18

GLOBAL TRANSFER PRICING SERVICES Global Transfer Pricing Review TAX

GLOBAL TRANSFER PRICING SERVICES

Global Transfer Pricing Review

TAX

Global Transfer Pricing Review 2

KPMG’s Global Transfer Pricing Review is designed to help multinational companies stay current with transfer pricing legislation worldwide. Compiled from information supplied by various KPMG International member firm professionals who provide transfer pricing services, thereview provides a snapshot of transfer pricing compliance requirements in 47 countries, including most Organisation for Economic Co-operation and Development (OECD) member countries and many in the Asia Pacific and Latin America regions. You can obtain regular updates to this printedversion at www.us.kpmg.com/services/GTPSReview.

KPMG’s Global Transfer Pricing Services (GTPS) network comprises morethan 600 professionals from KPMG International member firms who worktogether to provide local knowledge, experience, and global analysis to helpmultinational companies address their transfer pricing responsibilities. Ourpractice includes economists, tax practitioners, and financial analysts. We use our knowledge of local rules and how they interact to help member firm clients find tax-efficient pricing routes through an increasingly complexinternational web of transfer pricing rules.

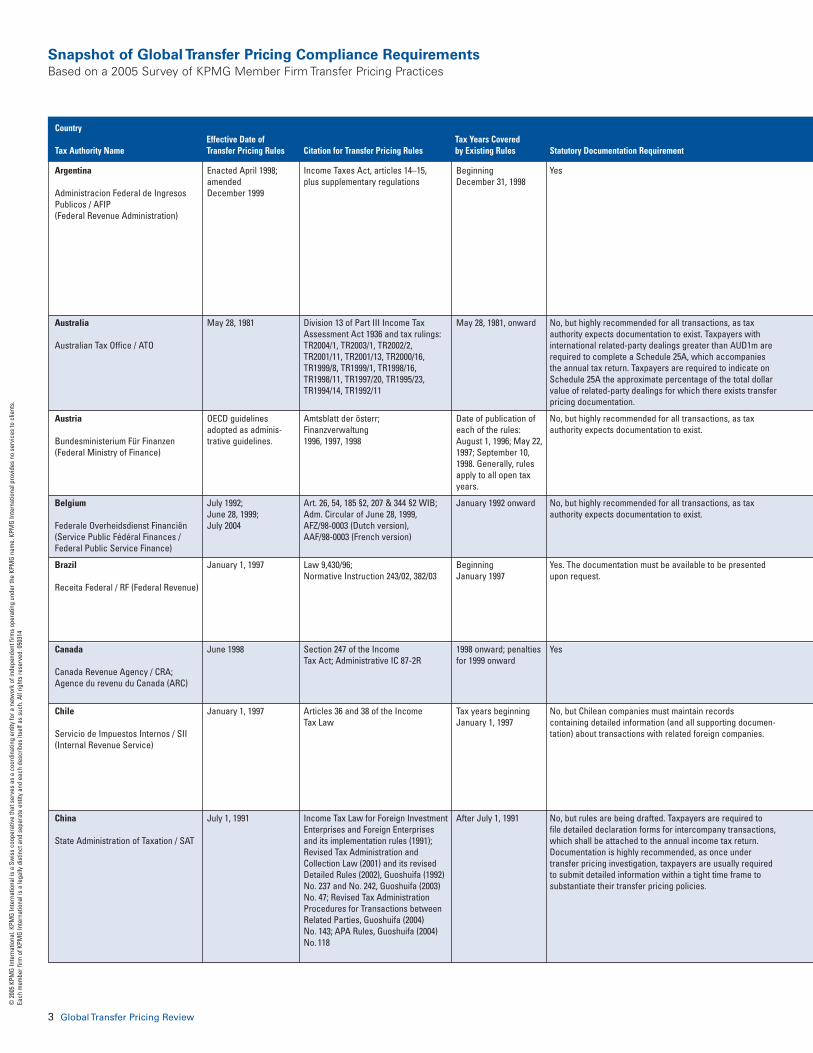

Snapshot of Global Transfer Pricing Compliance Requirements

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

3 Global Transfer Pricing Review

Beginning December 31, 1998

May 28, 1981, onward

Date of publication ofeach of the rules:August 1, 1996; May 22,1997; September 10,1998. Generally, rulesapply to all open taxyears.

January 1992 onward

Beginning January 1997

1998 onward; penaltiesfor 1999 onward

Tax years beginning January 1, 1997

After July 1, 1991

Yes

No, but highly recommended for all transactions, as taxauthority expects documentation to exist. Taxpayers withinternational related-party dealings greater than AUD1m arerequired to complete a Schedule 25A, which accompanies the annual tax return. Taxpayers are required to indicate onSchedule 25A the approximate percentage of the total dollarvalue of related-party dealings for which there exists transferpricing documentation.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Yes. The documentation must be available to be presentedupon request.

Yes

No, but Chilean companies must maintain records containing detailed information (and all supporting documen-tation) about transactions with related foreign companies.

No, but rules are being drafted. Taxpayers are required to file detailed declaration forms for intercompany transactions,which shall be attached to the annual income tax return.Documentation is highly recommended, as once under transfer pricing investigation, taxpayers are usually requiredto submit detailed information within a tight time frame to substantiate their transfer pricing policies.

Enacted April 1998;amended December 1999

May 28, 1981

OECD guidelines adopted as adminis-trative guidelines.

July 1992;June 28, 1999;July 2004

January 1, 1997

June 1998

January 1, 1997

July 1, 1991

Income Taxes Act, articles 14–15, plus supplementary regulations

Division 13 of Part III Income TaxAssessment Act 1936 and tax rulings: TR2004/1, TR2003/1, TR2002/2,TR2001/11, TR2001/13, TR2000/16,TR1999/8, TR1999/1, TR1998/16,TR1998/11, TR1997/20, TR1995/23,TR1994/14, TR1992/11

Amtsblatt der österr;Finanzverwaltung1996, 1997, 1998

Art. 26, 54, 185 §2, 207 & 344 §2 WIB; Adm. Circular of June 28, 1999, AFZ/98-0003 (Dutch version), AAF/98-0003 (French version)

Law 9,430/96; Normative Instruction 243/02, 382/03

Section 247 of the Income Tax Act; Administrative IC 87-2R

Articles 36 and 38 of the Income Tax Law

Income Tax Law for Foreign InvestmentEnterprises and Foreign Enterprisesand its implementation rules (1991);Revised Tax Administration andCollection Law (2001) and its revisedDetailed Rules (2002), Guoshuifa (1992)No. 237 and No. 242, Guoshuifa (2003)No. 47; Revised Tax AdministrationProcedures for Transactions betweenRelated Parties, Guoshuifa (2004) No. 143; APA Rules, Guoshuifa (2004)No. 118

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

Argentina

Administracion Federal de IngresosPublicos / AFIP(Federal Revenue Administration)

Australia

Australian Tax Office / ATO

Austria

Bundesministerium Für Finanzen (Federal Ministry of Finance)

Belgium

Federale Overheidsdienst Financiën(Service Public Fédéral Finances / Federal Public Service Finance)

Brazil

Receita Federal / RF (Federal Revenue)

Canada

Canada Revenue Agency / CRA; Agence du revenu du Canada (ARC)

Chile

Servicio de Impuestos Internos / SII (Internal Revenue Service)

China

State Administration of Taxation / SAT

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

Global Transfer Pricing Review 4

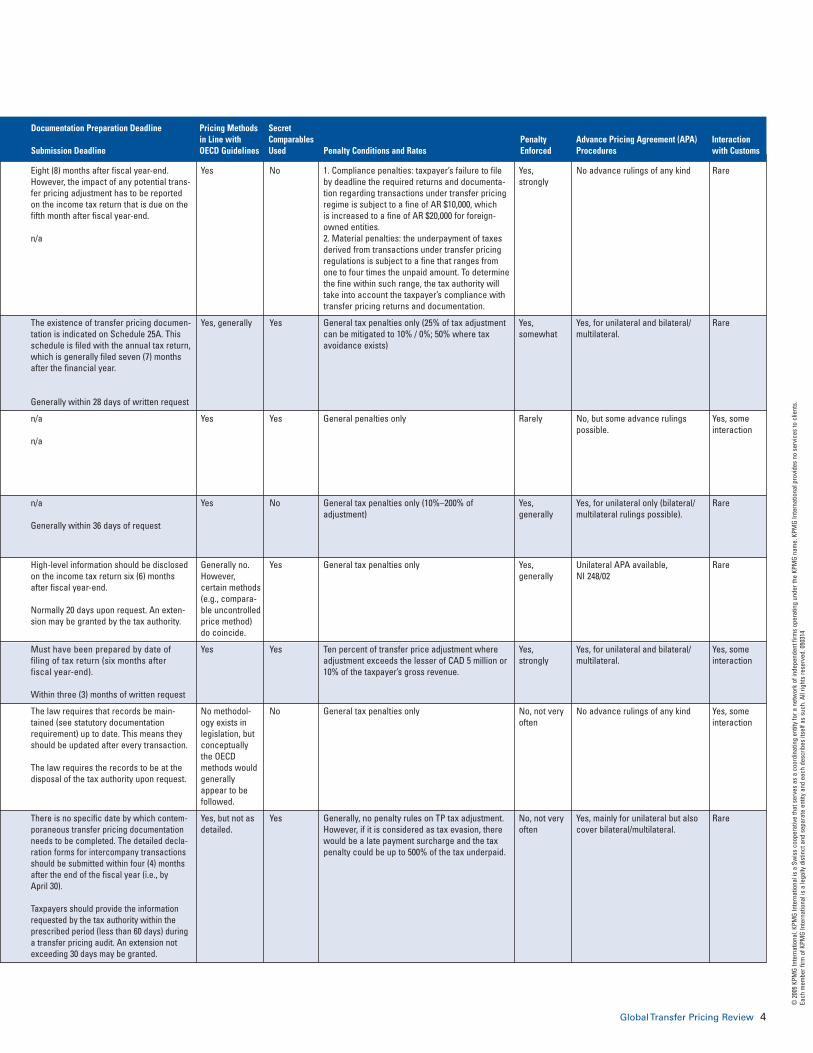

Yes, strongly

Yes, somewhat

Rarely

Yes, generally

Yes, generally

Yes, strongly

No, not veryoften

No, not veryoften

No advance rulings of any kind

Yes, for unilateral and bilateral/ multilateral.

