About This Industry ................................. 2 Industry Definition ......................................... 2 Main Activities ............................................... 2 Similar Industries .......................................... 2 Additional Resources .................................... 3

Industry Performance .............................. 4 Executive Summary ...................................... 4 Key External Drivers ..................................... 4 Current Performance .................................... 5 Industry Outlook............................................ 7 Industry Life Cycle ........................................ 9

Products & Markets ................................. 10 Supply Chain ................................................ 10 Products & Services ..................................... 11 Demand Determinants .................................. 13 Major Markets ............................................... 14 International Trade........................................ 15 Business Locations ....................................... 16

Key Success Factors ................................... 18 Cost Structure Benchmarks ......................... 19 Basis of Competition .................................... 21 Barriers to Entry ........................................... 22 Industry Globalization .................................. 23

Major Companies .................................... 24 Hilton Worldwide .......................................... 24 Marriott International, Inc. ............................ 25 Other Players ............................................... 26

Operating Conditions .............................. 28 Capital Intensity ........................................... 28 Technology & Systems ................................ 28 Revenue Volatility ........................................ 29 Regulation & Policy ...................................... 29 Industry Assistance ...................................... 29

Key Statistics ........................................... 30 Industry Data ................................................ 30 Annual Change ............................................ 30 Key Ratios .................................................... 31 Jargon .......................................................... 31

Global Hotels & Resorts

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 2

About This Industry

Industry Definition

Firms in this industry include hotel and resort accommodations, with private or shared facilities, and with or without meal services and restaurants attached. This includes both chain and franchised operators; however, it excludes all other forms of accommodation, such as motels; caravan parks and camping grounds; youth and backpacker hotels; and bed and breakfast establishments.

Main Activities

The primary activities of this industry are:

Operating holiday resorts

Operating hotels with private facilities The major products and services in this industry are:

Medium-end hotel accommodation

High-end hotel accommodation

Low-end hotel accommodation

Resort accommodation

Similar Industries

H4831-GL - Global Airlines Passenger airlines provide air transportation of passengers over scheduled or non-scheduled routes, domestically and internationally. H4911-GL - Global Travel Agency Services This industry is engaged in tour wholesaling or acting as retail travel agents in selling travel or tours to the general public and commercial clients. Q8721-GL - Global Casinos & Online Gambling Operators in this industry operate legal casino gaming and legal online gaming. X9001-GL - Global Tourism Companies in this industry are involved in international travel services.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 3

Additional Resources

For additional information on this industry: www.lodgingmagazine.com Lodging Magazine www.htrends.com Hospitality Trends www.4hoteliers.com 4 Hoteliers www.unwto.org World Tourism Organization

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 4

Industry Performance

Executive Summary

The Global Hotels and Resorts industry is recovering from the recent economic downturn, which led to decreased demand for all forms of travel accommodation. The industry is sensitive to a wide range of economic, social, demographic and geopolitical factors that affect domestic overnight travel within any country, as well as global international travel demand and patterns. With the onset of the global recession, both consumers and businesses became more concerned about their finances and cut back on luxuries, including travel. In 2009, as the global recession deepened and unemployment rose, a decline in the domestic travel rate and a 3.8% fall in international tourism arrivals (according to the United Nations World Tourism Organization) cut into demand for industry services. Since destination hotels and resorts rely heavily on domestic and foreign tourists, the decline in these travel rates hurt the global industry's bottom line. Nevertheless, international tourism arrivals have grown every year since 2010, leading to the industry's revival. 2013 is expected to be the fourth year of consecutive growth in global tourist arrivals, which are anticipated to rise 3.5%. The infusion of tourist dollars is expected to benefit hotels and resorts and increase room rates, causing industry revenue to grow 0.5% in 2013. Over the five years to 2013, industry revenue is expected to increase at an average annual rate of 0.2% to $592.6 billion. Travel spending is projected to increase over the next five years as global economic conditions continue to improve and consumer spending bolsters revenue for global hotels and resorts. International tourist arrivals in emerging economy destinations of Asia, Latin America, Eastern Europe, the Middle East and Africa will grow at double the pace of destinations in developed economies. The biggest growth will be seen in Asia and the Pacific, helping emerging economies surpass developed economies as the favored destination for tourists by 2015. In order to keep up with the aggressive rise in travel rates in these regions, more hotels and resorts will be built, which should increase the proportion of industry revenue generated from these regions and drive industry revenue growth as a whole. Over the five years to 2018, revenue is projected to increase at an average annual rate of 2.2% to $661.5 billion.

Key External Drivers

The key sensitivities affecting the performance of the Global Hotels & Resorts industry include: GDP of the BRIC nations International tourist arrivals in emerging economies (including Brazil, Russia, India and China, otherwise known as BRIC nations) will grow at double the pace of developed economy destinations in upcoming years. The performance of economic conditions at these travel hot spots will help determine the number of tourists they receive, the number of hotels and resorts built and, ultimately, the revenue growth of the Global Hotels and Resorts industry. GDP growth of the BRIC nations is expected to increase in 2014 and is a potential opportunity for the industry. Global consumer sentiment index Changes in consumer sentiment influence decisions that individuals make concerning expenditure on entertainment and traveling, particularly during an economic recession. Consumer sentiment is expected to increase over 2014; however, the index's ongoing volatility is a potential threat for the industry. Global per capita income Changes in per capita disposable income have a direct impact on travel demand and accommodation. As disposable incomes increase in countries around the world, this growth will benefit the Global Hotels and Resorts industry, as consumers will have more funds available for travel and accommodation. Global per capita income is expected to increase in 2014. Global tourist arrivals Trends in international and domestic visitor nights and their length of stay influences demand for

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 5

accommodations. A rise in international and domestic trips positively affects demand for hotels and resorts. The number of global tourist arrivals is expected to increase in 2014.

Current Performance

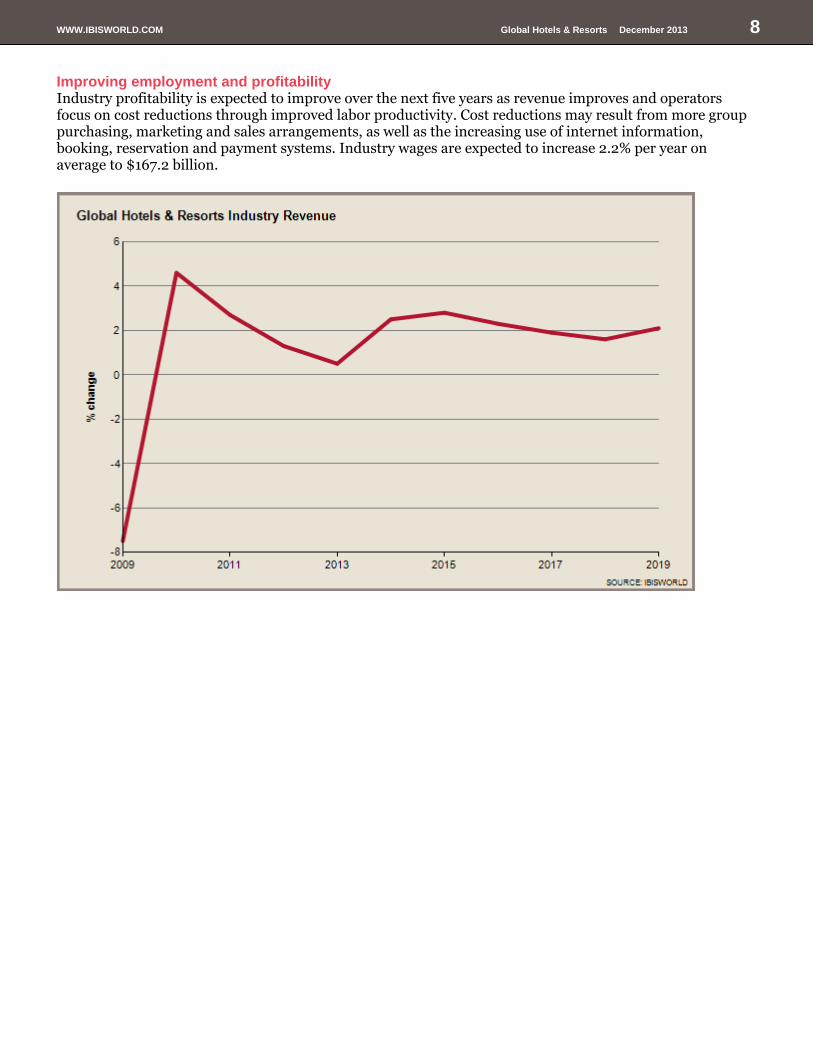

The Global Hotels and Resorts industry has rebounded from a recession-induced decline and experienced positive growth in each of the past four years. The industry's flat annualized growth rate of 0.2% over the five years to 2013 includes a steep decline of 7.5% in 2009 when demand for all forms of travel accommodation waned. In 2009, as the recession deepened and unemployment rose, a 3.8% fall in international tourism arrivals (according to the United Nation World Tourism Organization, or UNWTO) drove demand for the industry down as consumers become concerned about their finances and cut back on luxuries, including travel. Since destination hotels and resorts rely heavily on domestic and foreign tourists, the decline in travel hurt the global industry's bottom line. Nevertheless, international tourism recovered from 2010, growing 6.5% in that year alone and 2.9% per year on average over the five years to 2013. In 2013, the number of international arrivals is forecast to continue moving upwards, increasing 3.5%. The infusion of tourist dollars is expected to benefit hotels and resorts and increase room rates, causing industry revenue to grow 0.5% in 2013 to $592.6 billion. Impact of travel As the economy fell deeper into recession and unemployment rose, consumers became more selective about how they spent disposable income. In 2009, disposable income among OECD (Organization for Economic Cooperation and Development) countries declined 4.0% and recreational activities, including vacations, were some of the first expenditures cut from consumers' budgets. Businesses also cut back on nonessential travel and accommodations due to a decline in corporate profit. These trends began to reverse from 2010 as the economy slowly improved and fears surrounding the state of the global economy subsided. Consumers began taking trips that they delayed during the previous years, increasing demand for hotels and resorts. A steady uptick in consumer confidence has been one of the main reasons for the industry's improvement over the past four years. Regional trends The most notable industry trend over the past five years has been the performance of hotels in different regions, thanks to the contrasting trajectories that travel has taken in emerging economies compared with advanced economies. The number of international tourist arrivals to emerging economies, such as China, India, Brazil and Mexico, has been growing at about double the pace of travel to advanced economies such as the United States, Canada, Euro Area and Australia. According to the UNWTO, emerging economies had 46.8% of the share of international tourist share in 2012, up from just 31.9% in 1990. Asia and the Pacific recorded the fastest growth across all regions over the past five years, closely followed by Africa and the Americas, where international tourist arrivals grew at rates of above 5.0%. Tourism infrastructure in these regions has improved markedly and countries are pumping up the industry through extensive marketing campaigns. In comparison, tourism growth to traditional tourism hotspots, such as Canada, Western Europe and Australia, has waned. As a result, most of the industry's largest players have been focusing their development on emerging economies. For example, 85.0% of Starwood Hotels and Resorts Worldwide Inc.'s current development pipeline is focused outside of North America, with 44.0% in China alone. Industry structure Before mid-2008, industry operators achieved solid profit growth due to robust growth in hotel demand. Profit levels then fell from mid-2008 to early-2010 as hotel demand declined, even though some variable costs decreased. There are substantial fixed costs associated with operating a hotel, including maintenance and minimum labor requirements to deliver services to guests. Hotels and resorts also reduced their rates to keep occupancy rates from plummeting, which slashed profit margins. However, profit margins increased from mid-2010 through 2013, as demand conditions improve. Prevalent industry trends

