20

GLOBAL IPO MARKET OUTLOOK www.datasite.com www.mergermarket.com

| Date post: | 04-May-2019 |

| Category: |

Documents |

| Upload: | truongkiet |

| View: | 222 times |

| Download: | 0 times |

Global IPo Market outlook

www.datasite.com www.mergermarket.com

PAGE

02

www.mergermarket.com

Global IPO Market Outlook

www.datasite.com

ContentsForeword 3

Methodology 3

Survey Findings 4

Historical Data 14

About Merrill Corporation 16

About Merrill Datasite 17

Merrill Contacts 18

Notes and Contacts 19

www.mergermarket.com

PAGE

03

Respondents are optimistic that global IPO activity will increase over the course of the year. This increase will be largely driven by activity in the Asia-Pacific and North American regions, as rapid growth in China and economic recovery in the US are cited frequently by respondents as major catalysts for new offerings.

Respondents’ optimism is also reflected in their outlook for specific IPO drivers. Tellingly, respondents say offerings will be driven primarily by companies’ expansion plans, rather than their need to address debt or liquidity issues: one-third of respondents believe most companies will use IPOs to raise capital for organic growth, and one-fifth of respondents say most companies will use IPOs to finance acquisitions.

Favorable conditions in individual sectors will also contribute to an increase in the volume of IPOs. Energy will likely be the most active sector for new offerings this year, as commodity price stabilization and increased demand will allow for greater investor confidence. The healthcare industry will produce its fair share of IPOs as well, as healthcare reform in the US and rising demand in emerging markets create opportunities for investors in all regions.

Still, it could take some time for the IPO market to recover fully from a relatively flat period. More than half of respondents (53%) believe delayed or cancelled IPOs will materialize in 6 to 12 months, although it is worth noting that one-fifth of respondents believe these planned offerings will resurface in the next 3 to 6 months.

Not surprisingly, the US is expected to host the most significant IPO activity this year on its New York Stock Exchange (NYSE) and NASDAQ. But other Western exchanges, including the London Stock Exchange (AIM) and Euronext, could be rivaled by Asian exchanges, most notably the Shanghai Stock Exchange and the Hong Kong Stock Exchange.

Companies entering the public markets will naturally face a range of new pressures. The greatest challenge facing newly-listed firms this year will be managing relationships with stakeholders and shareholders (34%) and implementing new growth strategies (30%).

This report offers a close look at the IPO market from the perspective of the global business community. Respondents provide insight into the specific factors influencing IPO due diligence procedures, average premium rates and a range of other important issues. We hope you find this report both useful and informative and as always, we welcome your feedback.

Merrill DataSite® commissioned mergermarket to conduct interviews with 150 practitioners, including corporate executives, private equity investors, financial advisors, lawyers and bankers based in North America, Europe and the Asia-Pacific region. Respondents offered valuable insight into the current IPO market and provided a forecast for global IPO activity trends in the year ahead. All respondents are anonymous and results are presented in aggregate.

Welcome to the Global IPO Market Outlook, published by mergermarket in association with Merrill DataSite®. Based on a series of interviews with IPO professionals across North America, Europe and Asia, this report provides a detailed analysis of global IPO activity and forward-looking insight into where the market is headed in the upcoming months.

www.mergermarket.com

Foreword

MetHodoloGY

PAGE

04

www.mergermarket.com

Global IPO Market Outlook

surveY FIndInGs

In each of the following regions, what do you expect to happen to IPO activity levels over the next 12 months?

What will be the primary objective of companies’ IPO filings over the next 12 months?

32%1%

18%

21%

8%

20%

To raise capitalfor organic growth

To raise capitalfor acquisitions

To increase liquidity

Exit strategy forprivate equity orventure capitalfirms

To repay debt

Other

Increase significantly

Per

cent

age

of r

espo

nden

ts

0

20

40

60

80

100

EasternEurope

LatinAmerica

WesternEurope

NorthAmerica

Asia-Pacific

Increase Remain the same Decrease

30%

67%

19%

56%

6%

19%

5%

45%

12%

38%

31%

9%

60%

3%

43%

3%3%

51%

The outlook for the global IPO market is positive, with the majority of respondents expecting activity to increase or remain at its current level across all regions this year. Expectations are particularly high for the Asia-Pacific region, where respondents almost unanimously agree that IPO activity is set to increase over the next 12 months. Many of these respondents refer specifically to China, where an expanding middle class and rising consumer demand have created a favorable climate for companies in all sectors looking to go public. An executive based in Germany believes this environment will allow companies to “confidently move forward with their IPO plans” in the coming year.

