous equations models 22 1.8. Some examples of Structural VARs in the applied literature 23 1.8.1. Triangular representation deriving from the Choleski decomposition of Σ 24 1.8.2. Blanchard and Quah (1989) long run constraints 24 1.8.3. A traditional interpretation of macroeconomic fluctuations: Blanchard (1989) 26 Chapter 2: Identification analysis and F.I.M.L. estimation for the K-Model 29 2.1. Identification analysis 29 2.2. F.I.M.L. estimation 36 Chapter 3: Identification analysis and F.I.M.L. estimation for the C-Model 40 3.1. Identification analysis 40

xii

3.2. F.I.M.L. estimation 45 Chapter 4: Identification analysis and F.I.M.L. estimation for the AB-Model 48 4.1. Identification analysis 48 4.2. F.I.M.L. estimation 57 Chapter 5: Impulse response analysis and forecast error variance decomposition in SVAR modelling 60 5.1. Impulse response analysis 60 5.2. Variance decomposition (by Antonio Lanzarotti) 67 5.3. Finite sample and asymptotic distributions for dynamic simulations 73 Chapter 6: Long run a priori information. Deterministic components. Cointegration 78 6.1. Long run a priori information 78 6.2. Deterministic components 82 6.3. Cointegration 85 6.3.1. Representation and identification issues 88 6.3.2. Estimation issues 91 6.3.3. Interpretation of the cointegrating coefficients 98 6.3.4. Asymptotic distributions of the parameter estimates: Structural VAR analysis with cointegrated series 100 6.3.5. Finite sample properties 103 Chapter 7: Model selection in Structural VAR analysis 107 7.1. General aspects of the model selection problem 107 7.2. The dominance ordering criterion 108 7.3. The likelihood dominance criterion (LDC) 111 Chapter 8: The problem of non fundamental representations 114 8.1. Non fundamental representations in time series models 114 8.2. Economic significance of non fundamental representations and examples 118 8.3. Non fundamental representations and applied SVAR analysis 120

xiii

8.4. An example 125 Chapter 9: Two applications of Structural VAR analysis 131 9.1. A traditional interpretation of Italian macroeconomic fluctuations 131 9.1.1. The reduced form VAR model 132 9.1.2. Cointegration properties 133 9.1.3. Structural identification of instantaneous relationships 134 9.1.4. Dynamic simulation 135 9.2. The transmission mechanism among Italian interest rates 136 9.2.1. The choice of the variables 136 9.2.2. The reduced form VAR model 137 9.2.3. Cointegration properties 139 9.2.4. Structural identification of instantaneous relationships 143 9.2.5. Dynamic simulation 145 9.2.6. The Lippi-Reichlin criticism 149 Annex 1: The notions of reduced form and structure in Structural VAR modelling 151 Annex 2: Some considerations on the semantics, choice and management of the K, C, and AB-models 154 Appendix A 159 Appendix B 162 Appendix C (by Antonio Lanzarotti and Mario Seghelini) 165

References 174

xiv

1

Chapter 1 From VAR models to Structural VAR models

In this chapter we introduce the philosophy, the basic concepts and definitions of VAR analysis (sections 1.1 and 1.2). After that, in section 1.3 we discuss the problems of VAR estimation and in section 1.4 we describe the possible uses of VAR models. Then in section 1.5 we start dealing with Structural VAR analysis, pointing out the main features of the different classes of Structural VAR models, their likelihood functions (section 1.6) and their differences with respect to the standard simultaneous equations models (section 1.7). We conclude this chapter by providing examples of Structural VARs taken from the applied econometric literature (section 1.8). 1.1. Origins of VAR modelling

Before the last two decades, the traditional econometric analysis used to rely on the specification and estimation of large scale structural simultaneous models, in order to analyse the interactions between sets of macroeconomic variables. Uses of those systems ranged from forecasting to policy analysis and testing of competing economic theories. The research activity conducted by the Cowles Commissions in the United States in the period 1945-1970 was entirely based on such large scale models, whose specification was mainly inspired by theoretical considerations derived from the (then) prevailing Keynesian paradigm.

In the 1970s this approach to macroeconometric modelling came under fierce attack on different fronts. Firstly, the great turbulence of those years and the instability connected to unprecedented events such as the collapse of the Bretton Woods system and the oil shocks led to a widespread forecasting failure of the vast majority of the main macroeconometric models. Secondly, the economic profession started questioning the validity of Keynesian theories, and to advocate the use of models with an explicit treatment of the role of rational agents' expectations, in order to correctly represent the interactions among macroeconomic variables. Overlooking the forward-looking rational behaviour of agents would produce

2

structural models incapable of delivering correct answers to the usual policy analysis exercises.

Thirdly, the specification methodology of large scale macroeconometric models was deeply criticised by C.A. Sims (1980, 1982), who emphasised two different methodological weaknesses: i) the specification of simultaneous equations systems was largely based on the aggregation of partial equilibrium models, without any concern for the resulting omitted interrelations. ii) the dynamic structure of the model was often specified in order to provide restrictions necessary to achieve identification (or over-identification) of the structural form.

Motivated by these criticisms, Sims suggested scrapping Simultaneous Equations Systems altogether, and to use models whose specification had to be founded on the analysis of the statistical properties of the data under study. In fact, Sims suggested to specify vector autoregressions (VARs), i.e. multivariate models where each series under study is regressed on a finite number of lags of all the series jointly considered. Clearly, in a VAR model instantaneous relationships among variables are not accounted for and are "hidden" in the instantaneous correlation structure of the error terms.

Since the original proposal of Sims, VARs have encountered a widespread success: in many research environments they have supplanted traditional Simultaneous Equations Systems and they have proved to be very useful and flexible statistical tools. However, as it will soon become apparent, the main conceptual problem in their use is related to the interpretation of the instantaneous correlations among error terms, and therefore among observable variables. The structural VAR analysis is based on the attempt to give a sensible solution to this problem, based on the imposition of a set of restrictions. These restrictions become testable when they allow an over-identified structure to be obtained.

1.2. Basic concepts of VAR analysis

In order to introduce the basic elements of VAR analysis, let us suppose that we can represent a set of n economic variables using a vector (a column vector) yt of stochastic processes, jointly

3

covariance stationary without any deterministic part and possessing a finite order (p) autoregressive representation.

A(L) yt = εt A(L) = I-A1L-... -Ap L

p The roots of the equation det[A(L)] are outside the unit circle in

the complex domain and εt has an independent multivariate normal distribution with 0 mean.

εt ~ IMN(0,Σ) E(εt) = 0 E(εt εt′) = Σ det(Σ) ≠0 E(εt εs′) = [0] s ≠ t

In other words εt is a normally distributed vector white noise (henceforth VWN).

The yt process has a dual Vector Moving Average representation (Wold representation)

yt = C(L) εt C(L) = A(L)-1 C(L) = I + C1L + C2 L

2 +... where C(L) is a matrix polynomial which can be of infinite order and for which we assume that the multivariate invertibility conditions hold, i.e. det[C(L)] = 0 has all the roots outside the unit circle, so

C(L) -1 = A(L) From a sampling point of view, let us suppose that we have T+p

observations for each variable represented in the yt vector; we are thus able to study the system

A(L)yt = εt t = 1,... T This system can be conceived as a particular reduced form (in which all variables can be seen as endogenous).

In order to relate our discussion to the usual Simultaneous System formulae, this latest system can be re-written in compact form as follows (in relation to more usual Structural Simultaneous System Formulae we are assuming a "transposed" notation):

Y = A1Y-1 + A2Y-2 +... + ApY-p + V or even more compactly:

Y = Π X + V where

Y = [y1, y2,..., yT ] Y has dimension (n ×T)

4

Y-i = [y1-i, y2-i,..., yT-i ] Y has dimension (n×T) V = [ε1, ε2,..., εT ] V has dimension (n × T) Π = [A1, A2,..., Ap ] Π has dimension (n × np) X = [Y-1′, Y-2′,..., Y-p ′]′ X has dimension (np × T) If no restrictions are imposed on the Π matrix, the formulae for

asymptotic least squares estimation and maximum likelihood estimation of Π, say $Π , coincide:

$ ' ( ' )Π = −Y X XX 1

Notice that on the basis of this formula, the estimator $Π is independent of the variance-covariance matrix of the error terms εt.

