Global Timber Production, Trade, and Timberland Investments Speech Presented at the Southern Forest Resource Assessment Consortium 21-22 October 2008 Research Triangle Park, NC Fred Cubbage Professor North Carolina State University Department of Forestry and Environmental Resources

Transcript

Global Timber Production, Trade, and Timberland Investments

Speech Presented at the Southern Forest Resource Assessment Consortium

21-22 October 2008Research Triangle Park, NC

Fred CubbageProfessor

North Carolina State UniversityDepartment of Forestry and Environmental Resources

Current Research Components and Co-PIsGlobal and U.S. Trade

Ronalds Gonzalez, Sudipta Dasmohapatra, Daniel Saloni, Fred CubbageSadharga Koesbanda & Fred Cubbage

World Timber InvestmentsFred Cubbage, Patricio MacDonagh, Gustavo Balmelli, Rafael Rubilar, Rafael de la Torre, Ronalds Gonzalez, Omar Carrero, Greg Frey, Sadharga Koesbanda, Heyns Kotze, Jin Huang, Mauro Murara, Vitor Hoeflich, James Turner, Bob Abt

Colombia – Land, Site Quality, Transportation TradeoffsJuan Lopez, Rafael de la Torre, Fred Cubbage

Gross Domestic Product (GDP) and Growth, 2006Country GDP 2006

(Billion $US)GDP 2006 per

capita (000 $US) Forecast GDP

Growth, 2007 (%)

Argentina 213 5.5 7.5

Brazil 1 067 5.7 4.4

Chile 145 8.9 5.2

Colombia 135 2.9 5.5

Paraguay 10 1.6 5.0

Peru 93 3.4 6.0

Uruguay 19 6.0 6.0

Venezuela 182 6.8 6.2

S America Total 1 917 5.1 5.3

USA 7 814 37 ~2.4 (actual)

Africa (2004) Na 0.1-4.0 Na

Global 48 144 7.3 4.9

PriceWaterhouseCoopers 2007, IMF World Economics Outlook Database, FAO GFRA 2007

Forests and Plantations

Total World Forest Area By Region, 2005

1001832

677 635 572

20628

0

200

400

600

800

1000

1200

Europ

eS.

America

N. Ameri

ca

Africa

Asia

Ocean

iaC. A

merica

Mill

ion

Ha

FAO 2005; 3.952 billion ha total

Total Forest AreaFor Major Countries, 2005

809

478

310 303197 164 133 88 69 68

0100200300400500600700800900

Russian

Fed

Brazil

Canad

aU.S.A

.China

Australi

aD.R

. Congo

Indones

iaPeru India

Mill

ion

Ha

FAO 2007

Area of Planted Forests by Function, 2005

10798

44422

3833

2161517133

11326

2370

20474

326028

986 315192040

10000

20000

30000

40000

50000

Africa Asia Oceania Europe NorthAmerica

CentralAmerica

SouthAmerica

Mill

ion

Ha

Productive Forest Protective Forest

FAO 2005; 109.6 million ha productive (78%); 30.1 million ha protective (22%); 140.1 million ha total

Total Productive Plantation Area For Major Countries in the World, 2005

17061

11888

53843399 2661 1997 1968 1832 1792 1766 1573

28530

0

8000

16000

24000

32000

ChinaU.S.A

.Russ

ian FedBraz

ilIndon

esia

ChileThail

andFran

ceNew

Zealand

Viet N

amAustra

liaMalay

sia

Thou

sand

Ha

FAO 2007

Total Productive Plantation Area For Major Countries in the World, 2005

14261229

1067 1053

751 754627

312164

43

1471

0

500

1000

1500

2000

SpainS A

frica

Argen

tina

Portugal

IndiaUru

guayPeru

Venez

uelaColombia

Ecuad

orPara

guay

Thou

sand

Ha

FAO 2007, Asoplant 2007 for Venezuela

Industrial Roundwood Harvest from Plantations

172152

30

147

100

322

0

50

100

150

200

Europ

eS.

America

Africa

AsiaN. A

merica

Ocean

iaC. A

merica

Mill

ion

M 3

FAO 2006; country reports; Brown (1999); DANA; SOUTHEM, Siry et al. 2005

SummaryWorld forest plantations

Increasing in acreage and production (FAO 2007, Bael and Sedjo 2006)As were southern pine plantation in US South (Wear et al. 2007)Offsetting decline in natural forest extraction?Largest increase in southern hemisphere, China

U.S.Most plantations in AmericasBut with lower productivity rates than southern hemisphere

Industrial Roundwood Production

Ronalds Gonzalez, Sudipta Dasmohapatra, Daniel Saloni, Fred Cubbage

$0$20$40$60$80

$100$120$140$160$180

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Billion US$ Linear (Billion US$)

Global Trade in Forest Products expandedsince 1980, at about 4.5% per year . . .

AAGR = 4.5%

Schuler and Ince 2005

Also, with expanded pine plantation output, the Southern hemisphere & Latin America emerged as a growing softwood lumber supply source . . .

Oceania 8,961 8,963 2 1 (1)1. Papua New Guinea 5,533 5,533 0 0 02. Australia 3,092 3,092 0 0 0

