GIL 2011: Latin America The Global Community of Growth, Innovation and Leadership Cristiano Zaroni Director of Information and Communications Technologies for Frost & Sullivan Latin America 6 th December, 2011 São Paulo, Brazil 360 Degree Industry Perspective Information and Communications Technologies

Transcript

GIL 2011: Latin AmericaThe Global Community of Growth, Innovation and Leadership

Cristiano ZaroniDirector of Information and Communications Technologies for

Frost & Sullivan Latin America

6th December, 2011São Paulo, Brazil

360 Degree Industry PerspectiveInformation and Communications Technologies

2

Table of Contents

2. The Rise of Mobile Applications

7. Conclusions - How can we help you grow?

1. Future Connectivity and Broadband

6. Smart Devices

3. Contact Center and BPO

4. The Latin American Cloud

5. Social Networks

3

Key Opportunities in Latin American Information & Communication markets by 2020

4

Six ICT MicroTrends will have the largest impact on all business verticals in Latin America by 2020, leveraging economic growth

Agriculture

Oil & Gas

Materials

Mining

Economic DevelopmentConsumer

Products

Infrastructure

EnergyRetail

Automotive

Mobile Applications

Smart Devices

Cloud Computing

Social Networks

Contact Center & BPO

Broadband

5

Future Connectivity and Broadband

6

AsiaEurope

Latin America

North America

Africa

Oceania

Population (millions)

2025

2010

589

670

729

733352

398

4,167

4,773

43

36

1,033

1,400

By 2025, the Latin American potential market for ICT services is expected to be similar to Europe regarding the productive working-age population with a GDP per capita of $18,547.61.

Source: Population – UN estimativeGDP Per Capita – IMF and Frost&Sullivan projections

The expected increase on the Latin American GDP per capita should change consumption habits and increase demand for top end electronic devices, like smartphones and tablets.

7

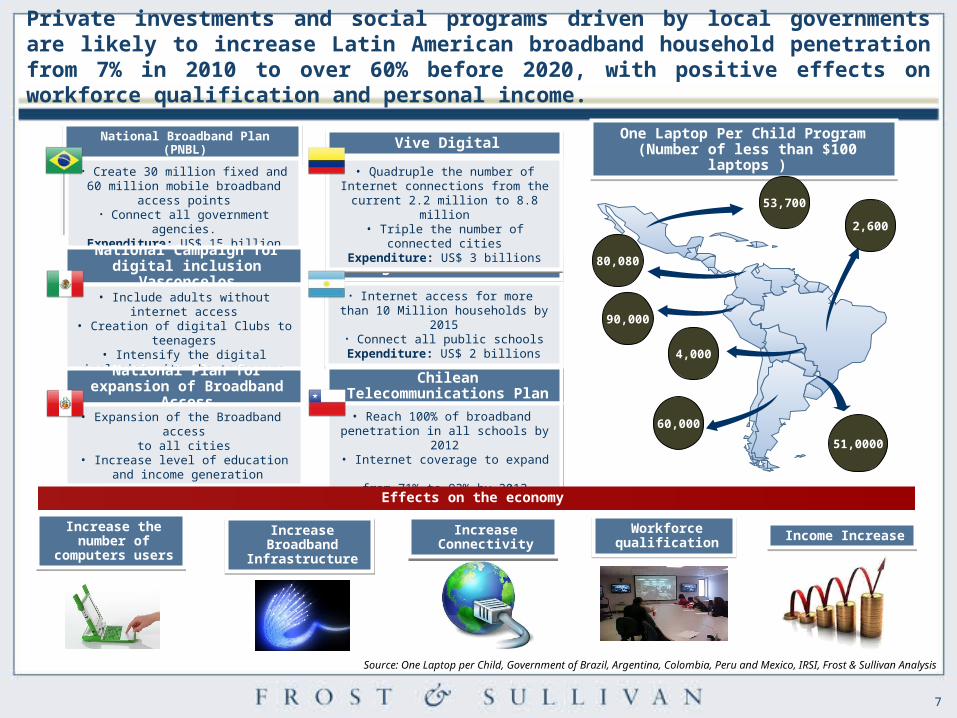

Private investments and social programs driven by local governments are likely to increase Latin American broadband household penetration from 7% in 2010 to over 60% before 2020, with positive effects on workforce qualification and personal income.

One Laptop Per Child Program (Number of less than $100 laptops )

One Laptop Per Child Program (Number of less than $100 laptops )

2,600

60,000

4,000

51,0000

90,000

80,080

53,700

National Broadband Plan (PNBL)National Broadband Plan (PNBL)

