60

Global market review of automotive roof systems – forecasts to 2011 2005 edition

Global market review of automotive roof systems

– forecasts to 2011

2005 edition

Page i

Global market review of automotive roof systems – forecasts to 2011 3rd edition by Matthew Beecham

July 2005

Published by

Aroq Limited Seneca House

Buntsford Park Road

Bromsgrove

Worcestershire

B60 3DX

United Kingdom

Tel: +44 (0)1527 573 600

Fax: +44 (0)1527 577 423

Web: www.just-auto.com

Registered in England no: 4307068

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page ii

Multi-user licence edition

This report is provided with a cost-effective multi-user licence and can be

freely and legally shared with your colleagues. This agreement includes

sharing electronically via your corporate intranet or the making of physical

copies for your company library. Excluded from this agreement is sharing any

part of this publication with, or transmitting via any means to, anybody outside

of your company. For further details regarding the terms of this licence please

contact:

Rebecca Rice Sales and marketing, just-auto.com

Tel: +44 (0)1527 573 605

Fax: +44 (0)1527 577 423

Email: [email protected]

Copyright statement

© 2005 All content copyright Aroq Limited. All rights reserved.

This publication, nor any part of it, may be copied, reproduced, stored in a

retrieval system, or be transmitted in any form by any means electronic,

mechanical, photocopying, recording or otherwise, for or to persons not

employed directly by your company, without the prior permission of Aroq

Limited. This report is the product of extensive research work. It is protected by

copyright under the Copyright, Designs and Patents Act 1988.

Aroq Limited offers a reward of £1,000 for information leading to the successful prosecution for illegal copying of this document.

The authors of Aroq Limited research reports are drawn from a wide range of

professional and academic disciplines. The facts within this report are believed

to be correct at the time of publication but cannot be guaranteed. All

information within this study has been reasonably verified to the author’s and

publisher’s ability, but neither accept responsibility for loss arising from

decisions based on this report.

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page iii

Table of contents

Multi-user licence edition............................................................................................................... ii Copyright statement .................................................................................................................. ii

Table of contents ........................................................................................................................... iii

List of tables .................................................................................................................................... v

List of figures ................................................................................................................................. vi

just-auto.com’s research portfolio .............................................................................................. vii Incredible ROI for your budget – single and multi-user licences..............................................vii

just-auto.com membership ......................................................................................................... viii

Chapter 1 Introduction.................................................................................................................... 1 Let’s start from the top .............................................................................................................. 1 Report coverage........................................................................................................................ 1

Chapter 2 The market ..................................................................................................................... 3 Market players........................................................................................................................... 3

ArvinMeritor ...................................................................................................................... 3 ASC .................................................................................................................................. 3 Bertone ............................................................................................................................. 8 Car Top Systems.............................................................................................................. 8 Edscha.............................................................................................................................. 8 Heuliez.............................................................................................................................. 8 Inalfa................................................................................................................................. 9 Karmann ........................................................................................................................... 9 Pininfarina......................................................................................................................... 9 Webasto ......................................................................................................................... 10

Mergers, acquisitions and joint venture activity ...................................................................... 10 Capital investment activity ...................................................................................................... 12 Market shares ......................................................................................................................... 12 Market forecasts...................................................................................................................... 15

Sunroof market ............................................................................................................... 15 Convertible roof market........................................................................................................... 19

Chapter 3 Technical review.......................................................................................................... 24 Roof trends.............................................................................................................................. 24 Retractable hard-tops.............................................................................................................. 26 Convertibles ............................................................................................................................ 29 Roof modules .......................................................................................................................... 30

Chapter 4 Manufacturers.............................................................................................................. 32

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page iv

ArvinMeritor............................................................................................................................. 32 ASC......................................................................................................................................... 33 Bertone.................................................................................................................................... 35 Car Top Systems .................................................................................................................... 35 Edscha .................................................................................................................................... 39 Heuliez .................................................................................................................................... 40 Inalfa Roof Systems BV .......................................................................................................... 42 Karmann.................................................................................................................................. 44 Pininfarina ............................................................................................................................... 48 Webasto .................................................................................................................................. 48

Online sources of information ..................................................................................................... 50 Free email newsletters ............................................................................................................ 50 Other research reports ............................................................................................................ 50 Global news and feature articles............................................................................................. 50 Search the web ....................................................................................................................... 50

Your feedback ............................................................................................................................... 51

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page v

List of tables

Table 1: Production of conventional-size sunroofs for light vehicle applications in Western Europe,

Japan, North America, 2000-2011¹ ² (Units, ‘000s) .................................................. 16

Table 2: Market value of conventional-size sunroofs for light vehicle applications in Western

Europe, Japan, North America, 2000-2011 (US$ ‘000s) .......................................... 17

Table 3: Production of large sunroofs for light vehicle applications in Western Europe, Japan,

North America, 2000-2011 (Units, ‘000s) ................................................................. 18

Table 4: Market value of large sunroofs for light vehicle applications in Western Europe, Japan,

North America, 2000-2011 (US$ ‘000s) ................................................................... 19

Table 5: Production of convertible roof systems in Europe and North America, 2003 and 2008

(units)........................................................................................................................21

Table 6: UK convertible car market registrations, 1994 – 2004 ..................................................... 22

Table 7: European convertible vehicle registrations, UK, Germany, France, Italy and Spain, 1999

– 2003....................................................................................................................... 23

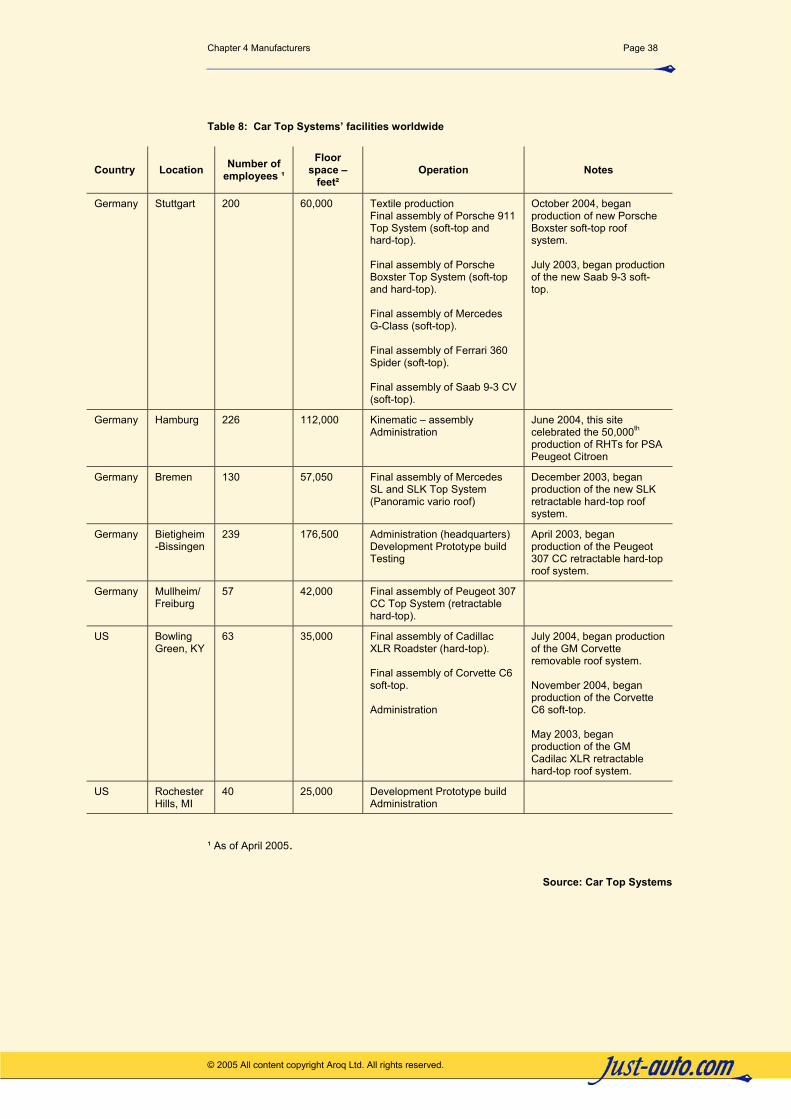

Table 8: Car Top Systems’ facilities worldwide.............................................................................. 38

