Duncan Meldrum Business of Cleans April 1, 2019 1 Global Economy Outlook*: The Backdrop for Semiconductors Business of Cleans April 1, 2019 Duncan Meldrum Chief Economist, Hilltop Economics, LLC [email protected]610-709-7951 *A global outlook based on Consensus Economics, Inc. CONSENSUS FORECASTS®

Transcript

Duncan MeldrumBusiness of Cleans April 1, 2019 1

Global Economy Outlook*: The Backdrop for Semiconductors

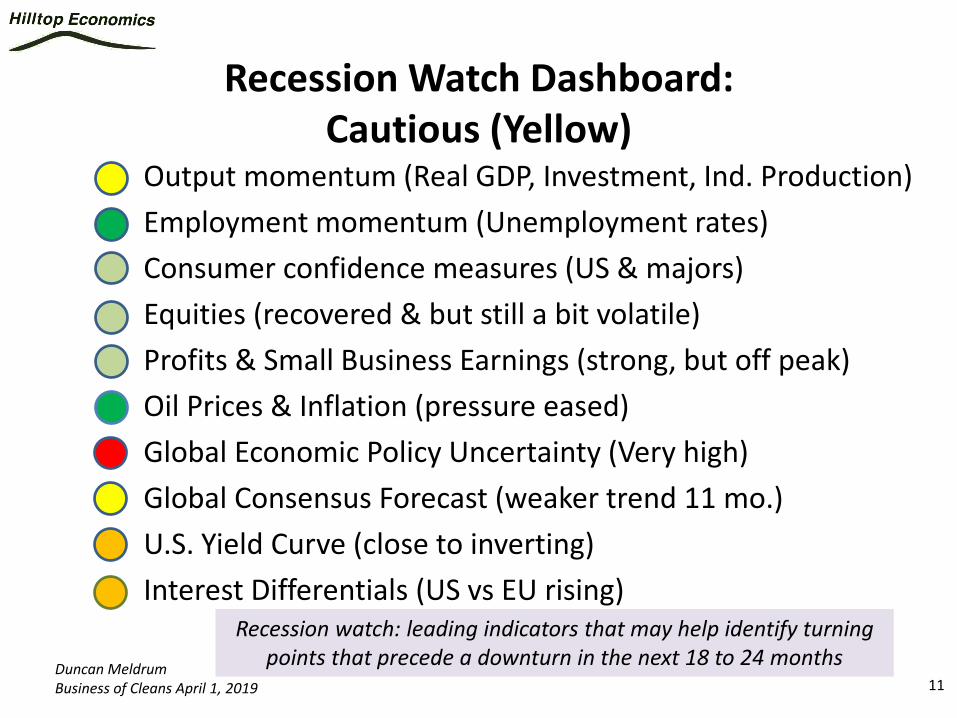

• In the accelerating phase of the economic cycle YES– Healthy consumer YES– Investment upsurge driving the global economy stronger YES– Slightly higher inflation, diverging interest rates YES– Currency unsettled YES– Potential for much higher economic policy uncertainty: trade,

geopolitics the current wild cards YES

• Healthy backdrop for semiconductor industry:– Demand for semiconductors grows above trend YES– Wafer Fab Equipment investment strong Peaked 18M5– Risks: excess capacity expansion, supply chain imbalances

(wafers?) and final demand uncertainty (5G, AI, mobile and computing devices)

2018 OUTCOME

Duncan MeldrumBusiness of Cleans April 1, 2019 4

Summary Overview: 2019-2020

• In the mature phase of the business cycle with decelerating growth and a rising risk of recession– Investment moderating despite need

• Less-healthy backdrop for semiconductor industry

SPCC 2019 Forecast

Duncan MeldrumBusiness of Cleans April 1, 2019 55

Consensus: Growth Weakens to Trend in 2019-20

MARCH 2019

-2

-1

0

1

2

3

4

5

07 08 09 10 11 12 13 14 15 16 17 18 19 20

World* Real GDP Growth

2018: 3.0% 2019: 2.7% 2020: 2.7%

% C

ha

ng

e

*World: 85 major economies,

Data: World Bank, Hilltop Economics,

Consensus Forecasts, Mar19

Duncan MeldrumBusiness of Cleans April 1, 2019 66

34

36

38

40

42

44

46

48

50

02 04 06 08 10 12 14 16 18

Actual Real GDP

Potential

TR

2010 U

S$

24 Major Developed Economies

Src: Hilltop Economics, World Bank, IMF

Estimating the Global Output GapA closed gap is the limiting factor to long-term growth

Output “Gaps”

Duncan MeldrumBusiness of Cleans April 1, 2019 77

Global Output Gap Disappeared in 2018In 2018, Real GDP finally pushed above potential