Under the hypothesis that the elements of yt are stationary, we can assume that

[ ] [ ]plimT

ET

t t t t t t p→∞

− − −= = =XX Q x x x y y y' ( ' ) , ' , ' ,... ' '1 2

where Q is a positive definite matrix. Under the hypotheses introduced, it can be easily shown that

T vec vec Nd

( $ ) ( , )Π Π Σ Π− → 0 where the symbol vec A shall indicate, as usual, the column vector obtained by stacking the elements of the A matrix column after

column, d

→ means convergence in distribution (hereafter we shall use usual asymptotic notations such as the one contained in White, 1984, and Serfling, 1980) and

Σ ΣΠ = ⊗−Q 1 If no restrictions are imposed on the Σ matrix, its maximum

likelihood estimate will be:

$ $ $ 'Σ = ∑−

=T t t

t

T1

1ε ε

where $ $ $ ... $ε = y A y A y A yt t t p t p− − − −− − −1 1 2 2 , or more compactly:

$ $ $ 'Σ = −T 1VV where $ $V Y X= − Π .

A consistent estimate of ΣΠ is given by: $ ( ' ) $Σ ΣΠ = ⊗−T XX 1

5

Having estimated the VAR parameters, it is possible to obtain an estimate of the VMA representation parameters, by means of the relationship A(L)C(L)=In. This relationship can be conveniently expressed in matrix terms, by means of the companion form of a VAR(p) system:

zt = A zt-1 + ηt, yt = J zt where:

zt = [yt', yt-1',..., yt-k +1']', ηt = [εt′, 0′]′,

[ ]M

A A A A

I 0 0 0

0 I 0 0

0 0 I 0

J I [0] 0=

⎡

⎣

⎢⎢⎢⎢⎢⎢⎢⎢

⎤

⎦

⎥⎥⎥⎥⎥⎥⎥⎥

−1 2 1...

...

...

... ... ... ... ...

...

... [ ]

k k

n

n

n

, = n

which can be used to obtain the vector moving average (VMA representation) as:

y JM J Cti

t ii

i t ii

k= ∑ = ∑−

=

∞

−=

−'ε ε

0 0

1.

Expression above shows how the VMA parameters can be seen as non linear functions of the VAR parameters. The VMA parameters can be estimated by transformation of the VAR parameters estimates:

$ $ ' ,

$

$ $ ... $ $

...

...

... ... ... ... ...

...

C JM J

M

A A A A

I 0 0 0

0 I 0 0

0 0 I 0

ii

k k

n

n

n

=

=

⎡

⎣

⎢⎢⎢⎢⎢⎢⎢⎢

⎤

⎦

⎥⎥⎥⎥⎥⎥⎥⎥

−1 2 1

The asymptotic distributions of VMA parameters estimates will be described in detail in chapter 5 and 6. In this section we briefly try to convey the intuition behind the available distributional results.

6

VMA parameters are non linear functions of the VAR parameters, and the asymptotic distribution of the OLS estimator of VAR parameters is known. It is then possible to obtain the asymptotic distribution of VMA parameters in the following way. For ease of exposition, let us suppose we have a VAR model of lag order equal to one 1

yt = A yt-1 + εt, εt ~ VWN (0, Σ) In this particularly simple context, the VMA parameters are

Bi = Ai, i = 1, 2,..., and their estimated counterparts are $ $B Ai

i i = , = 1, 2, ... ,

where $A is the OLS estimate of the VAR parameters with the usual asymptotic distribution

( )T vec vec N1 2/ -1 ~ ( , ).$A A 0 Q− ⊗Σ

Now, we consider vecBi as a function of vecA, and we find its first-order Taylor series expansion around vec $A :

-

-

-

vec vecvecvec

vec vec

vec vec

i ii

i j

j

ij

$ ( $ )

( $ ' ) ( $ ) ( $ )

$

B BBA

A A

A A A A

A A

≈ ⎡⎣⎢

⎤⎦⎥

=

= ⊗∑⎡⎣⎢

⎤⎦⎥

=

−

=

−

∂∂

1

1

from which2 it is possible to obtain

( )

( )

- ~

, -1

T vec vec

N

i i

i j

j

ij i j

j

ij

1/2

1

1

1

1

$

( $ ) ( $ ' ) ( $ ' ) ( $ )

B B

0 A A Q A A−

=

− −

=

−⊗∑⎡⎣⎢

⎤⎦⎥

⊗ ⊗∑⎡⎣⎢

⎤⎦⎥

⎧⎨⎩

⎫⎬⎭

Σ

This result conveys the intuition behind the asymptotic distribution of the VMA parameters, which will be discussed in detail in chapter 5.

1 Models with higher dynamics can be treated in exactly the same way. 2 It is easy to see that the terms with order higher than one are asymptotically negligible.

7

1.3. Efficient estimation: the BVAR approach We have already said in this chapter that the maximum likelihood

estimator of the VAR parameters asymptotically coincides with the OLS estimator. The immediate consequence of this fact is that in principle, the estimation of stationary VAR models can be done in a very easy and inexpensive way3, and the resulting estimates are clearly consistent.

In practice though, one of the most serious problems encountered when using VAR models is that these models often have a very high number of free parameters to be estimated. The VAR model has in fact a "profligate parameterization" (Sims, 1980): the number of parameters to be estimated in a VAR of order p is equal to n2 p + n (n +1)/2. For this reason only very small VAR models can be satisfactorily estimated by OLS or maximum likelihood, whereas the VAR analysis of vector series with dimension higher than 5 or 6 is usually precluded by a shortage of degrees of freedom in the typical sample sizes. In such cases, OLS estimates of VARs are typically inefficient, since the sample information is used to estimate a large number of parameters. As a result, the model becomes unreliable for inference in general, and for forecasting in particular.

Since the very start of the VAR literature, this over-parameterisation problem has always been carefully considered. Many different approaches have been proposed in order to obtain more efficient estimates in VAR models. All these approaches, in one way or another, are based on the attempt to constrain somehow the free parameters space4. A particularly successful approach is the use of Bayesian estimation techniques. This approach was first introduced by R. Litterman (1979, 1985) and Doan, Litterman and Sims (1984, henceforth DLS). In this section we briefly describe how the BVAR estimation approach works, and how it can be used to produce more efficient consistent estimates.

3 Things are a bit more complicated in the presence of cointegrated I(1) variables. In such case, the system can also be estimated via maximum likelihood with or without the imposition of the cointegrating rank constraints. For details see chapter 6. 4 See Lütkepohl (1991), chapter 5.

8

In a Bayesian setting, data are not the only sources of information, but they are combined with prior beliefs in order to produce a posterior probability density function (pdf) for the parameters. Imposing these prior beliefs in terms of a prior pdf amounts to somehow constraining the free parameter space, given that the specification of a prior pdf can be seen as the imposition of stochastic (i.e. subject to noise) constraints on the free parameters.

Let us consider the ith equation of the VAR: yit = xt' βi + εit, εit ~ N(0, σi

2) where xt is conveniently defined to include the first p lags of all the variables included in the VAR system.

We call θi = [βi ', σi 2

]' the vector of parameters appearing in the i-th equation. Then, the (partial) likelihood function for the ith equation reads

L(θ|y) = p(y|θ) = (2 π σi 2)-T/2 exp [-(1/2 σi

2) εi ' εi ], εi = [εi1, εi2,..., εiT] '. Classical inference consists in maximising the likelihood

function, in order to obtain an estimate of the parameters. Along with this point estimate, comes an estimate of the associated uncertainty, which is used to construct confidence intervals and to perform hypothesis testing.

The Bayesian approach is radically different: in the Bayesian analysis, there is no such thing as a "true" unknown value of the parameters. On the contrary, these are considered as random unobservable variables, on which the researcher might have some extra-sample (prior) information which is formalised as a "prior" distribution p(θi). Sample and non-sample information are combined by means of Bayes' theorem:

p(θ|y) = p(θ) p(y| θ)/ [∫ p(θ) p(y| θ)d θ ] = p(θ) p(y| θ)/p(y) ∝ p(θ) p(y| θ) The distribution p(θ|y) is called the "joint posterior distribution"

of the parameter vector. This pdf measures the uncertainty on the parameters which results after combining all the sources of available information. This posterior pdf is then used to obtain a point estimate of the parameter vector, usually given by the mode (say $θ ) or the expectation of the posterior pdf.

9

From a different viewpoint, and focusing only on the first order parameters βi, one can think of having prior information about q linear combination of the parameters in the form:

R βi = d + e0, E(e0) = 0, var(e0 e 0') = Σ0 This formulation differs from the usual linear constraints in that

the extra-sample information about βi is subject to error, which implies prior uncertainty.

