39

Globalization and South Asia: The Role of Foreign Direct Investment in Economic Development Dushni Weerakoon Research Fellow Institute of Policy Studies of Sri Lanka

| Date post: | 10-May-2018 |

| Category: |

Documents |

| Upload: | nguyencong |

| View: | 219 times |

| Download: | 0 times |

Globalization and South Asia: The Role of Foreign Direct Investment in Economic Development

Dushni Weerakoon Research Fellow

Institute of Policy Studies of Sri Lanka

Globalization and Foreign Direct Investment: The South Asian Experience

Globalization has seen significant developments in the world economy, creating greater

cohesion in international trade and finance and rapidly accelerating the integration of

developing countries into the global economy. However, these trends have not in any

sense been universally positive. For several reasons, the poorer economies have not

always seen benefits, and some of the richer developing countries have had a sharp

reminder of the potential adverse effects in the wake of the financial crisis in Southeast

Asia and more recent economic upheaval in Latin America.

South Asia as region was a relatively late comer to embrace ‘globalization’. South Asian

countries, that had very open economies in the immediate post-independence period in

the 1940s, had become some of the most highly protectionist in the world by the 1970s.

While this began to change gradually in the late 1970s, it was only in the 1990s that most

South Asian economies initiated substantive reform efforts involving both trade and

investment liberalization. Unilateral liberalization efforts were complemented by

multilateral efforts under the World Trade Organization (WTO) as well as regional trade

integration initiatives under the South Asian Association for Regional Cooperation

(SAARC).1

The major thrust of the liberalization effort in South Asia, and the most obvious

integration with the global economy, has been in the area of trade. While liberalization of

financial flows has taken place to some extent, most South Asian economies still retain

restrictions on the free flow of capital. Nevertheless, there is growing literature on the

1

nexus between trade and investment. Both theory and evidence suggest that measures that

reduce trade costs may provide an important stimulus not only to trade, but also to

foreign direct investment (FDI).2 Also, specific regional integration initiatives can

influence the level and pattern of FDI flows between member countries, as well as,

between member countries and outsiders. Economic integration can also affect the

absolute and relative growth rates in countries and thereby influence FDI that responds to

potential growth prospects of a region.

While it is increasingly recognized that trade and investment liberalization complement

each other, there is also concern about the economic role of FDI in developing countries.

This paper reports on an initial exploration of issues related to the role of FDI,

documenting the nature of intra-South Asian trade and investment flows, and presenting

the results of some preliminary investigations of the emerging trade and investment

linkages within South Asia. Section 2 will offer a brief review of the theory on linkages

between trade liberalization and investment flows. Section 3 will assess South Asia’s

increasing integration in the global economy and its attempts at regional economic

integration. Section 4 will present a more detailed examination of South Asia’s

experience with FDI, the sectoral distribution of such FDI and the role of regional

integration in promoting FDI in between South Asian countries. Section 5 will offer an

assessment of the (albeit limited) impact of FDI in South Asian economies, while section

6 concludes.

*********

2

Traditional models of trade in ‘goods’, assumed that factors of production such as labor

and capital were not internationally traded - i.e. not internationally ‘mobile’. In reality of

course factors are internationally mobile and have played a key role in shaping the global

economy. In recent years, with increasing liberalization of global capital movements (that

have facilitated a massive surge of global flows of both foreign direct and portfolio

investment), and in some instances, also of labor movements (as in the European Union),

there has been renewed interest in the theoretical and empirical analysis of the causes and

consequences of international factor mobility.

Early theoretical analyses of international factor mobility had two major strands. First,

trade theorists explored the implications of incorporating intermediate goods, and

international factor mobility in response to international factor price differences, in

standard trade models. Second, focussing on foreign direct investments undertaken by

firms, industrial organization theorists analysed the location choices of multinational

enterprises. This approach was pioneered by John Dunning (1977), who suggested that

firms undertake FDI when three factors are present, and the resulting advantages are

sufficient to offset the natural disadvantages of having to operate in a foreign country.

These are known as the ‘ownership, location and internalization’ (OLI) advantages. A

firm must have some product or technology that enables it to enjoy some market power in

a foreign market (‘ownership advantage’), the firm must see some advantage in

producing in the foreign location rather than at home (‘location advantage’), and there

must be some reason for it to want to exploit the ownership advantage internally, rather

than use a market based mechanism to gain payments for it (such as license or sell its

3

product or technology in the market for a fee). More recently, the blending of trade

theory and industrial organization in models that often explicitly incorporate scale

economies (‘New Trade Theory’) has stimulated the development of a number of

analytical models of the linkages between foreign trade and foreign investment (for a

review, see Markusen, 2000).

Differences in relative factor endowments - assumed to be exogenously given - are

central to explanations of international trade in models such as the Heckscher-Ohlin

model. One of the most celebrated ‘theorems’ associated with the Heckscher-Ohlin

model has been the ‘Factor Price Equalisation Theorem’, according to which sufficiently

similar economies will experience factor price equalization, even without free trade in

factors. In other words, trade in goods can ‘substitute’ for international factor movements

or trade in factors. By implication, greater international factor mobility can reduce

international trade, while trade liberalization, by encouraging greater trade in goods can

reduce incentives to trade in factors, including foreign investment flows. On the other

hand, other models, such as models that incorporate vertical inter-firm (backward or

forward) linkages, show that trade in goods complement trade in factors. If this were the

case, greater international factor mobility can enhance trade. Hence trade (foreign

investment) policy liberalization will have a positive effect on foreign investment (trade).

Considering the case of foreign direct investment and trade from the viewpoint of a

firm’s location choices, whether FDI and trade are complements or substitutes depends

on whether FDI is ‘horizontal’ or ‘vertical’. Horizontal FDI takes place when a

4

multinational enterprise (MNE) produces the same goods and services in multiple

countries, in order to avoid paying the ‘trade costs’ of exporting goods from one country

to another, but wishes to exploit its firm-specific advantages in production. With trade

liberalization, trade costs will come down, and the incentive to produce in multiple

country locations will diminish, particularly if there are significant economies of scale. In

this case FDI and trade are substitutes (see Markusen, 1984).3 Vertical FDI takes place

when a firm geographically fragments production by stages, in order to take advantage of

location-specific advantages such as lower factor prices in other countries. For example,

FDI and trade are complements if a MNE relocates part of its production chain, e.g. its

labor intensive assembly plant, to a low-wage country, and exports headquarter services

such as management skills, and intermediate inputs to that country, and then re-exports

final goods (Helpman, 1984). Imports of the ‘home’ country increase as it imports

products made by the foreign subsidiary, while its exports increase because the foreign

subsidiary requires capital and intermediate goods from home.

The theories of horizontal and vertical FDI developed side by side. Markusen et al (1996)

presented a unified theoretical framework incorporating both vertical and horizontal

FDI.4 In this framework, the type of FDI that emerge as a result of trade and investment

liberalization depends on various country characteristics. For example, if countries differ

significantly in relative factor endowments and, trade costs are low to moderate, then

vertical FDI dominates. On the other hand, when countries are similar in size and relative

endowments, and trade costs are moderate to high then horizontal FDI dominates. If a

country is small but skilled labor abundant, then vertical FDI is likely, and investment

5

liberalization can reverse the direction of trade because the country substitutes export of

(skilled labor intensive) services for the export of a good. The empirical literature on

whether FDI and trade are substitutes or complements has produced mixed results.5 This

is not surprising given the diverse motives that underlie international investment

decisions.

Though formal models that analyze the impact of RIAs on FDI, and on trade/investment

links are of relatively recent vintage and, in comparison with the case of trade, are in their

infancy, a considerable empirical literature has developed, analyzing in particular the

impact of integration initiatives in EU, and North America (NAFTA).6 Regional

integration typically reduces barriers to trade in goods as well as investment among

members; sometimes, as in the case of EU, it also reduces barriers to labor mobility. The

impact of regional integration arrangements (RIAs) on trade differ from those associated

with across the board reductions in barriers to trade, and have been analyzed in a large

literature that has followed the seminal work of Viner (1950).7 Available theory provides

no unambiguous predictions about the impact of RIAs, but likely outcomes associated

with a number of scenarios have been discussed.

RIAs can change the level and pattern of FDI, and thereby affect trade in ways that are

not fully captured in standard trade theoretic analyses of customs unions. Trade and

investment liberalization will change the location specific and firm-specific advantages.

RIAs, for example, can encourage geographical concentration: MNEs can restructure

their production bases to take advantage of reduced trade costs while exploiting scale

6

economies and agglomeration advantages. This may lead to FDI outflows from countries

that had earlier attracted ‘tariff hopping’ foreign firms to service protected domestic

markets because they can now be competitively supplied from production bases

elsewhere. On the other hand, better access to a larger market may attract FDI (from

within the region as well as from outside) to countries that have a strong locational

advantage. Such locational advantages may arise from availability of cheaper resources,

superior infrastructure, political stability, a more favorable policy regime, and a host of

other factors. Where firms have vertical linkages with other firms (as intermediate goods

suppliers or purchasers), reduced trade costs can lower the incentive to locate close to

these other firms; hence firm location may be more responsive to comparative factor

costs and advantages of being in similar industry clusters.8 Ethier (1998) has shown that

membership in RIAs can provide small but crucial competitive advantages to countries

that can help them attract large FDI inflows. Preferential treatment for RIA members can

generate not only the well known ‘trade creation’ and ‘trade diversion’ effects, but also

‘investment creation’ and ‘investment diversion’ effects. Economic integration can also

affect the absolute and relative growth rates in countries and thereby influence FDI that

responds to potential growth prospects of a region.