North America is also expected to see an increase in IPO activity by a significant majority of respondents (75%), due largely to economic recovery in the US. A financial advisor based in the US believes private equity exits will account for most IPOs announced in the upcoming year as investors take advantage of an improved valuation climate, while many other respondents believe IPO activity will reflect a significant improvement in investor confidence.

Companies’ growth strategies will likely be the primary driver of IPO activity this year. Approximately one-third of respondents believe most new listings will aim to raise capital for organic growth, and approximately one-fifth of respondents believe most companies will launch IPOs to raise capital for acquisitions.

Remaining respondents believe IPOs announced in the upcoming year will reflect companies’ need for liquidity (20%), or will come from private equity and venture capital exits (18%). Many respondents add that these drivers will vary on a regional basis: while IPOs in Western Europe will be driven by companies’ need for liquidity, IPOs in North America will reflect improved economic conditions. A corporate executive based in China explains, “Many companies are approaching list-able financial figures” in the US while another executive from the US agrees that “the window for investments is starting to open up” in the country.

PAGE

05

www.mergermarket.com

Which of the following sectors do you expect to produce the highest volume of IPOs globally over the next 12 months?

In which annual revenue range do you expect most companies planning an IPO in the next 12 months to fall?

9%

25%

31%

10%

25%

<US$10M

US$10M - US$50M

US$50M - US$100M

US$100M - US$300M

US$300M - US$500M

>US$500M

34%2%

2%2%

7%

21%

5%

4%

5%

8%

10%

Energy

Healthcare

Technology

Telecommunications

Consumer

Financial services

Industrials,manufacturing& engineering

Biotech & lifesciences

Chemicals

Media

Real estate

The largest percentage of respondents (34%) expect the most significant IPO activity to come from the energy sector due to a combination of improved investor confidence and favorable industry conditions. A financial advisor based in the US explains, “With commodity price stabilization, investors will be more willing to enter the energy market this year.” A lawyer based in Turkey adds, “Most of the energy projects that were stopped or halted during the crisis are resuming, and companies’ major source of capital for these projects will come from going public through an IPO.”

The healthcare sector is also expected to produce a high volume of IPOs this year, according to over one-fifth of respondents, many of whom refer to healthcare reform in the US as a catalyst for new offerings. Other respondents believe healthcare IPOs will reflect a high volume of new, growing companies in the sector.

Respondents’ expectations vary when it comes to typical offering sizes over the next 12 months. The largest percentage of respondents (31%) believe most companies seeking listings this year will have annual revenues in the US$50M to US$100M range, while one-quarter of respondents believe higher revenues between US$100M to US$300M will be the norm. Meanwhile, one-quarter of respondents are more bullish, expecting most IPOs to come from companies with revenues of US$500M or greater.

This division is reflected in respondents’ comments, which seem to vary according to their regional backgrounds. Many respondents based in Asia expect small or mid-market firms to generate the most significant IPO activity this year, while respondents based in North America believe larger firms will be most active. A financial advisor based in the US believes IPOs will attract “the most investor interest if they involve larger companies.”

Surv

ey F

Ind

InG

S

PAGE

06

www.mergermarket.com

Global IPO Market Outlook

In which percentage range do you expect most IPO premiums (the difference between the original offering price and the opening price) to fall over the next 12 months?

What percentage of IPOs do you expect to come from venture capital or private equity exits over the next 12 months?

Overall, 93% of respondents believe most premium rates will be below 20% this year, and nearly half of this group expects premiums to be 15% or lower. Remaining respondents have higher expectations, predicting that premiums will be in the 20% to 25% range.

Premiums are likely to depend on a number of factors this year. Interestingly, many respondents believe effective marketing pre-IPO can be especially influential, including a private equity practitioner based in France who explains, “Marketing of the planned IPO, as well a company’s reputation and its visibility, all play an important role.” Another private equity practitioner based in the UK believes that “growth always has the greatest impact on premium rates.”