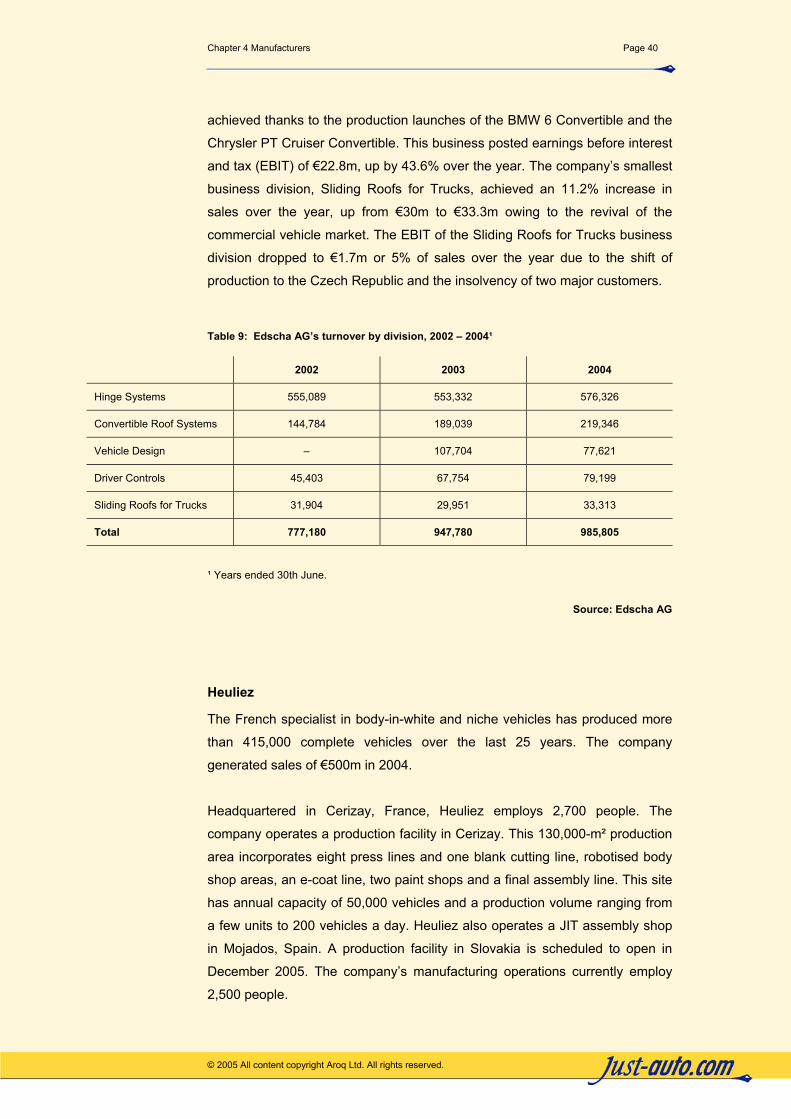

Table 9: Edscha AG’s turnover by division, 2002 – 2004¹ ............................................................. 40

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page vi

List of figures

Figure 1: Global market shares for vehicle sunroofs, 2004 (% of production volume) .................. 13

Figure 2: European OE market shares for vehicle sunroofs, 2004 (% of production volume) ....... 14

Figure 3: North American OE market shares for sunroofs, 2004 (% of production volume).......... 15

Figure 4: Opel Tigra TwinTop ........................................................................................................ 27

Figure 5: ArvinMeritor’s roof module with sunroof.......................................................................... 33

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page vii

just-auto.com’s research portfolio

just-auto.com has been providing timely auto industry intelligence to the

automotive industry globally since 1999. We use only experienced and

respected authors to publish our portfolio of automotive component sector

reports. Our approach is to cover niche technology sectors - often at a module

level, such as roof systems or fuel injection systems, to provide you with the

best available analysis at a good-value price point.

All of the reports in our growing portfolio, many in their 2nd or 3rd editions, give

you an essential overview of a sector. Each study profiles the key players,

assesses which technologies are being developed, and gives you other

essential intelligence including market share data, forecasts and exclusive

interviews with relevant senior executives.

A full list of available reports is online at www.just-auto.com/store

Incredible ROI for your budget – single and multi-user licences

We understand the pressure your research budget is under and price our

reports realistically. You won't find our reports with four, or even five-figure

price tags, but you will find that they make some of the competition look

expensive.

Each title is available to you on a single-user basis, supplied on the strict

understanding that each title is not to be copied or shared. Alternatively, titles

can be shared within departments or entire corporations via a cost-effective

multi-user licence. Multi-user licences can also save you money by avoiding

unnecessary order duplication. To further add value, all multi-user copies are

hosted on a password protected extranet for your department or company -

saving you time, resources and effort when sharing research with your

colleagues. To find out more about multi-user pricing please contact:

Rebecca Rice, research manager, just-auto.com

Tel: +44 (0)1527 573 605 Fax: +44 (0)1527 577 423

Email: [email protected]

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page viii

just-auto.com membership

As a 'consumer' of automotive research, just-auto site membership will be

especially valuable to you. For just £125 / $195 / €175* a year you will gain

access to a growing portfolio of exclusive management briefing reports, and

also receive 12 new reports for each year you are a member.

These reports are between 5,000 and 10,000 words and give you fresh insight

into diverse sectors such as retailing, transmissions, x-by-wire, aftermarket

issues and emerging markets.

As well as this impressive list of members' only reports, you also gain one

year’s access to a constantly updated stream of news, feature articles and

analysis at www.just-auto.com. Established in 1999, just-auto.com has

rapidly evolved into the premier source of global automotive news, analysis

and data for busy senior executives.

In addition, membership gives you full access to four years of news and

feature archives, key news headlines from around the web and your own email

alerting tool - AMANDA. In short, a one-stop shop for global automotive

intelligence.

For further details of this month’s special joining offer visit:

www.just-auto.com/offer.asp * Prices correct at time of publication.

© 2005 All content copyright Aroq Ltd. All rights reserved.

Chapter 1 Introduction

Chapter 1 Introduction

Page 1

© 2005 All content copyright Aroq Ltd. All rights reserved.

Let’s start from the top

Three roof design trends are notable:

○ First – the sheer size and sophistication of the products. Panoramic

sunroofs stretching the length and breadth of a vehicle are becoming

increasingly popular on both sides of the Atlantic.

○ Second – roof systems are fast becoming part of a car’s identity. For

example, the most eye-catching design feature on the Citroen C3 Pluriel is

the multi-function roof system, which allows the car to be a cabriolet,

spider, saloon and pickup.

○ Third – roof systems are developed along modular lines with suppliers

hoping that car manufacturers will begin standardising roofs to allow a

variety of pre-sized modules to fit the openings.

Despite the Japanese convertible market lagging behind Europe and North

America, open-top cars appear to be making a comeback. The quality of soft-

top designs has also improved significantly over the last decade. Better quality

materials have brought benefits in acoustics and cabin temperatures, enabling

us to drive soft-tops in comfort all year round. They can even be driven through

a car wash without any problems.

The trend toward more convertibles and open-top vehicles has created more

opportunities for suppliers. While Inalfa, ArvinMeritor and Webasto are

focussing on panoramic roofs, coachbuilders such as Karmann, Heuliez and

Pininfarina are concentrating on developing open-air roofs for mass

production.

Report coverage

In this third edition report, just-auto extends the analysis to provide market

volume and value forecasts by product segment for conventional-size sunroofs

in Western Europe, North America and Japan, from 2000 through 2011. We

Chapter 1 Introduction Page 2

© 2005 All content copyright Aroq Ltd. All rights reserved.

also take a closer look at the size of the convertible market in Europe and

North America, the reasons for growth including an exclusive interview with

ASC. In addition to highlighting the main market trends in roof systems,

chapter two identifies the main players and OE sunroof market shares. This

section concludes with a roundup of recent merger, acquisition and capital

investment activity. Chapter three reviews the technical advances in

conventional and large sunroofs. It also reviews the latest retractable hard-top

designs and roof modules. Chapter four provides brief profiles of the major roof

system manufacturers, namely, ArvinMeritor, ASC, Bertone, Car Top Systems,

Edscha, Heuliez, Inalfa, Karmann, Pininfarina and Webasto.

Chapter 2 The market

Chapter 2 The market

Page 3

© 2005 All content copyright Aroq Ltd. All rights reserved.

Market players

ArvinMeritor ArvinMeritor is one of the world's leading independent suppliers of sunroofs

and roof systems products for use in passenger cars, light trucks and sport

utility vehicles, including its Golde brand sunroofs. The company makes

complete roofs, some of which incorporate sunroofs that provide OEMs with

cost savings by reducing assembly time and parts. Its roof system

manufacturing facilities are located in North America and Europe. In late 2004,

the company formed a joint venture with Shanghai SIIC Transportation

Electronic Co Ltd to manufacture passenger vehicle sunroofs for a VW facility

in Shanghai, China.

ASC American Specialty Cars (ASC) is looking to emulate the success of European

styling and engineering houses such as Pininfarina, Karmann, Valmet and

Bertone by expanding into Europe and China. Formerly known as the

American Sunroof Company, ASC has kept its initials but re-invented itself

over the past two years as a specialist body engineering company for low

volume production vehicles.

The company has almost entirely come out of the sunroof business apart from

its joint venture with Yachio at Columbus, Ohio while it has also retained its 20-

year association with Toyota with the roof system on the Solara and with

Mitsubishi on the Eclipse. It sees China as a real opportunity and has already

been contracted by one North American manufacturer to design a line of

vehicles specifically for the Chinese market.

At the 2005 Detroit motor show, ASC showcased five concept vehicles

including a convertible version of the Chrysler 300 Hemi C, the first four-door

open-top since the Lincoln Continental of 1967. ASC took the current 300

Hemi C production body and conducted a full engineering exercise to ensure

that the concept had the necessary stiffness and was able to meet all the

safety standards of the production car. Europe is another hunting ground for

Chapter 2 The market Page 4

© 2005 All content copyright Aroq Ltd. All rights reserved.

growth, although the company accepts the competition there is greater and the

market more fragmented. ASC in its previous existence used to have

operations in Germany for Porsche and retains a small office in Ingolstadt to

liaise with manufacturers in the country. Growth in Europe would probably be

through a mixture of organic growth, acquisitions or joint ventures.

In 2002, the family of ASC’s late founder, Heinz Prechter, agreed to sell the

company to Questor Partners Fund II. Questor is a private-equity fund headed

by turnaround expert Jay Alix. ASC is now 100% privately held by Questor.

Exclusive interview with ASC

In an interview with just-auto, this report’s author Matthew Beecham talked

with Jeff Steiner, executive vice president and chief marketing officer, about

how the company has developed since Questor took over and how it is aiming

to extend its geographical reach.

just-auto: As we see it, ASC is in the throes of moving from an entrepreneurial

company – whose success was highly dependent on the abilities of its late

founder, Heinz Prechter – to a professionally managed one which relies on

technical capabilities, process and financial discipline to improve continuously.

