16

Global Payments Evolution Simon McConnell Clearing and FI Payments - EMEA

Global Payments Evolution

Simon McConnellClearing and FI Payments - EMEA

1. Global Payments Landscape

Despite challenges, Wholesale Transaction Banking remains attractive now and into the future.

Forecasted Growth in Transaction Banking

Transaction banking business represent around one quarter of totalbanking revenue

Historically stable with predictable business development and upward revenue trends

Attractive margins and low capital absorption in comparison with other traditional banking activities

Combined payments andtransaction-banking revenues will reach an estimated US$1.1 trillion by 2022

Revenue mix expected to shift from payment fees to account-related revenue, as pressure on transaction fees persists

Source: Boston Consulting Group, 2013.

1 Global Payments Landscape

2022

Forecasted Growth in Global PaymentsPercentage of Total Value of Worldwide Payments

2012

Source: Boston Consulting Group.

The worldwide payments market was worth US$377 trillion in 2012

… and this value is expected to increase to US$712 trillion by 2022

Europe

Africa

Middle East

Asia

Intra Regional Trade US$4.0–US$5.0 Trillion US$2.0–3.0 Trillion US$1–1.5 Trillion

US$0.5–1.0 Trillion US$200–500 Billion US$100–200 Billion US$50–100 Billion

North America

Latin America

2 Global Payments Landscape

Megatrends Continue to Shape Transaction Banking Landscape

Shifting Global Trade Patterns As emerging economies expand and develop local payment infrastructure, on-shore clearing

capabilities to acquire flows locally are becoming more and more prominent Shift in trade patterns and currency usage can lead to FX opportunities

Emerging Payment Types and Technologies Access to cutting edge payment mechanisms need not involve direct product development Collaboration in shaping and supporting new channels can provide linkage to flows

Regulatory Environment/Risk Management New regulations create an implicit need for solutions that can go far beyond the intention and

culminate in a comprehensive and valuable toolkit Mechanisms supporting better measurement, reporting and transparency are the need

of the hour

Increased Pressure on Revenue and Expenses Pressure on banks to do more with less Requires banks to ensure they are maximising the value from their flows

