23

Global Tactical Asset Allocation October 2003 Giorgio De Santis Managing Director Quantitative Strategies Group

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | job-goodman |

| View: | 219 times |

| Download: | 1 times |

Global Tactical Asset Allocation

October 2003

Giorgio De SantisManaging DirectorQuantitative Strategies Group

2Global Tactical Asset Allocation

A Overview of GTAA

i) Definition and objectives

ii) A brief history of (G)TAA

B Motivating GTAA

i) Theoretical justifications

ii) Some empirical evidence

C Implementing a GTAA program

i) Portfolio construction

ii) An example: Risk budget and optimal portfolio

iii) Benefits of using futures and forwards

D Concluding remarks

Discussion outline

Overview of GTAA

4Global Tactical Asset Allocation

GTAA is like security selection, where the securities are country stock markets, bond markets

and currencies.

In contrast to stock and bond selection strategies, which focus on individual stocks and

bonds, GTAA focuses on countries and broad asset classes.

GTAA is a global strategy designed to capture relative value opportunities across countries, currencies and asset classes

Traditional TAA

1

2

3

4

5Global Tactical Asset Allocation

1990s: Value-oriented TAA

managers experience difficult environment

Top-tier GTAA managers continue to deliver promising

results

2000: Renewed interest in GTAA strategies due to:

Increasing liquidity in global derivative markets

Increasing evidence of return predictability across and within asset

classes

Recognition that quantitative models can manage risk effectively

Increased familiarity of institutional investors with GTAA

1952 1960 1970 1980 1990 2000

Mid 1970s: Tactical Asset Allocation

(TAA) first used by US. pensions to capitalize on changing opportunities in a single country’s stock, bond and cash markets

Late 1980s: Interest in TAA increases

significantly following 1987 market crash

GTAA first used by US pensions to capitalize on changing opportunities at the country and global asset class level

1986: Brinson, Hood and Beebower

Strategic asset allocation explains more than 90% of institutional portfolio risk

Harry Markowitz publishes “Portfolio Selection”

Given a set of expected returns and risk estimates, portfolios with maximum return per unit of risk can be constructed

1964: Sharpe’s “Capital Asset Pricing Model”

In equilibrium, optimal portfolios are combinations of T-bills and the market capitalization portfolio

1991: Black-Litterman propose practical model to overcome shortcomings of traditional mean-variance analysis

1990: Black’s “Universal Hedging” defines global market equilibrium

A timeline of asset allocationThe evolution of modern portfolio theory

6Global Tactical Asset Allocation

A GTAA process seeks to: Reduce unintended asset allocation risk (Step 1): Generate alpha (Step 2):

Result: Improved information ratio

1 Unintended underlying portfolio allocation returns and tracking error represent the asset allocation of the underlying managers multiplied by the asset class returns. They do not represent the return on the actual underlying portfolio holdings (excess return from security selection) of active managers. Rather, they represent the return and

tracking error to the benchmark of the asset allocation “drift” due to changes in asset valuations as well as unintended country and currency exposures by the underlying active managers.Note: For illustrative purposes only. The returns presented herein are gross. Past performance is not indicative of future results, which may vary.

