41

Going Global – How Much is Enough? William (Bill) H. Hill, RBC Asset Management

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | claud-samuel-harvey |

| View: | 216 times |

| Download: | 1 times |

Going Global – How Much is Enough?

William (Bill) H. Hill, RBC Asset Management

CIFP June 2007 2

What we talked about last year

The importance of investor behaviourUnderstanding it so you can help manage it

The Case for America

International Investing

Our 2006 Outlook

How to keep clients on track

CIFP June 2007 3

What’s changed since last year?

What products are selling today vs. last year

Global Flows$11 Billion to Foreign Equity (International & Global)

$533 million to US Equity

$22 Billion to Balanced Funds

$11 billion in Cdn Equity Fund Redemptions

Product launchesMore than 60 global mandates launched since June 2006

Almost $4 billion in assets in those new funds

CIFP June 2007 4

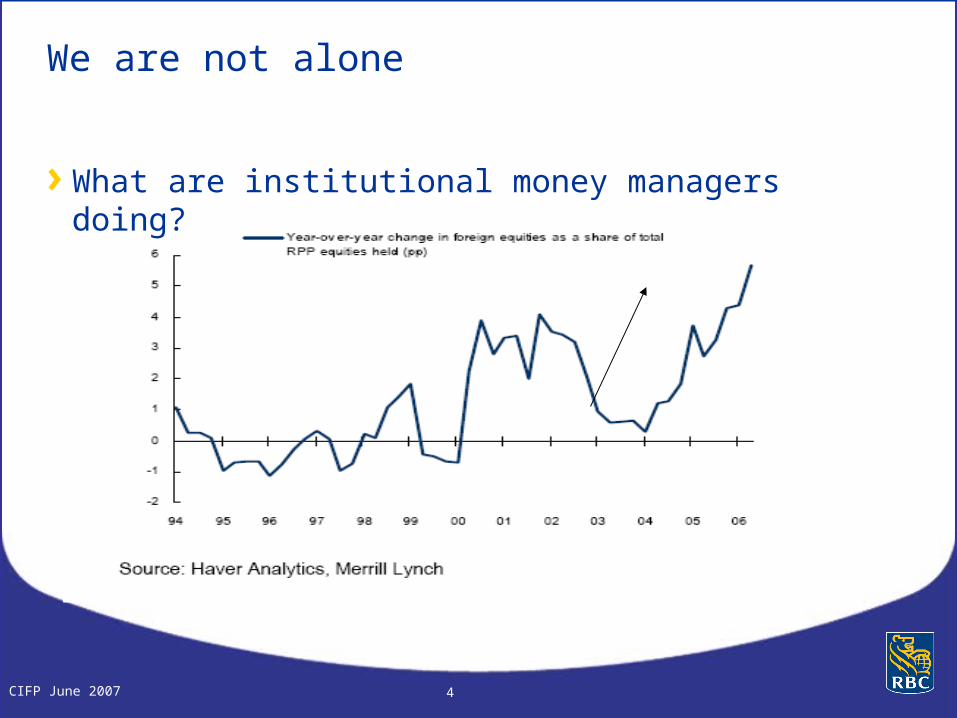

We are not alone

What are institutional money managers doing?

CIFP June 2007 5

What hasn’t changed

Client behaviour

Diversification is still key

Global investing should be the focus

CIFP June 2007 6

Going Global

So how much is enough?

35%

CIFP June 2007 7

Global investing challenges

Knowledge / exposure

Currency

Behavioural

CIFP June 2007 8

Global investing challenges – knowledge/exposure

Where’s Waldo?

Royal Bank of Canada

CIBC

Bank of MontrealCanadian Natural Resources

Suncor Energy

EnCana Corp.

TD Bank

Bank of Nova Scotia

Manulife

Sun Life Financial

Total S.A.

Procter & Gamble

UnitedHealth Group

Groupe Danone

Cemex

CVS Caremark Corp.

BBVA

Continental AG

Atlas Copco

Royal Bank of Scotland Group

CIFP June 2007 9

Global investing challenges – knowledge/exposure

Easier to be more familiar with Cdn / NA companies

Canada

Royal Bank of Canada

Manulife

Bank of Nova Scotia

TD Bank

EnCana Corp.

Suncor Energy

Canadian Natural Resources

Bank of Montreal

CIBC

Sun Life Financial

Which list do your clients know?

RBC Global Titans Fund

CVS Caremark Corp. (US)

Total S.A (France)

Groupe Danone (France)

Procter & Gamble (US)

Cemex (Mexico)

BBVA (Spain)

UnitedHealth Group (US)

Royal Bank of Scotland Group

Continental AG (Germany)

Atlas Copco (Sweden)

CIFP June 2007 10

$161

$357

$168

$319

$98

$465

$131

$416

$-

$100

$200

$300

$400

$500

1990 1995 2000 2005

Canadian Investment Abroad Foreign Investment in Canada

As countries become more economically integrated, global economies are looking beyond their borders for opportunities

Global Investing – The Realities

It’s not only Canadians who are investing more globally. Foreign investors are investing more here too.