Considering extra-sample information as q additional observations leads to a feasible GLS mixed estimator

~β i = [ $σ −2 X'X+ R' Σ0

-1 R]-1[ $σ −2 X'y+ R' Σ0-1d], (1.1)

var( ~β )= [ $σ −2 X'X+ R' Σ0

-1 R]-1,

where $σ 2 is any consistent estimate of the i-th equation error terms variance. The expression above corresponds to the well-known Theil-Goldberger (1961) mixed estimator. Litterman (1979) showed that ~

β i is an approximation of the posterior pdf mode, and can be used as a point estimate of the parameter vector.

In order to render the mixed estimation procedure operational, it is necessary to provide a prior distribution for the parameters of the model. In the classical BVAR literature (see for instance Litterman, 1979, 1986, DLS, 1984), the prior is specified taking into consideration that most observed economic time series have long run behaviour similar to that of a random walk process. This remark can be accommodated into a prior distribution framework by requiring that in every equation the parameter on the first lag of the dependent variable is given prior mean equal to one, and all the other parameters are given zero prior mean. This specification of the prior has become standard in the classical BVAR literature and the resulting prior has been termed Minnesota prior 5.

The second moments of the prior distribution are specified on the grounds of two considerations: 1) For easing the computations, the parameters in each equation are assumed as a-priori uncorrelated. In this way, the prior variance-covariance matrix of the parameters is clearly diagonal. 2) As regressors for yit, the own lags of yit are more

5 The term “Minnesota prior” arose because this approach was developed when both Sims and Litterman were at the University of Minnesota.

10

important than the lags of the other elements of the vector yt, and the importance of the single lag decreases with the lag order.

These considerations can be reflected in a prior distribution where the prior variances of the single autoregressive parameters aij,k are devised to become smaller as k increases, and when i≠j. This aim is accomplished in the classical BVAR literature by specifying prior variances according to the choice of a small set of hyperparameters as follows:

[var (aij,k)]1/2= s(aij,k) = γ k- δ f (i,j) σii /σjj, f (i,i) = 1, f (i,j) < 1 for i≠j,

and σii and σjj are the standard errors of the error terms in the i-th and j-th equations. These quantities appear in order to render scale-free the prior variance of aij,k, and in the application of the feasible mixed estimator they must be substituted with consistent estimates (say $σ ii and $σ jj). Calling Σ0 the resulting prior variance covariance matrix, the mixed estimator defined by expression (1.1) can be implemented 6 yielding VAR parameter estimates which are generally more efficient than the usual OLS estimates

The operational simplicity of the Minnesota prior approach is that the prior itself is governed by the choice of a finite set of hyperparameters, which should reflect the intensity of prior beliefs. In the applied BVAR literature though, the hyperparameters cannot be interpreted as reflecting subjective information and their choice is conducted as to optimise the forecasting performances of the model (see for instance DLS,1984)

Therefore, the results of the application of the BVAR procedure are

~( )A L and

~Σ , which are consistent estimates of the auto-

regressive parameters and of the unstructured errors variance covariance matrix. Like the usual OLS or maximum likelihood estimates, these Bayesian estimates can be used as a starting point for the estimation of a Structural VAR. Examples of this procedure are Sims (1986) and Canova (1991).

6 In the BVAR approach it is also possible to specify time varying VAR models, which are then estimated by means of Kalman Filter (see DLS, 1984). These models can be very useful for forecasting purposes, but less indicated for the dynamic simulation purposes typical of SVAR models.

11

1.4. Uses of VAR models

We have already seen that a VAR model is just a reduced form where instantaneous correlations are left uninterpreted. Nevertheless, a VAR model, can be used satisfactorily for a wide range of purposes, which are illustrated in the next three sub-sections. 1.4.1.Dynamic simulation

Imagine that the researcher is interested in the dynamic interactions among the variables in yt, say the effects on yi of a change occurred in yj h periods before. In this case it is possible to refer to the VMA representation of the VAR

yt = C(L) εt and imagine to perturb yjt with a shock εjt equal to one. The effect of this shock on yit+h could then be measured by the VMA coefficient cijh, i.e. the i-th row, j-th column element of the matrix Ch. The problem is that such a measure would not take into consideration the instantaneous correlations existing among the elements of εt and measured by the extra-diagonal elements of Σ. For this reason, it would not be legitimate to perturb one element of εt leaving the others to zero.

Therefore, a VAR model cannot be correctly used for dynamic simulations unless the researcher is ready to provide an interpretation of the instantaneous correlations among the elements of εt. This interpretation is called Structuralisation of the VAR. The issue of how to conduct dynamic simulations with Structural VARs will be analysed in detail in chapter 5. 1.4.2. Unconditional and conditional forecasting

A VAR model can be easily used to generate conditional and unconditional forecasts. From the theoretical point of view, we define the information available at T as the set

IT ={yτ: τ ≤ T} = {ετ: τ ≤ T} It is well known that the optimal linear forecast of yT+h given IT is the conditional expectation

12

y A y C

y y

t h t i t h i ti

p

i t h ii h

T T

+ + −=

+ −=

∞

= =

= ∀ ≤

∑ ∑| |

|

,1

ε

τ τ τ

Hence, the estimated VAR, or its dual estimated VMA representation can be used to obtain consistent estimates of the expressions above as:

$ $ $ $ $ ,

$

| |

|

y A y C

y y

T h T i T h i Ti

p

i T h ii h

T T

+ + −=

+ −=

∞

= =

= ∀ ≤

∑ ∑1

ε

τ τ τ

In this way, the estimated BVAR can be mechanically used to generate unconditional forecasts on the future values of the endogenous variables considered in the model.

This is of course straightforward, but two conceptual problems do arise. First of all, confidence intervals around point forecasts should be provided, in order to explicit the uncertainty connected to the estimation and extrapolation of the model. In principle, since multi-step forecast errors are continuous non-linear functions of the VAR parameters estimates, it is possible to obtain asymptotic distributions for the forecast errors, in the same way as asymptotic distributions can be found for the VMA parameters. Alternatively, finite sample forecast error variances estimates can be obtained numerically, for example resorting to bootstrapping techniques.

Another conceptual problem arises when the researcher wants to forecast conditional on some future values of the endogenous variables. The most appropriate way to consider this problem is to look at the VMA representation, and to imagine that conditioning on some future values of y entails to condition on some future non-zero values of the disturbances ε; in other words, some of the future ε's have to be different from zero in order to generate the future values of the y's which represent the scenario of the forecast. Given the contemporaneous correlation structure of the ε's given by the Σ matrix, it is conceptually inappropriate to impose non zero values to some elements of εT +j, whereas some others are left equal to zero. It is necessary then to work with the orthogonalised VMA representation yt = Φ(L) et, Φi = Ci P, PP' =Σ, et = P-1 εt

13

where P is the Choleski factor of Σ. The forecasts of yT+h, conditioned on the event that some future

values of yT+j, j = 1,..., h, are different from their unconditional forecasts, are then obtained as:

$ $ $|

* *|y e yT h T i T h i

i

h

T h T+ + −=

−

+= ∑ +Φ0

1

where the error terms [ ]e e e eh T T T hvec* * * *, , ...,= + + +1 2 are obtained as the solution of

min ' ,

. . ,e

e e

Re rh

h h

hs t =

and the constraints R eh = r are specified as to generate the scenario of the forecast. In this way, the conditional forecast $ |

*yT h T+ is obtained as an estimate of the projection of yT+h on IT

* = IT ∪YT+h*,

exploiting the contemporaneous correlations among the elements of y as measured by the Σ matrix. 1.4.3. Granger causality

VARs are unrestricted reduced form models, useful as a starting step in order to guide the specification of a fully fledged dynamic structural model. In this light, they are useful devices to analyse causation links among variables, and to guide the researcher in deciding which series, among the observed variables, are truly exogenous.

The concept of causation in econometric models dates back to the contributions of Wiener (1956), and Granger (1969). For a detailed account of the issue of causality in econometrics, it is possible to refer to Geweke (1984).

Imagine to analyse a (n ×1) vector of stationary time series yt, partitioned in two sub-vectors: y1t and y2t with dimensions (n1×1) and (n2 ×1) respectively, n1 + n2 = n. Define

It = { yτ : τ ≤ t }, I2t = { y2τ : τ ≤ t } i.e. It is the information set containing all the past and current values of yt, whereas I2t is the information set containing only the past and current values of y2t.

