27

PV Markzttan Masson, Director Becquerel Institute Global PV Markets & Industry Status Ir Gaëtan Masson Director, Becquerel Institute Vice-Chairman, EU PV Technology & Innovation Platform

PV Markzttan Masson, Director

Becquerel Institute

Global PV Markets &

Industry Status

Ir Gaëtan Masson

Director, Becquerel Institute

Vice-Chairman, EU PV Technology & Innovation Platform

2 ETIP-PV 2017 Becquerel Institute

2

BECQUEREL INSTITUTE

• Research oriented Institute and consulting company for Solar PV Technologies.

• Global PV Market Analysis including competitiveness and economics.

• Industry analysis together with quality & reliability.

• Integration into electricity systems (grids and markets).

• In-house experts / Global network of experts and stakeholders

• PV Market Alliance partner

3 ETIP-PV 2017 Becquerel Institute

3

DYING UTILITIE Revolution

Dead technologies Dying utilities

4 ETIP-PV 2017 Becquerel Institute

4

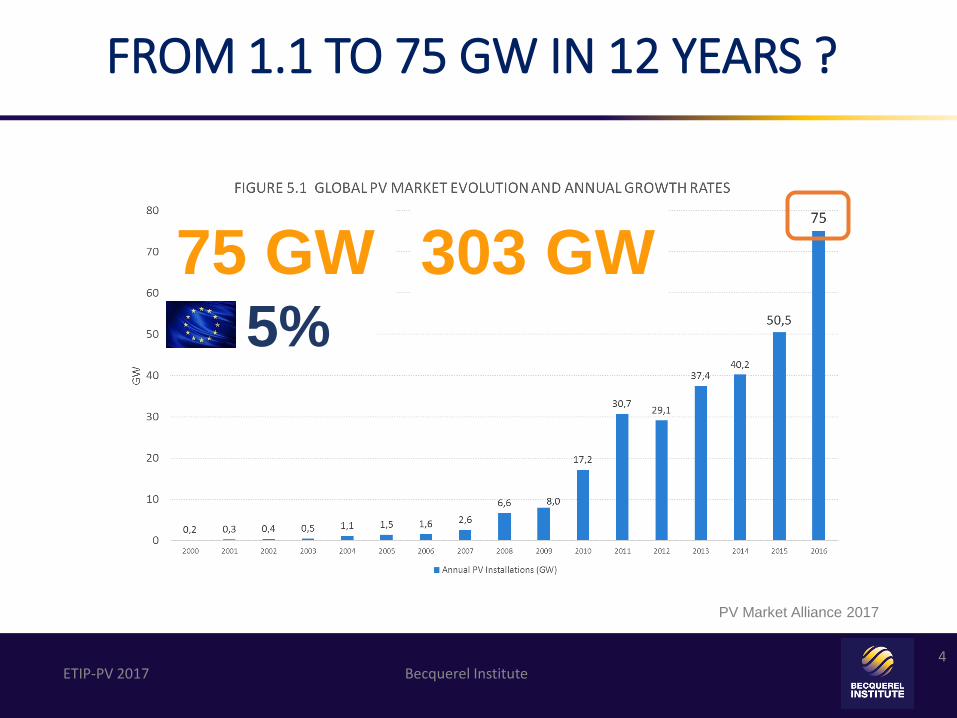

FROM 1.1 TO 75 GW IN 12 YEARS ?

