18

www.futuresource-consulting.com GLOBAL ED TECH DEVELOPMENTS IN 2014 18 th March 2015 Spending trends and key market developments Presenters: Mike Fisher Colin Messenger [email protected]

www.futuresource-consulting.com

GLOBAL ED TECH DEVELOPMENTS IN 2014

18th March 2015

Spending trends and key market developments

Presenters: Mike Fisher

Colin Messenger

| Futuresource Introduction

| Global Spend On Education Hardware in 2014

| Interactive Display Developments

| Computing in K-12 Developments

| Focus on Classroom Collaboration

| Questions

2 | © 2015 Futuresource Consulting Ltd

AGENDA

| Full service end-to-end research capabilities

| Global market coverage based on informed local

expertise

| Delivering excellence for 25 years

| Leading-edge data delivery and analysis

| Unrivalled client list, maintained through a

client-centred service approach

THE FUTURESOURCE FOCUS

Specialist Research & Consulting

3 | © 2015 Futuresource Consulting Ltd

6.18.1

9.4 10.2 10.5 10.6 11.5 12.3

4.5

4.3

5.25.0 4.6 4.2

4.13.8

0.6

0.5

0.40.3 0.3 0.2

0.20.2

0

2

4

6

8

10

12

14

16

18

2012 2013 2014 2015 2016 2017 2018 2019

Billions

ComplementaryDevices

ClassroomDisplays

Mobile PCs

11.2

12.9

14.915.5 15.115.3 15.7

16.3

GLOBAL K-12 EDUCATION HARDWARE SPEND

Total 2014 Worldwide Spend On Education Hardware – US$ 14.9 billion

4 | © 2015 Futuresource Consulting Ltd

# Market Value represents End User price excluding Tax

# Mobile PCs includes Notebooks, Netbooks, Chromebooks and Tablets purchased by institutions (not including ‘Bring Your Own’)

# Complementary devices includes Visualisers, Voting handsets, Voice Amplification, Lectern Panels and Education Slates

GLOBAL EDUCATION TECHNOLOGY SPEND - OVERVIEW 2014

Mobile PCs

$9.4 Bn

Classroom Displays

$5.2 BnIncluding:

IWB,

IFPD,

Interactive Projectors,

Projectors,

Attachment Devices,

Complementary Devices

$369mIncluding:

Visualisers,

Lectern Panels,

Voice Amplification,

Voting Systems,

Education Slates/Tablets

Mobile PC Account For 63% Of The Market

63%

35%

2%

5 | © 2015 Futuresource Consulting Ltd

INTERACTIVE DISPLAY MARKET REMAINS RESILIENT

Volumes To Decrease Slightly in 2015 But Value Increased By 19%

751

866

1,0

38

1,3

03

1,3

20

1,2

93

1,2

78

1,1

96

1,0

42

1,0

35

1,0

15

1.09

1.23

1.42

1.92

2.24

2.682.79

2.46

2.24 2.222.09

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

400

800

1,200

1,600

2,000

Valu

e –

Billions

(US$)