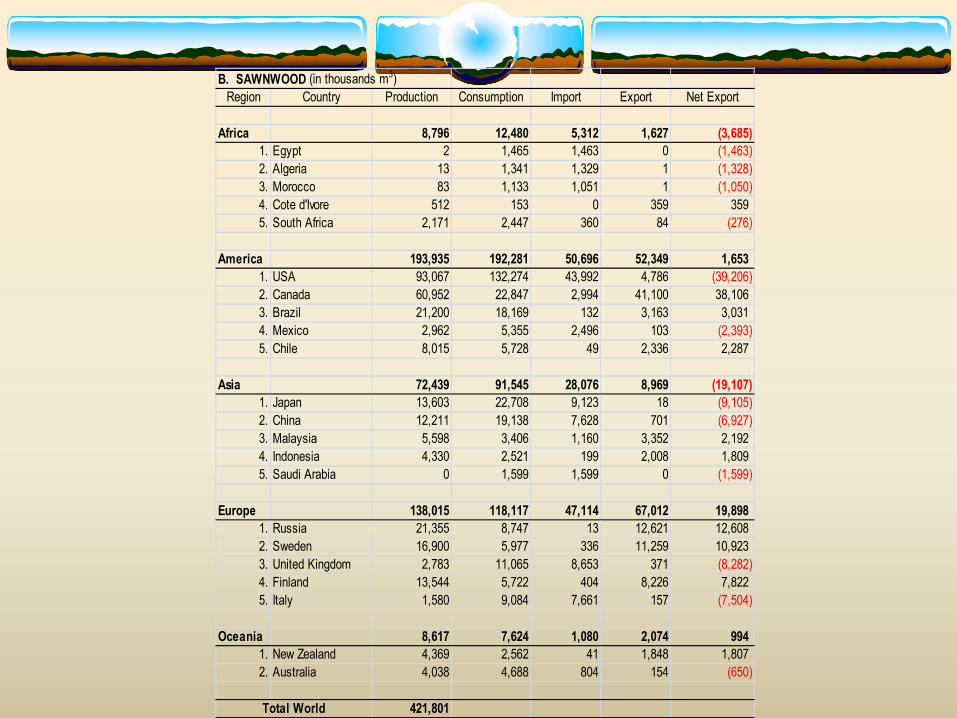

1,766,925Total World

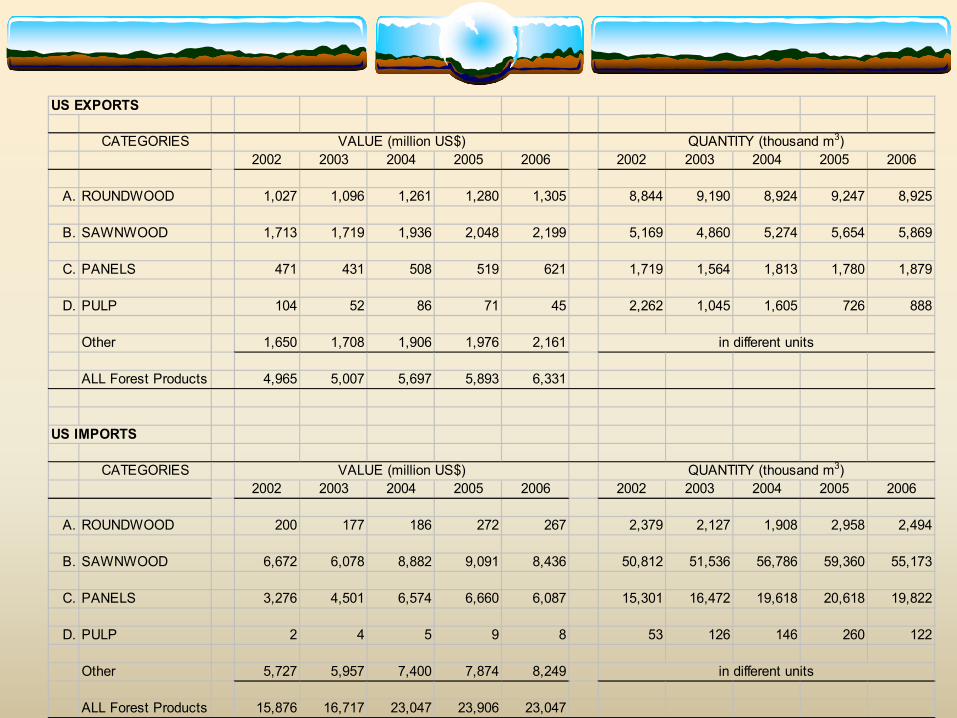

Summary: U.S. Forest ProductsRanking in the World

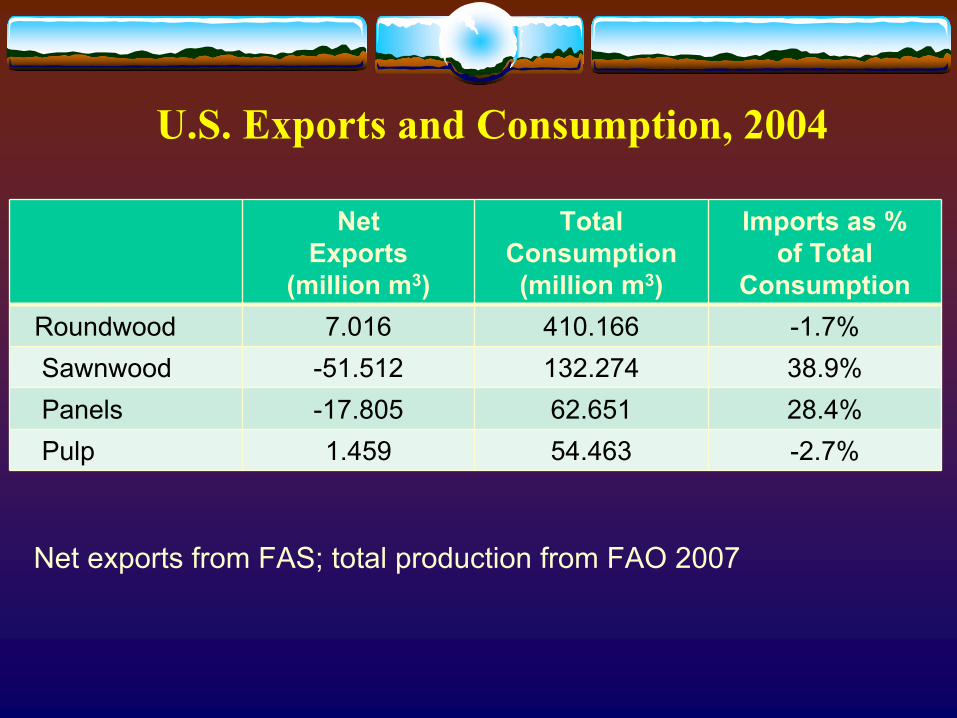

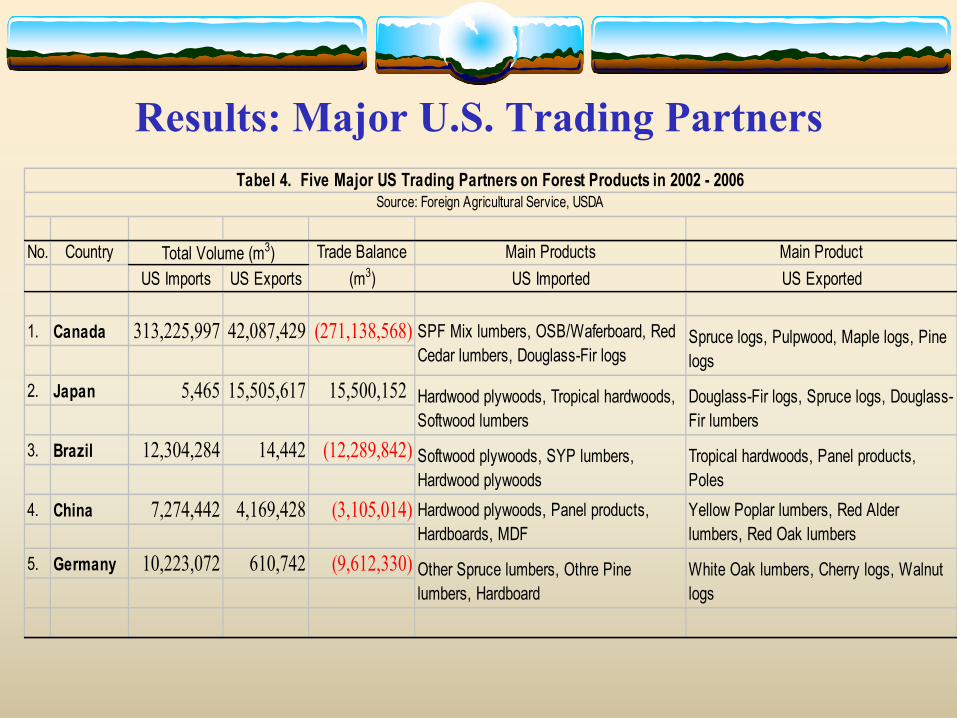

World-wide, U.S. ranked high for all forest productsFor forest production, consumption, and tradeU.S. largest consumer for all except fuelwood Ranked 1st in production except for panels and fuelwoodU.S. imported the most sawnwood of any countryU.S. was second largest roundwood exporter, after only Russia