*********

In the limited sense of economic integration, globalization has been most manifest

through closer integration in trade in goods and services, movement of capital, and flow

of finances. And although the process of globalization has come to be viewed almost as a

recent phenomenon, it has been a historical process that has advanced and receded. From

7

the mid 19th century to the outbreak of World War 1, there was rapid global integration

through increased trade flows, movement of capital, and migration of people. The inter-

war period witnessed the erection of barriers to restrict free movement of goods and

services with the onset of the Great Depression. Whilst global integration resumed post-

1945, the nature and speed of integration accelerated with rapid advances in technology

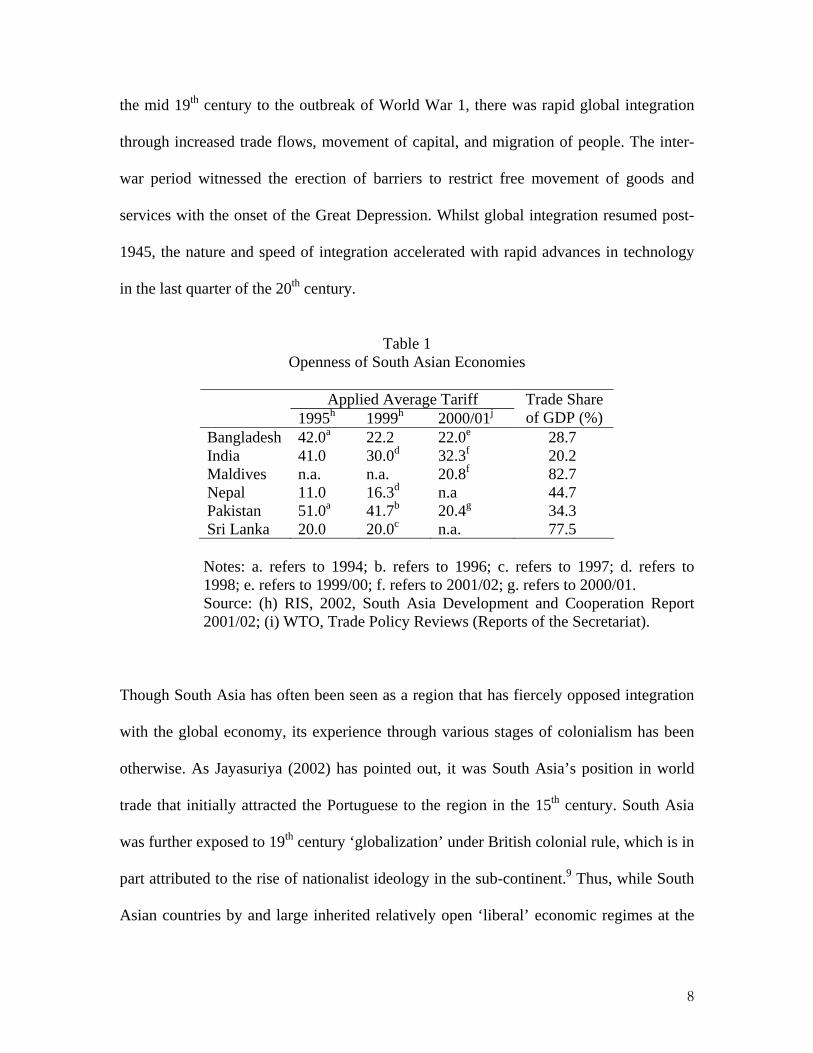

in the last quarter of the 20th century.

Table 1

Openness of South Asian Economies

Applied Average Tariff 1995h 1999h 2000/01j

Trade Share of GDP (%)

Bangladesh 42.0a 22.2 22.0e 28.7 India 41.0 30.0d 32.3f 20.2 Maldives n.a. n.a. 20.8f 82.7 Nepal 11.0 16.3d n.a 44.7 Pakistan 51.0a 41.7b 20.4g 34.3 Sri Lanka 20.0 20.0c n.a. 77.5

Notes: a. refers to 1994; b. refers to 1996; c. refers to 1997; d. refers to 1998; e. refers to 1999/00; f. refers to 2001/02; g. refers to 2000/01. Source: (h) RIS, 2002, South Asia Development and Cooperation Report 2001/02; (i) WTO, Trade Policy Reviews (Reports of the Secretariat).

Though South Asia has often been seen as a region that has fiercely opposed integration

with the global economy, its experience through various stages of colonialism has been

otherwise. As Jayasuriya (2002) has pointed out, it was South Asia’s position in world

trade that initially attracted the Portuguese to the region in the 15th century. South Asia

was further exposed to 19th century ‘globalization’ under British colonial rule, which is in

part attributed to the rise of nationalist ideology in the sub-continent.9 Thus, while South

Asian countries by and large inherited relatively open ‘liberal’ economic regimes at the

8

time of independence, they moved to progressively more dirigiste economic regimes in

the 1950s and 1960s. Development thinking was dominated by an ideological

commitment to import substitution, the outcome of which was a shift towards erection of

barriers to international trade and capital.

As a result, by the 1970s, tariff and, even more importantly, non-tariff barriers (NTBs)

were extremely high, state interventions in economic activity had become pervasive,

attitudes to foreign investments were negative, often hostile, and stringent exchange

controls were in place. But this started to change in the late 1970s, largely as a result of

recurrent balance of payments crises, and relatively slow growth, particularly in

comparison to the high performing East Asian economies. In 1977, Sri Lanka initiated a

process of policy liberalization, and was in turn followed by other countries in the 1980s.

However, this was often a rather hesitant liberalization process, and was very uneven

across countries. It was from the early 1990s, with the start of a major reform process in

India that the region as a whole really started to liberalize. By the end of the decade,

though important policy barriers to trade and foreign investment remained, throughout

the region enormous progress had been made in this direction. However, even by the

mid-1990s, in a global comparison of import protection rates, South Asia remained a

highly protected region (Blackhurst et al., 1996). Thus, despite the policy reform process,

South Asia as a region still lags significantly behind in terms of its ‘openness’ to trade

with the rest of the world (Table 1).

9

Most South Asian economies saw a significant improvement in GDP growth in the 1980s

and 1990s compared to growth rates achieved in the previous two decades. However, the

link between growth and openness of an economy to global competitive forces, and

indirectly therefore to the process of globalization, remains contentious. While some have

drawn a direct causal relationship between superior growth performance during 1980-

2000 and the globalization period in South Asia (Bhalla, 2002), others point to the fact

that the most significant impetus of liberalization in South Asia came only in the 1990s

(Jayasuriya, 2002). The difference in performance in the two decades is quite marginal,

and therefore, does not fully support the argument that improved growth was a direct

result of integration with the global economy.

Table 2

GDP Growth Rates

% Share of Industry in GDP

Average1981-90

Average 1991-95

Average 1996-2000

1990 2000 World 3.4 2.8 3.9 Developing Countries 4.2 6.1 5.1 Developing Asia 6.9 8.8 6.4 Bangladesh 4.3 4.5 5.1 16 25 India 5.9 5.0 6.2 27 27 Nepal 4.8 4.7 4.6 14 20 Pakistan 6.0 5.1 3.3 26 23 Sri Lanka 4.3 5.4 5.0 25 27 Source: IMF, World Economic Outlook, (various issues); WB, World Development Report, (various issues). To ascertain the sustainability of longer-term growth that may be correlated with

liberalization programs requires longer data-periods than available in the context of the

South Asian experience. Sustainability is country-specific, defining the timing,

10

sequencing and pacing of reforms. Thus, the reform process would differ between a

country that had a more ‘liberal’ economic policy regime in comparison to one that was

more ‘closed’ to begin with. Regionally, the reform process in South Asia has been more

gradual and hesitant in comparison, for example, with countries of the Southeast Asian

region. This has been more obvious in South Asia’s reluctance to integrate its financial

markets, and its continuing use of controls on the free flow of capital. In the aftermath of

the East Asian financial crises, most South Asian economies considered their stance to be

vindicated, as the contagion effect of the crisis took hold. The perceived adverse impact

of ‘globalization’ has to some extent reinforced a gradualist approach to further

liberalization of capital flows in the region.

*********

The unilateral trade liberalization process in South Asia also encompassed attempts at

regional trade integration under the framework of SAARC.10 This was partly a response

to the unprecedented resurgence in establishing RIAs on a global scale in the early 1990s.

A common argument put forward is that that the protracted nature of negotiations under

the Uruguay Round (UR) encouraged countries to look to regional partners as an

alternative means of pushing ahead with a reform agenda. The United States in particular

– long opposed to regionalism – initiated discussions on a North American Free Trade

Agreement (NAFTA) in the face of seeming intransigence on the part of the European

Community (EU) to arrive at an agreement on agriculture under the UR. However, even

with the successful conclusion of the UR in 1993, interest in regionalism did not wane. In

11

fact, the enthusiasm for expanding and deepening levels of integration has grown in most

regional groupings. This appears to suggest that the ‘second wave’ of regionalism has

been driven by compulsions of globalization. With heightened global competition, access

to enlarged markets and sources of capital become vital elements for economic

development and is a driving factor behind renewed interest in regional integration.