14

The concept of Granger causation can be described as follows. The vector y1t fails to Granger cause y2t if the predictive density of y2 has the following property

p (y2t+h |It) ≡ p (y2t+h | I2t), ∀ h ≥ 1 which means that conditioning also on the past of y1 does not alter the predictive density of y2. In other words, knowledge of past and current values of y1 does not help to predict future values of y2.

In the case of Granger non causality from y1 to y2, the VAR representation for yt is

A A

0 Ay

0

11 12

22

11 12

21 22

( ) ( )

( ),

( , ),

L L

L

VWN

t t

t

⎡

⎣⎢⎢

⎤

⎦⎥⎥

=

⎡

⎣⎢⎢

⎤

⎦⎥⎥

~ =

ε

ε Σ ΣΣ Σ

Σ Σ

where clearly the block A21(L) is equal to a (n2× n1) matrix of zeroes.

The block-triangular structure of the VAR representation is also retained by the associated VMA representation

yC C

0 CC It t n

L LL

= 0=⎡

⎣⎢⎤

⎦⎥11 12

22

( ) ( )( )

,ε

since the relationship A(L) C(L) = In implies

C I

C A C

0

1

1 2

=

= =−=

∑n

k j k jj

k

k, , , ...

Therefore all VMA coefficient matrices must be block triangular as the VAR matrices.

Also, non causality from y1 to y2 implies that the VAR representation can be transformed by pre-multiplying it by the matrix

A I0 I0

1 12 221

2

=−⎡

⎣⎢

⎤

⎦⎥

−n

n

Σ Σ

The result is the following system

15

A A

0 Ay

00

0

A

11 12

22

11 12 221

21

22

12 12 2210

* **

* * *

*

( ) ( )

( ),

( , ),[ ]

[ ]

( )

L L

L

VWN

t t

t

⎡

⎣⎢⎢

⎤

⎦⎥⎥

=

−⎡

⎣⎢⎢

⎤

⎦⎥⎥

=

−

−

~ =

ε

ε Σ ΣΣ Σ Σ Σ

Σ

Σ Σ

At this point, it can immediate be seen that: a) the error terms of the two blocks of equations are orthogonal b) in the first block of equations, we have also the contemporaneous values of the elements of y2 as regressors for y1t. These two considerations taken together mean that when y1 does not Granger-cause y2, y2 is also strictly exogenous (in the sense of Sims, 1972) with respect to y1.

Clearly, Granger non-causality from y1 to y2 is easily testable, by verifying the joint significance of the parameters in A21(L) in a VAR framework. For the details of this testing procedure, see Geweke (1984).

Some caution in interpreting the results of non-causality tests is necessary. First of all, results are usually very sensitive to the information set being used in the application (i.e. the set of series being included in the VAR): there is always the risk of finding "spurious" causation links deriving from omitted variables. Moreover, in the presence of forward-looking behaviour, Granger causality tests can deliver results which might be at odds with the "true" causation mechanisms driving the behaviour of the variables being analysed7.

1.5. Different classes of Structural VAR models

As we have already stressed, a VAR model has to be considered as a reduced form model where no explanations of the instantaneous relationships among variables are provided. These instantaneous

7 For a simple and very illuminating example of this, see Hamilton, 1994, Example 11.1.

16

relationships are naturally hidden in the correlation structure of the Σ matrix, and left completely uninterpreted.

This becomes evident when the model is put into its equivalent VMA representation, where the interpretability of the coefficients becomes problematic, given the contemporaneous correlation structure of the error terms. As we have already pointed out, Sims'(1980) original proposal consisted in moving from a non-orthogonal VMA to an orthogonalised VMA representation via Choleski factorisation of the Σ matrix. This amounts to starting from the reduced form VAR representation

A (L) yt = εt, εt ~ VWN (0,Σ) and to pre-multiply the system by the inverse of the Choleski factor of Σ

A*(L) yt = et, et ~ VWN (0,In)

A*(L)= A ii

p*

=∑

0, A0

*=P-1, Ai* = P-1 Ai,

P P' = Σ where P is the Choleski factor of Σ, and clearly A0

* is lower triangular with unit diagonal elements. This amounts to modelling contemporaneous relationships among the endogenous variables in a triangular recursive form. The resulting orthogonal VMA representation is

y C P e e

C P

t i t ii

i t ii

i i

= ∑ = ∑

= =

−=

∞

−=

∞

, 0 0

0

Φ

Φ Φ

,

Notice that, since Φ0 = P, the orthogonal VMA representation shocks et have instantaneous effects on the elements of yt according to the triangular scheme given by the Choleski factor P.

Moreover, it is true that given the matrix Σ, the Choleski factor P is uniquely determined. Nevertheless, if the elements of yt were permuted and arranged in yt

*, the rows and columns of Σ would have to be permuted accordingly to generate Σ*. The matrix Σ* would then have a different Choleski factor:

P* P*' = Σ* which would produce a different orthogonalised VMA representation. Therefore, the orthogonal VMA representation corresponding to the Choleski decomposition of variance covariance

17

matrix of the reduced form disturbances is unique only given a particular ordering of the observable variables contained in yt.

The triangular representation, which is sometimes referred to as Wold causal chain, is clearly a very particular one which cannot be considered suitable to every applied contexts. Sometimes, the researcher might have in mind different schemes for representing these instantaneous correlations, outside the straitjacket of the triangular structures.

In the recent literature, these alternative ways of modelling instantaneous correlations can be summarised in the following terms. Recent literature on the so-called Structural VAR approach uses different ways of structurising the VAR model. We will discuss three such ways: a KEY model which we will call the K-model, the C-model and the AB-model.

In addition to the hypotheses introduced earlier, for the K-model (KEY model) the following expression will hold: K-model

K is a (n ×n) invertible matrix such that K A(L) yt = K εt K εt = et E(et) = 0 E(et et') = In The K matrix "premultiplies" the autoregressive representation

and induces a transformation on the εt disturbances by generating a vector (et) of orthonormalised disturbances (its covariance matrix is not only diagonal but also equal to the unit matrix In). Contemporaneous correlations among the elements of y are therefore modelled through the specification of the invertible matrix K. The structural K-model can be thought of as a particular structural form with orthonormal disturbance vector.

Note that assuming we know the true variance covariance matrix of the εt terms from:

K εt = et K εt εt' K ' = et et'

taking expectations one immediately obtains KΣK' = In.

The previous equation implicitly imposes n(n+1)/2 non-linear restrictions on the K matrix, leaving n(n-1)/2 free parameters in K.

18

C-model

C is a (n ×n) invertible matrix such that A(L) yt = εt εt = C et E(et) = 0 E(et et') = In In this particular structural model, we have a structural form

where no instantaneous relationships among the endogenous variables are explicitly modelled. Each variable in the system is affected by a set of orthonormal disturbances whose impact effect is explicitly modelled via the C matrix.

Sims (1988) stresses the point that there is no theoretical reason to suppose that C should be a square matrix of the same order as K. If C were a square matrix, the number of independent (orthonormal) transformed disturbances would be equal to the number of equations. Many reasons lead us to think that the true number of originally independent shocks to our system could be very large. In that case the C matrix would be a (n× m) matrix, with m much greater than n. In this sense, this research path is opposite to the one studied by the factor analysis, which attempts to find m (the number of independent factors) strictly smaller than n. The case of a rectangular (n×m) matrix C, with m>n, conceals a number of problems connected with the completeness of the model and the aggregation over agents - see a short and not very illuminating discussion of this topic in Blanchard and Quah (1989). In this book, we will not face this problem and we will assume C square and invertible. Nevertheless, we think that many important issues can be better treated following the research path indicated before.

Turning back to our C model, the εt vector is regarded as being generated by a linear combination of independent (orthonormal) disturbances to which we will refer hereafter as et. This may have a different meaning than that of the K-model, where one is concerned with the explicit modelling of the instantaneous relationships among endogenous variables.

As for the C-model, notice that from εt = C et εt εt ' = C et et ' C '

taking expectations,

19

Σ =C C ' If, again, we assume to know Σ, the previous matrix equation implicitly imposes a set of n(n+1)/2 non-linear restrictions on the C matrix, leaving n(n-1)/2 free elements in C. AB-model

A, B are (n×n) invertible matrices8 such that: A A(L) yt = A εt A εt = B et E(et) = 0 E(et et ') = In In this kind of structural model, it is possible to model explicitly

the instantaneous links among the endogenous variables, and the impact effect of the orthonormal random shocks hitting the system.

Notice that the A matrix induces a transformation on the εt disturbance vector, generating a new vector (A εt) that can be conceived as being generated by linear combinations (through the B matrix) of n independent (orthonormal) disturbances, which we will refer to as et. Obviously this structure might have a different meaning than those of models K and C.