Improving the overall risk/return profile

Completion

Overlay

7Global Tactical Asset Allocation

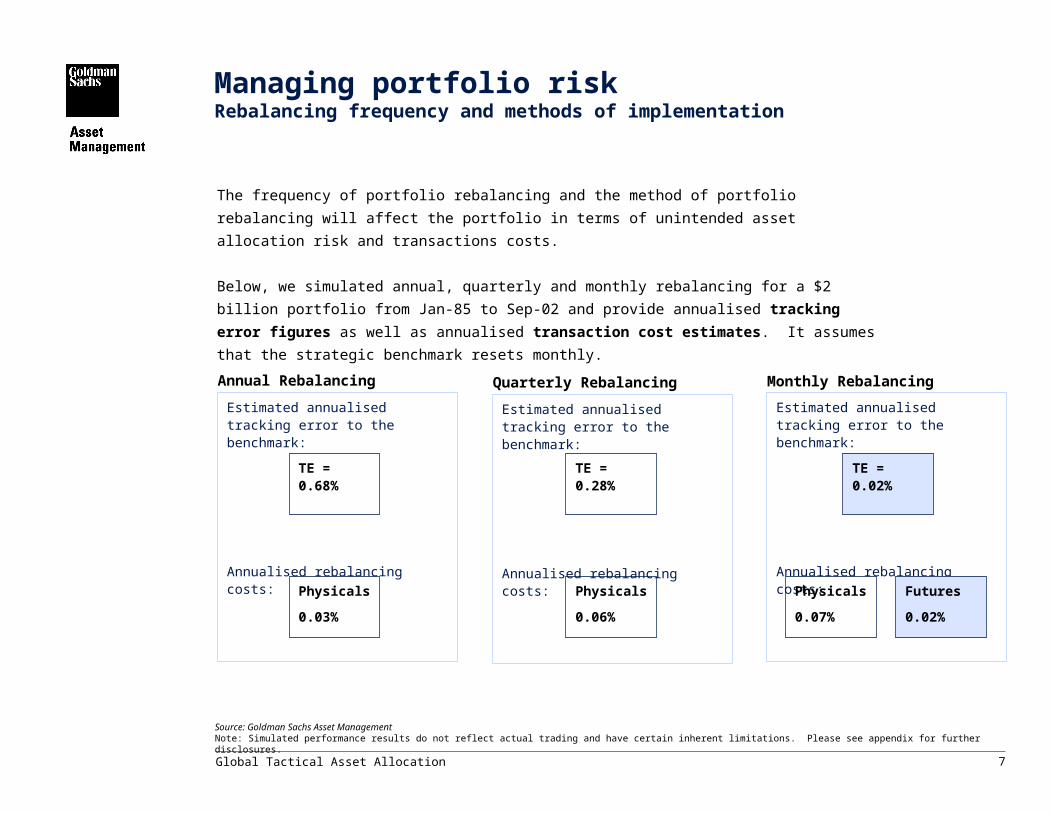

Managing portfolio riskRebalancing frequency and methods of implementation

The frequency of portfolio rebalancing and the method of portfolio rebalancing will affect the portfolio

in terms of unintended asset allocation risk and transactions costs.

Below, we simulated annual, quarterly and monthly rebalancing for a $2 billion portfolio from Jan-85

to Sep-02 and provide annualised tracking error figures as well as annualised transaction cost

estimates. It assumes that the strategic benchmark resets monthly.

Estimated annualised tracking error to the benchmark:

Annualised rebalancing costs:

Annual Rebalancing

Physicals

0.03%

TE = 0.68%

Estimated annualised tracking error to the benchmark:

Annualised rebalancing costs:

Quarterly Rebalancing

Physicals

0.06%

TE = 0.28%

Monthly Rebalancing

Estimated annualised tracking error to the benchmark:

Annualised rebalancing costs:

Physicals

0.07%

Futures

0.02%

TE = 0.02%

Source: Goldman Sachs Asset ManagementNote: Simulated performance results do not reflect actual trading and have certain inherent limitations. Please see appendix for further disclosures.

Theory and evidence in support of a GTAA program

9Global Tactical Asset Allocation

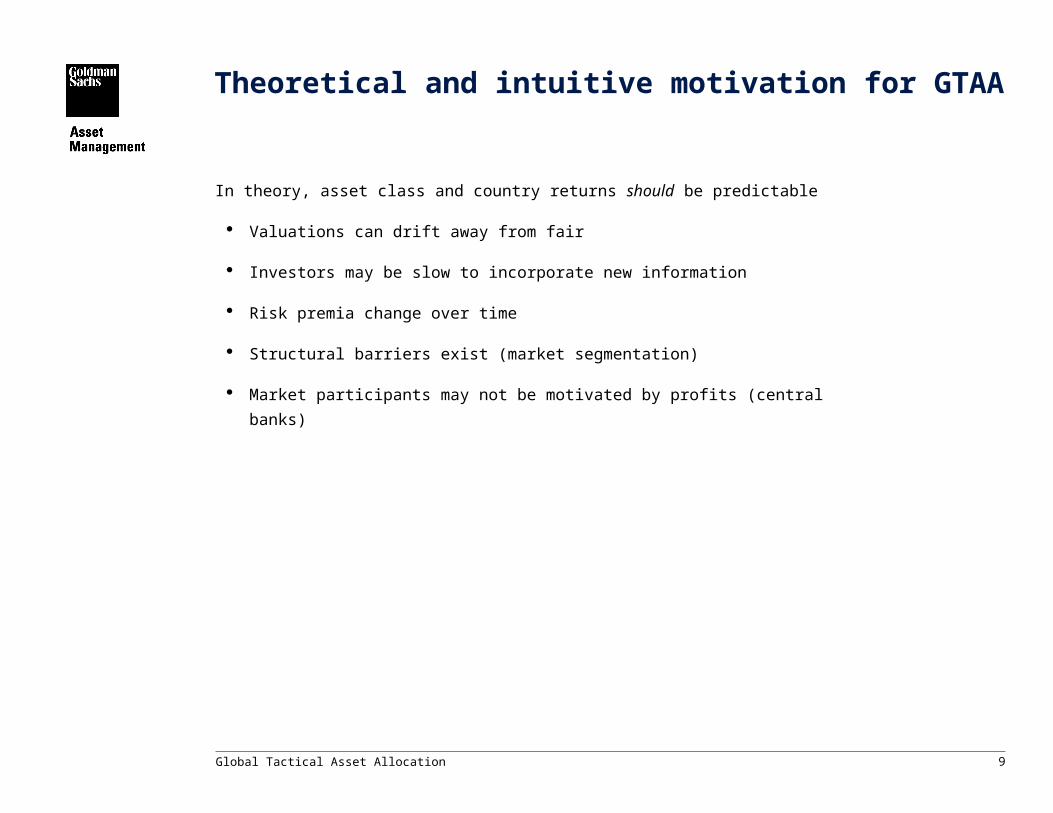

Theoretical and intuitive motivation for GTAA

In theory, asset class and country returns should be predictable

Valuations can drift away from fair

Investors may be slow to incorporate new information

Risk premia change over time

Structural barriers exist (market segmentation)

Market participants may not be motivated by profits (central banks)

10Global Tactical Asset Allocation

1 Global bond market tritile sorts cover period: January 1985 – December 2001Note: Simulated performance results do not reflect actual trading and have certain inherent limitations. Please see appendix for further disclosures.