Other respondents, including a US-based financial advisor, explain the causes of low premium rates: “Premiums often depend on whether the IPO has been priced perfectly. Over-pricing can lead to reduced demand which negatively affects premium rates.” Another explains, “IPO premiums often fall due to low investor demand and urgent need of cash.”

The largest percentage of respondents (37%) predict that 15% to 25% of IPOs announced this year will take the form of private equity or venture capital exits, while slightly more than one-quarter of respondents (27%) believe exits will account for 25% to 50% of IPOs over the next 12 months.

Exit activity will likely be higher in some regions than in others, as respondents have consistently pointed out that the North American region is seeing a far better valuation climate this year compared to last. This could make the upcoming 12 months an ideal time for North America-based private equity and venture capital firms to take their portfolio companies to market.

Survey FIndInGS

5%

37%

21%10%

27%

<5%

5% - 15%

15% - 25%

25% - 50%

50% - 75%

>75%

48%

45%

7% <15%

15% - 20%

20% - 25%

>25%

PAGE

07

www.mergermarket.com

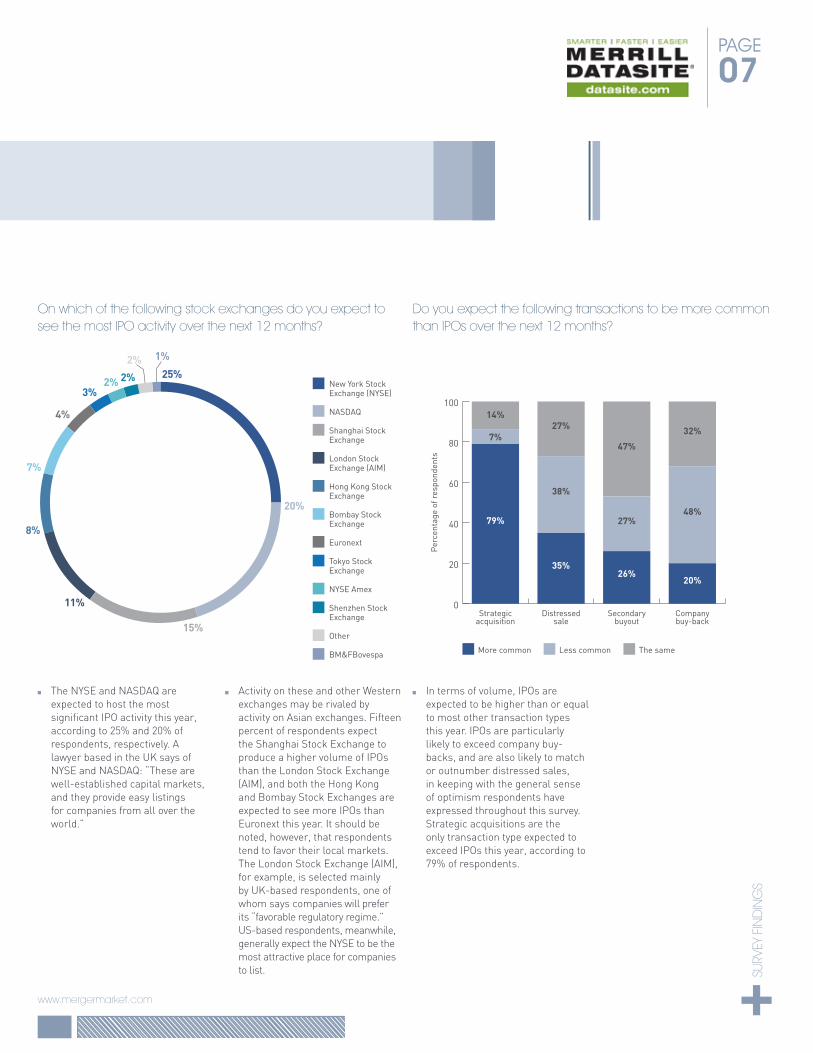

On which of the following stock exchanges do you expect to see the most IPO activity over the next 12 months?

The NYSE and NASDAQ are expected to host the most significant IPO activity this year, according to 25% and 20% of respondents, respectively. A lawyer based in the UK says of NYSE and NASDAQ: “These are well-established capital markets, and they provide easy listings for companies from all over the world.”