Volu

mes

-M

illions

Annual sales

Value $ M

6 | © 2015 Futuresource Consulting Ltd

# Market Value represents End User price excluding Tax

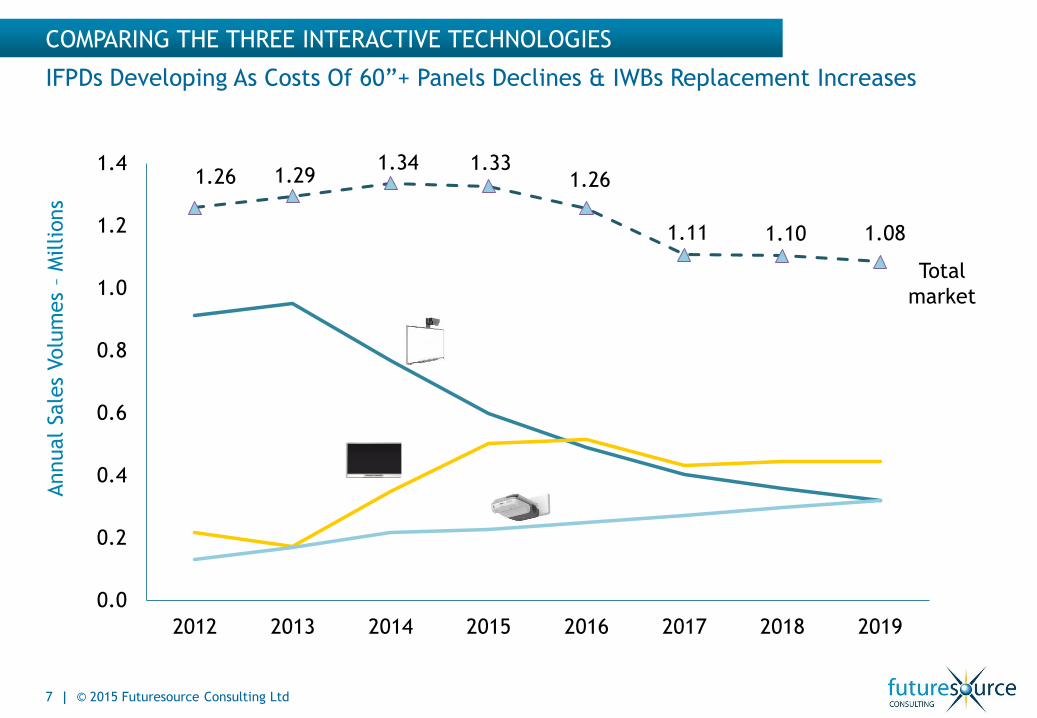

COMPARING THE THREE INTERACTIVE TECHNOLOGIES

1.26 1.291.34 1.33

1.26

1.11 1.10 1.08

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2012 2013 2014 2015 2016 2017 2018 2019

