29

© 2014 Eaton. All Rights Reserved.. Goldman Sachs Industrials Conference 2014 Alexander M. Cutler – Chairman and Chief Executive Officer November 12, 2014

© 2014 Eaton. All Rights Reserved..

Goldman Sachs Industrials Conference 2014

Alexander M. Cutler – Chairman and Chief Executive Officer

November 12, 2014

2 © 2014 Eaton. All Rights Reserved..

Forward-looking statements and non-GAAP financial information

This presentation or the comments we make today may contain forward-looking statements concerning the fourth quarter 2014 operating earnings per share, full-year 2014 operating earnings per share and net income per share, sales, bookings, margins, foreign exchange rates, cash flow, tax rate, acquisition synergies, divestitures, cost control measures and the performance of our worldwide markets. These statements should be used with caution and are subject to various risks and uncertainties, many of which are outside the company’s control. The following factors could cause actual results to differ materially from those in the forward-looking statements: unanticipated changes in the markets for the company’s business segments; unanticipated downturns in business relationships with customers or their purchases from us; competitive pressures on sales and pricing; increases in the cost of material and other production costs, or unexpected costs that cannot be recouped in product pricing; the introduction of competing technologies; unexpected technical or marketing difficulties; unexpected claims, charges, litigation or dispute resolutions; strikes or other labor unrest; the performance of recent acquisitions; unanticipated difficulties integrating acquisitions; new laws and governmental regulations; interest or tax rate changes; stock market and currency fluctuations; and unanticipated deterioration of economic and financial conditions in the United States and around the world. We do not assume any obligation to update these forward-looking statements. This presentation includes certain non-GAAP measures as defined by SEC rules. A reconciliation of those measures to the most directly comparable GAAP equivalent is provided in the investor relations section of our website at www.eaton.com.

3 © 2014 Eaton. All rights reserved.

Eaton – A Premier Power Management Company

• A balanced power management company

• Cooper acquisition creates a leading Electrical franchise

• Industrial businesses are well positioned for growth

• Summary and guidance

4 © 2014 Eaton. All rights reserved.

Eaton is a leading global power management company…

Uniquely positioned to provide safe, reliable, efficient and sustainable power management solutions for our global customers

Electrical Fluid Mechanical

Cities & Buildings

Industrial & Machinery

Information Technology

Energy & Utilities

Transportation Infrastructure

5 © 2014 Eaton. All rights reserved.

…consisting of premier power management franchises

• Among the four largest global Electrical companies, with the scale and scope to compete globally

• Comprehensive solutions from generation to the end user, with a portfolio of leading brands

• Serving key markets including oil & gas, industrial, utility, commercial & residential construction, machinery and data centers

• Hydraulics business that is among the three largest globally and serves a wide range of mobile and industrial customers

• Aerospace business serving global OEMs, airlines, and militaries with hydraulic power & motion control, fluid conveyance, fuel and engine solutions

• Vehicle business delivering solutions to the global commercial vehicle and passenger car markets focused on fuel efficiency, emissions and safety

ELECTRICAL INDUSTRIAL

2013 Sales: $13.5B 2013 Sales: $8.6B

6 © 2014 Eaton. All rights reserved.

We have created a portfolio capable of delivering stronger growth and more consistent earnings

61% 14%

8%

17%

2013 Segment Sales

Electrical Hydraulics

Aerospace Vehicle

50%

26%

24%

2013 Sales by Destination

U.S.Int'l DevelopedInt'l Emerging

29%

29%

31%

11%

2013 Cycle Sales

Early Mid Late No

7 © 2014 Eaton. All rights reserved.

Our results over the last decade reflect the successful execution of our transformation strategy

Sales

Elec / Hyd /Aero sales

Segmentmargins

Operatingcash flow

$22B

$8B

2013 2003

OperatingEPS

11% CAGR

$18B

$5B

$2.3B

$0.9B

$4.13

$1.36

12% CAGR

We are driving higher growth, profitability, and consistency

Internationalsales

Gro

wth

M

ix

Perf

orm

ance

3.7 times

2.6 times + 470 bps

3.6 times

14.9%

10.2%

$11B

$3B

8 © 2014 Eaton. All rights reserved.