• Create 30 million fixed and 60 million mobile broadband access points

• Connect all government agencies.Expenditure: US$ 15 billion

• Create 30 million fixed and 60 million mobile broadband access points

• Connect all government agencies.Expenditure: US$ 15 billion

Argentina ConnectedArgentina Connected

• Internet access for more than 10 Million households by 2015

• Connect all public schoolsExpenditure: US$ 2 billions

• Internet access for more than 10 Million households by 2015

• Connect all public schoolsExpenditure: US$ 2 billions

Vive DigitalVive Digital

• Quadruple the number of Internet connections from the current 2.2 million

to 8.8 million• Triple the number of connected cities

Expenditure: US$ 3 billions

• Quadruple the number of Internet connections from the current 2.2 million

to 8.8 million• Triple the number of connected cities

Expenditure: US$ 3 billions

National Campaign for digital inclusion Vasconcelos

National Campaign for digital inclusion Vasconcelos

• Include adults without internet access• Creation of digital Clubs to teenagers• Intensify the digital inclusion with the

teenagers promotions

• Include adults without internet access• Creation of digital Clubs to teenagers• Intensify the digital inclusion with the

teenagers promotions

National Plan for expansion of Broadband Access

National Plan for expansion of Broadband Access

• Expansion of the Broadband accessto all cities

• Increase level of education and income generation

• Expansion of the Broadband accessto all cities

• Increase level of education and income generation

Source: One Laptop per Child, Government of Brazil, Argentina, Colombia, Peru and Mexico, IRSI, Frost & Sullivan Analysis

Increase the number of

computers users

Increase the number of

computers users

Increase Broadband

Infrastructure

Increase Broadband

Infrastructure

Increase Connectivity

Increase Connectivity Income IncreaseIncome IncreaseWorkforce

qualificationWorkforce

qualification

Chilean Telecommunications Plan

Chilean Telecommunications Plan

• Reach 100% of broadband penetration in all schools by 2012

• Internet coverage to expand from 71% to 92% by 2012

• Reach 100% of broadband penetration in all schools by 2012

• Internet coverage to expand from 71% to 92% by 2012

Effects on the economy

8

Asia

Europe

Latin America

North America

Africa

Oceania

90%

41%

200%

140%

91%

200%

56%

150%

82%

112%

27%

4%

90%

56%

65%

7%

65%

11%

57%

83%

Broadband Penetration

Mobile Penetration

Source: 2009 telecommunications statistics from ITU 2020 projections from Frost & Sullivan

90%

200%

100%

68%

The infrastructure investments, associated with a better socioeconomic profile, are expected to drive mobile penetration (M2M included) in Latin America from 91% in 2009 to more than 200% in 2020, and fixed broadband from 7% to 65%.

Broadband Penetration

Mobile Penetration

Broadband Penetration

Mobile Penetration

Broadband Penetration

Mobile Penetration

Broadband Penetration

Mobile Penetration

Broadband Penetration

Mobile Penetration

2010

2020

Broadband penetration will increase until 2020, generating a 7.1% GDP increase on Latin America.

9

The fixed and mobile broadband development will demand investments on infrastructure, both public and private, likely to integrate economies.

Multimedia content applications over IP Multimedia content applications over IP

Internet of everythingInternet of everything

• The proliferation of smart devices, multimedia content and more machines being connected will lead to a exponential increase in data traffic

• Current submarine cables, backbones and backhauls will need to increase capacity to deal with the increased data traffic, and new infrastructure will need to be built

• Governments will be concerned with the strategic relevance of this infrastructure to support their economies, and are likely to do investments and stimulate private investments.

• The proliferation of smart devices, multimedia content and more machines being connected will lead to a exponential increase in data traffic

• Current submarine cables, backbones and backhauls will need to increase capacity to deal with the increased data traffic, and new infrastructure will need to be built

• Governments will be concerned with the strategic relevance of this infrastructure to support their economies, and are likely to do investments and stimulate private investments.

Currently Latin America does not have robust links to Europe, Africa and among Latin America countries. And the capacity for U.S. Cables may not supply the demand until 2020.

Currently Latin America does not have robust links to Europe, Africa and among Latin America countries. And the capacity for U.S. Cables may not supply the demand until 2020.

Local Latin American governments will invest both direct and indirectly to expand and develop telecom infrastructure throughout the region, generating new business opportunities for ICT market participants.

10

With the increasing broadband penetration and the trend towards personalized video content, the Pay TV business models is challenged, and there will be change regarding consumer behavior and advertisement business models.

• The Pay TV providers business model is against interactivity and customization trends.• Although the linear channel lineup has been increasing, customers are likely to adopt

video streaming over the internet to watch: • what they prefer, • when they want, • with mobility• In multiple devices

• The Pay TV providers business model is against interactivity and customization trends.• Although the linear channel lineup has been increasing, customers are likely to adopt

video streaming over the internet to watch: • what they prefer, • when they want, • with mobility• In multiple devices

• Capitalize social media content, and integrate into Pay TV offering• Provide applications for each platform (TV everywhere concept)• Develop new billing strategies: Pay per transaction, pay per time, etc.• Introduce cloud services, substituting the set-top-box with DVR by a box that connects

to a server• Redefine strategy to the mass media, consider the increasing advertising expenditures

in alternative medias and though different devices,

• Capitalize social media content, and integrate into Pay TV offering• Provide applications for each platform (TV everywhere concept)• Develop new billing strategies: Pay per transaction, pay per time, etc.• Introduce cloud services, substituting the set-top-box with DVR by a box that connects

to a server• Redefine strategy to the mass media, consider the increasing advertising expenditures

in alternative medias and though different devices,

With the growth of high-speed broadband penetration and the changing consumer behavior, the conditions for new business models opportunities will flourish

Current business modelCurrent business model

Future business modelsFuture business models

Source: Frost & Sullivan

11

Another consequence of the video content and other streaming services growth is telecom operators rethinking their business models to guarantee ROI in the long term.

In the long term, attack strategies are dominant over defense strategies due to broadband services price erosion and difficulty in obtaining ROI.