Yellow Poplar lumbers, Red Alder lumbers, Red Oak lumbers

Other Spruce lumbers, Othre Pine lumbers, Hardboard

White Oak lumbers, Cherry logs, Walnut logs

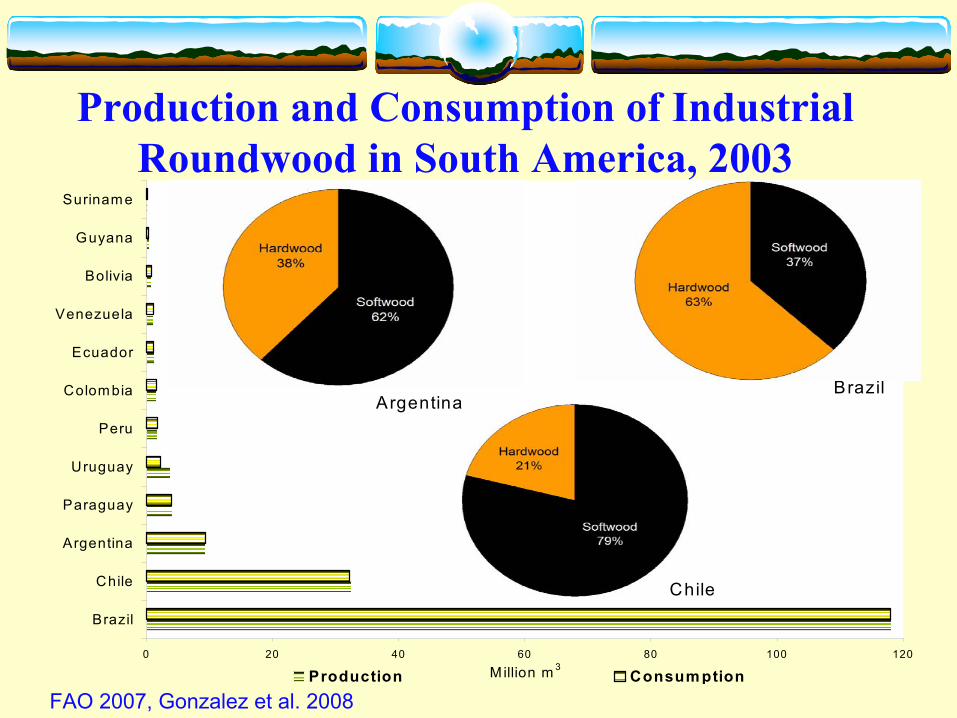

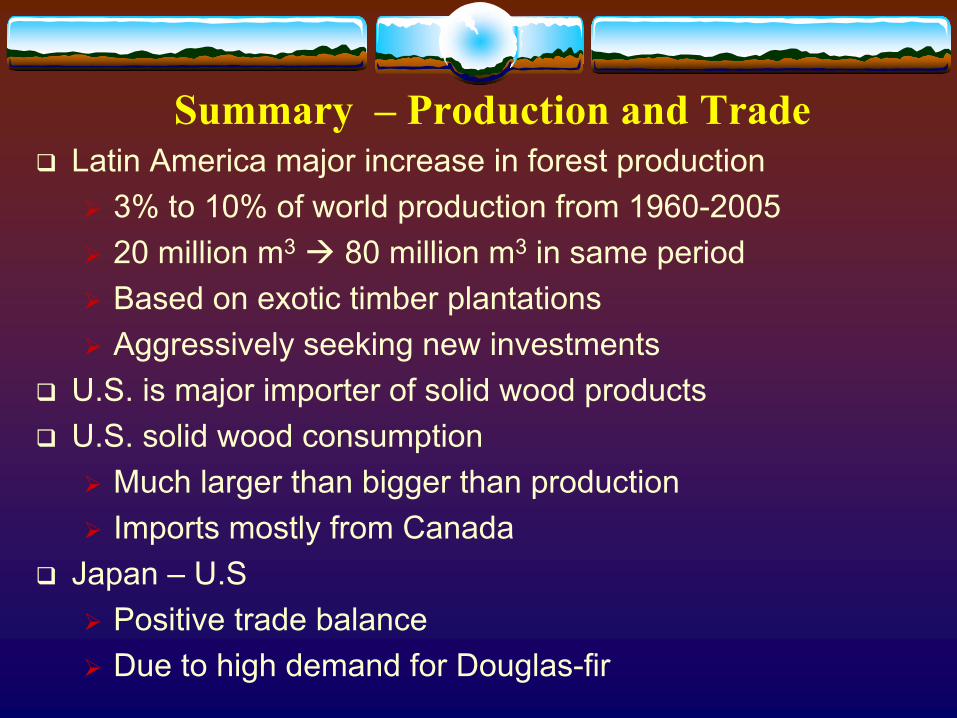

Summary – Production and TradeLatin America major increase in forest production

3% to 10% of world production from 1960-200520 million m3 80 million m3 in same periodBased on exotic timber plantationsAggressively seeking new investments

U.S. is major importer of solid wood productsU.S. solid wood consumption

Much larger than bigger than productionImports mostly from Canada

Japan – U.SPositive trade balanceDue to high demand for Douglas-fir

Global Timber Investment Returns

Co-Authors, Affiliations, Countries, 2008

Fred Cubbage North Carolina State University, USAPatricio Mac Donagh Universidad Nacional de Misiones, ArgentinaGustavo Balmelli Instituto Nacional de Investigación Agropecuaria, UruguayRafael Rubilar Universidad Concepcion de ChileRafael De La Torre Cellfor, USA, ColombiaRonalds Gonzalez NC State University, VenezuelaRonalds Gonzalez NC State University, VenezuelaHeyns Kote South AfricaGreg Frey NC State University, ParaguayJin Juang NC State University, ChinaVitor Hoeflich Universidade Federal do Paraná, BrasilMauro Murara Universidade de Contestado, BrasilJames Turner Scion Research, New ZealandBob Abt NC State University, New Zealand

MethodsSelect countries

Major world plantation timber producersArgentina, Brazil, Uruguay, Chile, US South

Select principal commercial timber species or prospectsAuthors’ estimates of:

Growth rates, typical current practices, geneticsFactor costs and output prices

Develop cash flow analyses / spreadsheetsCapital budgeting analysesIterative review by authors and foresters in each countrySensitivity analyses – land, reserves, subsidies

Assumptions

Discounted cash flow analysisReal (constant) input costs and timber prices

No inflationReal discount rate of 8%

No land costs in base caseBefore taxRepresentative sitesGood plantation and natural stand practices

Returns of Plantations, Brazil and Chile, 2008

5.73.6 2.9 2.8

0.8

25.5

20.8

16.3 15.613.1

0

5

10

15

20

25

30

Brasil Eucgrandis

Brasil P taeda Brasil Pelliotii

Chile Pradiata

sawtimber

Chile Pradiata

pulpwood

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land cost

Land Expectation Value Internal Rate of Return

Returns of Plantations, Argentina & Uruguay, 2008

3.2 3.2 2.4 1.8 1

2018.2

22.921.4

12.8

0

5

10

15

20

25

Argentina Ptaeda

ArgentinaEuc grandis

Uruguay Eucglobulus

Uruguay Eucgrandis

Uruguay Ptaeda

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land cost

Land Expectation Value Internal Rate of Return

Returns of Plantations, Colombia, 2008

5.4 5.44.1

16.6 15.5 14.7

11.2

1.6

0

5

10

15

20

25

ColombiaEucalyptus

Colombia Ptecunumanii

Colombia Pmaximinoi

Colombia Ppatula

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

.7.