Some evidence that country returns are predictable

Annualized gross returns on simulated three-way sorts of country and currency returns (1980 – 2001)

Currencies:

Global BondMarkets1:

Global Stock Markets:

Over time, inexpensive countries and high-momentum countries have provided significantly higher returns.

12.9%14.6%

17.8%

0.0%

5.0%

10.0%

15.0%

20.0%

High P/B Medium P/B Low P/B

Valuation theme

8.7%

9.5%10.0%

7.0%

8.0%

9.0%

10.0%

11.0%

Flat Curve Medium Curve Steep Curve

5.2%6.4%

9.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Expensive PPP Medium PPP Cheap PPP

Momentum theme

8.5%

15.4%

21.7%

0%5%

10%15%

20%25%

LowMomentum

MediumMomentum

HighMomentum

8.8%8.7%

9.2%

8.4%8.6%8.8%

9.0%9.2%9.4%

LowMomentum

MediumMomentum

HighMomentum

5.0%6.9%

8.4%

0.0%

2.0%4.0%

6.0%8.0%

10.0%

LowMomentum

MediumMomentum

HighMomentum

11Global Tactical Asset Allocation

The performance results stated above are backtested based on a methodology that is derived from an analysis of past market data with the benefit of hindsight. These results do not reflect the performance of a GSAM managed account or composite and are being shown for informational purposes only. If GSAM had managed your account during the period shown above it is highly improbable that your account would have been managed in a similar fashion due to differences in economic and market conditions. The performance results disclosed herein do not represent the results of actual trading using client assets. The backtested performance results depicted above do not reflect the deduction of advisory fees, brokerage or other commissions or exchange fees or any other expenses a client would have to pay.