75 GW 5%

PV Market Alliance 2017

303 GW

5 ETIP-PV 2017 Becquerel Institute

5

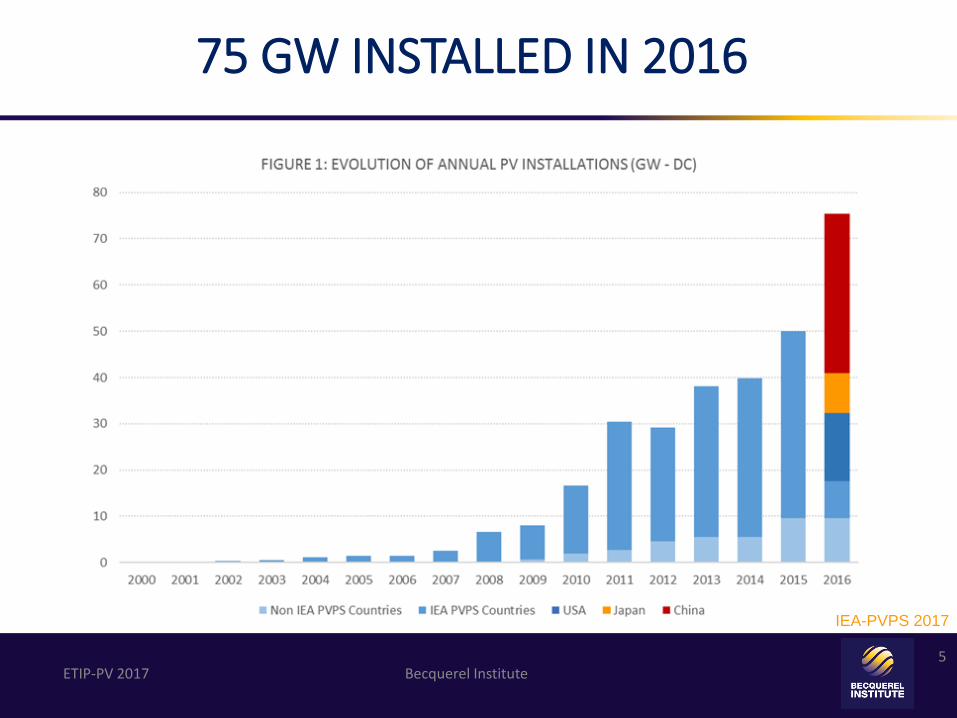

75 GW INSTALLED IN 2016

IEA-PVPS 2017

6 ETIP-PV 2017 Becquerel Institute

6

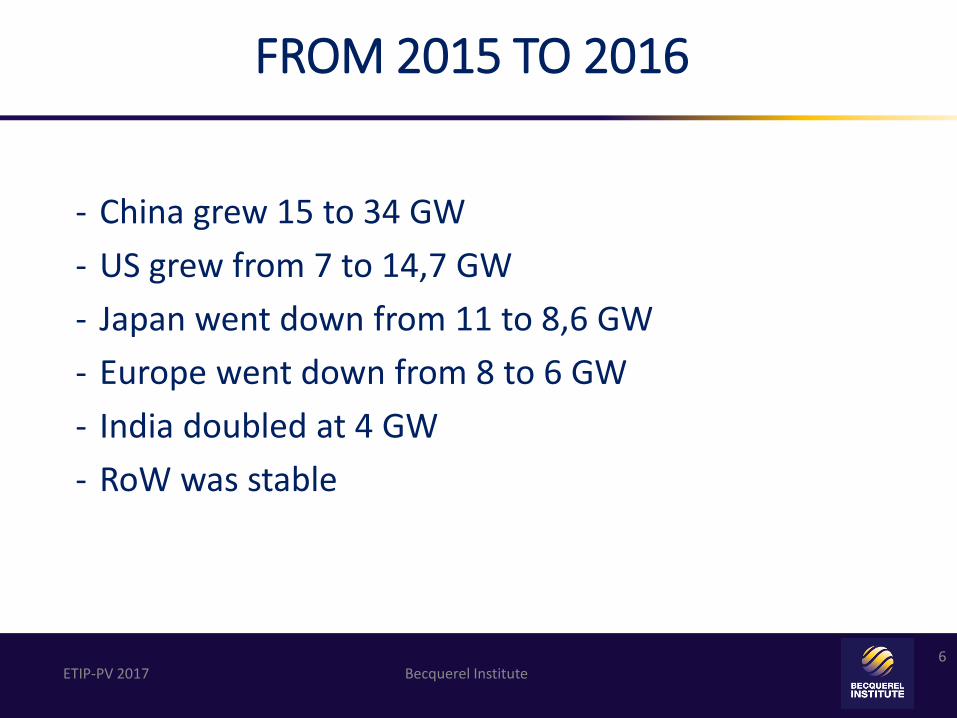

FROM 2015 TO 2016

- China grew 15 to 34 GW

- US grew from 7 to 14,7 GW

- Japan went down from 11 to 8,6 GW

- Europe went down from 8 to 6 GW

- India doubled at 4 GW

- RoW was stable

