28

Global Oil and Gas Market Outlook Guy Caruso, Senior Advisor Presented to AABE Annual Meeting April 18, 2012 Long Beach, CA

Global Oil and Gas Market Outlook

Guy Caruso, Senior Advisor

Presented to AABE Annual Meeting

April 18, 2012 Long Beach, CA

www.csis.org | 2

www.csis.org |

Key Factors in Oil Market Security

• The oil market is globalized.

• Production and reserves are highly concentrated and

supply chain is vulnerable. Cheapest resources in the

Middle East.

• Continual investment in new supplies needed to offset

declining production as well as to accommodate demand

growth.

• Global demand for oil will be driven by developing

countries.

• Resource nationalism will affect investment flows

• However, unconventional oil and gas may modify

the narrative.

80

90

100

110

120

130

140

Do

llars

/ B

arre

ll

OPEC agrees to maintain output level

Renewed concerns about Greece’s default risk

Riots in Egypt

Clashes in Iran and Bahrain

Unrest In Libya

Fukushima

Libyan Rebels Seize Oil Facilities

Protests in Syria Reports of

Eurozone and Chinese Manufacturing Contraction

Release of SPR

Greek Restructuring Announcement

Q1 US GDP revised down from 1.8% to 0.4%

Expiration Of QE2

US Debt Deal

US AAA Rating Downgrade

Libya Oil Resumption

Col. Gaddafi captured

Q4 US GDP revised up Down Jones at highest level since 2008

Iran Nuclear Development

Euro crisis

Iran Threatens to Close Straight of Hormuz

Chairman Bernanke testifies about the US economy and employment

IEF meeting

Saudi pledges to increase production

France hints

to SPR

release

New band?

www.csis.org | 5

www.csis.org | 6

www.csis.org | 7 World liquids production, 2010: 86.29 mmb/d

MENA 2010 Liquids Production, 2010: 30.24 mmb/d

MENA share of world liquids production, 2010: 35%

Middle East and North Africa Critical to Oil Supply Chain

www.csis.org |

Oil Market Uncertainty for 2012 What Will Happen with Iran?

Iranian Oil Exports • Pressure on Iran is increasing.

New US sanctions imposed.

• EU agreed to phase in ban on

Iranian oil imports.

• Korea and Japan in discussions

about the application of CBI

restrictions.

• How much additional volume will

China be willing to absorb?

• How will Saudi Arabia react?

• Iran reacting with continued saber

rattling mixed with possible

compromise.

• US military position clear – will not

tolerate interference with

international shipping.