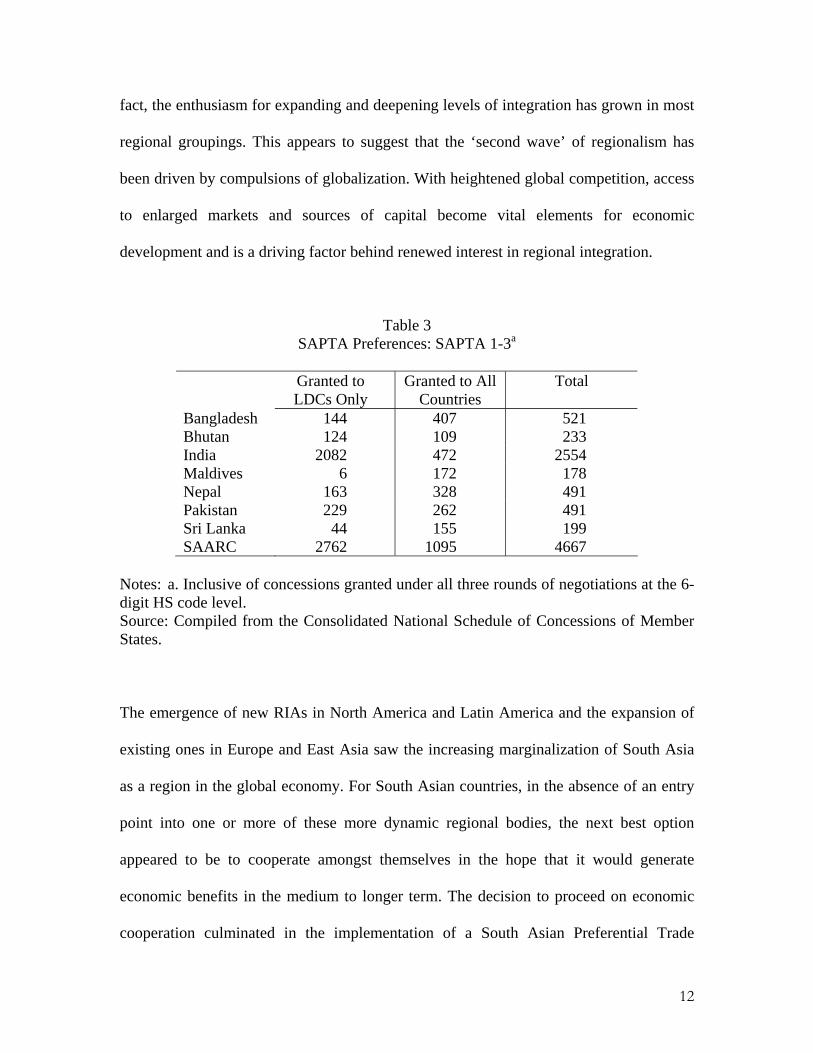

Table 3 SAPTA Preferences: SAPTA 1-3a

Granted to

LDCs Only Granted to All

Countries Total

Bangladesh 144 407 521 Bhutan 124 109 233 India 2082 472 2554 Maldives 6 172 178 Nepal 163 328 491 Pakistan 229 262 491 Sri Lanka 44 155 199 SAARC 2762 1095 4667

Notes: a. Inclusive of concessions granted under all three rounds of negotiations at the 6-digit HS code level. Source: Compiled from the Consolidated National Schedule of Concessions of Member States.

The emergence of new RIAs in North America and Latin America and the expansion of

existing ones in Europe and East Asia saw the increasing marginalization of South Asia

as a region in the global economy. For South Asian countries, in the absence of an entry

point into one or more of these more dynamic regional bodies, the next best option

appeared to be to cooperate amongst themselves in the hope that it would generate

economic benefits in the medium to longer term. The decision to proceed on economic

cooperation culminated in the implementation of a South Asian Preferential Trade

12

Agreement (SAPTA) in December 1995. In 1996, member states agreed in principle to

go a step further and attempt to enact a South Asian Free Trade Agreement (SAFTA).

While the timeframe for the establishment of SAFTA has suffered setbacks with the ebb

and flow of political tension in the region, the target date is likely to be 2008 after the

expected ratification of the Treaty in 2004.

Trade liberalization under the SAPTA process has so far encompassed three rounds of

negotiations. The first round of concessions came into effect in December 1995 where

tariff concessions were exchanged on a total of 226 products under the HS Code system

on a product-by-product basis.11 The second round also adopted the same negotiating

method and was completed in November 1996 with the exchange of concessions on

additional 1900 products. The third round of negotiations was completed in November

1998, combining both a product-by-product and chapter wise approach to include further

concessions on nearly 2500 tariff lines at 6-digit level of aggregation. With the

conclusion of the third round, nearly 4700 tariff lines out of a total of 6000 have been

covered by preferential access (Table 3). India has offered the largest number of

concessions followed by Bangladesh, Pakistan and Nepal. The LDC member states

within SAARC have also been offered a larger share of such concessions vis-à-vis the

non-LDC states.12

SAPTA to date has had no significant impact in changing the existing trade patterns in

South Asia (Table 4). Intra-SAARC trade remains a tiny fraction of total trade of the

region, being constrained not only by political and policy factors, but also by underlying

13

similarity of the economies that limits comparative advantage driven trade. SAPTA has

had a limited impact for a number of reasons: the product-by-product approach has failed

to produce any significant result as the emphasis was on the number of tariff items

negotiated rather than on the amount of trade liberalized; the negotiated products

included have been largely irrelevant to each others trading interests in the region; the

depth of tariff cuts have been marginal; the rules of origin (ROO) requirements also act

as an inhibiting factor; and, non-tariff barriers have further eroded the effectiveness of

tariff preferences granted (Weerakoon and Wijayasiri, 2002).

Table 4

Intra-SAARC Tradea

Intra-SAARC trade

(US $ mn) World trade of

SAARC countries (US $ mn)

Share of intra-SAARC trade in world trade of SAARC countries (%)

1980 1210 37885 3.2 1985 1054 44041 2.4 1990 1584 65041 2.4 1995 4228 104159 4.1 2000 5884 141978 4.1 2001 6537 139585 4.7

Notes: a. Data for Bhutan not available. Source: IMF, Direction of Trade Statistics, various issues.

The fact that countries share some basic similarities (low income, relatively labor

abundant, comparative advantage in similar commodities, dependence on markets outside

the region for their exports) reduce the potential for comparative advantage driven trade.

The economies are mostly agricultural based with a small industrial sector,

manufacturing only a narrow range of goods (with the exception of India). While trade

complementarities in other regions have grown on the basis of manufactured goods, this

14

has not taken place in South Asia due to the small size of the manufacturing sector and

the limited range of goods produced. The low volume of intra-regional trade that is taking

place is based largely on agricultural products, which are produced in some countries and

not in others. Therefore, although SAARC countries have diversified their exports, they

are still geared to markets outside the region, where they compete with one another’s

products.13 Low growth and demand in the region itself, abetted by historical trade links

with the developed countries have resulted in extra-regional trade patterns. The low per

capita income level also constrains potential for intra-industry trade, generally associated

with higher income countries.

It should be noted here that regional cooperation initiatives providing preferential

treatment to members has been largely confined to trade, and have not extended to

investment. Increasingly, however, trade flows have become corollary to investment

flows and there is evidence to suggest that the potential for expanding intra-SAARC

economic links, in both trade and investment, is not entirely absent.14 There are important

structural changes in intra-regional trade that may be important indicators of future

trends. Textile, and machinery and equipment have become increasingly more important

in intra-regional trade and a larger proportion of exports going into the region is now

manufactured products, while in the past, it was primary products (Jayasuriya and

Weerakoon, 2001). This shift into manufactured product trade, associated with the higher

level of industrialization of the region, opens up opportunities for scale economies and

intra-industry trade (complemented by investment flows) to play an increasing role.

15

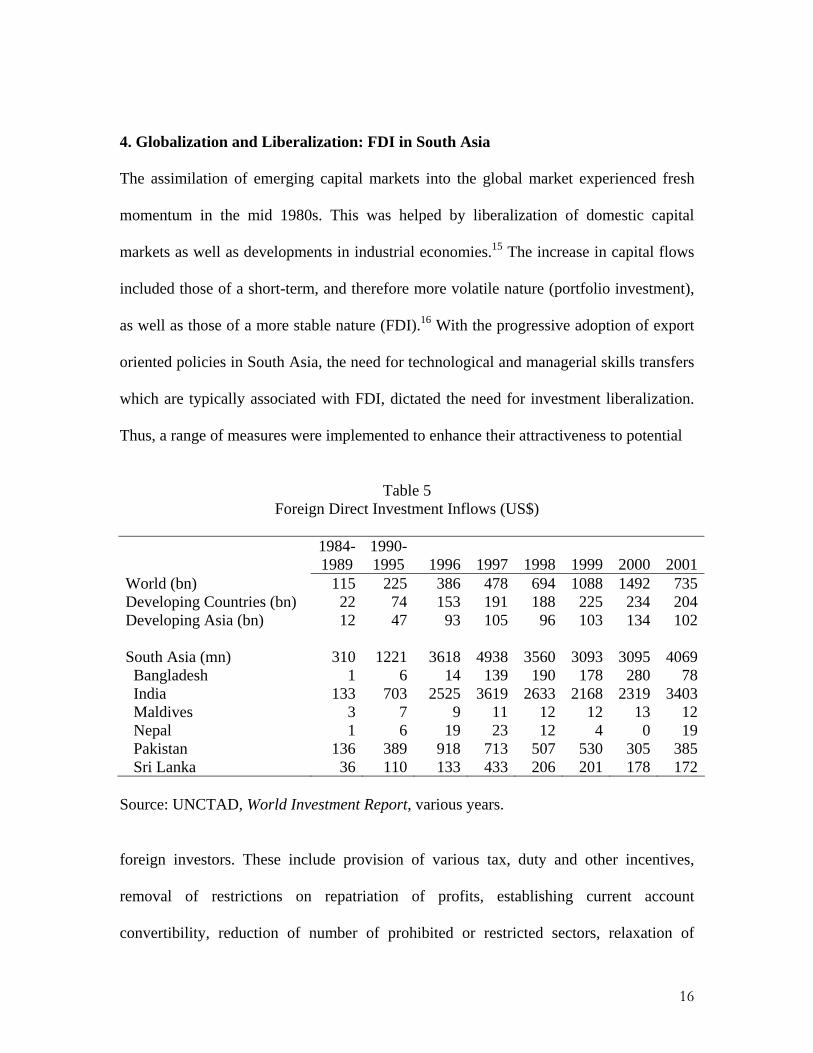

4. Globalization and Liberalization: FDI in South Asia

The assimilation of emerging capital markets into the global market experienced fresh

momentum in the mid 1980s. This was helped by liberalization of domestic capital

markets as well as developments in industrial economies.15 The increase in capital flows

included those of a short-term, and therefore more volatile nature (portfolio investment),

as well as those of a more stable nature (FDI).16 With the progressive adoption of export

oriented policies in South Asia, the need for technological and managerial skills transfers

which are typically associated with FDI, dictated the need for investment liberalization.