Notice also that the AB-model can be seen as the most general parameterisation nesting the C and K models as special cases. In fact, the C-model can be seen as a particular case of the AB-model, where A is chosen to be the identity matrix, and the K-model corresponds to an AB-model with a diagonal B matrix.

As in the previous case, from A εt = B et A εt εt ′A ′ = B B′

for Σ known, this equation again imposes a set of n(n+1)/2 non-linear restrictions on the parameters of the A and B matrices, leaving overall 2n2- n(n+1)/2 free elements.

1.6. The likelihood function for SVAR models

It is important to note that for any of the three classes of SVAR models described above, the log-likelihood function can be

8 The same argument discussed earlier on the size of the matrix C also applies to the matrix B.

20

considered as a function of Π and Σ. Following Sims (1986), and supposing that there are no cross restrictions on Π and Σ or, in more general terms, that there are no restrictions at all on Π while a set of restrictions are imposed on Σ, the identification and the F.I.M.L. estimation of the parameters of models K, C, and AB can be based on the analysis of the following likelihood function

( )L = - 2

| | -2

c T log T tr

T

Σ Σ Σ

Σ

−

−=

1

1

$

$ $ $ 'VV

which is the log-likelihood concentrated with respect to Π. The estimation of Π corresponding to the concentration of the log-likelihood clearly coincides with the OLS estimator when the log-likelihood is conditioned on the first p observations of the sample. Other consistent estimators would yield asymptotically equivalent results as for the subsequent estimation of the Σ matrix.

From this function, three different log-likelihood functions can be obtained for models K, C and AB by substituting Σ with its expressions in the three different cases: K-model

[ ] ( )L ( ) = + 2

| | -2

'2K K K Kc T log T tr $Σ

remembering that, from KΣK'= In, and taking into account the invertibility of K, we can write

Σ=K-1 K'-1 = (K' K)-1, Σ-1 = K'K log|(K′K)-1| = -log[|K|2]; C-model

[ ] ( )L ( ) = - 2

| | -2

2 -1C C C Cc T log T tr ' $Σ

remembering that Σ=C C', Σ-1 = (C C')-1 = C'-1 C-1

AB-model

21

[ ] [ ]

( )L ( ) = +

2 | | -

2 | | +

-2

2 2A B A B

A B B A

c T log T log

T tr ' ' $− −1 1 Σ

remembering that Σ=A-1BB'A'-1, Σ-1 = A'B'-1B-1A By simple inspection of the three log-likelihood functions

obtained by introducing the respective series of non-linear constraints on the matrices K, C, A and B, we can heuristically understand that, lacking further information, likelihood based estimators for the parameters K, C, A and B cannot be found.

All the sampling information necessary to obtain estimates of Σ is contained in $Σ which will have with probability equal to one n×(n+1)/2 distinct elements. By substituting Σ with its expression in terms of K, C, A and B (depending on the particular SVAR model being specified), we overcome the problem of finding a direct estimate of the n×(n+1)/2 elements in Σ (which in reality was not known). There still remains the problem of estimating n2 parameters for the K matrix in the K model, n2 parameters for the C matrix in the C model, and 2n2 parameters (n2 for A and n2 for B) in the AB-model.

It can be heuristically understood that from the sampling information contained in $Σ at most n×(n+1)/2 functionally independent parameters can be estimated in any of the three models. Without additional information we find ourselves in a typical situation of under-identification.

In general, in the existing applied literature the specification of Structural VAR models has been limited to situations of exact identification of the whole set of parameters. This is achieved by aptly imposing exclusion restrictions. One remarkable exception is given by a RATS routine written by T. Doan in three different versions (1987, 1988, 1989). Doan proposes a complete solution for the estimation of over-identified and exactly identified AB-models, with B diagonal and exclusion restrictions on the off-diagonal elements of the A matrix.

22

The exclusion restrictions and the need for exact identification greatly reduce the practical meaning of the Structural VAR approach for a number of reasons which shall be discussed below. To the best of our knowledge, still in the case of exact identification, two papers have tried to introduce new features. In the first of these two papers, Blanchard and Quah (1989), the C-model is used in a system with two variables, and exact identification is obtained by introducing a homogeneous restriction on the parameters of the C matrix, through an infinite-horizon theoretical constraint. In Keating (1990), instead, the AB-model is used for n = 3, with B diagonal and a set of non-linear restrictions on the off-diagonal elements of the A matrix. These restrictions are derived from a variant of Taylor's (1986) rational expectation model.

In what follows we have tried to solve the problem of identification, estimation and use of K, C, and AB-models with additional linear restrictions of the most general kind, namely

R K dk kvec = for K-model R C dc cvec = for C-model

R A dR B d

a a

b b

vecvec

==

⎧⎨⎩

for AB-model

where the Ri matrices (i = k, c, a, b) have full row rank. To these groups of non-homogeneous linear restrictions written

in implicit form correspond three groups of restrictions written in explicit form (see for example Sargan, 1988):

vec k k kK S s + = γ vec c c cC S s + = γ

vecvec

a a a

b b b

A S sB S s

+ +

==

⎧⎨⎩

γγ

where the Si matrices (i = k, c, a, b) have full column rank and the number of columns is equal to the number of free elements in the respective matrices. The number of rows in the Si is obviously n2

and the number of columns is n2 minus the rows of the corresponding Ri matrix.

The following identities will hold for the Ri, di, Si and si vectors and matrices

Ri Si = [0] [0] is a matrix of appropriate order

23

Ri si = di i = k, c, a, b Following the terminology of Magnus (1988), when di = 0, i = k,

c, a, b, the K, C, A, B matrices are called L-structures (linear structures), whereas when di ≠ 0 they are called affine structures.

1.7. Structural VAR models vs. dynamic simultaneous equations models

In this short section we explain the main conceptual differences between a Structural VAR model and the usual dynamic simultaneous equation system. In the absence of truly exogenous variables, the structural form of a dynamic simultaneous equation system for the (n ×1) vector of endogenous series yt can be written as

Γ(L) yt = ξt, ξt ~ VWN (0, Ω),

Γ Γ Γ( )L Ljj

pj = − ∑

=0

1

whereas the reduced form is A(L) yt = εt, εt ~ VWN (0, Σ), Σ = Γ0

-1 Ω Γ0-1 ′, Ai = Γ0

-1 Γi, i = 1, 2,..., p In dynamic simultaneous equation systems, identification is usually achieved by imposing constraints on the elements of the matrices Γi, i = 0, 2,..., p, and Ω.

In Structural VARs, no constraints are imposed on the matrices Γi, i = 1, 2,..., p, on the grounds of two different considerations. First of all, economic theory is usually not very informative on the elements of the matrices Γi, i = 1, 2,..., p; it is then considered preferable to leave these coefficients free, and let them be determined by the statistical properties of the observed data. Secondly, the restrictions on dynamic multipliers are precisely those "incredible" identifying restrictions so convincingly criticised by Sims (1980) which led to a widespread dissatisfaction towards standard Simultaneous Equation Systems.

In Structural VAR models, the constraints are usually imposed on the simultaneous relationships matrix Γ0 and on the variance covariance matrix of structural form disturbances. In this kind of approach, the researcher's focus is on a set of orthogonal

24

disturbances, intended as "behaviorally distinct sources of fluctuation" (Sims, 1986, p.9). The structural model is then:

Γ(L) yt = B et, et ~ VWN (0, In), B B′ = Ω and the researcher is willing to impose some constraints on the instantaneous effects of the et on the observable variables yt and on the instantaneous linkages among the endogenous variables.

In synthesis, in Structural VAR models no distinction is drawn between endogenous and exogenous variables, and the constraints are usually imposed on the simultaneous relationships matrix Γ0, which in this book is referred to as A matrix, and on the variance covariance matrix of structural form disturbances Ω, which is parameterised as Ω = B B′. This leads to the structural form

A A(L) yt = B et which represents the typical AB- structural VAR model. The K- and C-models originate as particular cases of the AB-model.

1.8. Some examples of Structural VARs in the applied literature

In this section we present some examples of different SVAR models appeared in the applied literature, in order to help the reader to fully understand the different features of the three classes of Structural Var models. 1.8.1. Triangular representation deriving from the Choleski decomposition of Σ

The triangular representation A*(L) yt = et, et ~ VWN (0,In)

A*(L)= A ii

p*

=∑

0, A0

*=P-1, Ai* = P-1 Ai, P P' = Σ

can easily be interpreted as a K-model, where clearly K = P-1. Since in this case K is by construction lower triangular, we have n(n-1)/2 exclusion restrictions on vecK, corresponding to the elements of K above its main diagonal. This number of restrictions is exactly equal to the number of elements of K which are left free after considering the relationship K Σ K' = In

25

Therefore, in the usual identification jargon, the order conditions for identification would suggest a situation of exact identification (see for details chapter 2).