Strategic OPTIONS

Not react, and benefit from the increasing demand for connectivity in the short term (dumb pipe).

Not react, and benefit from the increasing demand for connectivity in the short term (dumb pipe).

React and launch digital services to complement the connectivity offering (smart pipe)

React and launch digital services to complement the connectivity offering (smart pipe)

Fight against OTT providers, differentiating traffic SLAs, which could bring regulatory problems*.

Fight against OTT providers, differentiating traffic SLAs, which could bring regulatory problems*.

Partner with OTT providers, trying to negotiate a complimentay offering or even revenue sharing

Partner with OTT providers, trying to negotiate a complimentay offering or even revenue sharing

*Regulators in Brazil and Chile, for example, have positioned in favor of net neutrality. Source: Frost & Sullivan

In developing countries each 10% increase in broadband connections results in 1,38% additional GDP per capita growth

Smart devices will play a more complex role in the market switching from simple communication tool to an important service provider, changing the interactions among other value chains

2010 – 21, 0002020 – 14,6 Million 2010 – 21, 0002020 – 14,6 Million

Source: Frost & Sullivan, Brazilian Communication Ministry, World Bank, IPEA, Sousa, Oliveira, Kubota e Almeida

• 10% of lines in service are 3G

• High prices for data services

• Large amount of prepaid mobile users requires different strategies

• 24/7 connection: 3G dominance and expressive presence of 4G with LTE supremacy, enabling new applications for mobile devices

• Cloud intelligence will allow completely customized and predictive services

• Trade off between the speed of fixed internet and the extend of its use

• 24/7 connection: 3G dominance and expressive presence of 4G with LTE supremacy, enabling new applications for mobile devices

• Cloud intelligence will allow completely customized and predictive services

• Trade off between the speed of fixed internet and the extend of its use

In 2010, 444 cities were served with the PNBL, in 2014 it will be 4,278 cities

The number of Brazilian houses with broadband connections would grow from 15% to 61%, if the broadband cost reduces to R$ 35,00

5,6 Million 46,6 Million

14

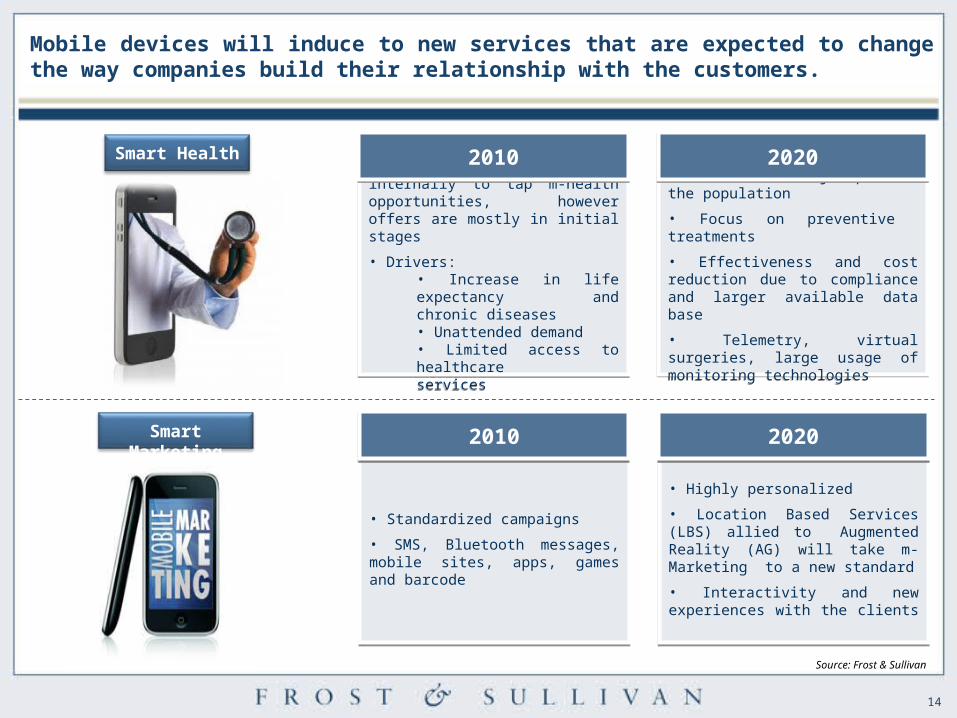

Mobile devices will induce to new services that are expected to change the way companies build their relationship with the customers.

Smart Health

Smart Marketing

• Companies are striving internally to tap m-health opportunities, however offers are mostly in initial stages

• Drivers: • Increase in life expectancy and chronic diseases• Unattended demand• Limited access to healthcare services

• Companies are striving internally to tap m-health opportunities, however offers are mostly in initial stages

• Drivers: • Increase in life expectancy and chronic diseases• Unattended demand• Limited access to healthcare services

20102010

• Services for major part of the population

• Focus on preventive treatments

• Effectiveness and cost reduction due to compliance and larger available data base

• Telemetry, virtual surgeries, large usage of monitoring technologies

• Services for major part of the population

• Focus on preventive treatments

• Effectiveness and cost reduction due to compliance and larger available data base

• Telemetry, virtual surgeries, large usage of monitoring technologies

20202020

• Standardized campaigns

• SMS, Bluetooth messages, mobile sites, apps, games and barcode

• Standardized campaigns

• SMS, Bluetooth messages, mobile sites, apps, games and barcode

20102010

• Highly personalized

• Location Based Services (LBS) allied to Augmented Reality (AG) will take m-Marketing to a new standard

• Interactivity and new experiences with the clients

• Highly personalized

• Location Based Services (LBS) allied to Augmented Reality (AG) will take m-Marketing to a new standard

• Interactivity and new experiences with the clients

20202020

Source: Frost & Sullivan

15

Smart Money

Smart Government

Source: Frost & Sullivan; United Nations

The emergence of new ways to spend money and the higher interface with government will empower customers.