Annual

Sale

s Volu

mes

–M

illions

7 | © 2015 Futuresource Consulting Ltd

IFPDs Developing As Costs Of 60”+ Panels Declines & IWBs Replacement Increases

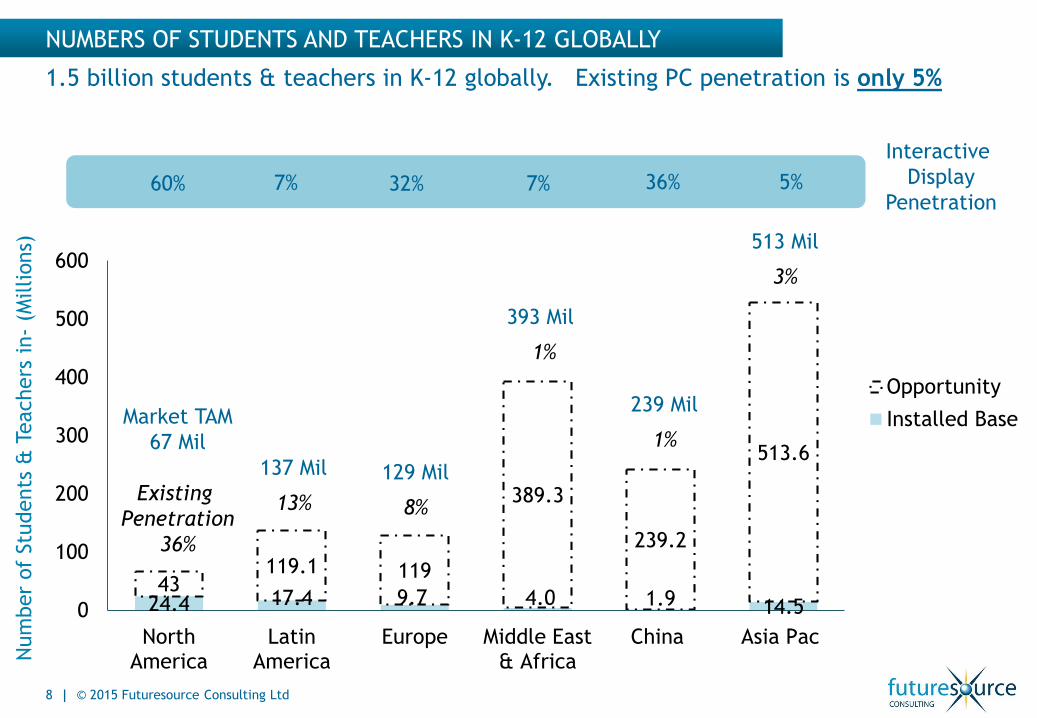

Total

market

24.4 17.4 9.7 4.0 1.9 14.543

119.1 119

389.3

239.2

513.6

0

100

200

300

400

500

600

NorthAmerica

LatinAmerica

Europe Middle East& Africa

China Asia Pac

Opportunity

Installed Base

Num

ber

of

Stu

dents

& T

eachers

in-

(Millions)

1.5 billion students & teachers in K-12 globally. Existing PC penetration is only 5%

NUMBERS OF STUDENTS AND TEACHERS IN K-12 GLOBALLY

8 | © 2015 Futuresource Consulting Ltd

Market TAM

67 Mil

Existing

Penetration

36%

137 Mil

13%

129 Mil

8%

393 Mil

1%

239 Mil

1%

513 Mil

3%

60% 7% 36%32% 7% 5%

Interactive

Display

Penetration

MOBILE PC/TABLET SHIPMENTS INTO K-12 INSTITUTIONS

9 | © 2015 Futuresource Consulting Ltd

5.5 6.99.6 10.6 11.5

4.45.8

6.47.4 7.4

3.4

3.8

4.95.6

7.0

4.0

5.9

5.7

6.16.2

0

10

20

30

40

2012 2013 2014 2015 2016

Volu

mes,

millions

North America South America EMEA Asia-Pacific

32.2

17.3

22.5

26.6

29.8

26.6 Million Devices Sold In 2014, Representing A 15% Growth

# Mobile PCs includes Notebooks, Netbooks, Chromebooks and Tablets purchased by institutions (not including ‘Bring Your Own’)

10 | © 2015 Futuresource Consulting Ltd

COUNTRIES WITH LARGE SCALE 1:1 PROJECTS IN 2014

France

Mexico

Nigeria Saudi

Arabia Brazil

India

Argentina

AustraliaBolivia

Chile

Colombia

Uruguay

Italy

Turkmenistan

Georgia

Russia

Spain

Turkey

USA

UAE

Thailand

Venezuela

Canada

11 | © 2015 Futuresource Consulting Ltd

COUNTRIES WITH EXPECTED & POTENTIAL NEW PROJECTS IN 2015

South

Africa

Japan

France

Mexico

Ecuador

Qatar Saudi Arabia

Peru

Brazil

India

Argentina

Bolivia

Chile

Colombia

Costa

Rica

Djibouti

Uruguay

El Salvador

Honduras

Italy

Turkmenistan

Georgia

Spain

KenyaMauritius

Turkey

USA

ThailandVenezuela

Tanzania

Nigeria

Uganda

Suriname

Canada

Panama

Chromebook yet to gain Significant Traction Outside of North America

38%32%

24%19%

50%56%

40%31%

67%

51%

16% 42%2%

4%

3%

2%

2% 62%

36%

17% 2%

22%

6%

4%44%35%

14%

45%

29%37% 38%

63%

19%

55%

0%

20%

40%

60%

80%

100%

Tablet

Netbook

Chromebook

Notebook

Europe Asia-PacificSouth AmericaNorth

America

FORM FACTOR MARKET SHARE BY REGION – SHIPMENT BASED

Middle

East

& Africa

2013 2014 2013 2014 2013 2014 2013 2014 2013 2014

12 | © 2015 Futuresource Consulting Ltd

# Mobile PCs includes Notebooks, Netbooks, Chromebooks and Tablets purchased by k-12 institutions (not including ‘Bring Your Own’)