3 Global Payments Landscape

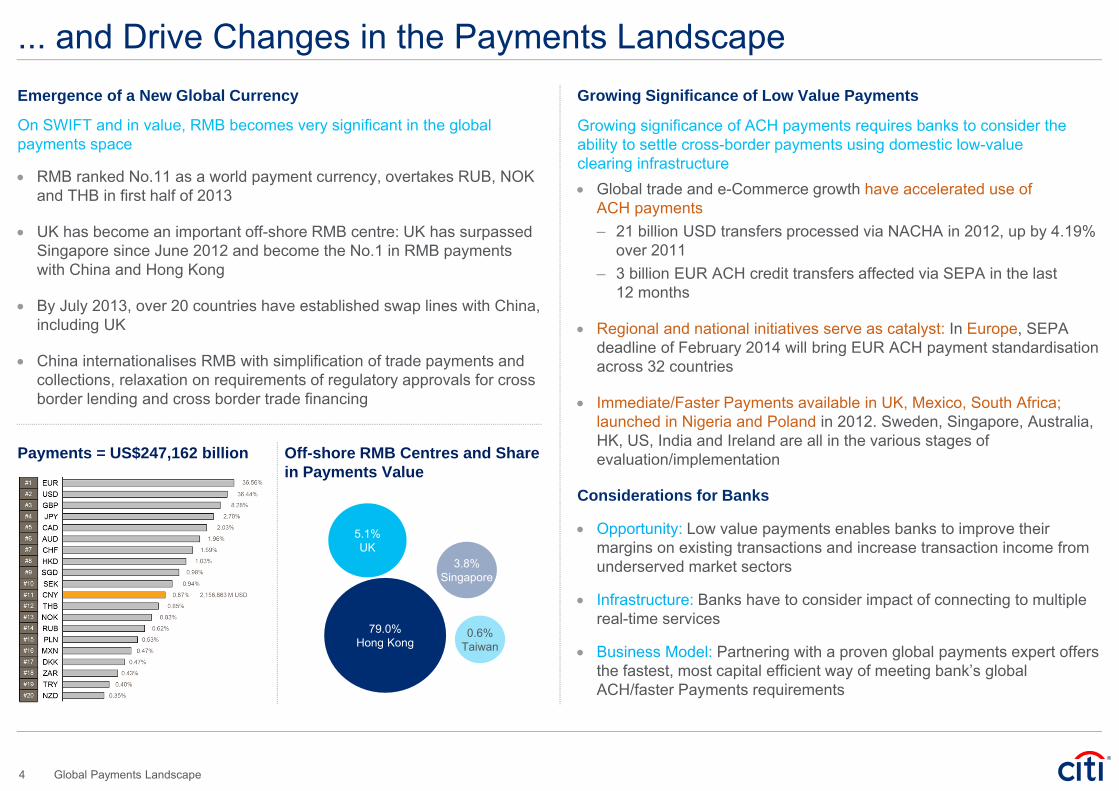

Emergence of a New Global Currency

... and Drive Changes in the Payments LandscapeGrowing Significance of Low Value Payments

Growing significance of ACH payments requires banks to consider the ability to settle cross-border payments using domestic low-valueclearing infrastructure Global trade and e-Commerce growth have accelerated use of

ACH payments– 21 billion USD transfers processed via NACHA in 2012, up by 4.19%

over 2011– 3 billion EUR ACH credit transfers affected via SEPA in the last

12 months

Regional and national initiatives serve as catalyst: In Europe, SEPA deadline of February 2014 will bring EUR ACH payment standardisation across 32 countries

Immediate/Faster Payments available in UK, Mexico, South Africa; launched in Nigeria and Poland in 2012. Sweden, Singapore, Australia, HK, US, India and Ireland are all in the various stages of evaluation/implementation

On SWIFT and in value, RMB becomes very significant in the global payments space

RMB ranked No.11 as a world payment currency, overtakes RUB, NOK and THB in first half of 2013

UK has become an important off-shore RMB centre: UK has surpassed Singapore since June 2012 and become the No.1 in RMB payments with China and Hong Kong

By July 2013, over 20 countries have established swap lines with China, including UK

China internationalises RMB with simplification of trade payments and collections, relaxation on requirements of regulatory approvals for cross border lending and cross border trade financing

Off-shore RMB Centres and Share in Payments Value

79.0%Hong Kong

5.1%UK

3.8%Singapore

0.6%Taiwan

Payments = US$247,162 billion

Considerations for Banks

Opportunity: Low value payments enables banks to improve their margins on existing transactions and increase transaction income from underserved market sectors

Infrastructure: Banks have to consider impact of connecting to multiple real-time services

Business Model: Partnering with a proven global payments expert offers the fastest, most capital efficient way of meeting bank’s global ACH/faster Payments requirements