7 ETIP-PV 2017 Becquerel Institute

7

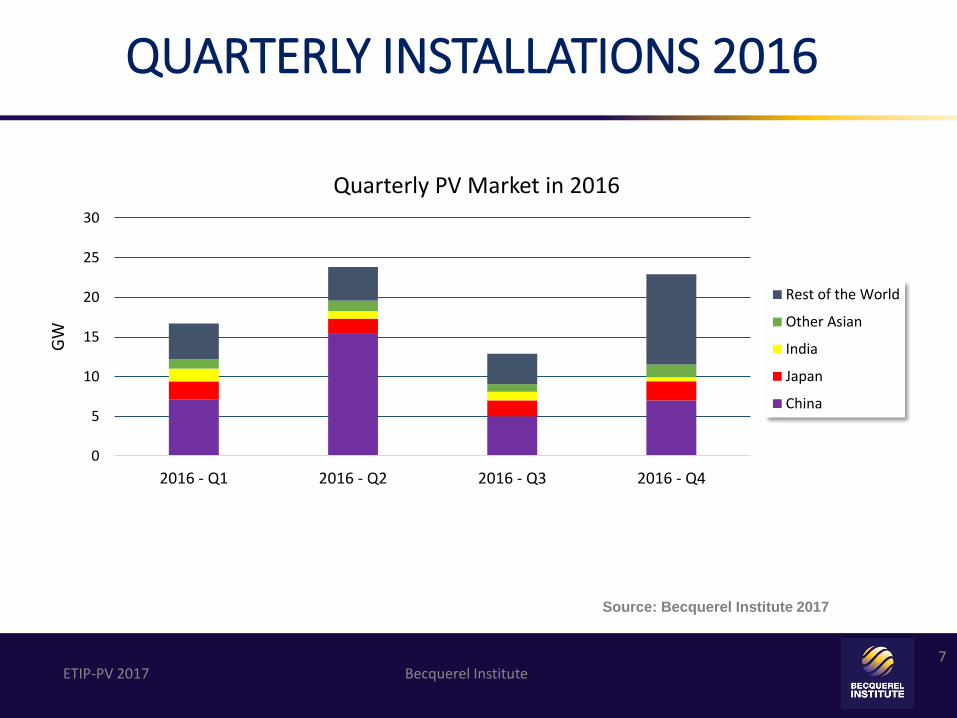

QUARTERLY INSTALLATIONS 2016

0

5

10

15

20

25

30

2016 - Q1 2016 - Q2 2016 - Q3 2016 - Q4

GW

Quarterly PV Market in 2016

Rest of the World

Other Asian

India

Japan

China

Source: Becquerel Institute 2017

8 ETIP-PV 2017 Becquerel Institute

8

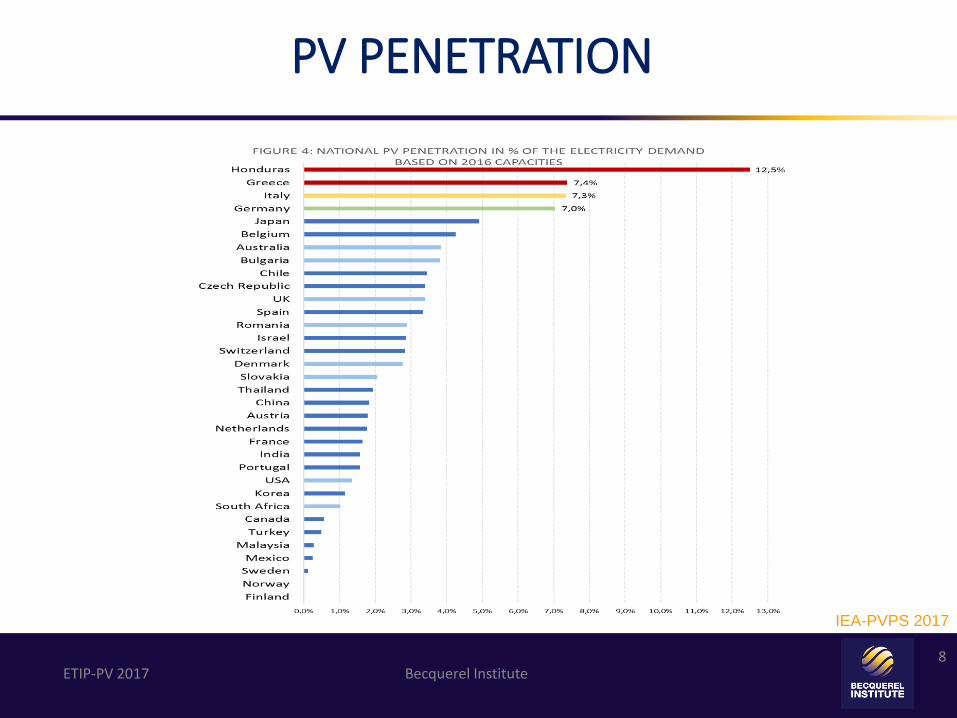

PV PENETRATION

IEA-PVPS 2017

9 ETIP-PV 2017 Becquerel Institute

9