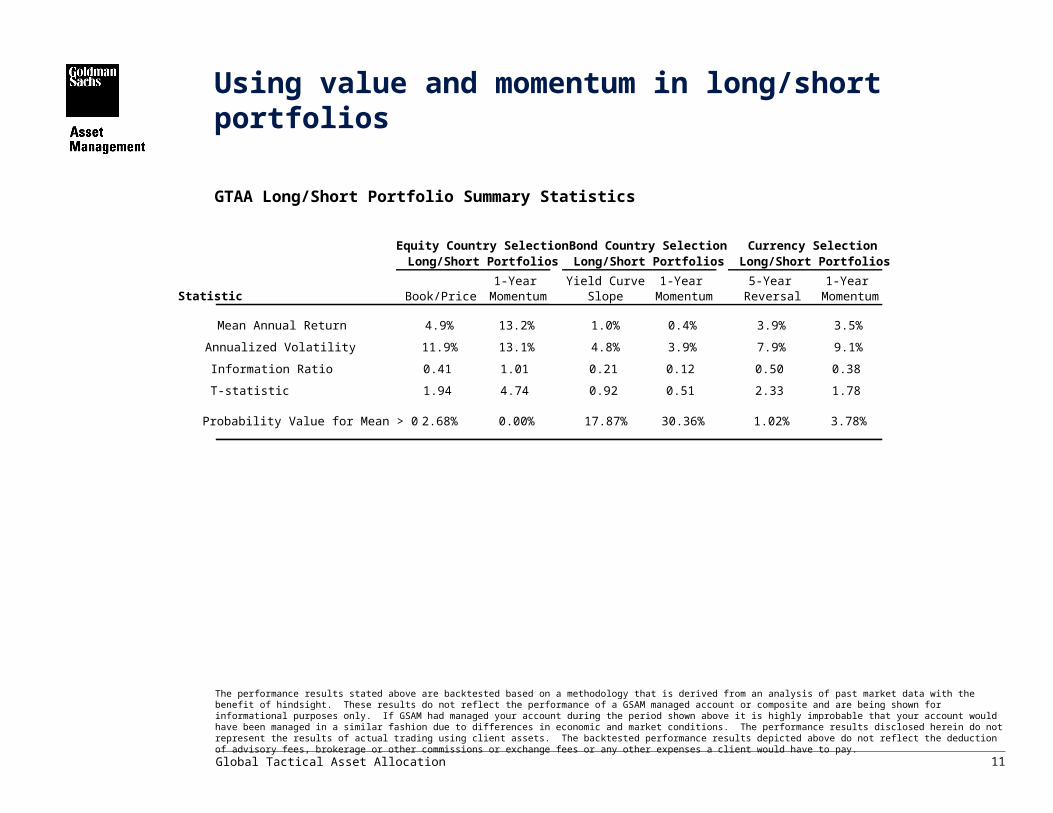

Using value and momentum in long/short portfolios

GTAA Long/Short Portfolio Summary Statistics

Equity Country Selection Long/Short Portfolios

Bond Country Selection Long/Short Portfolios

Currency Selection Long/Short Portfolios

Statistic Book/Price1-Year

MomentumYield Curve

Slope1-Year

Momentum5-Year

Reversal1-Year

Momentum

Mean Annual Return 4.9% 13.2% 1.0% 0.4% 3.9% 3.5%

Annualized Volatility 11.9% 13.1% 4.8% 3.9% 7.9% 9.1%

Information Ratio 0.41 1.01 0.21 0.12 0.50 0.38

T-statistic 1.94 4.74 0.92 0.51 2.33 1.78

Probability Value for Mean > 0 2.68% 0.00% 17.87% 30.36% 1.02% 3.78%

12Global Tactical Asset Allocation

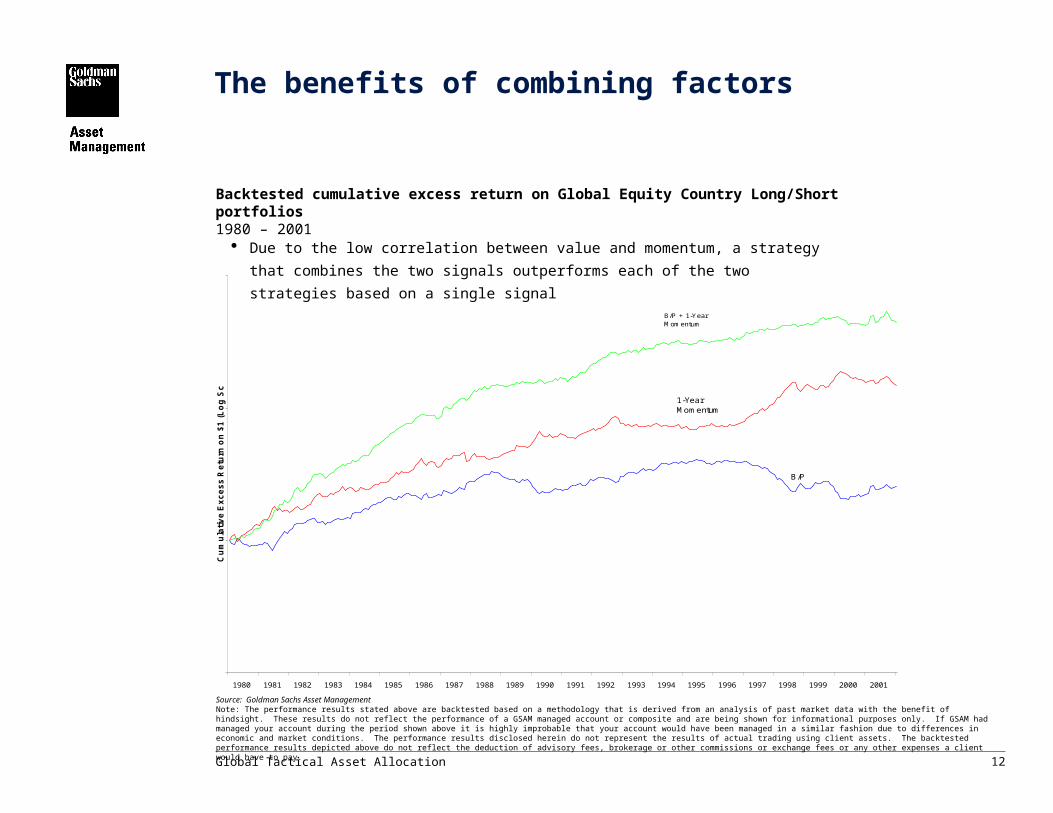

The benefits of combining factors

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Cu

mu

lati

ve

Ex

ce

ss

Re

turn

on

$1

(L

og

Sc

ale

)

B/P

1-Year Momentum

B/P + 1-Year Momentum

Source: Goldman Sachs Asset ManagementNote: The performance results stated above are backtested based on a methodology that is derived from an analysis of past market data with the benefit of hindsight. These results do not reflect the performance of a GSAM managed account or composite and are being shown for informational purposes only. If GSAM had managed your account during the period shown above it is highly improbable that your account would have been managed in a similar fashion due to differences in economic and market conditions. The performance results disclosed herein do not represent the results of actual trading using client assets. The backtested performance results depicted above do not reflect the deduction of advisory fees, brokerage or other commissions or exchange fees or any other expenses a client would have to pay.

Backtested cumulative excess return on Global Equity Country Long/Short portfolios 1980 – 2001

Due to the low correlation between value and momentum, a strategy that combines the

two signals outperforms each of the two strategies based on a single signal

13Global Tactical Asset Allocation

A simple stock/bond valuation timing model

Backtested cumulative excess return on a U.S. Stock/Bond Timing strategy 1926 – 2001

-

1.0

2.0

3.0

4.0

1925

1929

1933

1937

1941

1945

1949

1953

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

Cu

mu

lati

ve E

xces

s R

etu

rn o

n $

1

Source: Goldman Sachs Asset Management, Ibbotson AssociatesNote: The performance results stated above are backtested based on a methodology that is derived from an analysis of past market data with the benefit of hindsight. These results do not reflect the performance of a GSAM managed account or composite and are being shown for informational purposes only. If GSAM had managed your account during the period shown above it is highly improbable that your account would have been managed in a similar fashion due to differences in economic and market conditions. The performance results disclosed herein do not represent the results of actual trading using client assets. The backtested performance results depicted above do not reflect the deduction of advisory fees, brokerage or other commissions or exchange fees or any other expenses a client would have to pay.

Overweight in U.S. stocks versus bonds is proportional to the spread between trailing

S&P 500 earnings yield and intermediate-term bond yield.