4 Global Payments Landscape

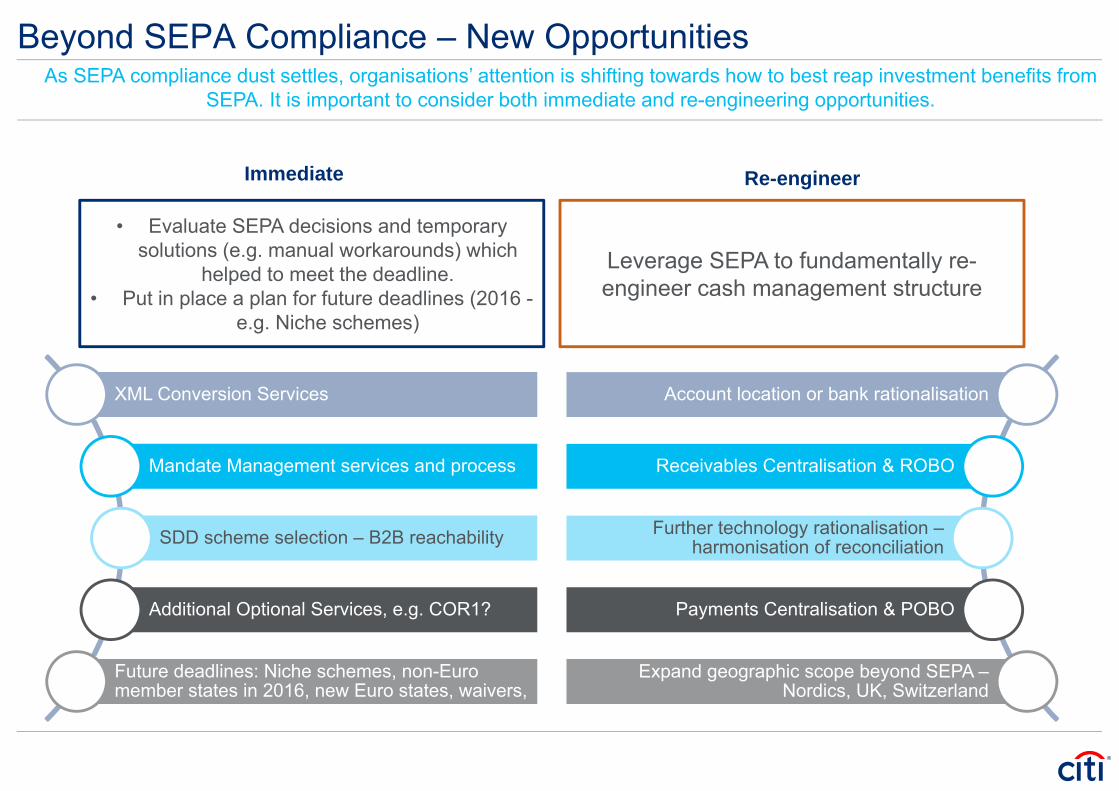

Beyond SEPA Compliance – New Opportunities

• Evaluate SEPA decisions and temporary solutions (e.g. manual workarounds) which

helped to meet the deadline.• Put in place a plan for future deadlines (2016 -

e.g. Niche schemes)

Leverage SEPA to fundamentally re-engineer cash management structure

XML Conversion Services

Mandate Management services and process

SDD scheme selection – B2B reachability

Additional Optional Services, e.g. COR1?

Future deadlines: Niche schemes, non-Euro member states in 2016, new Euro states, waivers,

Account location or bank rationalisation

Receivables Centralisation & ROBO

Further technology rationalisation –harmonisation of reconciliation

Payments Centralisation & POBO

Expand geographic scope beyond SEPA –Nordics, UK, Switzerland

As SEPA compliance dust settles, organisations’ attention is shifting towards how to best reap investment benefits from SEPA. It is important to consider both immediate and re-engineering opportunities.

