89

| Date post: | 07-Apr-2017 |

| Category: |

Economy & Finance |

| Upload: | usittech |

| View: | 1,332 times |

| Download: | 0 times |

General Meeting #610.13.2015University Securities Investment Teamtexasusit.org

TexasUSIT.org

Agenda• General Announcements• Market Update• Jack Butler

• Portfolio Update• Cliffe Kim

• Lecture: Generating Investment Theses• Dylan James

• Stock Pitch: IPG Photonics (IPGP)• Grant Kjeldsen, Sunny Pamidimukkala, Priyanka Suri,

Collin Hartman, Srija Nalla, Max Huang

10/6/15

TexasUSIT.org

General Announcements

10/6/15

• First TWO meetings are free!• Analyst Groups: CLOSED• Email [email protected] for WSJ log-in

information• UCF Workshop: Options Theory II• Thursday, Oct 1st – CBA 4.328, 7-8pm

TexasUSIT.org

USIT Social! • The Picnic• Saturday, October 17th • 7pm – 9pm • Meet at Littlefield Fountain at 6:30pm• RSVP online!!

10/6/15

TexasUSIT.org

Upgrade Capital

10/6/15

TexasUSIT.org

Upgrade Capital

10/6/15

Market UpdateJack Butler

TexasUSIT.org

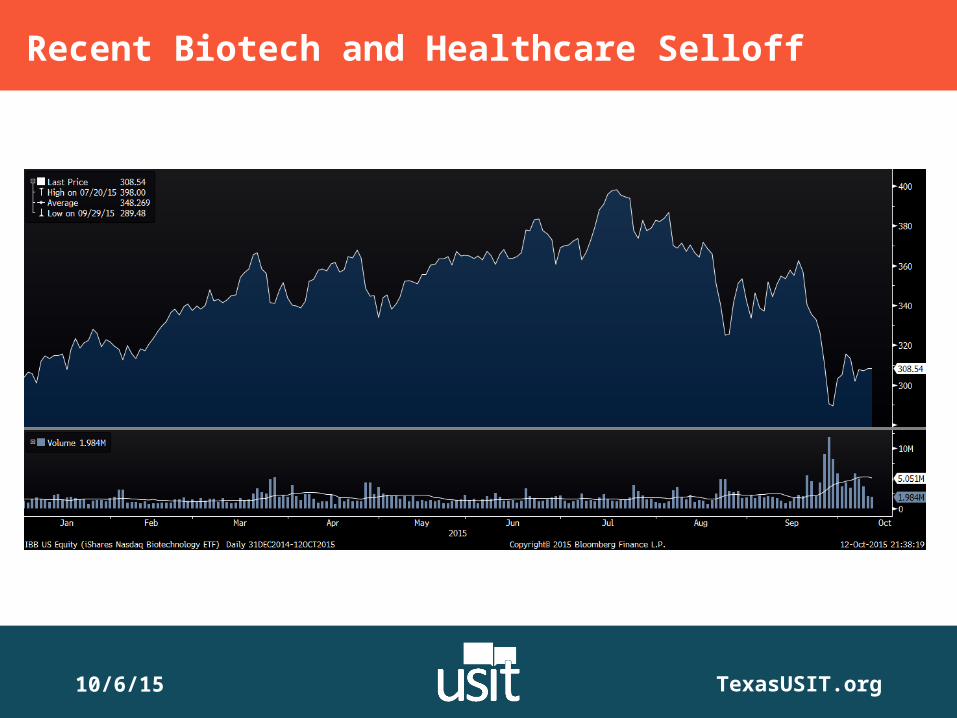

Recent Biotech and Healthcare Selloff

10/6/15

TexasUSIT.org

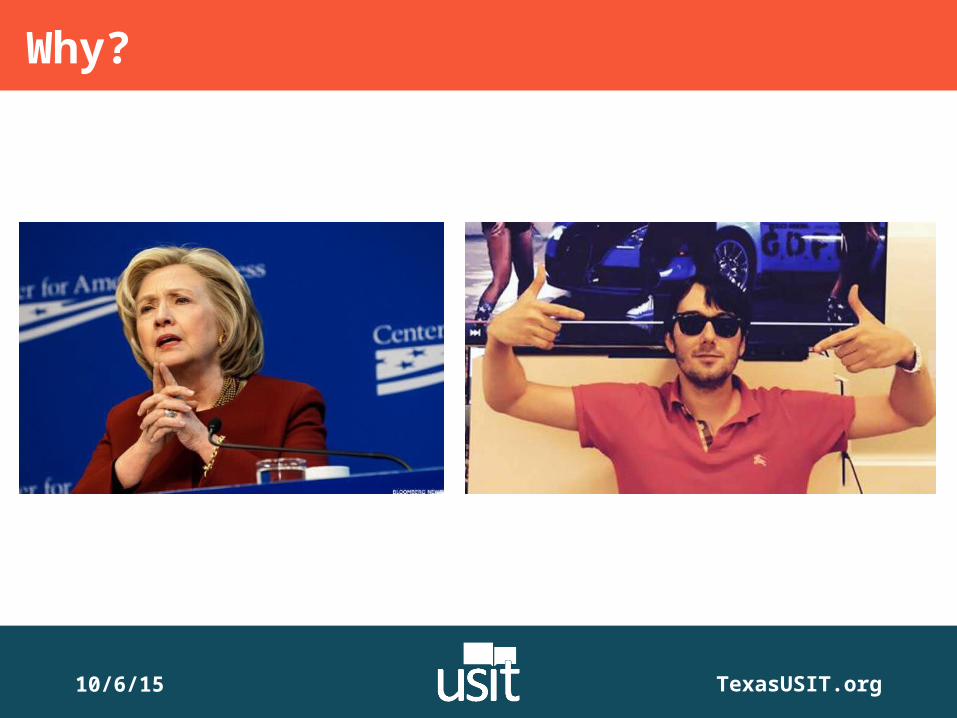

Why?

10/6/15

TexasUSIT.org

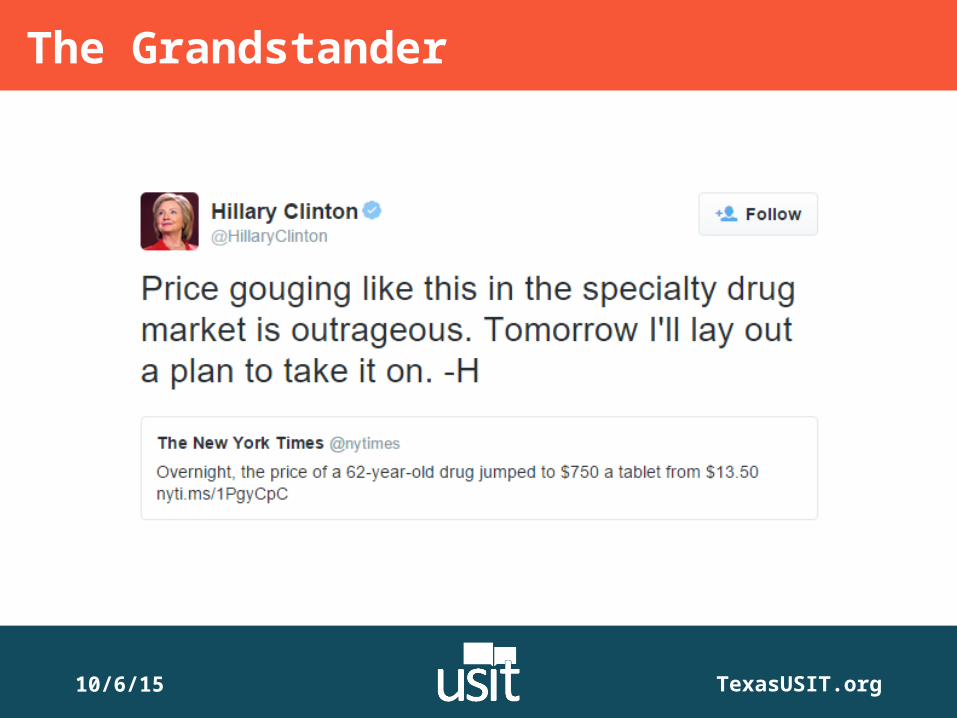

- Hedge fund manager- Owner of Turing Pharmaceuticals- Douche- Bought rights to existing HIV drug- Raised price from $13.50 to $750

Martin Shkreli

- Later said Turing would lower the price

The Compensator

10/6/15

TexasUSIT.org

The Grandstander

10/6/15

TexasUSIT.org

The Biotech Investor

10/6/15

TexasUSIT.org

Buying Opportunity? Too Soon to Tell?

The Value Play

10/6/15

TexasUSIT.org

Alcoa earnings miss: 7 cents per share, vs expected 13 cents

Why?

MORE upside?Falling aluminum prices

In Other News…

10/6/15

TexasUSIT.org

Stock down 23% off three-month highPrice targets lowered

Model X Luxury SUV• Model X price higher

than expected• Slow manufacturing,

fewer deliveries than expected

Tesla Continues to Slide

10/6/15

TexasUSIT.org

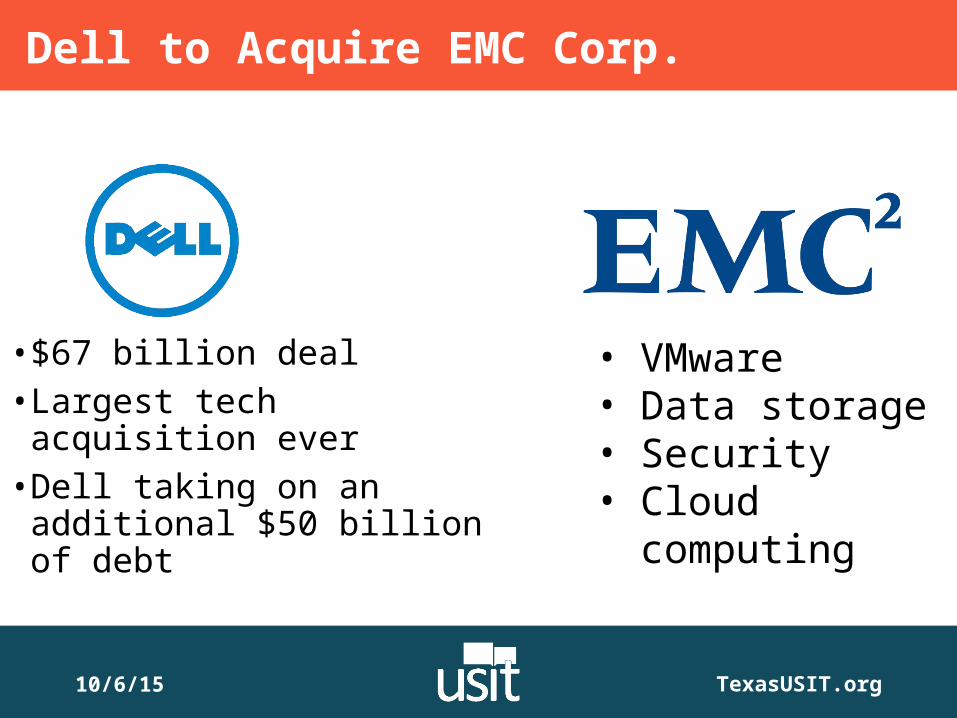

• $67 billion deal• Largest tech acquisition ever• Dell taking on an additional $50 billion of debt

• VMware • Data storage• Security• Cloud

computing

Dell to Acquire EMC Corp.