8% discount rate; no land cost

Land Expectation Value Internal Rate of Return

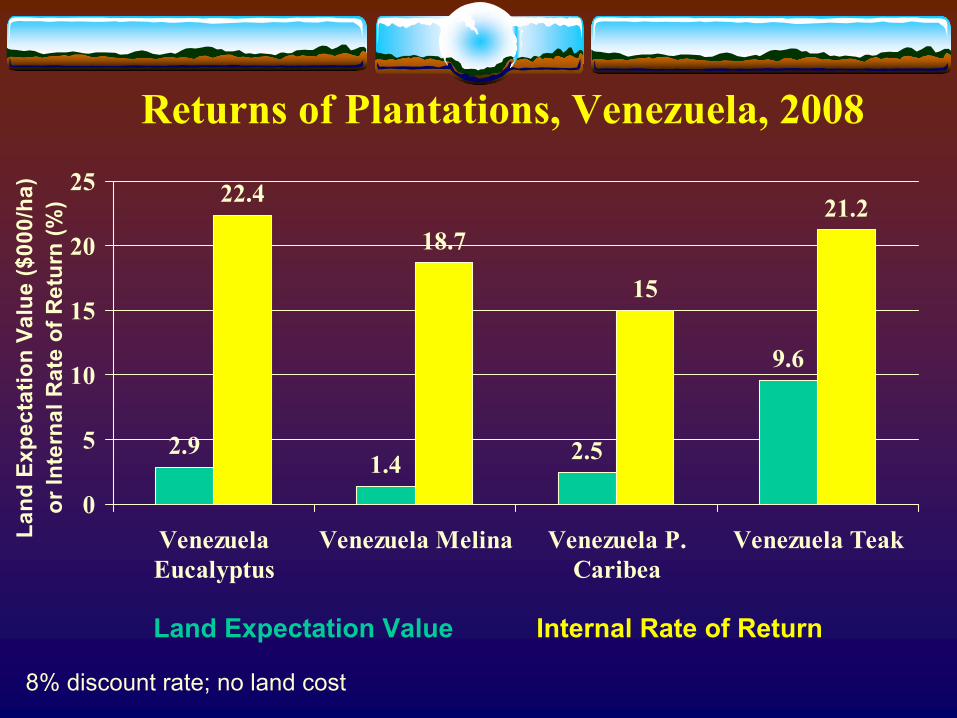

Returns of Plantations, Venezuela, 2008

2.91.4 2.5

9.6

22.4

18.7

15

21.2

0

5

10

15

20

25

VenezuelaEucalyptus

Venezuela Melina Venezuela P.Caribea

Venezuela TeakLand

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land cost

Land Expectation Value Internal Rate of Return

Returns of Plantations, Paraguay, 2008

1.64.2

2

12

21.4

15.4

0

5

10

15

20

25

Paraguay P taeda Paraguay Euc grandis Paraguay Euccamuldensis

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land

Land Expectation Value Internal Rate of Return

Returns of Plantations, South Africa, China, New Zealand, & USA, 2008

2.3 1.70.1

-0.2

0.2

12.411.1 12.1

7.6 8.5

-5

0

5

10

15

20

25

S Afrcia Eucgrandis

S Africa Ppatula

China Pmassoniana

New ZealandP radiata

USA P taeda

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land

Land Expectation Value Internal Rate of Return

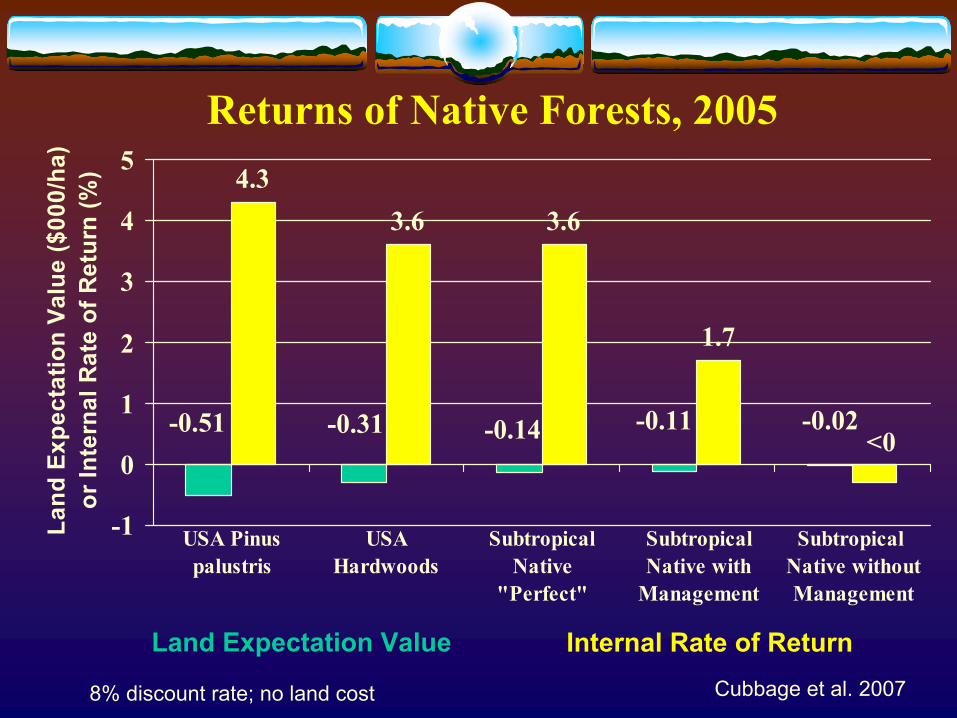

Returns of Native Species / Plantations, 2005

1.6

-0.15

12.410.9

7.8 7.4

-0.03

1 0.8

13.6

-5

0

5

10

15

Chile Nothofagus

dombeyiPlanted

BrasilAracauria

Planted

ChileNothofagus

nervosaplanted

USA Pinustaeda Natural

ArgentinaAracauria

Planted

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land cost

Land Expectation Value Internal Rate of Return Cubbage et al. 2007

Returns of Native Forests, 2005 4.3

3.6 3.6

1.7

-0.51 -0.11-0.14-0.31 -0.02<0

-1

0

1

2

3

4

5

USA Pinuspalustris

USAHardwoods

SubtropicalNative

"Perfect"

SubtropicalNative with

Management

Subtropical Native withoutManagement

Land

Exp

ecta

tion

Valu

e ($

000/

ha)

or In

tern

al R

ate

of R

etur

n (%

)

8% discount rate; no land cost

Land Expectation Value Internal Rate of ReturnCubbage et al. 2007

OECD 2007; Range of 1-7; Lowest number is least risky

Trade and Development: Debate and AcrimonyEvangelina Corrazzo, Carnival Queen of Gualeguaychú, Entre Rios, Argentina