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 6

Over the past few decades, technology has helped to increase productivity, decrease labor costs and enhance customer service. In particular, the industry has benefited from the increased prevalence of the internet through all aspects of society. Hotel operators use the internet to gather information, make bookings and buy supplies, which has lowered overall costs. The information gathered by operators via new technology also allows them to send better-targeted promotions by e-mail and social media. Many firms now operate guest rewards programs to attract and hold frequent travelers. Websites like Lastminute.com and Priceline.com, which offer advance bookings and significantly discounted room prices at the last minute, have flourished since the early 2000s. Most operators now allocate a portion of their expected unsold rooms to these websites, since travelers have become more confident in booking through them. The websites are either corporate-owned and managed or linked to other specialist travel operators. As a result in this increased productivity, industry employment growth has been relatively slow over the past five years, increasing just 0.7% per year on average to 4.2 million. This relatively low growth also reflects the cutting of surplus employees during the recession. In addition, industry operators have made greater use of casual employees, rather than full-time staff, to meet peak customer demand periods. Meanwhile, the number of industry establishments has grown at 1.3% per year on average over the past five years to 645,000. The expansion of the industry's biggest players into emerging economies has been the main reason behind this growth. Industry concentration has increased over the past five years as large, global hotel operators have increased their stranglehold on market share through buyouts and mergers. The top four operators in the industry, Hilton Worldwide, Marriott International, InterContinental Hotels Group and Wyndham Worldwide, are estimated to account for 13.2% of available market share in 2013.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 7

Industry Outlook

The Global Hotels and Resorts industry is expected to enjoy a more stable period over the next five years. The global economy will continue to improve, laying a foundation for reduced volatility, which has affected both revenue and profit over the past five years. Consumers will have more funds available for discretionary purchases due to consistent growth in per capita disposable income, which is expected to increase at an annualized 5.0% over the next five years. The industry's shift towards emerging economies will continue, taking advantage of improved tourism infrastructure in those regions. Over the five years to 2018, IBISWorld forecasts industry revenue will increase at an average annual rate of 2.2% to $661.5 billion. Tourism trends The industry's main driver is tourism and travel spending is projected to increase over the next five years as the global economy improves. The influx of tourist dollars will bolster revenue for global hotels and resorts. According to the United Nation World Tourism Organization's (UNWTO) Tourism Towards 2030, the number of international tourist arrivals worldwide is expected to increase by an average 3.3% a year from 2010 to 2030. Over time, the rate of growth will gradually slow, from 3.8% in the decade to 2020, to 2.5% in 2030. International tourist arrivals will increase by some 43.0 million a year to reach 1.8 billion by the year 2030. International tourist arrivals in emerging economy destinations of Asia, Latin America, Central and Eastern Europe, the Middle East and Africa are likely to grow at double the pace of developed economy destinations over the next five years. The biggest growth will be seen in Asia and the Pacific, where arrivals are forecast by UNWTO to increase by 4.9% per year on average to 2030. The Middle East and Africa are also expected to more than double their arrivals in this period. As a result, international hotel chains are going to experience the majority of their revenue and profit growth from emerging economies. Emerging economies are expected to surpass developed economies as the industry's number one source of revenue by 2015. In 2030, 57.0% of international arrivals will be in emerging economy destinations and 43.0% in developed economy destinations, according to the UNWTO. In order to keep up with the aggressive rise in travel rates in these emerging regions, more hotels and resorts will be built, which should increase the proportion of industry revenue that is generated from these regions and grow industry revenue as a whole. The industry will also benefit as the global economy improves, unemployment rates decline and consumers begin to spend money again, particularly on recreational activities like vacations and traveling. Disposable income among OECD countries is expected to increase over the five years to 2018 by an impressive 5.0% per year on average. Business spending is also forecast to increase, helping hotels and resorts increase their number of corporate clients. However, Western Europe is expected to experience subdued growth because it is a mature market and ongoing debt problems will continue to bog down several countries' recovery. The United States will also be hampered by a slow recovery as it continues to address its own structural economic changes. Trends promoting growth Over the next five years, investment in new hotel and motel rooms will gradually accelerate due to a sustained rise in tourist accommodation demand. More solid economic growth from 2013 to 2018 will likely mean investment will occur at a much faster pace to compensate for the dramatic decline in investment that the industry experienced over the past few years. Hotel investment by major operators will increasingly focus on opportunities in international travel markets and regions, including Russia, Eastern Europe, the Middle East, Latin America, Asia, China and India. Global hotels and resorts will also continue to segment into areas such as extended-stay, boutique hotels, resorts and spa and health retreats as guests search for more varied and hospitable accommodation experiences. The low-cost segment will also continue to expand and experience competition on the basis of price. This factor will place pressure on economy operators to hold or reduce costs. Overall, the number of industry enterprises is expected to jump 1.6% per year on average to 594,000, at a slightly faster rate than that of the past five years.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 8

Improving employment and profitability Industry profitability is expected to improve over the next five years as revenue improves and operators focus on cost reductions through improved labor productivity. Cost reductions may result from more group purchasing, marketing and sales arrangements, as well as the increasing use of internet information, booking, reservation and payment systems. Industry wages are expected to increase 2.2% per year on average to $167.2 billion.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 9

Industry Life Cycle

This industry is in the mature stage of its life cycle. Life Cycle Stage

Steady growth in the domestic tourism and business travel markets

More hotel and resort options allow the industry to better meet individual needs across markets

There has been strong growth in new emerging countries such as China and India

Despite the recent downturn in revenue, the Global Hotels and Resorts industry is in a mature phase. The latest decline in revenue can be directly attributed to the global economic recession as well as the industry's heavy dependence on tourism and disposable income levels. Over the ten years to 2018, industry value added, which measures an industry's contribution to GDP, will grow at an annual rate of 2.6% per year, compared to GDP growth over the same period of 5.4%. This is supported by the expected continuing growth in the international tourism and travel market. Tourism growth rates in North America and Europe are soft compared with emerging economies, meaning global hotel operators have increased their focus on emerging economies. This shift has intensified over the past five years as hotel chains chase revenue growth and higher profit margins in fast growing economies. The Asia Pacific region, Middle East and South America are especially popular among global hotel chains. For example, 85.0% of Starwood Hotels and Resorts Worldwide Inc.'s current development pipeline is focuses outside of North America, with 44.0% in China alone. Industry growth over the next five years will be supported by increasing international and domestic airline capacity and improvements in airline technology, including plane passenger capacity. Higher income in emerging economies will also boost tourist levels. In addition, the lifting of travel restrictions by governments around the world will assist in boosting tourist numbers, further benefiting hotels and resorts. Industry growth will be linked to the increasing propensity to travel for business as globalization continues to develop rapidly. Industry productivity is being assisted by increased utilization of technology by hotel operators. Direct bookings on the websites of major operators is increasing rapidly, with major hotel chains reporting that a consistently growing portion of their reservations are coming from the internet. Web-based bookings in all forms are expected to continue to expand rapidly.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 10

Products & Markets

Supply Chain

Key Buying Industries H4831-GL - Global Airlines Flight crews demand industry services. H4911-GL - Global Travel Agency Services Operators in this industry book hotel and resort accommodation on behalf of customers. Z01 - Global Consumers Consumers require accommodation when traveling, whether for business or pleasure. Key Selling Industries C1111-GL - Global Milk & Cream Manufacturing This industry supplies dairy products to hotels. C1112-GL - Global Fruit & Vegetables Processing This industry supplies fruits and vegetables to hotels. C1121-GL - Global Beer Manufacturing This industry supplies beer to hotels. C1122-GL - Global Spirits Manufacturing This industry supplies alcohol to hotels. Q8729-GL - Global Sports Betting & Lotteries Hotels and resorts accommodate visitors to casinos.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 11