• The available solutions are in test or initial stage

• Mobile phones and financial transactions walk side by side

• Risks regarding terrorism, false identity and the credit system

• The available solutions are in test or initial stage

• Mobile phones and financial transactions walk side by side

• Risks regarding terrorism, false identity and the credit system

20102010

• Convergence of financial services with mobile phones

• Virtual and physical shopping, transport payments, complex banking transactions

• Internet market leaders might emerge as strong actors

• Convergence of financial services with mobile phones

• Virtual and physical shopping, transport payments, complex banking transactions

• Internet market leaders might emerge as strong actors

20202020

• Insufficient G2C services

• Electronic passport, pioneer public transport projects, accident report, tax return and others

• Colombia, first e-government in the region on 2010

• Insufficient G2C services

• Electronic passport, pioneer public transport projects, accident report, tax return and others

• Colombia, first e-government in the region on 2010

20102010

• From e-government to Smart Government

• Real time pooling and voting, highly customized services and disseminated usage of national security services

• From e-government to Smart Government

• Real time pooling and voting, highly customized services and disseminated usage of national security services

20202020

16

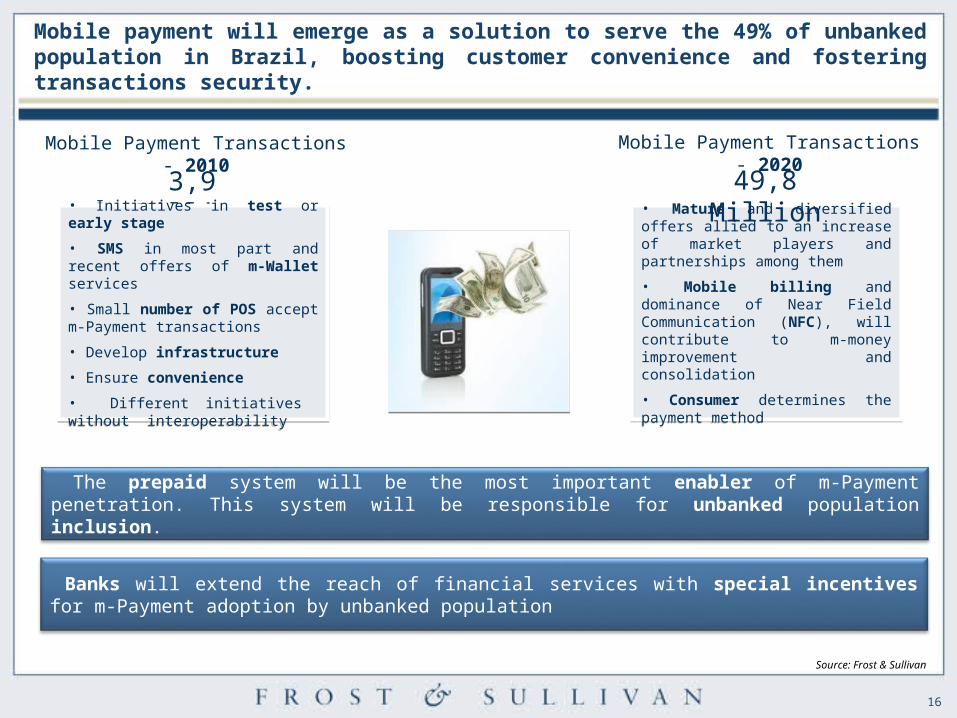

Banks will extend the reach of financial services with special incentives for m-Payment adoption by unbanked population

The prepaid system will be the most important enabler of m-Payment penetration. This system will be responsible for unbanked population inclusion.

Mobile payment will emerge as a solution to serve the 49% of unbanked population in Brazil, boosting customer convenience and fostering transactions security.

Mobile Payment Transactions - 2010

3,9 Million

• Initiatives in test or early stage

• SMS in most part and recent offers of m-Wallet services

• Small number of POS accept m-Payment transactions

• Develop infrastructure

• Ensure convenience

• Different initiatives without interoperability

• Initiatives in test or early stage

• SMS in most part and recent offers of m-Wallet services

• Small number of POS accept m-Payment transactions

• Develop infrastructure

• Ensure convenience

• Different initiatives without interoperability

• Mature and diversified offers allied to an increase of market players and partnerships among them

• Mobile billing and dominance of Near Field Communication (NFC), will contribute to m-money improvement and consolidation

• Consumer determines the payment method

• Mature and diversified offers allied to an increase of market players and partnerships among them

• Mobile billing and dominance of Near Field Communication (NFC), will contribute to m-money improvement and consolidation

• Consumer determines the payment method

Mobile Payment Transactions - 2020

49,8 Million

Source: Frost & Sullivan

17

Recently Latin American countries have passed through important improvements in e-government projects, however there are still great opportunities for innovations and investments to better serve the population.