Our dividend yield has been a major driver of our strong shareholder returns…

Total Shareholder Returns 2000 – Oct 31, 2014

3.7x

6.0x

2.3x

0x

1x

2x

3x

4x

5x

6x

7x

ShareAppreciation

Dividends TotalShareholder

Returns

0%

1%

1%

2%

2%

3%

3%

4%

4%

DB

:SIE

AB

B SU ETN

EMR LR U

TX

HO

N

ITW

RO

K

DO

V

PH IR

DH

R

Dividend Yield As of Oct 31, 2014*

* Eaton dividend yield reflects a quarterly dividend of $0.49/share

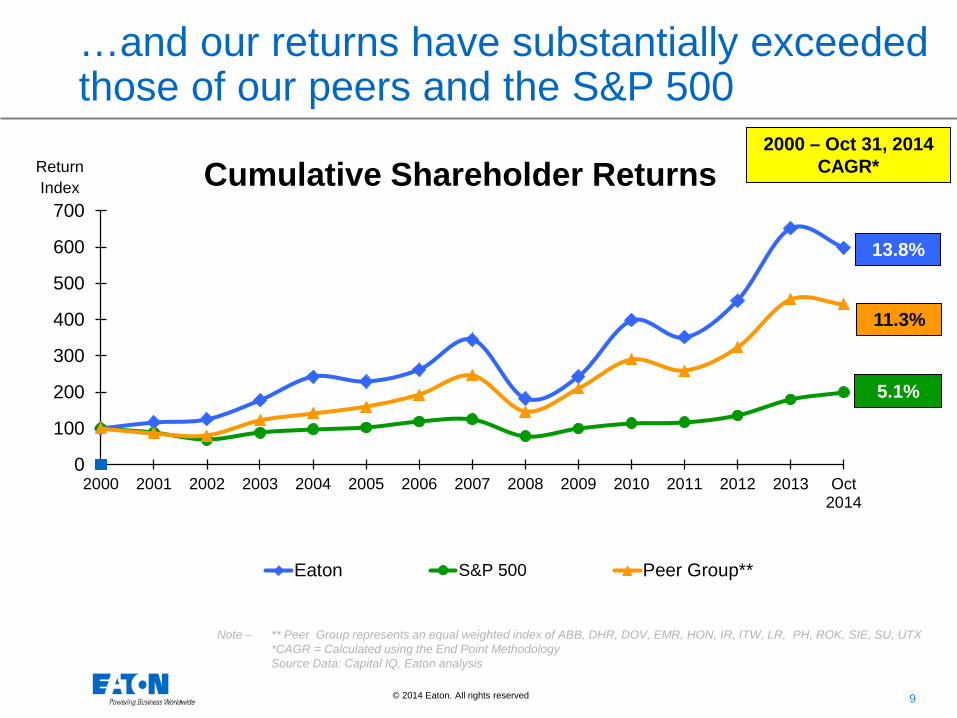

9 © 2014 Eaton. All rights reserved.

2000 – Oct 31, 2014 CAGR* Return

Index

13.8%

Note – ** Peer Group represents an equal weighted index of ABB, DHR, DOV, EMR, HON, IR, ITW, LR, PH, ROK, SIE, SU, UTX *CAGR = Calculated using the End Point Methodology Source Data: Capital IQ, Eaton analysis

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Oct2014

Cumulative Shareholder Returns

Eaton S&P 500 Peer Group**

11.3%

5.1%

…and our returns have substantially exceeded those of our peers and the S&P 500

10 © 2014 Eaton. All rights reserved.

Eaton – A Premier Power Management Company

• A balanced power management company

• Cooper acquisition creates a leading Electrical franchise

• Industrial businesses are well positioned for growth

• Summary and guidance

11 © 2014 Eaton. All Rights Reserved.

The Cooper acquisition significantly expanded our electrical solutions

Legacy Eaton

Former Cooper

Data Centers Industrial Utility Commercial / Residential Machinery

12 © 2014 Eaton. All Rights Reserved.

We are balanced both geographically and across key market segments Electrical Geographic Mix

2013 Sales $13.5B

U.S. 54%

Non-U.S. 46%

Electrical End Market Mix 2013 Sales $13.5B

Data Center / IT

17%

Resi 9%

Non-resi 30%

Industrial 32%

Utility 12%

13 © 2014 Eaton. All rights reserved.