at the EU-Latinoamerica Summitt, Vienna, Austria, 13 May 2006

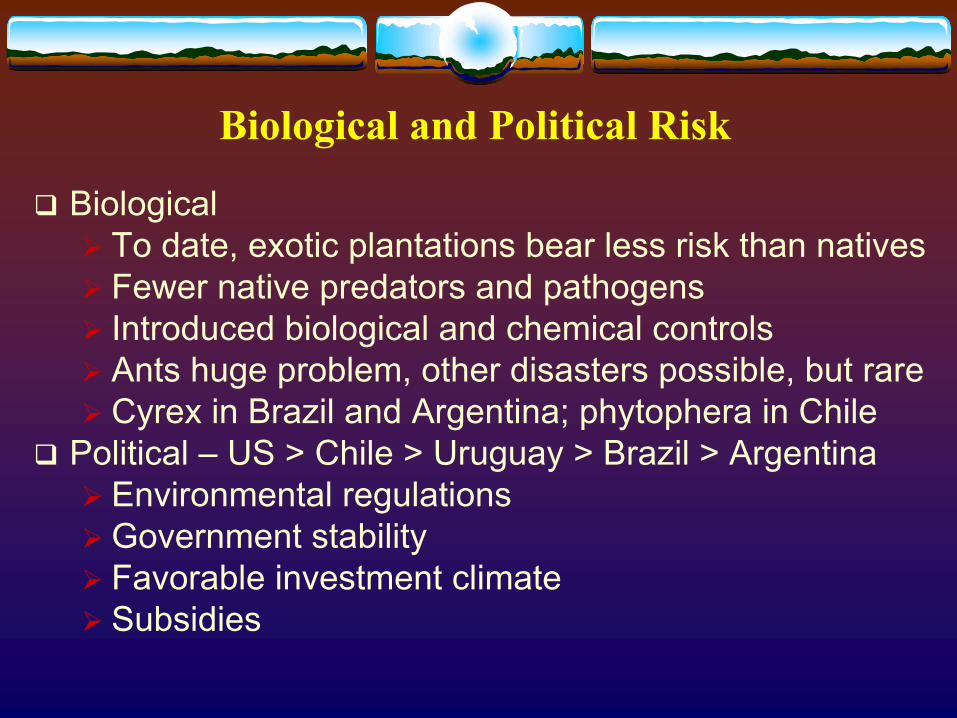

Biological and Political Risk

BiologicalTo date, exotic plantations bear less risk than nativesFewer native predators and pathogensIntroduced biological and chemical controlsAnts huge problem, other disasters possible, but rareCyrex in Brazil and Argentina; phytophera in Chile

Political – US > Chile > Uruguay > Brazil > ArgentinaEnvironmental regulationsGovernment stabilityFavorable investment climateSubsidies

Number of Days and Procedures Required to Start a Business in South America, 2006

Gonzalez et al. 2008, NCSU, from World Bank 2007

915

12 1115 14

17

1013

17

2732

43 4550

6974

102

116

152

0

20

40

60

80

100

120

140

160

Chile Argentina Colombia Uruguay Bolivia Ecuador Paraguay Peru Venezuela Brazil

Day

s

# Procedures # Days required for starting a business

Effect of Land Prices, Transportation Costs, and Site Productivity

on Timber Investment Returnsfor Pine Plantations in Colombia

Juan Lopez, Rafael de la Torre, and Fred CubbageNCSU, CellFor, & NCSU

Analysis of Factors Affecting Forest Investment Opportunities

Carter (2007), IQPC Timber Summit2007: Up to $4 billion seeking timber investmentsOn ~$40 billion base

Forest investments in Latin America increasingLatin America timber prices increasing > U.S.Large LAC plantation and production increasesTradeoffs between land quality, proximity, price crucial in purchase decisions

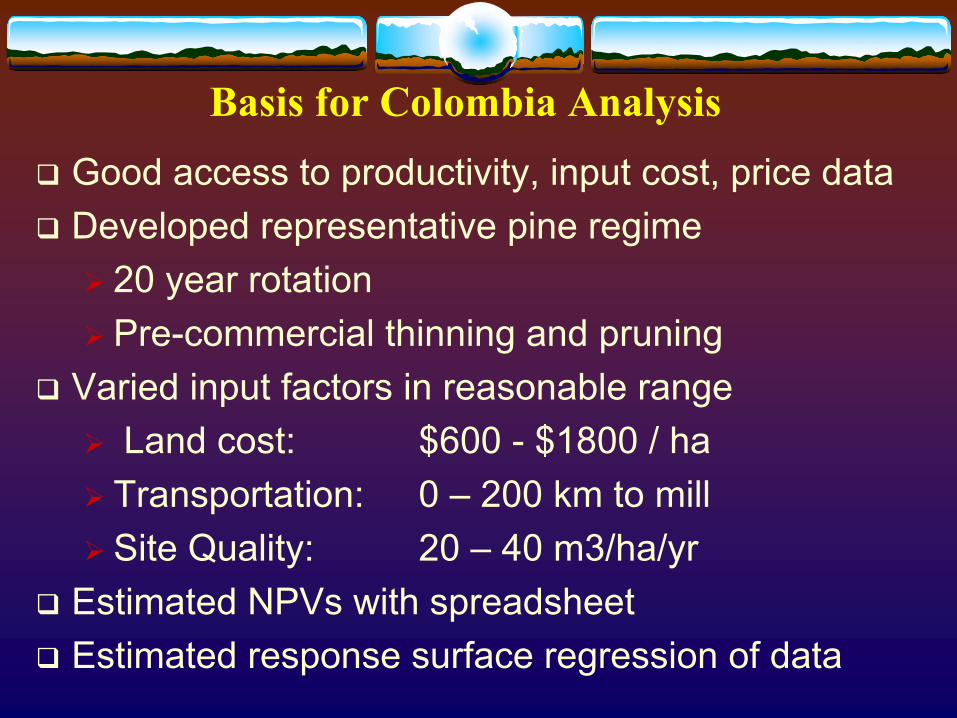

Basis for Colombia AnalysisGood access to productivity, input cost, price dataDeveloped representative pine regime