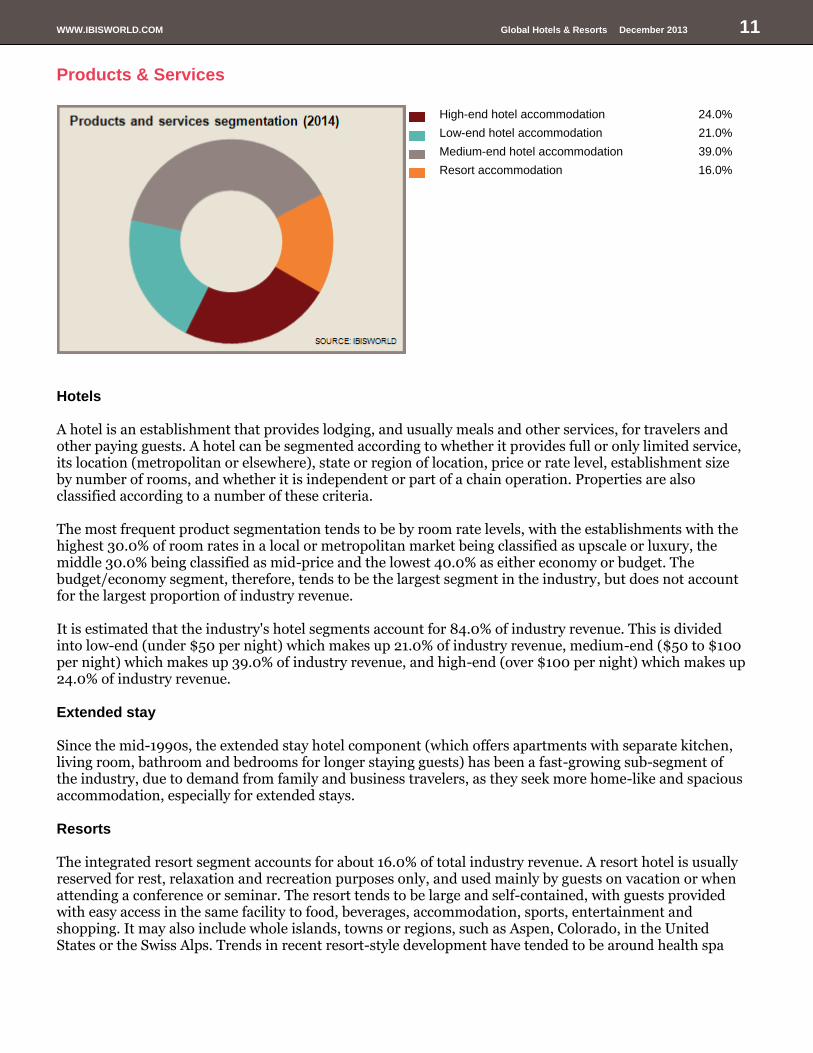

Products & Services

High-end hotel accommodation 24.0%

Low-end hotel accommodation 21.0%

Medium-end hotel accommodation 39.0%

Resort accommodation 16.0%

Hotels A hotel is an establishment that provides lodging, and usually meals and other services, for travelers and other paying guests. A hotel can be segmented according to whether it provides full or only limited service, its location (metropolitan or elsewhere), state or region of location, price or rate level, establishment size by number of rooms, and whether it is independent or part of a chain operation. Properties are also classified according to a number of these criteria. The most frequent product segmentation tends to be by room rate levels, with the establishments with the highest 30.0% of room rates in a local or metropolitan market being classified as upscale or luxury, the middle 30.0% being classified as mid-price and the lowest 40.0% as either economy or budget. The budget/economy segment, therefore, tends to be the largest segment in the industry, but does not account for the largest proportion of industry revenue. It is estimated that the industry's hotel segments account for 84.0% of industry revenue. This is divided into low-end (under $50 per night) which makes up 21.0% of industry revenue, medium-end ($50 to $100 per night) which makes up 39.0% of industry revenue, and high-end (over $100 per night) which makes up 24.0% of industry revenue. Extended stay Since the mid-1990s, the extended stay hotel component (which offers apartments with separate kitchen, living room, bathroom and bedrooms for longer staying guests) has been a fast-growing sub-segment of the industry, due to demand from family and business travelers, as they seek more home-like and spacious accommodation, especially for extended stays. Resorts The integrated resort segment accounts for about 16.0% of total industry revenue. A resort hotel is usually reserved for rest, relaxation and recreation purposes only, and used mainly by guests on vacation or when attending a conference or seminar. The resort tends to be large and self-contained, with guests provided with easy access in the same facility to food, beverages, accommodation, sports, entertainment and shopping. It may also include whole islands, towns or regions, such as Aspen, Colorado, in the United States or the Swiss Alps. Trends in recent resort-style development have tended to be around health spa

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 12

and eco-tourism accommodation, as some travelers become more health aware and environmentally conscious.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 13

Demand Determinants

Demand for the Hotels and Resorts industry is derived from both domestic and international visitors. Domestic tourism The majority of guests at hotels and resorts relate to domestic residents, taking business or vacation/pleasure trips, or visiting friends and relatives. Domestic demand for hotel/resort accommodation is, therefore, dependent on factors that affect travel, such as changes in household disposable income, which is influenced by changes in labor market growth as well as movements in local interest and tax rates. Changes in disposable income affect both the number of trips and expenditure by households while away, which in turn affects the growth and economic impact of this industry. Leisure time availability can affect tourism numbers. This includes the availability of leisure time and the recent reducing propensity of people in the labor market to use their vacation leave, due to work and family commitments. The relative cost of taking a holiday relates to the availability of cheap airfares and holiday packages, and the increasing supply of airline seats. Tourism promotions by private operators and federal and state governments, through travel and vacation shows, TV programs, and special sporting and other major events may also stimulate travel. Business travel Business travel, including for attendance at seminars and conferences, is also significant. However, this travel is more influenced by changes in economic growth, business sentiment and profitability. Also, economic conditions directly affect the number of business trips, the length of stay and budgeted travel amounts. Trip substitutability also influences business travel. Increasingly, some business travel can be substituted by communications and IT technology, including teleconferencing and conference calls. International tourism International tourism is one of the most highly competitive industries globally, with a multitude of countries and major cities seeking their fair share of this activity. International tourism is affected by global economic conditions, especially changes in economic growth, and particularly in major visitor origin countries/regions. Movements in relative exchange rates between countries also have an impact on the cost of travel, as well as the relative attractiveness of traveling to competing destinations. Wars, increasing geopolitical tensions or heightened fears of or actual terrorism activities affect international travel plans. Also, fears associated with the spread of SARS, avian flu, or swine flu influences travel demand and patterns.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 14

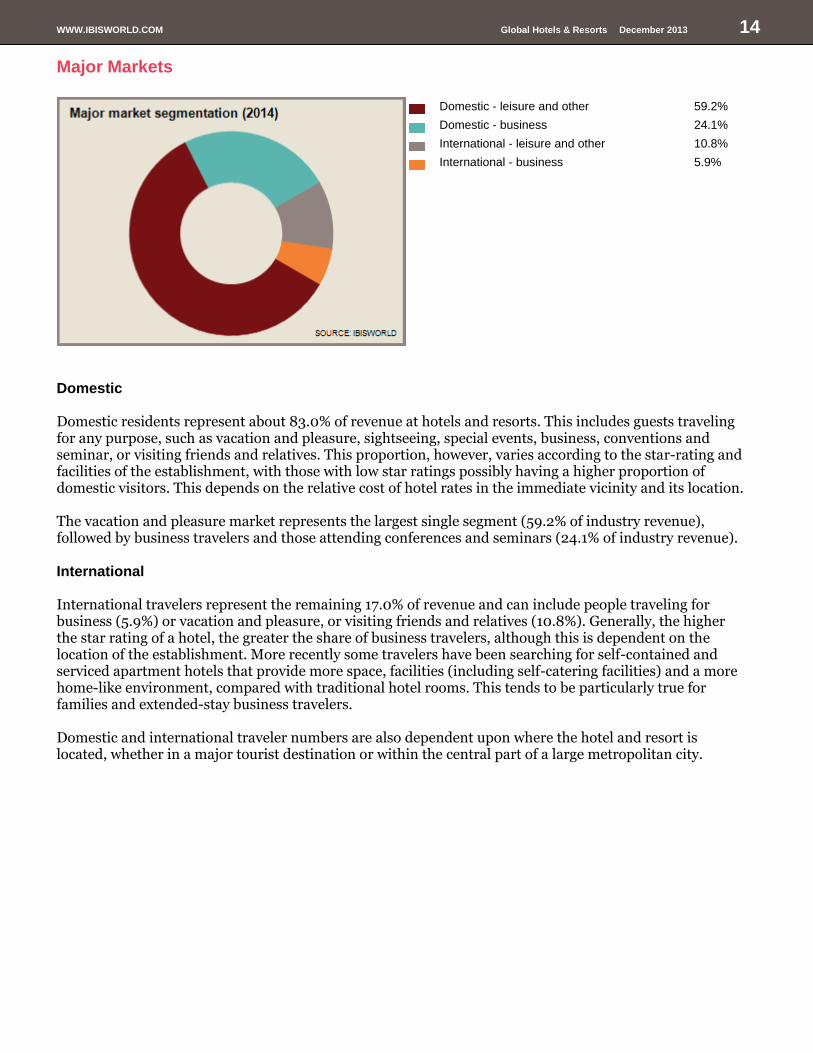

Major Markets

Domestic - leisure and other 59.2%

Domestic - business 24.1%

International - leisure and other 10.8%

International - business 5.9%

Domestic Domestic residents represent about 83.0% of revenue at hotels and resorts. This includes guests traveling for any purpose, such as vacation and pleasure, sightseeing, special events, business, conventions and seminar, or visiting friends and relatives. This proportion, however, varies according to the star-rating and facilities of the establishment, with those with low star ratings possibly having a higher proportion of domestic visitors. This depends on the relative cost of hotel rates in the immediate vicinity and its location. The vacation and pleasure market represents the largest single segment (59.2% of industry revenue), followed by business travelers and those attending conferences and seminars (24.1% of industry revenue). International International travelers represent the remaining 17.0% of revenue and can include people traveling for business (5.9%) or vacation and pleasure, or visiting friends and relatives (10.8%). Generally, the higher the star rating of a hotel, the greater the share of business travelers, although this is dependent on the location of the establishment. More recently some travelers have been searching for self-contained and serviced apartment hotels that provide more space, facilities (including self-catering facilities) and a more home-like environment, compared with traditional hotel rooms. This tends to be particularly true for families and extended-stay business travelers. Domestic and international traveler numbers are also dependent upon where the hotel and resort is located, whether in a major tourist destination or within the central part of a large metropolitan city.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 15

International Trade

Exports in this industry are low and steady. Imports in this industry are low and steady.

As a service-based industry, the Global Hotels and Resorts industry is not technically engaged in importing or exporting products, so international trade is not relevant to the industry. However, many hotels and resorts derive a significant proportion of their revenue from international guests. However, a number of industry players have operations abroad and earn a portion of their revenue overseas. Some hotel operators, such as Four Seasons Hotels and Resorts and Starwood Hotels and Resorts, earn well over 50.0% of their annual revenue from hotels located overseas. Many large operators have established franchised operations internationally. Given the mature stage of this industry's life cycle in developed economies such as the US, Canada and United Kingdom, many major operators are seeking to increase their growth in revenue and earnings through further global expansion.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 16