10/6/15

TexasUSIT.org

• SABMiller valued at $104.2 billion• Largest beer acquisition ever• New company will have over 28% global market share, $64 billion in revenue, toehold in high growth Asian and African markets

Anheuser-Busch InBev to Acquire SABMiller

10/6/15

Portfolio UpdateCliffe Kim

Name Price 5d Chg ($ · %) Mkt Value Total Chg ($ · %) 52wk Low

52wk High

AAL American Airlines 43.41 68.64 · 13.85% 564.33 114.92 · 25.57% 28.10 56.20AAPL Apple 111.79 10.08 · 0.43% 2347.59 889.26 · 60.98% 92.00 134.54ACC American Campus 37.52 3.40 · 0.91% 375.20 16.90 · 4.72% 32.12 45.38AGX Argan 35.27 -24.15 · -1.92% 1234.45 474.95 · 62.53% 28.62 42.50BABA Alibaba Group 69.67 28.75 · 9.00% 348.35 -59.35 · -14.56% 57.20 120BBRY BlackBerry 7.17 39.00 · 5.75% 717.00 -320.00 · -30.86% 5.96 12.63FNMA Fannie Mae 2.61 28.60 · 8.30% 373.23 -145.86 · -28.10% 0.01 3.51GENC Gencor 9.82 17.86 · 4.03% 461.54 -37.60 · -7.53% 8.90 10.17GILD Gilead Sciences 98.19 3.25 · 0.67% 490.95 -22.05 · -4.30% 85.95 123.37AJRD Aerojet Rocketdyne

17.25 -6.00 · -0.69% 862.50 11.50 · 1.35% 15.11 24.35

IDT IDT Corporation 14.24 8.25 · 0.78% 1068.00 -283.50 · -20.98% 13.26 23.24MUSA Murphy USA 55.24 -1.65 · -0.20% 828.60 239.10 · 40.56% 47.73 73.97PTC PTC Inc. 34.68 6.50 · 1.91% 346.80 8.70 · 2.57% 30.53 42.75RNET RigNet 30.06 10.00 · 3.44% 300.60 -153.60 · -33.82% 23.37 47.37SLCA U.S. Silica 17.25 22.05 · 9.32% 258.75 -168.75 · -39.47% 13.48 55.29SWKH SWK Holdings 13.70 49,420.00 ·

864.79%54800.00 54352.00 ·

1123.21%1.17 4.5

TRN Trinity Industries 27.08 27.82 · 8.58% 354.04 -47.06 · -11.79% 21.78 42.08HLT Hilton Worldwide Holdings

25.00 20.57 · 5.09% 425.00 -13.43 · -3.06% 20.72 31.60

05/02/2023 TexasUSIT.org

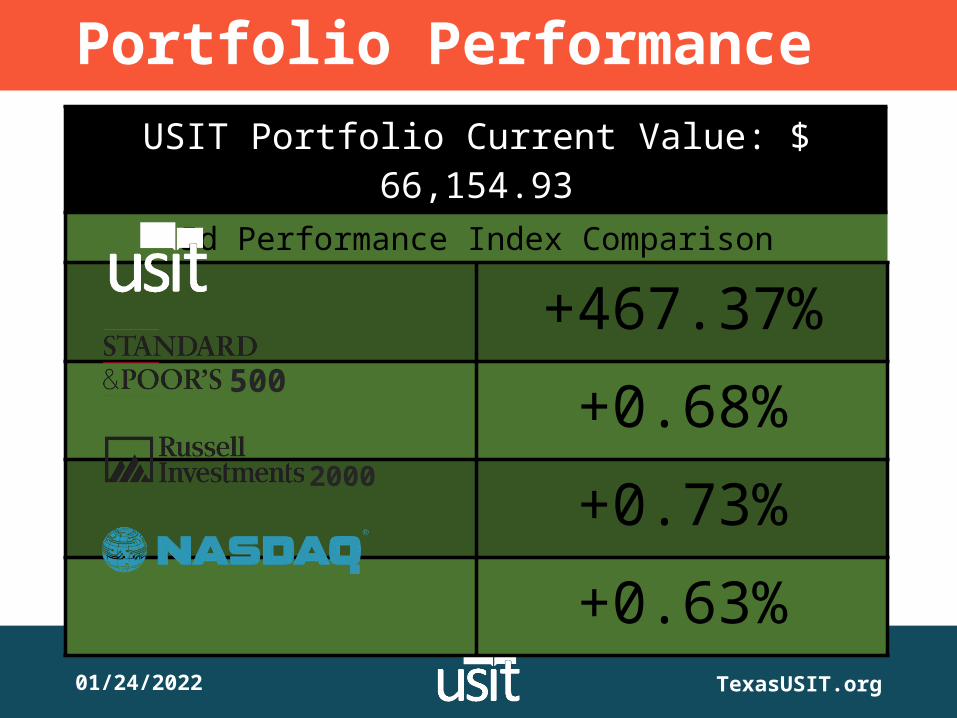

Portfolio PerformanceUSIT Portfolio Current Value: $ 66,154.93

5d Performance Index Comparison

+467.37%+0.68%+0.73%+0.63%

500

2000

05/02/2023 TexasUSIT.org

The IMPORTANT Question to Ask:• What happened with SWKH?• Why did it rise so dramatically??• How is this possible???

Where are we going to go for the next social?

#goodJobGuys

05/02/2023 TexasUSIT.org

The Choices:1. Hawaii• Actually go to an actual Hula Hut

2. Milano• Buy Italian tailored suits to impress recruiters

at the next Career Fair3. Las Vegas• Gamble away our returns and come back

with even HIGHER returns, repeat, etc.

Get your passports ready!

05/02/2023 TexasUSIT.org

The IMPORTANT Question to Ask:• What happened with SWKH?• Why did it rise so dramatically??• How is this possible???

Where are we going to go for the next social?

#goodJobGuys

05/02/2023 TexasUSIT.org

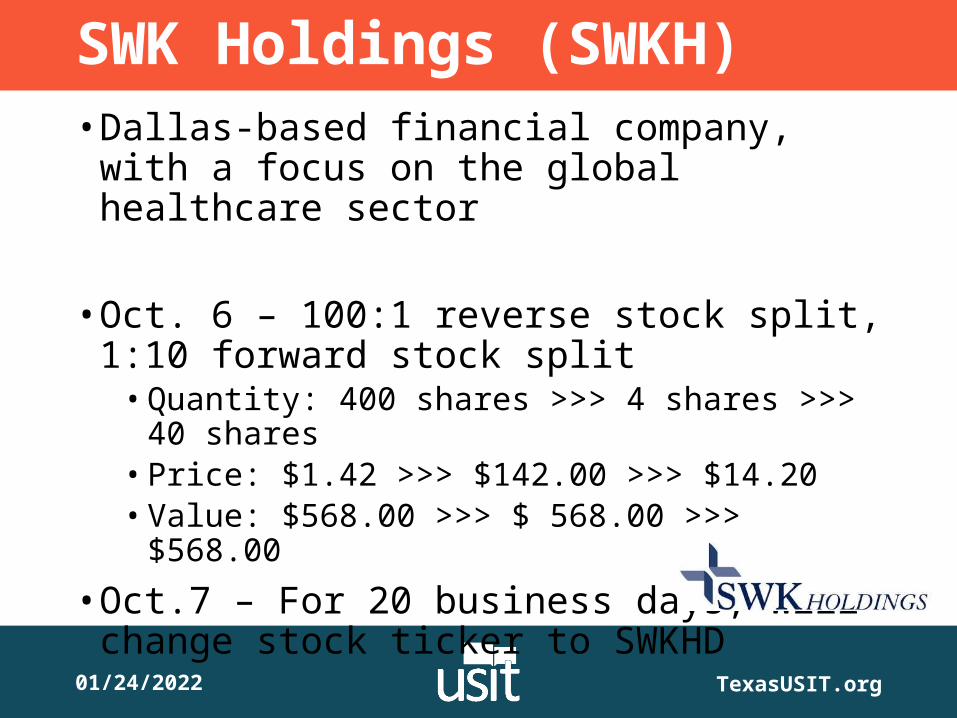

SWK Holdings (SWKH)• Dallas-based financial company, with a

focus on the global healthcare sector

• Oct. 6 – 100:1 reverse stock split, 1:10 forward stock split• Quantity: 400 shares >>> 4 shares >>> 40

shares• Price: $1.42 >>> $142.00 >>> $14.20• Value: $568.00 >>> $ 568.00 >>> $568.00

• Oct.7 – For 20 business days, will change stock ticker to SWKHD

05/02/2023 TexasUSIT.org

Reverse Stock Split?• Why do companies do reverse stock

splits?

• Perception Change: ($10 stock vs $1 stock)• Some institutions won’t buy stocks under $5

• Regulatory Reasons• Listing requirements of NYSE and NASDAQ

• Getting rid of small investors• Cash payout for small shares

05/02/2023 TexasUSIT.org

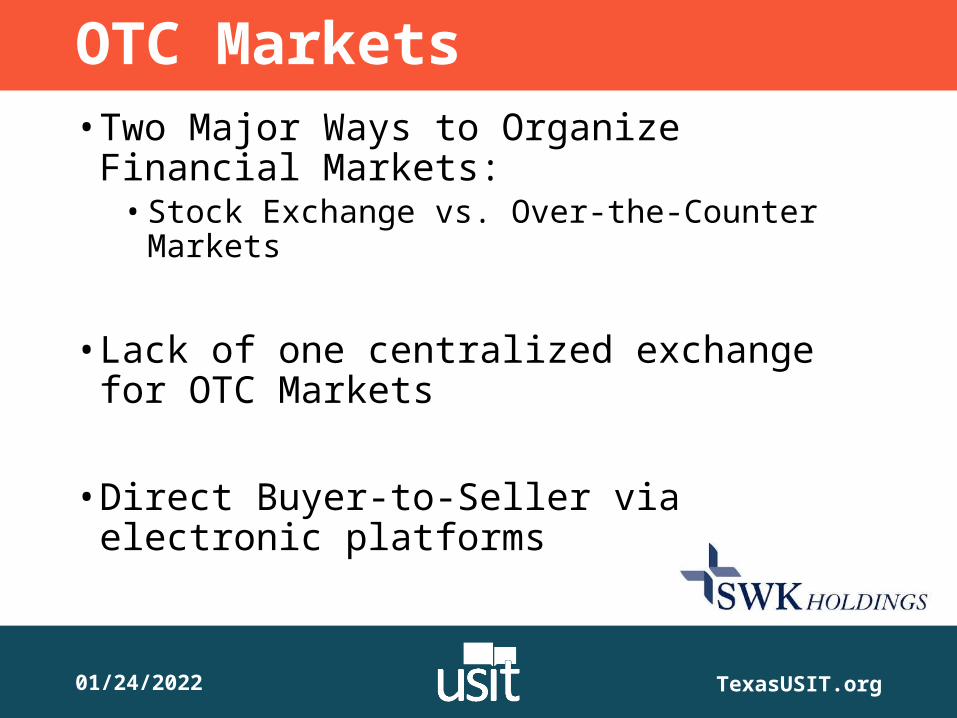

OTC Markets• Two Major Ways to Organize Financial

Markets:• Stock Exchange vs. Over-the-Counter Markets

• Lack of one centralized exchange for OTC Markets

• Direct Buyer-to-Seller via electronic platforms

05/02/2023 TexasUSIT.org

ConclusionReverse/Forward Stock Split+ OTC Market+ Lack of Coverage/Interest+ Change in Stock Ticker+ Google Finance being wonky

= False Hopes, Life Disappointments, Confused Cliffe

05/02/2023 TexasUSIT.org

Portfolio PerformanceUSIT Portfolio Current Value: $ 11,902.93

5d Performance Index Comparison

+2.08%+0.68%+0.73%+0.63%

500

2000

Lecture: Generating Investment ThesesDylan James

10-13-15

Constructing a ThesisThe ABCs

Investment “X” is undervalued because of “XYZ”