Jeff Steiner: I would agree with that. Heinz Prechter was a very intelligent and

charismatic man with great vision. He spent a lot of time carrying the company

on his personal energies. But today, some of our [new] leadership [team] has

come from the automakers and tier one suppliers. So we are used to working

as one. We are looking at this more as a company that is dependent on its

processes and systems than on any one individual. The acquisition by Questor

has been a very positive move for ASC, enabling the company to grow.

Questor invested money into the company, which has allowed us to fund an

aggressive new product development group, focus our R&D and

manufacturing processes.

j-a: Why are we seeing a resurgence of convertibles in the US?

Jeff Steiner: There are a couple of reasons for that. The first is due to the

current hyper-segmentation of the market. Automakers are looking for unique

features that are causing consumers to rush into a showroom and buy a car.

The second relates to the need to have fun in your vehicle. Some recent

Chapter 2 The market Page 5

© 2005 All content copyright Aroq Ltd. All rights reserved.

research estimated that 42% of the US market buys cars strictly on value-

based transportation needs. In other words, these consumers are not style-

conscious; they want basic, reliable transportation. [But] then the remaining

58% of the market are influenced by styling and perception. This group is

looking for more fun, style and emotion from their vehicle. Convertibles are a

way to achieve both. For automakers, it is a way to differentiate their product

line as well as add a little bit more fun and excitement for those consumers

looking for that.

j-a: ASC showcased its Helios four-door convertible concept at the Detroit auto show last January. And yet four-door convertibles have been extinct for 40 years. Why now?

Jeff Steiner: I think there are two reasons. The four-door convertible is first

and foremost a body-engineering challenge to make it work. We knew we

could put a convertible top on it – that was the easy part. The hard part was

whether we could make the body stiff enough to make a prototype. Our goal

for the [2005 Detroit] motor show was that we wanted an engineered,

production-feasible prototype that we could show and drive. It was a learning

laboratory for us. To my mind, there were three key things that came out of

that project.

The first is that we believed that we could do a four-door convertible on a rear-

wheel-drive architecture utilising a lot of the patents on the structural rigidity

elements that we put into it. So any rear-wheel-drive platform using our

structural technology could become a four-door convertible.

The second element is that a lot of those structural discoveries can also be

used on a two-door convertible because any convertible has an inherent

challenge in keeping the body as stiff as you would like it to be.

And the third element relates to the top system. Because we are trying to

package an enormous top into a very small package, we have a patent-

pending, inward-folding top mechanism which basically allows you to take a 2-

metre-long top and package it into a 0.5-metre space. That again can be

applied to smaller two-door convertibles. So on the 300 Hemi C production we

didn’t change the rear decklid at all to package that top. When the top is down

and you open the trunk, you can put four golf bags plus a few small suitcases.

Chapter 2 The market Page 6

© 2005 All content copyright Aroq Ltd. All rights reserved.

j-a: And you are targeting baby boomers for this system?

Jeff Steiner: Yes. Those consumers in their late 40s and early 50s are the

prime age to have a vehicle like this. We see a tremendous amount of wealth

in the US among that demographic group who are looking for fun vehicles.

j-a: What are the considerations you give when setting out to develop such a concept? I.e. for any company, this type of activity costs a lot of money and it also means you have to ramp up your skills as a supplier at the consumer level as well.

Jeff Steiner: We measure innovation not on the number of cool ideas we

create but on the cool ideas created that actually have true market value. We

use a process called Planned Innovation. It means you spend a lot of time

understanding the market need and target price in order for that to be

successful in the market. Once we establish that, we then have greater

confidence in spending serious money on engineering and developing it. The

Helios project started in November 2003 with the goal of showcasing it just

over a year later at the Detroit auto show in January 2005. Following the

Planned Innovation process, we took just over two months of upfront study of

setting the technical and financial targets in order to determine whether or not

it was possible to engineer a four-door convertible. We then invested some

heavy money to initiate the engineering work and prove out our theory. There’s

no point in spending US$10m on two really cool ideas only to discover that

nobody wants them.

j-a: What are the trends you are seeing in sunroof designs? Jeff Steiner: I think the general observation is that bigger equals better. The

challenge is weight: you are putting more weight on the roof, which for SUVs

and high centre of gravity vehicles is not a good thing. The second thing in a

lot of cases is the overall sun loading of a car. If you have a huge glass

panelled roof, that presents a problem from a heat-loading standpoint.

We are also seeing more combinations of fixed glass and moving glass roofs

because it is a feature that you need to experience. Once you experience a

vehicle with a lot of glass or an open-air vehicle and you can manage some of

the heat loads, you find that that is a very desirable feature that a consumer

wants for their next vehicle.

Chapter 2 The market Page 7

© 2005 All content copyright Aroq Ltd. All rights reserved.

j-a: Do you have any plans for international expansion?

Jeff Steiner: We are looking at growth opportunities in Europe as well as Asia.

The Chinese and Korean markets cannot be ignored. But the European market

is more mature. There are some good and well-established players that are

similar to ASC that are located in Europe such as Pininfarina and Karmann.

We continue to have discussions with European automakers primarily about

opportunities that they have in Europe as well as in the US. And in order for us

to be successful in meeting their needs, we are evaluating either partnering

with or setting up our own operations that support those European OEMs,

primarily from an engineering and design standpoint. And then if the right

opportunity presented itself, also from a manufacturing standpoint. Time will

tell and opportunities will dictate whether we do that or not.

j-a: What was the background to ASC’s decision to split the 50/50 joint venture with Germany’s Edscha, known as Premier Roof Systems?

Jeff Steiner: Edscha is a very reputable company. The joint venture was

formed in the US to supply BMW. Whenever you have a joint venture formed

by two companies in a market place where both have chosen to compete, it

becomes a challenge to manage that venture. It came to a point where both

companies were not putting in their best resources or effort into that particular

facility. We agreed that in order for that facility to continue to grow and

maintain good customer relationships with BMW, the best thing was to split it

into either a wholly-owned ASC component or Edscha component. We

mutually concluded that it made sense for Edscha to purchase that joint

venture.

In a news release issued in January 2005, Edscha said: “Two and a half years

after the BMW Z4 went into production, Edscha is now running the plant and

the project on its own. For Edscha the takeover not only signifies noticeable

efficiency potential in the organisation and production of the current roof

project, it also represents the commitment of the Convertible Roof Systems

Division to the North American market and its intention to further increase its

share of currently 20% in this market.”

Chapter 2 The market Page 8

© 2005 All content copyright Aroq Ltd. All rights reserved.

Bertone The Italian coachbuilder has built a number of prestigious models, including

the BMW C1, Citroen Berlingo, Fiat Punto cabriolet, Citroen Xantia and ZX,

and Daewoo Espero. In 2003, Bertone unveiled a new sports car concept

based around the BMW Z8, called the Birusa. The concept features a number

of novel technologies such as voice-activated door and sunroof opening.

Car Top Systems The German convertible roof specialist, Car Top Systems (CTS) was founded

as a 50/50 joint venture between Porsche and DaimlerChrysler in 1996. In

September 2003, Porsche purchased the remaining 50% shares from

DaimlerChrysler, making CTS a wholly owned subsidiary. CTS generated

sales of €420m in 2004 and produced some 190,000 roof systems.

Edscha Germany’s Edscha has strong positions in convertible roof systems, driver

controls (pedal boxes and parking brakes), sliding roofs for trucks and vehicle

design markets. Owned by EdCar Beteiligungs GmbH, Edscha operates from

25 sites worldwide. Edscha develops and manufactures soft-tops and hard-

tops for a number of convertibles in Europe, including the Audi TT, BMW 3

Series, Opel Astra, Smart roadster, BMW Z4 and 6 Series Convertible. In

2004, the company began supplying the roof of the Chrysler PT Cruiser

Convertible. Edscha is currently preparing a further six convertible roof designs

for series production. In 2004, Edscha produced 190,000 roofs. The company

has doubled its production in the last two years and quadrupled it in the last

five. Today, Edscha claims a 25% share of the European convertible roof

systems market and a 20% share of the North American convertible roof

systems market. Edscha’s acquisition of Premier Roof Systems has also

resulted in an increase in its market share with BMW. With the 3 Series, 6

Series and Z4, Edscha now supplies 100% of the current convertible model

range.

Heuliez The French specialist in body-in-white and niche vehicles, Heuliez has

produced more than 415,000 complete vehicles over the last 25 years. The

company generated sales of €500m in 2004. Headquartered in Cerizay,

France, Heuliez employs 2,700 people. The company operates a production

facility in Cerizay, a JIT assembly shop in Mojados, Spain. A production facility

in Slovakia is scheduled to open in December 2005. The company also

Chapter 2 The market Page 9

© 2005 All content copyright Aroq Ltd. All rights reserved.

operates a development centre in Le Pin (France), a design office and

showroom in Paris (Massy), a liaison office in Detroit and Tokyo and a

subsidiary company in Seoul, Korea.

Inalfa Inalfa Roof Systems, one of the largest roof systems suppliers, develops and

manufactures equipment for cars and trucks for most OE manufacturers.

Headquartered in Venray, the Netherlands, Inalfa Roof Systems employs

1,500 people at its operations in the US, Brazil, the Netherlands, UK, France,

Italy, Japan and South Korea. Technical centres in Venray (the Netherlands)

and Auburn Hills develop ever larger and more complex roof systems. Recent

innovative products are the rear sliding roof system of the GMC Envoy, the

multifunctional roof system for the Citroën C3 Pluriel and the BMW X3’s twin

panel panorama roof.

Karmann Wilhelm Karmann GmbH designs and develops cars in close co-operation with

its OEM customers. The company also produces stamped parts, bodies-in-

white and convertible tops. Headquartered in Osnabruck, Germany, Karmann

employs 8,750 people, of which just over 7,000 are based in Germany.