The recursive VAR corresponding to the Choleski decomposition of Σ can also be interpreted as a C-model A(L) yt = C et, et ~ VWN (0,In) where C = P. Again, since C is lower triangular, n (n -1)/2 exclusion constraints are introduced on C, exactly as many as the elements of C which are left free after considering the relationship Σ = C C' Therefore the usual order condition suggests that this is a case of exact identification of C (see for details chapter 3).

The exact identification of the triangular structure is confirmed by the fact that its estimate can be obtained by applying the Choleski decomposition to $Σ , the estimated variance-covariance matrix of the reduced form disturbances. 1.8.2.Blanchard and Quah (1989) long run constraints

Blanchard and Quah (1989) investigated the dynamic effects of demand and supply disturbances in a bivariate system

yt = Δyu

t

t

⎡

⎣⎢⎤

⎦⎥ = Φ(L) et, et ~ VWN (0,In)

where Δyt is the growth rate of real GDP and ut is the unemployment rate. Both series are stationary and therefore the Wold representation described above exists. The two authors imagine that the first element of et,, e1t, is a demand disturbance which has no long run effect on the level of output. The second disturbance e2t, is considered as a supply shock, which has long run effect on the level of output. These considerations imply the following constraint on the long run structural impulse response function: u1' Φ(1) u1 = 0, where u1' = [1, 0].

The model used by Blanchard and Quah can be interpreted as a C-model where

26

Φ(L) = C(L) C = c L c Lc L c L

c cc c

11 12

21 22

11 12

21 22

( ) ( )( ) ( )

⎡

⎣⎢⎤

⎦⎥⋅⎡

⎣⎢⎤

⎦⎥

and the long-run constraint can be written as c11(1) c11 + c12(1) c21 = 0

In this case, since the relationship Σ = C C' leaves only one free element on the C matrix, the usual order condition suggests that we are in a situation of exact identification9: this intuition is supported by the fact that any C matrix such that10

C C' = Σ can be defined as

C = P Q, Q Q' = Ιn i.e. as an orthonormal transformation of the Choleski factor P.

Defining

C(1) P = D = d dd d

11 12

21 22

⎡

⎣⎢⎤

⎦⎥, Q =

q qq q

11 12

21 22

⎡

⎣⎢⎤

⎦⎥

the C matrix satisfying Blanchard and Quah's long run constraint can be obtained by determining the elements of Q such that

q21 = - d11 q11 /d12 (long run constraint)

q q q qq q

12 21 22 11

112

212 1

= - , =+ =

⎧⎨⎩

(orthonormality of Q)

1.8.3. A traditional interpretation of macroeconomic fluctuations: Blanchard (1989)

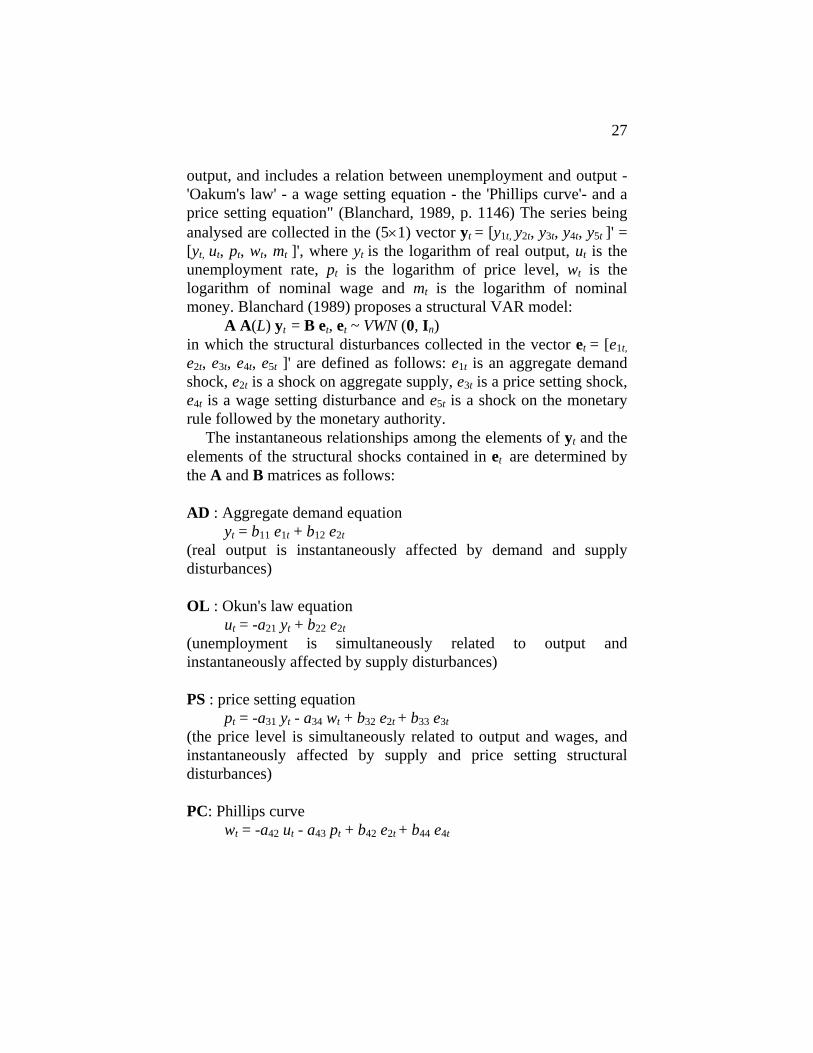

Blanchard (1989) uses the "traditional" Keynesian model to analyse the US macroeconomic fluctuations. by means of a structural AB model, which is intended to capture the main feature of a Keynesian model consisting of aggregate demand, aggregate supply and a monetary rule equation. "Aggregate demand characterizes the behaviour of the aggregate demand for goods given prices. Aggregate supply characterizes the behaviour of prices given

9 The fact that the long run constraint involves the reduced form cumulated impulse response functions coefficients which are not known and must be estimated causes some complications in the Structural VAR analysis. See section 6.1 for further details on this issue. 10 See Blanchard and Quah (1989), p. 657.

27

output, and includes a relation between unemployment and output -'Oakum's law' - a wage setting equation - the 'Phillips curve'- and a price setting equation" (Blanchard, 1989, p. 1146) The series being analysed are collected in the (5×1) vector yt = [y1t, y2t, y3t, y4t, y5t ]' = [yt, ut, pt, wt, mt ]', where yt is the logarithm of real output, ut is the unemployment rate, pt is the logarithm of price level, wt is the logarithm of nominal wage and mt is the logarithm of nominal money. Blanchard (1989) proposes a structural VAR model:

A A(L) yt = B et, et ~ VWN (0, In) in which the structural disturbances collected in the vector et = [e1t, e2t, e3t, e4t, e5t ]' are defined as follows: e1t is an aggregate demand shock, e2t is a shock on aggregate supply, e3t is a price setting shock, e4t is a wage setting disturbance and e5t is a shock on the monetary rule followed by the monetary authority.

The instantaneous relationships among the elements of yt and the elements of the structural shocks contained in et are determined by the A and B matrices as follows: AD : Aggregate demand equation

yt = b11 e1t + b12 e2t (real output is instantaneously affected by demand and supply disturbances) OL : Okun's law equation

ut = -a21 yt + b22 e2t (unemployment is simultaneously related to output and instantaneously affected by supply disturbances) PS : price setting equation

pt = -a31 yt - a34 wt + b32 e2t + b33 e3t (the price level is simultaneously related to output and wages, and instantaneously affected by supply and price setting structural disturbances) PC: Phillips curve

wt = -a42 ut - a43 pt + b42 e2t + b44 e4t

28

(nominal wage is simultaneously related to unemployment and prices, and instantaneously affected by supply and wage setting structural disturbances) MR : monetary rule equation

mt = -a51 yt -a52 ut - a53 pt - a54 wt + b55 e5t (nominal money is simultaneously related to output, unemployment, prices and wages, and instantaneously affected by monetary structural disturbances) For a thorough economic interpretation of these equations, see Blanchard (1989, section II).