10-13-15

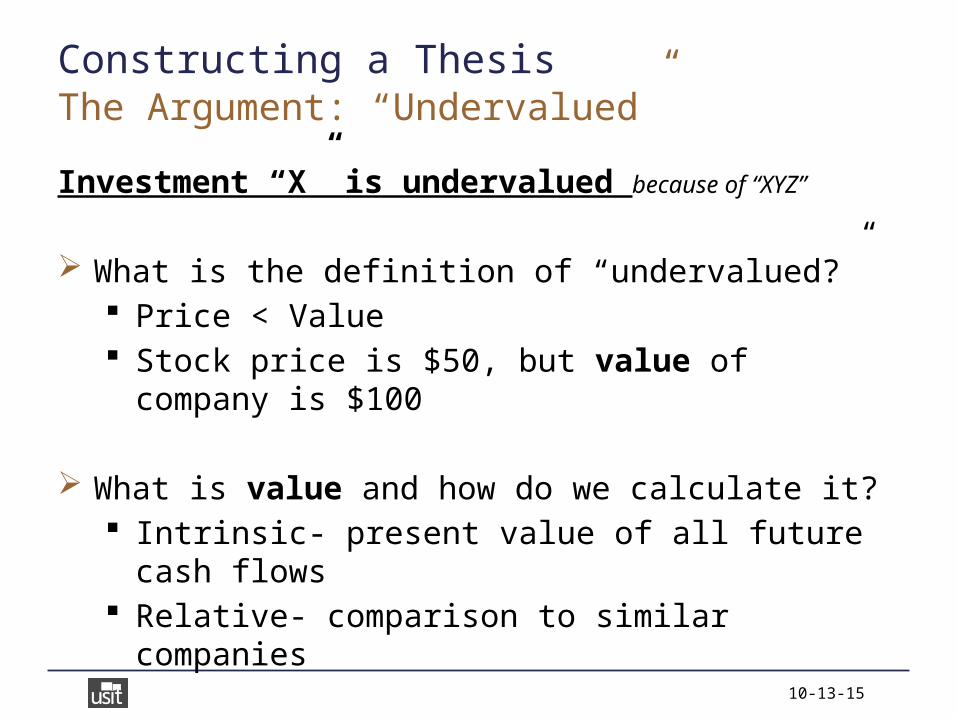

Constructing a Thesis

Investment “X” is undervalued because of “XYZ”

What is the definition of “undervalued?” Price < Value Stock price is $50, but value of company is $100

What is value and how do we calculate it? Intrinsic- present value of all future cash flows Relative- comparison to similar companies

The Argument: “Undervalued”

10-13-15

Constructing a Thesis

Investment “X” is undervalued because of “XYZ”

The fun part! Simply the ability to craft a coherent, logical argument Skillset not unique to finance (philosophy, debate, politics)

Will focus on providing examples particular to finance Can look for supporting evidence in two broad categories Fundamental vs. Technical

Supporting Evidence

10-13-15

Constructing a Thesis

Fundamental Analysis

Fundamental vs. Technical

10-13-15

Constructing a Thesis

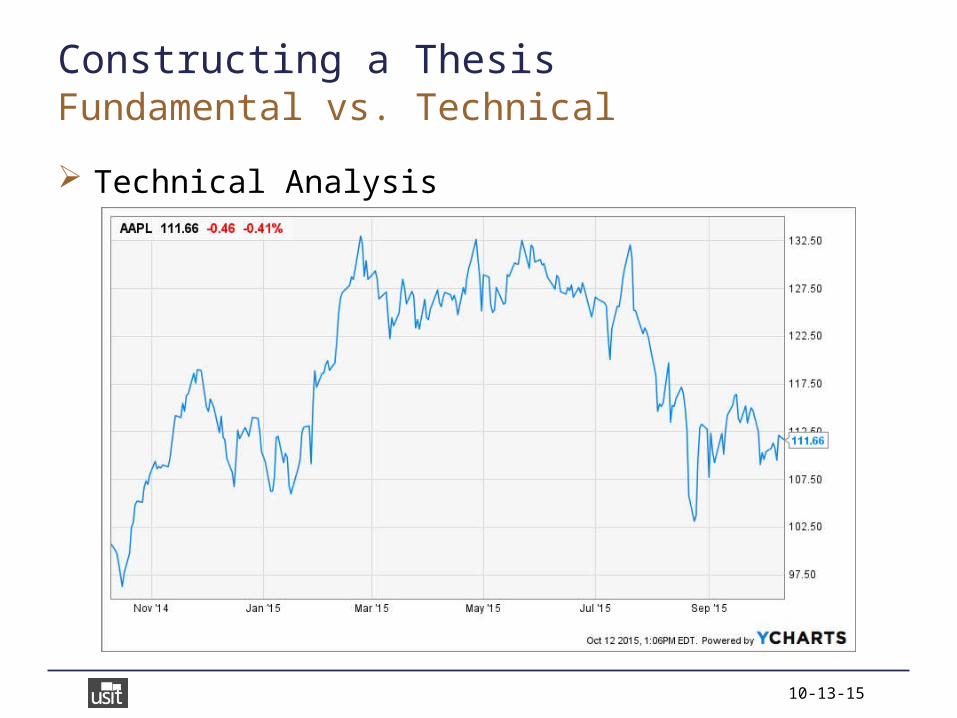

Technical Analysis

Fundamental vs. Technical

10-13-15

Warren Buffett: "I realized technical analysis didn't work when I turned the charts upside down and didn't get a different answer"

10-13-15

Constructing a Thesis

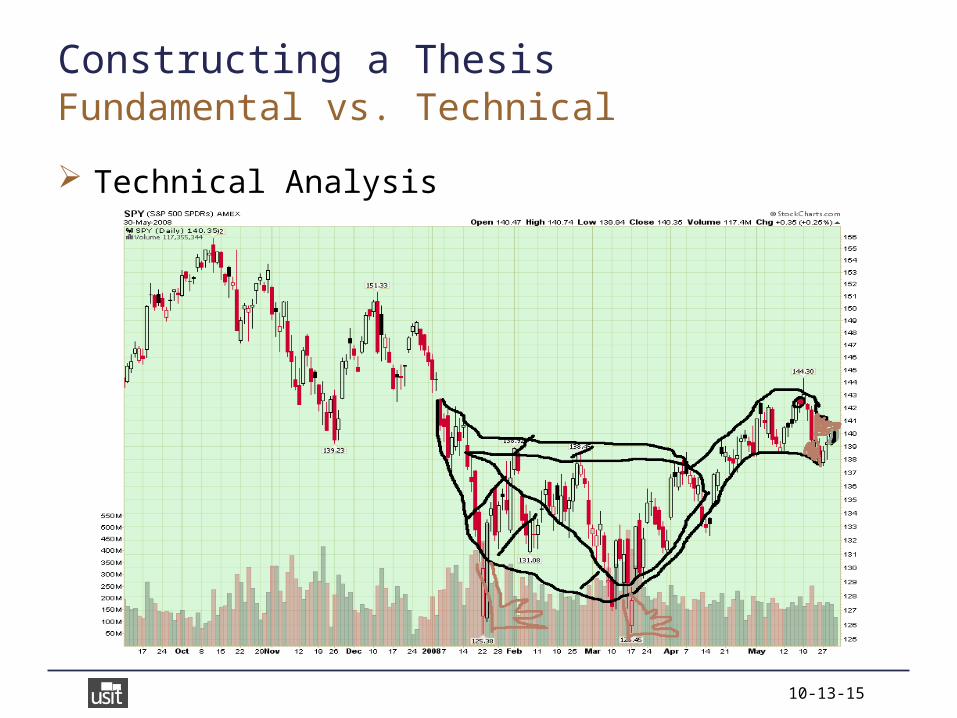

Technical Analysis

Fundamental vs. Technical

10-13-15

Constructing a Thesis

Technical Analysis

Fundamental vs. Technical

10-13-15

Constructing a Thesis

Technical Analysis

Fundamental vs. Technical

10-13-15

Constructing a Thesis

Technical Analysis

Fundamental vs. Technical

10-13-15

Constructing a Thesis

Growth Investors Search for companies that will grow at above-market rates,

willing to pay a premium for future growth Often buy stocks in popular sectors such as biotech Argue that investors are underestimating future growth

Value Investors Search for companies that are down on their luck, attempting

to buy at a discount with a margin of safety Often buy stocks in unpopular sectors such as energy Argue that investors are underestimating current value

Value vs. Growth

10-13-15

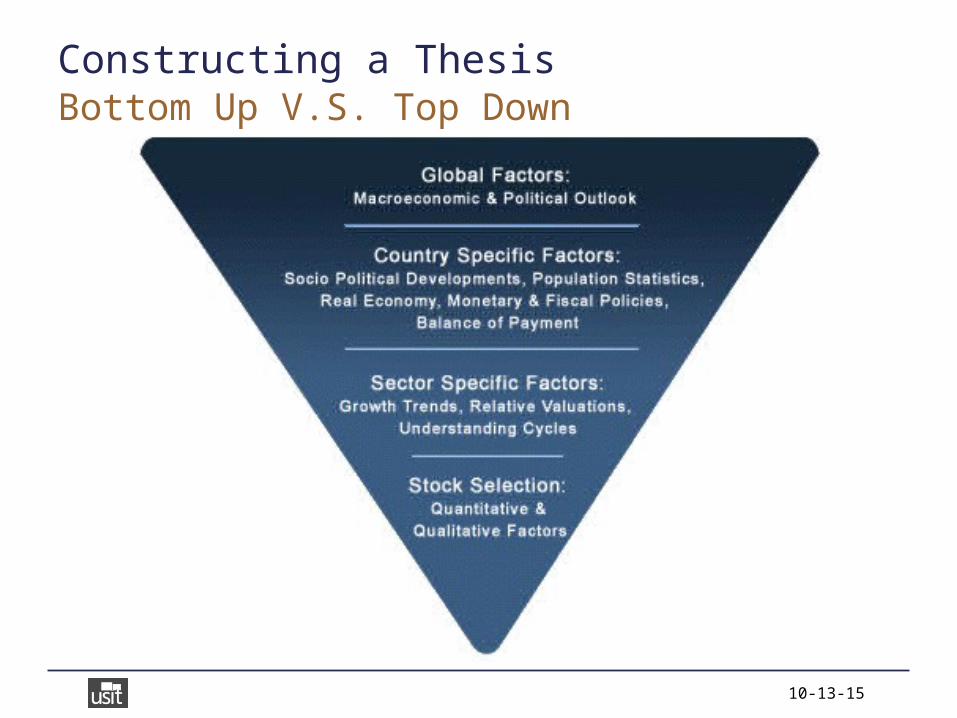

Constructing a ThesisBottom Up V.S. Top Down

10-13-15

Constructing a Thesis

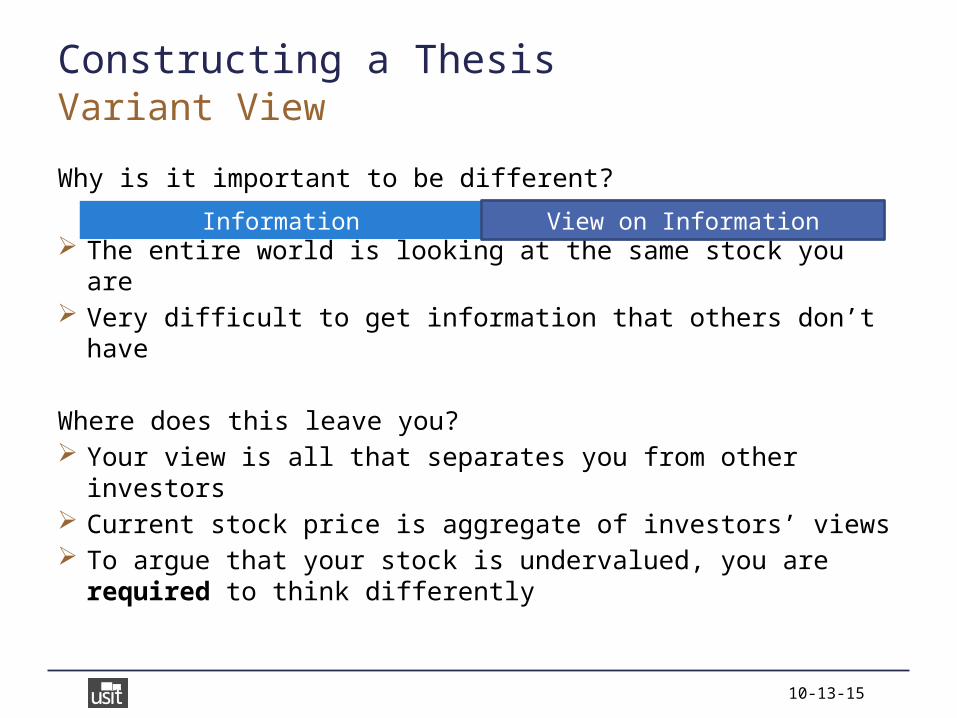

Why is it important to be different?