No, but some advance rulingspossible.

Yes, for unilateral only (bilateral/multilateral rulings possible).

Unilateral APA available, NI 248/02

Yes, for unilateral and bilateral/multilateral.

No advance rulings of any kind

Yes, mainly for unilateral but alsocover bilateral/multilateral.

Rare

Rare

Yes, some interaction

Rare

Rare

Yes, someinteraction

Yes, someinteraction

Rare

Eight (8) months after fiscal year-end.However, the impact of any potential trans-fer pricing adjustment has to be reportedon the income tax return that is due on thefifth month after fiscal year-end.

n/a

The existence of transfer pricing documen-tation is indicated on Schedule 25A. Thisschedule is filed with the annual tax return,which is generally filed seven (7) monthsafter the financial year.

Generally within 28 days of written request

n/a

n/a

n/a

Generally within 36 days of request

High-level information should be disclosedon the income tax return six (6) monthsafter fiscal year-end.

Normally 20 days upon request. An exten-sion may be granted by the tax authority.

Must have been prepared by date of filing of tax return (six months after fiscal year-end).

Within three (3) months of written request

The law requires that records be main-tained (see statutory documentationrequirement) up to date. This means theyshould be updated after every transaction.

The law requires the records to be at thedisposal of the tax authority upon request.

There is no specific date by which contem-poraneous transfer pricing documentationneeds to be completed. The detailed decla-ration forms for intercompany transactionsshould be submitted within four (4) monthsafter the end of the fiscal year (i.e., by April 30).

Taxpayers should provide the informationrequested by the tax authority within theprescribed period (less than 60 days) duringa transfer pricing audit. An extension notexceeding 30 days may be granted.

Yes

Yes, generally

Yes

Yes

Generally no.However, certain methods(e.g., compara-ble uncontrolledprice method)do coincide.

Yes

No methodol-ogy exists in legislation, butconceptuallythe OECD methods would generallyappear to befollowed.

Yes, but not asdetailed.

No

Yes

Yes

No

Yes

Yes

No

Yes

1. Compliance penalties: taxpayer’s failure to fileby deadline the required returns and documenta-tion regarding transactions under transfer pricingregime is subject to a fine of AR $10,000, which is increased to a fine of AR $20,000 for foreign-owned entities. 2. Material penalties: the underpayment of taxesderived from transactions under transfer pricingregulations is subject to a fine that ranges fromone to four times the unpaid amount. To determinethe fine within such range, the tax authority willtake into account the taxpayer’s compliance withtransfer pricing returns and documentation.

General tax penalties only (25% of tax adjustmentcan be mitigated to 10% / 0%; 50% where tax avoidance exists)

General penalties only

General tax penalties only (10%–200% of adjustment)

General tax penalties only

Ten percent of transfer price adjustment whereadjustment exceeds the lesser of CAD 5 million or10% of the taxpayer’s gross revenue.

General tax penalties only

Generally, no penalty rules on TP tax adjustment.However, if it is considered as tax evasion, therewould be a late payment surcharge and the taxpenalty could be up to 500% of the tax underpaid.

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

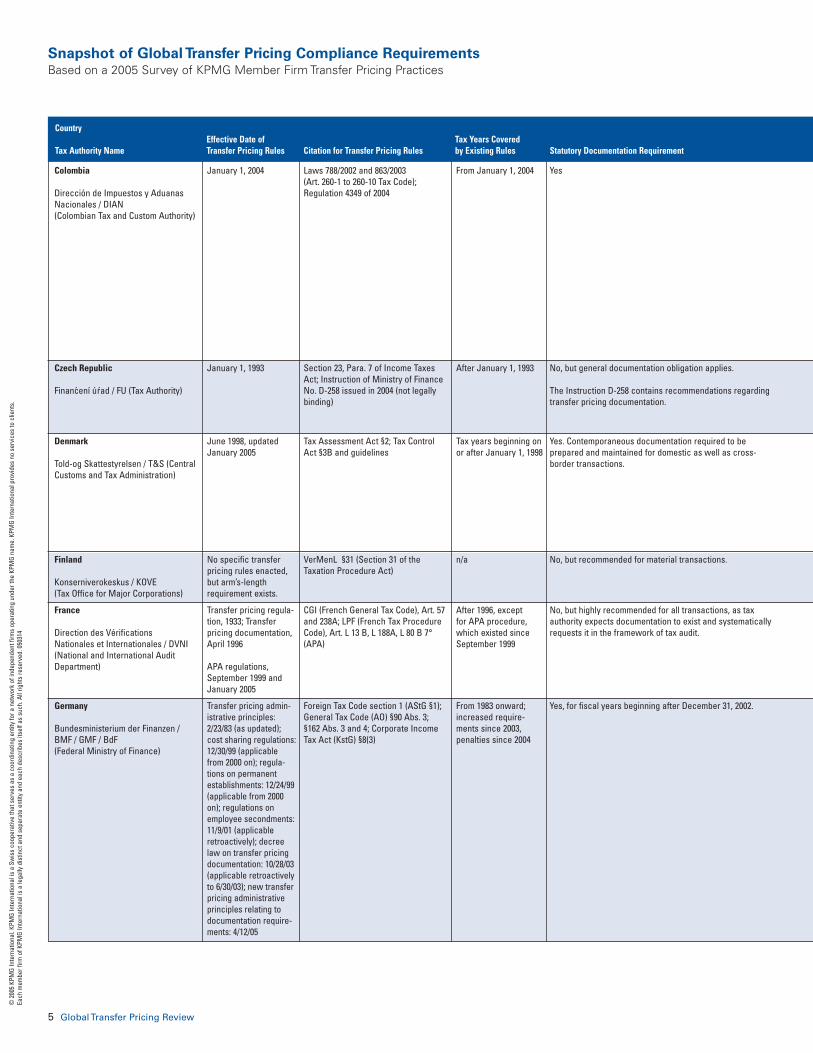

Colombia

Dirección de Impuestos y Aduanas Nacionales / DIAN (Colombian Tax and Custom Authority)

Czech Republic

Financení úrad / FU (Tax Authority)

Denmark

Told-og Skattestyrelsen / T&S (Central Customs and Tax Administration)

Finland

Konserniverokeskus / KOVE (Tax Office for Major Corporations)

France

Direction des Vérifications Nationales et Internationales / DVNI (National and International Audit Department)

Germany

Bundesministerium der Finanzen / BMF / GMF / BdF (Federal Ministry of Finance)

5 Global Transfer Pricing Review

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

From January 1, 2004

After January 1, 1993

Tax years beginning onor after January 1, 1998

n/a

After 1996, except for APA procedure,which existed sinceSeptember 1999

From 1983 onward;increased require-ments since 2003,penalties since 2004

Yes

No, but general documentation obligation applies.

The Instruction D-258 contains recommendations regardingtransfer pricing documentation.

Yes. Contemporaneous documentation required to be prepared and maintained for domestic as well as cross-border transactions.

No, but recommended for material transactions.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist and systematicallyrequests it in the framework of tax audit.

Yes, for fiscal years beginning after December 31, 2002.

January 1, 2004

January 1, 1993

June 1998, updatedJanuary 2005

No specific transferpricing rules enacted,but arm’s-lengthrequirement exists.

Transfer pricing regula-tion, 1933; Transfer pricing documentation,April 1996

APA regulations,September 1999 andJanuary 2005

Transfer pricing admin-istrative principles:2/23/83 (as updated);cost sharing regulations:12/30/99 (applicablefrom 2000 on); regula-tions on permanentestablishments: 12/24/99(applicable from 2000on); regulations onemployee secondments:11/9/01 (applicableretroactively); decreelaw on transfer pricingdocumentation: 10/28/03(applicable retroactivelyto 6/30/03); new transferpricing administrativeprinciples relating todocumentation require-ments: 4/12/05

Laws 788/2002 and 863/2003 (Art. 260-1 to 260-10 Tax Code);Regulation 4349 of 2004

Section 23, Para. 7 of Income TaxesAct; Instruction of Ministry of Finance No. D-258 issued in 2004 (not legallybinding)

Tax Assessment Act §2; Tax ControlAct §3B and guidelines

VerMenL §31 (Section 31 of theTaxation Procedure Act)

CGI (French General Tax Code), Art. 57and 238A; LPF (French Tax ProcedureCode), Art. L 13 B, L 188A, L 80 B 7°(APA)

Foreign Tax Code section 1 (AStG §1);General Tax Code (AO) §90 Abs. 3; §162 Abs. 3 and 4; Corporate IncomeTax Act (KstG) §8(3)