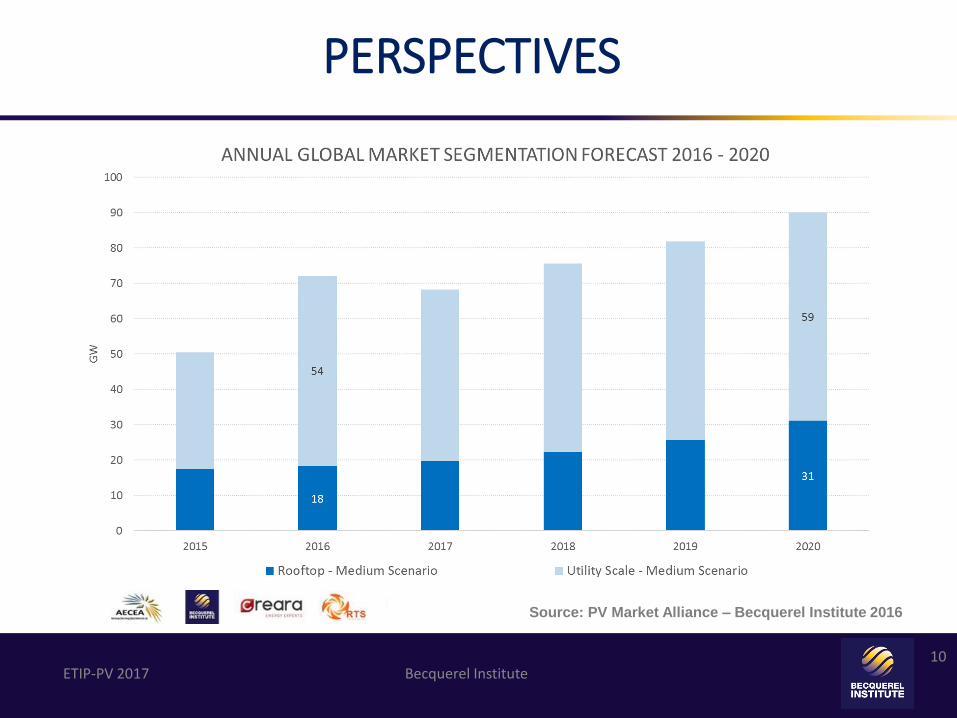

PERSPECTIVES

Source: PV Market Alliance – Becquerel Institute 2016

75

10 ETIP-PV 2017 Becquerel Institute

10

PERSPECTIVES

>>> The cheapest source of electricity

Source: PV Market Alliance – Becquerel Institute 2016

11 ETIP-PV 2017 Becquerel Institute

11

MARKET DRIVERS

PV market developments in …

- China ?

- Japan – stable or decreasing

- US – uncertain after 2017

- India growing

- Europe – stable or growing?