0

100

200

300

400

500

2013 2014 2015 2016

Syne

rgy

Prof

it ($

M)

Current Plan Original Plan

$115

$210

$360

Cooper synergies continue to exceed our initial expectations

We have clear line-of-sight to realizing an additional $95M synergies in 2014 and another $150M in 2015. In February we increased 2015 and 2016 synergies by $10M and $35M, respectively.

$475

$15

$35

$80

$150

$100 $175

$280 $325

$75

$175

$310

$375

Original Synergy Estimates Profits from Revenue Synergies Cost Synergies

Current Synergy Estimates

14 © 2014 Eaton. All Rights Reserved.

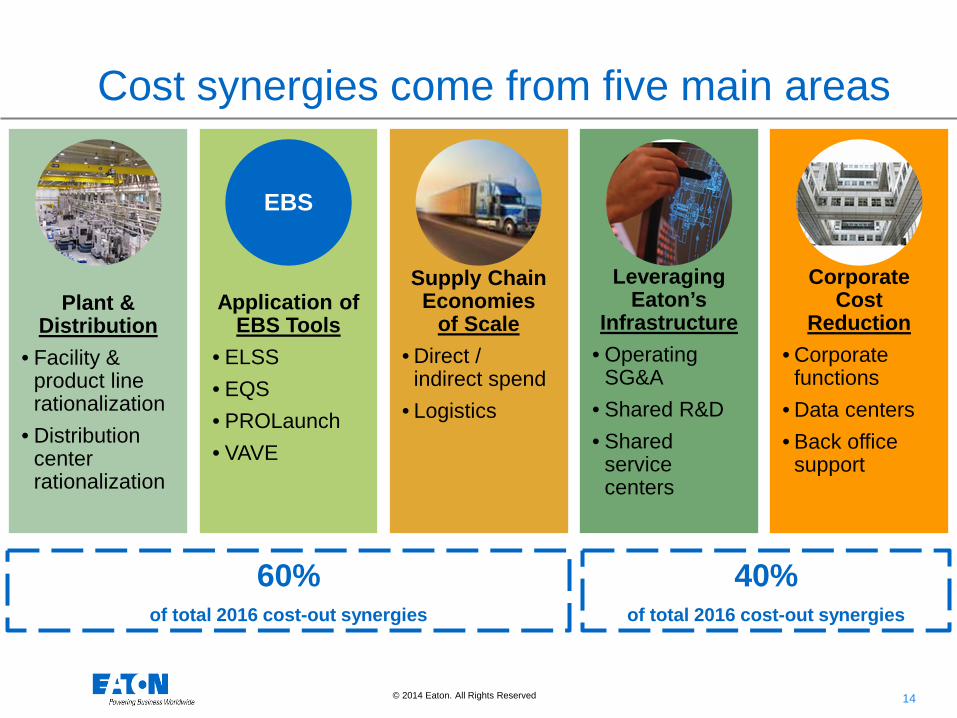

Corporate Cost

Reduction • Corporate

functions • Data centers • Back office

support

Plant & Distribution

• Facility & product line rationalization

• Distribution center rationalization

Application of EBS Tools

• ELSS • EQS • PROLaunch • VAVE

Supply Chain Economies

of Scale • Direct /

indirect spend • Logistics

Leveraging Eaton’s

Infrastructure • Operating

SG&A • Shared R&D • Shared

service centers

Cost synergies come from five main areas

EBS

60% of total 2016 cost-out synergies

40% of total 2016 cost-out synergies

15 © 2014 Eaton. All Rights Reserved.

Sales synergies come from four main areas

Geographic Expansion

• Pull-through opportunities

• Greater scale opportunities

Boost Channel

Sales • Distributor

conversion • Increased

penetration

Larger Package to Common Customers

• Oil & Gas • Data Centers • Mining • Utility

Service

Business • Large Cooper

installed base & relationships

• Leverage Eaton’s existing service business

70% of total 2016 sales synergies

30% of total 2016 sales synergies

16 © 2014 Eaton. All rights reserved.

Eaton – A Premier Power Management Company

• A balanced power management company

• Cooper acquisition creates a leading Electrical franchise

• Industrial businesses are well positioned for growth

• Summary and guidance

17 17 © 2014 Eaton. All rights reserved.