Thus, a range of measures were implemented to enhance their attractiveness to potential

Table 5

Foreign Direct Investment Inflows (US$)

1984-1989

1990-1995 1996 1997 1998 1999 2000 2001

World (bn) 115 225 386 478 694 1088 1492 735Developing Countries (bn) 22 74 153 191 188 225 234 204Developing Asia (bn) 12 47 93 105 96 103 134 102 South Asia (mn) 310 1221 3618 4938 3560 3093 3095 4069 Bangladesh 1 6 14 139 190 178 280 78 India 133 703 2525 3619 2633 2168 2319 3403 Maldives 3 7 9 11 12 12 13 12 Nepal 1 6 19 23 12 4 0 19 Pakistan 136 389 918 713 507 530 305 385 Sri Lanka 36 110 133 433 206 201 178 172

Source: UNCTAD, World Investment Report, various years.

foreign investors. These include provision of various tax, duty and other incentives,

removal of restrictions on repatriation of profits, establishing current account

convertibility, reduction of number of prohibited or restricted sectors, relaxation of

16

ownership restrictions, non-discrimination in favor of domestic investors, fast tracking of

FDI approvals, guarantees against nationalization and expropriation, and the setting in

place of internationally acceptable dispute resolution mechanisms.

Trends in FDI inflows reflect the fact that until recently, most countries in South Asia

were not seen by international investors as attractive investment destinations and, in any

case did not welcome foreign investments. Hence, until the 1990s, FDI flows were quite

minimal. FDI flows to South Asia started to pick up in the mid-1990s largely as a result

of progressive liberalization of FDI policies in most of the countries in the region (Table

5), and the adoption of generally more outward oriented policies.17

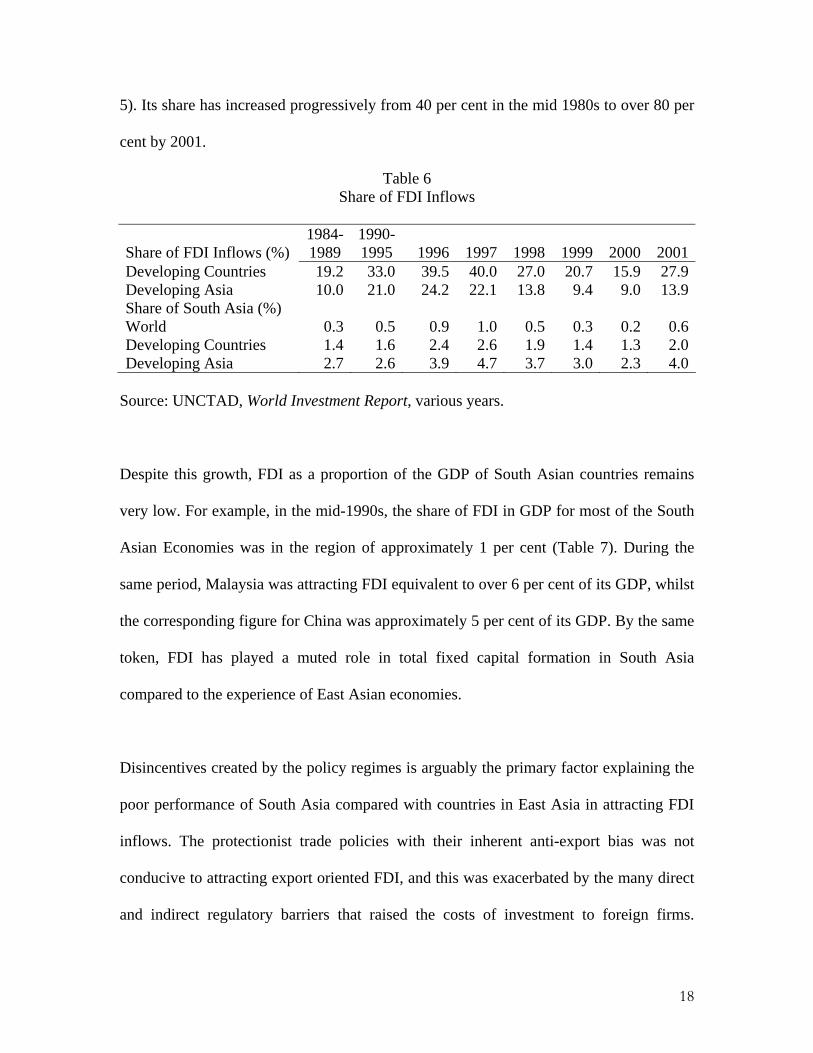

South Asia improved its share in terms of total FDI inflows to the world, developing

countries and Asia over the period 1985-1997 (Table 6). In the aftermath of the East

Asian financial crisis, the proportion of FDI flows to the region has declined, reflecting a

general slowdown in capital flows to the Asian region. In the latter part of the 1990s,

increased cross-border merger and acquisition activity saw a redirection of global FDI

inflows to developed regions of the world. The share of FDI to developing Asian

economies declined from 24.2 per cent in 1996 to 9 per cent in 2000. Notwithstanding

this trend, the magnitude of inflows attracted by the South Asian region remains

relatively meagre. In 2001, it was only US $ 4 billion, a mere 0.6 per cent of global

flows. In contrast, China received more than 47 billion of all global inflows. Within the

South Asian region, India has increasingly accounted for the bulk of FDI inflows (Table

17

5). Its share has increased progressively from 40 per cent in the mid 1980s to over 80 per

cent by 2001.

Table 6 Share of FDI Inflows

Share of FDI Inflows (%) 1984-1989

1990-1995 1996 1997 1998 1999 2000 2001

Developing Countries 19.2 33.0 39.5 40.0 27.0 20.7 15.9 27.9Developing Asia 10.0 21.0 24.2 22.1 13.8 9.4 9.0 13.9Share of South Asia (%) World 0.3 0.5 0.9 1.0 0.5 0.3 0.2 0.6Developing Countries 1.4 1.6 2.4 2.6 1.9 1.4 1.3 2.0Developing Asia 2.7 2.6 3.9 4.7 3.7 3.0 2.3 4.0

Source: UNCTAD, World Investment Report, various years.

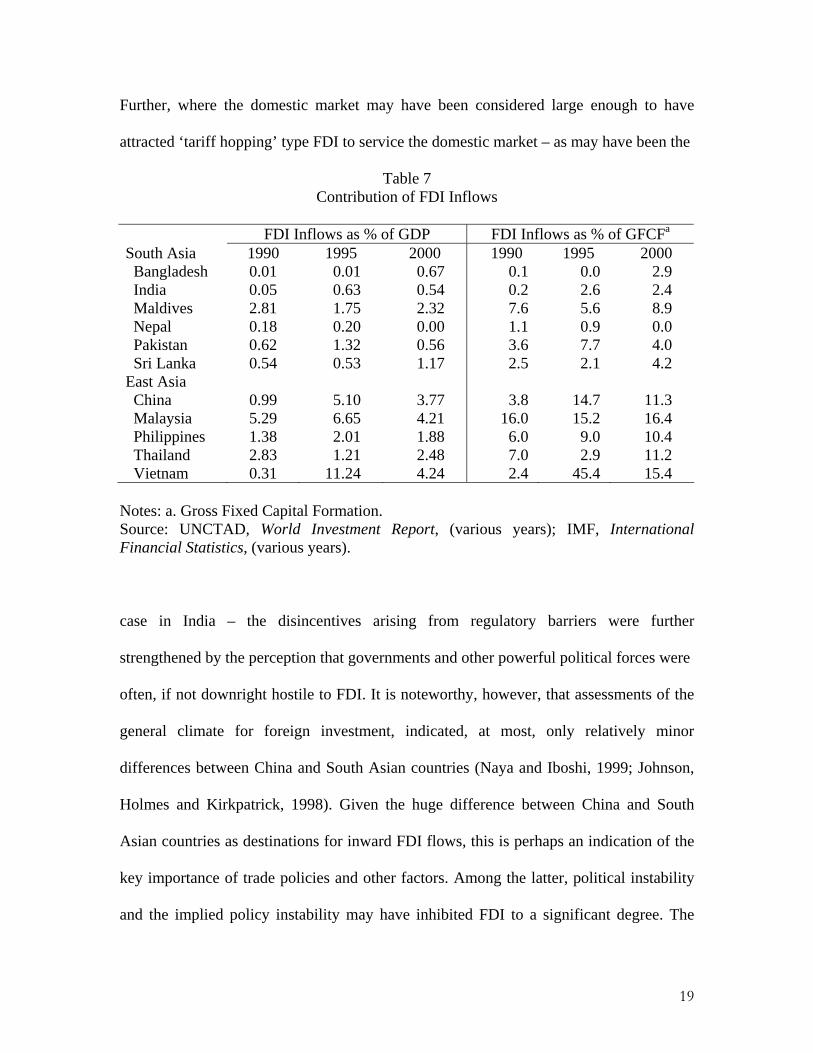

Despite this growth, FDI as a proportion of the GDP of South Asian countries remains

very low. For example, in the mid-1990s, the share of FDI in GDP for most of the South

Asian Economies was in the region of approximately 1 per cent (Table 7). During the

same period, Malaysia was attracting FDI equivalent to over 6 per cent of its GDP, whilst

the corresponding figure for China was approximately 5 per cent of its GDP. By the same

token, FDI has played a muted role in total fixed capital formation in South Asia

compared to the experience of East Asian economies.