- RoW: stable or growing

12 ETIP-PV 2017 Becquerel Institute

12

TECHNOLOGIES

13 ETIP-PV 2017 Becquerel Institute

13

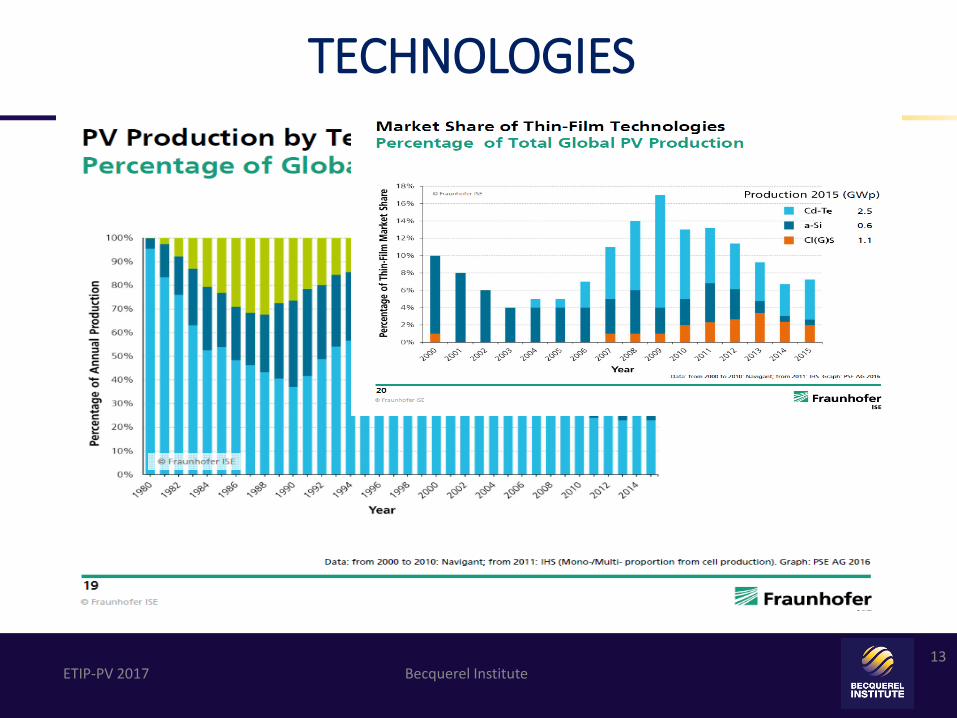

TECHNOLOGIES

14 ETIP-PV 2017 Becquerel Institute

14

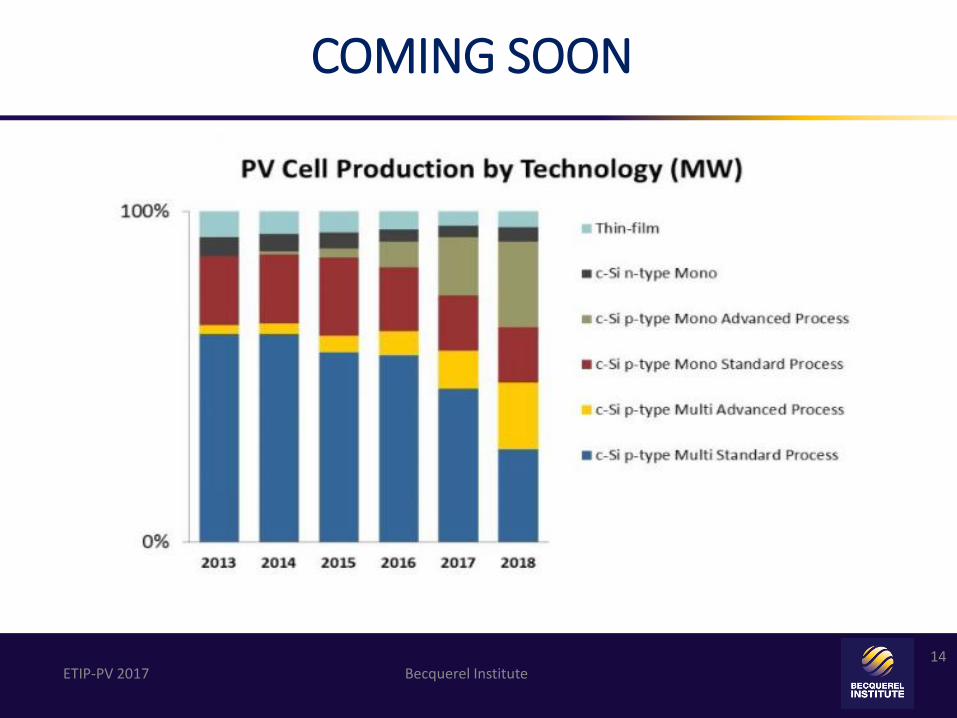