95

96

97

98

99

100

101

102

103

104

105

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Re

al G

DP

as

a P

erc

en

t of P

ote

ntia

l Ou

tpu

t

24 Major Developed Economies

Src: Hilltop Economics, World Bank, IMF

Output “Gaps”

Duncan MeldrumBusiness of Cleans April 1, 2019 88

A Weaker Investment Forecast(Investment SHOULD be picking up – as it did in 04-07)

-8

-6

-4

-2

0

2

4

6

8

95

96

97

98

99

100

101

102

103

104

105

02 04 06 08 10 12 14 16 18 20

%C

H V

S Y

R A

GO

Real G

DP

as a

Perc

en

t of P

ote

ntia

l GD

P

~25% of GDP

Duncan MeldrumBusiness of Cleans April 1, 2019 9

Investment Growth: Needed to Drive Cycle Higher But Forecast to Slow

• Revenue growth OK– Real GDP growth (volume) now at 2.7%

– Some inflation (price) on average from ~1% - 2%

– “Revenue” now ~4 ½ %

• Output gaps closed, need capital to grow

• Profitability still positive

• Risk aversion is the problem again – Forecasts on a downward trajectory

– Economic policy uncertainty volatile and high on a global level

– Interest rates reflecting the uncertainty

Duncan MeldrumBusiness of Cleans April 1, 2019 10

Many Reasons for the Return of Risk Aversion

• Economic Policy Uncertainty– Trade wars (shifting international institutional arrangement)– US (post-stimulus fiscal policy, post-govt shutdown, monetary

policy, immigration)– Europe (Brexit, Italy, France, EU-wide e.g. immigration)– China stimulus impact, international situations– Japan tax increases

• Financial markets– Concern with policy– Concern about profits– Concern about the strong dollar and rising US interest rates– Concern about debt– Which explains the weaker real investment forecast & the rising

probability of an economic downturn (recession), not just slower growth

Main Economic Indicators (database), http://dx.doi.org/10.1787/data-00052-en

Mar 26, 19

% Unemp. 2018 2019 2020

Japan 2.4 2.4 2.4

So. Korea 3.8 3.9 3.9

Taiwan 3.7 3.7 3.8

Germany 5.2 4.9 4.8

Eurozone 8.2 7.8 7.6

UK 4.1 4.1 4.2

US 3.9 3.7 3.7

Duncan MeldrumBusiness of Cleans April 1, 2019 15

CPI Inflation Weakens in 2019 Despite tightness in labor markets and closed output gaps

CPI % Change 2016 2017 2018 2019 2020

China 2.0 1.6 2.1 2.1 2.1

Japan (0.1) 0.5 1.0 0.7 1.0

South Korea 1.0 1.9 1.5 1.3 1.6

Taiwan 1.4 0.6 1.4 0.8 1.1

Germany 0.5 1.8 1.8 1.5 1.6

France 0.2 1.0 1.9 1.3 1.5

Italy (0.1) 1.2 1.2 0.9 1.2

UK 0.7 2.7 2.6 2.2 2.2

US 1.3 2.1 2.4 1.8 2.2

Hilltop Economics, Based on Consensus Forecasts, March 192018 actual vs. forecast: China: -0.2, Germany: +0.1, US & Japan no error

Duncan MeldrumBusiness of Cleans April 1, 2019 1616

Oil Prices

0

20

40

60

80

100

120

140

98 00 02 04 06 08 10 12 14 16 18 20 22

$/B

BL

- B

ren

t O

il P

ric

e

Source: NBER - Recession dating, EIA,

St Louis Federal Reserv e Economic Database

Fcst: Hilltop Economics from Consensus Forecasts Mar 19

Duncan MeldrumBusiness of Cleans April 1, 2019 1717

50

60

70

80

90

100

110

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

USA (to March 2019)

95

96

97

98

99

100

101

102

103

104

105

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CHINA (to December 18)

OECD, "Main Economic Indicators - complete database", http://dx.doi.org/10.1787/data-00052-en (Accessed on 3/27/19)Copyright, 2016, OECD. Reprinted with permission.

97.0

97.5

98.0

98.5

99.0

99.5

100.0

100.5

101.0

101.5

102.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

EUROZONE

GREAT BRITAIN

OECD, "Main Economic Indicators - complete database", http://dx.doi.org/10.1787/data-00052-en (Accessed on 3/27/19)Copyright, 2016, OECD. Reprinted with permission.

97.0

97.5

98.0

98.5

99.0

99.5

100.0

100.5

101.0

101.5

102.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

JAPAN (to February 2019)

OECD, "Main Economic Indicators - complete database", http://dx.doi.org/10.1787/data-00052-en (Accessed on 3/27/19)Copyright, 2016, OECD. Reprinted with permission.