Total exports 2.15 MMb/d

www.csis.org |

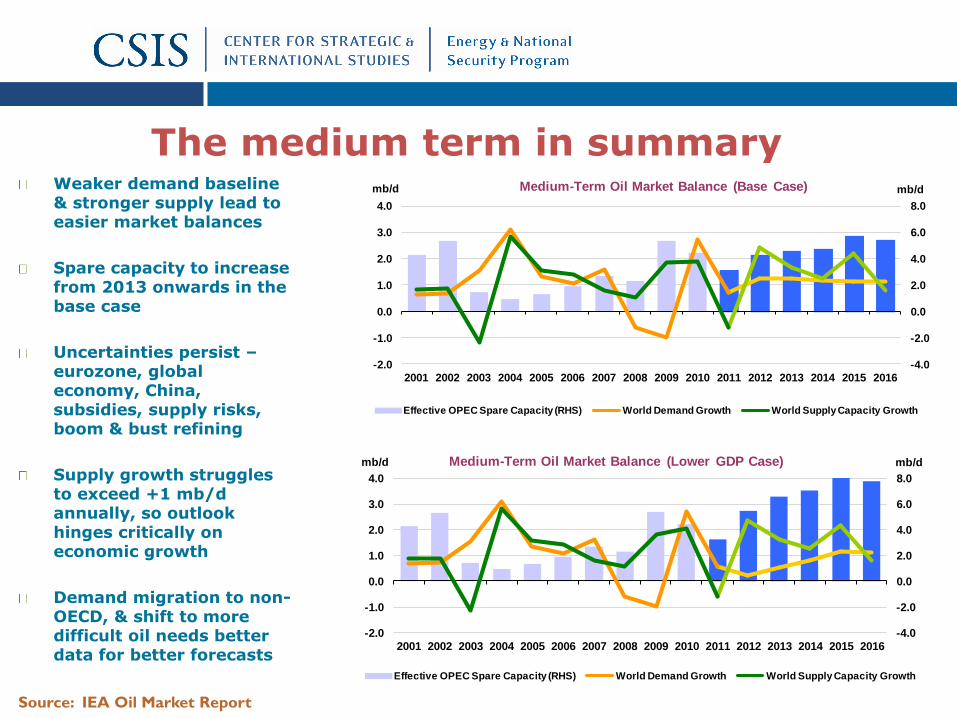

The medium term in summary Weaker demand baseline & stronger supply lead to easier market balances

Spare capacity to increase from 2013 onwards in the base case

Uncertainties persist – eurozone, global economy, China, subsidies, supply risks, boom & bust refining

Supply growth struggles to exceed +1 mb/d annually, so outlook hinges critically on economic growth

Demand migration to non-OECD, & shift to more difficult oil needs better data for better forecasts

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mb/dmb/d Medium-Term Oil Market Balance (Base Case)

Effective OPEC Spare Capacity (RHS) World Demand Growth World Supply Capacity Growth

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mb/dmb/d Medium-Term Oil Market Balance (Lower GDP Case)

Effective OPEC Spare Capacity (RHS) World Demand Growth World Supply Capacity Growth

Source: IEA Oil Market Report

The Shape Of The Economic Recovery Matters

-4

-2

0

2

4

6

8

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

An

nu

al

GD

P G

row

th (

%)

Emerging and Developing Economies

World

Advanced Economies

Source: IMF data, 2000-2009

www.csis.org |

Demand growth

is all about

non-OECD &

transport

Average Global Oil Demand Growth 1998-2004/2004-2010/2010-2016 Average Global Oil Demand Growth 2001-2006/2006-2011/2011-2016thousand barrels per day thousand barrels per day

(mb/d)

1998-2004 1.43 1.8%

2004-2010 0.81 1.0%

2010-2016 1.21 1.3%

Avg Global Demand Growth

19

-184-110

4213

66

202 176

23

391

-257-100

187

312 294

77 100 103

North America

Latin America Africa

Middle East

Europe FSU

722

576

801

Asia

OECD vs. Non-OECD Cumulative Oil Demand Growth

by Use, 1997-2015

(10)

(5)

-

5

10

15

20

25

30

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

mb/d

Non-OECD - Other

Non-OECD - Transportation

OECD - Other

OECD - TransportationOECD demand peaked in 2005

Demand growth now focused in 3 regions: Asia, Mid.East & L.America

Asia alone generates 55% of the total and China 35%

Premium & subsidised markets sustain growth, despite high prices

Understanding market trends requires better non-OECD data

Source: IEA Oil Market Report

www.csis.org |

Changing Supply Picture US Light Tight Oil Raises Non-OPEC Supply Estimates

Downward revisions in 2011-2013 due to unplanned outages, project delays, difficult

investment climate in some MENA countries.

Upward revisions due to uptick in E&P spending (rises by 22% in 2011, 10% in 2012), rosier

N. American outlook.

NGL supply revised up because producers are targeting liquids-rich tight oil plays.

12 Source: IEA Oil Market Report

380 620 870 1,140 1,320 1,530 1,7000

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2010 2011 2012 2013 2014 2015 2016

US Crude and Condensate Output

Total Light Tight OilGulf of MexicoAlaskaOther L48 Crude and Condensate

kb/d

-100

-600 -490-150

170

520710

-800-600-400-200

0200400600800

1000

2010 2011 2012 2013 2014 2015 2016

kb/d Non-OPEC Supply - Revisions

North America ChinaMiddle East OECD EuropeOth Asia OECD PacificAfrica Latin AmericaFSU Total Non-OPEC

