Global Economic Prospects 2004: Realizing the Development Promise of the Doha Agenda. Mick Riordan and Richard Newfarmer World Bank. Sept 3, 2003. Main messages…. Global recovery, though still fragile, is now underway, and developing countries are likely to grow faster than rich countries. - PowerPoint PPT Presentation

Global Economic Prospects 2004: Global Economic Prospects 2004: Realizing the Development Realizing the Development Promise Promise of the Doha Agenda of the Doha Agenda Sept 3, 2003 Mick Riordan and Richard Newfarmer World Bank

Transcript

Global Economic Prospects 2004:Global Economic Prospects 2004:

Realizing the Development Realizing the Development PromisePromise

of the Doha Agendaof the Doha Agenda

Sept 3, 2003

Mick Riordan and Richard NewfarmerWorld Bank

Global recovery, though still fragile, is now underway, and developing countries are likely to grow faster than rich countries.

The Doha Agenda has the potential to speed growth, raise incomes, and reduce poverty, and all countries have an interest in its success.

But to realize this potential, governments have to tackle inequities in the world trading system – and to forge an agreement than benefits the poor.

Main messages…Main messages…

0

1

2

3

4

5

1981 82 83 84 85 86 87 88 89

1990 91 92 93 94 95 96 97 98 99

2000 1 2 3 4

2005

Early 1990s recession

East Asia financial crisis

2001 downturn

The rich countries: a moderate recovery...The rich countries: a moderate recovery...Real GDP, percent changeReal GDP, percent change

Early 1980s recession

High income countriesHigh income countries

ForecastForecast

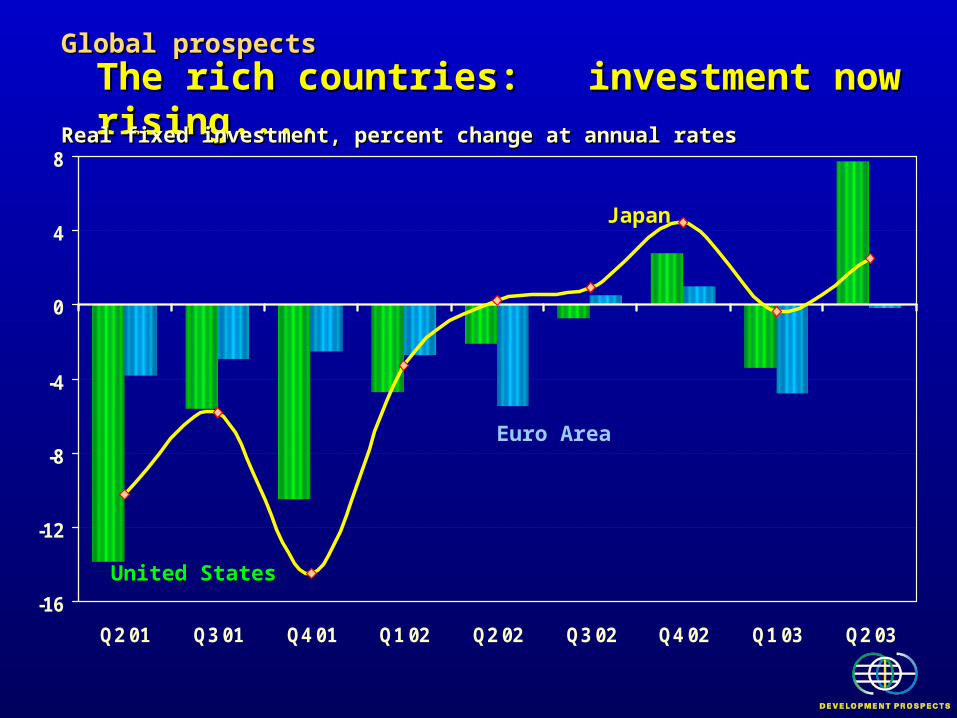

The rich countries: investment now rising....The rich countries: investment now rising....Global prospectsGlobal prospects

Real fixed investment, percent change at annual ratesReal fixed investment, percent change at annual rates

Longer-term structural problems persist in the rich countries

Potential for additional geopolitical shocks

And macro policy has largely run its course— may be insufficient to meet new challenges

- Interest rates at lows - Fiscal deficits widen across

the rich countries

Global prospectsGlobal prospects

... But risks remain... But risks remain

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

Germany United States Japan

General government financial balances, % GDPGeneral government financial balances, % GDP

Source: OECD data and projections.