Implementation of a GTAA program

15Global Tactical Asset Allocation

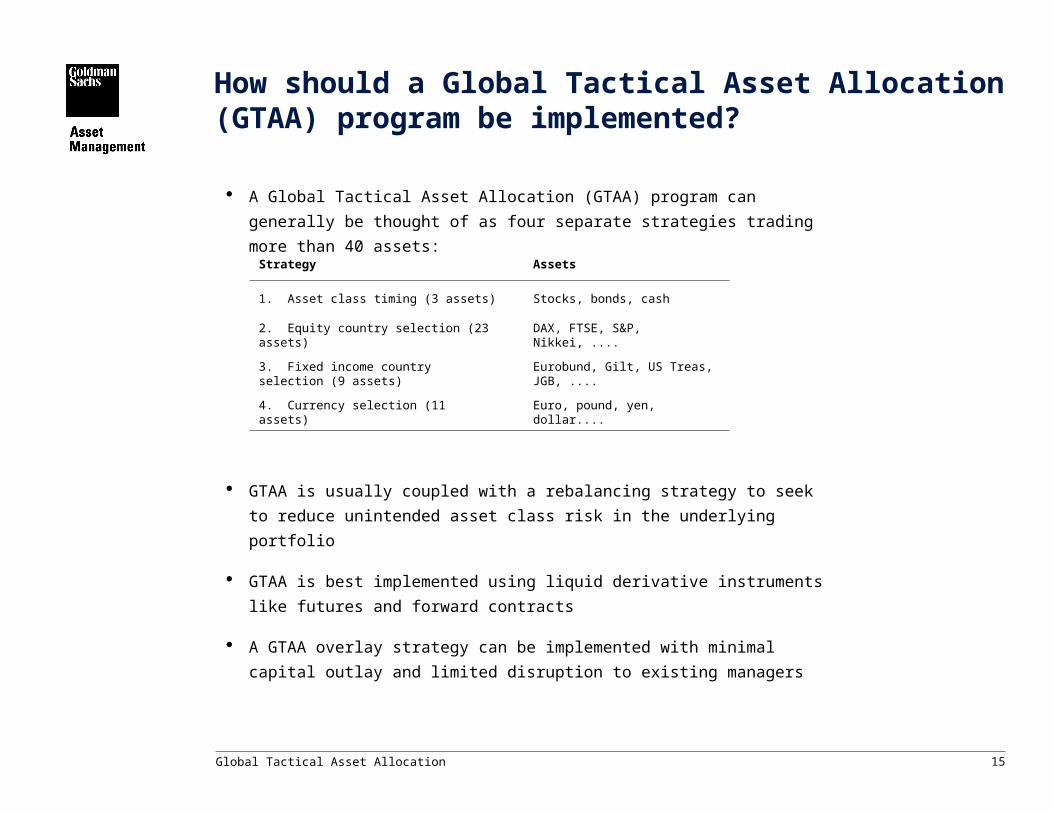

A Global Tactical Asset Allocation (GTAA) program can generally be thought of as

four separate strategies trading more than 40 assets:

GTAA is usually coupled with a rebalancing strategy to seek to reduce unintended

asset class risk in the underlying portfolio

GTAA is best implemented using liquid derivative instruments like futures and

forward contracts

A GTAA overlay strategy can be implemented with minimal capital outlay and

limited disruption to existing managers

How should a Global Tactical Asset Allocation (GTAA) program be implemented?

Strategy Assets

1. Asset class timing (3 assets) Stocks, bonds, cash

2. Equity country selection (23 assets) DAX, FTSE, S&P, Nikkei, ....

3. Fixed income country selection (9 assets)

Eurobund, Gilt, US Treas, JGB, ....

4. Currency selection (11 assets) Euro, pound, yen, dollar....

16

The ‘output’ of Black-Litterman is a vector of mixed expected returns.

Additional Views

(e.g. anomalies)

Black-Litterman Model

Black-Litterman ‘mixed’ E(R)s

Benchmark

Risk Aversion

Transaction Costs

Mean-Variance

OptimizationOptimal Portfolio

Weights

Equilibrium E(R)s

(we use CAPM)