Activity on these and other Western exchanges may be rivaled by activity on Asian exchanges. Fifteen percent of respondents expect the Shanghai Stock Exchange to produce a higher volume of IPOs than the London Stock Exchange (AIM), and both the Hong Kong and Bombay Stock Exchanges are expected to see more IPOs than Euronext this year. It should be noted, however, that respondents tend to favor their local markets. The London Stock Exchange (AIM), for example, is selected mainly by UK-based respondents, one of whom says companies will prefer its “favorable regulatory regime.” US-based respondents, meanwhile, generally expect the NYSE to be the most attractive place for companies to list.

do you expect the following transactions to be more common than IPOs over the next 12 months?

In terms of volume, IPOs are expected to be higher than or equal to most other transaction types this year. IPOs are particularly likely to exceed company buy-backs, and are also likely to match or outnumber distressed sales, in keeping with the general sense of optimism respondents have expressed throughout this survey. Strategic acquisitions are the only transaction type expected to exceed IPOs this year, according to 79% of respondents.

0

20

40

60

80

100

Companybuy-back

Secondarybuyout

Distressedsale

Strategicacquisition

The sameLess commonMore common

79%

7%

14%

35%

38%

27%

26%

27%

47%

20%

48%

32%P

erce

ntag

e of

res

pond

ents

25%2% 1%

2%2%

8%

20%

4%

3%

7%

11%

15%

New York StockExchange (NYSE)

NASDAQ

Shanghai StockExchange

London StockExchange (AIM)

Hong Kong StockExchange

Bombay StockExchange

Euronext

Tokyo StockExchange

NYSE Amex

Shenzhen StockExchange

Other

BM&FBovespa

Surv

ey F

Ind

InG

S

PAGE

08

www.mergermarket.com

Global IPO Market Outlook

do you expect carve-outs, or “partial IPOs”, to be higher in volume than traditional IPOs over the next 12 months?

What do you think has been the primary reason for the recent cancellations of planned IPOs?

37%

21%42%

Yes

No

No difference

38%

26%

7%

19%

10%

Uncertainty orinstability infinancial markets

Inability toraise financing

Managementunwilling to completetransaction at priceindicated by investors

Insufficient demand

Sector-specificconditions

Thirty-seven percent of respondents believe carve-outs will exceed traditional IPOs in volume this year. Several respondents based in Europe say companies’ continuous restructuring efforts will lead to an increase in carve-outs, spin-offs and divestitures in general, as these transactions will appeal to firms looking to focus on their core operations. A lawyer based in the UK explains, “Companies want to concentrate on their core activities and divest their non-core businesses.”

Still, the largest percentage of respondents (42%) believe carve-outs and IPOs will be equally popular this year. A financial advisor based in Holland explains that “companies may resist carve-outs as they can be hard to complete and the process might be too complicated for many companies.”

The largest percentage of respondents (38%) cite uncertain or unstable financial markets as the primary reason for cancelled IPOs over the past year. Just over one-quarter of respondents believe cancellations reflect companies’ inability to raise financing. Close to one-fifth believe cancellations stem from valuation difficulties, with company management teams unwilling to complete transactions at investors’ proposed prices.

Respondents from the UK and Japan point out that management teams have held onto unrealistic prices over the past year and have been reluctant to negotiate. But these companies may be in a better position to achieve their desired offering prices in the near future if investor confidence does indeed improve in the coming months.

Survey FIndInGS

PAGE

09

www.mergermarket.com

When do you expect the companies that have delayed a planned IPO to enter the market again?

3%

53%

17%5%

1%

21%

<3 months

3 - 6 months

6 - 12 months

12- 18 months

18- 24 months

>24 months

Most respondents (53%) believe companies that have put off their IPO plans will continue to do so for 6 to 12 months. A corporate executive based in the US explains, “Usually when a company pulls back an IPO they stay private for 12 to 18 months out of fear of rejection or lack of investor interest.” One-fifth of respondents believe delayed IPOs will materialize sooner rather than later, however, predicting that companies with delayed offerings will enter the market again in the next 3 to 6 months.

For potential issuers, which of the following will be the most important factor in selecting an underwriter?