• Digital identities

• Early e-Government initiatives• Collaboration between different

arms of government

Information served over the internet

Basic communication and productivity suites

e-Government becomes pervasive

• Disintermediation of government services

• Some citizens interact online with the government

e-Government may not always be motivated by democratic ideals but strengthened democratic institutions may emerge as a benefic consequence

• e-Government

Source: Frost & Sullivan; United Nations

Country Position

Colombia 31

Chile 34

Uruguai 36

Argentina 48

Brazil 61

18

Contact Center and Business Process Outsourcing

19

EnablersEnablers

EnvironmentEnvironment

InfrastructureInfrastructure

Labor PoolLabor Pool

BPO industries have transformed many outsourcing destinations and have served as drivers for growth. In Latin America, it will play a major role in fueling future economic development.

BPO is a human intensive industry that requires a large number of individuals to be present in a location, and many more to support and sustain these resources.

Stable political, economic and institutional conditions remain vital. Local and Regional governments must established secure and business-trusted environments to impel investments from abroad.

The CC-BPO industry relies on effective communication and interaction tools. Further, the growth of these hubs will demand the development of infrastructure in and around the sites to facilitate collaboration.

Outsourced jobs generally requires specialized skills and job profiles. Specific training and education programs around technical matters and foreign language will allow further grow in Latin America.

Growing outsourcing destinations such as Colombia, Peru and Nicaragua, along with other established markets such as Brazil and Mexico will drive Latin America to leapfrog by 2020 to US$ 18.5 billion.

2011 2020

Colombia’s vision in 2015: employ 88,200

workers, turning revenues of over

US$ 1 billion

Peru’s vision by 2017: employ 64,150

workers, turning revenues of US$ 554

million

Central America & Caribbean

countries are expected to have close to 152, 700 workers employed within existing and new cc cities and

hubs , contributing with US$ 2.1 billion

2015

2017

2020

Increased uptake by Governmentt, Retail, Banking

and larger Enterprises on Outsource non-core business

driving BPO / CC

2012

Brazil is expected to see new mega contact center hubs around and outside Sao Paulo, and expects revenues of US$10.3 billion, employing over 756,500 workers

Mexico’s vision by 2020: employ 172,000 workers

and turning revenues of US$

2.5 billion

Source: Frost & Sullivan

21

Latin America’s Contact Center / BPO industry is expected to employ close to 1.3 million people in 2020, consolidating its position as the main offshore option to India.

• CC/BPO 2010 $ 8.4 Billion

• CC/BPO 2020 $ 18.5 Billion

• CC/BPO 2010 $ 8.4 Billion

• CC/BPO 2020 $ 18.5 Billion

Vendor Consolidation: Clients will focus on managing fewer provider relationships.Vendor Consolidation: Clients will focus on managing fewer provider relationships.

Quality: Companies will continue to demand higher quality interactions and added value. Quality: Companies will continue to demand higher quality interactions and added value.

Hosted Solutions in the cloud: Virtualization technology will further penetrate the marketplace.

Hosted Solutions in the cloud: Virtualization technology will further penetrate the marketplace.

Increased Use of Analytics & Performance tools: Augmented level of company and agent productivity will be key.

Increased Use of Analytics & Performance tools: Augmented level of company and agent productivity will be key.

Vertical Expertise & Balanced Portfolio: Companies will be offering specialized solutions but still try to maintain a balanced portfolio.

Vertical Expertise & Balanced Portfolio: Companies will be offering specialized solutions but still try to maintain a balanced portfolio.

CALA consolidation as the main Nearshore option: Latin America will further penetrate U.S. Market gaining share over APAC locations.

CALA consolidation as the main Nearshore option: Latin America will further penetrate U.S. Market gaining share over APAC locations.

Contact Center / BPO Key Trends 2020

•CC/BPO 2010 seats 421,000

• CC/BPO 2020 seats 859,929

•CC/BPO 2010 seats 421,000

• CC/BPO 2020 seats 859,929

Source: Frost & Sullivan

22

The Latin American Cloud

23

The reality of SMBs must change quickly. They have to become more professional in terms of structure and management.

Today, with the global economy and the Internet, either you are constantly updated or you die in the market.

Small Business - Bahia

SMBs do not perceive access to credit as a way to expand or grow in capacity. It is more related to an organize cash flow.

Small Business - São Paulo

Today there is an enormous lack of affordable management software.