Disincentives created by the policy regimes is arguably the primary factor explaining the

poor performance of South Asia compared with countries in East Asia in attracting FDI

inflows. The protectionist trade policies with their inherent anti-export bias was not

conducive to attracting export oriented FDI, and this was exacerbated by the many direct

and indirect regulatory barriers that raised the costs of investment to foreign firms.

18

Further, where the domestic market may have been considered large enough to have

attracted ‘tariff hopping’ type FDI to service the domestic market – as may have been the

Table 7 Contribution of FDI Inflows

FDI Inflows as % of GDP FDI Inflows as % of GFCFa

South Asia 1990 1995 2000 1990 1995 2000 Bangladesh 0.01 0.01 0.67 0.1 0.0 2.9 India 0.05 0.63 0.54 0.2 2.6 2.4 Maldives 2.81 1.75 2.32 7.6 5.6 8.9 Nepal 0.18 0.20 0.00 1.1 0.9 0.0 Pakistan 0.62 1.32 0.56 3.6 7.7 4.0 Sri Lanka 0.54 0.53 1.17 2.5 2.1 4.2 East Asia China 0.99 5.10 3.77 3.8 14.7 11.3 Malaysia 5.29 6.65 4.21 16.0 15.2 16.4 Philippines 1.38 2.01 1.88 6.0 9.0 10.4 Thailand 2.83 1.21 2.48 7.0 2.9 11.2 Vietnam 0.31 11.24 4.24 2.4 45.4 15.4

Notes: a. Gross Fixed Capital Formation. Source: UNCTAD, World Investment Report, (various years); IMF, International Financial Statistics, (various years).

case in India – the disincentives arising from regulatory barriers were further

strengthened by the perception that governments and other powerful political forces were

often, if not downright hostile to FDI. It is noteworthy, however, that assessments of the

general climate for foreign investment, indicated, at most, only relatively minor

differences between China and South Asian countries (Naya and Iboshi, 1999; Johnson,

Holmes and Kirkpatrick, 1998). Given the huge difference between China and South

Asian countries as destinations for inward FDI flows, this is perhaps an indication of the

key importance of trade policies and other factors. Among the latter, political instability

and the implied policy instability may have inhibited FDI to a significant degree. The

19

strong positive response of FDI flows to trade and investment liberalization in Sri Lanka

in the early 1990s that tapered off with the subsequent escalation of political instability is

consistent with this explanation (see the discussion of this issue in Athukorala and

Rajapatirana, 2000). Further, poorly developed infrastructure facilities put South Asia at a

disadvantage relative to the East Asian countries who had already embarked on extensive

expansion and modernization of their infrastructure facilities, while (with the exception

of Sri Lanka) the generally low levels of literacy and investments in human capital may

also have deterred foreign investors.

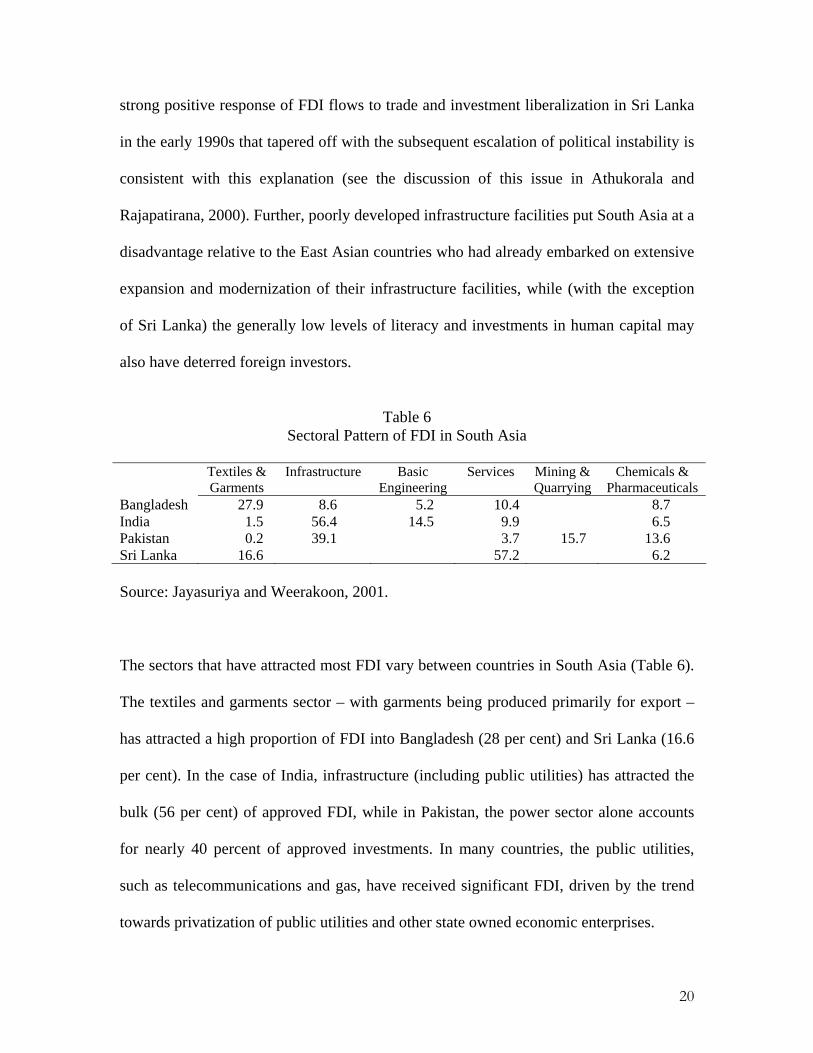

Table 6

Sectoral Pattern of FDI in South Asia Textiles &

Garments Infrastructure Basic

Engineering Services Mining &

Quarrying Chemicals &

Pharmaceuticals Bangladesh 27.9 8.6 5.2 10.4 8.7 India 1.5 56.4 14.5 9.9 6.5 Pakistan 0.2 39.1 3.7 15.7 13.6 Sri Lanka 16.6 57.2 6.2 Source: Jayasuriya and Weerakoon, 2001.

The sectors that have attracted most FDI vary between countries in South Asia (Table 6).

The textiles and garments sector – with garments being produced primarily for export –

has attracted a high proportion of FDI into Bangladesh (28 per cent) and Sri Lanka (16.6

per cent). In the case of India, infrastructure (including public utilities) has attracted the

bulk (56 per cent) of approved FDI, while in Pakistan, the power sector alone accounts

for nearly 40 percent of approved investments. In many countries, the public utilities,

such as telecommunications and gas, have received significant FDI, driven by the trend

towards privatization of public utilities and other state owned economic enterprises.

20

While FDI inflows have been attracted to export oriented industries that exploit

comparative advantage in labor and specific natural resources, South Asia has also

attracted home market oriented industries that supply goods and services that are

constrained primarily by high transport costs. This type of investment is different to the

tariff-hopping FDI that was attracted when markets for potentially importable products

were protected (and were expected to be protected in the longer run). Thus, investment

liberalization has attracted some FDI that competes with home-based firms in market

segments, such as the market in soft drinks and fast food.

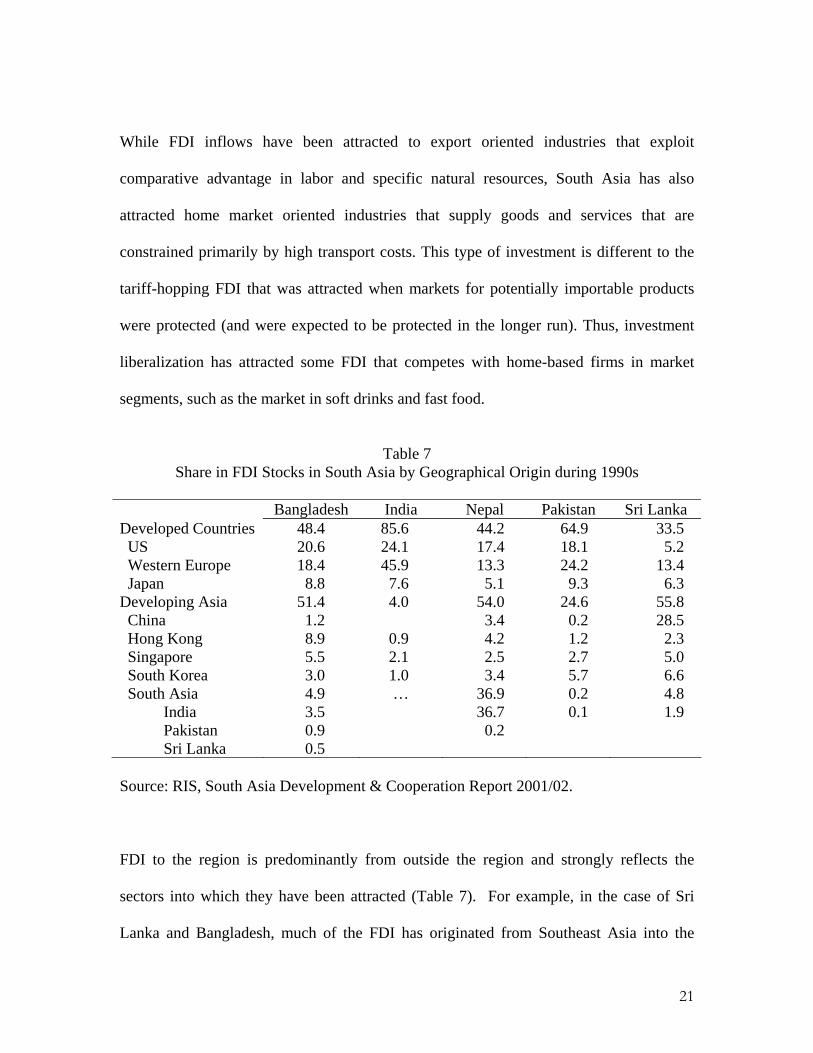

Table 7

Share in FDI Stocks in South Asia by Geographical Origin during 1990s Bangladesh India Nepal Pakistan Sri Lanka Developed Countries 48.4 85.6 44.2 64.9 33.5 US 20.6 24.1 17.4 18.1 5.2 Western Europe 18.4 45.9 13.3 24.2 13.4 Japan 8.8 7.6 5.1 9.3 6.3 Developing Asia 51.4 4.0 54.0 24.6 55.8 China 1.2 3.4 0.2 28.5 Hong Kong 8.9 0.9 4.2 1.2 2.3 Singapore 5.5 2.1 2.5 2.7 5.0 South Korea 3.0 1.0 3.4 5.7 6.6 South Asia 4.9 … 36.9 0.2 4.8 India 3.5 36.7 0.1 1.9 Pakistan 0.9 0.2 Sri Lanka 0.5 Source: RIS, South Asia Development & Cooperation Report 2001/02.