20012001

20022002 20032003

Global prospectsGlobal prospects

... But risks remain... But risks remainGeneral government financial balances, % GDPGeneral government financial balances, % GDP

Source: OECD data and projections.

20012001

20022002 20032003

Longer-term structural problems persist in the rich countries

Potential for additional geopolitical shocks

And macro policy has largely run its course— may be insufficient to meet new challenges

- Interest rates at lows - Fiscal deficits widen across

the rich countries

Hence, addressing the structural issues is key

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

Germany United States Japan

0

1

2

3

4

5

Early 1980s debt crisis

1990s recession Transition countries

East Asia financial crisis

2001 Global downturn

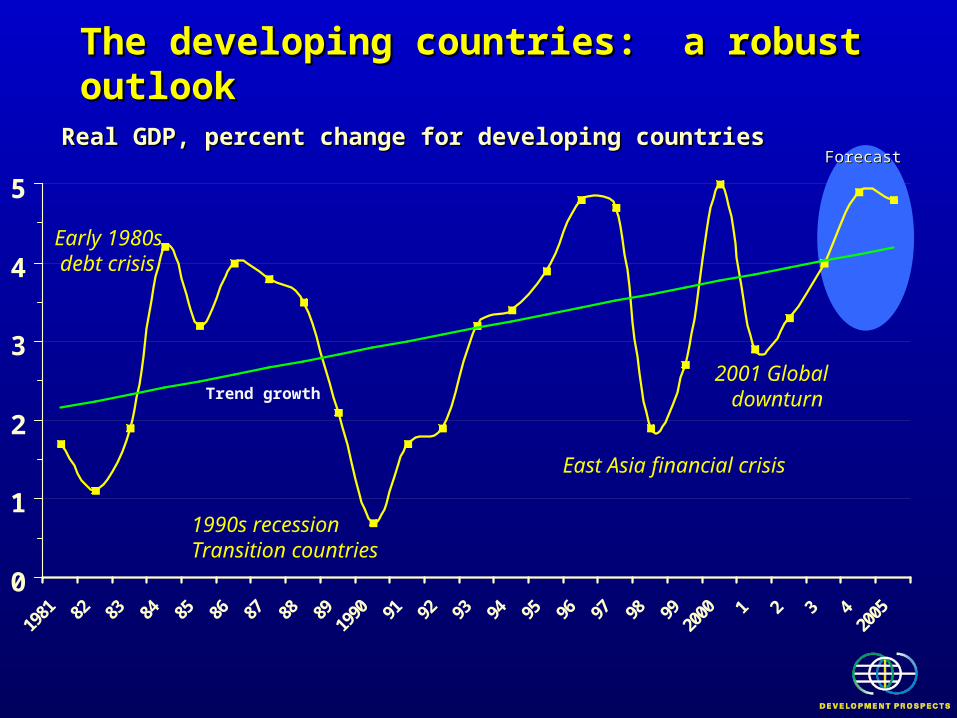

Real GDP, percent change for developing countriesReal GDP, percent change for developing countriesForecastForecast

The developing countries: a robust outlook The developing countries: a robust outlook

0

1

2

3

4

5

Early 1980s debt crisis

1990s recession Transition countries

East Asia financial crisis

2001 Global downturn

The developing countries: a robust outlook The developing countries: a robust outlook

Real GDP, percent change for developing countriesReal GDP, percent change for developing countries

Trend growth

ForecastForecast

6.1

-0.2

3.2 3.0

6.5

5.4

4.3

3.13.5 3.4

4.6

3.4

-1.0

0.5

2.0

3.5

5.0

6.5

East Asia South Asia East. Eur. &Central Asia

LatinAmerica

Middle East& NorthAfrica

Sub-SaharanAfrica

2001-2002 2003-2005

Global prospectsGlobal prospects

Real GDP growth, 2001-2005Real GDP growth, 2001-2005

Near-term step up in growth across regions... Near-term step up in growth across regions...