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

Global Transfer Pricing Review 6

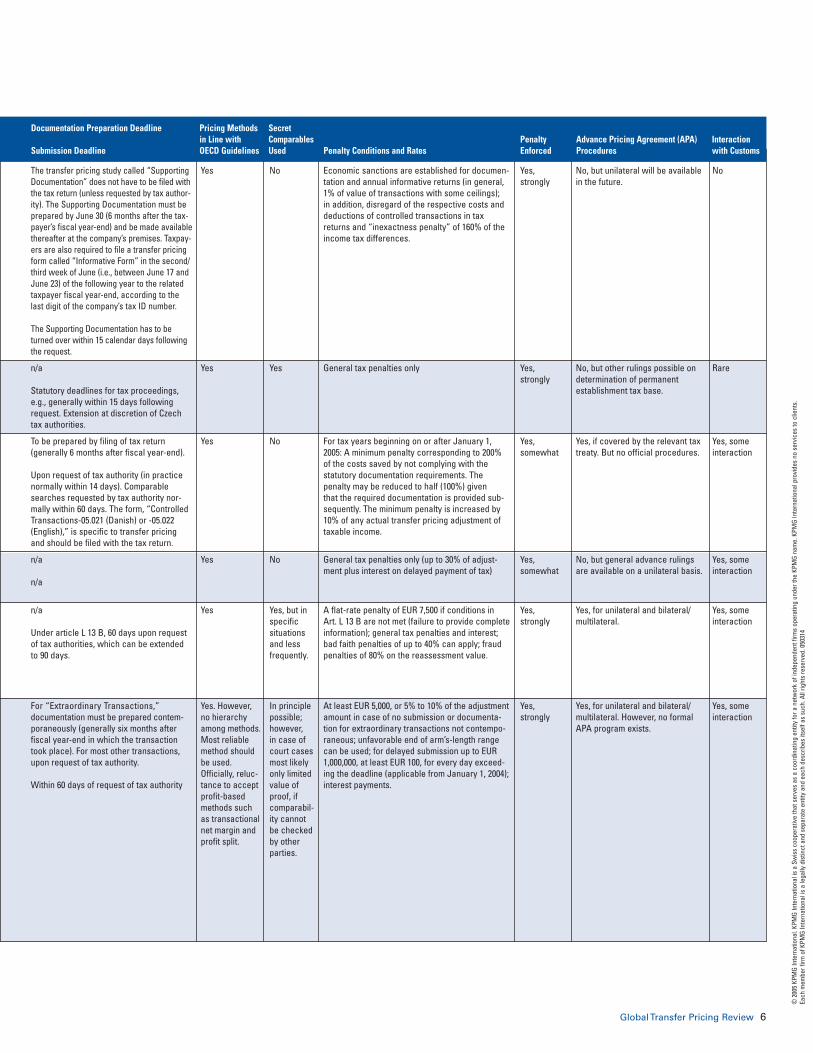

Yes, strongly

Yes, strongly

Yes, somewhat

Yes, somewhat

Yes, strongly

Yes, strongly

No, but unilateral will be availablein the future.

No, but other rulings possible ondetermination of permanentestablishment tax base.

Yes, if covered by the relevant taxtreaty. But no official procedures.

No, but general advance rulingsare available on a unilateral basis.

Yes, for unilateral and bilateral/ multilateral.

Yes, for unilateral and bilateral/ multilateral. However, no formalAPA program exists.

No

Rare

Yes, someinteraction

Yes, someinteraction

Yes, someinteraction

Yes, someinteraction

The transfer pricing study called “SupportingDocumentation” does not have to be filed withthe tax return (unless requested by tax author-ity). The Supporting Documentation must beprepared by June 30 (6 months after the tax-payer’s fiscal year-end) and be made availablethereafter at the company’s premises. Taxpay-ers are also required to file a transfer pricingform called “Informative Form” in the second/third week of June (i.e., between June 17 andJune 23) of the following year to the relatedtaxpayer fiscal year-end, according to thelast digit of the company’s tax ID number.

The Supporting Documentation has to beturned over within 15 calendar days followingthe request.

n/a

Statutory deadlines for tax proceedings,e.g., generally within 15 days followingrequest. Extension at discretion of Czechtax authorities.

To be prepared by filing of tax return (generally 6 months after fiscal year-end).

Upon request of tax authority (in practicenormally within 14 days). Comparablesearches requested by tax authority nor-mally within 60 days. The form, “ControlledTransactions-05.021 (Danish) or -05.022(English),” is specific to transfer pricingand should be filed with the tax return.

n/a

n/a

n/a

Under article L 13 B, 60 days upon requestof tax authorities, which can be extendedto 90 days.

For “Extraordinary Transactions,” documentation must be prepared contem-poraneously (generally six months after fiscal year-end in which the transactiontook place). For most other transactions,upon request of tax authority.

Within 60 days of request of tax authority

Yes

Yes

Yes

Yes

Yes

Yes. However, no hierarchyamong methods.Most reliablemethod shouldbe used.Officially, reluc-tance to acceptprofit-basedmethods suchas transactionalnet margin and profit split.

No

Yes

No

No

Yes, but inspecific situationsand lessfrequently.

In principlepossible;however, in case ofcourt casesmost likelyonly limitedvalue ofproof, ifcomparabil-ity cannotbe checkedby otherparties.

Economic sanctions are established for documen-tation and annual informative returns (in general,1% of value of transactions with some ceilings); in addition, disregard of the respective costs anddeductions of controlled transactions in taxreturns and “inexactness penalty” of 160% of theincome tax differences.

General tax penalties only

For tax years beginning on or after January 1,2005: A minimum penalty corresponding to 200% of the costs saved by not complying with thestatutory documentation requirements. Thepenalty may be reduced to half (100%) given that the required documentation is provided sub-sequently. The minimum penalty is increased by10% of any actual transfer pricing adjustment oftaxable income.

General tax penalties only (up to 30% of adjust-ment plus interest on delayed payment of tax)

A flat-rate penalty of EUR 7,500 if conditions in Art. L 13 B are not met (failure to provide completeinformation); general tax penalties and interest;bad faith penalties of up to 40% can apply; fraudpenalties of 80% on the reassessment value.

At least EUR 5,000, or 5% to 10% of the adjustmentamount in case of no submission or documenta-tion for extraordinary transactions not contempo-raneous; unfavorable end of arm’s-length rangecan be used; for delayed submission up to EUR1,000,000, at least EUR 100, for every day exceed-ing the deadline (applicable from January 1, 2004);interest payments.

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

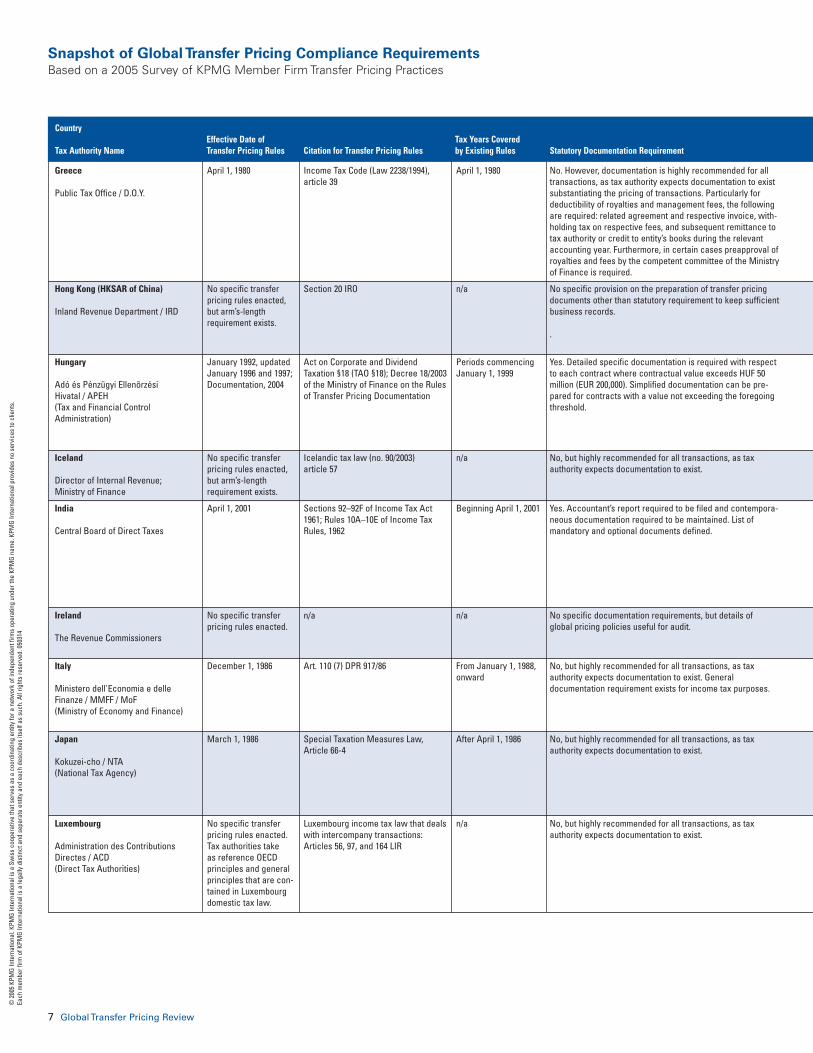

Greece

Public Tax Office / D.O.Y.

Hong Kong (HKSAR of China)

Inland Revenue Department / IRD

Hungary

Adó és Pénzügyi Ellenõrzési Hivatal / APEH(Tax and Financial Control Administration)

Iceland

Director of Internal Revenue; Ministry of Finance

India

Central Board of Direct Taxes

Ireland

The Revenue Commissioners

Italy

Ministero dell'Economia e delle Finanze / MMFF / MoF (Ministry of Economy and Finance)

Japan

Kokuzei-cho / NTA(National Tax Agency)

Luxembourg

Administration des Contributions Directes / ACD (Direct Tax Authorities)

7 Global Transfer Pricing Review

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

April 1, 1980

No specific transferpricing rules enacted,but arm’s-lengthrequirement exists.

January 1992, updatedJanuary 1996 and 1997;Documentation, 2004

No specific transferpricing rules enacted,but arm’s-lengthrequirement exists.

April 1, 2001

No specific transferpricing rules enacted.

December 1, 1986

March 1, 1986

No specific transferpricing rules enacted.Tax authorities take as reference OECDprinciples and generalprinciples that are con-tained in Luxembourgdomestic tax law.

Income Tax Code (Law 2238/1994), article 39

Section 20 IRO

Act on Corporate and DividendTaxation §18 (TAO §18); Decree 18/2003of the Ministry of Finance on the Rulesof Transfer Pricing Documentation

Icelandic tax law (no. 90/2003) article 57

Sections 92–92F of Income Tax Act1961; Rules 10A–10E of Income TaxRules, 1962

n/a

Art. 110 (7) DPR 917/86

Special Taxation Measures Law,Article 66-4

Luxembourg income tax law that dealswith intercompany transactions: Articles 56, 97, and 164 LIR

April 1, 1980

n/a

Periods commencingJanuary 1, 1999

n/a

Beginning April 1, 2001

n/a

From January 1, 1988,onward

After April 1, 1986

n/a

No. However, documentation is highly recommended for all transactions, as tax authority expects documentation to existsubstantiating the pricing of transactions. Particularly fordeductibility of royalties and management fees, the following are required: related agreement and respective invoice, with-holding tax on respective fees, and subsequent remittance to tax authority or credit to entity’s books during the relevantaccounting year. Furthermore, in certain cases preapproval ofroyalties and fees by the competent committee of the Ministry of Finance is required.