Business Locations

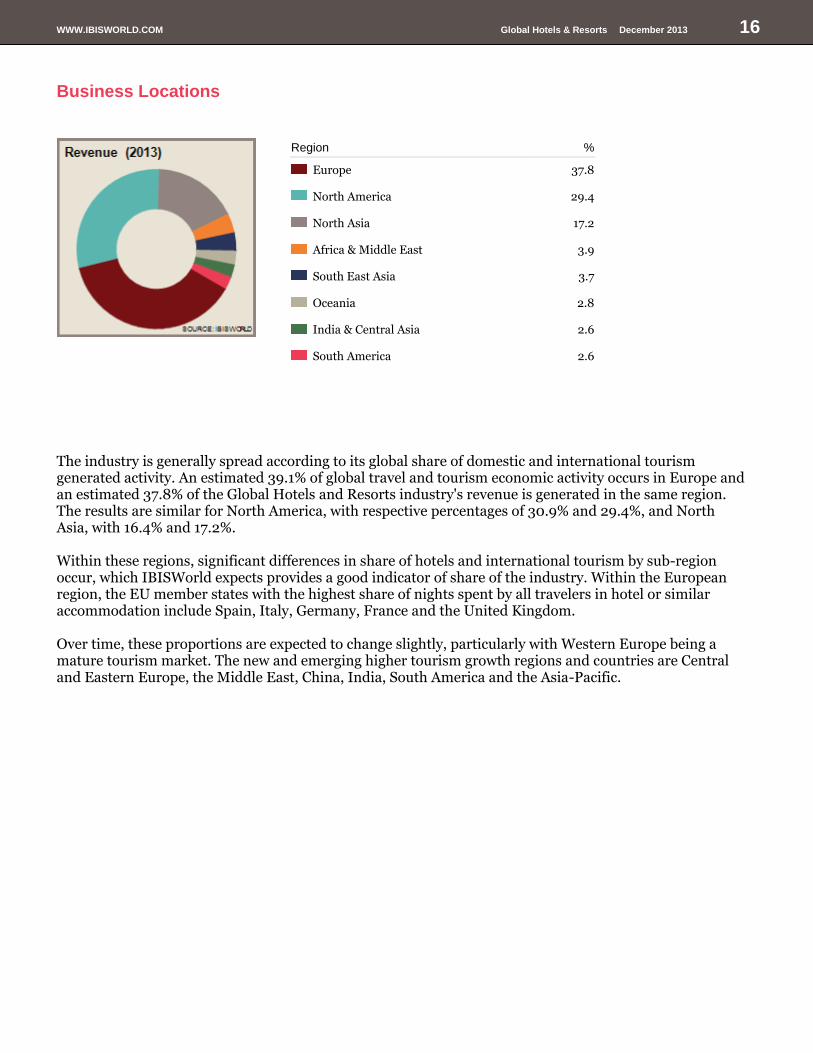

Region %

Europe 37.8

North America 29.4

North Asia 17.2

Africa & Middle East 3.9

South East Asia 3.7

Oceania 2.8

India & Central Asia 2.6

South America 2.6

The industry is generally spread according to its global share of domestic and international tourism generated activity. An estimated 39.1% of global travel and tourism economic activity occurs in Europe and an estimated 37.8% of the Global Hotels and Resorts industry's revenue is generated in the same region. The results are similar for North America, with respective percentages of 30.9% and 29.4%, and North Asia, with 16.4% and 17.2%. Within these regions, significant differences in share of hotels and international tourism by sub-region occur, which IBISWorld expects provides a good indicator of share of the industry. Within the European region, the EU member states with the highest share of nights spent by all travelers in hotel or similar accommodation include Spain, Italy, Germany, France and the United Kingdom. Over time, these proportions are expected to change slightly, particularly with Western Europe being a mature tourism market. The new and emerging higher tourism growth regions and countries are Central and Eastern Europe, the Middle East, China, India, South America and the Asia-Pacific.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 17

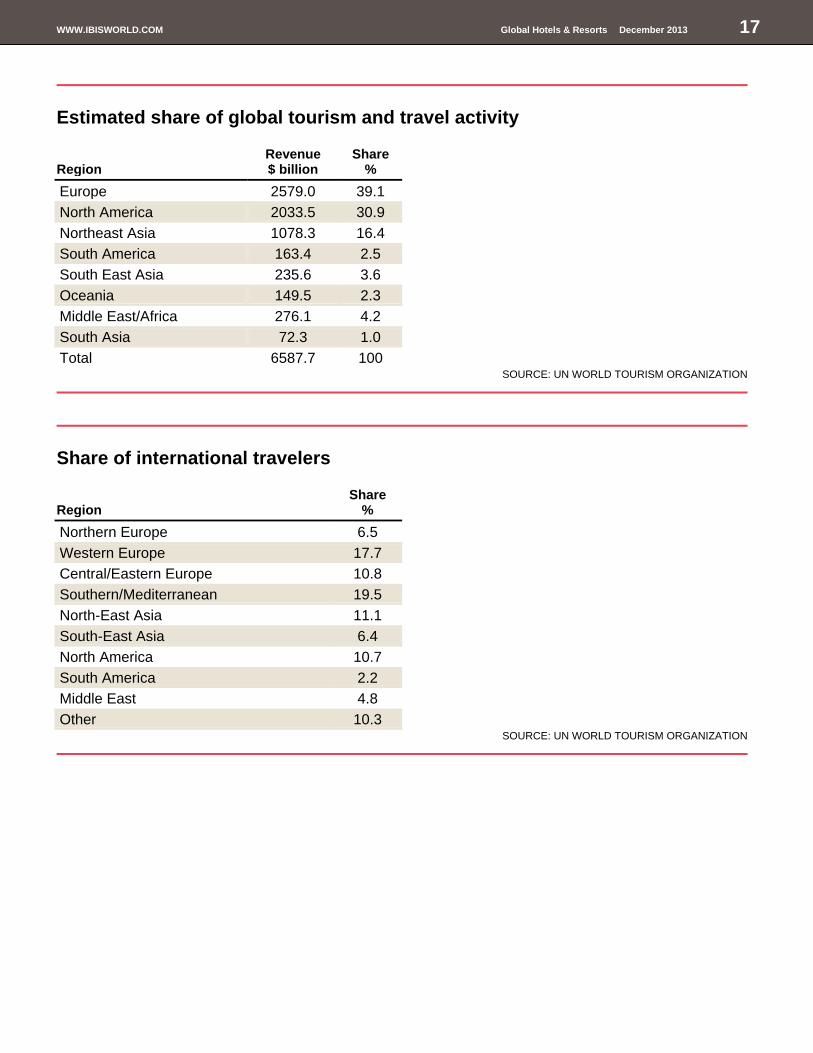

Estimated share of global tourism and travel activity

Region Revenue $ billion

Share %

Europe 2579.0 39.1

North America 2033.5 30.9

Northeast Asia 1078.3 16.4

South America 163.4 2.5

South East Asia 235.6 3.6

Oceania 149.5 2.3

Middle East/Africa 276.1 4.2

South Asia 72.3 1.0

Total 6587.7 100 SOURCE: UN WORLD TOURISM ORGANIZATION

Share of international travelers

Region Share

%

Northern Europe 6.5

Western Europe 17.7

Central/Eastern Europe 10.8

Southern/Mediterranean 19.5

North-East Asia 11.1

South-East Asia 6.4

North America 10.7

South America 2.2

Middle East 4.8

Other 10.3 SOURCE: UN WORLD TOURISM ORGANIZATION

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 18

Competitive Landscape

Market Share Concentration

Industry concentration is low.

IBISWorld estimates that in 2013, the industry's top four players will account for about 13.2% of the available market share, giving this industry a low level of concentration. Although industry concentration is low, it is increasing due to continuing hotel buyouts and mergers, and operators joining franchise and chain operators. Major companies in the hotel segment are increasingly seeking to operate on a global basis and have a presence in major regions and countries and in the major towns and cities in these areas. The merging of smaller operators with the major hotel companies on an international basis is expected to continue in the next five years. Industry concentration is continuing to increase among the major global operators, although this is more on a franchised or managed property basis.

Key Success Factors

The key success factors in the Global Hotels & Resorts industry are: Access to multiskilled and flexible workforce Access to multi-skilled and well trained staff is vital to ensure high levels of guest service and satisfaction. Being part of a franchising chain It is important for companies in the industry to closely evaluate the benefits of being part of a chain or franchised group, particularly in areas such as marketing and promotion. Receiving the benefit of word-of-mouth recommendations Good word-of-mouth recommendations are often the most successful promotional tool in the Hospitality industry. Proximity to key markets It is important for companies in the industry to be located close to other businesses that offer services and products for those in the same market. Ability to quickly adopt new technology Operators need to be aware of the new technology available in this industry for information, promotions, bookings and reservations and general management control systems. Ability to control stock on hand It is imperative for operators to understand the various room availability and tariff mechanisms used in this industry.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 19

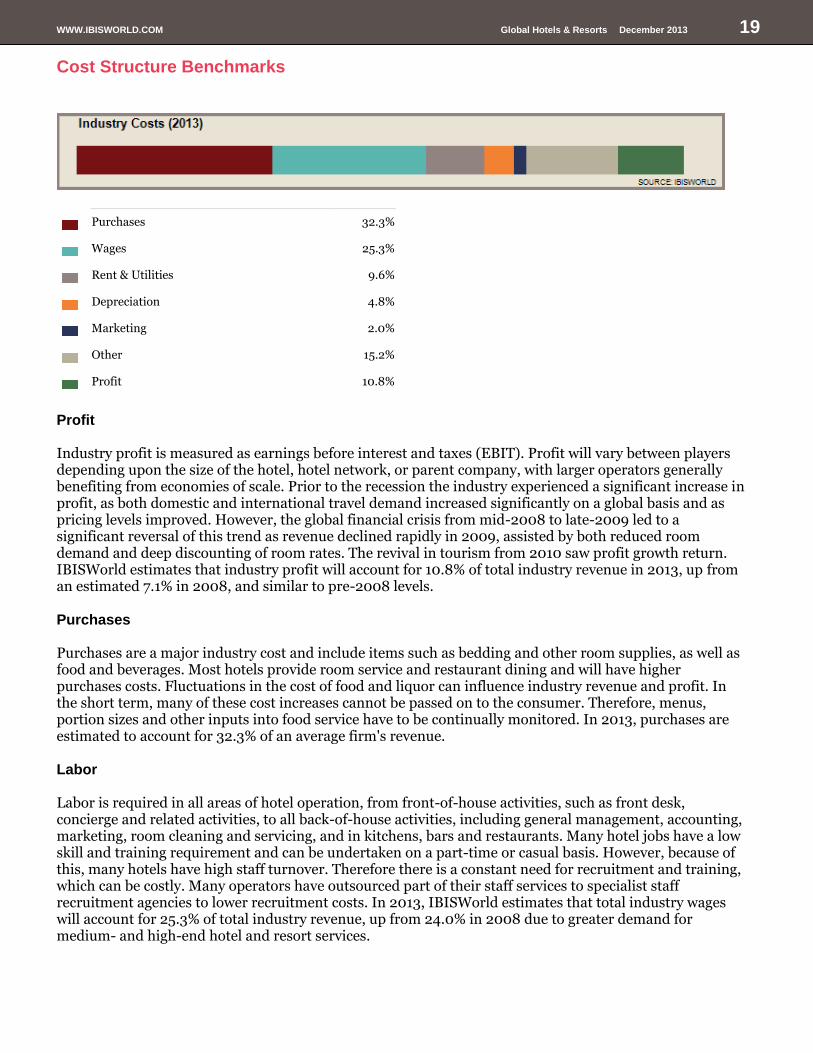

Cost Structure Benchmarks

Purchases 32.3%

Wages 25.3%

Rent & Utilities 9.6%

Depreciation 4.8%

Marketing 2.0%

Other 15.2%

Profit 10.8%

Profit Industry profit is measured as earnings before interest and taxes (EBIT). Profit will vary between players depending upon the size of the hotel, hotel network, or parent company, with larger operators generally benefiting from economies of scale. Prior to the recession the industry experienced a significant increase in profit, as both domestic and international travel demand increased significantly on a global basis and as pricing levels improved. However, the global financial crisis from mid-2008 to late-2009 led to a significant reversal of this trend as revenue declined rapidly in 2009, assisted by both reduced room demand and deep discounting of room rates. The revival in tourism from 2010 saw profit growth return. IBISWorld estimates that industry profit will account for 10.8% of total industry revenue in 2013, up from an estimated 7.1% in 2008, and similar to pre-2008 levels. Purchases Purchases are a major industry cost and include items such as bedding and other room supplies, as well as food and beverages. Most hotels provide room service and restaurant dining and will have higher purchases costs. Fluctuations in the cost of food and liquor can influence industry revenue and profit. In the short term, many of these cost increases cannot be passed on to the consumer. Therefore, menus, portion sizes and other inputs into food service have to be continually monitored. In 2013, purchases are estimated to account for 32.3% of an average firm's revenue. Labor Labor is required in all areas of hotel operation, from front-of-house activities, such as front desk, concierge and related activities, to all back-of-house activities, including general management, accounting, marketing, room cleaning and servicing, and in kitchens, bars and restaurants. Many hotel jobs have a low skill and training requirement and can be undertaken on a part-time or casual basis. However, because of this, many hotels have high staff turnover. Therefore there is a constant need for recruitment and training, which can be costly. Many operators have outsourced part of their staff services to specialist staff recruitment agencies to lower recruitment costs. In 2013, IBISWorld estimates that total industry wages will account for 25.3% of total industry revenue, up from 24.0% in 2008 due to greater demand for medium- and high-end hotel and resort services.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 20