20 year rotationPre-commercial thinning and pruning

Varied input factors in reasonable rangeLand cost: $600 - $1800 / ha

Transportation: 0 – 200 km to millSite Quality: 20 – 40 m3/ha/yr

Estimated NPVs with spreadsheetEstimated response surface regression of data

P. tecunumanii, 10 years old, Colombia

Estudio de P. maximinoi-8 anos- San Jose

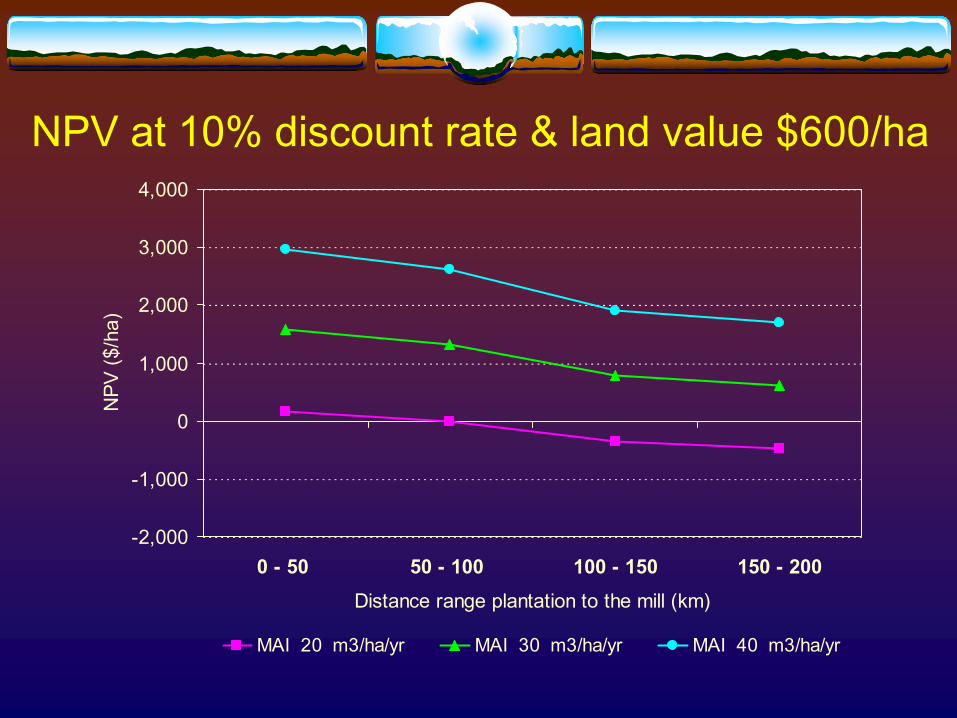

NPV at 10% discount rate & land value $600/ha

-2,000

-1,000

0

1,000

2,000

3,000

4,000

0 - 50 50 - 100 100 - 150 150 - 200Distance range plantation to the mill (km)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

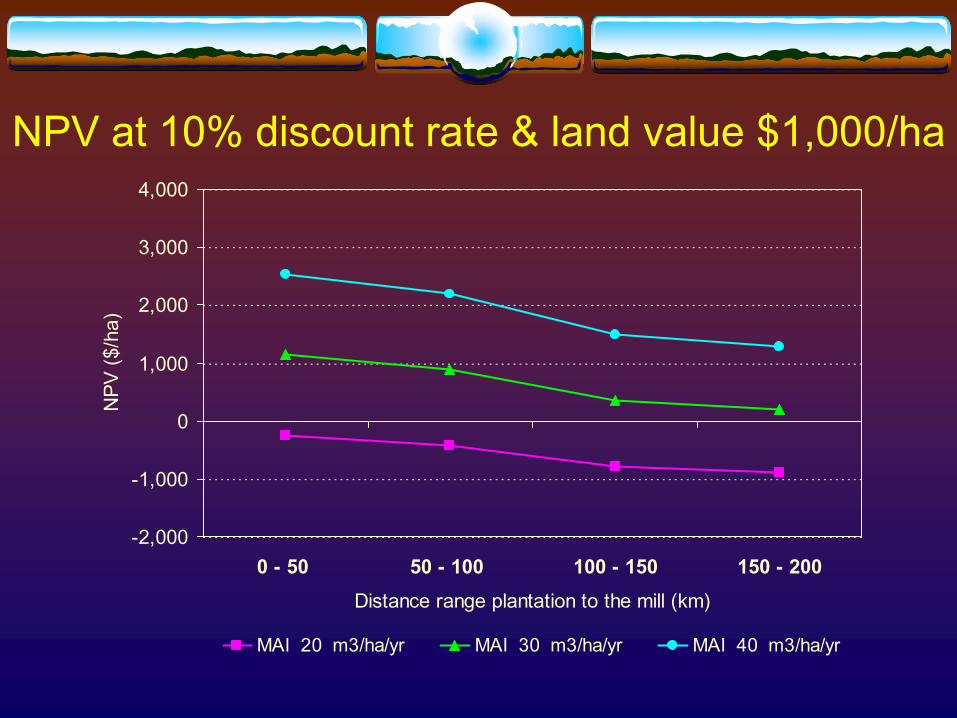

NPV at 10% discount rate & land value $1,000/ha

-2,000

-1,000

0

1,000

2,000

3,000

4,000

0 - 50 50 - 100 100 - 150 150 - 200Distance range plantation to the mill (km)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

NPV at 10% discount rate & land value $1,400/ha

-2,000

-1,000

0

1,000

2,000

3,000

4,000

0 - 50 50 - 100 100 - 150 150 - 200Distance range plantation to the mill (km)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

NPV at 10% discount rate & land value $1,800/ha

-2,000

-1,000

0

1,000

2,000

3,000

4,000

0 - 50 50 - 100 100 - 150 150 - 200Distance range plantation to the mill (km)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

NPV at 10% discount rate distance to the mill 0 to 50 kms

-2,000

-1,000

0

1,000

2,000

3,000

4,000

600 1000 1400 1800Land price ($/ha)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

NPV at 10% discount rate distance to the mill 50 to 100 kms

-2,000

-1,000

0

1,000

2,000

3,000

4,000

600 1000 1400 1800Land price ($/ha)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