No specific provision on the preparation of transfer pricingdocuments other than statutory requirement to keep sufficientbusiness records.

.

Yes. Detailed specific documentation is required with respectto each contract where contractual value exceeds HUF 50million (EUR 200,000). Simplified documentation can be pre-pared for contracts with a value not exceeding the foregoingthreshold.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Yes. Accountant’s report required to be filed and contempora-neous documentation required to be maintained. List ofmandatory and optional documents defined.

No specific documentation requirements, but details of global pricing policies useful for audit.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist. General documentation requirement exists for income tax purposes.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

Global Transfer Pricing Review 8

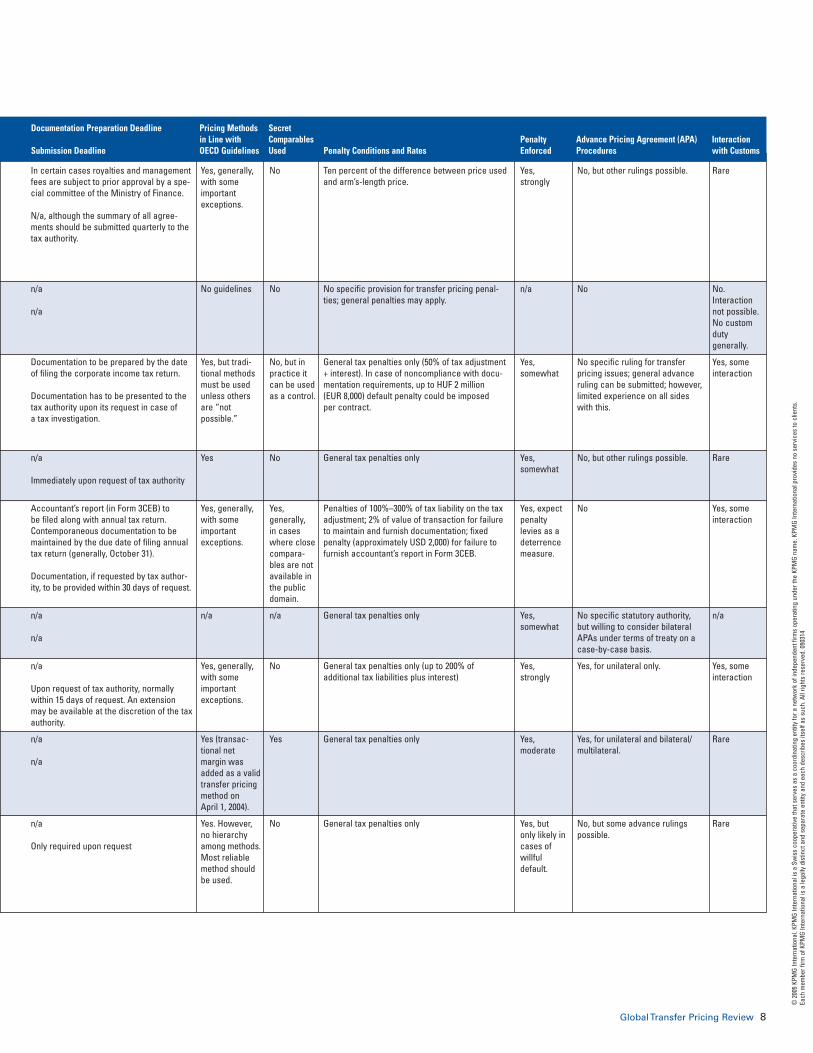

Yes, strongly

n/a

Yes, somewhat

Yes, somewhat

Yes, expectpenaltylevies as adeterrencemeasure.

Yes, somewhat

Yes, strongly

Yes, moderate

Yes, but only likely incases ofwillfuldefault.

No, but other rulings possible.

No

No specific ruling for transferpricing issues; general advanceruling can be submitted; however,limited experience on all sideswith this.

No, but other rulings possible.

No

No specific statutory authority,but willing to consider bilateralAPAs under terms of treaty on acase-by-case basis.

Yes, for unilateral only.

Yes, for unilateral and bilateral/ multilateral.

No, but some advance rulingspossible.

Rare

No.Interactionnot possible.No customduty generally.

Yes, someinteraction

Rare

Yes, someinteraction

n/a

Yes, someinteraction

Rare

Rare

Yes, generally,with someimportantexceptions.

No guidelines

Yes, but tradi-tional methodsmust be usedunless othersare “not possible.”

Yes

Yes, generally,with someimportantexceptions.

n/a

Yes, generally,with someimportantexceptions.

Yes (transac-tional net margin wasadded as a validtransfer pricingmethod on April 1, 2004).

Yes. However,no hierarchyamong methods.Most reliablemethod shouldbe used.

No

No

No, but inpractice itcan be usedas a control.

No

Yes, generally, in caseswhere closecompara-bles are notavailable inthe publicdomain.

n/a

No

Yes

No

Ten percent of the difference between price usedand arm’s-length price.

No specific provision for transfer pricing penal-ties; general penalties may apply.

General tax penalties only (50% of tax adjustment+ interest). In case of noncompliance with docu-mentation requirements, up to HUF 2 million (EUR 8,000) default penalty could be imposed per contract.

General tax penalties only

Penalties of 100%–300% of tax liability on the taxadjustment; 2% of value of transaction for failureto maintain and furnish documentation; fixedpenalty (approximately USD 2,000) for failure tofurnish accountant’s report in Form 3CEB.

General tax penalties only

General tax penalties only (up to 200% of additional tax liabilities plus interest)

General tax penalties only

General tax penalties only

In certain cases royalties and managementfees are subject to prior approval by a spe-cial committee of the Ministry of Finance.

N/a, although the summary of all agree-ments should be submitted quarterly to thetax authority.

n/a

n/a

Documentation to be prepared by the dateof filing the corporate income tax return.

Documentation has to be presented to thetax authority upon its request in case of a tax investigation.

n/a

Immediately upon request of tax authority

Accountant’s report (in Form 3CEB) to be filed along with annual tax return.Contemporaneous documentation to bemaintained by the due date of filing annualtax return (generally, October 31).

Documentation, if requested by tax author-ity, to be provided within 30 days of request.

n/a

n/a

n/a

Upon request of tax authority, normallywithin 15 days of request. An extensionmay be available at the discretion of the taxauthority.

n/a

n/a

n/a

Only required upon request

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

9 Global Transfer Pricing Review

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

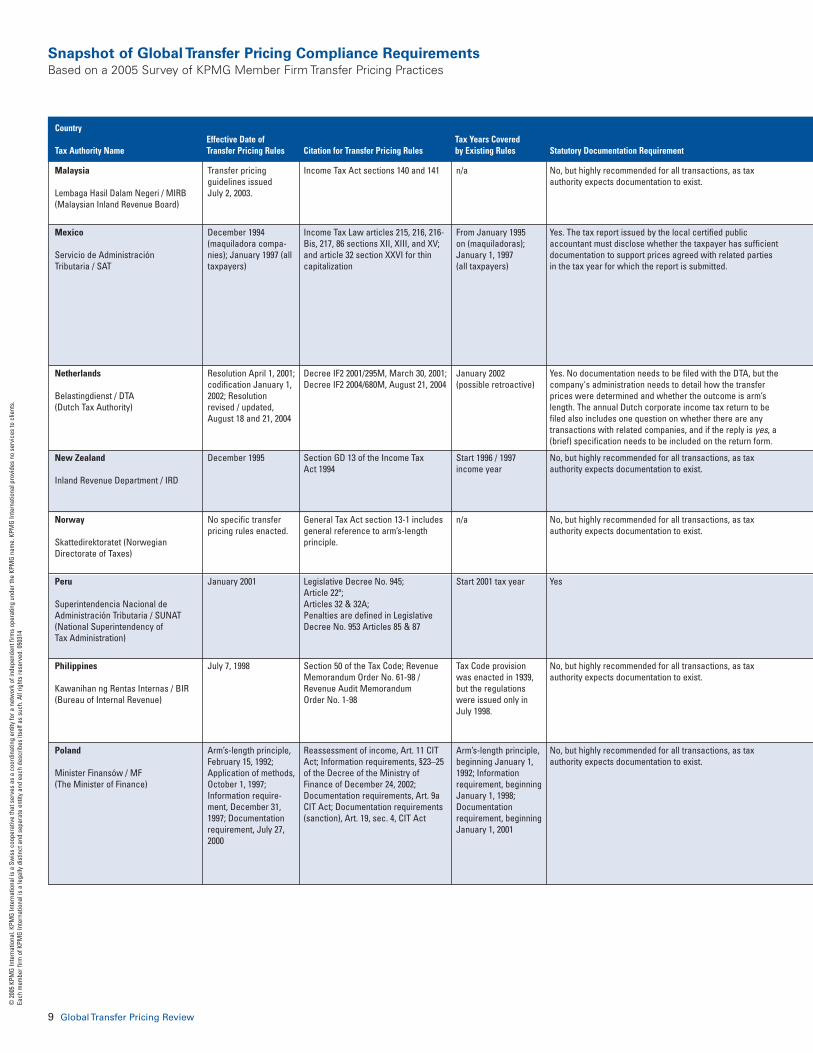

Malaysia

Lembaga Hasil Dalam Negeri / MIRB(Malaysian Inland Revenue Board)

Mexico

Servicio de Administración Tributaria / SAT

Netherlands

Belastingdienst / DTA (Dutch Tax Authority)

New Zealand

Inland Revenue Department / IRD

Norway

Skattedirektoratet (Norwegian Directorate of Taxes)

Peru

Superintendencia Nacional de Administración Tributaria / SUNAT (National Superintendency of Tax Administration)

Philippines

Kawanihan ng Rentas Internas / BIR (Bureau of Internal Revenue)

Poland

Minister Finansów / MF (The Minister of Finance)

Transfer pricing guidelines issued July 2, 2003.

December 1994(maquiladora compa-nies); January 1997 (alltaxpayers)

Resolution April 1, 2001;codification January 1,2002; Resolution revised / updated, August 18 and 21, 2004

December 1995

No specific transferpricing rules enacted.