32%

12%

26%

14%

16%

Industryexpertise

Reputation

Reputation ofunderwritingfirm’s industryanalyst

Outsiderelationshipsor contacts

Experience orvolume oftransactions

Issuers’ selection of an underwriter depends primarily on industry expertise and reputation, according to 32% and 26% of respondents, respectively. More specifically, 16% of respondents say the reputation of an underwriting firm’s industry analyst can be a selling point for potential issuers.

Respondents offer further insight into these factors, with one private equity practitioner based in Japan stating that underwriters must have experience in the issuer’s industry in order to “understand the type of company it is working with.” Other respondents, including two private equity executives based in Europe and the US, say an underwriting firm’s outside relationships are critical, as firms with strong relationships can often facilitate more investor interest than a firm with limited ties to potential investors.

www.mergermarket.com

Global IPO Market OutlookPAGE

10

On average, how much time do underwriters spend on due diligence in the pre-filing phase?

Pre-filing due diligence typically lasts from 1 to 3 months, with 48% of respondents citing a time range of 1 to 2 months and 29% of respondents citing a period of 2 to 3 months. A 10% minority of respondents report that due diligence in the pre-filing phase often exceeds 3 months, and many of these respondents believe economic conditions of the past year have led to lengthier due diligence procedures.

For potential investors, which of the following will be the most important factor in deciding whether to back a new IPO?

Not surprisingly, one-half of respondents believe financial performance is the primary factor influencing investors’ willingness to back a company’s IPO. Given continuous economic uncertainty, however, a corporate executive based in the US explains that a company’s financial performance may be difficult to gauge: “Earnings volatility and uncertainty have made it impossible to make normal predictions.”

Approximately one-fifth of respondents say sector-specific conditions will play a major role as well. A respondent based in Europe cites the healthcare sector as an example of an industry where favorable conditions are likely to stimulate investor interest: “There is a lot of space open for developing new medicines, the ageing population is fueling demand, and in general there are a number of smaller and larger entities looking for expansion.”

Survey FIndInGS

50%6%

21%

7%

16%

Financialperformance

Sector-specificconditions

Strength ofmanagementteam

Informationpresentedduring marketingperiod or“road show”

Informationpresentedin prospectus

13%

10%

29%

48%

<1 month

1 - 2 months

2 - 3 months

>3 months

www.mergermarket.com

PAGE

11

In your experience, has the due diligence process become more rigorous over the past two years?

The overwhelming majority of respondents say the due diligence process has become more rigorous in recent years, which is to be expected as issuers and investors adjust to new market realities. Indeed, many respondents say a heightened sense of caution in the business community overall has made due diligence processes more comprehensive. A lawyer based in the UK explains, “People are hesitant to invest in the market unless they completely investigate the hidden risk.” A financial advisor based in the US agrees, pointing out that “as a result of recent scandals, investors want to make sure the assets shown to them are genuine.”

Newly-listed firms are under considerable pressure as they transition into public companies, and respondents are fairly evenly divided as to which challenges are most significant. Over one-third of respondents (34%) say managing relationships with investors is the most significant challenge for newly-listed companies, followed closely by 30% of respondents who say newly-listed companies struggle most with implementing new growth strategies. An additional 23% of respondents say these companies tend to struggle most with new regulatory standards.

Which of the following typically poses the greatest challenge to newly-listed companies?

90%

10%Yes

No

34%

30%23%

13%

Managingrelationships withstakeholders/shareholders

Implementing newgrowth strategies

Complying withpublic companyregulations

Retainingkey talent

Surv

ey F

Ind

InG

S

www.mergermarket.com

Global IPO Market OutlookPAGE

12

Approximately one-third of respondents (31%) believe the stock price of a newly-listed firm is influenced most heavily by public perception, while other respondents are nearly evenly divided between investor relations (28%) and the stock’s performance immediately following its listing (26%).

A financial advisor based in Germany explains that all of these factors play a major role, and points out that newly-listed companies are still adjusting to increased visibility during the first 3 to 4 months: “The actual business performance after listing, how well the company is doing at implementing its strategy post-listing, are all on full display.”

In your experience, which of the following has the greatest influence on a newly-listed company’s stock price in its first 3 to 4 months?

Survey FIndInGS

31%

28%26%

15%

Public perception

Relationshipswith investors

Stock priceperformanceimmediatelyfollowing listing

Success of post-IPOstrategy

www.mergermarket.com

PAGE

13

datasite.com

M E R R I L L D A T A S I T E ®

“We need a faster,more efficient way tostore and accesscritical business information

without relying onpaper documents.”

