25

Global Financial Stability Outlook José Viñals Financial Counsellor and Director of the Monetary and Capital Markets Department PIIE, October 21, 2015

Global Financial Stability

Outlook

José Viñals

Financial Counsellor and Director of the Monetary and Capital Markets Department

PIIE, October 21, 2015

Financial

Stability Not

Yet Assured

Financial stability in

advanced economies

improved…

…but risks continue

to rotate to emerging

markets

Three Global

Transitions

• China rebalancing

• U.S. monetary

normalization

• Unraveling of the

commodity cycle

1

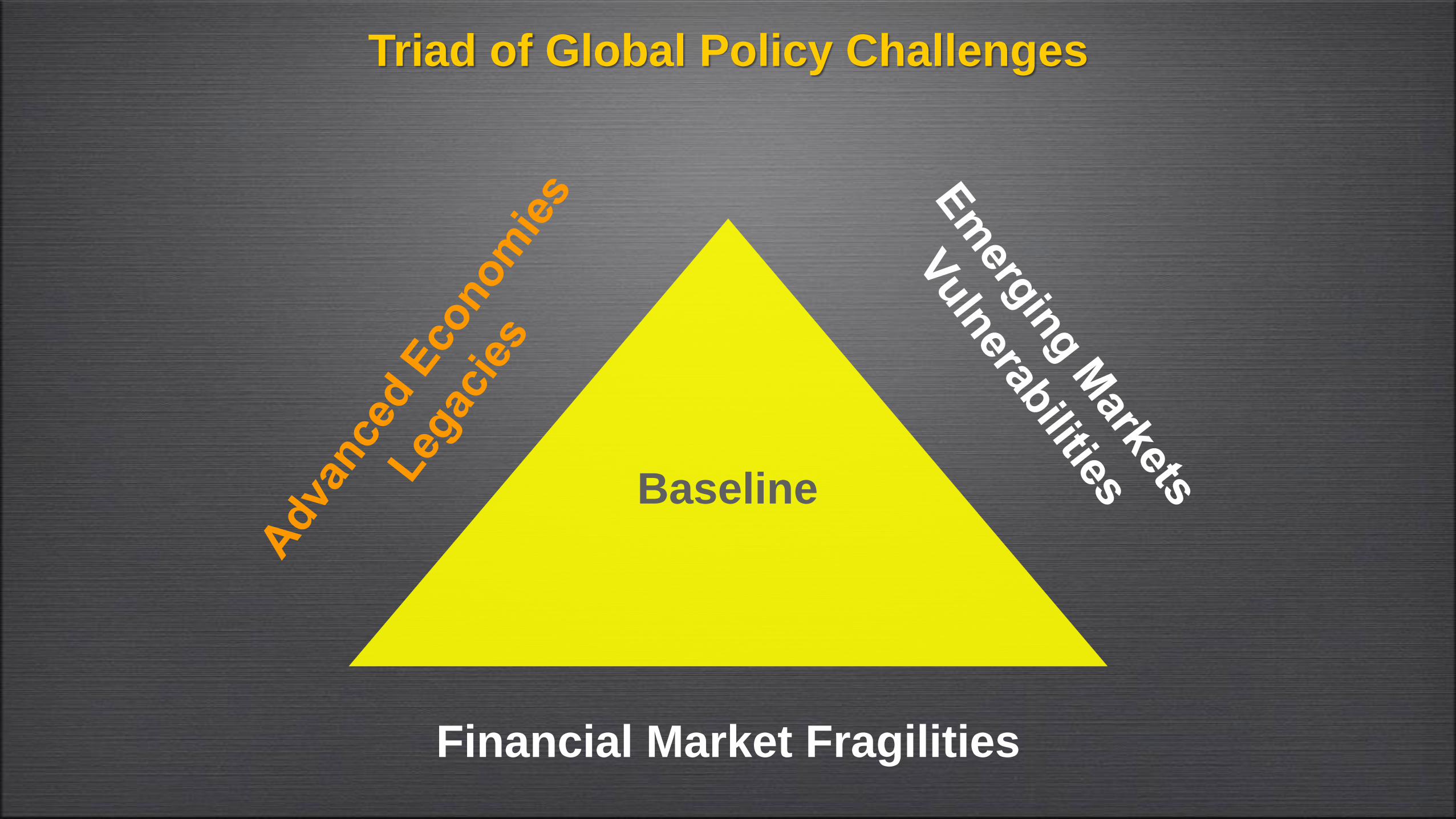

Global Financial Stability Needs Urgent Policy Upgrade