January 2001

July 7, 1998

Arm’s-length principle,February 15, 1992;Application of methods,October 1, 1997;Information require-ment, December 31,1997; Documentationrequirement, July 27,2000

Income Tax Act sections 140 and 141

Income Tax Law articles 215, 216, 216-Bis, 217, 86 sections XII, XIII, and XV;and article 32 section XXVI for thincapitalization

Decree IF2 2001/295M, March 30, 2001;Decree IF2 2004/680M, August 21, 2004

Section GD 13 of the Income Tax Act 1994

General Tax Act section 13-1 includesgeneral reference to arm’s-length principle.

Legislative Decree No. 945; Article 22º;Articles 32 & 32A; Penalties are defined in LegislativeDecree No. 953 Articles 85 & 87

Section 50 of the Tax Code; RevenueMemorandum Order No. 61-98 /Revenue Audit Memorandum Order No. 1-98

Reassessment of income, Art. 11 CITAct; Information requirements, §23–25of the Decree of the Ministry ofFinance of December 24, 2002;Documentation requirements, Art. 9aCIT Act; Documentation requirements(sanction), Art. 19, sec. 4, CIT Act

n/a

From January 1995 on (maquiladoras);January 1, 1997 (all taxpayers)

January 2002 (possible retroactive)

Start 1996 / 1997income year

n/a

Start 2001 tax year

Tax Code provisionwas enacted in 1939,but the regulationswere issued only inJuly 1998.

Arm’s-length principle,beginning January 1,1992; Informationrequirement, beginningJanuary 1, 1998;Documentationrequirement, beginningJanuary 1, 2001

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Yes. The tax report issued by the local certified publicaccountant must disclose whether the taxpayer has sufficient documentation to support prices agreed with related partiesin the tax year for which the report is submitted.

Yes. No documentation needs to be filed with the DTA, but thecompany's administration needs to detail how the transferprices were determined and whether the outcome is arm’slength. The annual Dutch corporate income tax return to befiled also includes one question on whether there are anytransactions with related companies, and if the reply is yes, a(brief) specification needs to be included on the return form.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Yes

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

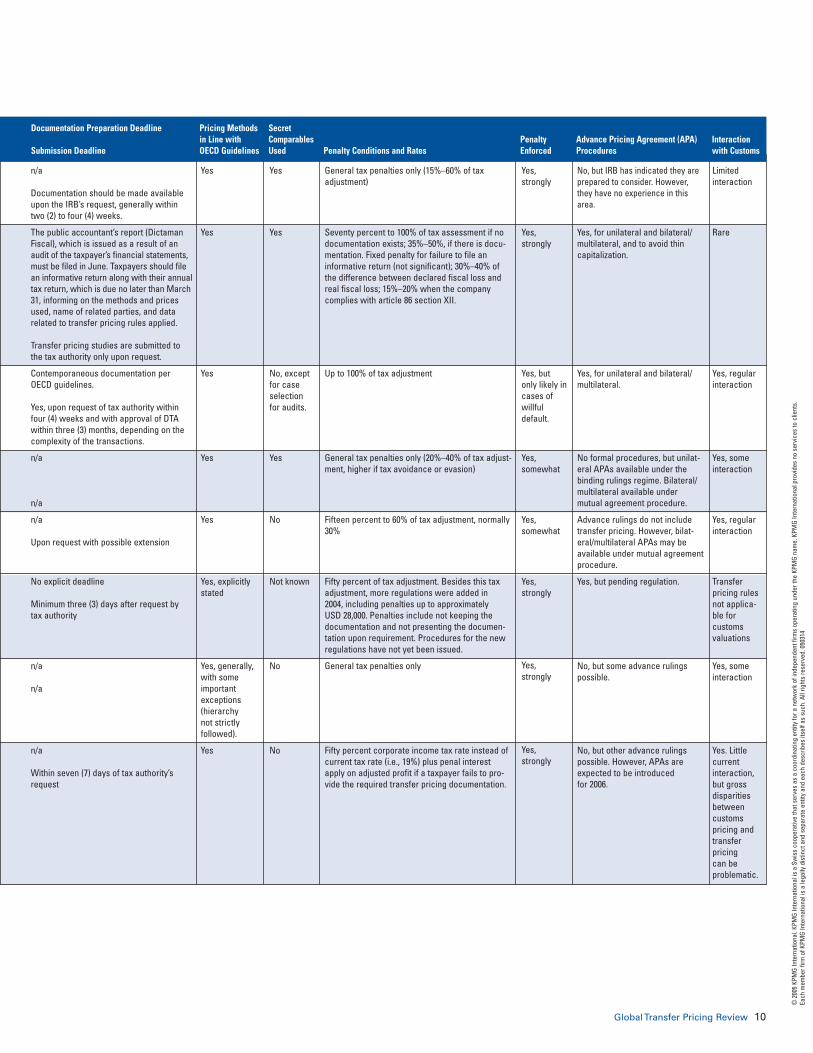

Global Transfer Pricing Review 10

Yes, strongly

Yes, strongly

Yes, but only likely incases ofwillfuldefault.

Yes, somewhat

Yes, somewhat

Yes, strongly

Yes, strongly

Yes, strongly

No, but IRB has indicated they areprepared to consider. However,they have no experience in thisarea.

Yes, for unilateral and bilateral/ multilateral, and to avoid thin capitalization.

Yes, for unilateral and bilateral/ multilateral.

No formal procedures, but unilat-eral APAs available under thebinding rulings regime. Bilateral/multilateral available undermutual agreement procedure.

Advance rulings do not includetransfer pricing. However, bilat-eral/multilateral APAs may beavailable under mutual agreementprocedure.

Yes, but pending regulation.

No, but some advance rulingspossible.

No, but other advance rulingspossible. However, APAs areexpected to be introduced for 2006.

Limitedinteraction

Rare

Yes, regularinteraction

Yes, someinteraction

Yes, regularinteraction

Transferpricing rulesnot applica-ble for customs valuations

Yes, someinteraction

Yes. Littlecurrentinteraction,but grossdisparitiesbetweencustomspricing andtransferpricing can be problematic.

Yes

Yes

Yes

Yes

Yes

Yes, explicitlystated

Yes, generally,with someimportantexceptions(hierarchy not strictly followed).

Yes

Yes

Yes

No, exceptfor caseselectionfor audits.

Yes

No

Not known

No

No

General tax penalties only (15%–60% of tax adjustment)

Seventy percent to 100% of tax assessment if nodocumentation exists; 35%–50%, if there is docu-mentation. Fixed penalty for failure to file aninformative return (not significant); 30%–40% ofthe difference between declared fiscal loss andreal fiscal loss; 15%–20% when the company complies with article 86 section XII.

Up to 100% of tax adjustment

General tax penalties only (20%–40% of tax adjust-ment, higher if tax avoidance or evasion)

Fifteen percent to 60% of tax adjustment, normally30%

Fifty percent of tax adjustment. Besides this taxadjustment, more regulations were added in 2004, including penalties up to approximately USD 28,000. Penalties include not keeping the documentation and not presenting the documen-tation upon requirement. Procedures for the newregulations have not yet been issued.

General tax penalties only

Fifty percent corporate income tax rate instead ofcurrent tax rate (i.e., 19%) plus penal interestapply on adjusted profit if a taxpayer fails to pro-vide the required transfer pricing documentation.

n/a

Documentation should be made availableupon the IRB’s request, generally withintwo (2) to four (4) weeks.

The public accountant’s report (DictamanFiscal), which is issued as a result of anaudit of the taxpayer’s financial statements,must be filed in June. Taxpayers should filean informative return along with their annualtax return, which is due no later than March31, informing on the methods and pricesused, name of related parties, and datarelated to transfer pricing rules applied.

Transfer pricing studies are submitted tothe tax authority only upon request.

Contemporaneous documentation perOECD guidelines.

Yes, upon request of tax authority withinfour (4) weeks and with approval of DTAwithin three (3) months, depending on thecomplexity of the transactions.

n/a

n/a

n/a

Upon request with possible extension

No explicit deadline

Minimum three (3) days after request by tax authority

n/a

n/a

n/a

Within seven (7) days of tax authority’srequest

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

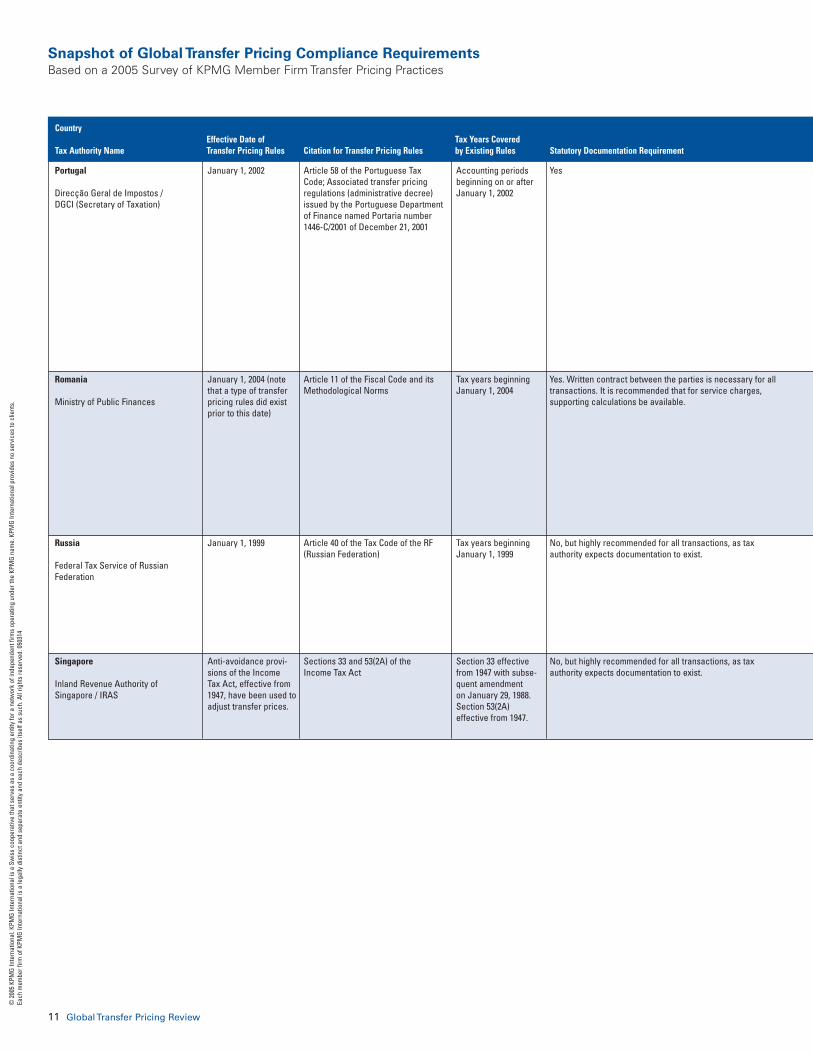

Portugal

Direcção Geral de Impostos / DGCI (Secretary of Taxation)

Romania

Ministry of Public Finances

Russia

Federal Tax Service of Russian Federation

Singapore

Inland Revenue Authority of Singapore / IRAS

11 Global Transfer Pricing Review

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

January 1, 2002

January 1, 2004 (notethat a type of transferpricing rules did existprior to this date)

January 1, 1999

Anti-avoidance provi-sions of the Income Tax Act, effective from1947, have been used toadjust transfer prices.