The entire world is looking at the same stock you are Very difficult to get information that others don’t have

Where does this leave you?

Variant View

Information View on Information

10-13-15

Constructing a Thesis

Why is it important to be different?

The entire world is looking at the same stock you are Very difficult to get information that others don’t have

Where does this leave you? Your view is all that separates you from other investors Current stock price is aggregate of investors’ views To argue that your stock is undervalued, you are required to

think differently

Variant View

Information View on Information

10-13-15

Constructing a Thesis

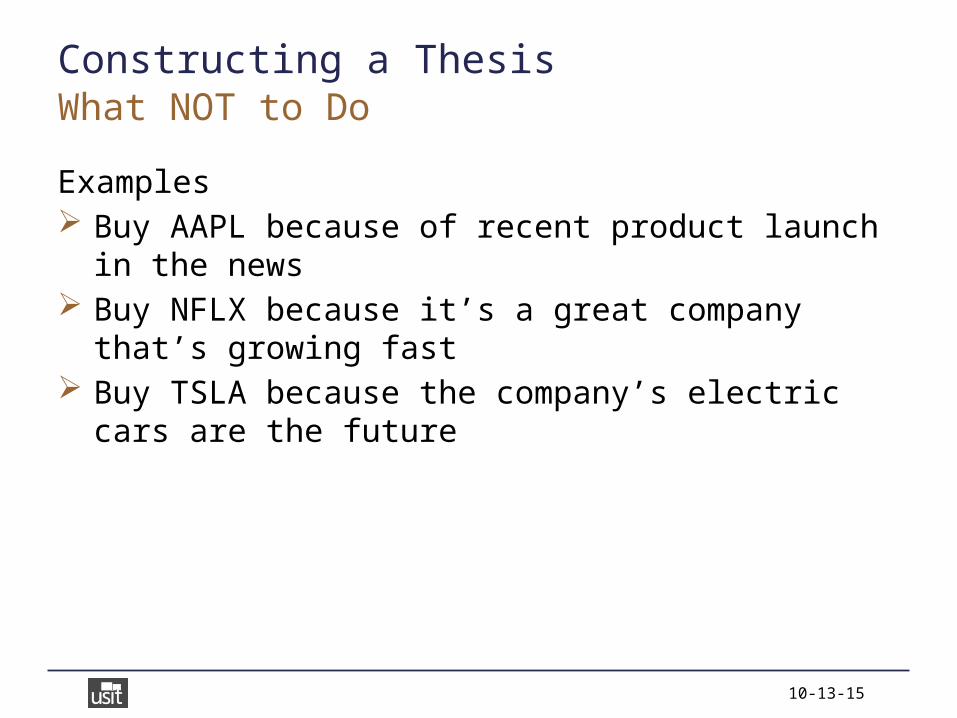

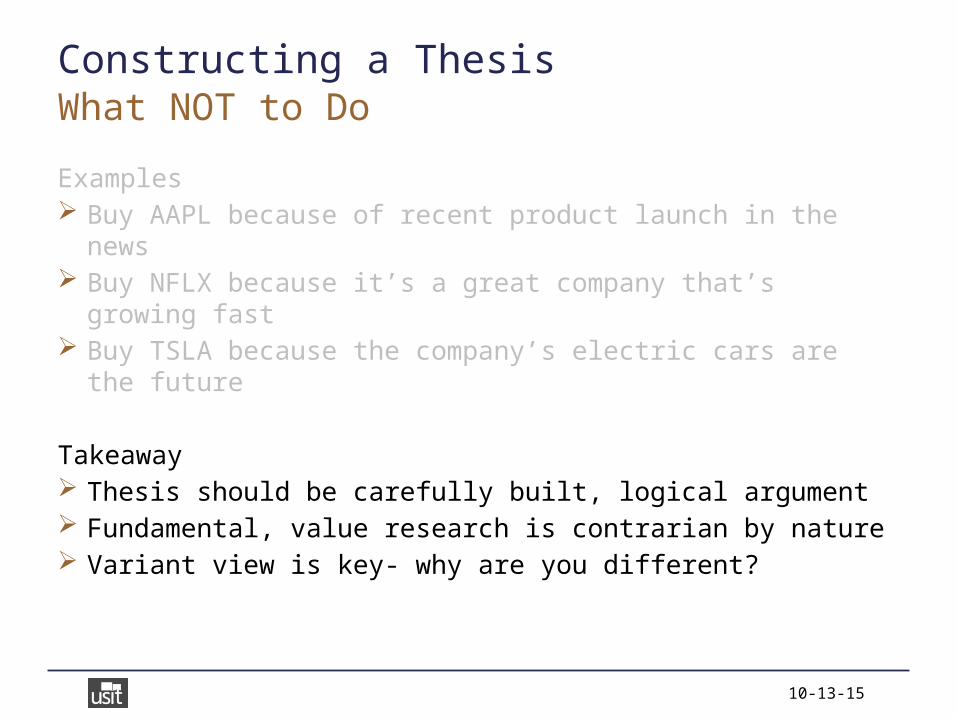

Examples Buy AAPL because of recent product launch in the news Buy NFLX because it’s a great company that’s growing fast Buy TSLA because the company’s electric cars are the future

What NOT to Do

10-13-15

Constructing a Thesis

Examples Buy AAPL because of recent product launch in the news Buy NFLX because it’s a great company that’s growing fast Buy TSLA because the company’s electric cars are the future

Takeaway Thesis should be carefully built, logical argument Fundamental, value research is contrarian by nature Variant view is key- why are you different?

What NOT to Do

Stock Pitch: IPG Photonics (IPGP)Pitch Team: Grant Kjeldsen, Sunny Pamidimukkala, Priyanka Suri, Collin Hartman, Srija Nalla, Max Huang

IPG

Phot

onics

CompanyThesis Industry RisksValuation

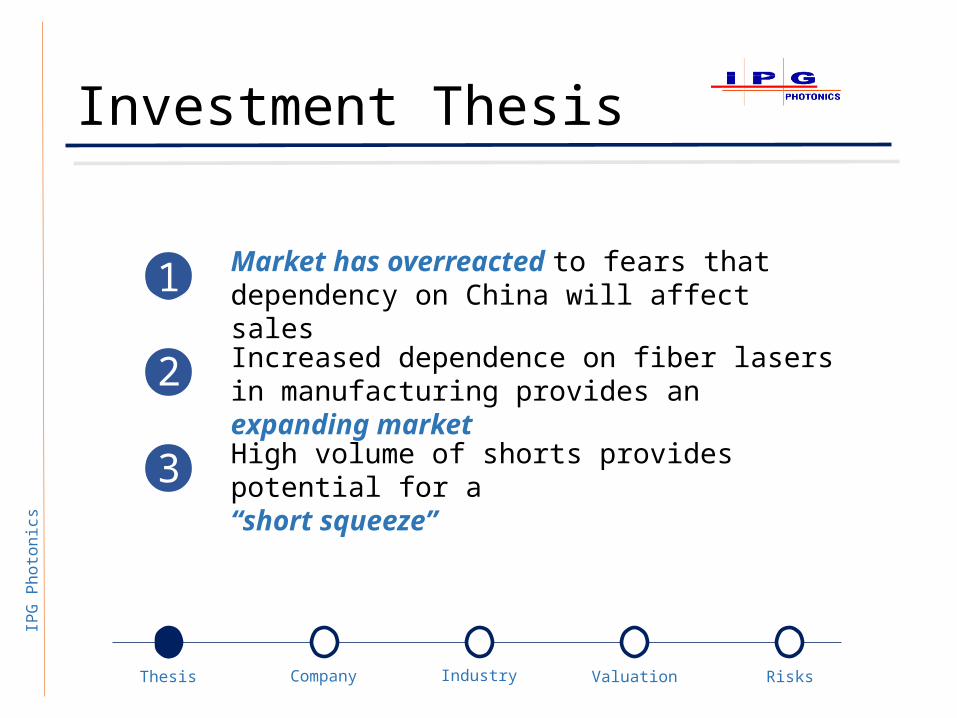

IPG Photonics Corp (IPGP)Chinese Economic Downturn Overshadows Revenue GrowthLONG, TP $94.38 (+23.7%)

PITCH TEAM

Grant Kjeldsen, DirectorSunny Pamidimukkala, Senior AnalystCollin Hartman, Junior AnalystPriyanka Suri, Junior AnalystSrija Nalla, AnalystMax Huang, Analyst

IPG

Phot

onics

CompanyThesis Industry RisksValuationInvestment Thesis

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Investment Thesis

3

2

1 Market has overreacted to fears that dependency on China will affect sales

Increased dependence on fiber lasers in manufacturing provides an expanding marketHigh volume of shorts provides potential for a “short squeeze”

IPG

Phot

onics

CompanyThesis Industry RisksValuationCompany Overview

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Company Overview Global Leader in Rapidly Expanding Technological Market

Growing international market

• Fiber laser usage quickly displacing conventional lasers: increased power, accuracy, customizability

• Diverse applications: materials processing, advanced tech, telecommunication, medical

• Uncontested leader in fiber laser industry

Fiber laser + laser amplifier manufacturer

• Products sold to OEMs, systems integrators and end users for use in many industries

• Significant quarterly revenue increase in Chinese sales department despite economic slowdown

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Company Overview Competitive Advantage

Vertical Integration• Reduce costs while controlling quality• Allows for protection of intellectual

property and trade secretss costControls qualityFirst mover advantage in fiber lasers• Dominance in market share• Allows creation of diverse customer base

across geographic locations

Strong Global Presence• Revenues seeing a positive trend in Asia• Infrastructure built up primarily in the US, China, and Europe

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Company Overview Diverse End Uses and Customers in Materials Processing

• Automotive• General Manufacturing• Heavy Industry• Aerospace• Semi-Electronics• Consumer

IPG

Phot

onics

CompanyThesis Industry RisksValuation

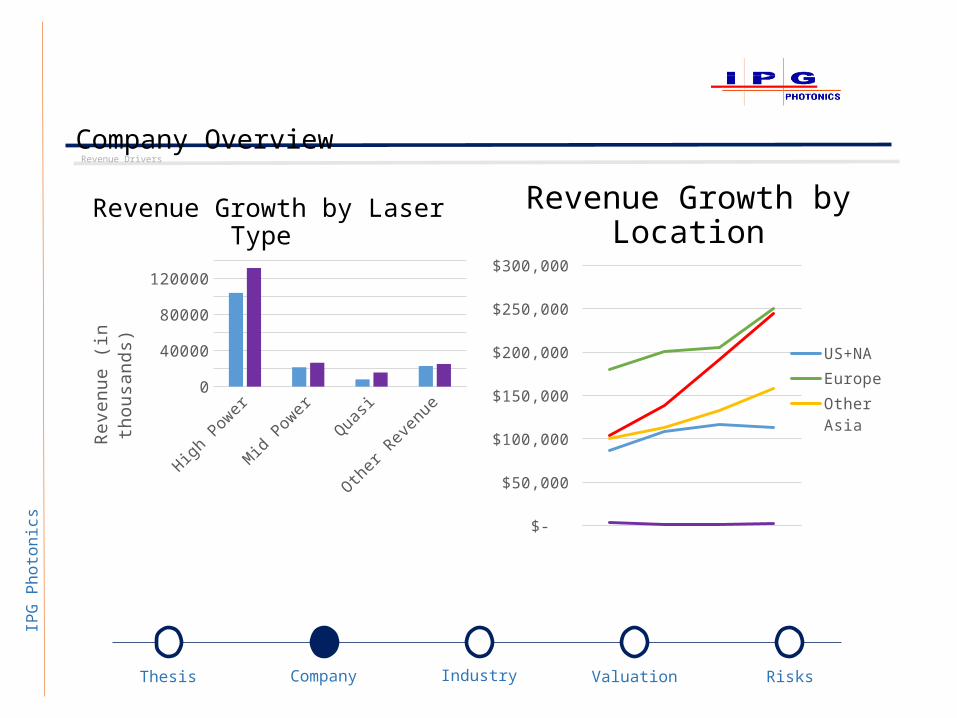

Company Overview Revenue Drivers

Revenue Growth by Laser Type

High Power

Mid Power

Quasi Other Revenue

0

20000

40000

60000

80000

100000

120000

140000

2014 Q2

Reve

nue

(in th

ousa

nds)

Revenue Growth by Location

2011 2012 2013 2014 $-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

US+NAEuropeOther AsiaChina

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Company Overview Chinese Market Slowdown?