CIFP June 2007 11

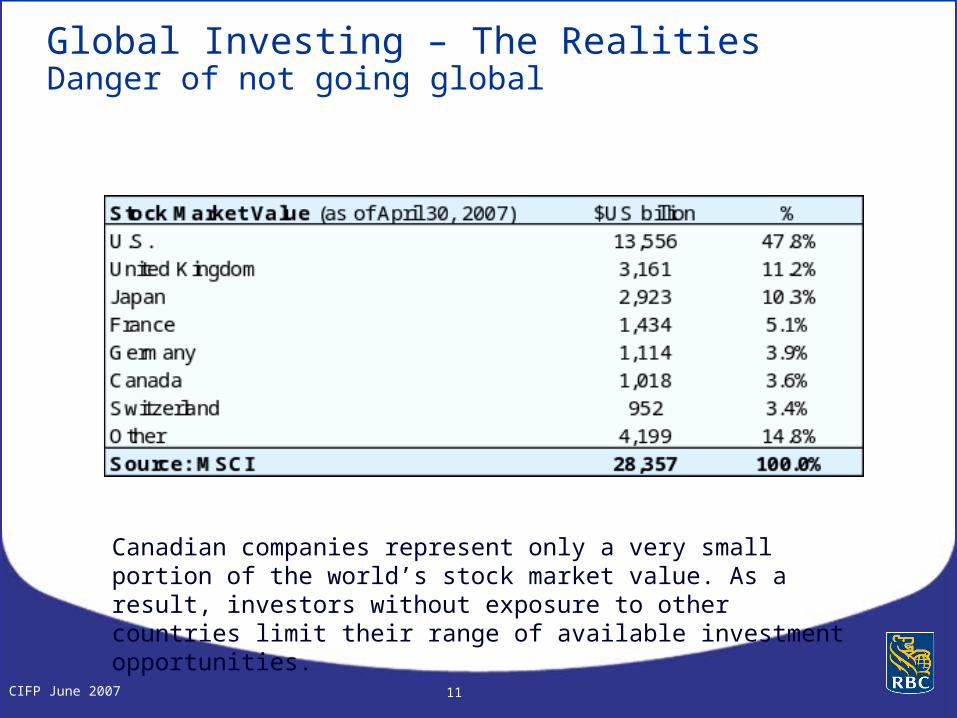

Global Investing – The RealitiesDanger of not going global

Canadian companies represent only a very small portion of the world’s stock market value. As a result, investors without exposure to other countries limit their range of available investment opportunities.

CIFP June 2007 12

Global Investing – The RealitiesCanada only offers exposure to a couple of sectors

Compared to the global economy, Canada’s economy is dominated by Financials and Resources companies.

CIFP June 2007 13

Global investing challenges – Knowledge/exposure

17.3%14.1%

9.7% 9.1%7.3%

4.6%1.3%

Emerging Mkts Canada Germany France U.K. Japan U.S.

Remember, you w ant to position your portfolio for the future - don't get caught looking in the rear view mirror.

Outperfomance of Canadian marketI don’t need to invest anywhere else – look at my amazing returns over the past 5 yrs!