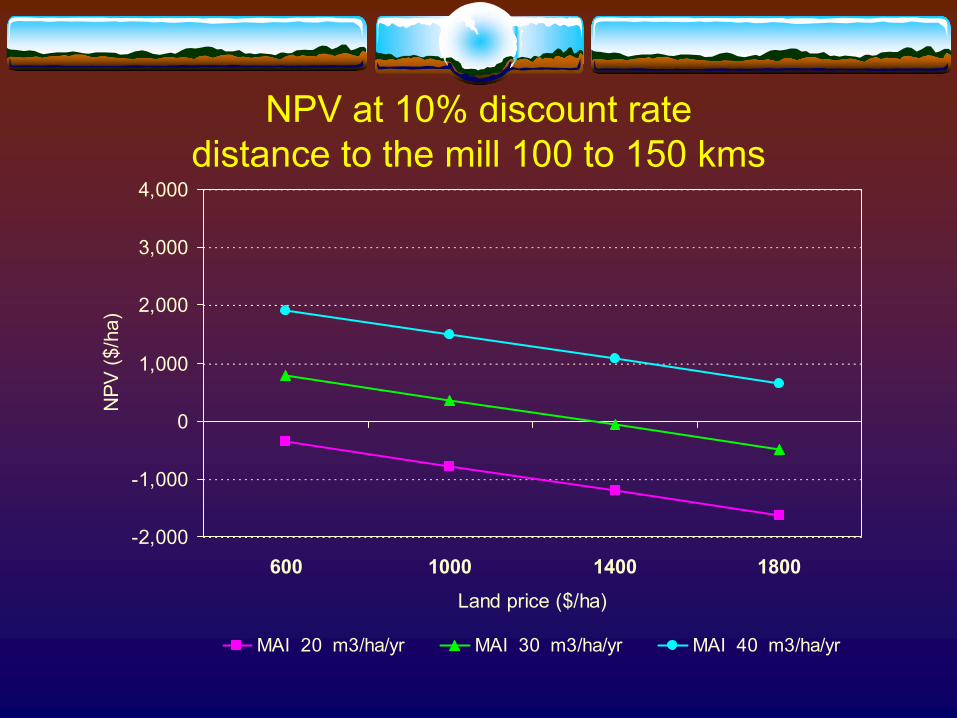

NPV at 10% discount rate distance to the mill 100 to 150 kms

-2,000

-1,000

0

1,000

2,000

3,000

4,000

600 1000 1400 1800Land price ($/ha)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

NPV at 10% discount rate distance to the mill 150 to 200 kms

-2,000

-1,000

0

1,000

2,000

3,000

4,000

600 1000 1400 1800Land price ($/ha)

NPV

($/h

a)

MAI 20 m3/ha/yr MAI 30 m3/ha/yr MAI 40 m3/ha/yr

Proportional Effects at Median Value

Discount Rate

NPV of Factor at Median Value ($/ha)

Land Price(@ $1200/ha)

Transportation Distance

(@100 km)

Mean Annual Increment

(@ 30 m3/ha/yr)8% -1183 -905 5002

10% -1262 -677 3693

12% -1316 -512 2756

Colombia Case ConclusionsInvestment case study for Latin AmericaResults at i=10%

Lower productivity – negative NPVs in all casesHigher productivity – always positive NPVMedium productivity – positive in most cases

Partial response at the meanMAI/Site quality ~ 2-4 times more important than land priceMAI/Site quality ~ 5 time more important than transport cost

Related SOFAC Projects

DemandNCASI

Demand – Jacek Siry – Data Disk

Census: ASM by State; Pulp& paper FinancialsLumberPanelsPaper & PaperboardPulpwoodTimber Product PricesDocumentation

NCASI – Fred Cubbage and Bob Abt

Identify Wood Production Systems and RegionsEstimate Wood Production and Harvesting CostsLegal and Environmental ContextInternational ComparisonsCooperators – Related Projects

Tom Fox, VPIBecky Barlow, Daowei Zhang, AuburnAndy Ezell, Mississippi State

Conclusions

Summary - PlantationsWorld forest plantations

increasing in acreage and productionAs were southern pine plantation on US SouthOffsetting decline in natural forest extraction?Largest increase in southern hemisphere, China

U.S.Most plantations in AmericasBut with lower productivity rates than southern hemisphere

Summary – Production and TradeLatin America major increase in forest production

3% to 10% of world production from 1960-200520 million m3 80 million m3 in same periodBased on exotic timber plantationsAggressively seeking new investments

U.S. is major importer of solid wood productsU.S. solid wood consumption

Much larger than bigger than productionImports mostly from Canada

Japan – U.SPositive trade balanceDue to high demand for Douglas-fir

ConclusionsExotic Plantations Returns

8% to 23% base IRRs w/o land costs Possibility for much greater returns in S AmericaAnd good returns in other Southern HemisphereEarly investors with cheap land costs have profited most; more difficult nowBut U.S. returns have dropped, S Hemisphere increased since 2005Colombia case

Site quality / silviculture has largest potential effect on timber investment returns2-5 times transport, land costs at mean values

ConclusionsInvestment Analysis - Approach and CaveatsRobust cooperative research estimate

Best available data – common practiceKnowledgeable local experts, extensive review

AssumptionsReal rates of return, 2008 pricesWithout land costs, taxesInput & timber prices vary by area, change with time

TechnologyBetter sites / growth possible better returnsBetter management possible better returnsAnd vice versa

Conclusions Forestry Sector Prospects

Economic development opportunityForest sector GDP

2-4% Brazil, Chile1.2% USA1% Argentina, Uruguay

2 new pulp mills each in Chile and in UruguayMany new mills or pulp lines in Brazil More opportunities on other Southern Hemisphere countriesMany sawmills and panel millsRapidly developing forest clusters

Conclusions Forestry Sector Prospects

Modest expansion everywhere Most timber need and greatest prices – Chile & Brazil Larger supply, increasing prices – Argentina New supply, establishing markets – Uruguay Stasis, declining prices – U.S. South Emerging opportunities – Colombia, others

Least risk in most developed markets/countriesLonger term less certainBiological risks may emergeBut with short rotationsAnd strong GDP and export growth

World Timber Productionand Timberland Investments

Speech Presented at the Southern Forest Resource Assessment Consortium

21-22 October 2008Research Triangle Park, NC

Cubbage_Timber_Production_Investments_V7; 20 October 2008

Fred CubbageProfessor

North Carolina State UniversityDepartment of Forestry and Environmental Resources