Policy

Upgrade

Needed

Collective effort to

enhance confidence

and build resilience

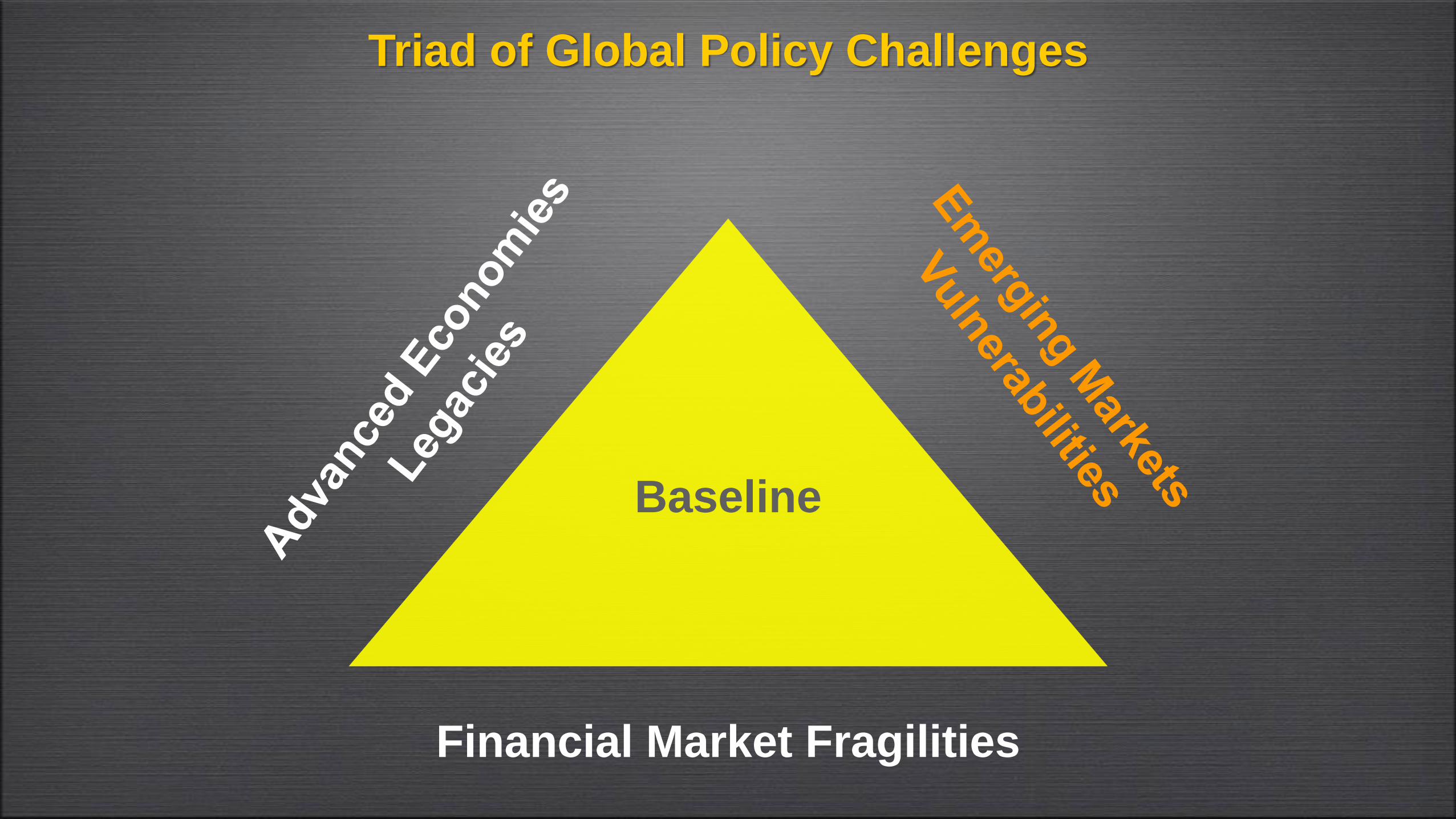

Triad of Global

Policy

Challenges

• Advanced economy

legacies

• Emerging market

vulnerabilities

• Financial market

fragilities

Financial Stability Overview

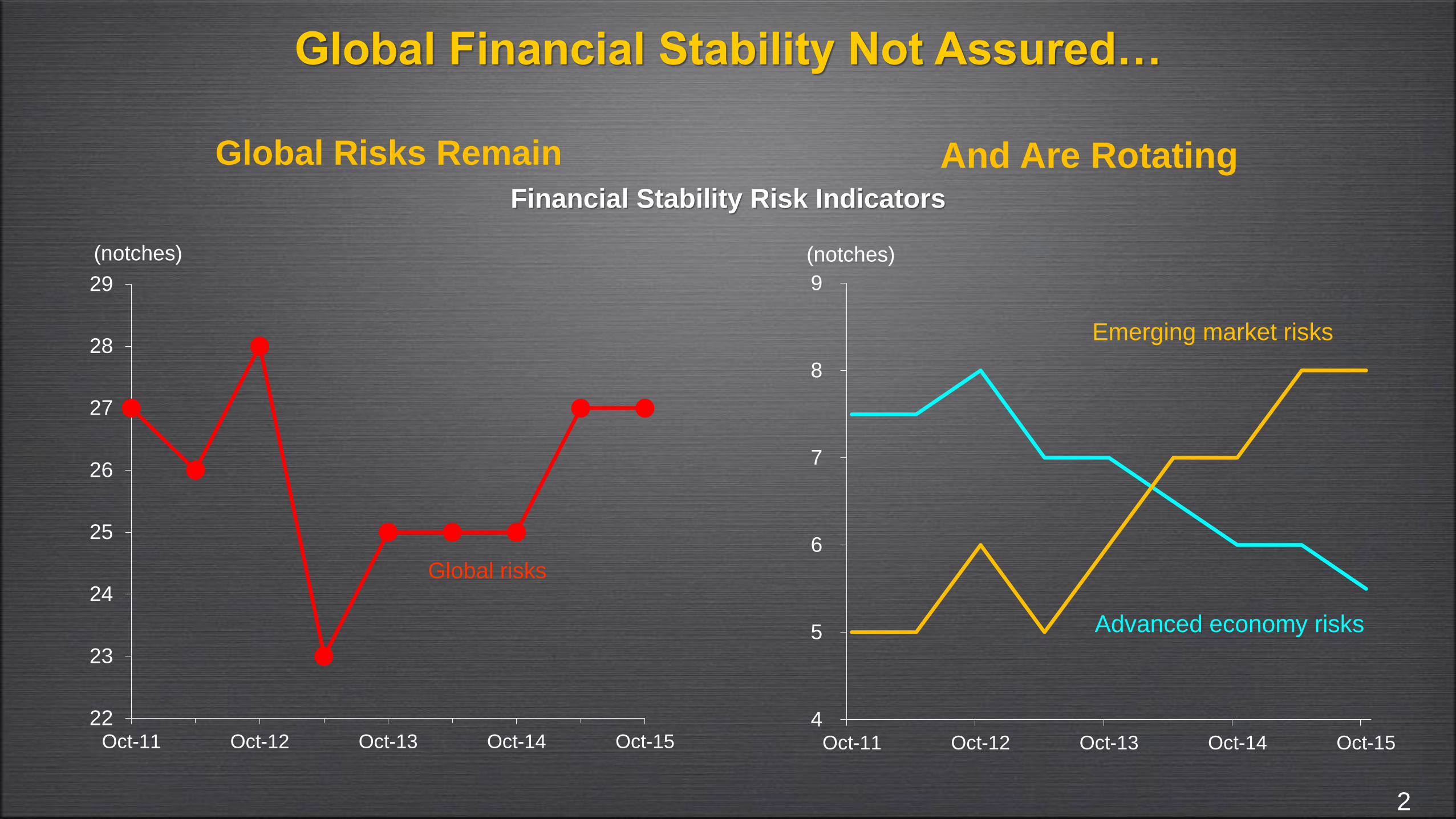

Global Financial Stability Not Assured…

And Are Rotating

22

23

24

25

26

27

28

29

Oct-11 Oct-12 Oct-13 Oct-14 Oct-15

(notches)

Global risks

Financial Stability Risk Indicators

2

Global Risks Remain

4

5

6

7

8

9

Oct-11 Oct-12 Oct-13 Oct-14 Oct-15

Advanced economy risks

Emerging market risks

(notches)