FDI to the region is predominantly from outside the region and strongly reflects the

sectors into which they have been attracted (Table 7). For example, in the case of Sri

Lanka and Bangladesh, much of the FDI has originated from Southeast Asia into the

21

textiles and garments sector to take advantage of quotas allocated under the Multi Fibre

Agreement (MFA). Similarly, countries such as India and Pakistan have seen a larger role

played by FDI from North America and Western Europe in sectors such as infrastructure.

The data is not adequate to determine accurately the degree to which non-infrastructure

related investments outside the textile and garments sectors are export oriented or home-

market oriented, but there are indications that significant amounts of FDI are coming in

to exploit the low labor cost advantages of South Asia, and to utilize them as export

platforms. To the extent that import protection is coming down, the tariff hopping motive

that attracts home market oriented investments weakens. On the other hand, the

increasingly more FDI friendly environment and the perception of improved growth

prospects following more liberal policies may make even some types of home market

oriented investments more attractive, even though with a more liberal trade regime,

import competition will be more intense and servicing the market from abroad may be

less difficult. Where economic prospects have dimmed because of political factors, and

confidence in institutions and broader economic management weakens, as is the case in

Pakistan and Sri Lanka, their attractiveness as investment destinations falls despite the

existence of a favorable policy regime.

While FDI from outside is far more important than intra-regional investments in most

countries (with Nepal, where Indian investments dominate, a conspicuous exception),

there are signs that intra-regional investments are increasing. The major outward FDI

flows are from Indian firms, who have started to expand FDI both within the SAARC

22

region (Bangladesh, Maldives, Nepal and Sri Lanka) and outside, particularly after the

Government of India liberalized its policy governing Indian overseas investments in the

early 1990s. Of course there have been Indian companies with considerable involvement

in joint ventures in neighboring countries, such as Sri Lanka and Nepal even as far back

as 1970s. In addition, there may have been considerable unrecorded outward FDI

undertaken through long established family-linked firms operating in these countries.

Recent estimates appear to suggest that not only are such investments on the rise, but that

firms from other SAARC member countries are also increasingly undertaking FDI within

the region, and investing in a range of sectors and activities (Jayasuriya and Weerakoon,

2001).

Investment from South Asia accounted for nearly 5 per cent of total FDI in Bangladesh of

which Indian invested alone stood at 3.5 per cent (Table 7). Indian investment is found to

be concentrated in services (33 per cent), fabricated metal products, machinery and

transport equipment (34 per cent) – primarily in steel manufacturing - and chemical,

petroleum, rubber and plastic products (18 per cent).18 Services sector investments

included software development, data entry and processing, hospitals and clinics, cold

storage, and hotels. Pakistan has investments in a range of non-metallic mineral products

(glass, cement, marble and stone products), and in food, beverages, and tobacco. Sri

Lankan firms had 11 ventures, mostly in services, including leasing, hospital, hotel and

restaurant, and shipping.

23

In India, despite its huge internal market, investments from the SAARC region have been

quite insignificant, both in relative and absolute terms, accounting for less than 1 per cent

of total foreign investment in India. Bangladesh is the largest investor from the region,

followed by Sri Lanka, Nepal and Maldives. The one SAARC country where regional

investment dominates in total FDI is Nepal where India is the single largest investor. On

the other hand, none of the SAARC countries register as significant investors in Pakistan

though available data indicate that there is some (albeit very limited) flow of FDI from

the regional economies.

In Sri Lanka, India is the largest investor among the SAARC countries, followed by

Pakistan and Maldives. (Sri Lankan firms, in turn, have also invested in Maldives.)

Indian investments are mainly in food, beverage and tobacco products (78 per cent);

chemical, petroleum, rubber and plastic products (13 per cent); and services (7 per cent).

Indian firms are active in the hotel and restaurant sector, as well as in the tea plantation

sector. Much of the investment from Pakistan are in textile, wearing apparel and leather

products category, while two of the three projects funded by firms from Maldives are in

services.

Regional integration can also attract FDI from outside the region to take advantage of

reduced trade costs and access to a larger market. However, there is little evidence of

such flows to South Asia at present. This is partly because the liberalization process is

proceeding in all countries in the region, even though there are still differences in the

levels of protection at present. As such, relatively little FDI can be drawn in to a country

24

with the aim of servicing another market, using opportunities to exploit regional trade

preferences. Moreover, trade integration has so far been very limited in South Asia. Thus,

for countries like Sri Lanka, the opportunity to attract outside FDI to supply, say the

Indian market, is now considerably diminished. (Of course this may still occur if the

partner country has some intrinsic comparative advantage and the foreign firm has some

firm-specific asset that it does not want to market directly.)

With the anticipated move to a free trade area, and with reduced intra-regional trade

costs, scale economies will play an increasingly more important role, and production will

get more concentrated in regional locations to maximize use of location specific assets

(comparative advantage). This means that there may be some substitution of trade for

FDI, as some earlier established foreign subsidiaries contract or close down and that

market is supplied from elsewhere. Thus, we can expect that horizontal FDI will occur

only where proximity to the market is at a premium. Of course horizontal FDI will

continue to occur – and may even be enhanced - in industries such as tourist resorts and

hotels, where the primary service has to be supplied in situ with network benefits being

internalized within the multinational. To the extent that regional links strengthen, firms

from within the region will have a competitive edge in servicing these markets (compared

with outsiders) because of their established positions within the national markets.

*********

25

Globalization has economic, political and cultural impacts, the effects of which, it is

argued, may be particularly powerful in culturally heterogeneous societies divided along

lines of identity such as language, religion, ethnicity, caste, class, etc. (Barker, 1999).

South Asia, with its complex economic and political history, with the world’s largest

concentration of the poor, and a high degree of political volatility, is particularly

vulnerable to charges of inequities of globalization. The rest of this section will look

primarily at available evidence on the economic impact of FDI in South Asia. Given the

limited volume of FDI inflows to the region, the evidence at best remains fairly sketchy.

FDI is argued to contribute to growth in developing countries by creating employment,

increasing exports, and introducing new management and production techniques. There is

certainly country evidence to support some of these arguments. Existing empirical

literature on Sri Lanka’s experience with FDI appears to offer support to the hypothesis

that FDI can be more efficient in raising manufactured export growth (Athukorala, 1995,

1998; Athukorala and Jayasuriya, 2000). And a recent study by Agarwal (2000) has

found evidence that FDI has had a strong complementary effect on investment in South

Asia, leading to additional investment by host country investors. But, by and large, the

evidence remains mixed. Other studies that have assessed whether FDI increases

aggregate investment in developing countries (including India) have argued that FDI

inflows seem to have a negative effect on domestic investment (Fry, 1995; Dhar and Roy,

1996).

26

Agarwal (2000) also finds that FDI inflows have helped South Asian countries to achieve

faster economic growth, beginning in the 1980s and especially over the 1990s.19

Chakraborty and Basu (2002) also find FDI to be positively related to growth in the case

of India. However, the evidence, by and large, remains unclear. Other studies suggest that

the relationship between FDI and growth depends on country specific factors and no

simple conclusions can be drawn (de Mello (1997). Even if a positive correlation is

found, the issue of causality remains unresolved. It could well be that FDI increases

growth, but also that the prospect of higher growth attracts FDI. For the most part, the

evidence that FDI contributes to growth is encouraging rather than compelling (see

Lensink and Morissey, 2001).

While FDI may contribute to growth in developing countries, benefits also may not

always be equally distributed. The distribution of gains from FDI is also linked to some

degree to the sectors in which FDI is directed. FDI inflows to relatively capital intensive

and skill-intensive manufacturing sectors will have a different employment and income

impact than on FDI flowing to labor intensive and unskilled manufacturing. Similarly,

FDI into financial services is also more likely to be associated with high skill intensive

employment and income. Thus, FDI may have an uneven distributional impact within

economies as well as between countries and regions. Recent evidence from five East

Asian economies and five African economies suggest that foreign-owned firms tend to

pay higher wages, but skilled workers tend to benefit more than less-skilled workers

(Velde and Morrissey, 2001, 2002).

27

Systematic evidence on the effects of FDI in South Asian economies is lacking. In the

case of both Sri Lanka and Bangladesh, vertical FDI has been the dominant source to take

advantage of an abundant source of relatively cheap labor. The leading sector which has

attracted FDI has been the textiles and garments sector, employing typically unskilled

female labor. In Sri Lanka, the garments sector has come to dominate manufacturing in

the post-liberalization period, accounting for over 50 per cent of total export earnings for

the country. In addition, it provides employment to over 5 per cent of the total labor force

(and one-third of total manufacturing sector labor employment). Of this, 87 per cent of

employment in the garment sector is female, and they account for 90 per cent of

relatively unskilled machine operator jobs (Kelegama and Epaarachchi, 2002).20 Thus,

the garment industry, driven by inward FDI was a significant source of new employment

opportunities for young female labor. Conversely, liberalization also had a severe impact

on the domestic textile sector with a significant corresponding loss of employment. Prior

to liberalization, the domestic textile industry is estimated to have employed 150,000, but

this figure had fallen to 25,000 by the end of the 1980s (Ministry of Handloom and

Textiles, 1991). Thus, while new employment opportunities were created, this was

accompanied by significant displacement of employment in import competing industries.