The structural VAR model described above has a VAR reduced form

A(L) yt = εt, εt ~ VWN (0, Σ) and the reduced form vector error term εt is related to the structural vector error term et through the set of linear relationships

A εt = Bt et Notice that the structure specified by Blanchard leads to the

following A and B matrices:

A B

1

=

⎡

⎣

⎢⎢⎢⎢⎢

⎤

⎦

⎥⎥⎥⎥⎥

=

⎡

⎣

⎢⎢⎢⎢⎢

⎤

⎦

⎥⎥⎥⎥⎥

0 0 0 01 0 0 00 1 0

0 1 01

0 0 00 0 0 00 0 00 0 00 0 0 0

21

31 34

42 43

51 52 53 54

11 12

22

32 33

42 44

55

aa a

a aa a a a

b bbb bb b

b

,

The two matrices have 17 free elements, while the estimated variance-covariance matrix of the unstructured VAR model disturbances ( $Σ ) contains only 15 different elements. The usual order conditions for identification seems to suggest that the above structure is not identified. For this reason, Blanchard (1989) assigned fixed numerical values to the coefficients a34 and b12. The numerical value given to a34 was derived from previous studies, whereas that assigned to b12 resulted from a sort of calibration reasoning.

Giannini, Lanzarotti and Seghelini (1995) presenting a variant of Blanchard's model applied to Italian data, choose not to set the above mentioned two parameters to fixed constant values, but rather

29

to specify some extra constraints in order to obtain an over-identified structure. For details see section 9.1 of this book.

29

Chapter 2 Identification analysis and F.I.M.L. estimation for the K-Model

In this chapter we present the condition for the identification of the K-model (section 2.1) and we describe how an identified structure can be estimated by means of F.I.M.L. (section 2.2).

2.1. Identification analysis

The K-model1 is completely defined by the following equations and distributional assumptions: K εt = et E(et) = 0, E(et et ') = In εt ~ IMN(0, Σ) det (Σ) ≠ 0 (εt, the vector of the VAR model disturbances A(L)yt = εt is a Gaussian vector white noise, i.e. a vector of independent multivariate normally distributed variables with an associated positive definite variance-covariance matrix).

All the sampling information concerning Σ is contained in the $Σ matrix:

$$ $ '

Σ =VVT

The $Σ matrix can be viewed as the unrestricted estimate of the variance-covariance matrix of the disturbances of the "reduced form": A(L)yt = εt

The corresponding log-likelihood function of the K-model for the parameters of interest (the n2 parameters in the K matrix) is

[ ]L c T T tr( $K K K K) = + 2

log | | -2

( ' ) 2 Σ (2.1)

With respect to this function, the associated density function and the "structural" parameter space, we will assume that the usual

1 Hereafter we will drop the i index (i = k, c, a, b ) to Ri , di , γi , Si , si matrices and vectors unless ambiguity arises.

30

regularity conditions hold, as reported in Rothenberg's (1971) fundamental paper on identification.

The conditions KΣK' = In obviously introduce a set of non-linear restrictions on the parameter space. Therefore, in general, we can obtain only necessary and sufficient conditions for local identification of the parameters in the K matrix as opposed to global identification (see Rothenberg, 1971, p.578).

Moreover, if we are interested only in the joint identification of all K matrix parameters (in the sense of Wegge (1965), we are interested in the identification criteria of a system of equations as a whole) and not in the "isolated" identification of a proper subset of parameters of the K matrix. In Structural VAR Econometrics all the equations of a structuralised VAR are used together, thus "isolated" identification of a proper subset of the parameters in question is of virtually no interest.

In order to achieve identification we will assume that the parameters contained in the K matrix satisfy the set of independent, non-contradictory, non-homogeneous linear restrictions stated in implicit form as follows R vec K = d (2.2) where R is a r×n2 full row rank matrix and d is a possibly non zero r×1 vector, or in explicit form vec K = S γ + s (2.3) where S is a n2×l full column rank matrix with l = n2- r, s is a n2×1 vector and

R S 0

R s d

=

=×

×

[ ]r l

r 1

Following Rothenberg (1971), in order to geometrically analyse the local non-identification situation in the absence of a-priori information contained in (2.2) or (2.3), we will compute the information matrix (the sample information matrix) of the vectorised elements of the K matrix, without taking into account the set of linear restrictions (2.2) or (2.3).

For this purpose we shall compute the vector of partial first derivatives of the log-likelihood function with respect to vec K (the

31

"score " vector) and then the Hessian matrix of the log-likelihood (always with respect to vec K). From this last expression we can then easily compute the sample information matrix.

Taking into account the symbols and notations presented in Appendix A, the score of the likelihood function is (see Appendix B for calculation)2

∂∂

Lvec

f vecK

K= ' ( ) f '(vec K) is a 1× n2 row vector

f vec T T vecr' ( ) ( ) ( )' ( $ ) K K K I= − ⊗−1 Σ or equivalently (see Pollock, 1979), taking into account that (A)r = [vec(A')]' f vec T vec T vec' ( ) [ ( ' ) ]' ( )' ( $ ) K K K I= − ⊗−1 Σ ; obviously the first order conditions for maximisation of the likelihood function are f vec

n n' ( )( )

[ ]( )

K 01 2 1 2×

=×

in row form, or [ ]f vec

nf vec

n n' ( )( )

' ( )( )

[ ]( )

K K 02 1 2 1 2 1×

=×

=×

in column form. Referring again to Appendix A for notation rules and to

Appendix B for calculation, the Hessian matrix of the log-likelihood with respect to vec K is defined as

∂∂ ∂

∂∂

∂∂

2 L L L( )( )'

'

vec vec vec vecK K K K= ⎛

⎝⎜⎞⎠⎟

.

The resulting Hessian can be written as

{H KK K

K K( )( )( )'

( ' )vecvec vec

T

2

= = − ⊗− −∂∂ ∂

L 1 1 OT

+ }$Σ ⊗ I .

2 In order to simplify notation, the In identity (n ×n) matrix will hereafter be substituted simply by I. Identity matrices of different orders will be indicated with their proper corresponding indexes.

32

The sample information matrix of the elements of vec (K) (without taking into account the set of linear restrictions on this vector) has two equivalent definitions for "regular" likelihood functions IT (vec K) = E [-H(vec K)] (*) IT (vec K) = E [f (vec K)⋅ f '(vec K)] (**)

Following (*) and taking into account that E( $ ) ( ' ) ( ' )Σ = =− − −K K K K1 1 1 IT (vec K) = T {[K-1⊗(K')-1] OT +[ K-1 (K')-1] ⊗I} and the properties of the commutation matrix OT (see Pollock 1979 and Magnus 1988) for A, B square matrices of order n (A⊗B) OT = OT ( B⊗A) we can write IT (vec K) = T {(K-1⊗I) OT (K'-1⊗I) + (K-1 ⊗I) (K'-1⊗I) } and finally IT (vec K) = T {(K-1⊗I) ( I

n2 + OT )(K'-1⊗I)}. The corresponding asymptotic information matrix

I (vec K) = plim vecT

T T→∞

1 I K( )

will simply be I (vec K) = {(K-1⊗I) ( I

n2 + OT )(K'-1⊗I)}. The sample information matrix and the asymptotic information

matrix have dimension (n2× n2); it is easily seen however that in our case these matrices are singular, their rank being equal to n(n+1)/2.

Since (K-1⊗I) and (K'-1⊗I) are invertible matrices, the rank of IT (vec K) and I (vec K) is equal to the rank of ( I

n2 + OT ) Using Magnus' (1988) notation and results3, we define: Nn = (1/2)( I

n2 + OT )

obviously4 r(Nn) = r ( In2 + OT ), but Nn is an idempotent matrix5 with

rank n(n+1)/2.

3 See Magnus (1988), p.48. In our notation, the OT matrix replaces Magnus’ Knn commutation matrix.

33

Assuming that the "true" value of the vector of parameters vec(K0) is a regular point of the information matrix IT (vecK) (in the sense of definition 4 of Rothenberg 1971, p.579) and on the basis of Theorem 1 in Rothenberg (1971) which states as the necessary and sufficient condition for the local identification of vec(K0) the non-singularity of IT (vecK0) we can assert, in view of the singularity of IT (vecK) over all the (admissible) parameter space, that vec(K0) is unidentifiable.

In order to get necessary and sufficient conditions for the local identification of the complete vector vecK, we must re-introduce our a-priori information contained in R vecK = d which has thus far been overlooked.