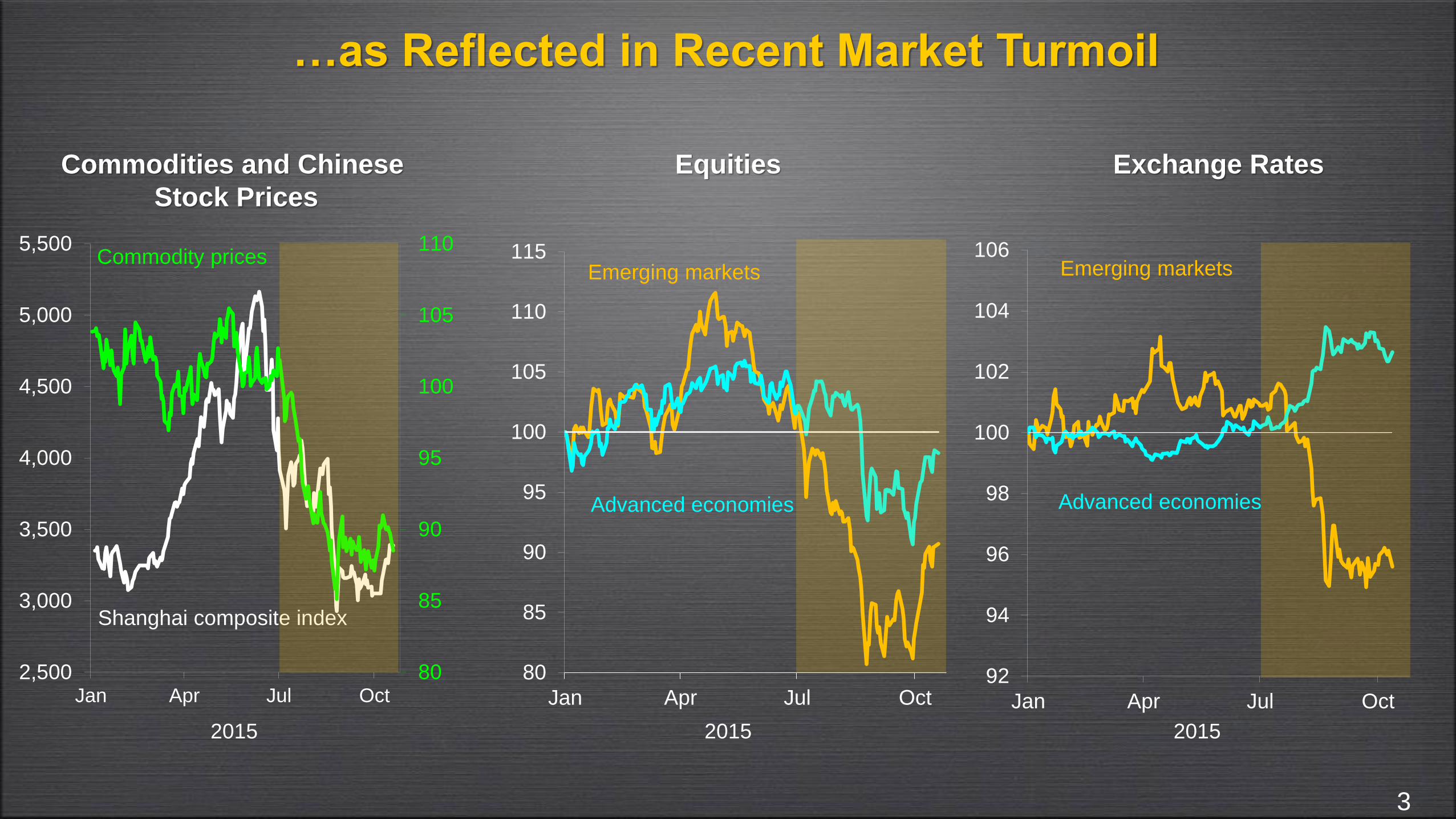

…as Reflected in Recent Market Turmoil

Commodities and Chinese

Stock Prices

Equities

2015 2015 2015

Exchange Rates

3

80

85

90

95

100

105

110

2,500

3,000

3,500

4,000

4,500

5,000

5,500

Jan Apr Jul Oct

Commodity prices

Shanghai composite index

80

85

90

95

100

105

110

115

Jan Apr Jul Oct

Emerging markets

Advanced economies

92

94

96

98

100

102

104

106

Jan Apr Jul Oct

Emerging markets

Advanced economies

Global Policy Challenges

Triad of Global Policy Challenges

Financial Market Fragilities

Baseline:

Financial Stability

Not Yet Assured

4

Triad of Global Policy Challenges

Financial Market Fragilities

Baseline

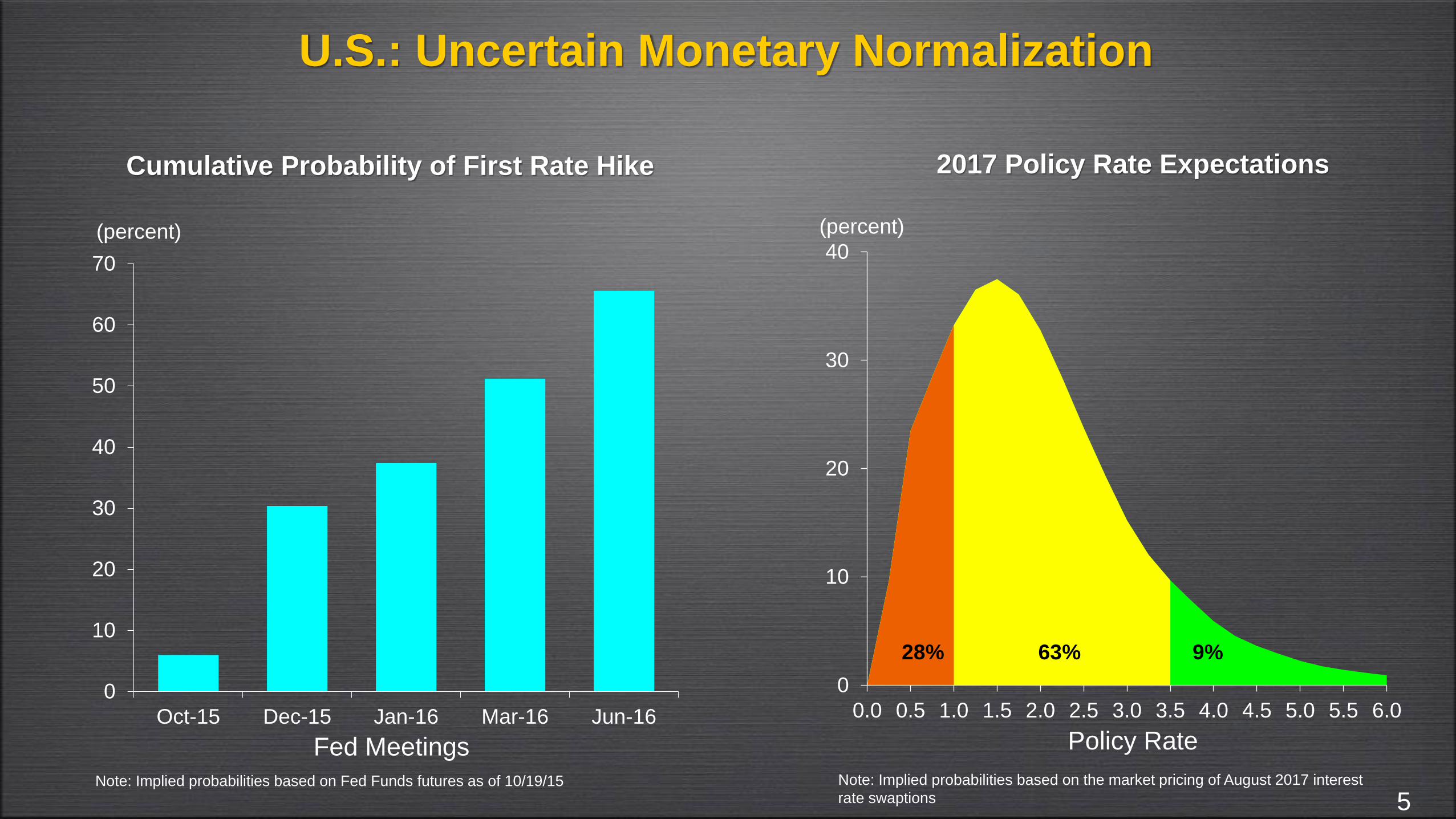

U.S.: Uncertain Monetary Normalization

Cumulative Probability of First Rate Hike 2017 Policy Rate Expectations

Policy Rate

Note: Implied probabilities based on Fed Funds futures as of 10/19/15 Note: Implied probabilities based on the market pricing of August 2017 interest

rate swaptions

Fed Meetings

5

0

10

20

30

40

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0

(percent)

28% 63% 9%

0

10

20

30

40

50

60

70

Oct-15 Dec-15 Jan-16 Mar-16 Jun-16

(percent)