Historical Data

Covariance

Matrix

From Views to an Optimal Portfolio:The Black-Litterman Model

17Global Tactical Asset Allocation

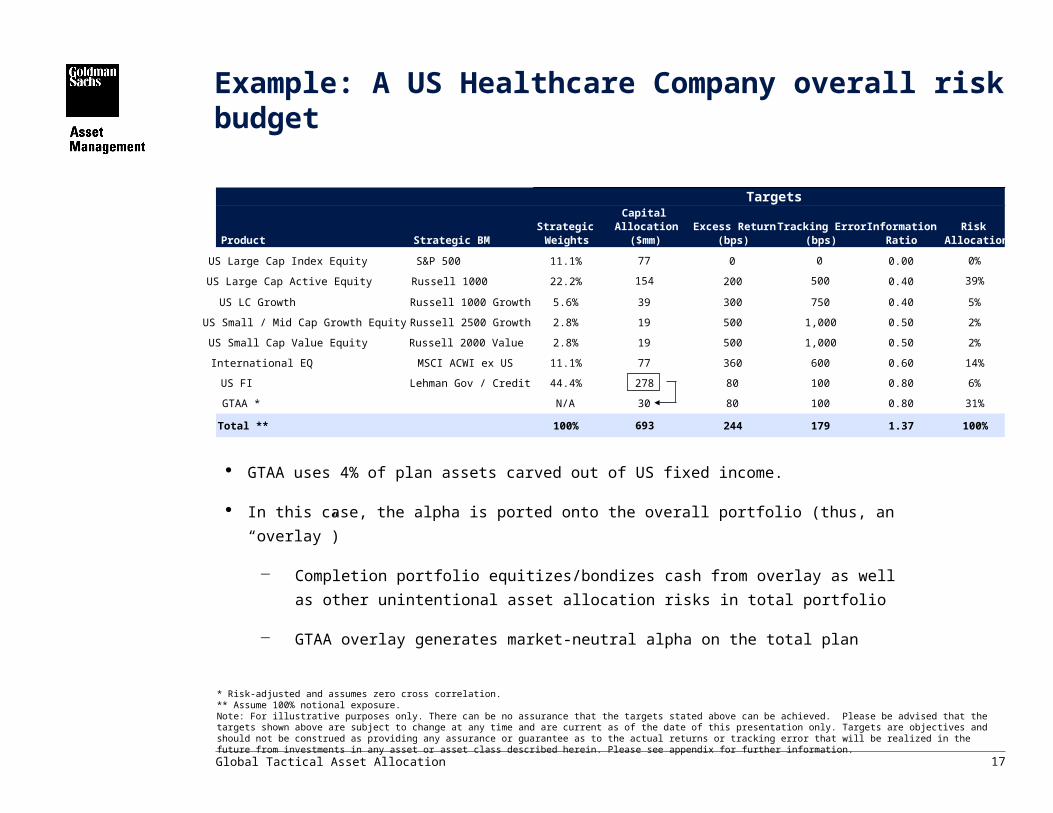

Example: A US Healthcare Company overall risk budget

GTAA uses 4% of plan assets carved out of US fixed income.

In this case, the alpha is ported onto the overall portfolio (thus, an “overlay”)

Completion portfolio equitizes/bondizes cash from overlay as well as other

unintentional asset allocation risks in total portfolio

GTAA overlay generates market-neutral alpha on the total plan

* Risk-adjusted and assumes zero cross correlation. ** Assume 100% notional exposure.Note: For illustrative purposes only. There can be no assurance that the targets stated above can be achieved. Please be advised that the targets shown above are subject to change at any time and are current as of the date of this presentation only. Targets are objectives and should not be construed as providing any assurance or guarantee as to the actual returns or tracking error that will be realized in the future from investments in any asset or asset class described herein. Please see appendix for further information.

Product Strategic BMStrategic Weights

Capital Allocation

($mm)Excess Return

(bps)Tracking Error

(bps)Information

RatioRisk

Allocation

US Large Cap Index Equity S&P 500 11.1% 77 0 0 0.00 0%

US Large Cap Active Equity Russell 1000 22.2% 154 200 500 0.40 39%

US LC Growth Russell 1000 Growth 5.6% 39 300 750 0.40 5%

US Small / Mid Cap Growth Equity Russell 2500 Growth 2.8% 19 500 1,000 0.50 2%

US Small Cap Value Equity Russell 2000 Value 2.8% 19 500 1,000 0.50 2%

International EQ MSCI ACWI ex US 11.1% 77 360 600 0.60 14%

US FI Lehman Gov / Credit 44.4% 278 80 100 0.80 6%

GTAA * N/A 30 80 100 0.80 31%

Total ** 100% 693 244 179 1.37 100%

Targets

18

Our completion trades seek to minimize the expected tracking error to the benchmark portfolio.

Our overlay trades seek to maximize expected return subject to risk and other constraints.

1 North America equity weight includes a 1.8% equity overweight from our asset class timing strategy.2 Dollar Block fixed income weight includes a 13.7% fixed income overweight from our asset class timing strategy.

Overlay maximizes expected return while

taking a measured amount of tactical risk

Note: Portfolio holdings are subject to change without prior notice. The above portfolio holdings may vary for each client in the strategy based on market conditions, client guidelines and diversity of portfolio holdings. Expected returns are statistical estimates of hypothetical average returns of economic asset classes, derived from statistical models. Actual returns are likely to vary from expected returns. Expected return models apply statistical methods and a series of fixed assumptions to derive estimates of hypothetical average asset class performance. Reasonable people may disagree about the appropriate statistical model and fixed assumptions. These models have limitations, as the assumptions may not be consensus views, or the model may not be updated to reflect current economic or market conditions. Accordingly, these models should not be relied upon to make predictions of actual future account performance. Goldman Sachs has no obligation to provide recipients hereof with updates or changes to such data. Please see appendix for further information.

For illustrative purposes only.