Karmann has won a prestigious contract to supply the convertible roof for the

next Chrysler Sebring, another success for European roof suppliers building

business in North America. Based on sales of 40,000 units, the deal will be

worth US$14m a year, rising to US$60m if Karmann also succeeds in getting

the business for an optional folding hard-top.

Pininfarina The Italian coachbuilder Pininfarina made its name originally as a styling

house, but it is increasingly known as a niche vehicle manufacturer. The

company is promoting its backroom engineering skills, and has formed an

engineering division with a dedicated facility near Turin to gain new business.

In late 2004, Pininfarina exited the joint venture with Webasto, known as

OASYS, (or Open Air Systems). Webasto has purchased Pininfarina’s stake in

OASYS, making it a 100% affiliated company. OASYS remains an exclusive

supplier to Pininfarina.

Chapter 2 The market Page 10

© 2005 All content copyright Aroq Ltd. All rights reserved.

Webasto Webasto's US roof systems business already dominates the local sunroof

market, but the company is planning to further increase its market share and

expand into new areas such as convertibles and body systems. The

company's recent display vehicle, the Welcome 2, sports a large sunroof, a

retractable boot lid, retractable tailgate, sliding cargo bed system and an

electric boot scraper that emerges from underneath each door. A major part of

the company's growth strategy will be in convertibles, despite the fact that US

demand has softened in recent years. Webasto aims to design convertibles

that will retract during driving and retractable roofs that will incorporate

sunroofs. Demand for the UltraView roof, fitted to the Cadillac SRX, is strong

and Webasto has a new plant in Lexington, which will supply the roof system

for the Mercedes GST cross utility plus other systems for Chrysler and

Hyundai.

Mergers, acquisitions and joint venture activity

In 2004, ArvinMeritor formed a 50/50 joint venture between its Light Vehicle

Systems business group and Chinese auto parts supplier Shanghai SIIC

Transportation Electronic Company Ltd. The joint venture, named Shanghai

ArvinMeritor Automotive Parts Company Ltd, manufactures sunroofs for

Shanghai Volkswagen at a facility in Shanghai.

In January 2005, Edscha took control of Premier Roof Systems LLC, the US-

based joint venture with ASC Inc (as noted above). This venture has been

renamed Edscha Roof Systems LLC. In late 1999, ASC and Edscha joined

forces at the request of BMW to work on the roof system of the BMW Z4

roadster. ASC was the incumbent North American convertible roof supplier for

the Z3, the Z4’s predecessor built in the US. Meanwhile, Edscha was (and still

is) a supplier of convertible roofs to BMW with experience expertise in latches,

complex roof movement sequences, lightweight construction and drives. In

August 2000, Premier Roof Systems was set up as a 50/50 joint venture. A

year later, the partners opened a manufacturing facility in Greer, near the

BMW plant in Spartanburg, South Carolina, US.

In 2004, Pininfarina exited its 50/50 joint venture, OASYS, with Webasto.

OASYS manufactures retractable hard-tops at operations in Stockdorf,

Germany and Turin, Italy. OASYS developed the roof system for the Mini

Chapter 2 The market Page 11

© 2005 All content copyright Aroq Ltd. All rights reserved.

Cabriolet and it has been developing the retractable hard-top for the Golf-

based Volkswagen Cabriolet. Webasto has purchased Pininfarina’s stake in

OASYS, making it a 100% affiliated company. OASYS remains an exclusive

supplier to Pininfarina.

In explaining the decision to split the joint venture with Pininfarina, Webasto’s

Healy told just-auto: “We parted company on very good terms. We still have a

lot of ties with Pininfarina because of our existing contracts. This business

[OASYS] is going very well in Europe with a lot of innovative products coming

out. Our strategy was to initially entrench ourselves in Europe before moving

into other regions. OASYS’ activities in North America will certainly increase in

the next two years. We are preparing ourselves for the next contracts that

come up.”

In 2002, Webasto AG became a major supplier in the US sunroof market

following its purchase of Magna International Inc’s 50% stake in Webasto

Sunroofs Inc, of Rochester Hills, Michigan. The purchase ends a 16-year joint

venture between Webasto and Magna. Two months later, Webasto

consolidated its aftermarket business in the US. Webasto Sunroofs Inc and

Hollandia Sunroofs Inc merged to become Webasto-Hollandia North America

Inc of Brighton, Michigan. Hollandia had been the North American distribution

channel for Vermuelen Hollandia Sunroofs of the Netherlands. The Magna

deal also allowed Webasto the freedom to separate the aftermarket division

and consolidate it with Hollandia.

In 2003, Webasto acquired Genion Fahrzeugtechnik GmbH, a developer of

vehicle roof systems. Genion is based in Gaimersheim, near Ingolstadt with

branches in Wolfsburg and Sindelfingen. The company employs 80 people and

generated sales of €10m in 2002.

In 2004, Webasto and Indian automotive component major Sumi Motherson

set up a joint venture to make sunroofs. The initial investment is pegged at

€1.5m and the joint venture partnership is 51/49 in favour of the German firm.

The assembly unit is based in Noida, near Delhi, though the plan is to use

Motherson’s existing facilities across India in future. The company has already

launched a range of sunroofs in India under the Hollandia brand name with

prices varying between €245 for a simple, pop-up, manual operation and

€2,725. The joint venture plans to take the franchise route for distribution. The

management believes that they can achieve 10% fitment in all new cars sold.

Chapter 2 The market Page 12

© 2005 All content copyright Aroq Ltd. All rights reserved.

Guenther Schwanitz, GM-emerging markets for Webasto AG, said: “India

holds a lot of potential for automotive lifestyle products and we will supply

sunroofs for any car from a Maruti to a Maybach.” India has not been a strong

market for sunroofs and Webasto is the first major brand to enter the market.

Capital investment activity

In 2003, Car Top Systems expanded its facility in Bremen, Germany to

accommodate the next generation of Mercedes-Benz SLK retractable hard-top

roof systems.

In 2003, Inalfa Roof Systems USA opened a new assembly plant in Grand

Blanc, Michigan, to make tilt/slide sunroofs for the new Chrysler 300C sedan

and Dodge Magnum, assembly of which began in Brampton, Canada, in

January 2004. The company also supplies sunroofs for the Dodge Ram

Pickup, Jeep Grand Cherokee and General Motors GMT 800 pickup line.

In 2003, Webasto Roof Systems Inc opened a 200,000-ft² facility in Lexington,

Kentucky. The US$28m plant is the company’s second assembly facility in

Lexington, located directly across the street from its current 115,000-ft² plant.

The plant produces automotive roof systems that require the encapsulation of

large glass assemblies. In Asia, Webasto is expanding its manufacturing

presence. The company has opened a second factory near Seoul, South

Korea. Webasto has also expanded its manufacturing capacity in Shanghai,

first for sunroof systems. In Palmela, Portugal, Webasto is building a

production facility. The site is located on the VW Autoeuropa supplier park,

south of Lisbon. The €34m facility will produce complete roof systems for VW,

creating 170 jobs.

Market shares

For some time, the ‘big three’ sunroof makers – Webasto, ArvinMeritor and

Inalfa – have collectively dominated the OE vehicle sunroof market. The

German group Webasto still claims to lead the global sunroof market with a

39% share, followed by Inalfa and ArvinMeritor.

Chapter 2 The market Page 13

© 2005 All content copyright Aroq Ltd. All rights reserved.

Figure 1: Global market shares for vehicle sunroofs, 2004 (% of production volume)

39%

25%

15%

21%

Webasto

Inalfa

ArvinMeritor

Others

Source: just-auto.com

Aisin Seiki leads the Japanese OE sunroof market, closely followed by

Webasto. ArvinMeritor has around 5-10% of the Japanese sunroof market.

Other leading suppliers are Ohi Seisakusho (supplying Nissan), and Yachayo

(supplying Honda).

The blossoming Chinese sunroof market is led by Webasto, followed by Aisin

and Inalfa. From the end of 2006, Inalfa Roof Systems will supply the sunroofs

for the Cadillac STS to SGM in China. This is the first order for Inalfa Roof

Systems to GM in China. In the US, Inalfa already supplies the Cadillac STS

sunroof to GM North America.

Inalfa Roof Systems has also won an order to supply the sunroof for the next

Nissan X-Trail. Production is scheduled to commence in August 2006. With an

initial annual production volume of over 100,000 units, thus is the second

largest sunroof volume of all models in Nissan. It is a joint project between

several Inalfa companies, led by Nihon Inalfa. The Japanese office is

responsible for the overall programme management. The development is

carried out at Inalfa’s largest technical centre at its headquarters in Venray, the

Netherlands. Assembly will take place at the Kyunggi-Do plant of Inalfa Roof

Systems Korea. This order, together with the Maxima, Titan, Armada and

Quest sunroof business in North America, establishes Inalfa Roof Systems as

a major supplier to Nissan.

Chapter 2 The market Page 14

© 2005 All content copyright Aroq Ltd. All rights reserved.

In Australia, Webasto claims to have 90% of the sunroof aftermarket,

distributing a range of products through its own subsidiary. In addition, the

company sells a number of sunroofs to HSV (Holden Special Vehicles).

In the European market, Webasto leads the OE market for sunroofs, followed

by Inalfa and ArvinMeritor.

Figure 2: European OE market shares for vehicle sunroofs, 2004 (% of production volume)

43%

29%

20%

8%

Webasto

Inalfa

ArvinMeritor

Others

Source: just-auto.com

As far as the European sunroof aftermarket is concerned, manufacturers point

out that it has more or less collapsed following laws being enforced by the car

industry forbidding dealers to cut a hole in a car’s roof after it has left the

factory. There are concerns by the vehicle makers that the safety of the vehicle

will be compromised if a hole is cut in the top of it. Although suppliers can still

fit sunroofs as a retrofit item, the cost of cutting through the red tape makes it

prohibitive.