Global prospectsGlobal prospects

Real GDP Real GDP per capitaper capita growth, 1990s and 2006-2015 growth, 1990s and 2006-2015

... and improved per-capita growth longer term ... and improved per-capita growth longer term

6.4

3.3

1.71.2

-0.2

5.4

4.13.3

2.5 2.5

1.6

-1.8-2.5

-1.0

0.5

2.0

3.5

5.0

6.5

East Asia South Asia East. Eur. &Central Asia

LatinAmerica

Middle East& NorthAfrica

Sub-SaharanAfrica

1990s 2006-2015

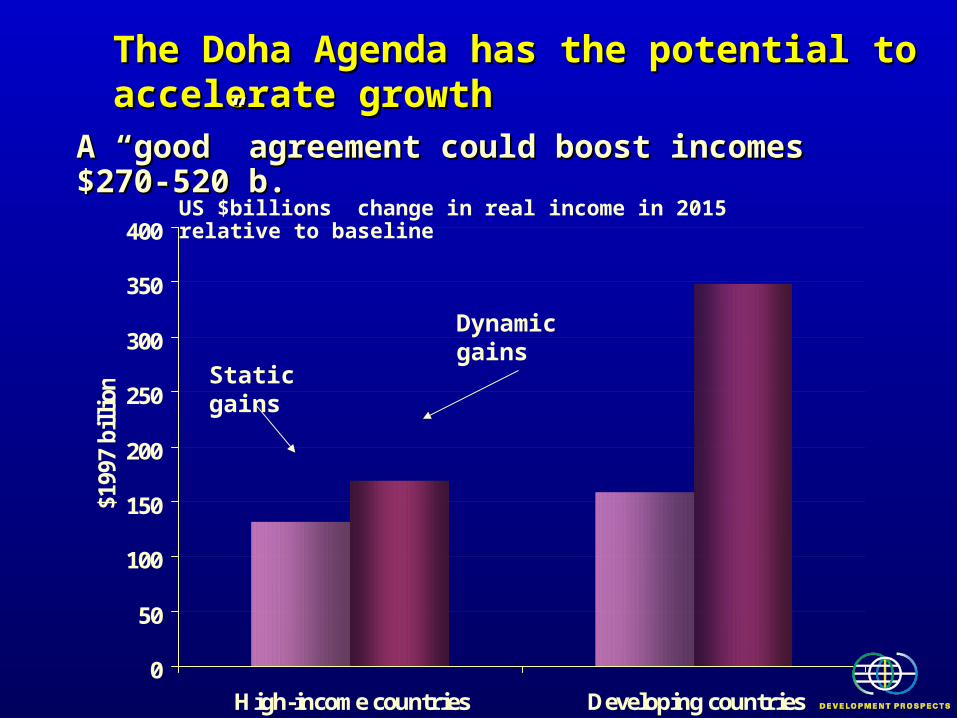

The Doha Agenda has the potential to The Doha Agenda has the potential to accelerate growth accelerate growth

0

50

100

150

200

250

300

350

400

High-income countries Developing countries

$199

7 bi

llion

Static gains

Dynamic gains

US $billions change in real income in 2015 relative to baseline

A “good” agreement could boost incomes $270-520 b. A “good” agreement could boost incomes $270-520 b.

More people would be lifted above the More people would be lifted above the poverty line…140 million…many in Africapoverty line…140 million…many in Africa

0

10

20

30

40

50

60

70

East Asiaand Pacific

Europe andCentral Asia

LatinAmerica and

theCaribbean

Middle Eastand North

Africa

South Asia Sub-SaharanAfrica

Mill

ions

Source: World Bank staff simulations.

change in the number of poor in 2015 relative to the baseline

$1 per day$1 per day

$2 per day$2 per day

Agriculture is a priority, particularly reducing border protection and subsidies in rich countries

Reducing protection on manufactures, particularly in the South

Helping low-income countries reduce reliance on trade preferences and increase competitiveness exports

But to realize development promise, an But to realize development promise, an agreement has to reduce barriers to the agreement has to reduce barriers to the products the poor produceproducts the poor produce

Developing countries have failed to penetrate agricultural markets of rich countries

0

5

10

15

20

25

30

1980 1990 2000

Exports to poor countriesExports to poor countries

Exports to rich countriesExports to rich countries

0

5

10

15

20

25

30

1980 1990 2000

Developing countries’ share of total world exportsDeveloping countries’ share of total world exports