2014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

$-

$50.0

$100.0

$150.0

$200.0

$250.0

Quarterly Revenue

reve

nue

in th

ousa

nds

2014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

0%

5%

10%

15%

20%

25%

30%

% Quarterly Revenue Growth vs Previous Year

% g

rowt

h

slowd

own

begi

ns

slowd

own

begi

ns

IPG

Phot

onics

CompanyThesis Industry RisksValuation

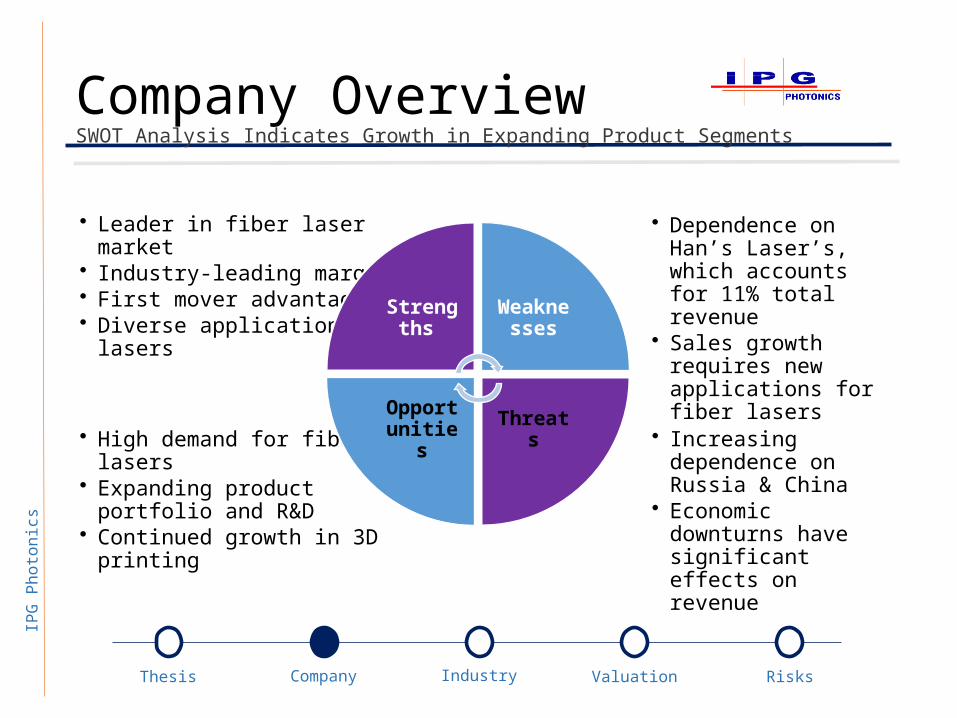

Company OverviewSWOT Analysis Indicates Growth in Expanding Product Segments

• Increasing dependence on Russia & China

• Economic downturns have significant effects on revenue

• High demand for fiber lasers• Expanding product portfolio

and R&D• Continued growth in 3D

printing

• Dependence on Han’s Laser’s, which accounts for 11% total revenue

• Sales growth requires new applications for fiber lasers

• Leader in fiber laser market• Industry-leading margins• First mover advantage• Diverse applications for

lasersStreng

ths Weaknesses

Threats

Opportunities

IPG

Phot

onics

CompanyThesis Industry RisksValuationIndustry Overview

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Industry Overview

Barriers to Entry

Bargaining Power of Buyers

Threat of Substitutes

Intensity of Rivalry

Threat of Substitutes

Bargaining Power of Suppliers

HIGH

MODERATE

LOW

MODERATE

LOW

Large startup costs discourage new entrants High costs of resources, human capital, and research

and development

Industry is not contract-based, so buyers can alter the product volumes they demand

Top 5 customers account for 23% of sales

Firms compete based on differentiation from competitors in prices and products

IPGP has an individualized approach

Compete with non-laser production methods, such as water-jet cutting and resistance welding

Manufacturing equipment is specialized

Bargaining power of suppliers is minimized due to IPGP’s vertical integration

Materials required to build lasers produced in-house

Industry Dynamic

Porter’s Assessment

Rationale

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Industry OverviewIndustry improvements have produced success

Vertical integration has allowed IPGP to create personalized laser diodes and finished fiber lasers and amplifiers, which has reduced manufacturing costs and increased quality.

Lower costs the average cost per watt of output power has decreased dramatically over the past decade.

Expanded Product Portfolio IPGP continues to invest in research and development to add additional wavelengths and power levels, while developing new product lines.