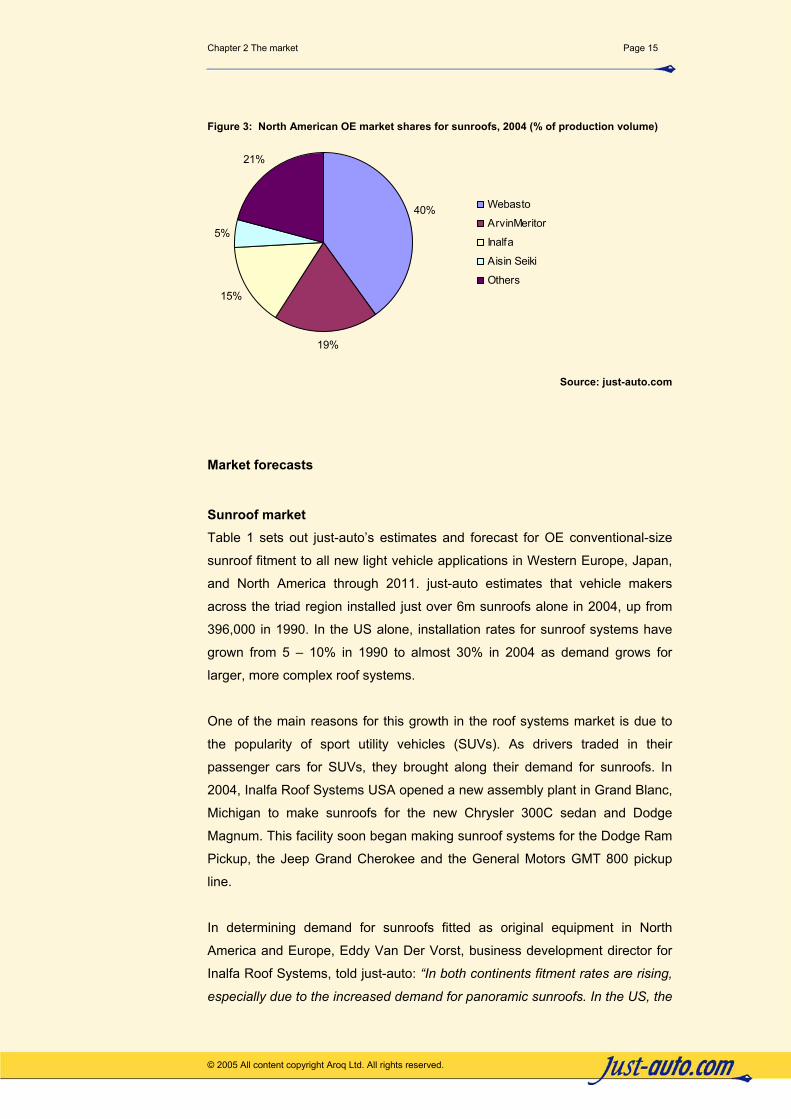

In North America, Webasto is the number one supplier of OE sunroofs,

followed by ArvinMeritor and Inalfa Roof Systems USA. Collectively, these

three suppliers have three-quarters of the US OE sunroof market. Aisin Seiki

supplies sunroofs to Toyota.

Chapter 2 The market Page 15

© 2005 All content copyright Aroq Ltd. All rights reserved.

Figure 3: North American OE market shares for sunroofs, 2004 (% of production volume)

40%

19%

15%

5%

21%

Webasto

ArvinMeritor

Inalfa

Aisin Seiki

Others

Source: just-auto.com

Market forecasts

Sunroof market Table 1 sets out just-auto’s estimates and forecast for OE conventional-size

sunroof fitment to all new light vehicle applications in Western Europe, Japan,

and North America through 2011. just-auto estimates that vehicle makers

across the triad region installed just over 6m sunroofs alone in 2004, up from

396,000 in 1990. In the US alone, installation rates for sunroof systems have

grown from 5 – 10% in 1990 to almost 30% in 2004 as demand grows for

larger, more complex roof systems.

One of the main reasons for this growth in the roof systems market is due to

the popularity of sport utility vehicles (SUVs). As drivers traded in their

passenger cars for SUVs, they brought along their demand for sunroofs. In

2004, Inalfa Roof Systems USA opened a new assembly plant in Grand Blanc,

Michigan to make sunroofs for the new Chrysler 300C sedan and Dodge

Magnum. This facility soon began making sunroof systems for the Dodge Ram

Pickup, the Jeep Grand Cherokee and the General Motors GMT 800 pickup

line.

In determining demand for sunroofs fitted as original equipment in North

America and Europe, Eddy Van Der Vorst, business development director for

Inalfa Roof Systems, told just-auto: “In both continents fitment rates are rising,

especially due to the increased demand for panoramic sunroofs. In the US, the

Chapter 2 The market Page 16

© 2005 All content copyright Aroq Ltd. All rights reserved.

market of pick-up trucks has just begun to be fitted with OEM sunroofs, which

gives another push in the demand. Inalfa Roof Systems US supplies three of

the five big selling pick-up trucks in the US at this moment. However the

booming European panoramic sunroofs have not yet experienced their

breakthrough in the US.”

Table 1: Production of conventional-size sunroofs for light vehicle applications in Western Europe, Japan, North America, 2000-2011¹ ² (Units, ‘000s)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Western Europe 2000 2040 2081 2122 2165 2208 2252 2297 2343 2390 2438 2487

Japan 1800 1818 1836 1855 1873 1892 1911 1930 1949 1969 1988 2008

North America 1900 1938 1977 2016 2057 2098 2140 2183 2226 2271 2316 2362

Total 5700 5796 5894 5993 6095 6198 6303 6410 6518 6630 6742 6857

¹ Includes all types of sunroof although majority are tilt and slide variety.

² Even though the European sunroof market continues to shrink, please bear in mind that some of

the European production is exported to the US.

Source: just-auto.com

Table 2 sets out just-auto’s estimates and forecasts of the market value of OE

conventional-size sunroofs across Western Europe, North America and Japan.

In calculating these figures, we have assumed an ‘average’ wholesale (factory

gate) price of a sunroof in 2001 as US$170 for each region. That is based on

the fact that a standard manual powered sunroof costs the OEM approximately

US$130 whereas a powered sunroof costs US$190. Given that about 80% of

vehicle sunroofs across Europe are electric and 20% are manually operated,

we have weighted the average price toward the powered sunroof. US-based

vehicle makers are also using powered sunroofs as another way in which to

differentiate their cars from competing models.

Overall, just-auto estimates the triad regional market for passenger car and

light truck OE sunroof applications was worth nearly US$1m in 2000. That

figure could reach US$1.16m by the end of the decade.

Chapter 2 The market Page 17

© 2005 All content copyright Aroq Ltd. All rights reserved.

Table 2: Market value of conventional-size sunroofs for light vehicle applications in Western Europe, Japan, North America, 2000-2011 (US$ ‘000s)

2000 2001 2002 2003 2004 2005

Western Europe 340000 346800 353736 360811 368027 375387

Japan 306000 309060 312151 315272 318425 321609

North America 323000 329460 336049 342770 349626 356618

Total 969000 985320 1001936 1018853 1036078 1053614

2006 2007 2008 2009 2010 2011

Western Europe 382895 390553 398364 406331 414458 422747

Japan 324825 328073 331354 334668 338014 341395

North America 363750 371025 378446 386015 393735 401610

Total 1071470 1089651 1108164 1127014 1146207 1165752

Source: just-auto.com

While table 2 above considers the conventional sunroof market – most of

which are tilt and slide or spoiler designs – table 3 below sets out just-auto’s

estimates and forecasts for the size of the large sunroof market. We estimate

that just over one million large (panoramic) sunroofs were produced in 2004

across Western Europe, Japan and North America. That figure could more

than quadruple by 2011. All roof manufacturers predict massive growth in large

sunroofs worldwide. In an exclusive interview with just-auto, Brett Healy, vice

president of business development planning for Webasto Roof Systems

explained how the company is aiming to grow in the North American sunroof

market. He said: “The first step is to sell more of what you have. That is

working for us. At an industry level, approximately 25% of new vehicles come

equipped with sunroofs. We are above that in the projects, we sell actually

closer to 30%. We see that increasing by about 2% per year. Our mission is

50/50 2010. That means 50% fitment rate with a 50% market share for sunroof

systems in North America by 2010. Will we hit that? I’m not sure but it is

tracking very positive.

“The second step is that our customers are starting to look at roof systems in

three categories. The first category is a traditional sunroof in which our

Chapter 2 The market Page 18

© 2005 All content copyright Aroq Ltd. All rights reserved.

customers are beginning to respond to our recommendations to ‘commonise’,

i.e. use the same sunroof on many vehicles. That way we can give them better

prices because of leverage. Quality goes up, too. We are now seeing that

consistently across multiple customers. Secondly, we see the growth of

panorama roofs in North America.

“And then there is a new niche which falls in between a traditional sunroof and

a full panorama roof system. We call it a bottom load big roof. It typically has

moving glass in the forward passenger area and fixed or moving glass in the

rear passenger area. It is a unit which installs from underneath which is more

traditional to a normal sunroof. We believe this will be the fastest area for

growth.

“Over the next two car cycles, we see the majority of applications being

traditional sunroofs, although the share of these bottom load big roof and

panoramic systems is increasing very fast.”

Table 3: Production of large sunroofs for light vehicle applications in Western Europe, Japan, North America, 2000-2011 (Units, ‘000s)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Western Europe 20 42 105 220 330 416 524 660 832 1048 1320 1664

Japan 18 38 100 210 330 396 475 570 684 821 985 1182

North America 19 40 115 250 405 494 603 735 897 1095 1335 1629

Total 57 120 320 680 1065 1306 1602 1966 2413 2964 3641 4475

Source: just-auto.com

The following table sets out just-auto’s estimates and forecasts of the market

value of OE large sunroofs across Western Europe, North America and Japan.