Article 58 of the Portuguese TaxCode; Associated transfer pricing regulations (administrative decree)issued by the Portuguese Departmentof Finance named Portaria number1446-C/2001 of December 21, 2001

Article 11 of the Fiscal Code and itsMethodological Norms

Article 40 of the Tax Code of the RF(Russian Federation)

Sections 33 and 53(2A) of the Income Tax Act

Accounting periodsbeginning on or afterJanuary 1, 2002

Tax years beginningJanuary 1, 2004

Tax years beginningJanuary 1, 1999

Section 33 effectivefrom 1947 with subse-quent amendment on January 29, 1988.Section 53(2A) effective from 1947.

Yes

Yes. Written contract between the parties is necessary for alltransactions. It is recommended that for service charges, supporting calculations be available.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

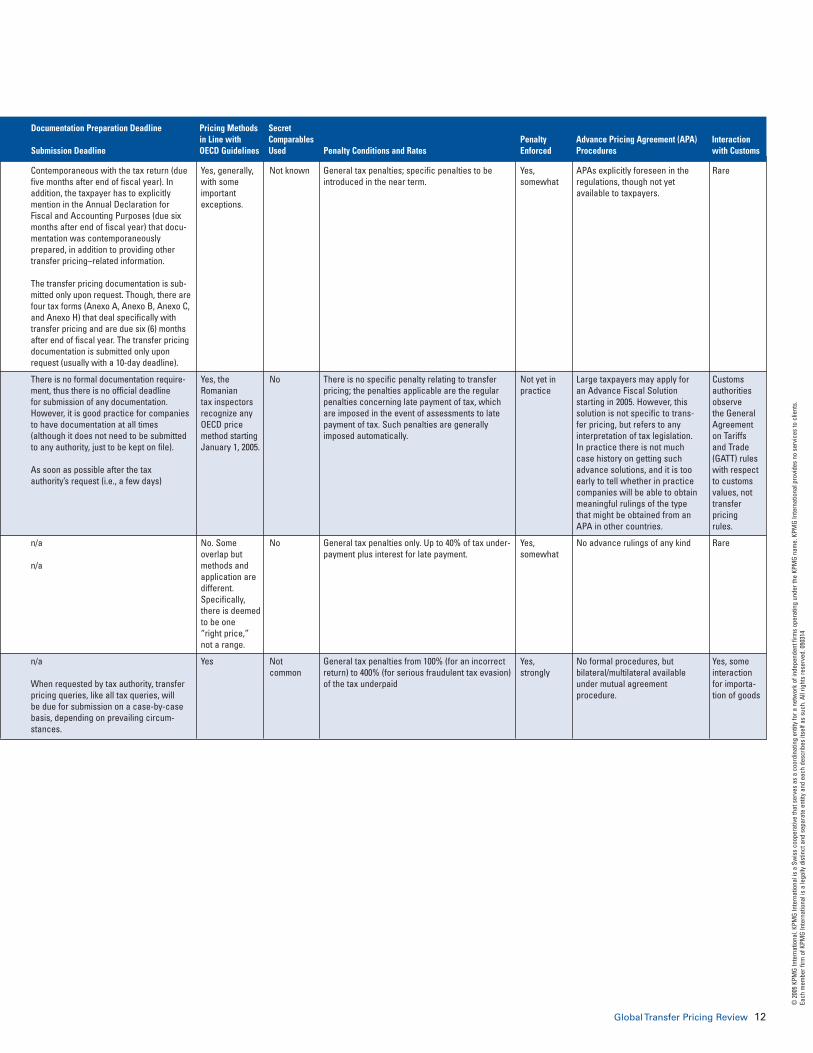

Global Transfer Pricing Review 12

Yes, somewhat

Not yet inpractice

Yes, somewhat

Yes, strongly

APAs explicitly foreseen in theregulations, though not yetavailable to taxpayers.

Large taxpayers may apply foran Advance Fiscal Solutionstarting in 2005. However, thissolution is not specific to trans-fer pricing, but refers to anyinterpretation of tax legislation.In practice there is not muchcase history on getting suchadvance solutions, and it is tooearly to tell whether in practicecompanies will be able to obtainmeaningful rulings of the typethat might be obtained from anAPA in other countries.

No advance rulings of any kind

No formal procedures, but bilateral/multilateral availableunder mutual agreement procedure.

Rare

Customsauthoritiesobserve the GeneralAgreementon Tariffsand Trade(GATT) ruleswith respectto customs values, nottransferpricingrules.

Rare

Yes, someinteractionfor importa-tion of goods

Yes, generally,with someimportantexceptions.

Yes, theRomanian tax inspectors recognize anyOECD pricemethod startingJanuary 1, 2005.

No. Some overlap butmethods andapplication aredifferent.Specifically,there is deemedto be one “right price,” not a range.

Yes

Not known

No

No

Not common

General tax penalties; specific penalties to beintroduced in the near term.

There is no specific penalty relating to transferpricing; the penalties applicable are the regularpenalties concerning late payment of tax, whichare imposed in the event of assessments to latepayment of tax. Such penalties are generallyimposed automatically.

General tax penalties only. Up to 40% of tax under-payment plus interest for late payment.

General tax penalties from 100% (for an incorrectreturn) to 400% (for serious fraudulent tax evasion)of the tax underpaid

Contemporaneous with the tax return (duefive months after end of fiscal year). Inaddition, the taxpayer has to explicitly mention in the Annual Declaration forFiscal and Accounting Purposes (due sixmonths after end of fiscal year) that docu-mentation was contemporaneously prepared, in addition to providing othertransfer pricing–related information.

The transfer pricing documentation is sub-mitted only upon request. Though, there arefour tax forms (Anexo A, Anexo B, Anexo C,and Anexo H) that deal specifically withtransfer pricing and are due six (6) monthsafter end of fiscal year. The transfer pricingdocumentation is submitted only uponrequest (usually with a 10-day deadline).

There is no formal documentation require-ment, thus there is no official deadline for submission of any documentation.However, it is good practice for companiesto have documentation at all times(although it does not need to be submittedto any authority, just to be kept on file).

As soon as possible after the tax authority’s request (i.e., a few days)

n/a

n/a

n/a

When requested by tax authority, transferpricing queries, like all tax queries, will be due for submission on a case-by-casebasis, depending on prevailing circum-stances.

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

13 Global Transfer Pricing Review

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

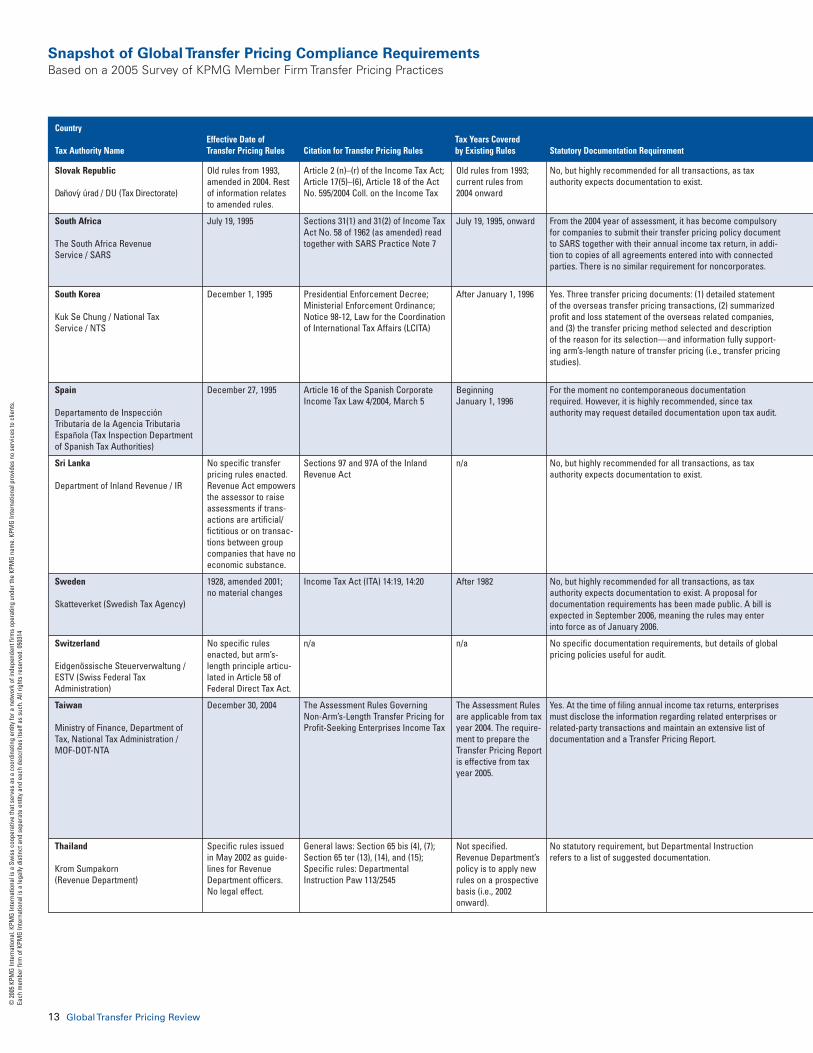

Slovak Republic

Danovy úrad / DU (Tax Directorate)

South Africa

The South Africa Revenue Service / SARS

South Korea

Kuk Se Chung / National Tax Service / NTS

Spain

Departamento de Inspección Tributaria de la Agencia Tributaria Española (Tax Inspection Department of Spanish Tax Authorities)

Sri Lanka

Department of Inland Revenue / IR

Sweden

Skatteverket (Swedish Tax Agency)

Switzerland

Eidgenössische Steuerverwaltung / ESTV (Swiss Federal Tax Administration)

Taiwan

Ministry of Finance, Department of Tax, National Tax Administration / MOF-DOT-NTA

Thailand

Krom Sumpakorn (Revenue Department)

Old rules from 1993,amended in 2004. Restof information relates to amended rules.