Small Business - São Paulo

Source: Frost & Sullivan

24

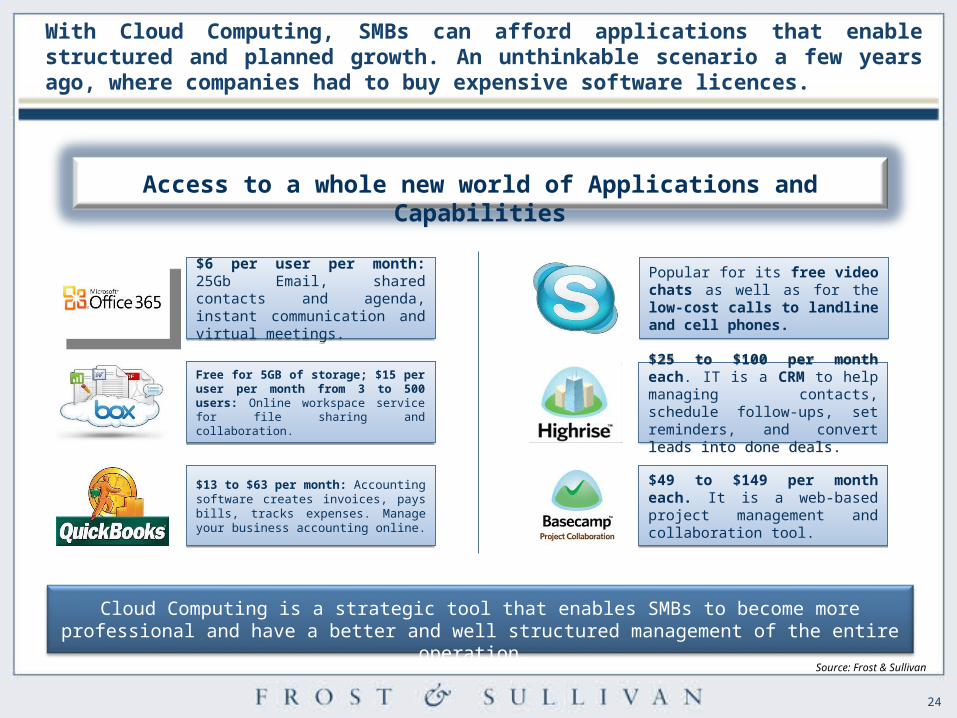

With Cloud Computing, SMBs can afford applications that enable structured and planned growth. An unthinkable scenario a few years ago, where companies had to buy expensive software licences.

Access to a whole new world of Applications and Capabilities

$6 per user per month: 25Gb Email, shared contacts and agenda, instant communication and virtual meetings.

$6 per user per month: 25Gb Email, shared contacts and agenda, instant communication and virtual meetings.

Free for 5GB of storage; $15 per user per month from 3 to 500 users: Online workspace service for file sharing and collaboration.

Free for 5GB of storage; $15 per user per month from 3 to 500 users: Online workspace service for file sharing and collaboration.

$13 to $63 per month: Accounting software creates invoices, pays bills, tracks expenses. Manage your business accounting online.

$13 to $63 per month: Accounting software creates invoices, pays bills, tracks expenses. Manage your business accounting online.

Popular for its free video chats as well as for the low-cost calls to landline and cell phones.

Popular for its free video chats as well as for the low-cost calls to landline and cell phones.

$25 to $100 per month each. IT is a CRM to help managing contacts, schedule follow-ups, set reminders, and convert leads into done deals.

$25 to $100 per month each. IT is a CRM to help managing contacts, schedule follow-ups, set reminders, and convert leads into done deals.

$49 to $149 per month each. It is a web-based project management and collaboration tool.

$49 to $149 per month each. It is a web-based project management and collaboration tool.

Cloud Computing is a strategic tool that enables SMBs to become more professional and have a better and well structured management of the entire operation.

Source: Frost & Sullivan

25

Despite all the benefits experienced with cloud base solutions, there are still great issues to discuss. From security to legal aspects, the market has a lot of questions to answer.

Regulations

Governance

Applications

Lack of Control

ConsumerizationConsumerization SecuritySecurity AvailabilityAvailability Data LossData Loss

Privacy

MobilityMobility

ArchitectureArchitecture

BillingBilling

SLAsSLAs

LegalLegal

Cloud Ownership. Who owns the Cloud?

Source: Frost & Sullivan

26

End-User empowerment: with all the possibilites regarding internet, connectivity and cloud computing, consumers can impact directly on brand credibility and rapidly influence multiple users.

Microblogging

Photo Sharing

Media Sharing

Aggregators

Vídeo SharingSocial Relationship

Local SC PlatformsMusic Sharing

Arab Spring

Brazil against

corruption

Social Movements

Political Movements

...and there is more...

Imagine what can happen to your company, your strategic plans, file, data and brand image.

Source: Frost & Sullivan

27

With all of the changes in the market, we are facing a new world with increasingly complex business challenges. How to be prepared in order to take advantage of rising opportuinities?

Mobility is rapidly increasing together with the amount of data generated by corporations, end-users and M2M. The challenge is how to control and monitor all this data to guarantee its security and its use as strategic information. A bigger and more complex world of Analytics is ahead.

Mobility is rapidly increasing together with the amount of data generated by corporations, end-users and M2M. The challenge is how to control and monitor all this data to guarantee its security and its use as strategic information. A bigger and more complex world of Analytics is ahead.

Data Explosion driving new Business Analytics MarketData Explosion driving new Business Analytics Market

The ROI expected by the end-user is changing to a more complex demand. Executives who buy technologies require a more detailed analysis focused on business benefits including not only cost reduction, but also processing optimization, revenues, scalability, time to market and so on.

The ROI expected by the end-user is changing to a more complex demand. Executives who buy technologies require a more detailed analysis focused on business benefits including not only cost reduction, but also processing optimization, revenues, scalability, time to market and so on.

ROI – Consultive ApproachROI – Consultive Approach

The new CIO works closely with the CFO, COO and CEO developing products, processes, sales operation and operational areas. His role has become more important, because he understands corporate technology, and is able to see how to improve business areas.

The new CIO works closely with the CFO, COO and CEO developing products, processes, sales operation and operational areas. His role has become more important, because he understands corporate technology, and is able to see how to improve business areas.