Consumer Confidence Indexes Are HighBut off the 2018 peaks, with the exception of China

Peak

Duncan MeldrumBusiness of Cleans April 1, 2019 1818

400

800

1,200

1,600

2,000

2,400

2,800

3,200

98 00 02 04 06 08 10 12 14 16 18

S&

P 5

00

In

de

x

Shaded areas indicate recessions

Equity Prices Well Above December Lows as of End-

March, but Volatility Unsettling

18

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

II III IV I II III IV I II

2017 2018 2019

Duncan MeldrumBusiness of Cleans April 1, 2019 1919

Consensus: Profits Grow in Line with Revenue At Least Through 2020

4

5

6

7

8

9

10

11

12

13

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

Before Tax Profit (ZCPROFIT/GDP)

After Tax Profit (ZCPAT/GDP)

Pe

rce

nt

of

GD

P (

"M

arg

in")

Src: U.S. Bureau of Economic Analysis,

Hilltop Economics forecast based on Consensus Mar 19

Duncan MeldrumBusiness of Cleans April 1, 2019 2020

Small Business Optimism: Dropped Sharply in Q1Earnings Still High, But Off the Peaks

20

Src: NFIB, January 2019 release of Nov – Dec Survey data

Duncan MeldrumBusiness of Cleans April 1, 2019 2121

0

40

80

120

160

200

240

280

320

98 00 02 04 06 08 10 12 14 16 18 20

Global Economic Policy Uncertainty

Source: Scott Baker, Nicholas Bloom and Stev en J. Dav is

at www.PolicyUncertainty.com. Through February 2019

Ind

ex,

1997-2

015 M

ean

=100.0

Financial Crisis >

Uncertainty Peaked at Crisis Levels in January 2019

Uncertainty over future economic policy skyrocketed back to levels high enough- in the grey zone on the graph- to dampen investment by the middle of 2018.

Duncan MeldrumBusiness of Cleans April 1, 2019 2222

0

100

200

300

400

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

US

Europe

Ind

ex

Source: Scott Baker, Nicholas Bloom and Steven J. Davis

at www.PolicyUncertainty.com. Through Feb 19

Financial Crisis >

Economic Policy Uncertainty: U.S. & Europe

0

50

100

150

200

250

300

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Ind

ex

Source: Scott Baker, Nicholas Bloom and Steven J. Davis

at www.PolicyUncertainty.com. Through Feb 19

Financial Crisis >

Economic Policy Uncertainty: Japan

0

200

400

600

800

1,000

1,200

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

jpolunc_gbr

UK Economic Policy Uncertainty

Source: Scott Baker, Nicholas Bloom and Steven J. Davis

at www.PolicyUncertainty.com. Through Jan 19

<-

Lo

w U

ncert

ain

ty H

igh

->

0

200

400

600

800

1,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

jpolunc_kor

Economic Policy Uncertainty: China

Ind

ex

Source: Scott Baker, Nicholas Bloom and Steven J. Davis

at www.PolicyUncertainty.com. Through Feb 19

Uncertainty UP Everywhere Except U.S.

Duncan MeldrumBusiness of Cleans April 1, 2019 2323

Global Real GDP Forecasts for 2019 Lowered –Eleven Months in a Row

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

3.0

3.1

3.2

3.3

2018 2019 2020

%C

H V

S Y

R A

GO

Jan 17-Mar 19 Forecasts

Duncan MeldrumBusiness of Cleans April 1, 2019 2424

Yield Curve on Verge of Signaling RecessionUncertainty & fear of recession driving U.S. longer-term rates lower;

Consensus (the arrows) too optimistic as of the end of March

-1

0

1

2

3

4

5

6

2004 2006 2008 2010 2012 2014 2016 2018 2020

Fed Funds Rate (Policy)

3 Month T-Bill

10 Year T-Bond

Shaded area indicates recession

Pe

rce

nt

Duncan MeldrumBusiness of Cleans April 1, 2019 2525

U.S. Yield Curve Foreshadows RecessionSeven (eight?) inversions, seven recessions in the past 50 years

-4

-3

-2

-1

0

1

2

3

4

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

YIELD CURVE DAILY:

10 YR Minus 1 YR Treasuries

Pe

rce

nt

Shaded areas indicate recessions

Duncan MeldrumBusiness of Cleans April 1, 2019 2626

Different International Interest Rate TrendsA risk to financial flows, currencies, and a contributor to uncertainty

-1

0

1

2

3

4

5

6

7

00 02 04 06 08 10 12 14 16 18 20

3 Month LIBOR - US$

3 Month LIBOR - Euro

3 Month LIBOR - Japanese Yen

Perc

en

t

Duncan MeldrumBusiness of Cleans April 1, 2019 27

Summary: 2019-20• The world economy has moved into a decelerating phase

of the business cycle.

• Consensus expects slightly below-trend growth in key output measures (investment, consumption) that drive semiconductor demand.

• Recession risks rising from economic policy uncertainty (globally).