Source: TSX, S&P, MSCI at April 30, 2007

CIFP June 2007 14

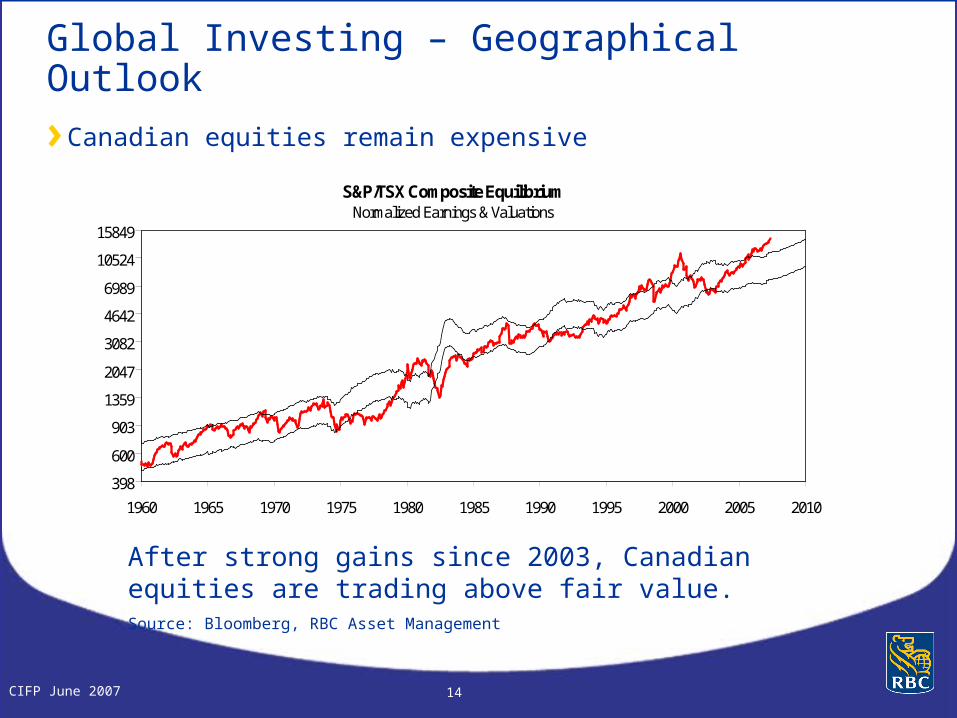

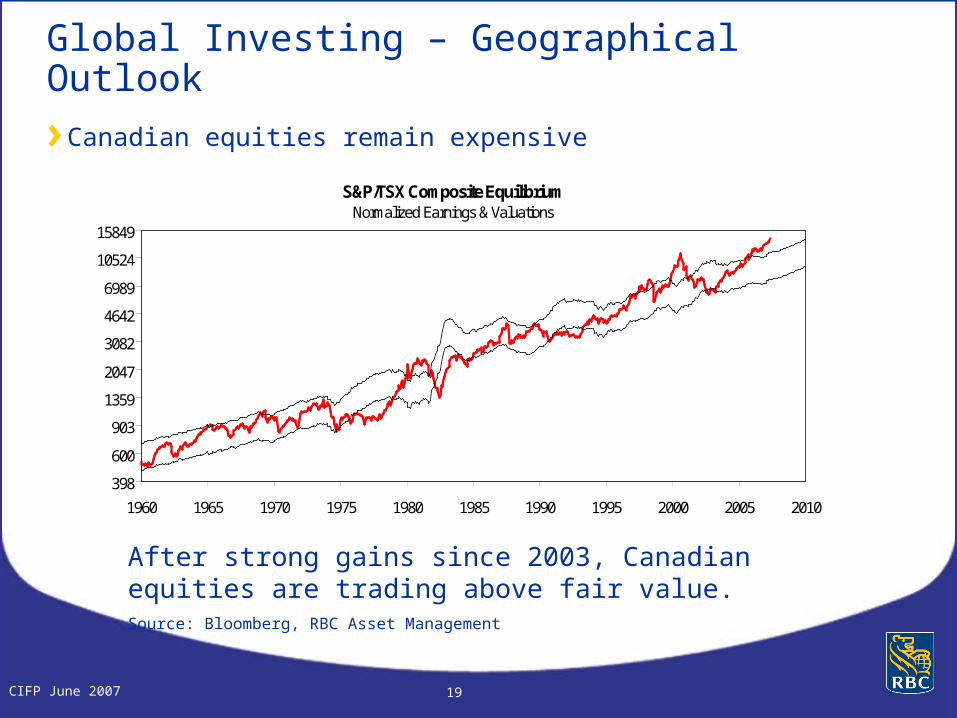

Global Investing – Geographical Outlook

S&P/TSX Composite EquilibriumNormalized Earnings & Valuations

398

600

903

1359

2047

3082

4642

6989

10524

15849

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Source: Bloomberg, RBC AM

May '07 Range: 7696 - 11435 (Mid: 9566)May '08 Range: 8090 - 12022 (Mid: 10056)Current (22-May-07): 14112

Canadian equities remain expensive

After strong gains since 2003, Canadian equities are trading above fair value.Source: Bloomberg, RBC Asset Management

CIFP June 2007 15

Strong upside in Natural Resources for a

prolonged period!