In calculating these figures, we have again assumed an ‘average’ wholesale

price of a large sunroof in 2000 as US$600 for each region. As volumes

increase, unit price will inevitably fall.

Chapter 2 The market Page 19

© 2005 All content copyright Aroq Ltd. All rights reserved.

Overall, just-auto estimates the triad regional market for passenger car and

light truck OE large sunroof applications was worth US$34.2m in 2000. That

figure could reach nearly US$2bn by 2011.

Table 4: Market value of large sunroofs for light vehicle applications in Western Europe, Japan, North America, 2000-2011 (US$ ‘000s)

2000 2001 2002 2003 2004 2005

Western Europe 12000 24444 59277 120473 175288 214237

Japan 10800 22116 56454 114997 175288 204035

North America 11400 23280 64922 136901 215126 254580

Total 34200 69840 180653 372371 565702 672852

2006 2007 2008 2009 2010 2011

Western Europe 261840 320021 391130 478039 584260 714082

Japan 237497 276446 321784 374556 435983 507485

North America 301270 356523 421910 499288 590857 699221

Total 800608 952991 1134823 1351883 1611100 1920787

Source: just-auto.com

Convertible roof market

Demand for convertibles worldwide is increasing. “We expect global demand

for convertibles will double over the next ten years,” said Dr Christian P Eick,

marketing & public affairs manager for Wilhelm Karmann GmbH, in an

exclusive interview with just-auto. “There are a number of reasons for that.

First, we see the retractable hard-top as additional demand. In other words, we

do not see a trade-off between soft-tops and retractable hard-tops. Second, we

are seeing convertibles becoming a ‘must’ in OEMs’ product line-up. There are

still a number of brands that do not yet have convertibles in their product line.

We expect to see that change over the next decade. By 2007, we expect to

have more retractable hard-tops than soft-tops in the world because [of] the

introduction of retractable hard-tops in the compact segment.

Chapter 2 The market Page 20

© 2005 All content copyright Aroq Ltd. All rights reserved.

“On the other hand, we expect to see a solid proportion of certain luxury

models with soft-tops. VW has just disclosed that Karmann will develop partly

the body and deliver the roof system for the Bentley Convertible. This is also a

soft-top. Overall, however, we predict that the market for soft-tops will remain

stable while the proportion of retractable hard-tops will reach more than 50%

by 2015, up from 35% today.”

The French specialist in body-in-white and niche vehicles, Heuliez also

believes that the retractable hard-top market is set to blossom. “When the

Mercedes SLK appeared on the market seven years ago, the consensus was

that the retractable hard-tops technology would soon replace the conventional

soft-tops and will be exclusively dedicated to exclusive car segments,” said

Bernard Girard, director of Heuliez Deutschland and business development, in

an exclusive interview with just-auto. “But opinions have changed. Most people

would now agree that retractable hard-tops can be largely integrated in almost

all car segments and that it will not only be considered as the replacement of

the soft-top.”

Heuliez is in total agreement with Karmann with regard to the direction of the

convertible market. “We believe that the volume of convertible vehicles

equipped with soft-tops will progress slowly and almost stagnate,” added

Girard. “Today in Europe, 70% of the convertibles have a soft-top and only

30% have a retractable hard-top. We believe that this ratio will be inversed in

2010. Parallel to this, the volume of convertible vehicles in general will rise. In

2003, the sales of convertibles in Europe have increased to reach 2.5% of the

total volume of cars. This part was only 0.8% in 1990. If this growth continues,

we can expect in 2010 a volume of convertibles increased by almost 6% in

comparison with today. Some 70% of this recalculated volume should be

equipped with a retractable hard-top. There are sceptics about the application

of retractable hard-tops to large roofs, involving multi-part complex roof

systems. Today, the big unknowns are cost and reliability of such systems. As

these larger vehicles will be launched soon, these factors will have a big

influence on the evolution of the retractable hard-top through this decade.”

On that basis, just-auto estimates that there were some 390,000 convertible

systems produced in Europe in 2003, of which 260,000 were soft-tops,

100,000 retractable hard-tops and 30,000 one-piece hard-tops. By 2008, we

forecast that some 585,000 convertibles will be produced in Europe, of which

Chapter 2 The market Page 21

© 2005 All content copyright Aroq Ltd. All rights reserved.

200,000 will be soft-tops, 350,000 retractable hard-tops and just 35,000 one-

piece hard-tops.

The convertible market in North America is also blossoming. In 2003, just-auto

estimates there were some 344,000 convertible systems produced, of which

290,000 were soft-tops, 30,000 retractable hard-tops and 24,000 one-piece

hard-tops. By 2008, we predict that some 525,000 convertibles will be

produced in North America, of which 340,000 will be soft-tops, 170,000

retractable hard-tops and just 15,000 one-piece hard-tops. It should be noted

that these estimates and forecasts differ from just-auto’s second edition of this

report title. The second edition was sourced to a single company. Table 5,

however, has been completely revised based on estimates from a number of

sources as well as just-auto’s own database.

Table 5: Production of convertible roof systems in Europe and North America, 2003 and 2008 (units)

Europe North America

Soft-tops Retractable hard-tops

One-piece hard-tops Soft-tops Retractable

hard-tops One-piece hard-tops

2003 260,000 100,000 30,000 290,000 30,000 24,000

2008 200,000 350,000 35,000 340,000 170,000 15,000

Source: just-auto.com

Furthermore, the latest year-end figures from ACEA, the European carmakers’

trade association, confirm that coupe/convertibles are taking market share

away from soft-tops and coupes thanks to new models such as the Renault

Megane CC and Opel Tigra. France's PSA has driven the boom with its

Peugeot 307CC and 206CC, both with folding steel roofs previously limited to

luxury cars such as the Mercedes SL. The Peugeot 206 CC was Europe's

most popular convertible in 2003, with sales of around 60,000 units, followed

by the Citroen C3 Pluriel and the BMW Z4 (both with sales of around 23,000

units). In terms of resale value, the Peugeot 206 CC is said to be third in its

category, behind the Mercedes-Benz SLK and SL.

Latest sales figures from the UK indicate that Britons are leading the rest of

Europe with regard to driving convertibles. The numbers reflect a ten-year

Chapter 2 The market Page 22

© 2005 All content copyright Aroq Ltd. All rights reserved.

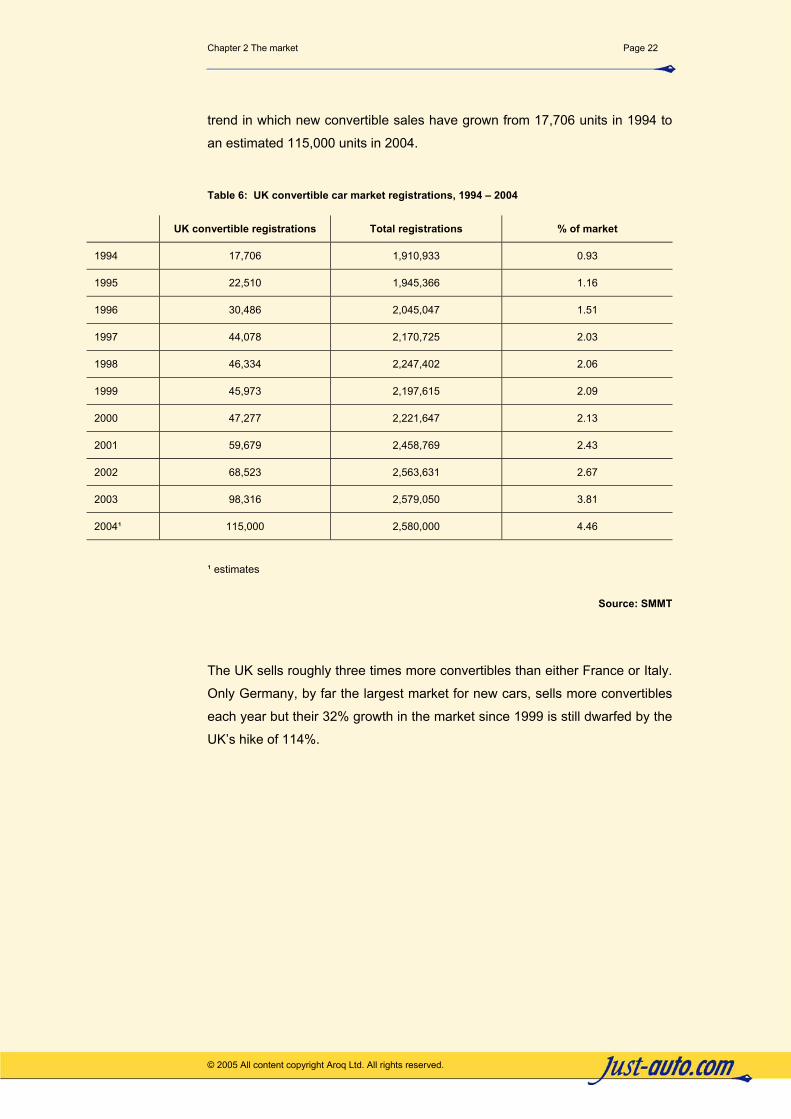

trend in which new convertible sales have grown from 17,706 units in 1994 to

an estimated 115,000 units in 2004.