www.csis.org | 13

www.csis.org | 14

www.csis.org |

0

25

50

75

100

125

150

175

200

225

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

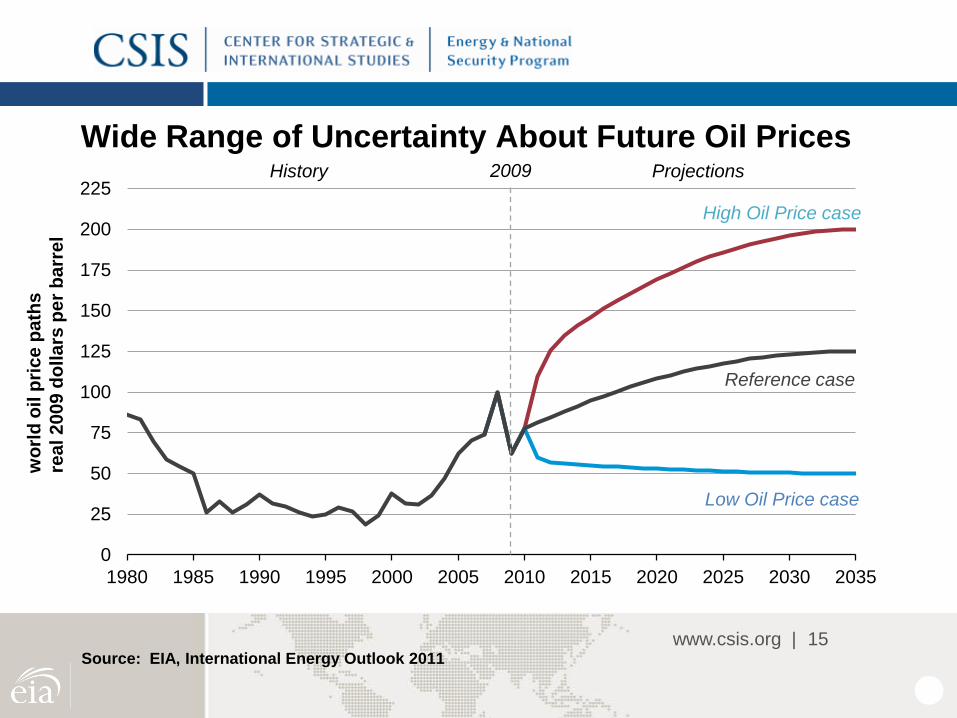

Wide Range of Uncertainty About Future Oil Prices

15

wo

rld

oil

pri

ce

pa

ths

rea

l 2

00

9 d

oll

ars

pe

r b

arr

el

Source: EIA, International Energy Outlook 2011

Projections History 2009

High Oil Price case

Low Oil Price case

Reference case

www.csis.org | 16

www.csis.org | 17

www.csis.org |

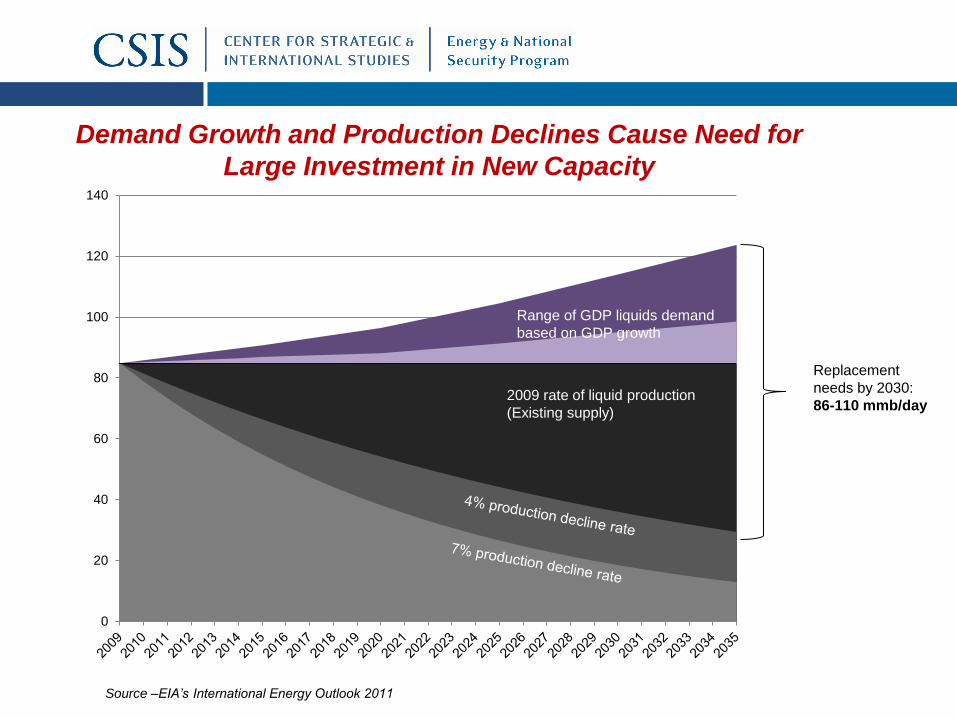

Source –EIA’s International Energy Outlook 2011

Demand Growth and Production Declines Cause Need for

Large Investment in New Capacity

Source –EIA’s International Energy Outlook 2011

0

20

40

60

80

100

120

140

Range of GDP liquids demand

based on GDP growth

2009 rate of liquid production

(Existing supply)

Replacement

needs by 2030:

86-110 mmb/day

www.csis.org | 19

Middle East and North Africa have World’s

Lowest Cost Petroleum Resources

Source: IEA World Energy Outlook 2009

www.csis.org |

Fiscal needs of key producing countries keep