Benchmark Weights

UnderlyingWeights

CompletionTrades

Completion Portfolio Total

WeightsOverlay

DeviationsTotal Portfolio

WeightsEquity country selection

Emerging Markets 1.1% 1.2% 0.0% 1.2% 0.0% 1.2%Asia ex Japan 0.7% 0.7% -0.3% 0.4% 1.0% 1.4%Canada 0.5% 0.5% 0.1% 0.6% 0.1% 0.7%Europe 4.2% 4.2% 0.2% 4.4% -1.6% 2.8%Japan 2.2% 2.2% 0.0% 2.2% 1.3% 3.6%United Kingdom 2.4% 2.5% -0.3% 2.1% -0.3% 1.8%US Small Cap 3.6% 5.5% 0.4% 5.8% 0.0% 5.8%US Large Cap1 40.9% 32.9% 5.8% 38.7% 2.4% 41.0%

Total Equity 55.56% 49.67% 5.88% 55.55% 2.85% 58.40%

Fixed income country selection

Dollar Block2 44.4% 42.8% 1.7% 44.4% 18.2% 62.6%Europe 0.0% 0.0% 0.0% 0.0% 14.5% 14.5%Japan 0.0% 0.0% 0.0% 0.0% -13.0% -13.0%United Kingdom 0.0% 0.0% 0.0% 0.0% -12.2% -12.2%

Total Fixed Income 44.44% 42.75% 1.69% 44.44% 7.47% 51.92%

Currency selection

Dollar Block 1.2% 1.2% 0.0% 1.2% 1.6% 2.7%Europe 6.6% 6.7% -0.1% 6.6% -0.5% 6.1%Japan 2.2% 2.2% 0.0% 2.2% 3.4% 5.6%

Total Currency 10.00% 10.12% -0.12% 10.00% 4.46% 14.46%

Total Exposure 100.00% 92.43% 7.57% 100.00% 10.32% 110.32%

Estimated Annualized Expected Return -0.35% 0.00% 2.58%Estimated Annual TE 1.20% 0.29% 1.22%Expected Information Ratio -0.29 0.00 2.12

Regional Summary

[A] [B] [C] = [A] + [B] [D] [E] = [C] + [D]

2

Completion reduces unintended asset

allocation risk

US Healthcare Company GTAA portfolio snapshotAs of July 31, 2002

19Global Tactical Asset Allocation

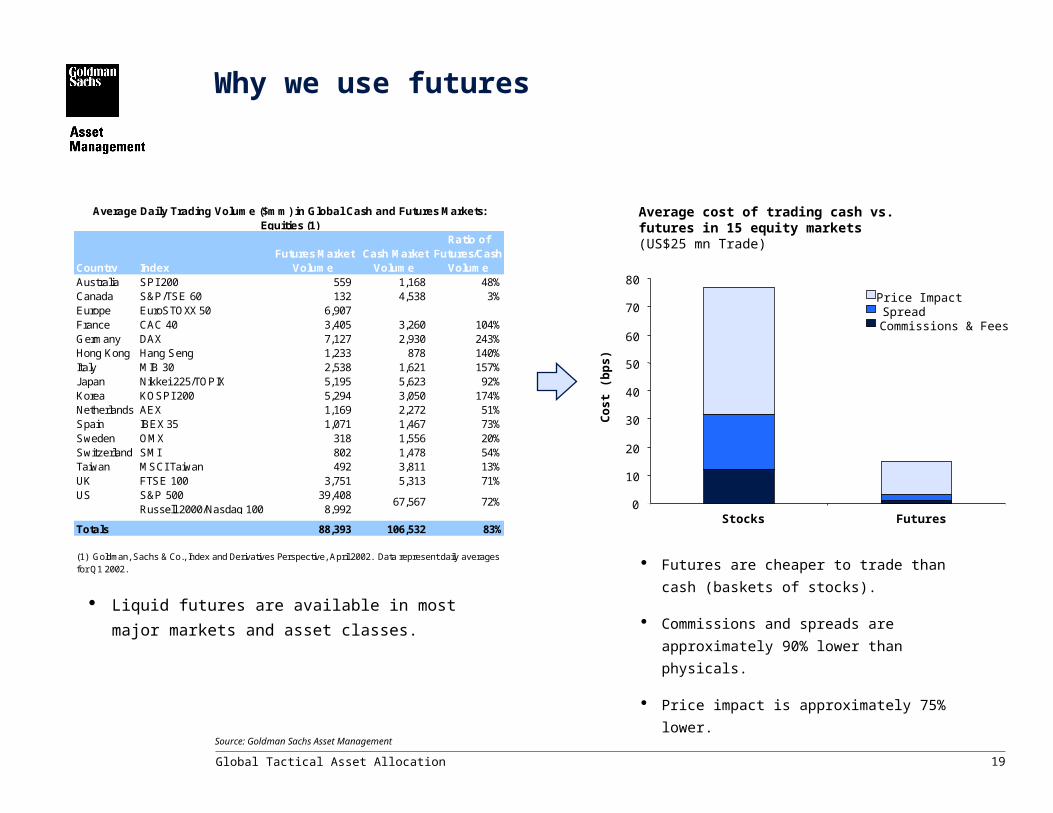

Why we use futures

Futures are cheaper to trade than cash

(baskets of stocks).

Commissions and spreads are

approximately 90% lower than physicals.

Price impact is approximately 75% lower.