ManufacturingManufacturing AgricultureAgriculture

Exports to rich countriesExports to rich countries

Exports to poor countriesExports to poor countries

Protection in rich countries is high and unchanged since Protection in rich countries is high and unchanged since the Uruguay round…the Uruguay round…

Industrial countries: Producer SupportIndustrial countries: Producer Support

Direct subsidies

* As a percent of output at world pricesSource: OECD

perc

e nt *

Border protection

0

50

100

150

200

250

300

86-88 99-01 86-88 99-01 86-88 99-01Other

industrialEU US Japan

86-88 99-01

Protection in rich countries is high and unchanged since Protection in rich countries is high and unchanged since the Uruguay round…though developing countries have the Uruguay round…though developing countries have reduced barriersreduced barriers

Developing countries: average tariffs for Developing countries: average tariffs for agricultureagriculture

Industrial countries: Producer Support EstimateIndustrial countries: Producer Support Estimate

Direct subsidies

* As a percent of output at world pricesSource: OECD

perc

e nt *

perc

e nt

Border protection

0

50

100

150

200

250

300

86-88 99-01 86-88 99-01 86-88 99-01Other

industrialEU US Japan

86-88 99-01

Source: TRAINS

0

50

100

150

200

250

300

1990 1995 2000

Rich countries levy higher tariffs on imports Rich countries levy higher tariffs on imports from developing countriesfrom developing countries

0123456789

Industrial LatinAmerica

andCaribbean

Sub-SaharanAfrica

East Asia Europeand

CentralAsia

MiddleEast

SouthAsia

Av tariffs of industrial countries charged to exporters Av tariffs of industrial countries charged to exporters from various regions, 1997 (percent)from various regions, 1997 (percent)

……and so do other developing countriesand so do other developing countries

0

5

10

15

20

25

East Asia Europeand

CentralAsia

LatinAmerica

MiddleEast

SouthAsia

Sub-SaharanAfrica

Industrial

Protection rates faced by Latin American exporters of manufactures, 1997

percent

Developing countries pay more of their foreign Developing countries pay more of their foreign tariffs to rich countries and to neighborstariffs to rich countries and to neighbors

0102030405060708090

100

Industrial East Asia Europe andCentral

Asia

LatinAmerica

andCaribbean

Middle Eastand North

Africa

South Asia Sub-SaharanAfrica

Share of tariff burden, percent

Rest of worldRest of world

Intra-regionIntra-region

IndustrialIndustrial

Developing countries have an interest in reducing protection Developing countries have an interest in reducing protection in the South as well as the Northin the South as well as the North

Share of LDCs in EU and US imports, 1966–2002 (percent)

Low income countries have relied too much Low income countries have relied too much on trade preferences..with only marginal on trade preferences..with only marginal successsuccess

Share of LDCs in EU and US imports, 1966–2002 (percent)

Low income countries have relied too much Low income countries have relied too much on trade preferences..with only marginal on trade preferences..with only marginal successsuccess

0.0%

0.2%0.4%

0.6%0.8%

1.0%

1.2%1.4%

1.6%1.8%

2.0%

1996 1997 1998 1999 2000 2001 2002

CBI

AGOA

Andean

Share of preferential programs in US imports, 1966–2002 (percent)

Improving trade logistics can be as Improving trade logistics can be as important as cutting tariffs…ports, customs, important as cutting tariffs…ports, customs, transporttransport

0 2 4 6 8 10 12

South Asia

Africa

Latin Americaand Caribbean

East Asia andPacific

Developed

Average number of days to clear customs for sea cargo

Source: International Exhibition Logistics Associates, based on a sample of countries in each region

Development assistance is key to improving ports, customsDevelopment assistance is key to improving ports, customsand trade infrastructureand trade infrastructure

For the development promise of the Doha For the development promise of the Doha agenda to be realized, all countries have to agenda to be realized, all countries have to take responsibilitytake responsibility

Rich countries have to lead in agriculture, labor- intensive manufactures, and development assistance as well as in services (mode 4)

Middle-income countries have to be willing to lower high external tariffs—benefiting themselves and their neighbors

Low-income countries have to rely less on preferences and reform trade-related institutions.

Global Economic Prospects 2004:Global Economic Prospects 2004:

Realizing the Development Realizing the Development PromisePromise