IPG

Phot

onics

CompanyThesis Industry RisksValuation

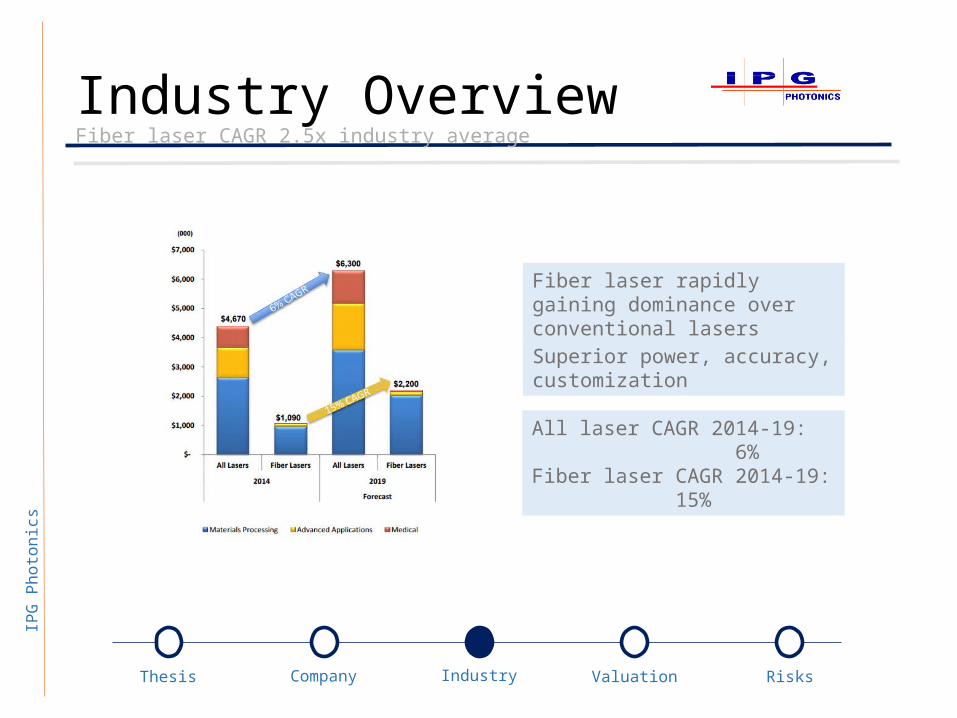

Industry OverviewFiber laser CAGR 2.5x industry average

Fiber laser rapidly gaining dominance over conventional lasers

All laser CAGR 2014-19: 6%Fiber laser CAGR 2014-19: 15%

Superior power, accuracy, customization

IPG

Phot

onics

CompanyThesis Industry RisksValuationValuation

IPG

Phot

onics

CompanyThesis Industry RisksValuation

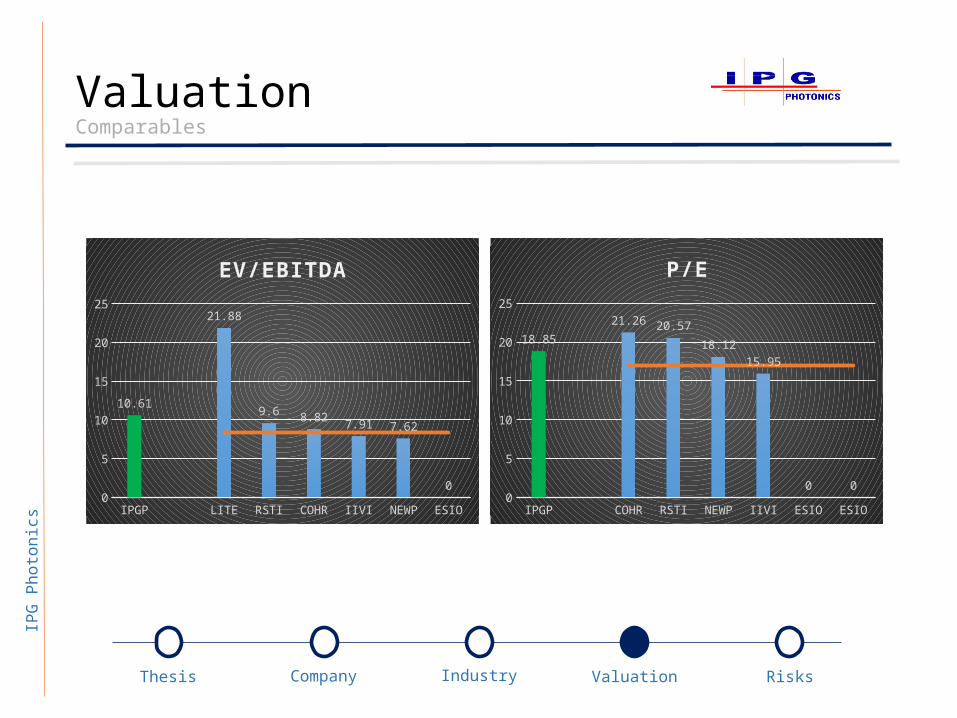

ValuationComparables

IPGP LITE RSTI COHR IIVI NEWP ESIO0

5

10

15

20

25

10.61

21.88

9.6 8.82 7.91 7.62

0

EV/EBITDA

IPGP COHR RSTI NEWP IIVI ESIO ESIO0

5

10

15

20

25

18.85

21.26 20.57

18.1215.95

0 0

P/E

IPG

Phot

onics

CompanyThesis Industry RisksValuation

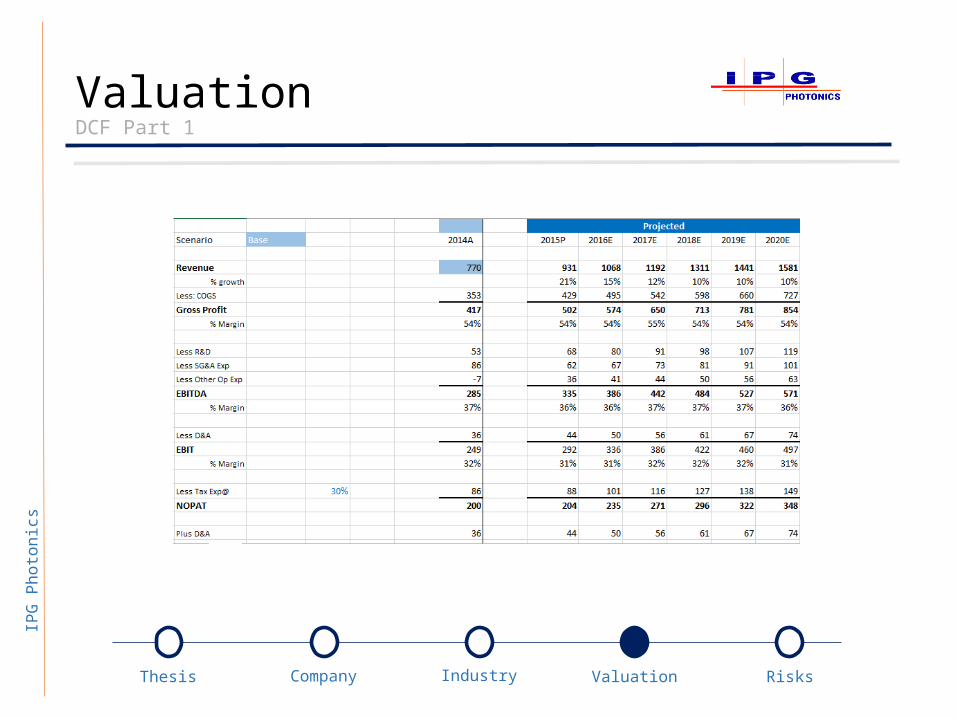

ValuationDCF Part 1

IPG

Phot

onics

CompanyThesis Industry RisksValuation

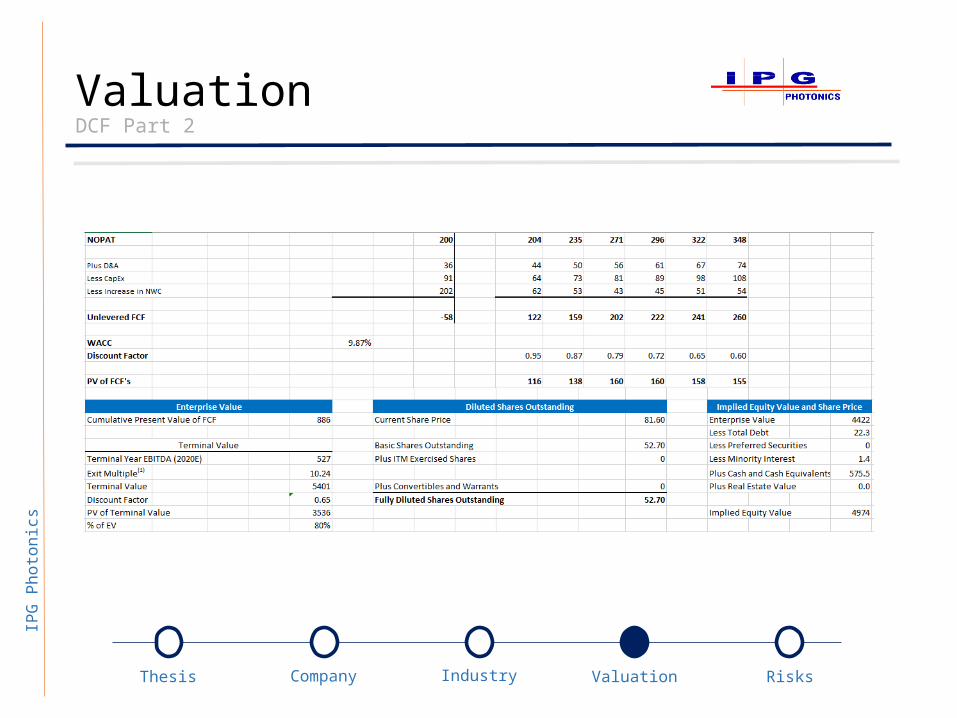

ValuationDCF Part 2

IPG

Phot

onics

CompanyThesis Industry RisksValuation

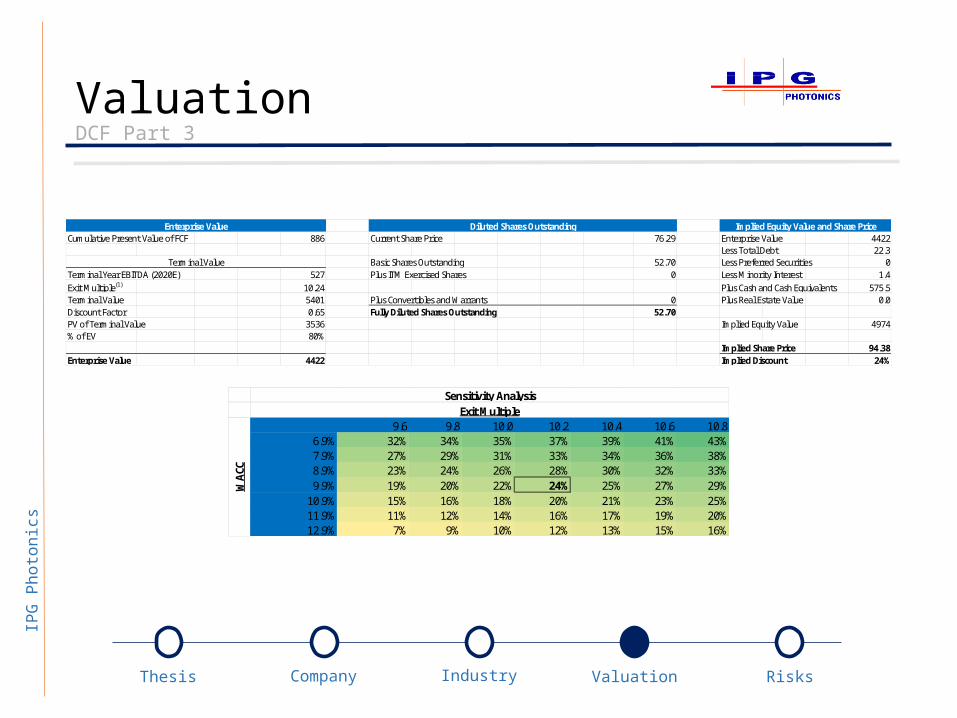

ValuationDCF Part 3

Cumulative Present Value of FCF 886 Current Share Price 76.29 Enterprise Value 4422Less Total Debt 22.3

Basic Shares Outstanding 52.70 Less Preferred Securities 0Terminal Year EBITDA (2020E) 527 Plus ITM Exercised Shares 0 Less Minority Interest 1.4Exit Multiple(1) 10.24 Plus Cash and Cash Equivalents 575.5Terminal Value 5401 Plus Convertibles and Warrants 0 Plus Real Estate Value 0.0Discount Factor 0.65 Fully Diluted Shares Outstanding 52.70PV of Terminal Value 3536 Implied Equity Value 4974% of EV 80%

Implied Share Price 94.38Enterprise Value 4422 Implied Discount 24%

Enterprise Value

Terminal Value

Diluted Shares Outstanding Implied Equity Value and Share Price

9.6 9.8 10.0 10.2 10.4 10.6 10.86.9% 32% 34% 35% 37% 39% 41% 43%7.9% 27% 29% 31% 33% 34% 36% 38%8.9% 23% 24% 26% 28% 30% 32% 33%9.9% 19% 20% 22% 24% 25% 27% 29%

10.9% 15% 16% 18% 20% 21% 23% 25%11.9% 11% 12% 14% 16% 17% 19% 20%12.9% 7% 9% 10% 12% 13% 15% 16%

Sensitivity AnalysisExit Multiple

WAC

C

IPG

Phot

onics

CompanyThesis Industry RisksValuation

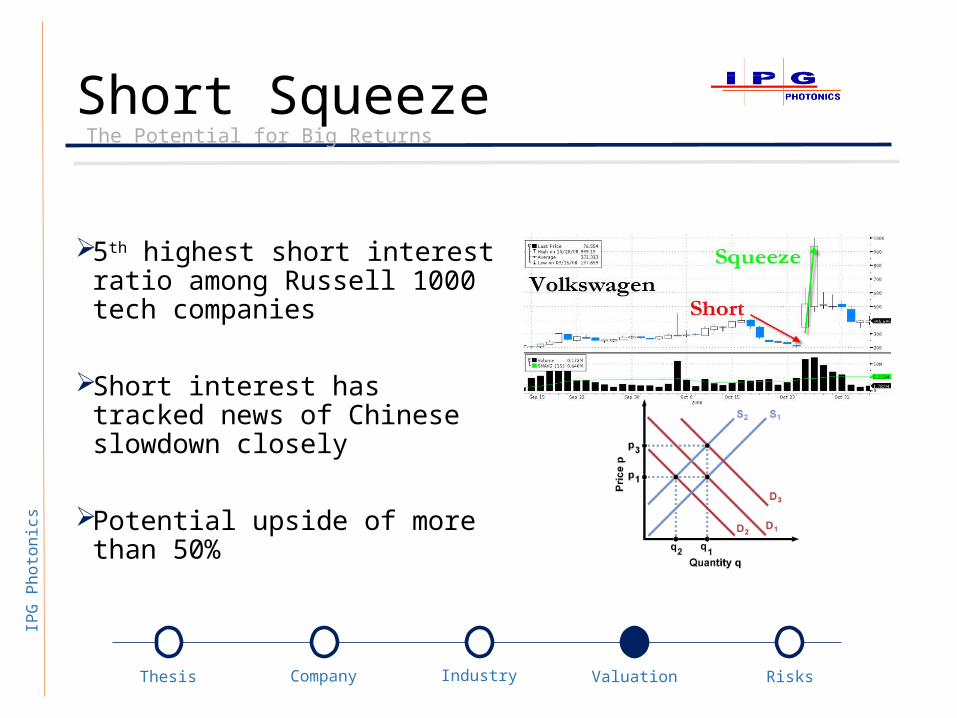

Short Squeeze The Potential for Big Returns

5th highest short interest ratio among Russell 1000 tech companies

Short interest has tracked news of Chinese slowdown closely

Potential upside of more than 50%

IPG

Phot

onics

CompanyThesis Industry RisksValuationRisks and Mitigants

IPG

Phot

onics

CompanyThesis Industry RisksValuation

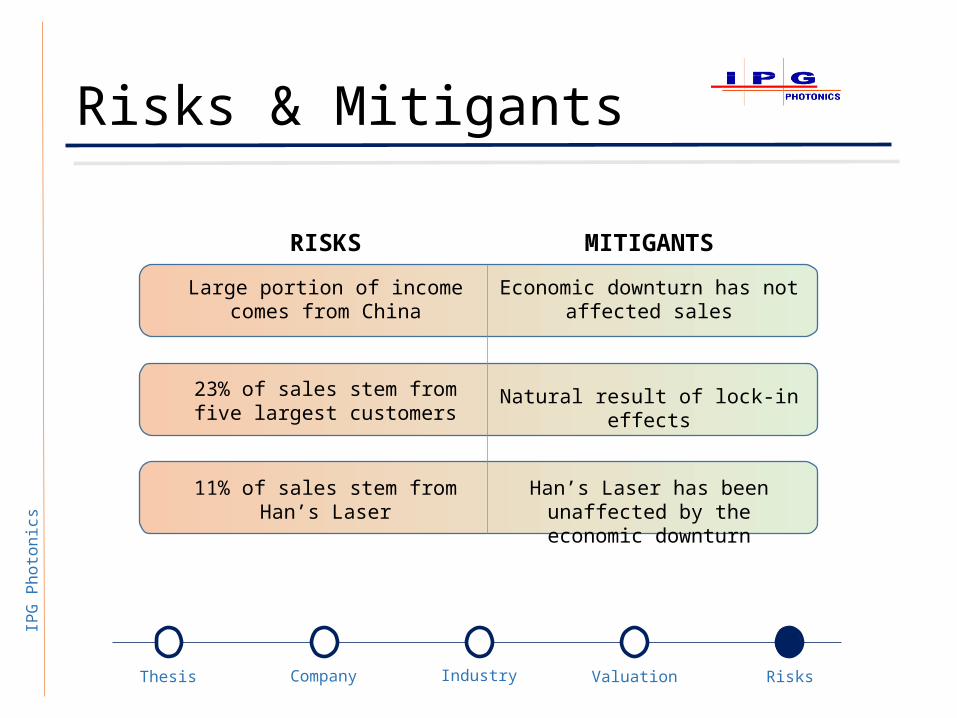

Risks & Mitigants

Large portion of income comes from China

23% of sales stem from five largest customers

11% of sales stem from Han’s Laser

Economic downturn has not affected sales

Natural result of lock-in effects

Han’s Laser has been unaffected by the economic

downturn

RISKS MITIGANTS

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Conclusion

321Investors misgauged sensitivity to China

Expanding fiber laser industry

Potential shortsqueeze

TP: $ 94.38 (+23.7%)

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Questions?