Depreciation The level of depreciation a hotel operator is exposed to depends heavily on if they own the freehold to the premises. A greater percentage of hotel operators are choosing to rent rather than own the actual hotel property they manage, preferring to outsource the property-risk to investors. The industry's average level of depreciation has, therefore, grown over the five years to 2013 to represent an estimated 4.8% of total industry revenue. Other hotel investments that contribute to the high depreciation level include fixtures and fittings for rooms, restaurant equipment and capital improvement expenditure. Other Marketing costs and royalty fees are another significant cost for those industry participants that operate on a franchise basis. Franchisees typically pay an annual fee of 4.0% to 6.0% of total revenue. The industry average is significantly lower as less than half the industry's hotels are franchised. Rent and utilities both account for between 3.0% and 5.0% of revenue. However, this varies considerably across the industry due to the different ownership structures. Operators are also subject to a range of other costs associated with the normal course of doing business such as repairs and maintenance fees, professional and business fees such as those paid to lawyers, accountants and consultants and insurance and administrative overheads.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 21

Basis of Competition

Competition is high and increasing. Operators in this industry experience competition with other industry players (internal competition) and operators from other industries (external competition). The level of competition in this industry is currently high and increasing. Internal competition Internal industry competition is high and increasing, and quite often price or rate-based, as there are a large number of small operators and several very large international companies. At most price points, hotels look to attract travelers by offering competitive prices with a range and quality of service to maximize client satisfaction, while minimizing room vacancy rates. Room discounting increases during difficult economic periods, with fewer discounts offered in boom times. Other factors affecting competition include the location, being in an area which has a high level activity from both tourists and business travelers enhances demand, as well as the star-rating of the hotel/resort, and having both the required quality of facilities and service standards. The actual quality and level of service and hospitality provided by management and staff of the hotel or resort is also important, especially if it matches the expectations and demands of guests in all areas of operation. For some travelers, hotel branding and image associated with an establishment or franchised hotel name is important as a guarantee of facilities and service. The extent of information available on the establishment on company websites is also significant, as well as the increasing ability for guests to make a direct booking and payment over the internet. External competition The industry also faces competition from other segments of the wider accommodation market, including motels, bed and breakfast establishments, and hostels. As the tourism market segments further, resulting in new and emerging needs for travelers, external industry competition will increase.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 22

Barriers to Entry

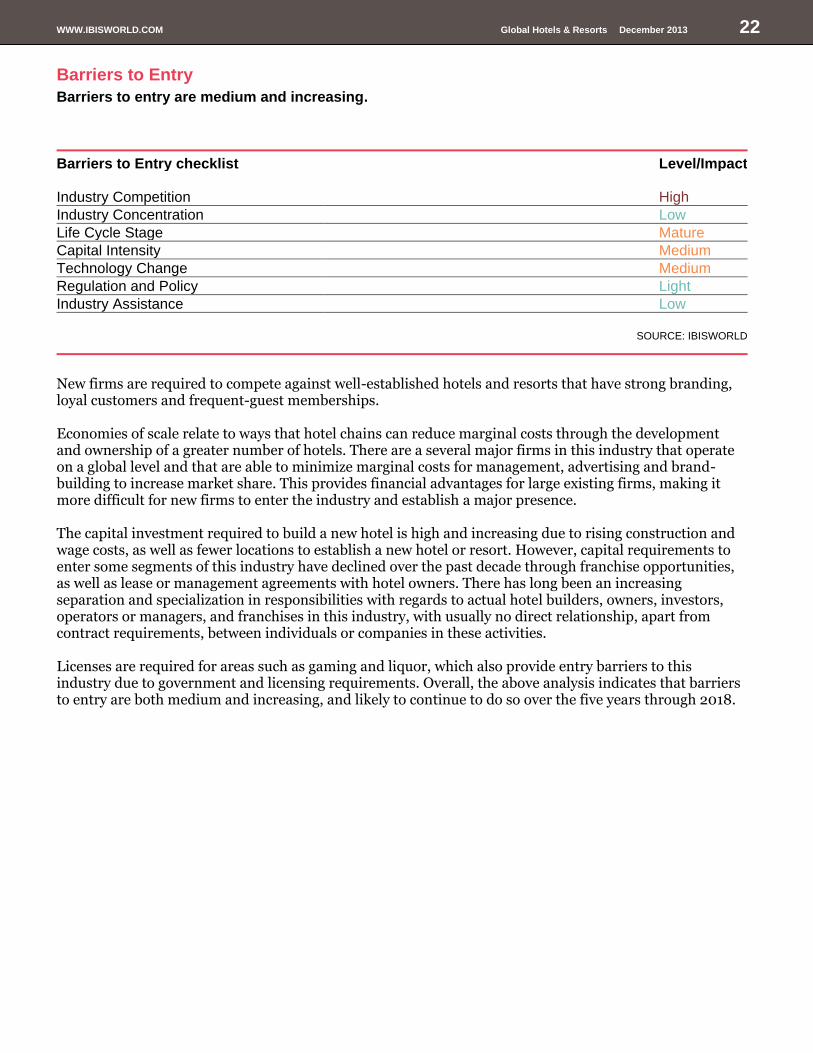

Barriers to entry are medium and increasing.

Barriers to Entry checklist Level/Impact Industry Competition High

Industry Concentration Low

Life Cycle Stage Mature

Capital Intensity Medium

Technology Change Medium

Regulation and Policy Light

Industry Assistance Low

SOURCE: IBISWORLD

New firms are required to compete against well-established hotels and resorts that have strong branding, loyal customers and frequent-guest memberships. Economies of scale relate to ways that hotel chains can reduce marginal costs through the development and ownership of a greater number of hotels. There are a several major firms in this industry that operate on a global level and that are able to minimize marginal costs for management, advertising and brand-building to increase market share. This provides financial advantages for large existing firms, making it more difficult for new firms to enter the industry and establish a major presence. The capital investment required to build a new hotel is high and increasing due to rising construction and wage costs, as well as fewer locations to establish a new hotel or resort. However, capital requirements to enter some segments of this industry have declined over the past decade through franchise opportunities, as well as lease or management agreements with hotel owners. There has long been an increasing separation and specialization in responsibilities with regards to actual hotel builders, owners, investors, operators or managers, and franchises in this industry, with usually no direct relationship, apart from contract requirements, between individuals or companies in these activities. Licenses are required for areas such as gaming and liquor, which also provide entry barriers to this industry due to government and licensing requirements. Overall, the above analysis indicates that barriers to entry are both medium and increasing, and likely to continue to do so over the five years through 2018.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 23

Industry Globalization

The level of globalization is low and increasing.

The majority of operators in this industry are regarded as having a low globalization level, due to many hotels being locally-owned and earning most of their sales from domestic activities. However, globalization within the hotel segment is increasing rapidly, due to the presence of major international hotel owners and managers that operate on a global scale, such as Marriott, Hilton, Accor and InterContinental hotels. This industry is expected to be subject to an increasing globalization level in upcoming years. This is the result of hotels seeking an international market presence for its travelers, the increased globalization of many major companies and business clients around the world, from the increasing of world-wide marketing and branding of hotels and resorts, as well as online booking and reservation systems.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 24