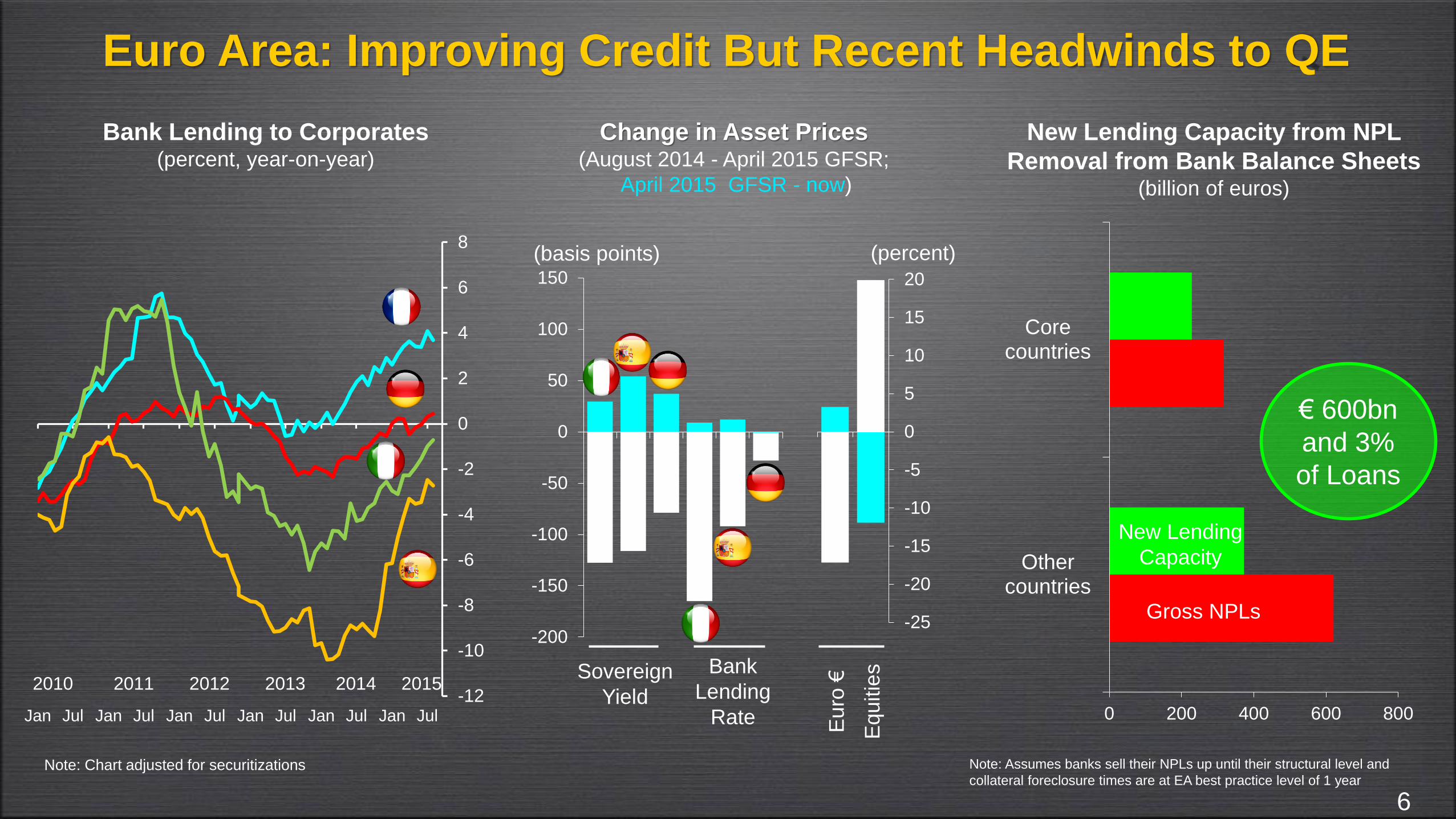

Euro Area: Improving Credit But Recent Headwinds to QE

Bank Lending to Corporates(percent, year-on-year)

New Lending Capacity from NPL

Removal from Bank Balance Sheets(billion of euros)

6

Note: Assumes banks sell their NPLs up until their structural level and

collateral foreclosure times are at EA best practice level of 1 yearNote: Chart adjusted for securitizations

€ 600bn

and 3%

of Loans

Change in Asset Prices(August 2014 - April 2015 GFSR;

April 2015 GFSR - now)

Sovereign

Yield

Bank

Lending

Rate

Equitie

s

Euro

€

-12

-10

-8

-6

-4

-2

0

2

4

6

8

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul

2010 2011 2012 2013 2014 2015

0 200 400 600 800

Othercountries

Corecountries

Gross NPLs

New Lending

Capacity

-200

-150

-100

-50

0

50

100

150

(basis points)

-25

-20

-15

-10

-5

0

5

10

15

20

(percent)

Triad of Global Policy Challenges

Financial Market Fragilities

Baseline

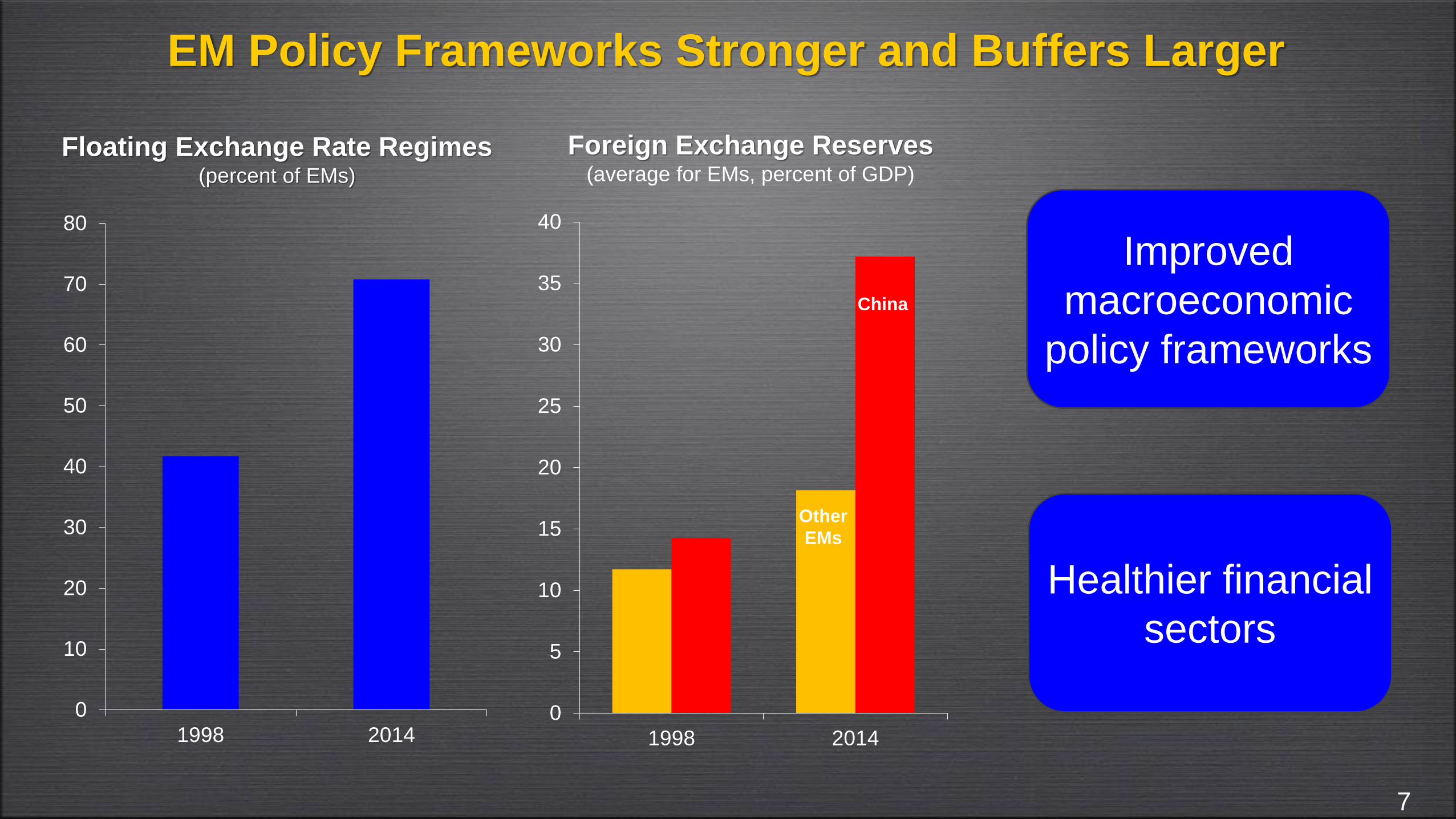

EM Policy Frameworks Stronger and Buffers Larger

Foreign Exchange Reserves(average for EMs, percent of GDP)