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Appendix

IPG

Phot

onics

CompanyThesis Industry RisksValuation

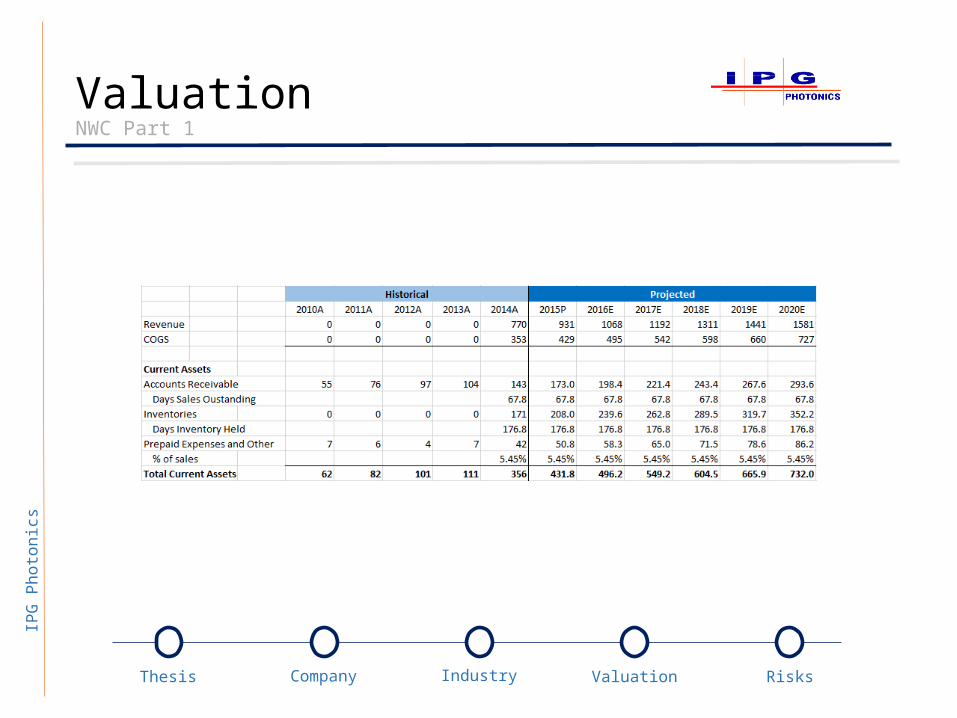

ValuationNWC Part 1

IPG

Phot

onics

CompanyThesis Industry RisksValuation

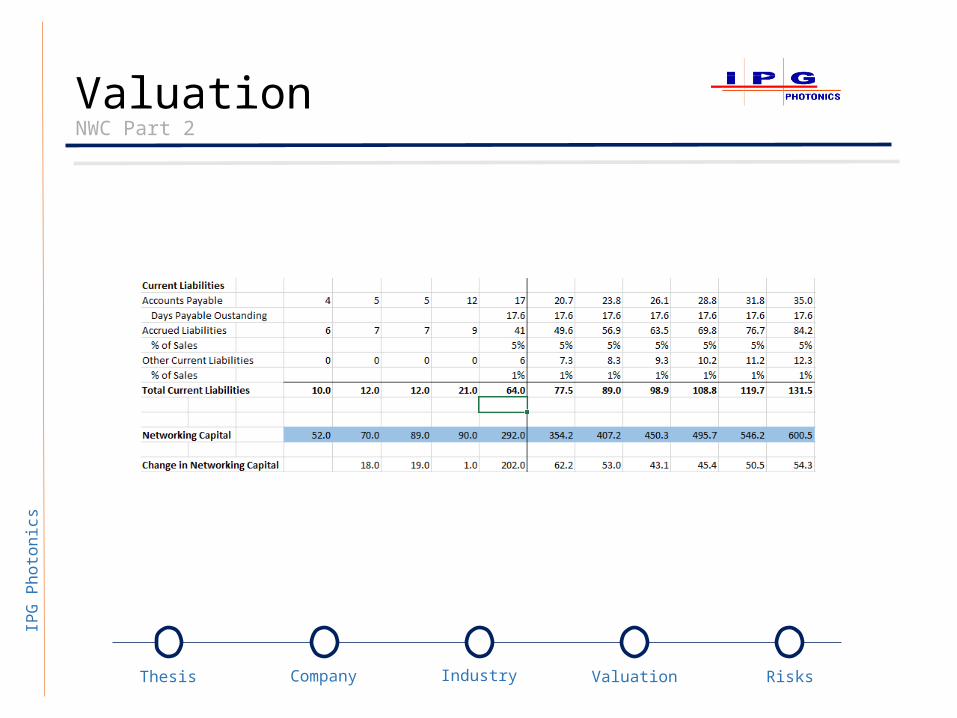

ValuationNWC Part 2

IPG

Phot

onics

CompanyThesis Industry RisksValuation

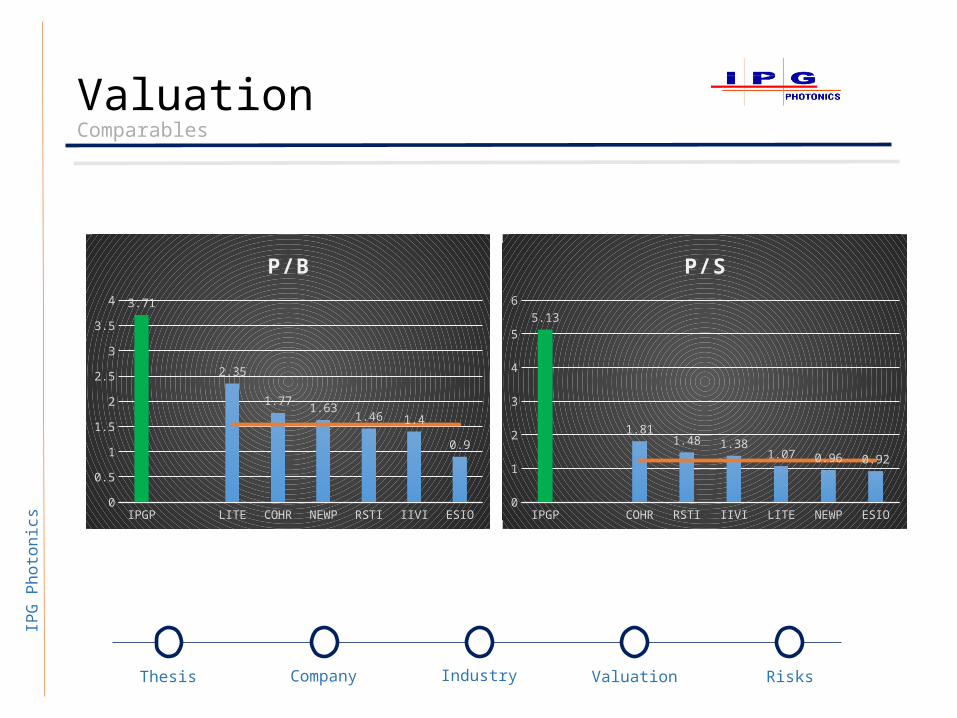

ValuationComparables

IPGP LITE COHR NEWP RSTI IIVI ESIO0

0.5

1

1.5

2

2.5

3

3.5

4 3.71

2.35

1.77 1.631.46 1.4

0.9

P/B

IPGP COHR RSTI IIVI LITE NEWP ESIO0

1

2

3

4

5

6

5.13

1.811.48 1.38

1.07 0.96 0.92

P/S

IPG

Phot

onics

CompanyThesis Industry RisksValuation

ValuationComparables

IPG

Phot

onics

CompanyThesis Industry RisksValuation

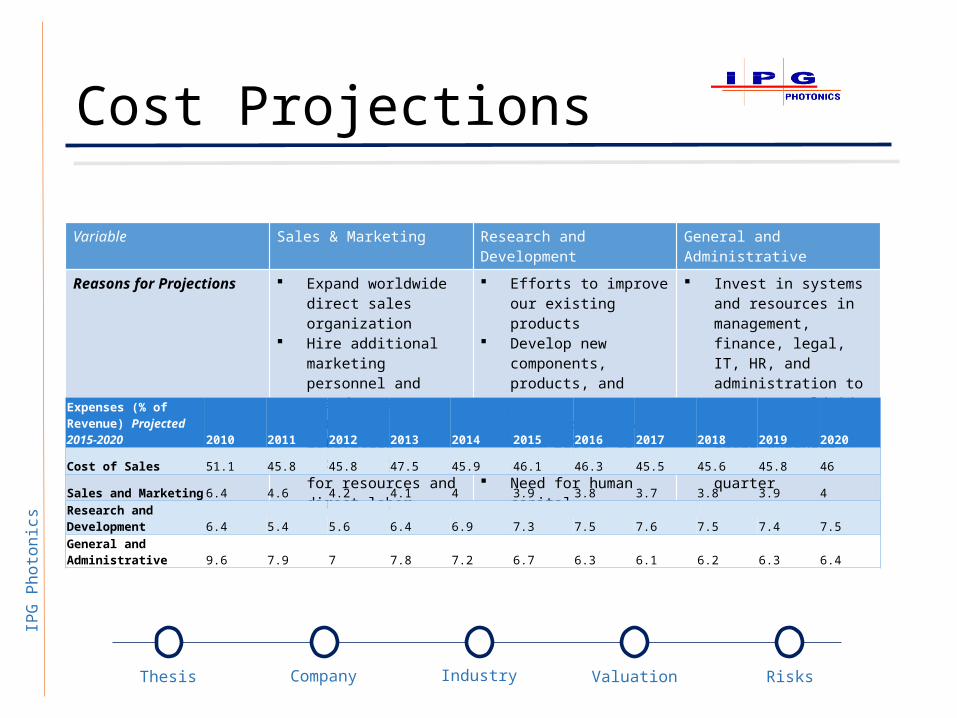

Cost ProjectionsVariable Sales & Marketing Research and Development General and Administrative

Reasons for Projections Expand worldwide direct sales organization

Hire additional marketing personnel and spend more on marketing activities

Increasing costs for resources and direct labor

Efforts to improve our existing products

Develop new components, products, and systems

Expenses may vary from period to period

Need for human capital

Invest in systems and resources in management, finance, legal, IT, HR, and administration to support worldwide operations

Legal expenses vary quarter to quarter

Expenses (% of Revenue) Projected 2015-2020 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Cost of Sales 51.1 45.8 45.8 47.5 45.9 46.1 46.3 45.5 45.6 45.8 46