July 19, 1995

December 1, 1995

December 27, 1995

No specific transferpricing rules enacted.Revenue Act empowersthe assessor to raiseassessments if trans-actions are artificial/fictitious or on transac-tions between groupcompanies that have no economic substance.

1928, amended 2001; no material changes

No specific rulesenacted, but arm’s-length principle articu-lated in Article 58 ofFederal Direct Tax Act.

December 30, 2004

Specific rules issued in May 2002 as guide-lines for RevenueDepartment officers. No legal effect.

Article 2 (n)–(r) of the Income Tax Act;Article 17(5)–(6), Article 18 of the ActNo. 595/2004 Coll. on the Income Tax

Sections 31(1) and 31(2) of Income TaxAct No. 58 of 1962 (as amended) readtogether with SARS Practice Note 7

Presidential Enforcement Decree;Ministerial Enforcement Ordinance;Notice 98-12, Law for the Coordinationof International Tax Affairs (LCITA)

Article 16 of the Spanish CorporateIncome Tax Law 4/2004, March 5

Sections 97 and 97A of the Inland Revenue Act

Income Tax Act (ITA) 14:19, 14:20

n/a

The Assessment Rules Governing Non-Arm’s-Length Transfer Pricing forProfit-Seeking Enterprises Income Tax

General laws: Section 65 bis (4), (7);Section 65 ter (13), (14), and (15);Specific rules: DepartmentalInstruction Paw 113/2545

Old rules from 1993;current rules from 2004 onward

July 19, 1995, onward

After January 1, 1996

Beginning January 1, 1996

n/a

After 1982

n/a

The Assessment Rulesare applicable from taxyear 2004. The require-ment to prepare theTransfer Pricing Reportis effective from taxyear 2005.

Not specified.Revenue Department’spolicy is to apply newrules on a prospectivebasis (i.e., 2002onward).

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

From the 2004 year of assessment, it has become compulsoryfor companies to submit their transfer pricing policy documentto SARS together with their annual income tax return, in addi-tion to copies of all agreements entered into with connectedparties. There is no similar requirement for noncorporates.

Yes. Three transfer pricing documents: (1) detailed statementof the overseas transfer pricing transactions, (2) summarizedprofit and loss statement of the overseas related companies,and (3) the transfer pricing method selected and descriptionof the reason for its selection—and information fully support-ing arm’s-length nature of transfer pricing (i.e., transfer pricingstudies).

For the moment no contemporaneous documentationrequired. However, it is highly recommended, since taxauthority may request detailed documentation upon tax audit.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist.

No, but highly recommended for all transactions, as taxauthority expects documentation to exist. A proposal for documentation requirements has been made public. A bill isexpected in September 2006, meaning the rules may enter into force as of January 2006.

No specific documentation requirements, but details of globalpricing policies useful for audit.

Yes. At the time of filing annual income tax returns, enterprisesmust disclose the information regarding related enterprises orrelated-party transactions and maintain an extensive list ofdocumentation and a Transfer Pricing Report.

No statutory requirement, but Departmental Instruction refers to a list of suggested documentation.

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

Global Transfer Pricing Review 14

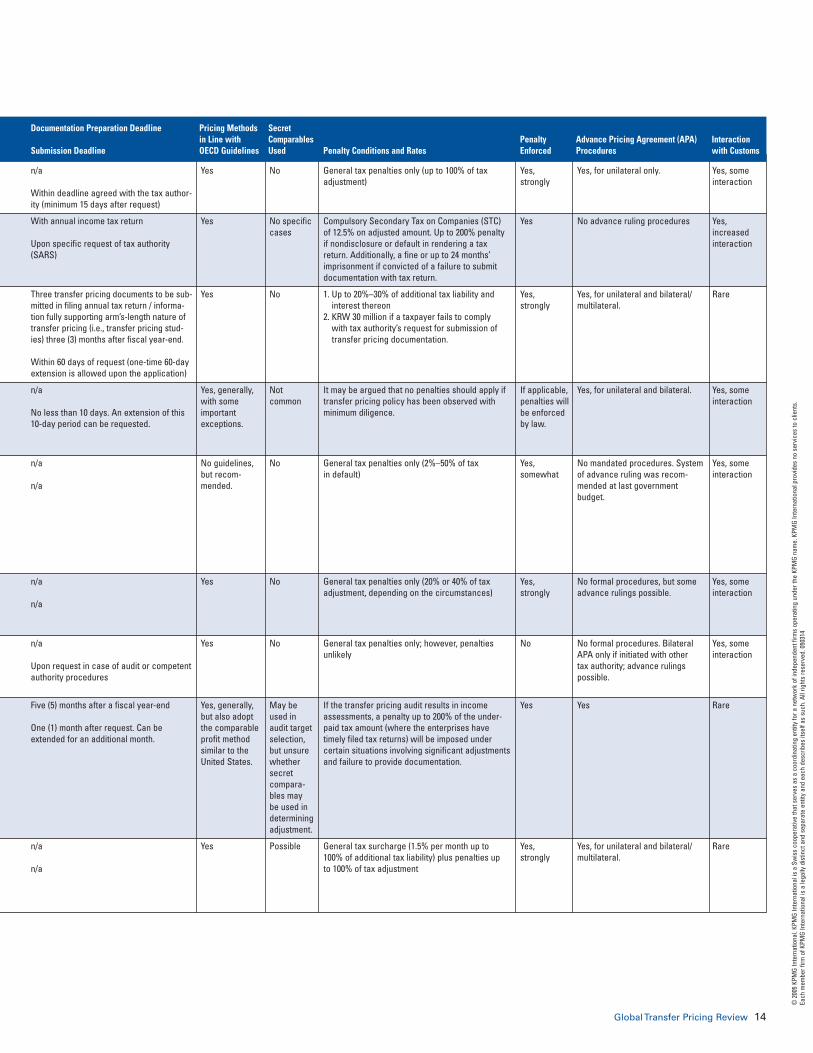

Yes, strongly

Yes

Yes, strongly

If applicable,penalties willbe enforcedby law.

Yes, somewhat

Yes, strongly

No

Yes

Yes, strongly

Yes, for unilateral only.

No advance ruling procedures

Yes, for unilateral and bilateral/ multilateral.

Yes, for unilateral and bilateral.

No mandated procedures. Systemof advance ruling was recom-mended at last governmentbudget.

No formal procedures, but someadvance rulings possible.

No formal procedures. BilateralAPA only if initiated with other tax authority; advance rulingspossible.

Yes

Yes, for unilateral and bilateral/ multilateral.

Yes, someinteraction

Yes,increasedinteraction

Rare

Yes, someinteraction

Yes, someinteraction

Yes, someinteraction

Yes, someinteraction

Rare

Rare

Yes

Yes

Yes

Yes, generally,with someimportantexceptions.

No guidelines,but recom-mended.

Yes

Yes

Yes, generally,but also adoptthe comparableprofit methodsimilar to theUnited States.

Yes

No

No specificcases

No

Not common

No

No

No

May beused inaudit targetselection,but unsurewhethersecret compara-bles may be used indeterminingadjustment.

Possible

General tax penalties only (up to 100% of taxadjustment)

Compulsory Secondary Tax on Companies (STC) of 12.5% on adjusted amount. Up to 200% penaltyif nondisclosure or default in rendering a taxreturn. Additionally, a fine or up to 24 months’imprisonment if convicted of a failure to submitdocumentation with tax return.

1. Up to 20%–30% of additional tax liability andinterest thereon

2. KRW 30 million if a taxpayer fails to comply with tax authority’s request for submission oftransfer pricing documentation.

It may be argued that no penalties should apply iftransfer pricing policy has been observed withminimum diligence.

General tax penalties only (2%–50% of tax in default)

General tax penalties only (20% or 40% of taxadjustment, depending on the circumstances)

General tax penalties only; however, penaltiesunlikely

If the transfer pricing audit results in incomeassessments, a penalty up to 200% of the under-paid tax amount (where the enterprises have timely filed tax returns) will be imposed under certain situations involving significant adjustmentsand failure to provide documentation.

General tax surcharge (1.5% per month up to 100% of additional tax liability) plus penalties up to 100% of tax adjustment

n/a

Within deadline agreed with the tax author-ity (minimum 15 days after request)

With annual income tax return

Upon specific request of tax authority(SARS)

Three transfer pricing documents to be sub-mitted in filing annual tax return / informa-tion fully supporting arm’s-length nature oftransfer pricing (i.e., transfer pricing stud-ies) three (3) months after fiscal year-end.