•China driving demand, & just getting started

•India, Russia & Brazil add to pressure

DEMAND

Pressure Increasing

•Underinvestment in exploration &

development for past two decades

•Restrained capital spending due to high costs

relative to commodity prices

SUPPLY

Lagging for awhile

Global Investing – The Realities

The Canada story

CIFP June 2007 16

Across the Huangpu River to Pudong, Shanghai, 1984

CIFP June 2007 17

Across the River Now…

CIFP June 2007 18

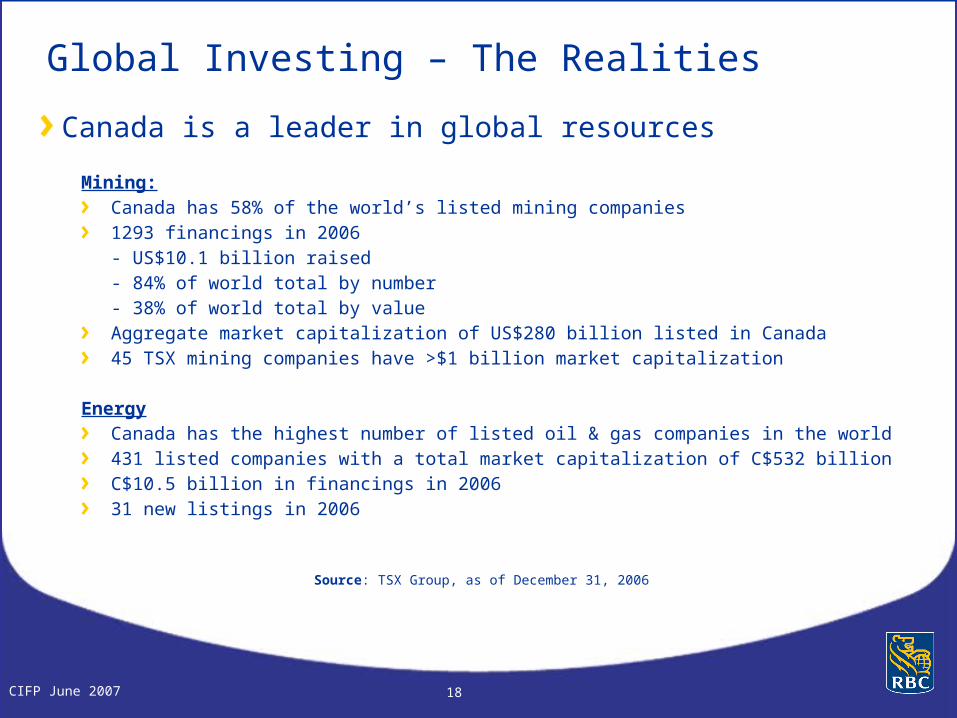

Source: TSX Group, as of December 31, 2006

Mining:Canada has 58% of the world’s listed mining companies 1293 financings in 2006- US$10.1 billion raised- 84% of world total by number- 38% of world total by valueAggregate market capitalization of US$280 billion listed in Canada45 TSX mining companies have >$1 billion market capitalization

EnergyCanada has the highest number of listed oil & gas companies in the world431 listed companies with a total market capitalization of C$532 billionC$10.5 billion in financings in 200631 new listings in 2006

Global Investing – The Realities

Canada is a leader in global resources

CIFP June 2007 19

Global Investing – Geographical Outlook

S&P/TSX Composite EquilibriumNormalized Earnings & Valuations

398

600

903

1359

2047

3082

4642

6989

10524

15849

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Source: Bloomberg, RBC AM

May '07 Range: 7696 - 11435 (Mid: 9566)May '08 Range: 8090 - 12022 (Mid: 10056)Current (22-May-07): 14112

Canadian equities remain expensive

After strong gains since 2003, Canadian equities are trading above fair value.Source: Bloomberg, RBC Asset Management