Immediate Re-engineer

2. Regulatory Changes

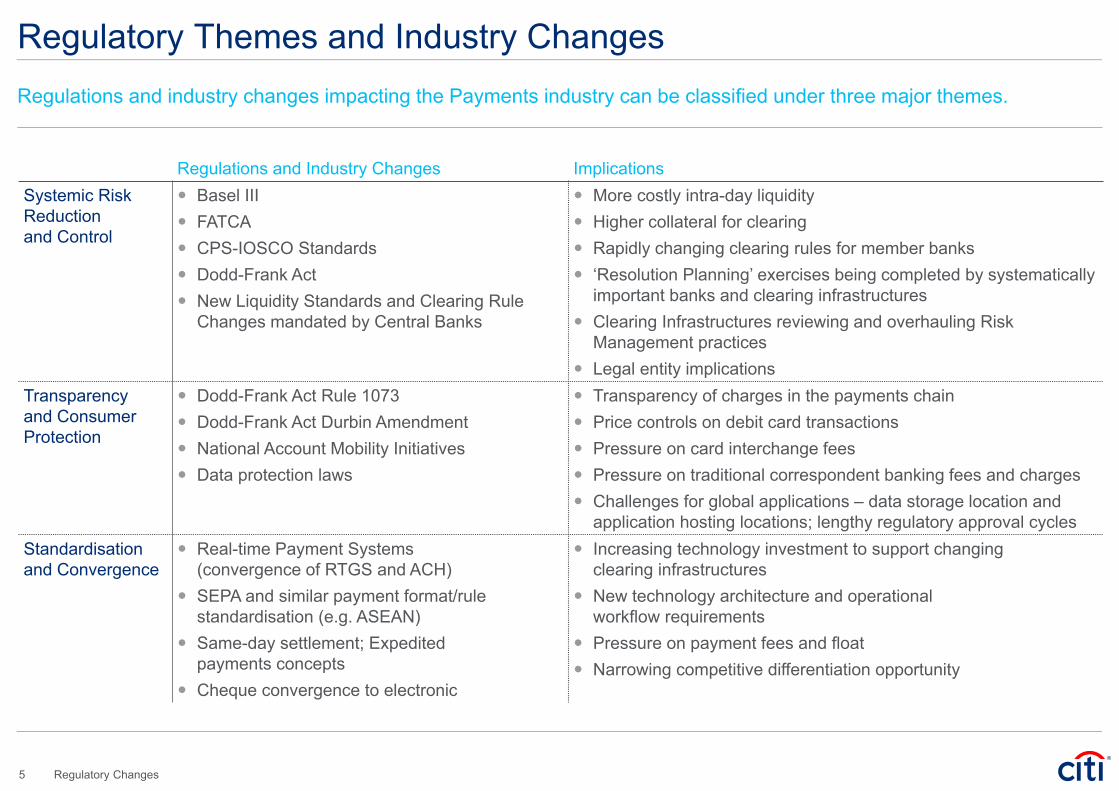

Regulations and Industry Changes ImplicationsSystemic Risk Reduction and Control

Basel III FATCA CPS-IOSCO Standards Dodd-Frank Act New Liquidity Standards and Clearing Rule

Changes mandated by Central Banks

More costly intra-day liquidity Higher collateral for clearing Rapidly changing clearing rules for member banks ‘Resolution Planning’ exercises being completed by systematically

important banks and clearing infrastructures Clearing Infrastructures reviewing and overhauling Risk

Management practices Legal entity implications

Transparency and Consumer Protection

Dodd-Frank Act Rule 1073 Dodd-Frank Act Durbin Amendment National Account Mobility Initiatives Data protection laws

Transparency of charges in the payments chain Price controls on debit card transactions Pressure on card interchange fees Pressure on traditional correspondent banking fees and charges Challenges for global applications – data storage location and

application hosting locations; lengthy regulatory approval cyclesStandardisation and Convergence

Real-time Payment Systems (convergence of RTGS and ACH)

SEPA and similar payment format/rule standardisation (e.g. ASEAN)

Same-day settlement; Expedited payments concepts

Cheque convergence to electronic

Increasing technology investment to support changing clearing infrastructures

New technology architecture and operational workflow requirements

Pressure on payment fees and float Narrowing competitive differentiation opportunity

Regulatory Themes and Industry ChangesRegulations and industry changes impacting the Payments industry can be classified under three major themes.

5 Regulatory Changes

Recent Developments

Proposed Payment Services Directive II and regulation on Card Interchange Fees published in the 24th of July 2013 by the EU Commission

It is not expected that the directive will be rushed through before May 2014 EU elections and therefore unlikely that PSD II will be agreed and adopted before Q1/Q2 2015.