We thought of that.

Locate the documents you need in a matter of seconds with Merrill DataSiteTM. These days, it seems thateverybody wants instant answers. That’s why so many companies rely on the Merrill DataSite online documentwarehousing solution to simplify information storage and management. We make it easy to transform thousands – or millions – of paper documents into a secure, virtual document library that is accessible aroundthe clock to authorized users via the Internet worldwide.

Best of all, you don’t have to be an expert to get started. Merrill DataSite’s expert project managers are available24-7 to help you. We’ve helped clients launch thousands of virtual document libraries of all sizes – valuable experience that we’ll put to work for you.

At Merril DataSite, we believe in sharing ideas and best practices that assist companies in expanding and capturing new opportunities. To download our FREE industry survey reports please visit the Merrill DataSite Knowledge Center at www.datasite.com.

www.mergermarket.com

Global IPO Market Outlook

0

50

100

150

200

250

300

350

400

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Num

ber

of d

eals

European buyouts

European exits

PAGE

14

HIstorICal data

European M&A quarterly private equity trend

North American M&A quarterly private equity trend

value

value

volume

volume

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Valu

e (€

m)

European buyouts

European exits

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Valu

e (U

S$m

)

North American buyouts

North American exits

0

25

50

75

100

125

150

175

200

225

250

275

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Num

ber

of d

eals

North American buyouts

North American exits

PAGE

15

www.mergermarket.com

Asia-Pacific M&A quarterly private equity trend

value volume

0

5,000

10,000

15,000

20,000

25,000

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q1 04

Valu

e (U

S$m

)

Asia-Pacific buyouts

Asia-Pacific exits

0

20

40

60

80

100

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Num

ber

of d

eals

Asia-Pacific buyouts

Asia-Pacific exits

Latin American M&A quarterly private equity trend

value volume

0

500

1,000

1,500

2,000

2,500

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Valu

e (U

S$m

)

Latin American buyouts

Latin American exits

0

3

6

9

12

15

Q210*

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Q404

Q304

Q204

Q104

Num

ber

of d

eals

Latin American buyouts

Latin American exits

www.mergermarket.com

Global IPO Market Outlook

www.mergermarket.com

about MerrIll CorPoratIon

www.datasite.com

PAGE

16

Merrill transaction and Compliance servicesThrough a broad range of tools and services, Merrill Corporation streamlines document composition, filing, printing, distribution and electronic access to the transaction and regulatory compliance activities of its clients engaged in securities offerings, reorganizations, mergers and acquisitions, SEC and other regulatory filings. As a registered, third-party service provider offering public companies expert EDGARization and XBRL filing services, Merrill professionals can compose, edit, electronically file, manage and distribute data in printed or electronic format.

Merrill’s Legal Solutions provide both on-demand and on-site litigation support, information management and electronic and print document management services for law firms, corporate legal departments and professional services firms. Examples of our expertise include the creation of searchable litigation document repositories, management of electronic data discovery and the delivery of real-time court reporting and deposition videography services.

Merrill’s Marketing and Communication Solutions supply brand identity management, customer communication and packaged direct marketing programs for sales professionals in industries such as real estate, mutual funds and insurance. Examples of our services include customizable corporate identity materials, direct-mail marketing pieces and promotional programs supported by web-based technologies.

Merrill’s Translations Services provide a range of translation options to help clients achieve the most efficient and cost effective approach to their translation projects. Merrill Brink offers extensive legal translation services for international litigation, intellectual property, patents, contractual matters, antitrust matters, mergers and acquisitions, arbitration and more.

about Merrill datasite®

Revolutionizing the due diligence process Merrill DataSite is designed for rapid deployment and can be up and running within two hours of a client’s need. Our team can scan, upload and organize thousands of pages of content from any source in 24 hours or less. Every aspect of the process, from document scanning to VDR hosting and project management is delivered by Merrill’s multilingual team, available around the clock worldwide.

With Merrill DataSite, all documents are captured and indexed to an online database and because all rights are designated by the client, security and control are guaranteed. Each user’s ability to view, print or access source documents is set up by the client administrator and can be changed at any time. Merrill DataSite provides useful tools including full search, viewer audit capability, Q&A and detailed user activity tracking that help clients maintain tighter control and have greater insight into reviewer behavior.