CIFP June 2007 20

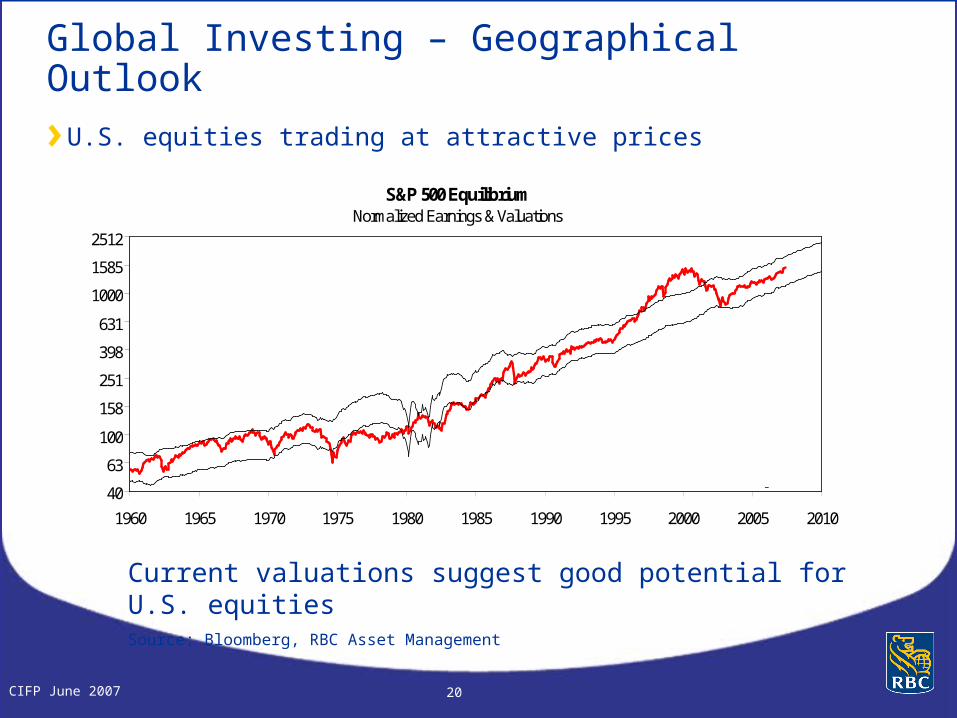

Global Investing – Geographical Outlook

U.S. equities trading at attractive pricesS&P 500 Equilibrium

Normalized Earnings & Valuations

40

63

100

158

251

398

631

1000

1585

2512

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Source: Bloomberg, RBC AM

May '07 Range: 1134 - 1822 (Mid: 1478)May '08 Range: 1245 - 2002 (Mid: 1624)Current (22-May-07): 1524

Current valuations suggest good potential for U.S. equitiesSource: Bloomberg, RBC Asset Management

CIFP June 2007 21

Global Investing – Geographical Outlook

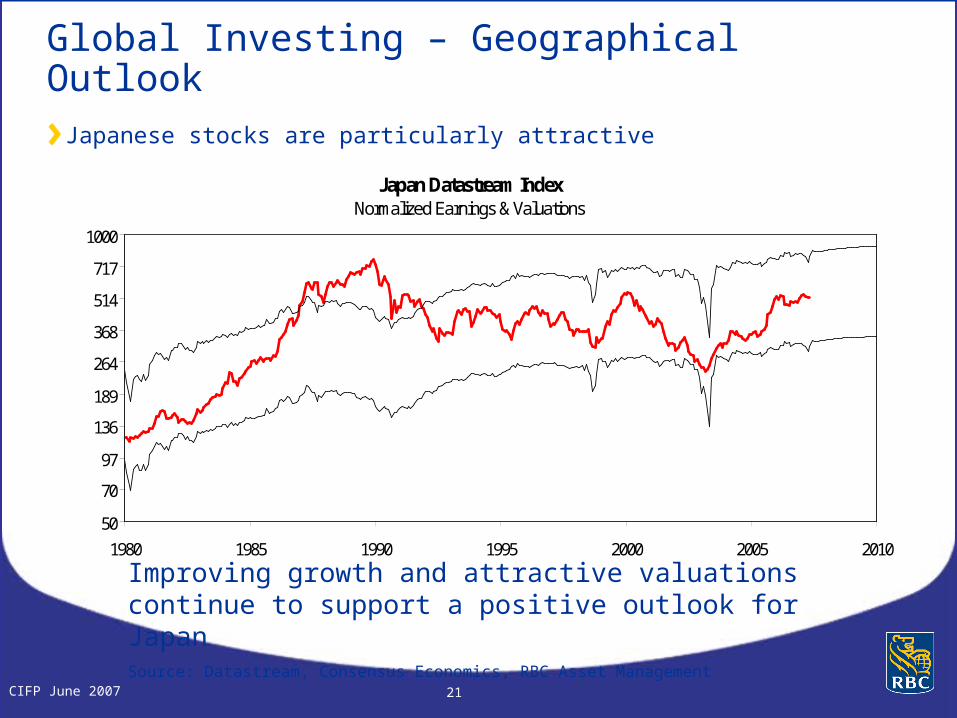

Japanese stocks are particularly attractive

Improving growth and attractive valuations continue to support a positive outlook for JapanSource: Datastream, Consensus Economics, RBC Asset Management

Japan Datastream IndexNormalized Earnings & Valuations

50

70

97

136

189

264

368

514

717

1000

1980 1985 1990 1995 2000 2005 2010

Source: Datastream, Consensus Economics, RBC AM

May '07 Range: 312 - 798 (Mid: 555) May '08 Range: 337 - 861 (Mid: 599)Current (22-May-07): 518

CIFP June 2007 22

Global investing challenges - Currency

0.7%

5.8%9.1%

-6.9%

3.6% 5.4%

-0.6%

-23.4%

-7.6%-3.3%

-0.1%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

In 2003 and 2004, the decline in the U.S. dollar (and rise in the Canadian dollar) had a significant impact on returns for Canadian investors holding U.S dollar securities

Difference in Canadian investor returns and U.S. investor returnsS&P 500 Index

CIFP June 2007 23

Global investing challenges - Behavioural

People see what they want to see.

It’s just the way we’re built…and conditioned.

The size of the bowl or plate biases how much a person eats by an average of 20-30%.

You'll eat 35% more dining with a friend than when eating alone and double the amount of food ingested when dining with 7 or more people.