Proposed Changes in the PSD II

1. Introduction of ‘third party payment providers’ (TPPs) – can perform services with access to the customer's account and initiating payments .The provider will be licensed under PSD II. Specific for online banking in the context of e-commerce transactions over the web.

– PSD II established the right for all users (consumer and corporate) to make use of such service providers..– Customers encouraged to give away their personalised security details in order to enable the TPP to access online banking portal and to

initiate the payment on their behalf. – The TPP will be able to do so without first enrolling with the account holding bank– TPP will re-use the customer's authentication details and perform an impersonation (which in case of fraud would be a ‘man-in-the-middle-

attack’). – The burden of proof would always remain with the account holding bank, which will not be able to proof that a third party accessed the

account.

2. Payment systems that are designated by the Settlement Finality Directive (e.g. Target2, Euro 1, CHAPS etc.) should allow indirect participation to non-bank payment institutions:

– Potential concern is that direct participating banks would have to take indirect non-bank payment institutions onto their books.

3. Directive maintains the ability to agree different liability rules and some of the operational code of conduct related elements with corporate clients (as compared to consumers)

4. The initial concern that the Commission would propose strict liability for PSD transactions that have one leg outside the EU, has been removed and additional information requirements proposed for all currencies and transactions with one leg outside the EU, are now limited to consumer information requirements and will not impact corporations/business users.

Update on Payment Services Directive IIEU Commission is currently reviewing PSD II with continued advocacy by Citi

7 Regulatory Changes

3. Partnership Opportunities

Benefit from Trends through Partnership

Growth Driven by New Global Dynamics …

Banks intermediating flows over an extensive network can benchmark pricing points such as beneficiary deductions locally rather than go through the “trial and error” method and leave money on the table

Lower transaction costs to our clients by formulating interbank charging agreements with numerous of banks at reduced rates

Generate incremental fee income from capturing FX fromcross-border payments

… assisting you to Drive Revenue by leveraging a robust GlobalBranch Network

Capabilities to Address Client Needs …

Offer ‘one-stop-shop’ solutions for domestic and international payments needs

Flexible infrastructure and active collaboration provides the opportunity to acquire more share of the growing globalpayments wallet

… increasing Client Stickiness with innovative tools and expansion of payment types

Responding to a New Regulatory Environment …

Thought leadership and shared intellectual property can help to meet the evolving needs of clients and respond to theever-increasing regulatory demands

Improve data capture and quality, as well as analytics, to improve client and regulatory insight

… solutioning forTransparency and Controlfor effective response to regulatory changes(i.e. Dodd-Frank 1073)

Streamlined Technology and Processing …

Differentiate yourself in the market with state-of-the-art proprietaryback-end technology platform, with on-going enhancementsand updates

Leveraging the partner with multitude of correspondent relationships and branch networks

… gaining Cost Efficiencies by leveraging technology platforms andtransactions processing