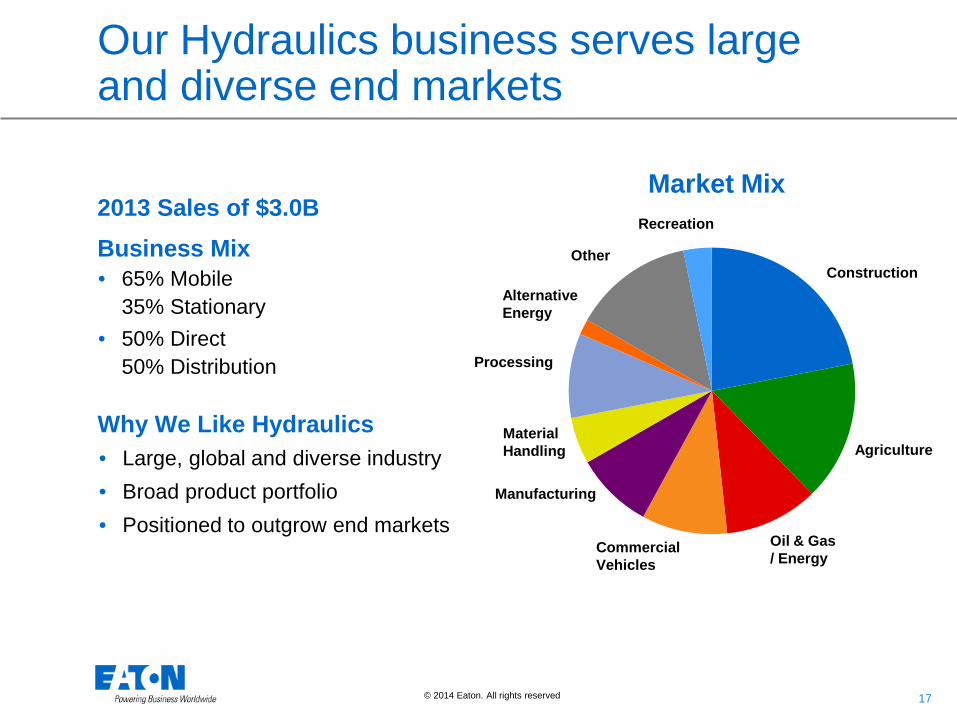

Our Hydraulics business serves large and diverse end markets

• 65% Mobile 35% Stationary

• 50% Direct 50% Distribution

2013 Sales of $3.0B Business Mix

Market Mix

• Large, global and diverse industry • Broad product portfolio • Positioned to outgrow end markets

Why We Like Hydraulics

Construction

Agriculture

Oil & Gas / Energy

Commercial Vehicles

Manufacturing

Material Handling

Processing

Other

Recreation

Alternative Energy

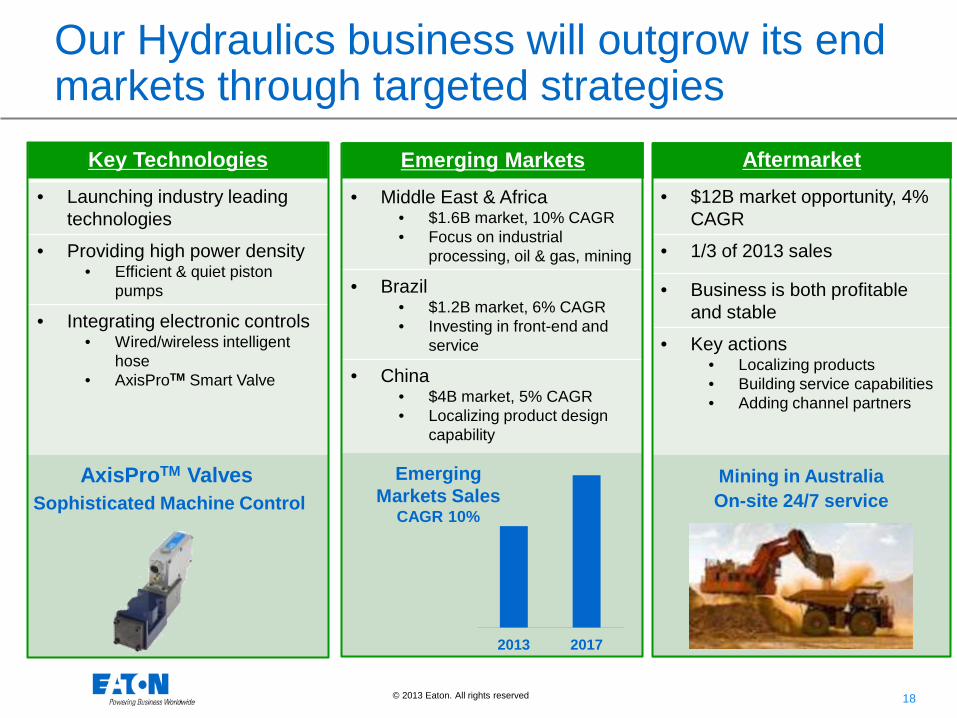

18 18 © 2013 Eaton. All rights reserved.