There is little technology transfer associated with FDI inflows into the garments sectors,

albeit with the possibility of some degree of managerial skills transfer. FDI inflows into

more skill intensive industries such as the manufacture of automobiles and consumer

goods can bring in new technology. If such foreign firms are more capital intensive,

employment levels may fall in the short-term, but in the longer term technology driven

28

productivity enhancement may confer wider benefits to the host economy. Nevertheless,

evidence from India finds that FDI inflows are found to be labor displacing. The

technology transfer brought in by FDI is found to cause an excess supply of labor, creating

downward pressure on unit labor costs (Chakraborty and Basu, 2002). While the

international evidence on the nature and extent of technology transfer from foreign to

domestic firms is mixed, evidence from India again points to some positive spillovers.21

India has seen a relatively higher share of FDI going into technology intensive sectors

such as basic engineering and chemicals and pharmaceutical sectors than most other

South Asian economies (see Table 6).

If FDI inflows represent additional investment, it should provide employment. However,

increasingly FDI inflows are for mergers and acquisitions, attracted by the trend towards

privatization of public utilities and other state owned economic enterprises. Such FDI

inflows may not necessarily increase employment. In the case of India, for example, there

is evidence to suggest that multinational corporations have been notably active in

acquisitions, accounting for nearly a third of all corporate acquisitions during the period

1991-97 (Basant, 2000). Such FDI inflows can also lead to increasing market

concentration in some sectors.22 Similarly, in Sri Lanka, privatization of state owned

enterprises have seen monopoly status being conferred on multinationals for an agreed

period of time as an additional inducement to attract such investors. For example, a large

multinational (Shell Overseas) was granted a monopoly status for a five year period with

the privatization of Sri Lanka’s state owned gas company. Such deals have often been

driven by the need to attract greater inflows of FDI for domestic fiscal purposes rather

29

than imperatives associated with improving efficiency. Lack of transparency in such

negotiations (for example, as in the case of Enron in India) have perpetuated a degree of

unease and contributed towards instilling a negative perception of multinational driven

FDI in some quarters of South Asian society, reinforcing historical hostility to foreign

investment. Such sentiments in turn have been transferred to the whole concept of

‘globalization’ and its resultant impact on host economies.

Concerns with globalization have been reinforced with developments in the multilateral

agenda on future trade negotiations. With more and more countries adopting liberal

economic policies and integrating with the global economy, South Asian economies too

have to compete more fiercely for foreign investment. As more countries progressively

liberalize their trade regime, in the expectation that more FDI will follow, ‘new issues’

linking trade and FDI flows are being thrust on developing countries. Increasingly,

environmental, health and labor standards are coming on to the multilateral agenda under

the WTO, with the caveat that free trade should involve a ‘level playing field’ by

harmonizing domestic policies across countries in these areas. Harmonized standards are

encouraged on the grounds that FDI will move to countries that maintain low standards

on environment, labor, etc. While there is no defensible evidence to support such

arguments, the linking of labor standards to FDI and trade have compelled some South

Asian economies (for example, the carpet industry in Nepal) to adopt international

guidelines. Similarly, in Sri Lanka, increasingly FDI in the garments industry is also

being linked to the welfare of workers. Often, inspection teams are sent to examine and

report on the working conditions of factory workers prior to the placement of orders.

30

Thus, FDI may also contribute ‘positively’ to improved welfare of labor, as long as such

measures are not used as protectionist tools to restrict market access of developing

country exports.

While there has been a general acceptance of the positive and desirable nature of FDI in

South Asia, pockets of resistance to foreign investment and ‘globalization’ continue to be

heard, spurred by the lack of transparency and perceived corruption in some major

projects involving FDI (such as the case of Enron in India’s power sector). The

transformation of the information-entertainment industry in most South Asian countries

with the infusion of FDI has also generated concern over the ‘westernization’ of cultures

in the region. Nevertheless, it would be difficult to argue convincingly that South Asia –

which remains one of the poorest regions of the world – constrained by inadequate

domestic financial resources, is likely to be better off without participating actively in the

global economy. The issue that confronts the region is how to exploit opportunities of

globalization – in this instance, increased access to FDI – while ensuring that its gains are

equitably distributed.

*********

The relative paucity of FDI inflows to South Asia in the past is not difficult to fathom,

given the inward looking policies and the relatively inhospitable environments for inward

FDI. In recent times, the liberalization process in the region has infused a dynamism to

the region’s economies in several ways. Economies are becoming more open, outward

oriented, and more receptive to foreign investment and trade; at the same time, many

31

business firms are expanding their horizons, and are not only entering into joint ventures

and other partnerships with foreign firms but are also taking the initiative to undertake

FDI in other countries. The degree to which FDI from outside has been attracted to the

region has been primarily affected by the overall liberalization policies – in particular the

degree to which trade liberalization has been accompanied by domestic market reforms,

the liberalization of FDI regulations and the development of a more FDI friendly policy

stance – and the growth dynamics of the individual countries.

Though the extent of FDI links in South Asian economies are still rather limited,

increased inflows (both from outside and within the region) indicate the potential and the

manner in which future developments will occur in a more liberal trading and investment

environment in South Asia. At present, the relatively limited progress with preferential

liberalization within the SAPTA framework obviously limits the extent to which regional

FDI flows will be stimulated. Larger outside FDI flows will require substantially greater

progress with the overall trade and investment regulation process, complementary

domestic market and institutional reforms and expansion and modernization of

infrastructure facilities. Though short term adjustment costs are obviously important, and

must be taken into account in introducing policy changes, it seems also clear that in order

to achieve sustained and high growth, South Asia must open up and exploit growth

opportunities.

Nevertheless, keeping in mind the political volatility of the region, FDI policies should be

geared to those that increase the potential for employment and for wider benefits to the

32

economy from transfer of technology, improved productivity and growth. Domestic firms

should be encouraged to increase efficiency in order to benefit from linkages with and

spillovers from foreign firms. Ensuring a fair distribution of the gains from FDI will be

critical in building mass support, not only for the domestic liberalization agenda but also

for integration with the global economy. It is clear that South Asia cannot afford to step

back from the process of globalization. The challenge will be to ensure that the general

thrust of liberalization fosters more efficient, gainful and sustainable trade-investment

links that contributes to overall growth while ensuring that other social objectives, such

as reducing inequities and levels of poverty, are not undermined.

References Agarwal, P., 2000. Economic Impact of Foreign Direct Investment in South Asia. Indira

Gandhi Institute of Development Research, Mumbai, India, (mimeo). Athreye, S., and S. Kapur, 2001. Private Foreign Investment in India: Pain or Panacea?

World Economy, 24(3). Athukorala, P., 1995. Foreign Investment and Exports: Sri Lanka. World Economy, 18(4). Athukorala, P., 1998. Trade Policy Issues in Asian Development. London: Routledge. Athukorala, P., and S.K. Jayasuriya, 2000. Trade Policy Reforms and Industrial

Adjustment in Sri Lanka. The World Economy, 23(1). Athukorala, P., and S. Rajapatirana, 2000. Liberalization and Industrial Transformation:

Sri Lanka in International Perspective. Oxford and New Delhi: Oxford University Press.

Barker, C., 1999. Television, Globalization and Cultural Identities. Buckingham and Philadelphia: Open University.

Basant, R., 2000. Corporate Response to Economic Reforms. Economic and Political Weekly, 35(10).

Basant, R., and B. Fikkert, 1996. The Effects of R&D, Foreign Technology Purchase, and Domestic and International Spillovers on Productivity in Indian Firms. The Review of Economics and Statistics, 78(2).

Bhalla, S., 2002, Imagine There’s No Country: Poverty, Inequality and Growth in the Era of Globalization. Institute of International Economics, Washington, D.C.

Blackhurst, R., A. Enders, and J.F. Francois, 1996. The Uruguay Round and Market Access: Opportunities and Challenges for Developing Countries. In Martin, W. and L.A. Winters (eds.) The Uruguay Round and the Developing Countries. Cambridge: Cambridge University Press.

33

Blomstrom, M., R. Lipsey and K. Kilchycky, 1988. US and Swedish Direct Investment and Exports. In R. Baldwin (ed.) Trade Policy Issues and Empirical Analysis. Chicago: Chicago University Press.

Caves, R. E., 1996. Multinational Enterprise and Economic Analysis. Cambridge: Cambridge University Press.

Chakraborty, C., and P. Basu, 2002. Foreign Direct Investment and Growth in India: A Cointegration Approach. Applied Economics, 34(9).

De Mello, Jr, L.R., 1997. Foreign Direct Investment in Developing Countries and Growth: A Selective Survey. Journal of Development Studies, 34(1).

Dunning, J. H., 1977. Trade, Location of Economic Activity, and MNE: A Search for an Eclectic Approach. In Ohlin, B., P.O. Hesselborn, and P.M. Wijkman (eds.) The International Allocation of Economic Activity. London: MacMillan.

Eklohm, K., 1998. Headquarter Services and Revealed Factor Abundance. Review of International Economics, 6(545-553).