1

2

3

4

8 Partnership Opportunities

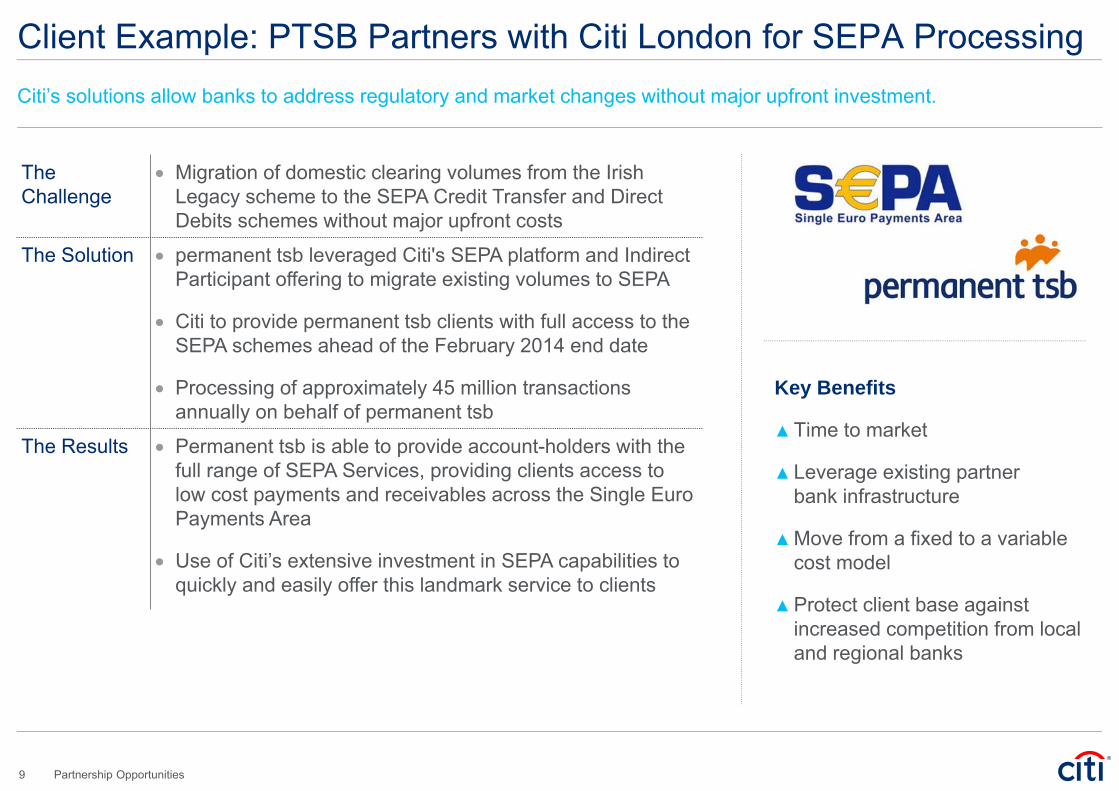

Client Example: PTSB Partners with Citi London for SEPA ProcessingCiti’s solutions allow banks to address regulatory and market changes without major upfront investment.

The Challenge

Migration of domestic clearing volumes from the Irish Legacy scheme to the SEPA Credit Transfer and Direct Debits schemes without major upfront costs

The Solution permanent tsb leveraged Citi's SEPA platform and Indirect Participant offering to migrate existing volumes to SEPA

Citi to provide permanent tsb clients with full access to the SEPA schemes ahead of the February 2014 end date

Processing of approximately 45 million transactions annually on behalf of permanent tsb

The Results Permanent tsb is able to provide account-holders with the full range of SEPA Services, providing clients access to low cost payments and receivables across the Single Euro Payments Area

Use of Citi’s extensive investment in SEPA capabilities to quickly and easily offer this landmark service to clients

Key Benefits

▲Time to market

▲Leverage existing partner bank infrastructure

▲Move from a fixed to a variable cost model

▲Protect client base against increased competition from local and regional banks

9 Partnership Opportunities

Client Example: Global Bank Expanding FX CapabilitiesCiti’s solution allows banks to expand their FX capabilities in cross-currency payments whilst improving transactional margin.

The Challenge

Global bank needed to derive additional revenue from payment flows to US

Eliminate the need for the bank to undertake development in payment conversion capability for local currencies

The Solution Citi’s Global Clearing Multi-currency Gateway capabilities leveraged in converting customer transaction messages from EUR and GBP to USD of the beneficiary account domiciled in the US

Transactions eligible for auto conversion identified from information available to Citi about the currency of the relevant beneficiary bank account held in thedestination country

Transparent FX rates applied on client customers’ transfers – fixed spreads over interbank Reuter’s comparable rates refreshed hourly

The Results FX conversion process is moved to Citi and bank gets a share of the FX revenue

Bring quickly to market the cross-currencypayments solutions

Key Benefits

▲ Increase revenues through FX revenue share

▲Automated foreign exchange conversion for higher STP rates

▲Partner bank local market expertise translating into lower level of erroneous conversions