Following Rothenberg (1971) and taking into account that, since these constraint are linear, the Jacobian matrix of the partial derivatives of the system of constraints with respect to vecK is simply R, we can construct the following matrix

VT (vecK)= I KR

T vec( )⎡⎣⎢

⎤⎦⎥

or equivalently

V(vecK)= I KR

( )vec⎡⎣⎢

⎤⎦⎥

The two matrices are of (n2 +r)×n2 order. Following Theorem 2 in Rothenberg (1971) and assuming that

the "true" vector vec(K0) is a regular point (in the sense of Rothenberg) of VT (vecK) and V(vecK), a necessary and sufficient condition for the local identification of vec(K0) is that the rank of VT (vecK) or V(vecK) evaluated at K0 be n2. In other words, the VT (or V) matrices evaluated at vecK0 must be full column rank matrices.

4 As usual, r (A) stands for the rank of matrix A. 5 From the property of the matrix OT : OT ⋅OT = I

n2 .

34

This necessary and sufficient condition is very difficult to verify in our context. Thus, we will try to obtain more tractable conditions which are still absolutely equivalent to those of Rothenberg's Theorem 2 6.

Looking at V(vecK) "augmented" matrix

V(vecK)= ( )(2 )( ' )-1 -1K I N K IR

⊗ ⊗⎡⎣⎢

⎤⎦⎥

n

we can proceed as follows: the rank of V(vecK) is left unchanged if we pre-multiply and post-multiply this matrix by arbitrary non-singular matrices, obviously of the appropriate order.

If V(vecK) is first pre-multiplied by the block diagonal matrix

12 2

( )[ ][ ]

K I 00 I⊗⎡

⎣⎢⎤⎦⎥r

and then post-multiplied by (K'⊗I) the following (n2+r)×n2 matrix is obtained

NR K I

n( ' )⊗

⎡⎣⎢

⎤⎦⎥

Under the condition that (K'⊗I) is invertible (i.e. that K must always be invertible), the matrix above has the same rank as VT and V.

The condition of full column rank (n2) of this matrix is equivalent to the condition that the following homogeneous system of (n2+r) equations in n2 unknowns

NR K I y 0n

( ' ) [ ]⊗⎡⎣⎢

⎤⎦⎥

=

6 In our context IT (vecK), I (vecK) are matrices of constant rank n (n +1)/2 over the admissible parameter space (looking at the information matrix, the admissible space is also constrained by the invertibility of the K matrix). We can heuristically find a necessary condition for identification: taking into account the rank of the matrix IT (vecK), a necessary condition is that it be “augmented” by at least n (n -1)/2 independent rows. In other words, a necessary condition for identification is as follows: r, the number of restrictions on vecK, must be greater than or equal to n (n -1)/2.

35

has only one admissible solution y 0=×

[ ]n2 1

.

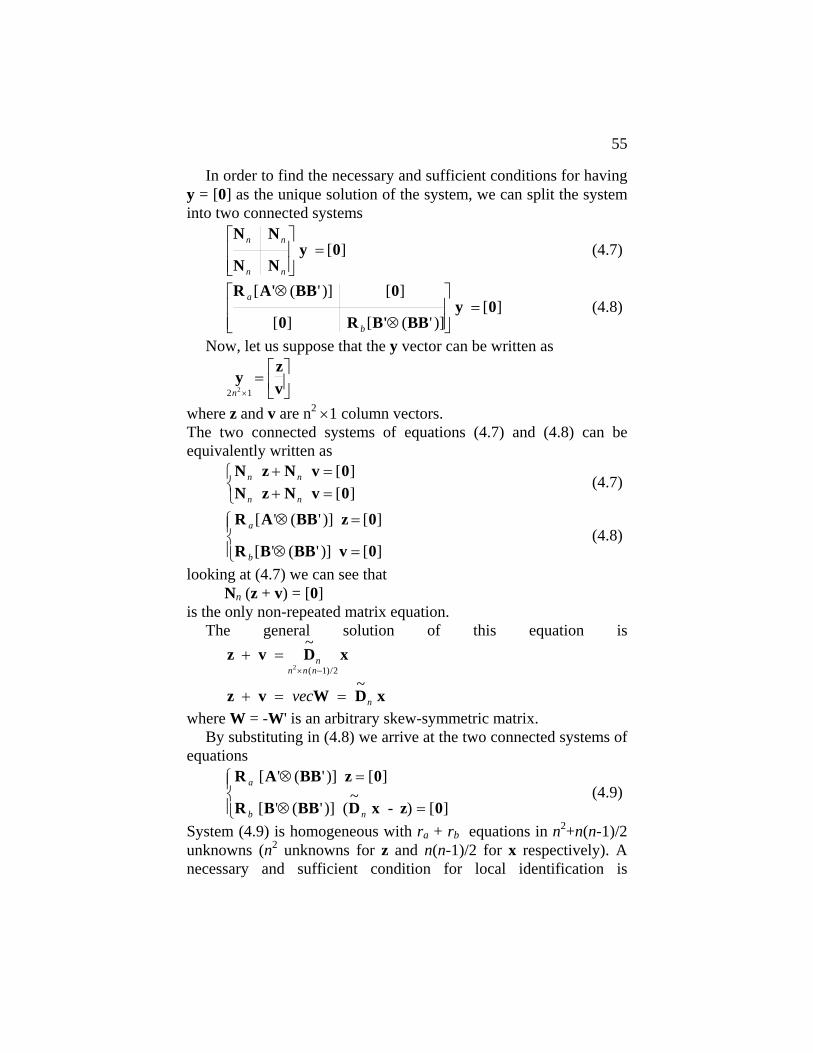

The system can be split into two connected systems of equations Nn y = [0] (2.4) R(K'⊗I)y=[0] (2.5) System (2.4) has n2 equations in n2 unknowns. System (2.5) has r equations in n2 unknowns. The two systems are connected because they share the same n2 unknowns.

In order to find closed formulae for the identification analysis we can now proceed in two ways: i) the general solution of system (2.4) is found and inserted in system (2.5) or ii) the general solution of system (2.5) is found and inserted in system (2.4). The former procedure will be followed. The alternative has the advantage of leading to more "parsimonious" conditions for identification, which however are more difficult to interpret.

Considering system (2.4) and looking for the general solution of this system of equations, we will follow Magnus (1988). The vector representing the general solution of system (2.4) can be written as y D x= ~

n where the ~Dn matrix, defined in Magnus (1988), pp. 94-5, is a (n2×n(n-1)/2) full column rank matrix and x is a n(n-1)/2 vector of free elements.

The ~Dn matrix main feature is that for any real valued vector x it generates the vectorised form of a skew-symmetric matrix (say W

( )n n×,

where W = -W') of order n: y = vecW = ~Dn x. We can easily check that this is a solution of system (2.4), remembering the property of the commutation matrix OT : OT vecA = vec(A') for A (n× n) and that for a skew symmetric matrix vec W = -vecW' so for

N In n= +

12 2( OT )

N D x N W In n n nvec~ (= = + 1

2 2 OT )= 12

(vecW+OT vecW)=

36

= 12

(vecW + vecW') = 12

(vecW-vecW) = [0]

This solution is also the general solution by virtue of theorem 9.1 of Magnus (1988), p. 146. Having found the general solution of system (2.4), we can insert it in system (2.5), arriving at R K I D x 0( ' )~ [ ]⊗ =n (2.6) Assuming the invertibility of the K matrix, the necessary and sufficient condition for identification of the "true" vector vec(K0)7 can be wholly derived from system (2.6) and can be stated in two equivalent forms: a) condition for identification

Assuming the invertibility of the K matrix, the true vector vec(K0) is locally identified if and only if the matrix R K I D( ' )~⊗ n evaluated at K0 has full column rank n(n-1)/2. b) condition for identification

Assuming the invertibility of the K matrix, the true vector vec(K0) is locally identified if and only if the system R K I D x 0( ' )~ [ ]⊗ =n with the matrix R K I D( ' )~⊗ n evaluated at K0 has the only admissible solution x=[0].

In practical applications, condition a) can be used and numerically checked remembering to use vecK = S γ +s and assigning "random" numbers to the elements of the γ vector in order to insert an "appropriate" matrix in the (K'⊗ I) nucleus of the formula. The numerical check of the condition does not contribute much to understanding the role and working of different typical constraints.

In Appendix C condition b) is used for the symbolic analysis of a number of interesting cases.

7 Obviously, the “true” vector vec(K0) must satisfy the constraint R vec(K0) = d.

37

2.2. F.I.M.L. estimation Having assured the local identification of our vector of