About 1 in 5 employees have more than 50% of their work-related investment plans in company stock

One third of Canadians have no foreign content in their RRSPs

CIFP June 2007 24

Canadian government bond market is shrinking

-

50

100

150

200

250

300

350

De

c-8

4

De

c-8

5

De

c-8

6

De

c-8

7

De

c-8

8

De

c-8

9

De

c-9

0

De

c-9

1

De

c-9

2

De

c-9

3

De

c-9

4

De

c-9

5

De

c-9

6

De

c-9

7

De

c-9

8

De

c-9

9

De

c-0

0

De

c-0

1

De

c-0

2

De

c-0

3

De

c-0

4

De

c-0

5

De

c-0

6

Go

ve

rnm

en

t B

on

d O

uts

tan

din

g (

CA

D$

bill

ion

)

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

% o

f W

orl

d G

ov

ern

me

nt

Bo

nd

Canadian Govt Bond (CAD$ bil)

Canadian Govt Bond % Global GovtBond (rhs)

Source: Citigroup WGBI

CIFP June 2007 25

The Case For Hedging Global Bonds

Risk (STD)

Return (GM)January 1987 - December 2006

Risk vs. Return

3.0% 10.0%4.0% 5.0% 6.0% 7.0% 8.0% 9.0%5.0%

9.0%

5.2%5.4%5.6%5.8%6.0%6.2%6.4%6.6%6.8%7.0%7.2%7.4%7.6%7.8%8.0%8.2%8.4%8.6%8.8%

Citigroup Canada 1+ Yr Gvt TR

Citigroup Canadian $ Hedged Wld Gvt TR

Citigroup World 1+ Yr Gvt TR CADHedged global bonds have provided better returns at much lower risk levels

Source: RBC Asset Management with data provided by Ibbotson EnCorr

CIFP June 2007 26

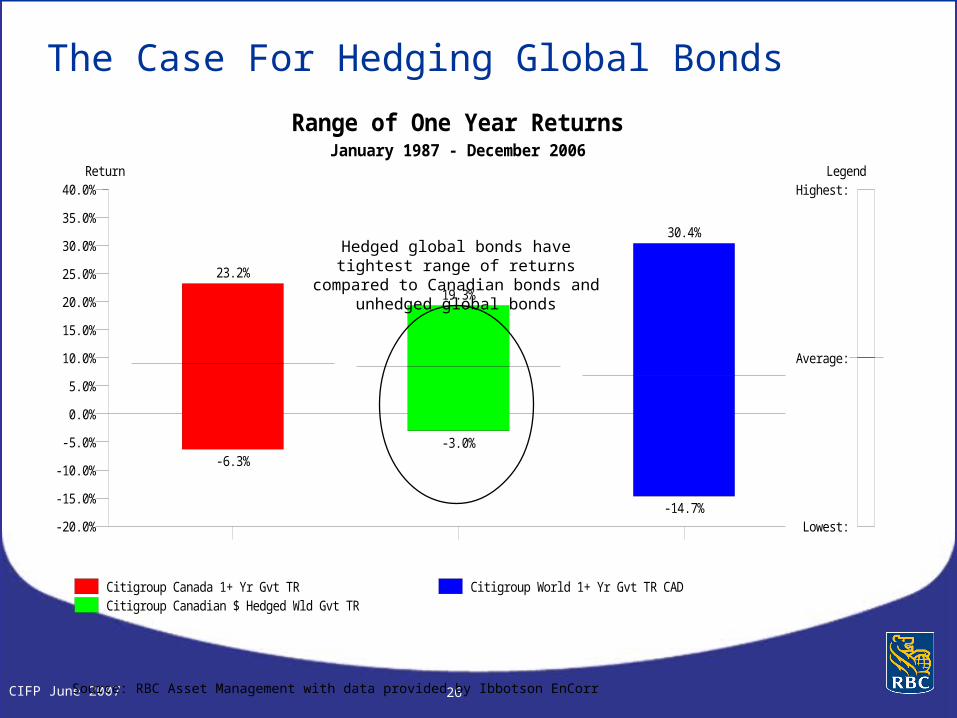

The Case For Hedging Global Bonds

Source: RBC Asset Management with data provided by Ibbotson EnCorr

ReturnJanuary 1987 - December 2006

Range of One Year Returns

-20.0%

40.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

23.2%

-6.3%

19.3%

-3.0%

30.4%

-14.7%

Citigroup Canada 1+ Yr Gvt TRCitigroup Canadian $ Hedged Wld Gvt TR

Citigroup World 1+ Yr Gvt TR CAD

Highest:

Average:

Lowest:

Legend

Hedged global bonds have tightest range of returns compared to Canadian bonds

and unhedged global bonds

CIFP June 2007 27

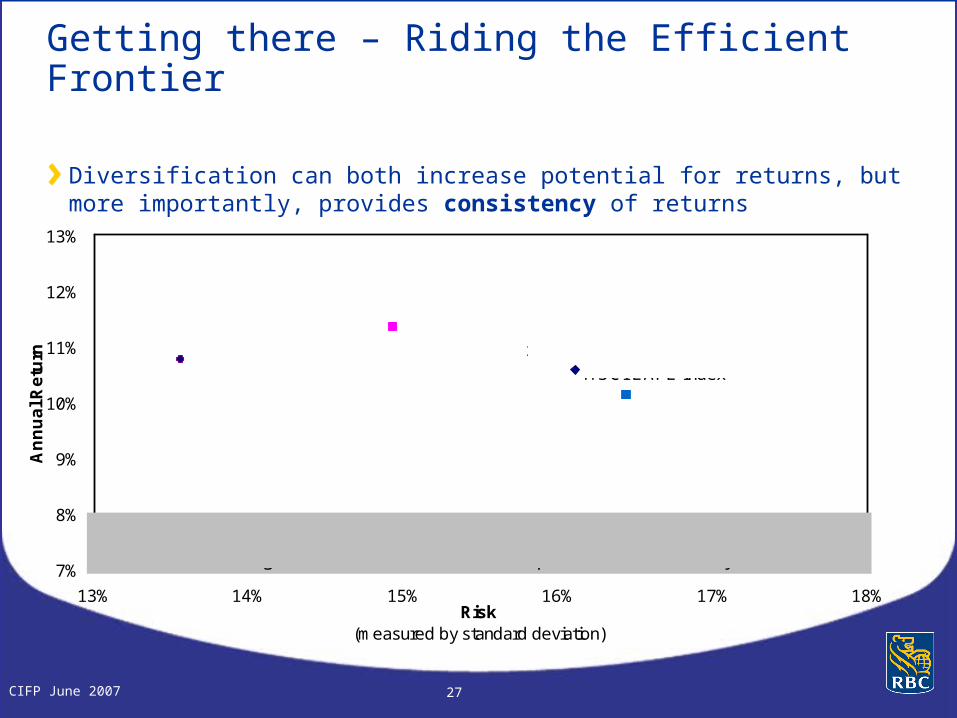

Getting there – Riding the Efficient Frontier

Diversification can both increase potential for returns, but more importantly, provides consistency of returns

7%

8%

9%

10%

11%

12%

13%

13% 14% 15% 16% 17% 18%Risk

(measured by standard deviation)

An

nu

al R

etu

rn

Canadian EquitiesS&P / TSX Composite Index

International Equities MSCI EAFE Index

U.S. EquitiesS&P 500 Index

A combination of Canadian, U.S. and International equities has historically provided investors with higher returns and less risk than a portfolio invested solely in Canada.

Diversified Portfolio40% Canada40% U.S.20% International

CIFP June 2007 28

How much is enough?

Criteria to considerInvestor characteristics – risk and return

Currency needs – income, expenses, retirement

Risk management – diversification benefits

Your own asset mix approachFamiliarity with client situation and needs

Your style – prefer standalone funds or managed solutions?

Level of ongoing involvement – rebalancing requirements

CIFP June 2007 29

How much is enough?

What is the RBC Asset Management approach?