COMING SOON

15 ETIP-PV 2017 Becquerel Institute

15

COSTS AND PRICES

16 ETIP-PV 2017 Becquerel Institute

16

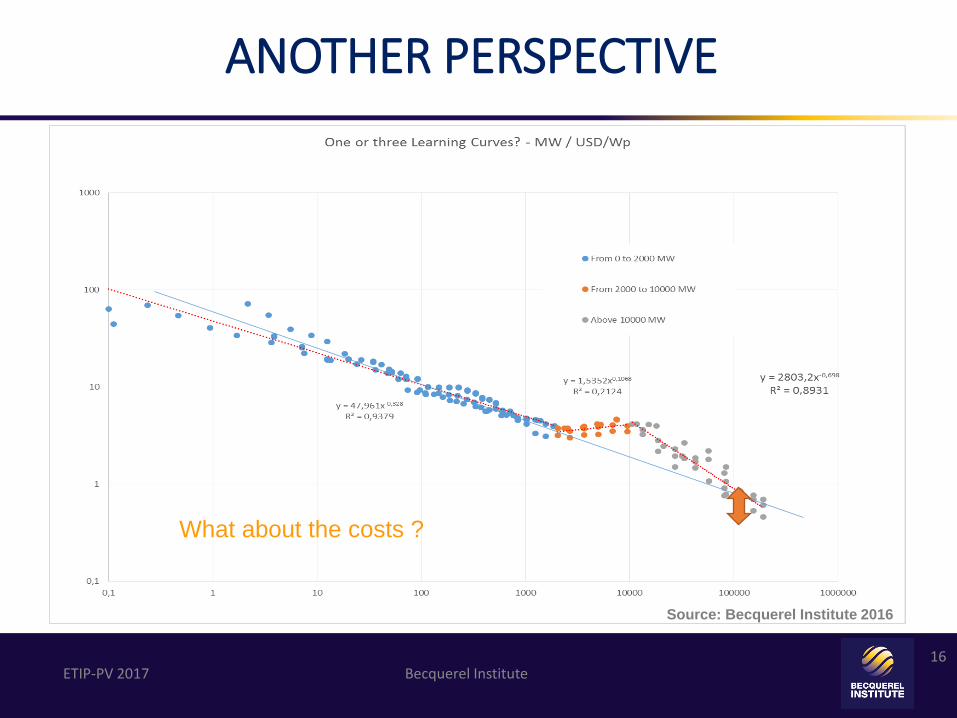

ANOTHER PERSPECTIVE

Source: Becquerel Institute 2016

What about the costs ?