Merrill DataSite enhances transaction success Merrill DataSite is the industry’s acknowledged leader. More than 61,000 different private and public companies across the globe have leveraged Merrill DataSite to increase the value of the following types of transactions:

Mergers, acquisitions and divestitures

Private placement transactions

Leveraged buyout transactions

Bankruptcy and reorganization transactions

Financial restructuring transactions

Initial public offerings and dual-track processes

Asset purchases and liquidations

Post-merger integration

Founded in 1968 and headquartered in st. Paul, Minnesota, Merrill Corporation is a leading provider of outsourced solutions for complex business communication and information management. Merrill’s services include document and data management, litigation support, language translation services, fulfillment, imaging and printing. Merrill serves the corporate, legal, financial services, insurance and real estate markets. with more than 5,000 people in over 70 domestic and 15 international locations, Merrill empowers the communications of the world’s leading organizations.

www.mergermarket.com

PAGE

17

about MerrIll datasIte®

Merrill datasite - built with the client in mindMerrill DataSite was created to meet its clients’ needs and built to their specifications. Since 2002 we have consistently leveraged the experiences of our clients to add leading-edge functionality to the available toolset. Merrill DataSite allows its users and administrators to:

Examine documents immediately. Patented technology ensures you never have to wait for a document to be downloaded. Because the data resides on Merrill’s servers, you can simultaneously view an unlimited number of documents in multiple windows without having to close out or save to your “temp” file. When faced with hundreds of documents to review, this feature saves significant time and expense.

Designate user permissions. Team administrators can control which users will be able to view, print or download specific documents, folders or projects - simply and quickly.

Search every word in every document. With large document collections, sophisticated search features are key to finding critical information and accelerating the due diligence process. Merrill DataSite boasts the latest search technology. Optical Character Recognition (OCR) is applied to each processed page, so that the data room is fully text- and title-searchable. With a simple right click, the powerful search engine can locate strings of characters, and using fuzzy logic, will return search results from the entire data room in ranked order. Furthermore, the engine is fault tolerant and allows for spelling errors while returning results. Merrill DataSite also provides advanced concept and pattern search features to allow synonyms and misspellings to be incorporated into query results.

Protect confidential information. ”View-only” documents are never downloaded. Merrill DataSite, not the computer’s browser, controls the caching process providing unmatched security levels. Unlike other VDR providers, images are never viewable on the PC’s cache after the conclusion of a session.

Track all activity accurately. Auditing and reporting tools provide a verifiable accounting of each individual’s time spent viewing both documents and specific pages – information that adds negotiating leverage.

need to work remotely?No problem. Whether you’re working in Beijing or New York, you can view your documents online without having to navigate through internal firewalls and email restrictions that often exist for outside company connections and delay the due diligence process.

security is our highest priorityMerrill has been a trusted provider of secure information to the financial and legal industries for more than 40 years. Our employees execute letters of confidentiality and we are audited annually (internal and third-party) to make certain our IT infrastructure and processes remain sound. Merrill DataSite was the first virtual data room to receive the ISO 27001 certification for its comprehensive Information Security Management System (ISMS). The ISO 27001 standard, developed by the International Organization for Standards to establish international requirements for information security and certification of ISMS, is designed to ensure effective protection of information assets in foreign markets, as well as across national and regional boundaries.

the best tool in the industryMerrill DataSite technology allows for the fastest conversion of soft and hard copy documents to the electronic viewing platform. As a result, designated administrators are able to review documents the moment they are available.

Through secure, simultaneous access, full text search capabilities and robust reporting tools, both archival and transactional due diligence processes are streamlined. As a result, Merrill DataSite gives you more insight and control, and dramatically reduces transaction time and costs.