Source: Goldman Sachs Asset Management

Average cost of trading cash vs. futures in 15 equity markets (US$25 mn Trade)

0

10

20

30

40

50

60

70

80

Stocks Futures

Co

st

(bp

s)

Price ImpactSpreadCommissions & Fees

Country Index Futures Market

Volume Cash Market

Volume

Ratio of Futures/Cash

VolumeAustralia SPI 200 559 1,168 48%Canada S&P/TSE 60 132 4,538 3%Europe EuroSTOXX 50 6,907 France CAC 40 3,405 3,260 104%Germany DAX 7,127 2,930 243%Hong Kong Hang Seng 1,233 878 140%Italy MIB 30 2,538 1,621 157%Japan Nikkei 225/TOPIX 5,195 5,623 92%Korea KOSPI 200 5,294 3,050 174%Netherlands AEX 1,169 2,272 51%Spain IBEX 35 1,071 1,467 73%Sweden OMX 318 1,556 20%Switzerland SMI 802 1,478 54%Taiwan MSCI Taiwan 492 3,811 13%UK FTSE 100 3,751 5,313 71%US S&P 500 39,408

Russell 2000/Nasdaq 100 8,992

Totals 88,393 106,532 83%

(1) Goldman, Sachs & Co., Index and Derivatives Perspective, April 2002. Data represent daily averages for Q1 2002.

67,567 72%

Average Daily Trading Volume ($mm) in Global Cash and Futures Markets: Equities (1)

Liquid futures are available in most major markets

and asset classes.

Summary

21Global Tactical Asset Allocation

The modern GTAA program is a well diversified strategy unlike traditional TAA

Potential for more consistently positive excess return

The strategy is implemented using low cost derivative instruments

Transaction costs are approximately 80% lower than for traditional strategies

GTAA can reduce unintended asset allocation risk and add potential alpha

Can significantly improve a fund’s overall information ratio

FEATURE BENEFIT

Low correlation with other active risks Average correlation between active manager returns and GTAA manager returns is approximately 0.01

Comparative advantages of a GTAA strategy

Source: Goldman Sachs Asset Management

22Global Tactical Asset Allocation

A Quantitative Approach to Portfolio Management

23Global Tactical Asset Allocation

This material is provided for educational purposes only and should not be construed as investment advice or an offer to sell or the solicitation of offers to buy any security. Opinions expressed herein are current opinions as of the date appearing in this material only.

This presentation does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation.

Prospective investors should inform themselves and take appropriate advice as to any applicable legal requirements and any applicable taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant to the subscription, purchase, holding, exchange, redemption or disposal of any investments.

Past performance is not a guide to future performance and the value of investments and the income derived from those investments can go down as well as up. Future returns are not guaranteed and a loss of principal may occur.

Opinions expressed are current opinions as of the date appearing in this material only. No part of this material may be i) copied, photocopied or duplicated in any form, by any means, or ii) redistributed without Goldman Sachs Asset Management's prior written consent.

Simulated performance results have certain inherent limitations. Such results are hypothetical and do not represent actual trading, and thus may not reflect material economic and market factors, such as liquidity constraints, that may have had an impact on the Adviser’s actual decision-making. Simulated results are also achieved through the retroactive application of a model designed with the benefit of hindsight. The results shown reflect the reinvestment of dividends and other earnings, but do not reflect advisory fees, transaction costs and other expenses a client would have paid, which would reduce return. No representation is made that a client will achieve results similar to those shown.

Effect of fees on performance:The following table provides a simplified example of the effect of management fees on portfolio returns. For example, assume a portfolio has a steady investment return, gross of fees, of 0.5% per month and total management fees of 0.05% per month of the market value of the portfolio on the last day of the month. Management fees are deducted from the market value of the portfolio on that day. There are no cash flows during the period. The table shows that, assuming that other factors such as investment return and fees remain constant, the difference increases due to the compounding effect over time. Of course, the magnitude of the difference between gross-of-fee and net-of-fee returns will depend on a variety of factors, and the example is purposely simplified. Period Gross Return (%) Net Return (%) Differential (%)1 year 6.17 5.54 0.632 years 12.72 11.38 1.3410 years 81.94 71.39 10.55

In the event any of the assumptions used in this presentation do not prove to be true, results are likely to vary substantially from the examples shown herein. These examples are for illustrative purposes only and do not purport to show actual results.

The strategy discussed herein may include the use of derivatives. Derivatives often involve a high degree of financial risk in that a relatively small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable as well as favorable, in the price of the derivative instrument.

References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time (each, an “index”) are provided for your information only. Reference to the indices shown herein does not imply that the portfolio will achieve returns, volatility or other results similar to such indices. The composition of the index may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change over time.

Tracking Error is one possible measurement of the dispersion of a portfolio’s returns from its stated benchmark. More specifically, it is the standard deviation of such excess returns. Tracking error figures are representations of statistical expectations falling within “normal” distributions of return patterns. Normal statistical distributions of returns suggests that approximately two thirds of the time the annual gross returns of the accounts will lie in a range equal to the benchmark return plus or minus the tracking error if the market behaves in a manner suggested by historical returns. Targeted tracking error therefore applies statistical probabilities (and the language of uncertainty) and so cannot be predictive of actual results. The tracking error that will actually be achieved may inherently lie outside of the range suggested by a "normal " statistical distribution of returns. The actual tracking error is the result of many factors (including but not limited to market volatility, company specific anomalies, instability of correlation between benchmark holdings, timing differences between the calculation of the portfolio value and the valuation of the benchmark by the index provider. In addition, past tracking error is not indicative of future tracking error and there can be no assurance that the tracking error actually reflected in your accounts will be at levels either specified in the investment objectives or suggested by our forecasts.

© Copyright 2003 Goldman, Sachs & Co. All rights reserved. Member SIPC/NASD.

General notes