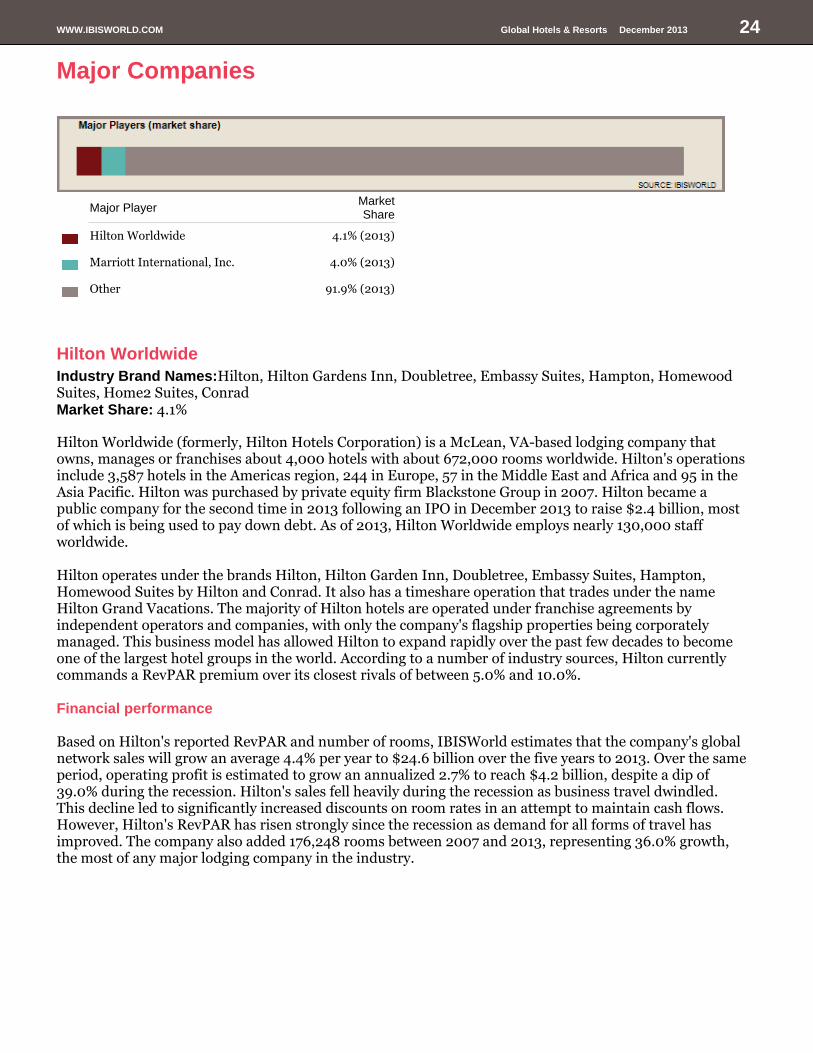

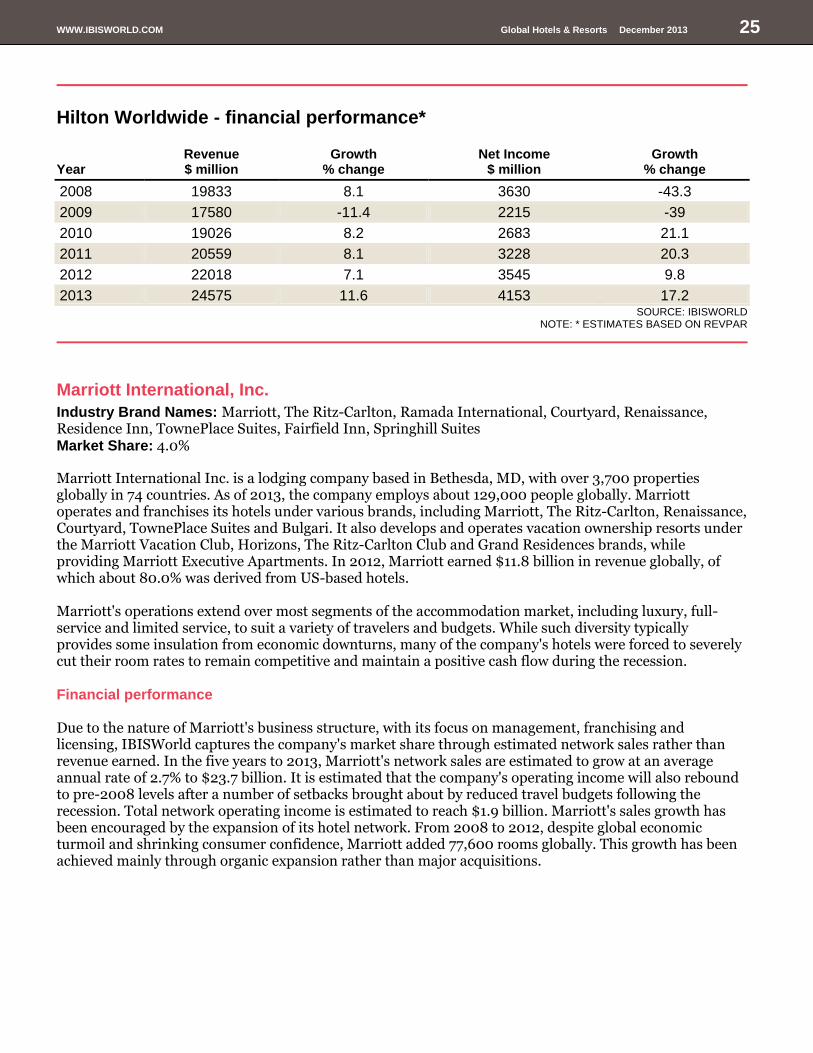

Hilton Worldwide (formerly, Hilton Hotels Corporation) is a McLean, VA-based lodging company that owns, manages or franchises about 4,000 hotels with about 672,000 rooms worldwide. Hilton's operations include 3,587 hotels in the Americas region, 244 in Europe, 57 in the Middle East and Africa and 95 in the Asia Pacific. Hilton was purchased by private equity firm Blackstone Group in 2007. Hilton became a public company for the second time in 2013 following an IPO in December 2013 to raise $2.4 billion, most of which is being used to pay down debt. As of 2013, Hilton Worldwide employs nearly 130,000 staff worldwide. Hilton operates under the brands Hilton, Hilton Garden Inn, Doubletree, Embassy Suites, Hampton, Homewood Suites by Hilton and Conrad. It also has a timeshare operation that trades under the name Hilton Grand Vacations. The majority of Hilton hotels are operated under franchise agreements by independent operators and companies, with only the company's flagship properties being corporately managed. This business model has allowed Hilton to expand rapidly over the past few decades to become one of the largest hotel groups in the world. According to a number of industry sources, Hilton currently commands a RevPAR premium over its closest rivals of between 5.0% and 10.0%. Financial performance Based on Hilton's reported RevPAR and number of rooms, IBISWorld estimates that the company's global network sales will grow an average 4.4% per year to $24.6 billion over the five years to 2013. Over the same period, operating profit is estimated to grow an annualized 2.7% to reach $4.2 billion, despite a dip of 39.0% during the recession. Hilton's sales fell heavily during the recession as business travel dwindled. This decline led to significantly increased discounts on room rates in an attempt to maintain cash flows. However, Hilton's RevPAR has risen strongly since the recession as demand for all forms of travel has improved. The company also added 176,248 rooms between 2007 and 2013, representing 36.0% growth, the most of any major lodging company in the industry.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 25

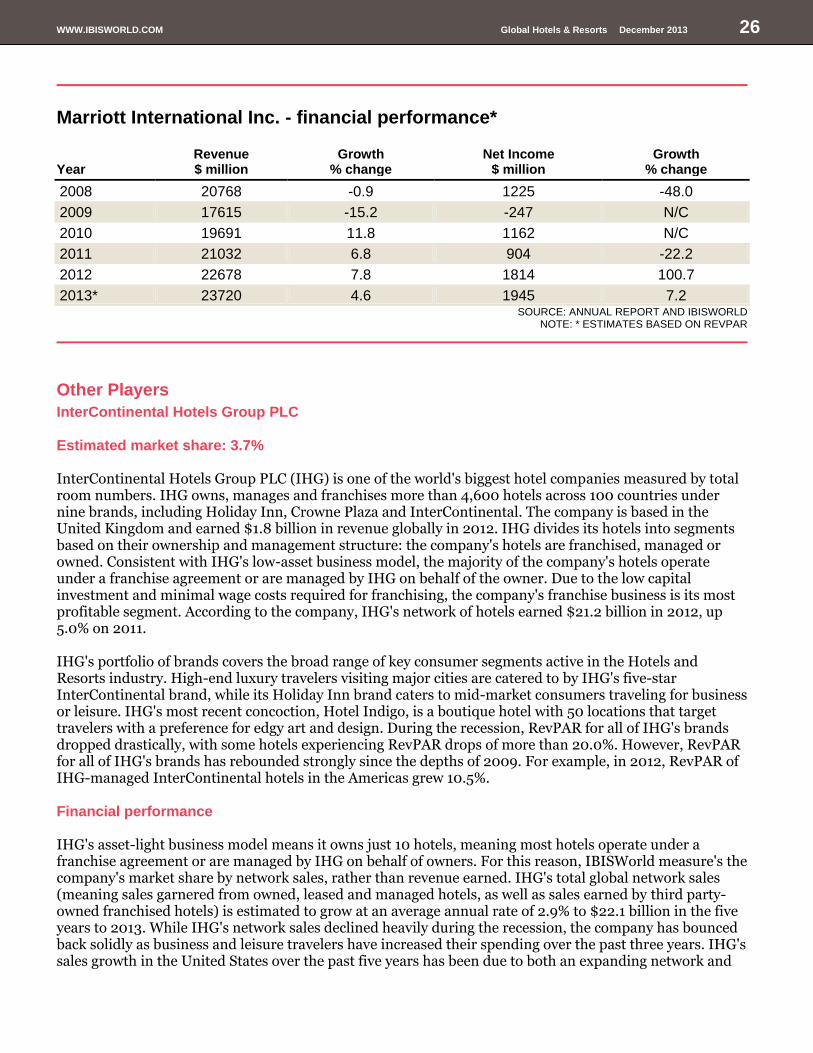

Marriott International Inc. is a lodging company based in Bethesda, MD, with over 3,700 properties globally in 74 countries. As of 2013, the company employs about 129,000 people globally. Marriott operates and franchises its hotels under various brands, including Marriott, The Ritz-Carlton, Renaissance, Courtyard, TownePlace Suites and Bulgari. It also develops and operates vacation ownership resorts under the Marriott Vacation Club, Horizons, The Ritz-Carlton Club and Grand Residences brands, while providing Marriott Executive Apartments. In 2012, Marriott earned $11.8 billion in revenue globally, of which about 80.0% was derived from US-based hotels. Marriott's operations extend over most segments of the accommodation market, including luxury, full-service and limited service, to suit a variety of travelers and budgets. While such diversity typically provides some insulation from economic downturns, many of the company's hotels were forced to severely cut their room rates to remain competitive and maintain a positive cash flow during the recession. Financial performance Due to the nature of Marriott's business structure, with its focus on management, franchising and licensing, IBISWorld captures the company's market share through estimated network sales rather than revenue earned. In the five years to 2013, Marriott's network sales are estimated to grow at an average annual rate of 2.7% to $23.7 billion. It is estimated that the company's operating income will also rebound to pre-2008 levels after a number of setbacks brought about by reduced travel budgets following the recession. Total network operating income is estimated to reach $1.9 billion. Marriott's sales growth has been encouraged by the expansion of its hotel network. From 2008 to 2012, despite global economic turmoil and shrinking consumer confidence, Marriott added 77,600 rooms globally. This growth has been achieved mainly through organic expansion rather than major acquisitions.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 26