Floating Exchange Rate Regimes (percent of EMs)

7

Improved

macroeconomic

policy frameworks

Healthier financial

sectors

0

10

20

30

40

50

60

70

80

1998 20140

5

10

15

20

25

30

35

40

1998 2014

China

Other

EMs

Many EMs in Late Stages of the Credit Cycle

Credit Excesses(deviation of credit-to-GDP ratio

from trend, percent)I. EXPANSIONIV. REPAIR

III. DOWNTURN II. PEAK

-5

0

5

10

15

20

25

Chin

a

Thaila

nd

Turk

ey

Bra

zil

Indon

esia

Mala

ysia

Saud

i A

rabia

Mexic

o

Russia

Arg

entina

Pola

nd

India

South

Afr

ica

$3 trillion

AEs

EMs

Note: Credit gap estimates according to the Basel III

methodology for the countercyclical capital buffer

New Bank NPL Formation (net of recovery, percent of RWA)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2014201220102008

Emerging

markets

Advanced

economies

8

Credit Cycle

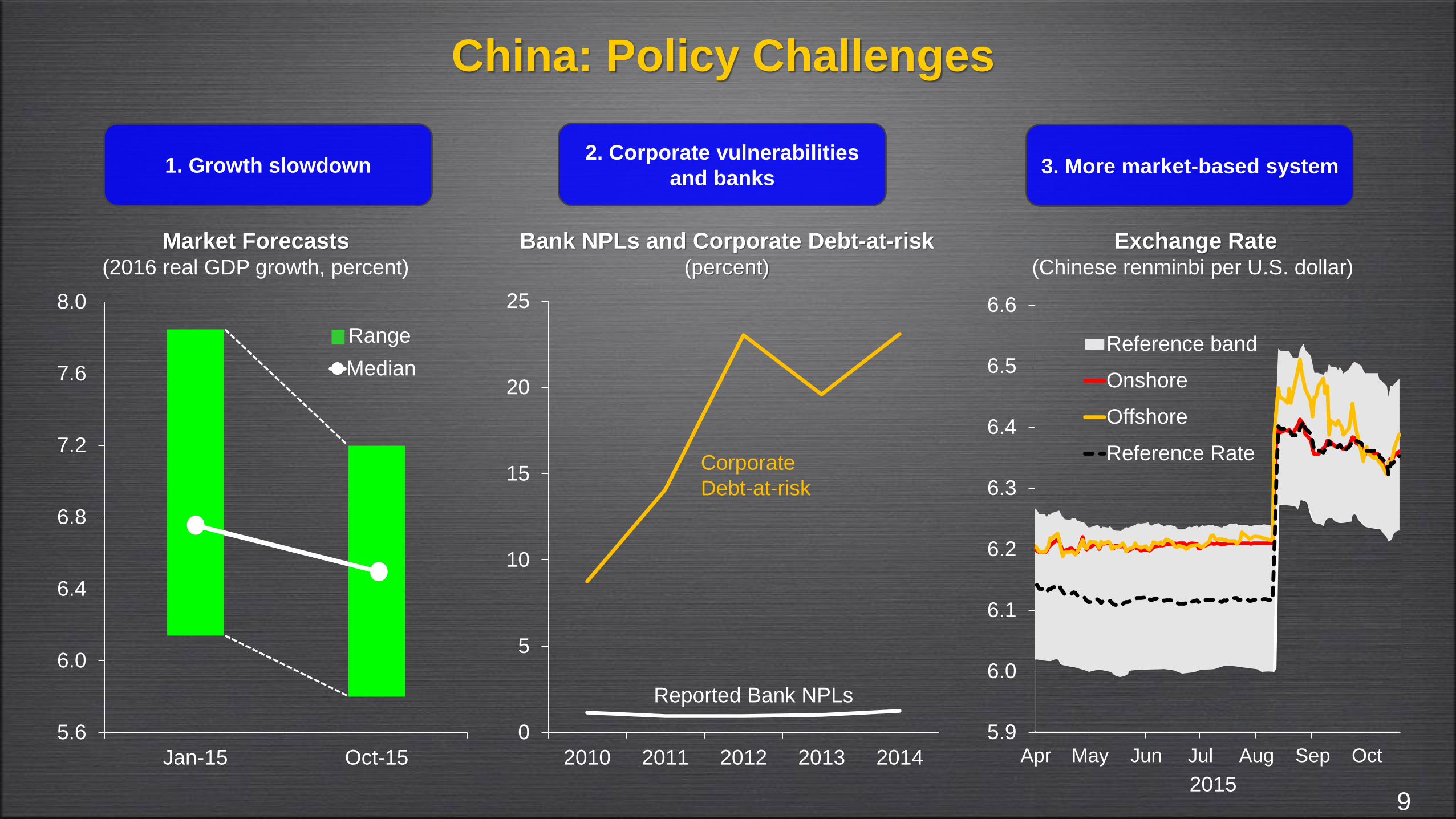

China: Policy Challenges

3. More market-based system

Exchange Rate(Chinese renminbi per U.S. dollar)

0

5

10

15

20

25

2010 2011 2012 2013 2014

Corporate

Debt-at-risk

Reported Bank NPLs

Bank NPLs and Corporate Debt-at-risk(percent)

92015

2. Corporate vulnerabilities

and banks1. Growth slowdown

Market Forecasts (2016 real GDP growth, percent)