17 ETIP-PV 2017 Becquerel Institute

17

PV PRICE LEARNING CURVE

0,4 USD/Wp

97%

production

37% LC

20% LC

0,45 USD/WP – 275 GW

Source: Becquerel Institute 2016

0,38 USD/WP – 300 GW

18 ETIP-PV 2017 Becquerel Institute

18

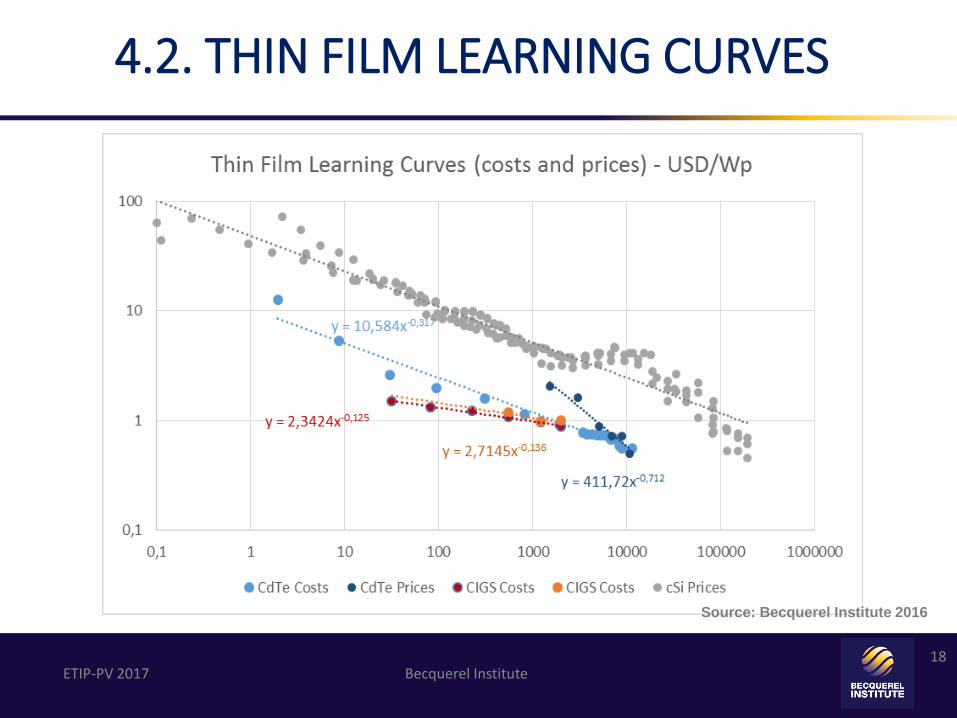

4.2. THIN FILM LEARNING CURVES

Source: Becquerel Institute 2016

19 ETIP-PV 2017 Becquerel Institute

19

PRICE EVOLUTION OF PV COMPONENTS

0

0,1

0,2

0,3

0,4

0,5

0,6

PV Grade Polysilicon(9N/9N+)

156 mm Multi cSiSolar Wafer

156 mm Mono cSiSolar Wafer

156 mm Mono cSiSolar Wafer Outside

China

Multi cSi Cell Mono cSi Cell Multi cSi SolarModule

USD

/W

Q3 2016 Q3 2016 Q4 2016 Q4 2016

Source: Becquerel Institute 2017

20 ETIP-PV 2017 Becquerel Institute

20

PRICE AND MARKET SITUATION

- Low module prices reflect uncertainty and overcapacities. But what over the other steps of the value chain?

- High demand in Q1 2017 in China could mean a growing market depending on Q3-Q4. Uncertainty again.

- Time to unlock new markets if demand goes down is > 1 year. Faster this time? Non-tier-1 markets are not growing fast.