Table 6: UK convertible car market registrations, 1994 – 2004

UK convertible registrations Total registrations % of market

1994 17,706 1,910,933 0.93

1995 22,510 1,945,366 1.16

1996 30,486 2,045,047 1.51

1997 44,078 2,170,725 2.03

1998 46,334 2,247,402 2.06

1999 45,973 2,197,615 2.09

2000 47,277 2,221,647 2.13

2001 59,679 2,458,769 2.43

2002 68,523 2,563,631 2.67

2003 98,316 2,579,050 3.81

2004¹ 115,000 2,580,000 4.46

¹ estimates

Source: SMMT

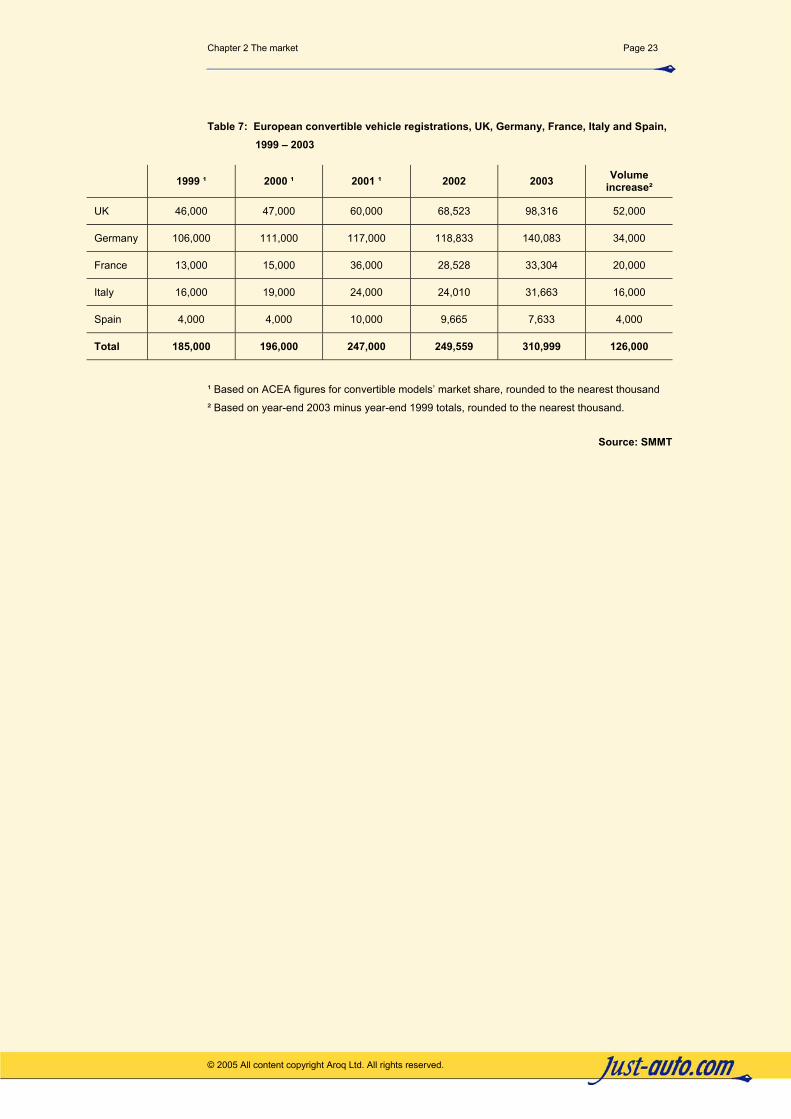

The UK sells roughly three times more convertibles than either France or Italy.

Only Germany, by far the largest market for new cars, sells more convertibles

each year but their 32% growth in the market since 1999 is still dwarfed by the

UK’s hike of 114%.

Chapter 2 The market Page 23

© 2005 All content copyright Aroq Ltd. All rights reserved.

Table 7: European convertible vehicle registrations, UK, Germany, France, Italy and Spain, 1999 – 2003

1999 ¹ 2000 ¹ 2001 ¹ 2002 2003 Volume increase²

UK 46,000 47,000 60,000 68,523 98,316 52,000

Germany 106,000 111,000 117,000 118,833 140,083 34,000

France 13,000 15,000 36,000 28,528 33,304 20,000

Italy 16,000 19,000 24,000 24,010 31,663 16,000

Spain 4,000 4,000 10,000 9,665 7,633 4,000

Total 185,000 196,000 247,000 249,559 310,999 126,000

¹ Based on ACEA figures for convertible models’ market share, rounded to the nearest thousand

² Based on year-end 2003 minus year-end 1999 totals, rounded to the nearest thousand.

Source: SMMT

Chapter 3 Technical review

Chapter 3 Technical review

Page 24

© 2005 All content copyright Aroq Ltd. All rights reserved.

Roof trends

The roof systems are fast becoming part of a car’s identity. For example, the

most eye-catching design feature on the Citroen C3 Pluriel is the multi-function

roof system, which allows the car to be a cabriolet, spider, saloon and pickup.

The car industry has discovered that the roof is an area where they can make

money. Panoramic sunroofs stretching the length and breadth of a vehicle are

becoming increasingly popular on both sides of the Atlantic. In fact,

manufacturers report an “unbelievable” amount of interest in large sunroofs.

The trend is toward roof systems, mainly of glass, with big openings that can

be adjusted even during driving. These designs give the best of both worlds:

saving on cost (compared to a convertible) and adding to the versatility of the

car. Again, the owner of a Citroen Pluriel can modify the car to suit their needs,

and all at a much lower cost.

Citroen is not alone in roof innovations. In the US, an increasing number of

cars with panoramic glass roofs are being offered, notably the Pontiac G6 GT

with its four-panel glass sunroof (the same model Oprah Winfrey gave to XXX

members of her audience in a media stunt in September 2004.) The popularity

of large and expensive sunroof systems on US vehicles is soaring and they

are available as options on everything from a Mini to a Cadillac SRX. This

burgeoning new market offers suppliers a great opportunity to develop model-

differentiating and value-added products, which translate into higher profits for

them and OEMs.

Inalfa Roof Systems’ consumer research confirms demands for light and airy

cabins. In an exclusive interview with just-auto, Eddy Van Der Vorst, business

development director for Inalfa Roof Systems, said: “A clinic conducted in

cooperation with a customer and a research institute told us that the main

benefits consumers see in their sunroofs are sky view and a brighter

compartment. Consumers are starting to realise that air-conditioning is for

cooling and a sunroof is for light and fresh air.”

Van Der Vorst also points out some challenges of panoramic sunroofs in terms

of design and manufacture. He told us: “A glass roof becoming larger and

Chapter 3 Technical review Page 25

© 2005 All content copyright Aroq Ltd. All rights reserved.

larger has a rising impact on the body structure. This impact plays an

increasing role in sunroof design. Another aspect is the rising weight. Ways to

reduce weight of the roof module is thus the other challenge.”

Webasto reports that the classic slide-tilt sunroof remains one of the top-selling

products of its roof systems business, but the trend is towards large-scale

sunroof systems. Webasto supplies panorama roofs for the Renault Scenic,

Cadillac SRX and the Mini. The German roof supplier has also developed the

lamella roof for the Mercedes-Benz A-Class; for the first time, polycarbonate is

being used in its construction instead of glass. Webasto has already

developed a steel louvers roof.

With the latest polycarbonate roof, Webasto claims a weight saving (19kg

instead of 22.5 kg for a steel louvered roof). The composition of polycarbonate

material made it possible to create a more flexible shape, says Webasto. The

polycarbonate components can also be configured in three dimensions and

integrated into existing systems relatively easily. This results in design benefits

for the A-Class louvered roof. The plastic panel is bonded onto an aluminium

reinforcement frame, making each louver a stable, load-bearing unit. The

louver surfaces are tinted grey and protected against scratching by a

polysiloxane coating. The surface coating is subject to the same resilience

requirements as the vehicle framework. The net result is a 928 x 850 mm roof

with transparent louvers. Two individually operated manual blinds made from a

semitransparent material keep the amount of isolation within reasonable limits

when the roof is closed. When the blinds are closed with the roof open, they

form a wind barrier to protect the occupants from draughts. The scratchproof

external coating is resistant to UVA, UVB and UVC, therefore providing the

passengers with additional protection against the sun.

The designers paid special attention to the seal integrity and low noise when

developing the louvred roof. For example, the gaps between the louvers are

equipped with a special triple seal system that, in conjunction with the water

management function, provides protection against moisture penetration into

the car. An aerodiffusor and a wind deflector louver also protect against wind

noise at high speeds.

In Europe, the market for panoramic glass roofs is blossoming with suppliers

preparing for increased demand. For example, Spanish supplier Grupo Antolin

recently won important new panoramic roof contracts from GM and PSA and

Chapter 3 Technical review Page 26

© 2005 All content copyright Aroq Ltd. All rights reserved.

this business now forms the fourth key business area for the company. Antolin

sold 20% of its shares to Spanish banks to raise the €80m needed to get into

the market and compete with rivals such as ArvinMeritor and Webasto. It sees

panoramic roofs as an important new trend and will supply the new Astra

Coupe and new Citroen Picasso minivan in 2005 and 2006 respectively.

Retractable hard-tops

Another area of roof design gaining increasing attention is retractable hard-

tops. Several coachbuilders have perfected the art of folding the metal.

“We believe that innovation and creativity in the field of retractable hard-tops

should not focus on complexity but much more in simplicity, manufacturability

and reliability,” said Bernard Girard, director of Heuliez Deutschland and

business development. “We have demonstrated this with the Opel Tigra

TwinTop, developed and produced at Heuliez. The innovations of this car are

not in the roof kinematics but in the packaging of the roof into the car and in its

modular plug and play assembly concept. We believe that there is great

potential for integrating very simple roof systems into very innovative

packaging. This will be the best way to develop the market.”