CIO becoming a growth enablerCIO becoming a growth enabler

Source: Frost & Sullivan

28

Security is one of the main concerns in the market and needs to be closely discussed. How to control and garantee security with mobility and data explosion?

Infrastructure SecutiryInfrastructure Secutiry

The reality and priorities regarding security are changing among companies in all verticals in the market due to new business models and trends, like cloud computing and mobility. We are moving from a pure infrastruture security model to a more complex scenario regarding information security.

The reality and priorities regarding security are changing among companies in all verticals in the market due to new business models and trends, like cloud computing and mobility. We are moving from a pure infrastruture security model to a more complex scenario regarding information security.

Information SecutiryInformation Secutiry

Firewall

VPN

Gateway

Data Loss

Correlate Event

Biometrics

Mobile Shipments (Brazil)Mobile Shipments (Brazil)

20102010 12.8 Mi Mobile Devices12.8 Mi Mobile Devices

20202020 97.1 Mi Mobile Devices97.1 Mi Mobile Devices

How to maximize devices security?

How to offer Cloud based Apps to be accessed from any device anywhere?

Can I outsource managed security from these devices? Which Apps can be hosted in the Cloud?

Source: Frost & Sullivan

29

SMART Clouds in 2020: FLEXIBLE and CUSTOMIZED Clouds Created By Consolidation Of Different Off-premise HYBRID Cloud Services

SMART Clouds address a particular business (or personal) need for a specific period of time and can be integrated with existing on-premise IT infrastructure base - seamlessly and

securely.

SMART Clouds address a particular business (or personal) need for a specific period of time and can be integrated with existing on-premise IT infrastructure base - seamlessly and

securely.

One – Stop Shop Enterprise End-To-End Solutions for a Specific Period of Time

Easy Set-Up of Home Based Offices

Standardized Application Programming Interface (API) allowing for faster time to market of new services, utilizing smart network asset

Saves Downtime of Searching for Specific Business Solutions

SELF SERVICE IT - Selective Choice of Information (Eg. Retail Clouds)

GREEN IT: Energy and Cost Saving Benefits as Capacity of Cloud can be Customized to the Size of Workload

Availability of Free Large Virtual Infrastructure for Storage and Networking

Easy Integration of On-Premise IT infrastructure with SMART Clouds

Integration of Several Hybrid Clouds Enables Seamless Real-Time Switching from Public to Private Clouds driving the Need For High Security Levels

Benefits of flexibility, technology advances and cost savings would help reduce operational expenditure

Everything-as-a-ServiceSource: Frost & Sullivan

30

Social Networks

31

19951985 2005

Roadmap: from mere communication platforms, SNs are bound to become a virtual environment with multiple uses, from collaborative working platforms to a giant database of customer’s information.

2010 2015 2020

Single online profile, social data

intelligence, highly personalized environments

Online BBS Communities,

closed groups for communication

Media sharing now available, relative

popularization

Massive adoption, real time highly

interactive environment , online

profiles

Mobile applications, increase in the corporate usage (advertisement, recruitment, customer relationship), location-

SNs are expected to permeate user’s life on many aspects. Augmented reality, geosocial features and data mining software will bring users to a greater level of immersion, and allow companies to develop personalized strategies to reach customers

Geographic services and capabilities will enable additional social dynamics to SNs, such as augmented reality features.

Geographic services and capabilities will enable additional social dynamics to SNs, such as augmented reality features.

Geosocial NetworkingGeosocial Networking

Virtualized and highly collaborative environments will be default, workers will participate on projects that fit best to their expertise.

Virtualized and highly collaborative environments will be default, workers will participate on projects that fit best to their expertise.

Virtual Work EnvironmentVirtual Work Environment

The population will be more politically engaged and politics will rely on the use of SNs to nurture a closer relationship with the public.

The population will be more politically engaged and politics will rely on the use of SNs to nurture a closer relationship with the public.

Political EngagementPolitical Engagement

Higher integration of SNs. Profiles will be open to various channels, allowing users to generate one single profile and export its data to multiple environments.

Higher integration of SNs. Profiles will be open to various channels, allowing users to generate one single profile and export its data to multiple environments.

Products, services and media content will be offered and tailored according to individuals tastes and preferences based on online profiles.

Products, services and media content will be offered and tailored according to individuals tastes and preferences based on online profiles.

Content PersonalizationContent Personalization

Data mining and semantic comprehension software will extract knowledge from SNs databases, to be used as strategic guidelines by companies.

Data mining and semantic comprehension software will extract knowledge from SNs databases, to be used as strategic guidelines by companies.

SN Data IntelligenceSN Data Intelligence

The purchase process will be heavily influenced by recommendations and interests directly related to the user’s personal profile and its social circles.

The purchase process will be heavily influenced by recommendations and interests directly related to the user’s personal profile and its social circles.

Smart CommerceSmart Commerce

Source: Frost & Sullivan

33

Smart Devices

34

Consumer Electronics In 2020: Faster, smaller, cheaper and customized with shorter development life-cycles, these devices will be connected to the users online profile and offer a seamless personalized experience.

Smart Interconnected DevicesSmart Interconnected Devices Holographic ProjectionHolographic Projection Mobile Phones: Projection, Visual Search and MorphingMobile Phones: Projection,

Visual Search and Morphing

Consumer devices will be interconnected to the user’s profile, guaranteeing a personalized experience based on preferences.