5.9

6.0

6.1

6.2

6.3

6.4

6.5

6.6

Apr May Jun Jul Aug Sep Oct

Reference band

Onshore

Offshore

Reference Rate

5.6

6.0

6.4

6.8

7.2

7.6

8.0

Jan-15 Oct-15

Median

Range

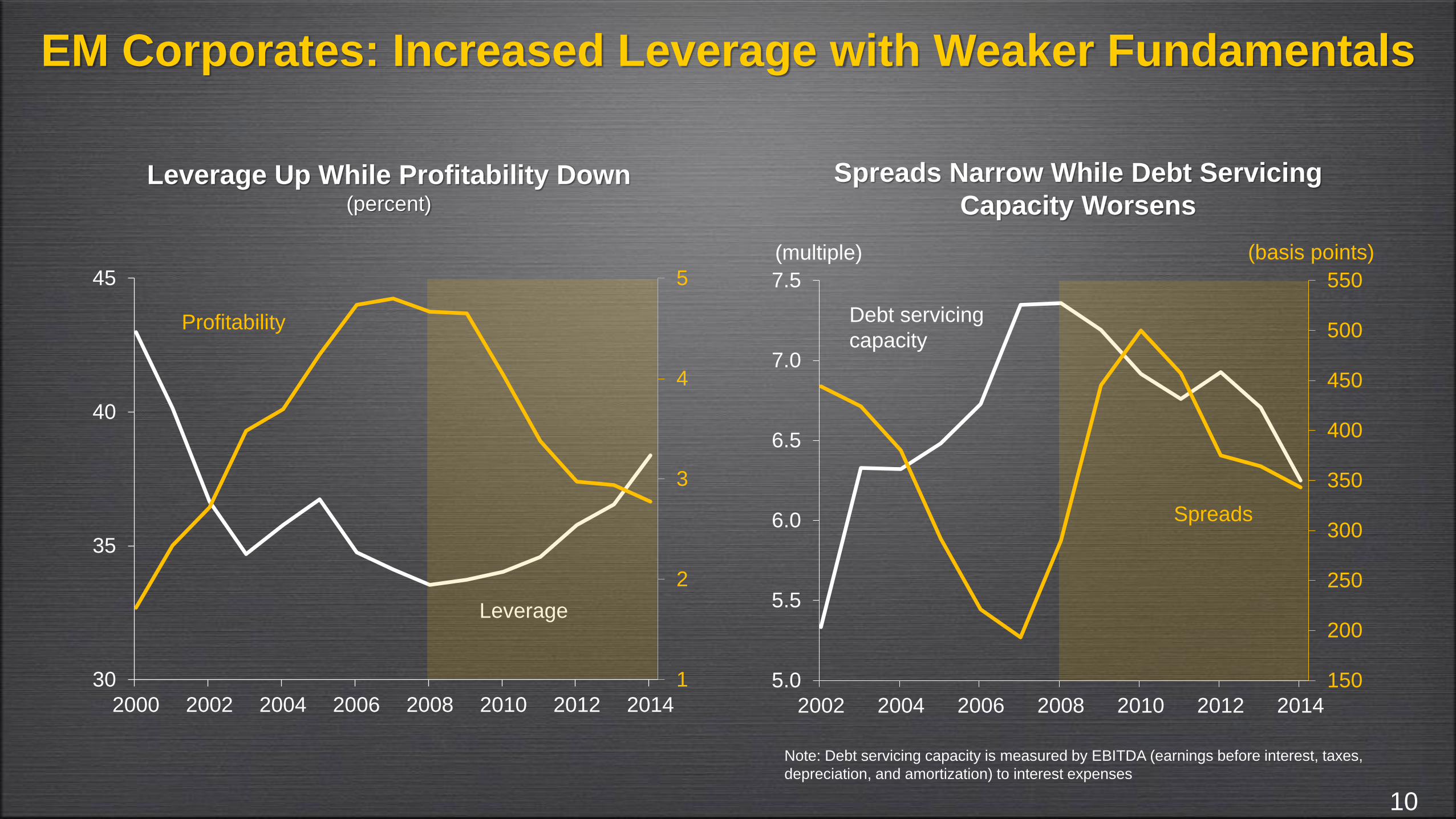

EM Corporates: Increased Leverage with Weaker Fundamentals

Leverage Up While Profitability Down(percent)

Spreads Narrow While Debt Servicing

Capacity Worsens

10

(multiple) (basis points)

Note: Debt servicing capacity is measured by EBITDA (earnings before interest, taxes,

depreciation, and amortization) to interest expenses

1

2

3

4

5

30

35

40

45

2000 2002 2004 2006 2008 2010 2012 2014

Profitability

Leverage

150

200

250

300

350

400

450

500

550

5.0

5.5

6.0

6.5

7.0

7.5

2002 2004 2006 2008 2010 2012 2014

Debt servicing

capacity

Spreads

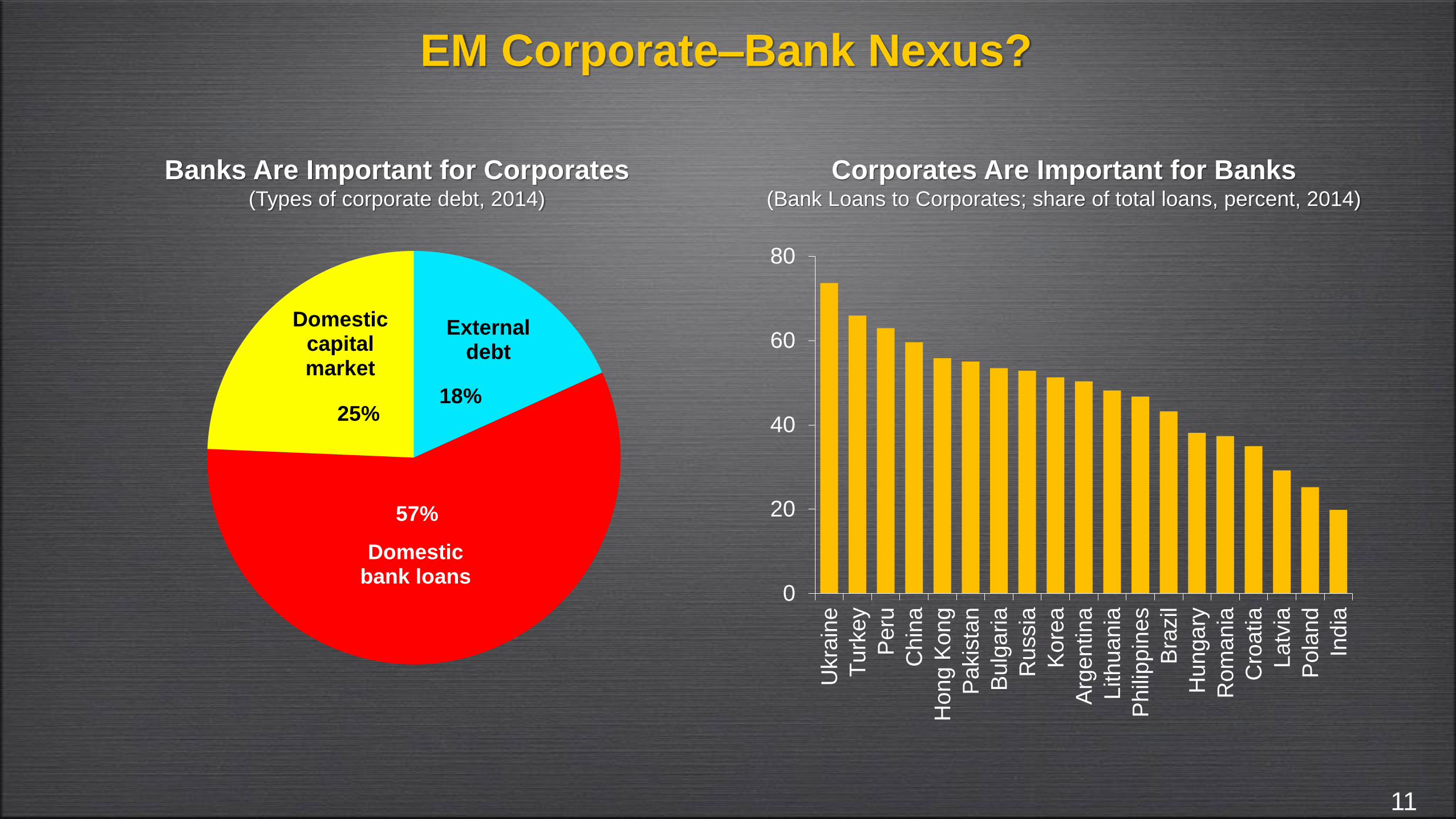

EM Corporate–Bank Nexus?