As a leading provider of VDR solutions worldwide, Merrill DataSite has empowered nearly 1.6 million unique visitors to perform electronic due diligence on thousands of transactions totalling trillions of dollars in asset value.

www.datasite.comsmarter, Faster, easier!

www.datasite.com

www.mergermarket.com

Global IPO Market OutlookPAGE

18

www.mergermarket.com

MerrIll ContaCtsMerrill DataSite (Division of Merrill Corporation) ContactsTel: +44 20 7422 6100 (Europe) 1.888.867.0309 (US)

executive Management

Ed Bifulk President Tel: +1 212 229 6563

Paul Hartzell Senior Vice President Tel: +1 212 367 5950

executive sales

Chris Beckmann Regional Director, Europe Tel: +49 69 25617 110

Will Brown Regional Director, Europe Tel: +44 20 7422 6100

Ana Paula Macêd Távora de Castro Regional Director, South America Tel: +55 11 9908 0858

Manuel Bentosinos Regional Director, Mexico Tel: +52 55 9171 2237

Alex Gross Regional Director, Europe Tel: +49 69 25617 199

Michael Hinchliffe Regional Director, Europe Tel: +44 20 7422 6100

Ari Lee Regional Director, Greater China Tel: +852 9855 3758

Merlin J. Piscitelli Regional Director, Europe Tel: +44 20 7422 6100

Jérôme Pottier Regional Director, France Tel: +33 (0) 1 40 06 13 12

Colin Schopbach Regional Director, Europe Tel: +44 20 7422 6100

Anna Scott Regional Director, Europe Tel: +44 20 7422 6100

John McElrone Regional Director, New York Tel: +1 212 229 6656

Steve Piccone VP, New York Tel: +1 212 229 6883

Shelle Martin Regional Director, New York Tel: +1 212 229 6613

William Polese Regional Director, New York Tel: +1 212 229 6612

Adam Kuritzky Regional Director, New York Tel: +1 917 934 7340

Forrest R. Doane Regional Director, New York Tel: +1 917 934 7341

Matthew Mezzancello Regional Director, New York Tel: +1 917 934 7346

Michael Kennedy Regional Director, Boston Tel: +1 207 829 4369

Mark Plaehn Regional Director, Chicago Tel: +1 312 674 6527

Anthony Crosby Regional Director, Chicago Tel: +1 312 674 6511

Kelly Jackowski Regional Director, Chicago Tel: +1 312 674 6508

Paul Kleinkauf Regional Director, Southeast Tel: +1 404 602 3251

Dan Phelan Regional Director, Los Angeles Tel: +1 213 253 2139

Brian Gilbreath Regional Director, Omaha Tel: +1 404 934 8085

Jay Loyola Regional Director, Irvine Tel: +1 949 622 0663

Nicholas Renter Regional Director, Dallas Tel: +1 214 754 2100

Ryan MacMillan Regional Director, Canada Tel: +1 416 214 2448

Andrew Buonincontro Regional Director, Palo Alto Tel: +1 650 493 1400

Hank Gregory SVP, Western Canada & US Tel: + 604 603 4360

Mark Tully Regional Director, Palo Alto +1 650 493 1400

Erik Sandie Regional Director, Palo Alto +1 650 493 1400

Notes

mergermarket is an unparalleled, independent Mergers & Acquisitions (M&A) proprietary intelligence tool. Unlike any other service of its kind, mergermarket provides a complete overview of the M&A market by offering both a forward-looking intelligence database and an historical deals database, achieving real revenues for mergermarket clients.

Any queries regarding this publication or the data within should be directed to:

Erik Wickman Director, Remark Americas Tel: +1 212 686 3329 [email protected]

notes and ContaCts

PAGE

19

www.merrilldatasite.com www.mergermarket.com

www.datasite.com

disclaimer

This publication contains general information and is not intended to be comprehensive nor to provide financial, investment, legal, tax or other professional advice or services. This publication is not a substitute for such professional advice or services, and it should not be acted on or relied upon or used as a basis for any investment or other decision or action that may affect you or your business. Before taking any such decision you should consult a suitably qualified professional adviser. Whilst reasonable effort has been made to ensure the accuracy of the information contained in this publication, this cannot be guaranteed and neither Mergermarket nor any of its subsidiaries nor any affiliate thereof or other related entity shall have any liability to any person or entity which relies on the information contained in this publication, including incidental or consequential damages arising from errors or omissions. Any such reliance is solely at the user’s risk.

11 West 19th Street, 2nd FloorNew York, NY 10011USA

t: +1 212 686-5606f: +1 212 [email protected]

80 StrandLondon, WC2R 0RLUnited Kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]

Suite 2001Grand Millennium Plaza181 Queen’s Road, CentralHong Kong

t: +852 2158 9700f: +852 2158 [email protected]