5

Global Financial Outlook José Viñals Financial Counsellor & Director of Monetary and Capital Markets IMF IFSWF 6 th Annual Meeting, November 20, 2014

Global Financial Outlook

José Viñals Financial Counsellor

&

Director of Monetary and Capital Markets

IMF

IFSWF 6th Annual Meeting, November 20, 2014

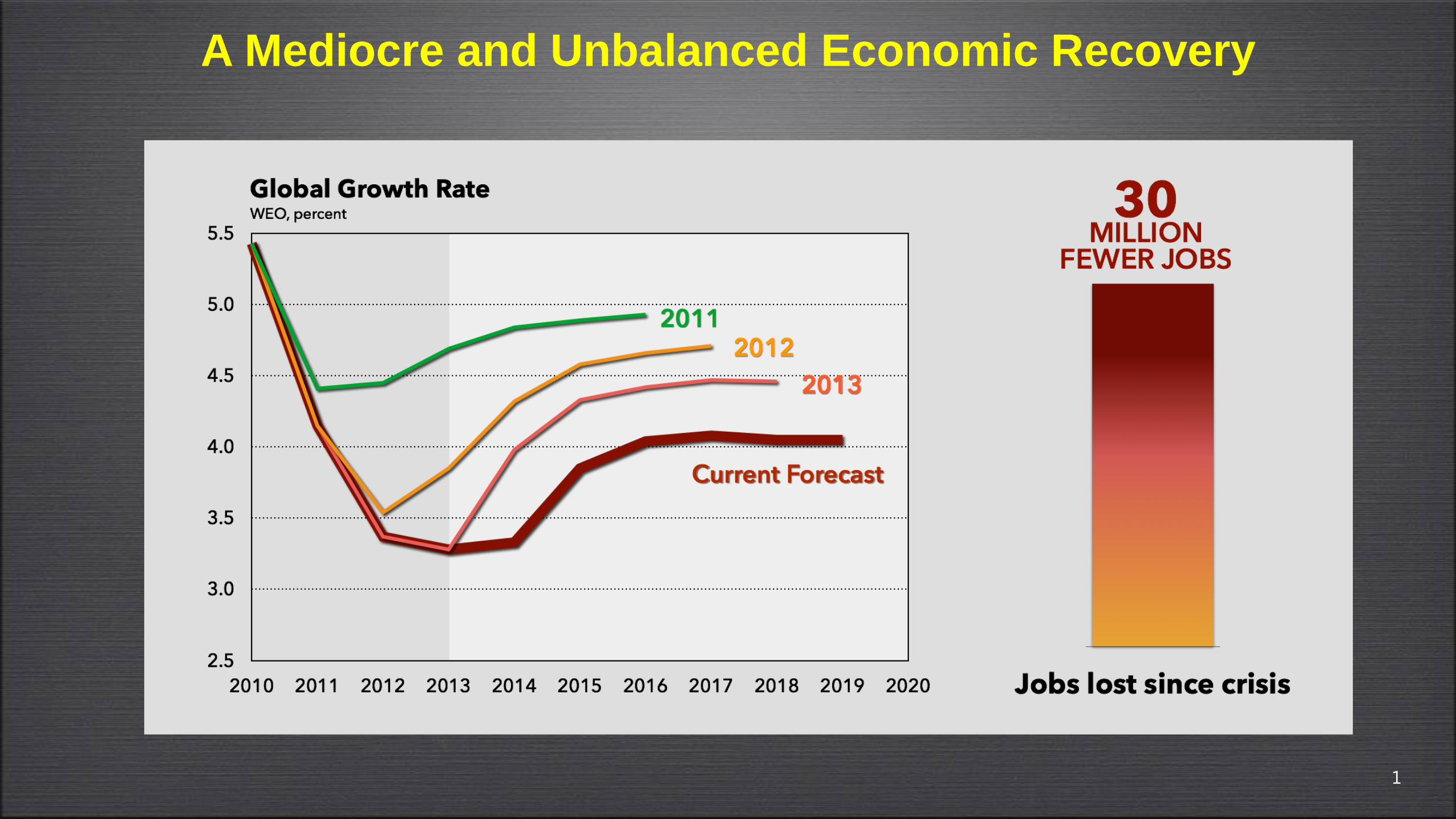

A Mediocre and Unbalanced Economic Recovery

1

Too little economic risk-taking and too much financial risk-taking

2

Banks Safer…

Advanced Economies (percent of sample assets)

0

10

20

30

40

50

60

70

80

90

100

Dec-08 Jun-14

Resolution & Recap

Significant business

model transition

needed

Best positioned to

support the

recovery

58%

Bank Capital Ratio > 8%

38%

4%

… Many Not Strong Enough

to Support Recovery

3

Liquidity Illusion Today – Liquidity Trap Tomorrow?

…But Deteriorating Structural Market Liquidity… Ample Monetary Liquidity…

0

2

4

6

8

10

2007 2008 2009 2010 2011 2012 2013 2014

(USD tn)

Central Bank Balance Sheets

FED ECB BOJ BOE* SNB

* Bank of England data unavailable before 2006 due to definitional changes on

the BoE’s balance sheet items

11.0

11.5

12.0

12.5

13.0

13.5

2007 2008 2009 2010 2011 2012 2013

Size of Trades (> 5mn; 6-month average; investment grade)

(USD mn)

4