Sales and Marketing 6.4 4.6 4.2 4.1 4 3.9 3.8 3.7 3.8 3.9 4

Research and Development 6.4 5.4 5.6 6.4 6.9 7.3 7.5 7.6 7.5 7.4 7.5

General and Administrative 9.6 7.9 7 7.8 7.2 6.7 6.3 6.1 6.2 6.3 6.4

IPG

Phot

onics

CompanyThesis Industry RisksValuation

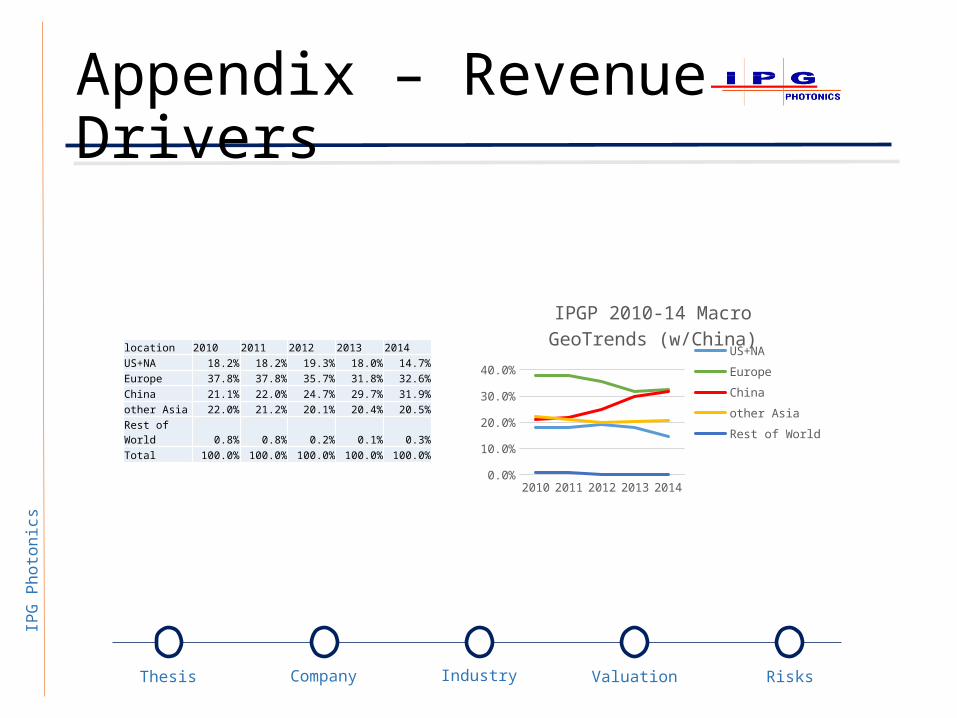

Appendix – Revenue Drivers

location 2010 2011 2012 2013 2014US+NA 18.2% 18.2% 19.3% 18.0% 14.7%Europe 37.8% 37.8% 35.7% 31.8% 32.6%China 21.1% 22.0% 24.7% 29.7% 31.9%other Asia 22.0% 21.2% 20.1% 20.4% 20.5%Rest of World 0.8% 0.8% 0.2% 0.1% 0.3%Total 100.0% 100.0% 100.0% 100.0% 100.0%

2010 2011 2012 2013 20140.0%5.0%

10.0%15.0%20.0%25.0%30.0%35.0%40.0%

IPGP 2010-14 Macro GeoTrends (w/China)

US+NAEuropeChina other AsiaRest of World

IPG

Phot

onics

CompanyThesis Industry RisksValuation

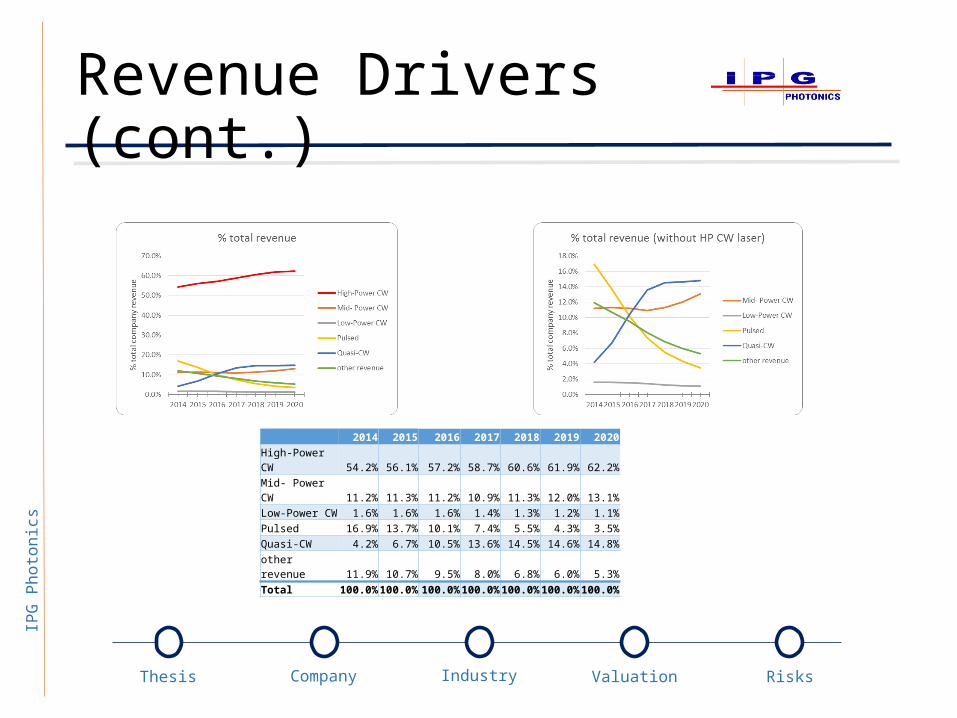

Revenue Drivers (cont.)

2014 2015 2016 2017 2018 2019 2020High-Power CW 54.2% 56.1% 57.2% 58.7% 60.6% 61.9% 62.2%Mid- Power CW 11.2% 11.3% 11.2% 10.9% 11.3% 12.0% 13.1%Low-Power CW 1.6% 1.6% 1.6% 1.4% 1.3% 1.2% 1.1%Pulsed 16.9% 13.7% 10.1% 7.4% 5.5% 4.3% 3.5%Quasi-CW 4.2% 6.7% 10.5% 13.6% 14.5% 14.6% 14.8%other revenue 11.9% 10.7% 9.5% 8.0% 6.8% 6.0% 5.3%Total 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

IPG

Phot

onics

CompanyThesis Industry RisksValuation

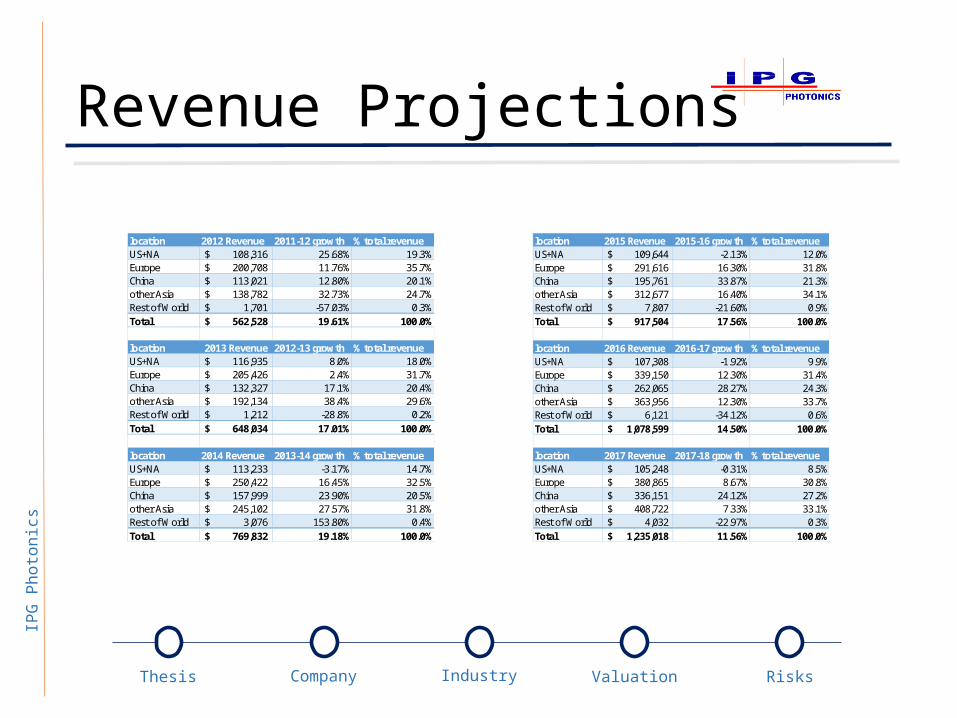

Revenue Projectionslocation 2012 Revenue 2011-12 growth % total revenueUS+NA 108,316$ 25.68% 19.3%Europe 200,708$ 11.76% 35.7%China 113,021$ 12.80% 20.1%other Asia 138,782$ 32.73% 24.7%Rest of World 1,701$ -57.03% 0.3%Total 562,528$ 19.61% 100.0%

location 2013 Revenue 2012-13 growth % total revenueUS+NA 116,935$ 8.0% 18.0%Europe 205,426$ 2.4% 31.7%China 132,327$ 17.1% 20.4%other Asia 192,134$ 38.4% 29.6%Rest of World 1,212$ -28.8% 0.2%Total 648,034$ 17.01% 100.0%

location 2014 Revenue 2013-14 growth % total revenueUS+NA 113,233$ -3.17% 14.7%Europe 250,422$ 16.45% 32.5%China 157,999$ 23.90% 20.5%other Asia 245,102$ 27.57% 31.8%Rest of World 3,076$ 153.80% 0.4%Total 769,832$ 19.18% 100.0%

location 2015 Revenue 2015-16 growth % total revenueUS+NA 109,644$ -2.13% 12.0%Europe 291,616$ 16.30% 31.8%China 195,761$ 33.87% 21.3%other Asia 312,677$ 16.40% 34.1%Rest of World 7,807$ -21.60% 0.9%Total 917,504$ 17.56% 100.0%

location 2016 Revenue 2016-17 growth % total revenueUS+NA 107,308$ -1.92% 9.9%Europe 339,150$ 12.30% 31.4%China 262,065$ 28.27% 24.3%other Asia 363,956$ 12.30% 33.7%Rest of World 6,121$ -34.12% 0.6%Total 1,078,599$ 14.50% 100.0%

location 2017 Revenue 2017-18 growth % total revenueUS+NA 105,248$ -0.31% 8.5%Europe 380,865$ 8.67% 30.8%China 336,151$ 24.12% 27.2%other Asia 408,722$ 7.33% 33.1%Rest of World 4,032$ -22.97% 0.3%Total 1,235,018$ 11.56% 100.0%

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Revenue Projections (cont.)location 2018 Revenue 2018-19 growth % total revenueUS+NA 104,922$ -0.42% 7.6%Europe 413,886$ 4.36% 30.0%China 417,230$ 22.93% 30.3%other Asia 438,681$ 6.10% 31.8%Rest of World 3,106$ -7.89% 0.2%Total 1,377,826$ 10.15% 100.0%

location 2019 Revenue 2019-20 growth % total revenueUS+NA 104,481$ -0.49% 6.9%Europe 431,932$ 2.22% 28.5%China 512,901$ 20.98% 33.8%other Asia 465,441$ 5.34% 30.7%Rest of World 2,861$ -5.68% 0.2%Total 1,517,616$ 9.32% 100.0%

2020 Revenue 2020-21 growth % total revenueUS+NA 103,969$ -0.08% 6.3%Europe 441,521$ 2.05% 26.6%China 620,508$ 18.67% 37.4%other Asia 490,296$ 5.09% 29.6%Rest of World 2,698$ -3.77% 0.2%Total 1,658,991$ 9.02% 100.0%

CAGR: 13.21%

2012 562,528$ Y/Y Growth2013 648,034$ 15.20%2014 769,832$ 18.80%2015 917,504$ 19.18%2016 1,078,599$ 17.56%2017 1,235,018$ 14.50%2018 1,377,826$ 11.56%2019 1,517,616$ 10.15%2020 1,658,991$ 9.32%

Total Revenues

20112012201320142015201620172018201920202021 $-

$500,000 $1,000,000 $1,500,000 $2,000,000

Total Revenue

2012 2013 2014 2015 2016 2017 2018 2019 20200.00%

5.00%

10.00%

15.00%

20.00%

25.00%

YoY growth

IPG

Phot

onics

CompanyThesis Industry RisksValuation

Industry OverviewAcross-board growth of fiber laser market share

The technology leader and most profitable company in the

rapidly growing fiber laser market

Vote: texasusit.org/portfolioVoting opens after DCF Analysis

![STIFF RING SUBFRAME KITstiffring.com/model.pdf · 28 City 6th Gen [GM6] Front - Year 2013 up Front 8 29 City 6th Gen [GM6] Rear - Year 2013 up Rear 2 30 City SX8 3rd Gen [3A2/3A3]](https://static.documents.pub/doc/80x56/60b17914e1c3d51b4d476141/stiff-ring-subframe-28-city-6th-gen-gm6-front-year-2013-up-front-8-29-city-6th.jpg)