Corporates Are Important for Banks(Bank Loans to Corporates; share of total loans, percent, 2014)

Banks Are Important for Corporates(Types of corporate debt, 2014)

External debt

Domestic bank loans

Domestic capital market

57%

18%25%

11

0

20

40

60

80

Ukra

ine

Tu

rke

y

Pe

ru

Ch

ina

Hong K

ong

Pa

kis

tan

Bu

lgaria

Russia

Kore

a

Arg

entina

Lithuania

Phili

ppin

es

Bra

zil

Hungary

Ro

ma

nia

Cro

atia

Latv

ia

Po

land

India

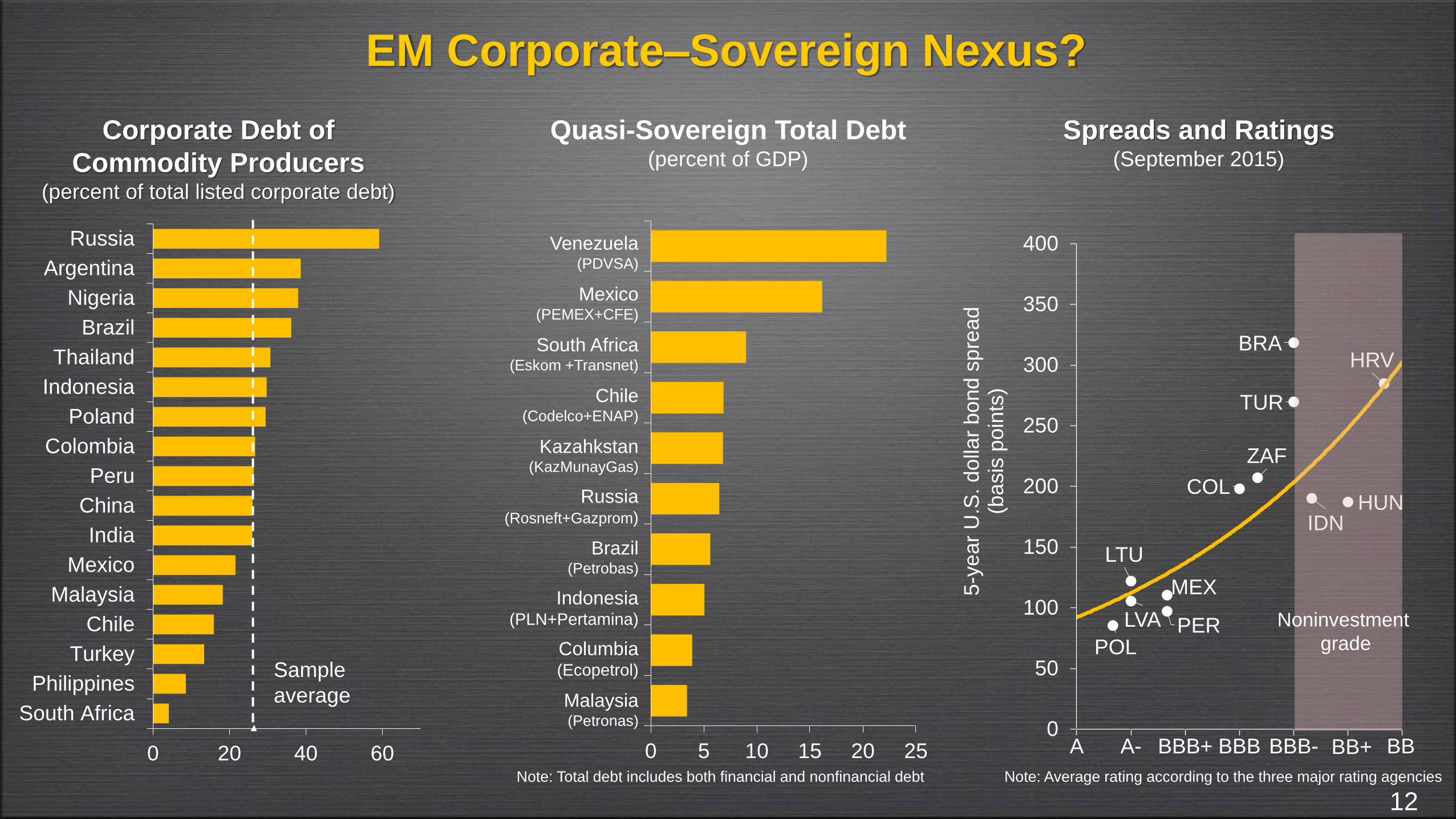

EM Corporate–Sovereign Nexus?

Spreads and Ratings(September 2015)

Note: Average rating according to the three major rating agencies

12

Quasi-Sovereign Total Debt(percent of GDP)

Corporate Debt of

Commodity Producers(percent of total listed corporate debt)

0 20 40 60

South Africa

Philippines

Turkey

Chile

Malaysia

Mexico

India

China

Peru

Colombia

Poland

Indonesia

Thailand

Brazil

Nigeria

Argentina

Russia

Sample

average

0 5 10 15 20 25

Venezuela (PDVSA)

Mexico(PEMEX+CFE)

South Africa(Eskom +Transnet)

Chile(Codelco+ENAP)

Kazahkstan(KazMunayGas)

Russia(Rosneft+Gazprom)

Brazil(Petrobas)

Indonesia(PLN+Pertamina)

Columbia(Ecopetrol)

Malaysia(Petronas)

Note: Total debt includes both financial and nonfinancial debt

BRA

COL

MEX

PER POL

HUN

TUR

ZAF

HRV

LTU

LVA

IDN

A A- BBB+ BBB BBB- BB+ BB0

50

100

150

200

250

300

350

400

5-y

ear

U.S

. do

llar

bo

nd

sp

read

(b

asis

po

ints

)

Noninvestment

grade

Triad of Global Policy Challenges

Financial Market Fragilities

Baseline

Amplifiers of Volatility: Market Illiquidity and Leverage

Note: Refers to regulated bond funds domiciled in Europe and the

U.S.

Bond Funds

Hidden Leverage(trillions of U.S. dollars)

Reduced Dealer Market-Making(trillions of U.S. dollars)

Lower Liquidity Raises Volatility(millions of U.S. dollars; index)

40

60

80

100

120

140

160

180

200

220

240

0 1,000 2,000 3,000 4,000

Hig

her

vola

tilit

y

Lower market depth

Latest 12 months

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2010 2014

-22%

13

0.0

0.5

1.0

1.5

2.0

2.5

$1.5

tn

$0.6

tn

Derivative

exposures

Assets under

management

$2.1

tn

Note: Refers to U.S. banks

Putting It All Together:

Global Spillovers and Scenarios for Financial Stability

14

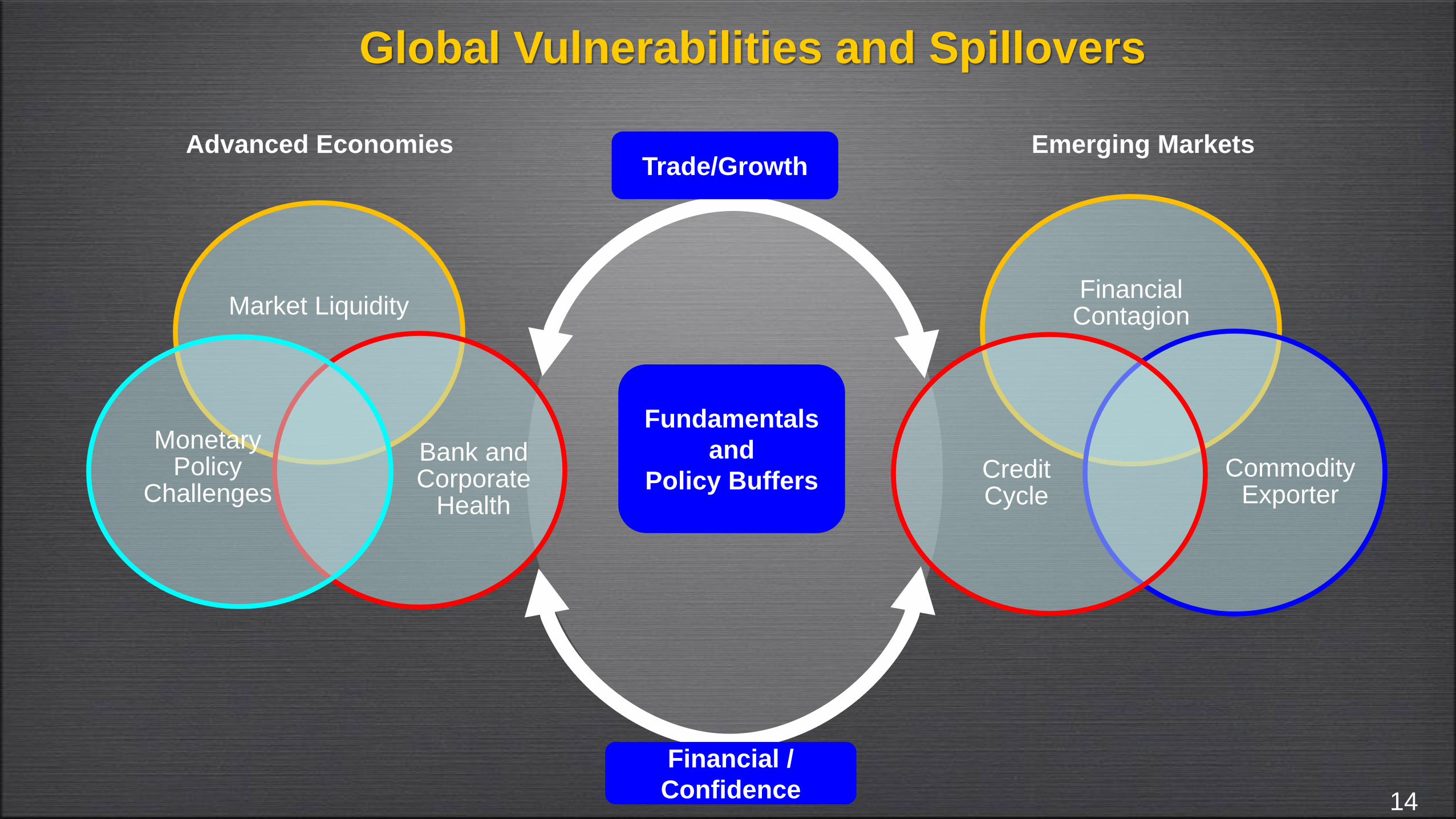

Financial Contagion

CommodityExporter

Credit Cycle

PHL

COL

CHN

POL

TUR

ARG CHL MYS SAUIND

BRA

MEXZAF

THA

IDN

RUS

Global Vulnerabilities and SpilloversEmerging Markets

Market Liquidity

Bank and Corporate

Health

Monetary Policy

Challenges

14

Financial Contagion

Commodity Exporter

Credit Cycle

Advanced Economies Emerging MarketsTrade/Growth

Financial /

Confidence

Fundamentals

and

Policy Buffers

Global Vulnerabilities and Spillovers

Three Scenarios for Financial Stability

15

Disruptive

shifts in asset

markets

+0.4%

-2.4%

2.8%

Successful

normalization

Financial stability

not assuredBaseline

Global

output

Smooth

decompression

Abrupt

decompression

Risk premia

compressed

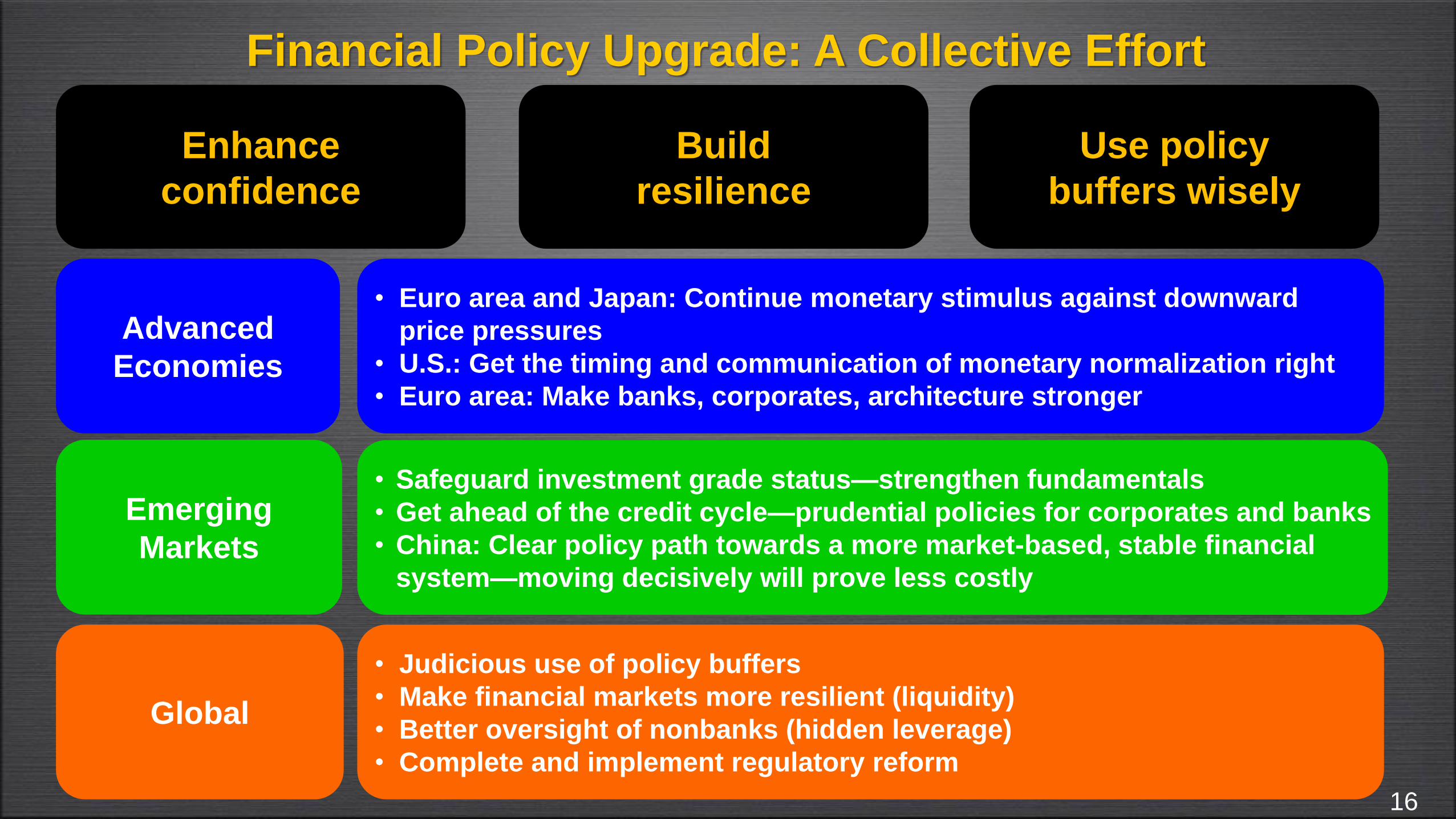

Financial Policy Upgrade: A Collective Effort

16

Build

resilience

Use policy

buffers wisely

Enhance

confidence

Financial Policy Upgrade: A Collective Effort

Advanced

Economies

• Euro area and Japan: Continue monetary stimulus against downward

price pressures

• U.S.: Get the timing and communication of monetary normalization right

• Euro area: Make banks, corporates, architecture stronger

Emerging

Markets

• Safeguard investment grade status—strengthen fundamentals

• Get ahead of the credit cycle—prudential policies for corporates and banks

• China: Clear policy path towards a more market-based, stable financial

system—moving decisively will prove less costly

Global

• Judicious use of policy buffers

• Make financial markets more resilient (liquidity)

• Better oversight of nonbanks (hidden leverage)

• Complete and implement regulatory reform

16

Enhance

confidence

Build

resilience

Use policy

buffers wisely