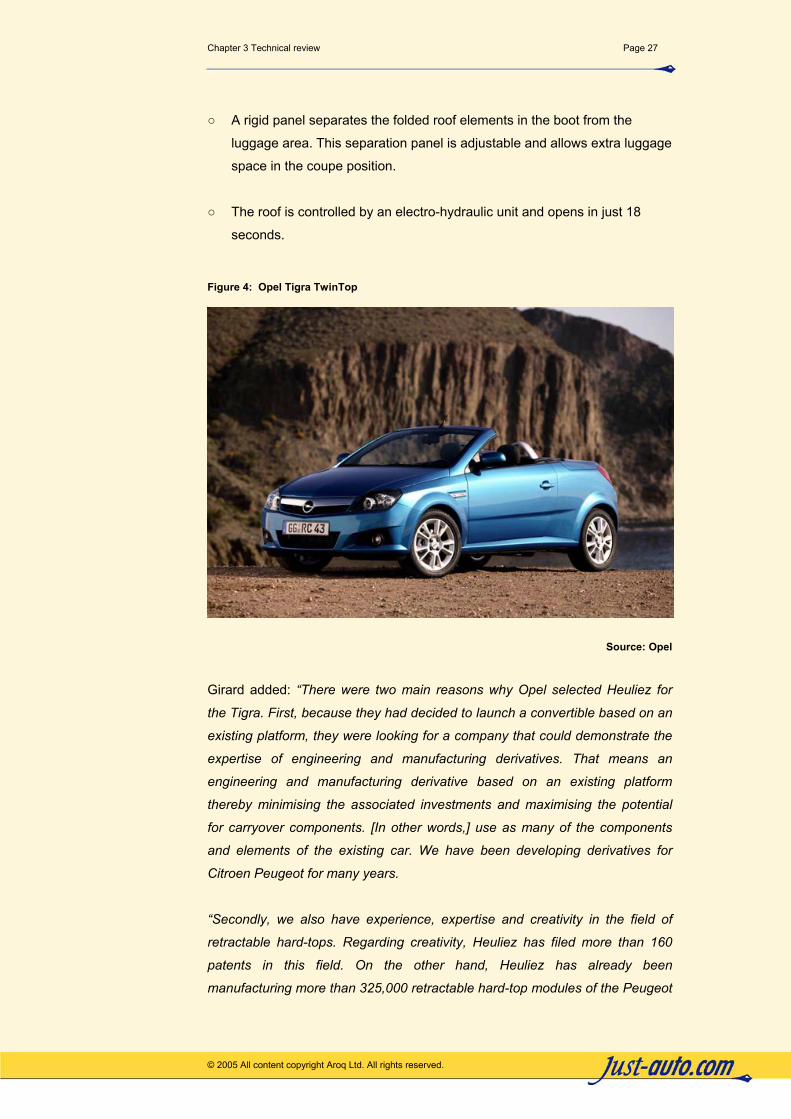

In June 2004, Heuliez began producing the Opel Tigra TwinTop two-seater

roadster equipped with a retractable hard-top at a rate of 210 vehicles per day.

Some specific novel design elements of this retractable hard-top include:

○ The two roof elements do not fold completely one over the other, but keep

an open area which enables a ‘cargo area’, accessible from the passenger

compartment.

○ The rear window element folds diagonally behind the seats, optimising the

luggage space and loading diagonal: the folded roof elements do not use

the entire length of the trunk and the luggage space height remains

unchanged.

○ Fully automatic deck lid opening.

○ Combined hinge/latch units in the front and back of the deck lid. The same

mechanisms are used for both front and rear opening movements.

Chapter 3 Technical review Page 27

© 2005 All content copyright Aroq Ltd. All rights reserved.

○ A rigid panel separates the folded roof elements in the boot from the

luggage area. This separation panel is adjustable and allows extra luggage

space in the coupe position.

○ The roof is controlled by an electro-hydraulic unit and opens in just 18

seconds.

Figure 4: Opel Tigra TwinTop

Source: Opel

Girard added: “There were two main reasons why Opel selected Heuliez for

the Tigra. First, because they had decided to launch a convertible based on an

existing platform, they were looking for a company that could demonstrate the

expertise of engineering and manufacturing derivatives. That means an

engineering and manufacturing derivative based on an existing platform

thereby minimising the associated investments and maximising the potential

for carryover components. [In other words,] use as many of the components

and elements of the existing car. We have been developing derivatives for

Citroen Peugeot for many years.

“Secondly, we also have experience, expertise and creativity in the field of

retractable hard-tops. Regarding creativity, Heuliez has filed more than 160

patents in this field. On the other hand, Heuliez has already been

manufacturing more than 325,000 retractable hard-top modules of the Peugeot

Chapter 3 Technical review Page 28

© 2005 All content copyright Aroq Ltd. All rights reserved.

206 CC since the production launch of this vehicle in September 2000. This

production volume is today unique in the field of retractable hard-tops.”

Meanwhile, Inalfa Roof Systems has developed and is assembling two

separate sunroof systems for the new Renault Modus, a combination of

supermini and mini-minivan attracting acclaim in Europe for its flexible cabin

layout and ingenious touches such as an available boot access hatch in the

rear tailgate. With a glass surface of more than 1400mm x 900mm, the

optional exterior sliding roof adds to the impression of spaciousness in the new

car. The transparent roof system covers almost the full roof panel and consists

of two flush-fitting panels. The rear panel is fixed; the forward panel can tilt and

slide open in three positions and the maximum opening is 500mm x 700 mm.

To minimise cabin heat, both glass panels are made of sun blocking glass and

two manually operated sunshades can be pulled across. When the roof is

opened a wind deflector unfolds to prevent wind noise.

Inalfa also developed a twin panel pop-up roof offered as an option for the

Modus. Two flush-fit glass panels can be tilted manually and independently, or

can be completely removed from their aperture. A bag behind the rear bench

seat stores the glass panels. The Renault Modus is one of the first of a new

generation of compact cars to be equipped with a large glass roof system that

can tilt and slide to create such a large opening. The two sunroof projects were

designed and engineered jointly by Inalfa and Renault, and both types were

based on proven Inalfa technology already in development and/or production

for Mercedes-Benz, BMW, Land Rover and other carmakers.

Webasto has also developed a new roof design. Based on a four-seater BMW

convertible, it combines the advantages of a coupé with sunroof with those of a

convertible. While driving along, says Webasto, the driver can open a large

glass sunroof and, depending on his preference and on the weather, can

electrically fold the whole roof away completely in top boxes. The luggage

room of the basic vehicle remains as unaffected as the silhouette of the

opened convertible. Wolfgang Thurow, board member responsible for roof

systems said: “The task we set ourselves was difficult, as you can imagine.

They had to combine all the advantages of different conflicting roof systems

without disadvantaging the car buyer. The result was a prototype based on a

BMW 3-Series convertible. Its particular strength is the practical synthesis of

convertible and sunroof, which brings benefits whether the roof is open or

closed.”

Chapter 3 Technical review Page 29

© 2005 All content copyright Aroq Ltd. All rights reserved.

Convertibles

ASC used the 2005 Detroit motor show to reveal its four-door convertible, the

Helios (pronounced he-lee-ohs). The company claims that the Helios

represents a feasible prototype that could allow any carmaker to create the

first production four-door convertible in nearly 40 years. The last four-door

convertible, the Lincoln Continental Convertible, was discontinued in 1967. To

achieve the structural integrity required in a four-door convertible, ASC fitted a

novel cross-car steel bulkhead just behind the car’s front seats. The bulkhead

is attached to new half B-pillars positioned between the front and rear doors –

designed to keep the car solid and quiet as well as transfer the force of a side-

impact collision into the body of the car, rather than the occupants. New, front-

seat mechanisms allow the front seats to sit over the bulkhead, ensuring full

adjustment of the front seats. The 5’8” convertible roof system packs into the

area behind the rear seats allowing ‘ample room for carrying four, full-size golf

bags’ in the boot. The resulting vehicle is a four-door convertible that weighs

300 pounds more than a similar-sized large sedan.

ASC also used the 2005 Detroit motor showcase its GTO Stinger, a vehicle

model that could be offered by ASC as a dealer-upfit package by the end of

2005. Features include body panels using ASC’s new composites process,

including a new hood, wheel flares, custom two-piece fascias and two-piece

rocker panels. Other parts made using the company’s new carbon filter include

a spoiler on the deck lid, fascia inserts and appliqués on both exterior mirror-

surrounds.

Ford of Europe is to launch a production version of its Focus Vignale cabriolet

concept by the end of 2006. The concept, shown at the 2004 Paris motor

show, was designed by Pininfarina and features a retractable hard-top

designed and built by OASYS, the Pininfarina/Webasto roof systems joint

venture. Pininfarina will build the model in Turin with components sourced from

the Ford plant in Saarlouis, Germany. The Vignale is based on a four-door

version of the new Ford Focus.

Valmet Automotive displayed a new Audi A4 Coupe Cabrio concept at the

2004 Geneva motor show, with a fully automatic three-panel retractable hard-

top. The three panels are stacked parallel when the top is down. Most of the

design is a carry-over from the original A4 cabriolet including the A pillars and

Chapter 3 Technical review Page 30

© 2005 All content copyright Aroq Ltd. All rights reserved.

windscreen, but the rear side windows have been lengthened to offer a better

rear view and allow more light into the cabin. Valmet's Technical Centre

completed the project in only three months.

Roof modules

Vehicle makers are gradually taking the idea of one-piece roof modules

seriously, and it seems only a matter of time before they are in widespread

use. Assembly advantages are impressive, as without its roof the unfinished

vehicle will offer much better access for interior assembly tasks, while bodies-

in-white can be further standardised as all roof options will come with the 'drop-

in' roof module. Webasto was the first supplier to manufacture a large roof

module, which it built for the Smart. It then began manufacturing a new

generation of convertible roofs.

ArvinMeritor’s Light Vehicle Systems division supplies complete roof modules

consisting of a roof headliner bound to an outer shell. These modules can