pressure on oil prices

Breakeven costs, budget breakeven and commercially attractive

prices for current oil production for selected producers, mid-2011

Budget breakeven

Commercially attractive

Breakeven production cost

Qat

ar

Kuw

ait

Saudi Arabia

UA

E Liby

a

Russia

Vene

zuel

a

Ang

ola

Alg

eria

Iraq Nig

eria

Ec

uado

r

Iran

Super majors

0

20

40

60

80

100

120

0 5 10 15 20 25 30 35 40 45 0

Oil production (mb/d)

Do

llars

per

ba

rrel

5 10

www.csis.org |

N.A. Oil Supply Has Upside Potential But Risk of Decline

High production opportunities enabled by access frameworks

www.csis.org |

North American Shale Resources are Wide Spread

N.A.Gas Resources Have Potential to Supply the Market for Decades

High demand, advanced technology, moderate development cost

www.csis.org | 24

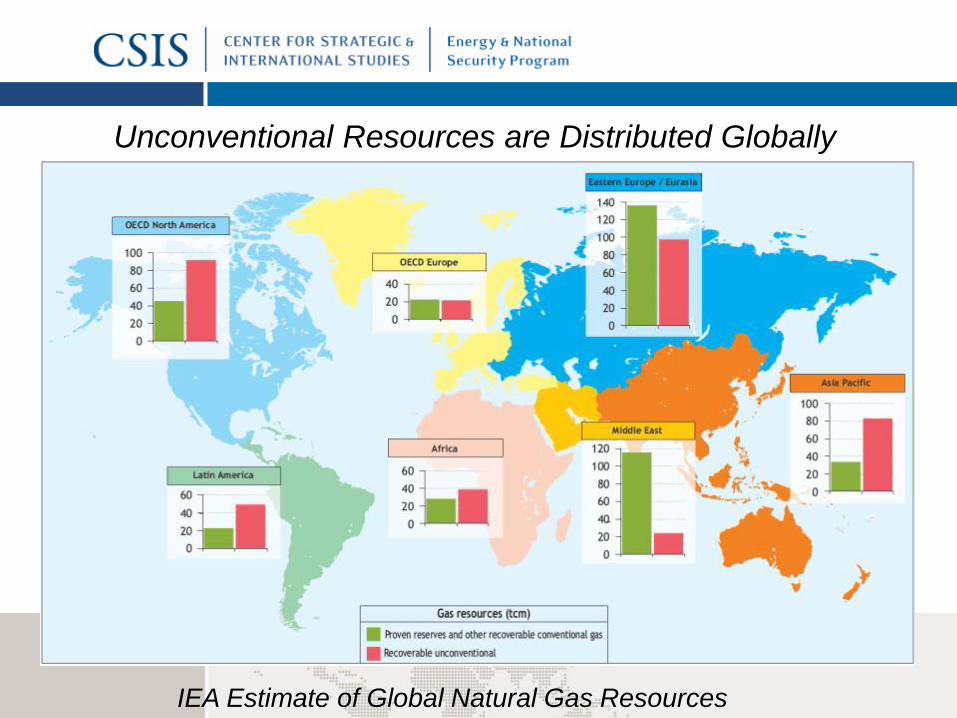

Unconventional Resources are Distributed Globally

IEA Estimate of Global Natural Gas Resources

Implications of Shale Gas “Revolution”

• Natural gas and oil prices have been delinked in the North American market.