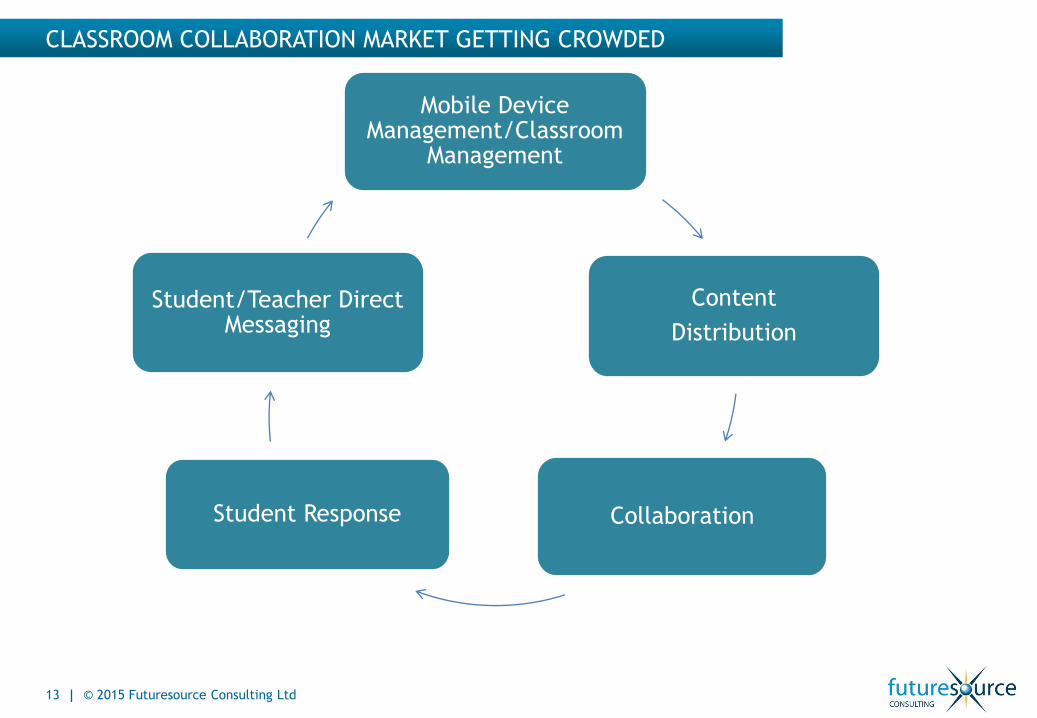

CLASSROOM COLLABORATION MARKET GETTING CROWDED

13 | © 2015 Futuresource Consulting Ltd

Mobile Device Management/Classroom

Management

Content

Distribution

CollaborationStudent Response

Student/Teacher Direct Messaging

14 | © 2015 Futuresource Consulting Ltd

MANY DIFFERENT SUPPLIERS APPROACHING FROM DIFFERENT ANGLES

Mobile Device

Management

Classroom

ManagementInteractive

Display

Software

Cloud

Based

Productivity

2 Way

Content

Sharing

MDM/Classroom

Management

Content

DistributionCollaboration

Student

Response

Vendor &

Background

Content

Distribution

Content

Mirroring

Q & A

Student/Teacher

Direct Messaging

Instant

Messaging

Adaptive

Q & A

Full

Communicat

ion

IT Based Classroom

Management Specialists

Voting Specialists

Publishers

Productivity Providers

Standard offering

Some providers

offering

Collaboration Focused

Software Houses

Interactive Display

Specialists

| Futuresource Introduction

| Global Spend On Education Hardware in 2014

| Interactive Display Developments

| Computing in K-12 Developments

| Focus on Classroom Collaboration

| Questions

• Futuresource Universe Of Education Spend Report

15 | © 2015 Futuresource Consulting Ltd

AGENDA

16 | © 2015 Futuresource Consulting Ltd

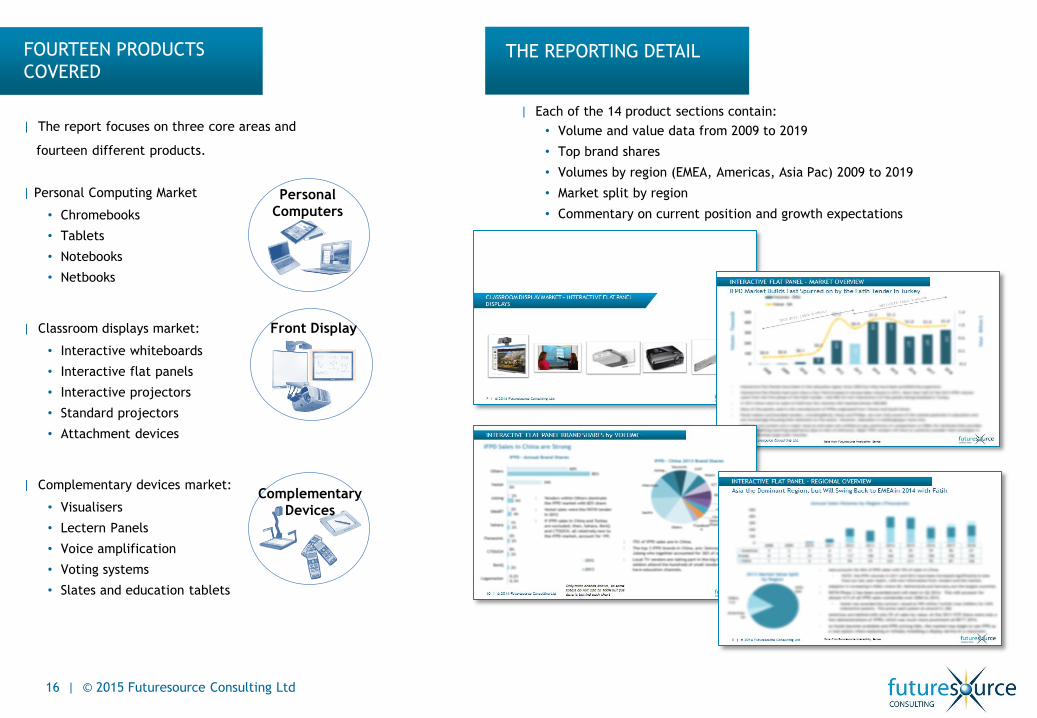

FOURTEEN PRODUCTS

COVERED

| Each of the 14 product sections contain:

• Volume and value data from 2009 to 2019

• Top brand shares

• Volumes by region (EMEA, Americas, Asia Pac) 2009 to 2019

• Market split by region

• Commentary on current position and growth expectations

| Personal Computing Market

• Chromebooks

• Tablets

• Notebooks

• Netbooks

| Classroom displays market:

• Interactive whiteboards

• Interactive flat panels

• Interactive projectors

• Standard projectors

• Attachment devices

| Complementary devices market:

• Visualisers

• Lectern Panels