10 Partnership Opportunities

4. Innovation @ Citi

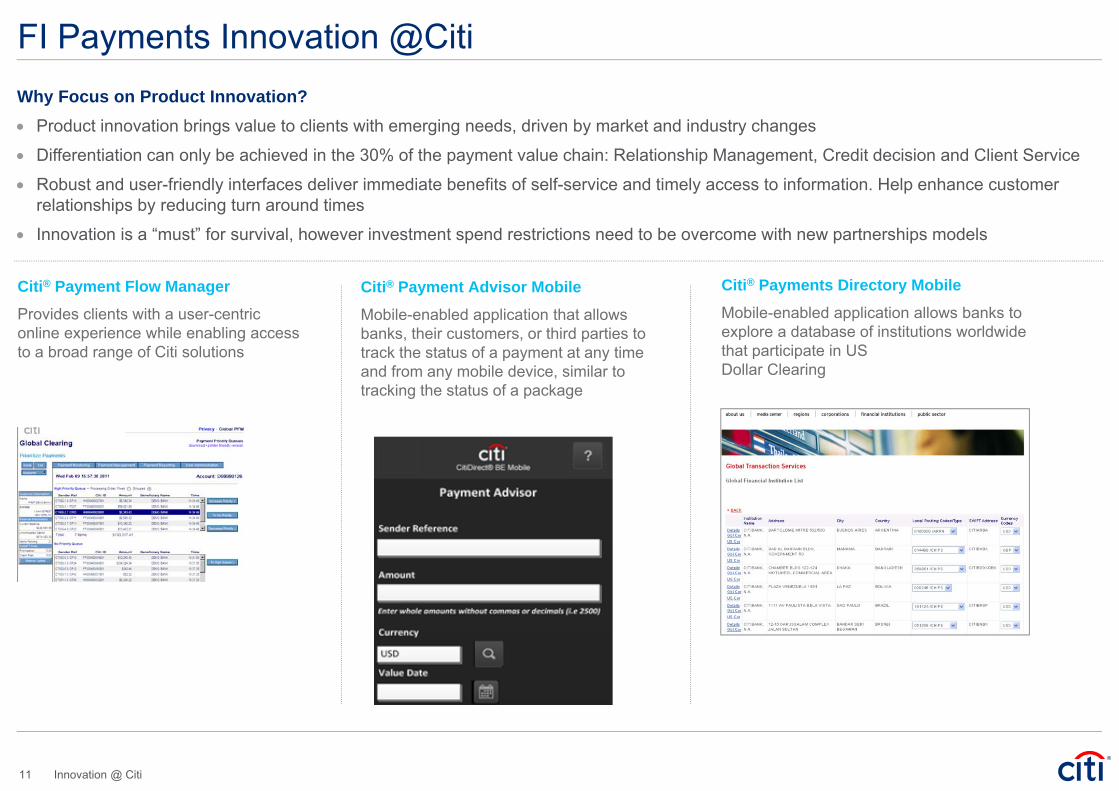

FI Payments Innovation @Citi

Citi® Payment Flow Manager

Provides clients with a user-centric online experience while enabling access to a broad range of Citi solutions

Citi® Payment Advisor Mobile

Mobile-enabled application that allows banks, their customers, or third parties to track the status of a payment at any time and from any mobile device, similar to tracking the status of a package

Citi® Payments Directory Mobile

Mobile-enabled application allows banks to explore a database of institutions worldwide that participate in USDollar Clearing

Why Focus on Product Innovation? Product innovation brings value to clients with emerging needs, driven by market and industry changes

Differentiation can only be achieved in the 30% of the payment value chain: Relationship Management, Credit decision and Client Service

Robust and user-friendly interfaces deliver immediate benefits of self-service and timely access to information. Help enhance customer relationships by reducing turn around times

Innovation is a “must” for survival, however investment spend restrictions need to be overcome with new partnerships models

11 Innovation @ Citi