Touchscreen Window With Built-in Camera, Scanner, Wi-fi, Google Maps Intuitive Search Tools.

Mobile Projection Technology

Morphing– Allowing Users to Transform Mobiles Into Different Shapes

E-MediaE-Media

Digital Paper E-Media Displays

Products will communicate to enhance usage, ranging from intelligent cars with cloud based anti-collision systems, to smart houses that optimize energy expenditure.

Through the use of motion detection sensors, it can be applied to remote collaborative functions, prototype designing and improved communication systems.

Source: Frost & Sullivan

35P5DB-MT

Fixed and mobile broadband access are likely to grow at double-digit CAGR in the next decade, pushed by connected devices.

4G rollout will start by 2012, to reach 29 million

lines by 2016

CAGR: 163.4%

4G rollout will start by 2012, to reach 29 million

lines by 2016

CAGR: 163.4%

Total pay-TV subscribers expected to reach 61

million by 2015

CAGR: 13.0%

Total pay-TV subscribers expected to reach 61

million by 2015

CAGR: 13.0%

416 million 3G lines by 2016

CAGR: 48.0%

416 million 3G lines by 2016

CAGR: 48.0%

An impressive increase in broadband subscribers

77 million (2015)

CAGR: 17.1%

An impressive increase in broadband subscribers

77 million (2015)

CAGR: 17.1%

Internet users

216 million (2010)

Growth will be boosted by mobile device

penetration

Internet users

216 million (2010)

Growth will be boosted by mobile device

penetration

The mobile subscriber base

705 million (2016)

CAGR: 8.0%

The mobile subscriber base

705 million (2016)

CAGR: 8.0%

Video games and over-the-top to grow

penetration with the local presence of Microsoft, Sony, Apple and other

manufacturers

Video games and over-the-top to grow

penetration with the local presence of Microsoft, Sony, Apple and other

manufacturers

Machine-to-Machine (M2M)

The most recent development in the industry, with high

expectations

Machine-to-Machine (M2M)

The most recent development in the industry, with high

expectationsSource: Frost & Sullivan, ITU

36

Latin America will switch-off analogue television by 2022; over 572 Million people should have access to DTT transmission, and most of them to interactive services.

2010:•45% of the Brazilians with Digital TV coverage•DTT in some mobile devices (handsets, GPS, pen drive)•TV sets and set-top-boxes with interactivity middeware Ginga: 0%

2020:•99% of the Brazilians with Digital TV coverage•DTT in all devices with screens (Tablets, buit-in cars, etc.) •TV sets and set-top-boxes with interactivity middleware Ginga: 100% of the shipments from 2013, gradually substituting all devices

Digitalization and interactivity is likely to create business opportunities in the media and communication industry on the continent

Country Switch-off

Argentina 2019

Brazil 2016

Chile 2016

Colombia 2019

Mexico 2015

Venezuela 2015

• T-Commerce• T-Learning• T-Gov• T-Banking

• User participation• Content search• Others

Business opportunities

Note: Honduras and Paraguay are the last to switch-off analogue TV, in 2022Source: Regulators and Brazilian Ministry of Communications, Frost & Sullivan analysis.

The analogue TV switch-off, in the six major Latin American

economies, is planned to happen until 2019

37

The increased digitalization of content, associated with smart device penetration and internet access will pressure business models of content producers and distributors.

• Personalized television (multiple channels, over-the-top and VoD)

• Digital magazines and newspapers

• Digital radio, with text and audio information

• Personalized television (multiple channels, over-the-top and VoD)

• Digital magazines and newspapers

• Digital radio, with text and audio information

• Linear television (few free channels and limited line up in Pay TV service)

• Paper magazines and newspapers

• Analogue radio, with audio information

• Linear television (few free channels and limited line up in Pay TV service)

• Paper magazines and newspapers

• Analogue radio, with audio information

Advertising expedintures (illustrative)

Cheaper ElectronicsCheaper Electronics

Fixed and mobile broadband penetration

Fixed and mobile broadband penetration

Change in consumer behaviorChange in consumer behavior

Source: Frost & Sullivan

38

Conclusions

39

How will the government address regulation issues with new technologies in a transparent and effective way? How will it be able to foment the national industry?

How will the government address regulation issues with new technologies in a transparent and effective way? How will it be able to foment the national industry?

How will companies maintain their core business whilst expanding, exploring and adapting to new realities and markets?

How will companies maintain their core business whilst expanding, exploring and adapting to new realities and markets?

Technologies hereby presented will require important investments, how will companies guarantee an interesting ROI to maintain profitable?

Technologies hereby presented will require important investments, how will companies guarantee an interesting ROI to maintain profitable?

Will the consumer’s learning curve keep up to the speed of adoption of new technologies? How to educate users in that matter?

Will the consumer’s learning curve keep up to the speed of adoption of new technologies? How to educate users in that matter?

7

Fonte: Frost & Sullivan

A continent burgeoning with opportunity in “enabling” connectivity. However, there are still many challenges to be addressed.

Social Media has changed from a communication platform to an strategic subject for both corporations and consumers, how will companies make the best use of it?

Social Media has changed from a communication platform to an strategic subject for both corporations and consumers, how will companies make the best use of it?