Within 60 days of request (one-time 60-dayextension is allowed upon the application)

n/a

No less than 10 days. An extension of this10-day period can be requested.

n/a

n/a

n/a

n/a

n/a

Upon request in case of audit or competentauthority procedures

Five (5) months after a fiscal year-end

One (1) month after request. Can beextended for an additional month.

n/a

n/a

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

15 Global Transfer Pricing Review

Snapshot of Global Transfer Pricing Compliance RequirementsBased on a 2005 Survey of KPMG Member Firm Transfer Pricing Practices

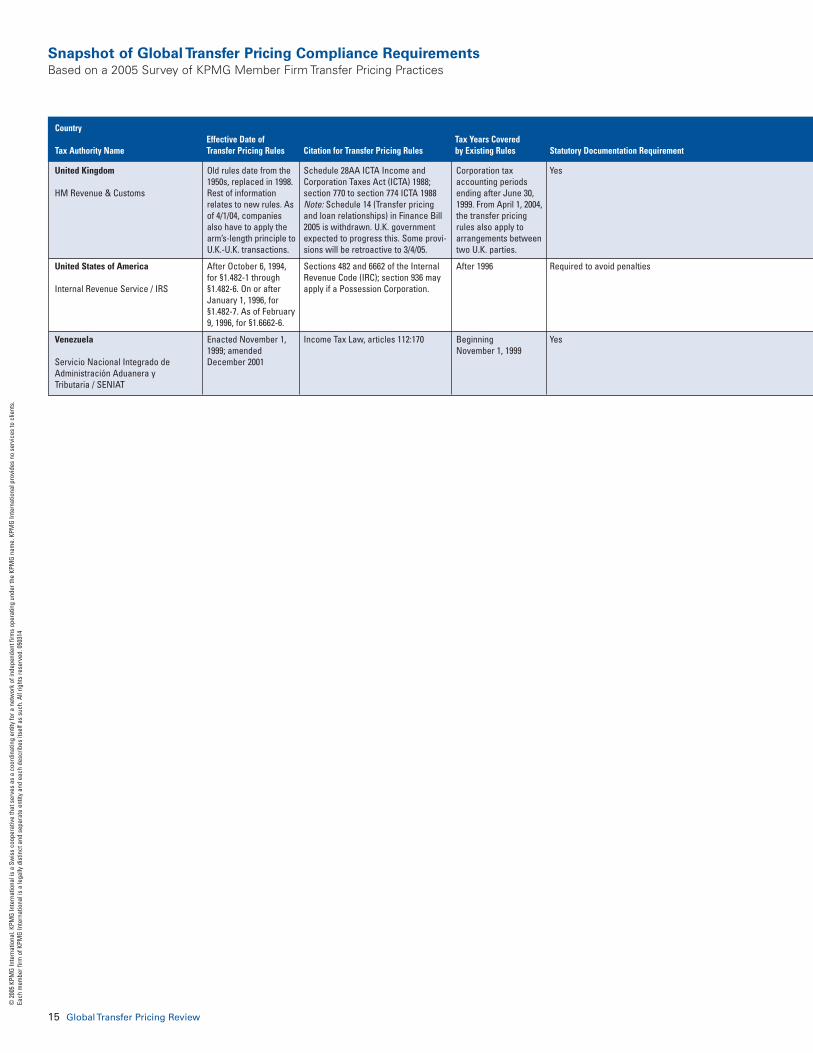

United Kingdom

HM Revenue & Customs

United States of America

Internal Revenue Service / IRS

Venezuela

Servicio Nacional Integrado de Administración Aduanera y Tributaria / SENIAT

Old rules date from the1950s, replaced in 1998.Rest of informationrelates to new rules. Asof 4/1/04, companiesalso have to apply thearm’s-length principle toU.K.-U.K. transactions.

After October 6, 1994,for §1.482-1 through§1.482-6. On or afterJanuary 1, 1996, for§1.482-7. As of February9, 1996, for §1.6662-6.

Enacted November 1,1999; amendedDecember 2001

Schedule 28AA ICTA Income andCorporation Taxes Act (ICTA) 1988;section 770 to section 774 ICTA 1988Note: Schedule 14 (Transfer pricingand loan relationships) in Finance Bill2005 is withdrawn. U.K. governmentexpected to progress this. Some provi-sions will be retroactive to 3/4/05.

Sections 482 and 6662 of the InternalRevenue Code (IRC); section 936 mayapply if a Possession Corporation.

Income Tax Law, articles 112:170

Corporation taxaccounting periodsending after June 30,1999. From April 1, 2004,the transfer pricingrules also apply toarrangements betweentwo U.K. parties.

After 1996

Beginning November 1, 1999

Yes

Required to avoid penalties

Yes

Country Effective Date of Tax Years Covered

Tax Authority Name Transfer Pricing Rules Citation for Transfer Pricing Rules by Existing Rules Statutory Documentation Requirement

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

Global Transfer Pricing Review 16

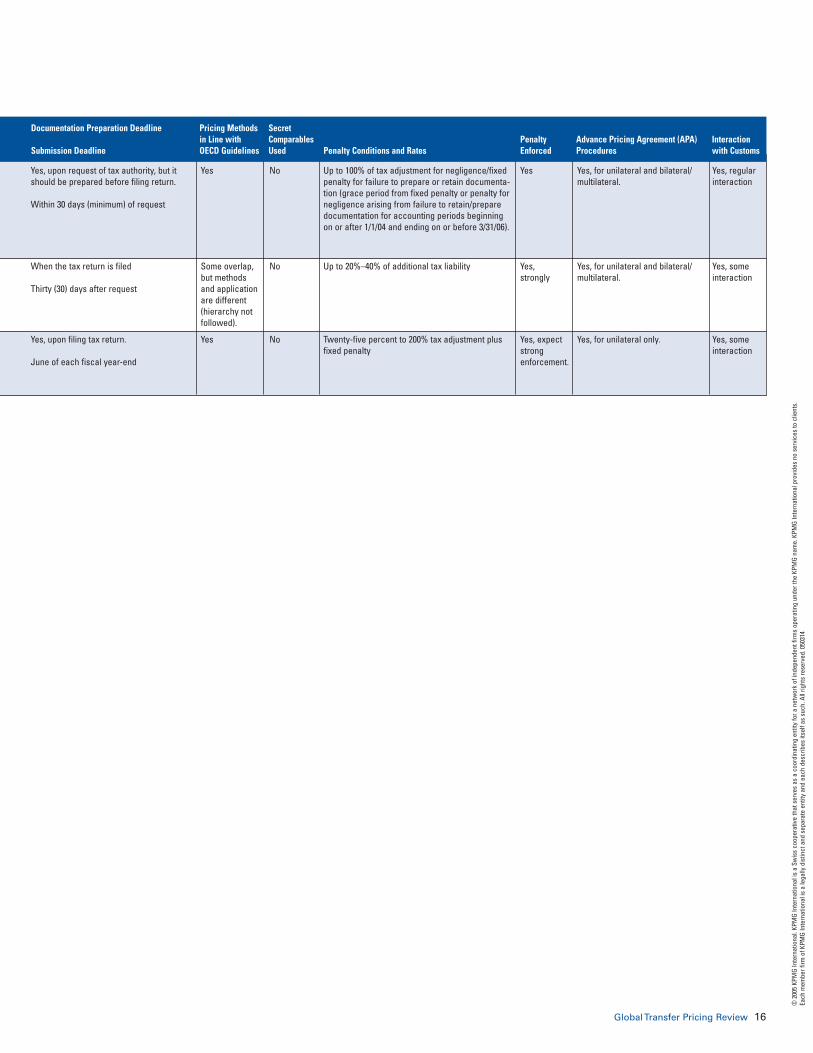

Yes

Yes, strongly

Yes, expectstrongenforcement.

Yes, for unilateral and bilateral/ multilateral.

Yes, for unilateral and bilateral/ multilateral.

Yes, for unilateral only.

Yes, regularinteraction

Yes, someinteraction

Yes, someinteraction

Yes

Some overlap,but methodsand applicationare different (hierarchy notfollowed).

Yes

No

No

No

Up to 100% of tax adjustment for negligence/fixedpenalty for failure to prepare or retain documenta-tion (grace period from fixed penalty or penalty fornegligence arising from failure to retain/preparedocumentation for accounting periods beginningon or after 1/1/04 and ending on or before 3/31/06).

Up to 20%–40% of additional tax liability

Twenty-five percent to 200% tax adjustment plusfixed penalty

Yes, upon request of tax authority, but itshould be prepared before filing return.

Within 30 days (minimum) of request

When the tax return is filed

Thirty (30) days after request

Yes, upon filing tax return.

June of each fiscal year-end

Documentation Preparation Deadline Pricing Methods Secretin Line with Comparables Penalty Advance Pricing Agreement (APA) Interaction

Submission Deadline OECD Guidelines Used Penalty Conditions and Rates Enforced Procedures with Customs

© 2

005

KPM

G In

tern

atio

nal.

KPM

G In

tern

atio

nal i

s a

Swis

s co

oper

ativ

e th

at s

erve

s as

a c

oord

inat

ing

entit

y fo

r a n

etw

ork

of in

depe

nden

t firm

s op

erat

ing

unde

r the

KPM

G na

me.

KPM

G In

tern

atio

nal p

rovi

des

no s

ervi

ces

to c

lient

s.Ea

ch m

embe

r firm

of K

PMG

Inte

rnat

iona

l is

a le

gally

dis

tinct

and

sep

arat

e en

tity

and

each

des

crib

es it

self

as s

uch.

All

right

s re

serv

ed. 0

5031

4

For more information about KPMG’s Global Transfer Pricing Review or theGlobal Transfer Pricing Services practice, contact your local KPMG adviser or e-mail us at [email protected].

The information contained herein is of a general nature and is not intended to address the circumstances of any particu-lar individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee thatsuch information is accurate as of the date it is received or that it will continue to be accurate in the future. No oneshould act upon such information without appropriate professional advice after a thorough examination of the particularsituation.

KPMG International is a Swiss cooperative that serves as a coordinating entity for a network of independent firms oper-ating under the KPMG name. KPMG International provides no audit or other client services. Such services are providedsolely by member firms of KPMG International (including sublicensees and subsidiaries) in their respective geographicareas. KPMG International and its member firms are legally distinct and separate entities. They are not and nothing con-tained herein shall be construed to place these entities in the relationship of parents, subsidiaries, agents, partners, orjoint venturers. No member firm has any authority (actual, apparent, implied, or otherwise) to obligate or bind KPMGInternational or any other member firm, nor does KPMG International have any such authority to obligate or bind anymember firm, in any manner whatsoever.

KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

© 2005 KPMG International. KPMG International is a Swiss cooperative that serves as a coordinating entity for a networkof independent firms operating under the KPMG name. KPMG International provides no services to clients. Each memberfirm of KPMG International is a legally distinct and separate entity and each describes itself as such. All rights reserved.050314