RBC Investment Strategy CommitteeFirm wide asset allocation recommendations

Investor profile recommendationsBased on strategy committee recommendations

Implementation in investor portfoliosModel portfolios, fund-of-funds

CIFP June 2007 30

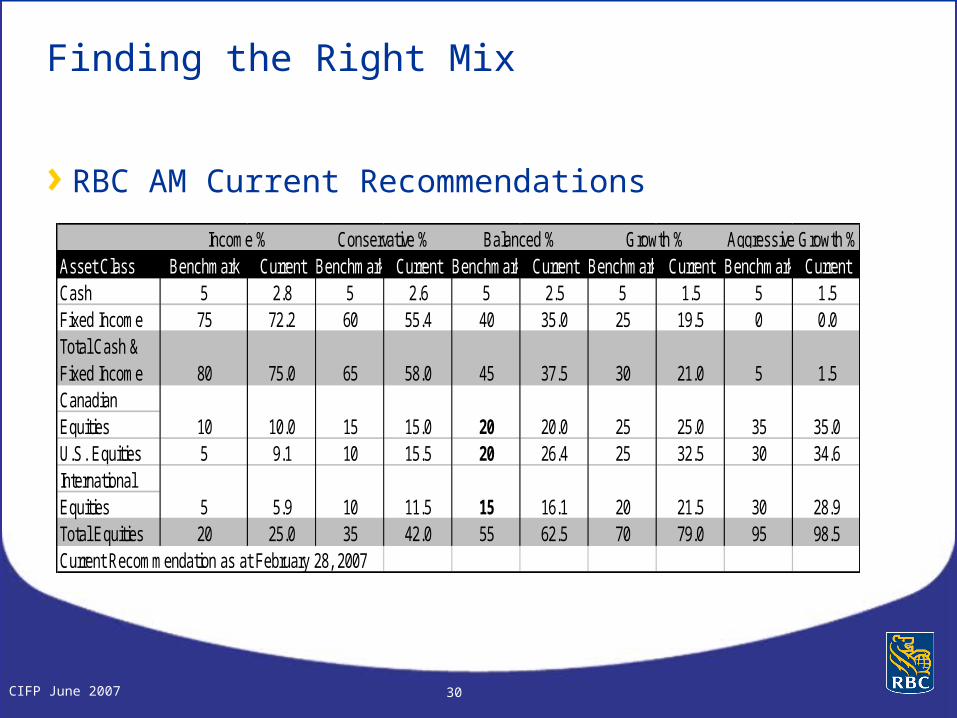

Finding the Right Mix

RBC AM Current Recommendations

Asset Class Benchmark Current Benchmark Current Benchmark Current Benchmark Current Benchmark CurrentCash 5 2.8 5 2.6 5 2.5 5 1.5 5 1.5Fixed Income 75 72.2 60 55.4 40 35.0 25 19.5 0 0.0Total Cash &Fixed IncomeCanadianEquitiesU.S. Equities 5 9.1 10 15.5 20 26.4 25 32.5 30 34.6InternationalEquitiesTotal Equities 20 25.0 35 42.0 55 62.5 70 79.0 95 98.5Current Recommendation as at February 28, 2007

Aggressive Growth %

21.0

25.0

Income % Conservative % Balanced % Growth %

5

35

30

1.5

35.0

28.9

30

25

20 21.5

45

20

15

37.5

20.0

16.1

80

10

5

75.0

10.0

5.9

65

15

10

58.0

15.0

11.5

CIFP June 2007 31

And now for the HOW…

Individual securities

ETFs

Individual funds

Fund of Funds

Combination of all of the above

32CIFP June 2007 32

Trade Execution

Diversification

Managing Currency

Access to research

Reporting

Challenges involved with investing in global segregated securities

Global Investing – Additional Challenges

CIFP June 2007 33

Global Investing – The Realities

Challenges identified: currency, execution, fixed income, are all difficult to take on as an individual investor…

But can be efficiently and effectively managed through mutual funds

Funds even help manage behavioural challengesStaying investedNot chasing performanceRebalancingdiversification

CIFP June 2007 34

One way or another

Different solutions can mean very different results

CIFP June 2007 35

Clients Succeed with Packaged Solutions

15.714.7

11.69.6

-3.8 -5.1

200220042003

Self-directed Investors in 401 k Investor in "Premixed Funds" in 401k

“Premixed Funds” target date and target risk funds/ portfolios

Source: Hewitt Associates, January 2006

Money Magazine, October 2006

Good for you…and good for them.

CIFP June 2007 36

If you’re looking at mutual funds, here are some things to consider when hiring an asset management company

… always important investment considerations but especially critical for a global strategy

CIFP June 2007 37

Value

Experienced managers

Consistent discipline

Track record of performance

Value for moneyA shop that can deliver:

Global opportunities through global footprint

Currency experience and expertise– Size and scale enables us to have dedicated team

Trading execution excellence

CIFP June 2007 38

Choice

Broad spectrum of fundsGlobalInternationalRegionalSectorStyleCurrency hedged or un-hedged options

Single fund or portfolio solution

Purchase options to suit client needs and advisor style

CIFP June 2007 39

Transparency

Know what you’re getting

The importance of clear investment mandates in portfolio construction

Confidence that a fund will do what it says it’s going to do

Are Canadian equity funds truly Canadian?

Apples to apples comparisons becoming difficult

The importance of clear, predictable fees

CIFP June 2007 40

Success

Serious about ours

Committed to yours

CIFP June 2007 41

Disclosure

The information contained in this report has been compiled by RBC Asset Management Inc. (“RBC AM”) from sources believed to be reliable, but no representations or warranty, express or implied, are made by RBC AM, its affiliates or any other person as to its accuracy, completeness or correctness. All opinions and estimates contained in this report constitute RBC AM’s judgement as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. This report may not be reproduced, distributed or published without the written consent of RBC Asset Management.To the full extent permitted by law neither RBC AM nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. Past performance does not indicate future performance.RBC Asset Management Inc. provides global wealth management services. RBC Asset Management Inc. and Royal Bank of Canada are separate corporate entities, which are affiliated. ® Registered trademark of Royal Bank of Canada. Used under license. © Copyright 2007. All rights reserved.