Marriott International Inc. - financial performance*

Year Revenue $ million

Growth % change

Net Income $ million

Growth % change

2008 20768 -0.9 1225 -48.0

2009 17615 -15.2 -247 N/C

2010 19691 11.8 1162 N/C

2011 21032 6.8 904 -22.2

2012 22678 7.8 1814 100.7

2013* 23720 4.6 1945 7.2 SOURCE: ANNUAL REPORT AND IBISWORLD

NOTE: * ESTIMATES BASED ON REVPAR

Other Players

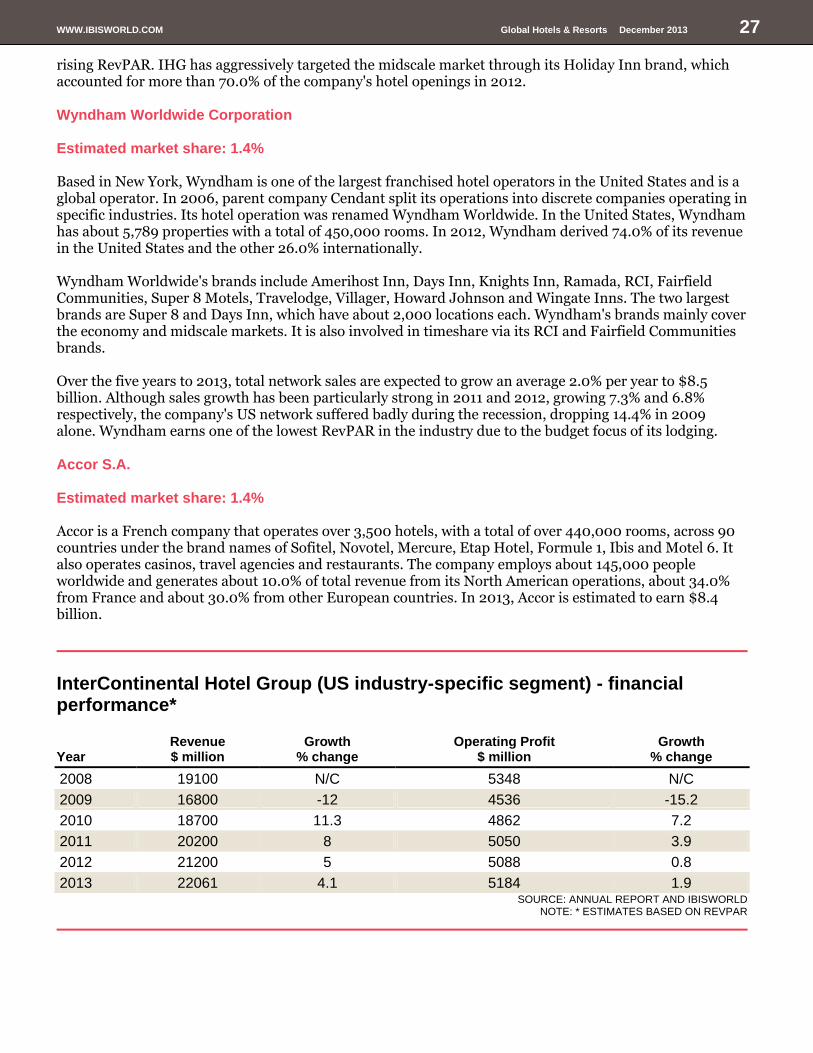

InterContinental Hotels Group PLC Estimated market share: 3.7% InterContinental Hotels Group PLC (IHG) is one of the world's biggest hotel companies measured by total room numbers. IHG owns, manages and franchises more than 4,600 hotels across 100 countries under nine brands, including Holiday Inn, Crowne Plaza and InterContinental. The company is based in the United Kingdom and earned $1.8 billion in revenue globally in 2012. IHG divides its hotels into segments based on their ownership and management structure: the company's hotels are franchised, managed or owned. Consistent with IHG's low-asset business model, the majority of the company's hotels operate under a franchise agreement or are managed by IHG on behalf of the owner. Due to the low capital investment and minimal wage costs required for franchising, the company's franchise business is its most profitable segment. According to the company, IHG's network of hotels earned $21.2 billion in 2012, up 5.0% on 2011. IHG's portfolio of brands covers the broad range of key consumer segments active in the Hotels and Resorts industry. High-end luxury travelers visiting major cities are catered to by IHG's five-star InterContinental brand, while its Holiday Inn brand caters to mid-market consumers traveling for business or leisure. IHG's most recent concoction, Hotel Indigo, is a boutique hotel with 50 locations that target travelers with a preference for edgy art and design. During the recession, RevPAR for all of IHG's brands dropped drastically, with some hotels experiencing RevPAR drops of more than 20.0%. However, RevPAR for all of IHG's brands has rebounded strongly since the depths of 2009. For example, in 2012, RevPAR of IHG-managed InterContinental hotels in the Americas grew 10.5%. Financial performance IHG's asset-light business model means it owns just 10 hotels, meaning most hotels operate under a franchise agreement or are managed by IHG on behalf of owners. For this reason, IBISWorld measure's the company's market share by network sales, rather than revenue earned. IHG's total global network sales (meaning sales garnered from owned, leased and managed hotels, as well as sales earned by third party-owned franchised hotels) is estimated to grow at an average annual rate of 2.9% to $22.1 billion in the five years to 2013. While IHG's network sales declined heavily during the recession, the company has bounced back solidly as business and leisure travelers have increased their spending over the past three years. IHG's sales growth in the United States over the past five years has been due to both an expanding network and

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 27

rising RevPAR. IHG has aggressively targeted the midscale market through its Holiday Inn brand, which accounted for more than 70.0% of the company's hotel openings in 2012. Wyndham Worldwide Corporation Estimated market share: 1.4% Based in New York, Wyndham is one of the largest franchised hotel operators in the United States and is a global operator. In 2006, parent company Cendant split its operations into discrete companies operating in specific industries. Its hotel operation was renamed Wyndham Worldwide. In the United States, Wyndham has about 5,789 properties with a total of 450,000 rooms. In 2012, Wyndham derived 74.0% of its revenue in the United States and the other 26.0% internationally. Wyndham Worldwide's brands include Amerihost Inn, Days Inn, Knights Inn, Ramada, RCI, Fairfield Communities, Super 8 Motels, Travelodge, Villager, Howard Johnson and Wingate Inns. The two largest brands are Super 8 and Days Inn, which have about 2,000 locations each. Wyndham's brands mainly cover the economy and midscale markets. It is also involved in timeshare via its RCI and Fairfield Communities brands. Over the five years to 2013, total network sales are expected to grow an average 2.0% per year to $8.5 billion. Although sales growth has been particularly strong in 2011 and 2012, growing 7.3% and 6.8% respectively, the company's US network suffered badly during the recession, dropping 14.4% in 2009 alone. Wyndham earns one of the lowest RevPAR in the industry due to the budget focus of its lodging. Accor S.A. Estimated market share: 1.4% Accor is a French company that operates over 3,500 hotels, with a total of over 440,000 rooms, across 90 countries under the brand names of Sofitel, Novotel, Mercure, Etap Hotel, Formule 1, Ibis and Motel 6. It also operates casinos, travel agencies and restaurants. The company employs about 145,000 people worldwide and generates about 10.0% of total revenue from its North American operations, about 34.0% from France and about 30.0% from other European countries. In 2013, Accor is estimated to earn $8.4 billion.

InterContinental Hotel Group (US industry-specific segment) - financial performance*

Year Revenue $ million

Growth % change

Operating Profit $ million

Growth % change

2008 19100 N/C 5348 N/C

2009 16800 -12 4536 -15.2

2010 18700 11.3 4862 7.2

2011 20200 8 5050 3.9

2012 21200 5 5088 0.8

2013 22061 4.1 5184 1.9 SOURCE: ANNUAL REPORT AND IBISWORLD

NOTE: * ESTIMATES BASED ON REVPAR

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 28

Operating Conditions

Capital Intensity

The level of capital intensity is medium.

This industry is highly customer service oriented

Labor input is required in almost all areas of hotel operation The Global Hotels and Resorts industry is subject to a moderate level of capital intensity. For every $1.00 the average restaurant in the industry spends on wages in 2013, it will spend an estimated $0.19 on the use and replacement of capital. Both labor and capital play an important role in the industry. As a service-based industry, hotel and resort operators are highly dependent on direct labor input across all areas of operation, from front-desk service, reservations, room service and cleaning, food preparation, liquor and beverage service, and back of house operational management. Due to the service nature of the industry, many of these labor-intensive functions cannot be substituted by technology or machinery. To meet customers' expectations and provide a hospitable stay, trained staff are required. Labor costs can be managed by bringing on an appropriate number of trained casual and part-time staff at peak guest periods. Capital costs are also high and operators are exposed to a high level of depreciation. Investment in buildings, fixtures and fittings, restaurant equipment and capital improvement expenditure all contribute to high capital costs. However, a greater percentage of hotel operators are choosing to rent rather than own the actual hotel property they manage, preferring to outsource the property-risk to investors, lowing their capital costs.

Technology & Systems

The level of technology change is medium.

The use of technology in this industry mainly relates to communications, such as fax, e-mail and web-based information, as well as booking and reservation systems. Hotels require computerized and online booking and reservation systems that incorporate room management, accounting and management information systems, as well as direct approval and payment facilities. Some companies in this industry have adopted franchise and chain models for their hotels, which reduces company exposure, debt levels and risks. This has also extended towards recent floats of hotel property trusts, and the public floating of some major hotel management companies. However, due to the increased uncertainty related to operators retaining their property management agreement (with more stringent and unfavorable conditions on these agreements), some operators are choosing to purchase properties to ensure market presence and certainty is maintained. For major hotels, the provision of wiring and points for computer and internet access for clients is important. Also, direct bookings on the web sites of major operators and discount sites continue to increase strongly. Other hotel groups release their excess rooms at deep discounts and at short notice to other web-based hotel accommodation sellers. Marriott and Hyatt have established a separate internet company to supply the hotel industry with everything from bath soap to electricity, and this is now extending to other operators.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 29

Revenue Volatility

Industry revenue volatility is medium.

Industry revenue volatility is medium due to the industry's dependence on both business and leisure-related travel, which has some volatility with changes in economic conditions and therefore accommodation demand. There is also some reliance on growth in international business and leisure travel, which is sensitive to economic and political uncertainties. Industry revenue volatility increased in the past five years, with an estimated 7.5% drop in industry revenue in 2009. Industry revenue rebounded in 2010 with estimated growth of 4.6%, followed by smaller increases in subsequent years. Future industry revenue volatility is forecast to be low as the global economy recovers and domestic and international tourist numbers increase steadily, driving demand for hotel and resort services.

Regulation & Policy

The level of regulation is light and the trend is steady. Regulations outline the legislative requirements for hotels and resorts operating in this industry. With few government controls and regulations for hotel and resort operations, this industry is subject to a light and steady regulatory level. The industry is not regulated to any great extent, but does have to conform to laws and regulations applicable in the country of operation. These can include general local planning rules, including fire safety; general public health, such as food safety and handling within restaurants; occupational health and safety regulations for workers and guests; and, liquor licensing laws, if a hotel is licensed.

Industry Assistance

The level of industry assistance is low and the trend of industry assistance is increasing. There are no specific tariffs for this industry.