• Voice amplification

• Voting systems

• Slates and education tablets

| The report focuses on three core areas and

fourteen different products.

THE REPORTING DETAIL

Complementary

Devices

Front Display

Personal

Computers

17 | © 2015 Futuresource Consulting Ltd

ANALYST OVERVIEW

PRESENTATION

| The value-added PPT presentation allows our analysts to explore

trends and hot topics in greater detail adding insight and meaning to

the raw data.

| The report contents will include:

• Report Background, Objectives and Methodology

• Global Classroom Technology Spend Overview

• Category volume, value and share

• Spend by region, product and category

• Key developments impacting the EdTech market

• Data privacy issues

• The rise of Chromebooks

• The drive to Vocational learning

• Coding

• Classroom collaboration

• Who is offering what?

• Analysis of trends in classroom collaboration

• Global Education Decision-Making and Funding

• How decision making works

• Four typical processes and mapping key countries to

these

• Tenders and Large-Scale Nationwide Investments

• Analysis of large scale EdTech deployments taking place

as well as new projects developing. Over 30 countries

covered.

About Futuresource Consulting

Futuresource Consulting is a specialist research and knowledge-based consulting

company with a heritage stretching back to the 1980s.

Its insight and global market coverage are based on informed regional expertise,

ensuring its portfolio of world-class clients is fully supported in research, analysis,

strategic planning and decision making.

| Consumer Electronics

| Print & Imaging

| Entertainment Content & Distribution

| Education Technology

| Optical Disc Manufacturing

| Broadcast Equipment

| Professional Displays talk to us…

Futuresource Consulting

+44 (0)1582 500 100

www.futuresource-consulting.com

18 | © 2015 Futuresource Consulting Ltd