21 ETIP-PV 2017 Becquerel Institute

21

FOOD FOR THOUGHTS

22 ETIP-PV 2017 Becquerel Institute

22

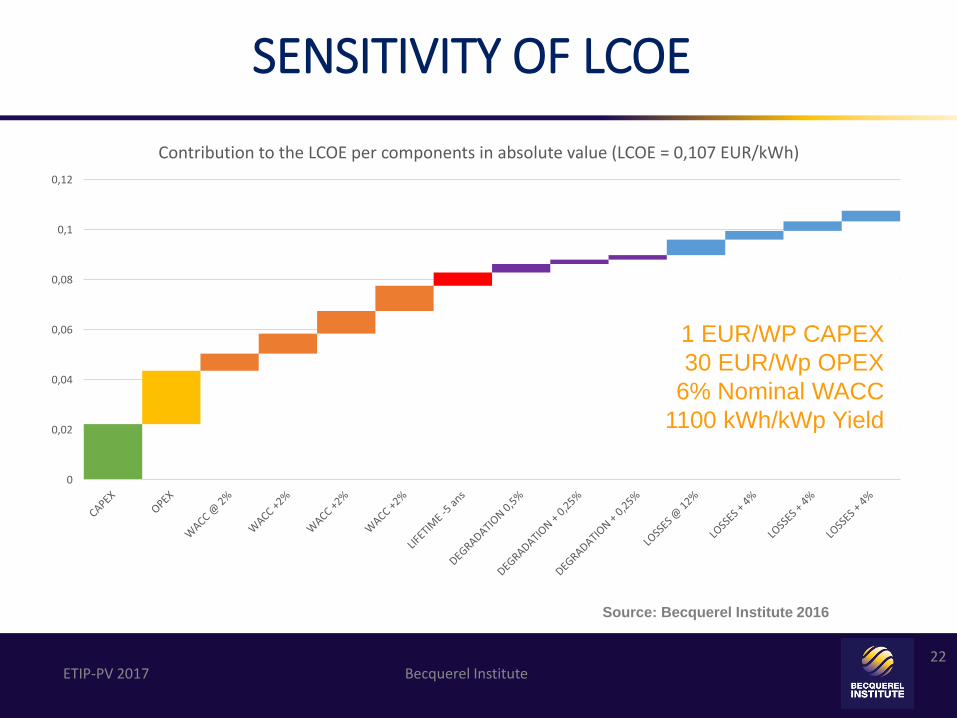

SENSITIVITY OF LCOE

0

0,02

0,04

0,06

0,08

0,1

0,12

Contribution to the LCOE per components in absolute value (LCOE = 0,107 EUR/kWh)

Source: Becquerel Institute 2016

1 EUR/WP CAPEX

30 EUR/Wp OPEX

6% Nominal WACC

1100 kWh/kWp Yield

23 ETIP-PV 2017 Becquerel Institute

23

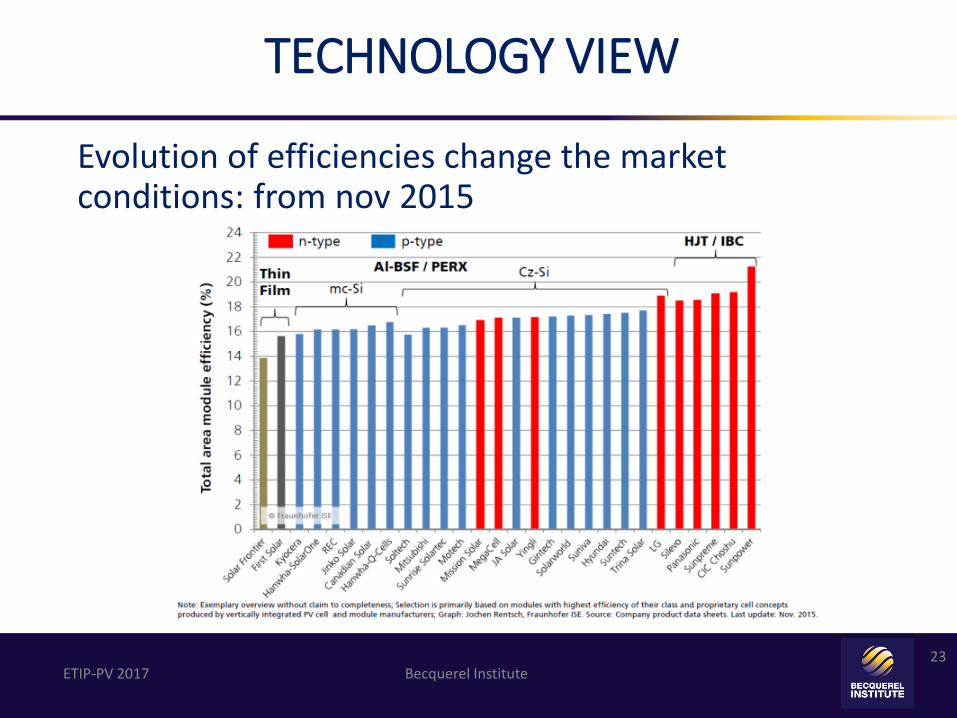

TECHNOLOGY VIEW

Evolution of efficiencies change the market conditions: from nov 2015

24 ETIP-PV 2017 Becquerel Institute

24

GAME CHANGER?

Evolution of efficiencies change the market conditions: thin film CdTe become more competitive while all efficiencies are improving.

Source: Becquerel Institute 2017

25 ETIP-PV 2017 Becquerel Institute

25

CONCLUSIONS

Will we reach more than 75 GW ? Yes but when?

China is the key market to follow.

And the speed at which the market can develop.

Technologies are not eternal.

Leaders are also under pressure.

The future is open

26 ETIP-PV 2017 Becquerel Institute

26

ENJOY THE SUN EVEN IF…