• Natural gas will be the fuel of choice for power generation. Affects coal, nuclear and renewables.

• Petrochemical and gas based industries beginning to consider expanding operations in US.

• Gas may begin to make serious penetration as a transportation fuel.

• Natural gas exports from North America will being and may

grow. Alaska gas export option being considered.

BUT …realizing the full promise of shale resources is

not a certainty and US domestic policy is important!

Technical/Economic Challenges

• All shales are not alike; application of drilling/reservoir fracturing

technology & operational experience matters

• Steep decline rates require ongoing investment and drilling; and repeated

fracturing

• Cost escalation and low commodity prices limit prospects

Environmental/Regulatory/Societal Challenges

• Well design and management of surface chemicals/materials are the

best barriers to protecting water aquifers

• Disclosure of components of fracking fluids should/is happening

• Scale of water use, treatment & disposal are challenging

• Community Issues – infrastructure, land use, population density, noise,

haze, road congestion and repair are “real” and need to be addressed

• Regulation and enforcement are essential

www.csis.org |

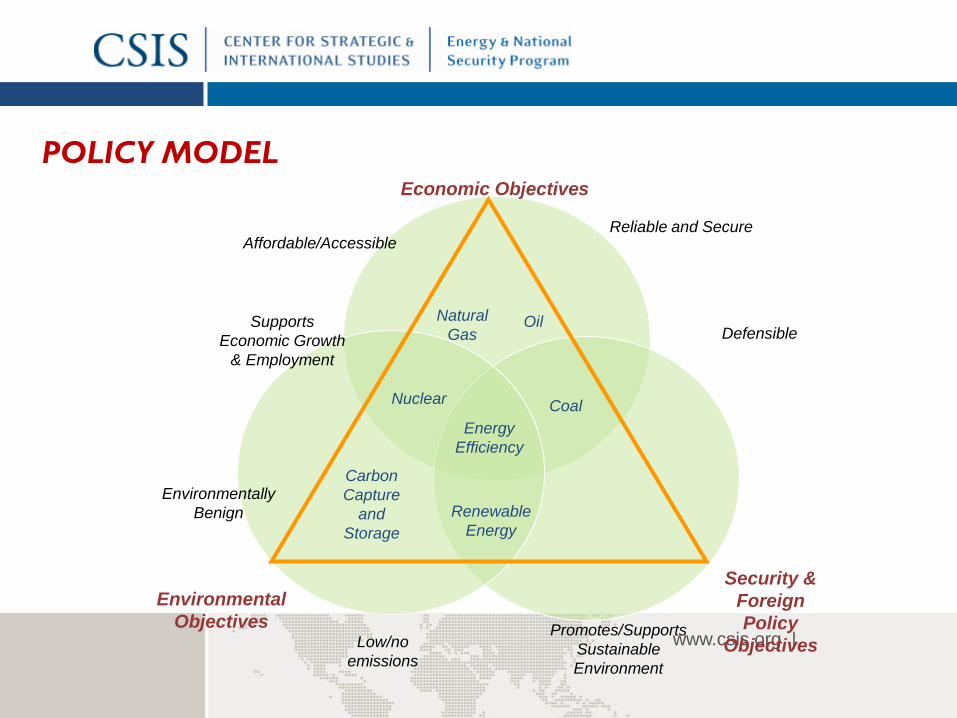

Security &

Foreign

Policy

Objectives Promotes/Supports

Sustainable

Environment

Defensible Natural

Gas Oil

Energy

Efficiency

Nuclear

Renewable

Energy

Coal

Economic Objectives

Environmental

Objectives

POLICY MODEL

Affordable/Accessible

Supports

Economic Growth

& Employment

Environmentally

Benign

Low/no

emissions

Reliable and Secure

Carbon

Capture

and

Storage

www.csis.org | 28

Thank You