The Global Hotels and Resorts industry benefits from the tourism advertising and promotional activities of national and provincial governments to attract international tourists. These funds are of direct assistance to operators, many of which may not directly contribute financially or link onto any strategic promotional initiatives internationally. In some developing countries, approved new hotel and resorts or their expansion may be entitled to receive an investment allowance to offset against chargeable income. In addition, some countries have negotiated a double taxation agreement with other countries under which exemptions or tax concessions granted by a national government are not negated by an imposition of tax in the country of residence of the investor. Finally, governments in some countries reduce or eliminate taxation payable by non-residents on profit from the sale of investment land used for particular purposes that may include hotel and resort developments. These policies are usually designed to attract investment and employment to countries or even regions within them. Governments may also offer accelerated depreciation and investment allowances as incentives for the building of accommodation.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 30

Key Statistics

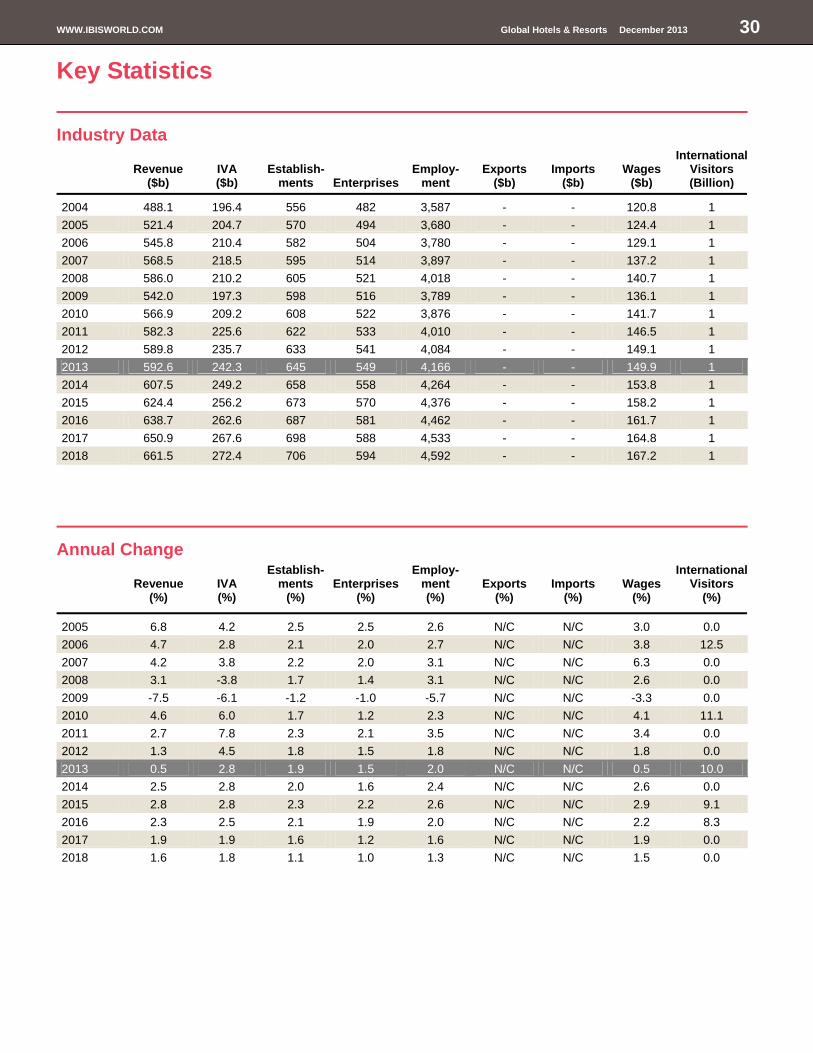

Industry Data

Revenue ($b)

IVA ($b)

Establish-ments Enterprises

Employ-ment

Exports ($b)

Imports ($b)

Wages ($b)

International Visitors (Billion)

2004 488.1 196.4 556 482 3,587 - - 120.8 1

2005 521.4 204.7 570 494 3,680 - - 124.4 1

2006 545.8 210.4 582 504 3,780 - - 129.1 1

2007 568.5 218.5 595 514 3,897 - - 137.2 1

2008 586.0 210.2 605 521 4,018 - - 140.7 1

2009 542.0 197.3 598 516 3,789 - - 136.1 1

2010 566.9 209.2 608 522 3,876 - - 141.7 1

2011 582.3 225.6 622 533 4,010 - - 146.5 1

2012 589.8 235.7 633 541 4,084 - - 149.1 1

2013 592.6 242.3 645 549 4,166 - - 149.9 1

2014 607.5 249.2 658 558 4,264 - - 153.8 1

2015 624.4 256.2 673 570 4,376 - - 158.2 1

2016 638.7 262.6 687 581 4,462 - - 161.7 1

2017 650.9 267.6 698 588 4,533 - - 164.8 1

2018 661.5 272.4 706 594 4,592 - - 167.2 1

Annual Change

Revenue (%)

IVA (%)

Establish-ments

(%) Enterprises

(%)

Employ-ment (%)

Exports (%)

Imports (%)

Wages (%)

International Visitors

(%)

2005 6.8 4.2 2.5 2.5 2.6 N/C N/C 3.0 0.0

2006 4.7 2.8 2.1 2.0 2.7 N/C N/C 3.8 12.5

2007 4.2 3.8 2.2 2.0 3.1 N/C N/C 6.3 0.0

2008 3.1 -3.8 1.7 1.4 3.1 N/C N/C 2.6 0.0

2009 -7.5 -6.1 -1.2 -1.0 -5.7 N/C N/C -3.3 0.0

2010 4.6 6.0 1.7 1.2 2.3 N/C N/C 4.1 11.1

2011 2.7 7.8 2.3 2.1 3.5 N/C N/C 3.4 0.0

2012 1.3 4.5 1.8 1.5 1.8 N/C N/C 1.8 0.0

2013 0.5 2.8 1.9 1.5 2.0 N/C N/C 0.5 10.0

2014 2.5 2.8 2.0 1.6 2.4 N/C N/C 2.6 0.0

2015 2.8 2.8 2.3 2.2 2.6 N/C N/C 2.9 9.1

2016 2.3 2.5 2.1 1.9 2.0 N/C N/C 2.2 8.3

2017 1.9 1.9 1.6 1.2 1.6 N/C N/C 1.9 0.0

2018 1.6 1.8 1.1 1.0 1.3 N/C N/C 1.5 0.0

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 31

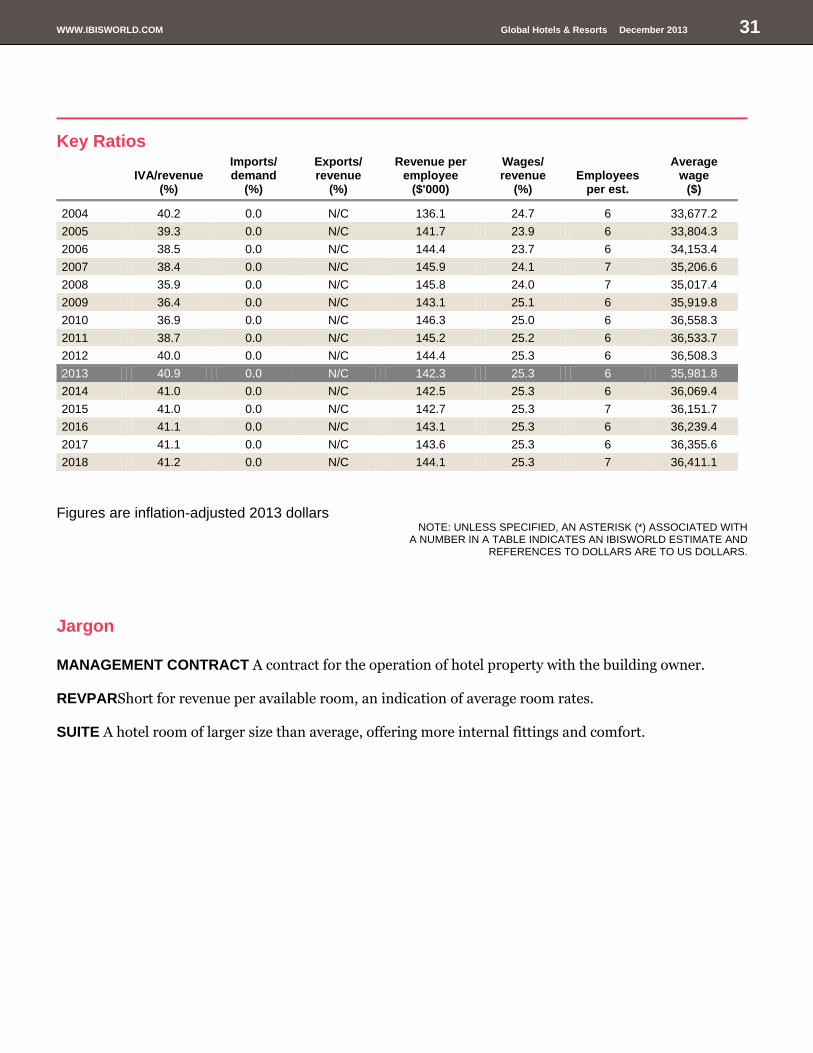

Key Ratios

IVA/revenue (%)

Imports/ demand

(%)

Exports/ revenue

(%)

Revenue per employee

($'000)

Wages/ revenue

(%) Employees

per est.

Average wage

($)

2004 40.2 0.0 N/C 136.1 24.7 6 33,677.2

2005 39.3 0.0 N/C 141.7 23.9 6 33,804.3

2006 38.5 0.0 N/C 144.4 23.7 6 34,153.4

2007 38.4 0.0 N/C 145.9 24.1 7 35,206.6

2008 35.9 0.0 N/C 145.8 24.0 7 35,017.4

2009 36.4 0.0 N/C 143.1 25.1 6 35,919.8

2010 36.9 0.0 N/C 146.3 25.0 6 36,558.3

2011 38.7 0.0 N/C 145.2 25.2 6 36,533.7

2012 40.0 0.0 N/C 144.4 25.3 6 36,508.3

2013 40.9 0.0 N/C 142.3 25.3 6 35,981.8

2014 41.0 0.0 N/C 142.5 25.3 6 36,069.4

2015 41.0 0.0 N/C 142.7 25.3 7 36,151.7

2016 41.1 0.0 N/C 143.1 25.3 6 36,239.4

2017 41.1 0.0 N/C 143.6 25.3 6 36,355.6

2018 41.2 0.0 N/C 144.1 25.3 7 36,411.1

Figures are inflation-adjusted 2013 dollars

NOTE: UNLESS SPECIFIED, AN ASTERISK (*) ASSOCIATED WITH A NUMBER IN A TABLE INDICATES AN IBISWORLD ESTIMATE AND

REFERENCES TO DOLLARS ARE TO US DOLLARS.

Jargon

MANAGEMENT CONTRACT A contract for the operation of hotel property with the building owner. REVPARShort for revenue per available room, an indication of average room rates. SUITE A hotel room of larger size than average, offering more internal fittings and comfort.

WWW.IBISWORLD.COM Global Hotels & Resorts December 2013 32

Disclaimer This product has been supplied by IBISWorld Inc. (“IBISWorld”) solely for use by its authorized licensees strictly in accordance with their license agreements with IBISWorld. IBISWorld makes no representation to any person with regard to the completeness or accuracy of the data or information contained herein, and it accepts no responsibility and disclaims all liability (save for liability which cannot be lawfully disclaimed) for loss or damage whatsoever suffered or incurred by any other person resulting from the use of, or reliance upon, the data or information contained herein. Copyright in this publication is owned by IBISWorld Inc. The publication is sold on the basis that the purchaser agrees not to copy the material contained within it for other than the purchasers own purposes. In the event that the purchaser uses or quotes from the material in this publication – in papers, reports or opinions prepared for any other person – it is agreed that it will be sourced to IBISWorld Inc.

IBISWorld's reports are more than just numbers. They combine data and analysis to answer the questions that successful businesses ask.

Who is IBISWorld? We are strategists, analysts, researchers and marketers. We provide answers to information-hungry, time-poor businesses. Our goal is to provide real-world answers that matter to your business. When tough strategic, budget, sales and marketing decisions need to be made, our suite of industry, economy and risk reports give you thoroughly researched answers quickly. IBISWorld Membership IBISWorld offers tailored membership packages to meet your needs.