Ethier. M., 1998. The New Regionalism. The Economic Journal, 108(449). Griffith-Jones, S., M. Montes, and A. Nasution, 1997. A Latin American and Asian

Perspective on Managing Capital Surges, (mimeo). Helpman, E., 1984. A Simple Theory of International Trade with Multinational

Corporations. Journal of Political Economy, 92(451-472). Hine, R. C., 1994. International Economic Integration. In Greenaway, D. and L.A. Winters

(eds.) Surveys in International Trade. Oxford: Blackwell Publishers. IDCJ, 1996. Schemes of Regional Economic Cooperation Aimed at Fostering Economic

Growth in South Asia: The Role of Japan. International Development Centre of Japan, Tokyo.

Jayasuriya, S., 2002. Globalization, Equity and Poverty: The South Asian Experience. A paper presented at the 4th Annual Global Development Conference on “Globalization and Equity”, Cairo, Egypt, January 19-21, 2003.

Jayasuriya, S., and D. Weerakoon, 2001. FDI and Economic Integration in the SAARC Region. In T.N. Srinivasan (ed.) Trade, Finance and Investment in South Asia. New Delhi: Social Sciences Press.

Johnson, B.T., K.R.Holmes and M. Kirkpatrick, 1999. Heritage Foundation/Wall Street Journal 1998 Index of Economic Freedom. The Heritage Foundation and Dow Jones and Co., Washington, D.C. and New York, N.Y.

Kathuria, V., 1998. Foreign Firms and Technology Transfer Spillovers to Indian Manufacturing Firms. INTECH Discussion Paper No. 9804, United Nations University.

Kelegama. S., and R. Epaarachchi, 2002. Productivity, Competitiveness and Job Quality in the Garment Industry in Sri Lanka. In G. Joshi (ed.), Garment Industry in South Asia - Rags or Riches? Competitiveness, Productivity and Job Quality in the post-MFA Environment. New Delhi: International Labor Organization.

Lensink, R., and O. Morissey, 2001. FDI Flows, Volatility and Growth. University of Nottingham: CREDIT Research Paper 01/06.

Lipsey, R.E. and M.Y. Weiss, M. Y., 1981. Foreign Production and Exports in Manufacturing Industries. Review of Economics and Statistics, 63(488-94).

Lipsey, R.E. and M.Y. Weiss, 1984. Foreign Production and Exports of Individual Firms. Review of Economics and Statistics, 66(304-8).

34

Markusen, J.R., 2000. Foreign Direct Investment and Trade. Policy Discussion Paper No: 0019, Centre for International Economic Studies, University of Adelaide.

Markusen, J.R., 1984. Multinationals, Multi-plant Economies, and the Gains from Trade. Journal of International Economics, 16(205-226).

Markusen, J.R., A.J. Venables, D.E. Konan and K.H. Zhang, 1996. A Unified Treatment of Horizontal Direct Investment, Vertical Direct Investment, and the Pattern of Trade in Goods and Services. NBER Working Paper 5696.

Ministry of Handloom and Textiles, 1991. Review of Activities 1989-91. Ministry of Handloom and Textiles, Colombo, Sri Lanka.

Mukherji , I.N., 2000. Indo-Sri Lanka Trade and Investment Linkages with Special Reference to SAPTA and Free Trade Agreement. South Asia Economic Journal, 1(1).

Mukherji, I.N., 1998. India’s Trade and Investment Linkages with Nepal: Some Reflections. South Asian Survey, 5(2).

Naya, S.F., and P.I. Iboshi, 1999. Trade and Investment Policy Matrix and Liberalization Agenda for Asia and the Pacific. In United Nations Economic and Social Committee for Asia and Pacific: Trade and Investment Policy Scenarios and Liberalization Agenda for Asia and the Pacific, United Nations, New York

Ozawa, T., 1992. Cross-investment between Japan and the EC: Income Similarity, Product Variation, and Economies of Scope. In Cantwell, J (ed.) Multinational Investment in Modern Europe: Strategic Interaction in the Integrated Community, Aldershot: Edward Elgar-Publishing.

Pain, N., and K. Wakelin, 1998. Export Performance and the Role of Foreign Direct Investment. Manchester School Supplement, 66(62-88).

Rahman, M., 1998. Harnessing Competitive Strength through Enhancement of Technological Capability: A Study on Export Oriented Apparels Sector of Bangladesh. Bangladesh Institute of Development Studies, Dhaka, (mimeo).

RIS, 2002. South Asia Development and Cooperation Report 2001/02. Research and Information System for the Non-Aligned and Other Developing Countries, New Delhi, India.

Velde, D.W., te and O. Morrissey, 2002. Foreign Direct Investment, Skills and Wage Inequality in East Asia”,

www.odi.org.uk/iedg/FDI_who_gains/FDIWhoGains.htmlVelde, D.W., te and O. Morrissey, 2001. Foreign Ownership and Wages: Evidence from

Five African Countries. CREDIT Discussion Paper 01/19. Weerakoon, D., and J. Wijayasiri, 2002. Regionalism in South Asia: The Relevance of

SAPTA for Sri Lanka. South Asia Economic Journal, 3(1). Weerakoon, D., and J. Wijayasiri, 2001. Regional Economic Cooperation in South Asia:

A Sri Lankan Perspective. International Economic Series No. 6, Institute of Policy Studies, Colombo, Sri Lanka.

Viner, J., 1950. The Customs Union Issue. Carnegie Endowment for International Peace, New York.

1 SAARC was established in 1985 by Bangladesh, Bhutan, India, Nepal, Maldives, Pakistan, and Sri Lanka.

35

2 FDI is conventionally defined as a form of international inter-firm cooperation that involves a significant equity stake in, or effective management control of foreign firms (de Mello, 1997: 4). These differ from ‘portfolio investments’ – purchases by foreigners of bonds, stocks and other financial market instruments - primarily in terms of the degree to which such investments provide the potential for managerial control. 3 See Caves (1996) for a discussion of the factors that influence an MNE’s trade and investment decisions. (‘Trade costs’ include all costs that are incurred in conducting international trade and include transport costs, tariffs, and other transactions costs). 3 See also, Markusen (2000) and Markusen and Venebales (1998). 4 See also, Markusen (2000) and Markusen and Venebales (1998). 5 There are many empirical studies that explore the links between trade and investment (eg. Lipsey and Weiss, 1981 and 1984; Blomström et al., 1988;, Ekholm, 1998; Pain and Wakelin, 1998). 6 See Ethier (1998) for a formal discussion, and also Ozawa (1992). 7 The concepts of ‘trade diversion’ and ‘trade creation’ are associated with the preferential and discriminatory nature of trade liberalization in RIAs, so that trade is encouraged among members, sometimes at the expense of non-members. For a survey, see Hine (1994). 8 See Amiti (1998) for a discussion of these issues. 9 For example, Jayasuriya (2002) argues that opening up the economies to the world economy was viewed as a mechanism for the exploitation of the colonial nations by a growing South Asian nationalist ideology. 10 Although the SAARC Charter included economic cooperation in its agenda, it was only in the late 1980s that explicit attention was paid to formulating a policy framework to initiate the process. 11 This entails an exchange of 'offer' and 'request' lists of goods on a bilateral basis where the results are later multilateralized. 12 Bangladesh, Bhutan, the Maldives and Nepal are considered LDC member states within SAARC. 13 For example, garments form the largest single export of Bangladesh, Sri Lanka and Nepal, and it is a major export category of India, Pakistan and the Maldives. 14 See Mukherji (1998) for a study of trade and investment links between India and Nepal, and Mukherji (2000) for a study of trade and investment linkages between India and Sri Lanka. See also Jayasuriya and Weerakoon (2001) for a more detailed assessment of potential trade-investment nexus in South Asia. 15 The latter include regulatory changes in the US and other financial centers in the late 1980s that resulted in increasing amounts of capital being managed by institutional investors. In addition, the revaluation of the Japanese yen in the mid 1980s saw a surge of outward capital from Japan as well. 16 It is practically impossible to gauge whether capital flows are of a temporary or permanent nature. The distinction is, however, of importance to policy makers in order to identify the potential vulnerability of an economy to reversals and hence be in a better position to take corrective measures. The possibility of volatility and reversibility seem to depend on the type of inflows. Foreign direct investment (FDI) that comes in the form of finance flows is no different from portfolio investment. However, if it comes in the form

36

of import surplus -- that is, in terms of machinery and capital -- it is likely to be of a much more stable nature (Griffith-Jones et al., 1997). 17 There are major problems with the available FDI figures for the SAARC countries. Often the data available is for approvals, but not for realized investments. Annual data are often cumulated with no adjustments for changes in purchasing power. There are sometimes wide discrepancies between national and international data sources, and among national sources themselves. Hence the data given here should be treated with considerable caution. 18 See Jayasuriya and Weerakoon (2001) for details. 19 The impact of FDI inflows on GDP growth was found to be negative prior to 1980. This is argued to be because FDI inflows may have earned excessive profits and led to immiserizing growth when there were severe trade and financial markets distortions in most South Asian economies. 20 It has been estimated that at the end of the 1990s, the garment industry in Bangaldesh provided total employment to approximately 1.5 million, of whom 1.2 million were women (Rahman, 1998). 21 See Basant and Fikker (1996) and Kathuria (1998) quoted in Athreye and Kapur (2001). 22 One of the largest multinationals in India, Hindustan Lever (a subsidiary of Unilever) acquired Tata Oils (its principal rival in oil in India), Brooke Bond Lipton (India’s largest company in food and beverages), Pond’s India (cosmetics), Kwality, and Milkfood (processed foods) in a series of mergers and acquisitions after 1992 (Athreye and Kapur, 2000).

37

Dushni Weerakoon has a BSc in Economics with First Class Honors from the Queen’s University of Belfast, Northern Ireland, UK. Has a Masters and PhD in Economics from the University of Manchester, UK. Currently a Research Fellow of the Institute of Policy Studies of Sri Lanka. Research interests include trade policy and regional integration and macroeconomic policy management.

38