Aftermarket • $12B market opportunity, 4%

CAGR

• 1/3 of 2013 sales

• Business is both profitable and stable

• Key actions • Localizing products • Building service capabilities • Adding channel partners

Emerging Markets • Middle East & Africa

• $1.6B market, 10% CAGR • Focus on industrial

processing, oil & gas, mining

• Brazil • $1.2B market, 6% CAGR • Investing in front-end and

service

• China • $4B market, 5% CAGR • Localizing product design

capability

Key Technologies • Launching industry leading

technologies

• Providing high power density • Efficient & quiet piston

pumps

• Integrating electronic controls • Wired/wireless intelligent

hose • AxisProTM Smart Valve

Our Hydraulics business will outgrow its end markets through targeted strategies

Sophisticated Machine Control AxisProTM Valves

2013 2017

Emerging Markets Sales

CAGR 10%

Mining in Australia On-site 24/7 service

19 19 © 2014 Eaton. All rights reserved.

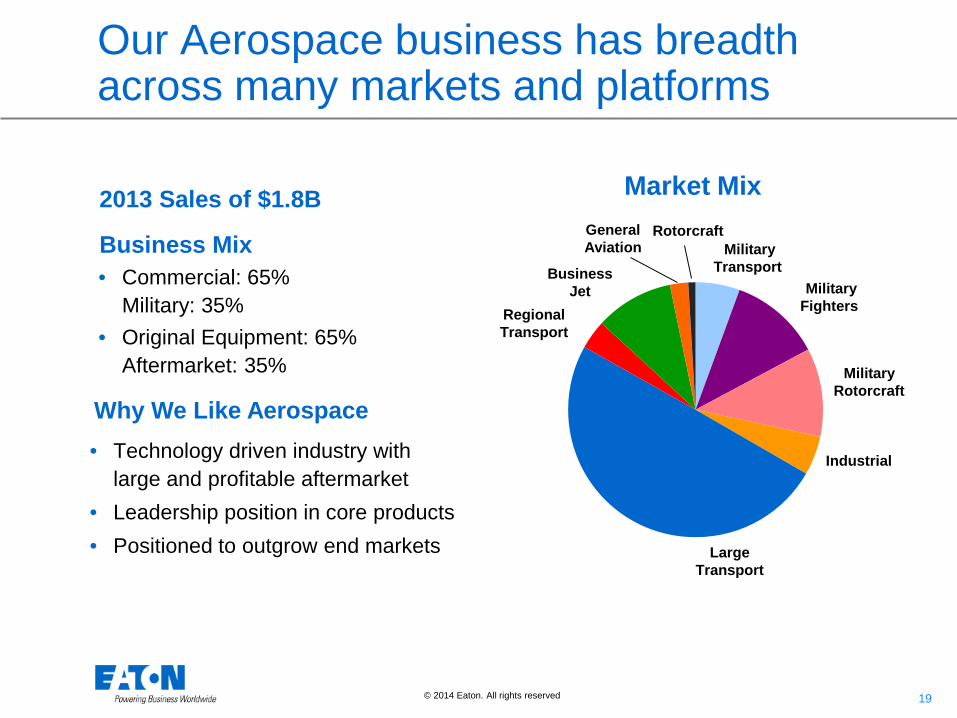

Our Aerospace business has breadth across many markets and platforms

• Commercial: 65% Military: 35%

• Original Equipment: 65% Aftermarket: 35%

2013 Sales of $1.8B

Business Mix

• Technology driven industry with large and profitable aftermarket

• Leadership position in core products • Positioned to outgrow end markets

Why We Like Aerospace

Market Mix Rotorcraft

Military Fighters

General Aviation Military

Transport

Military Rotorcraft

Large Transport

Regional Transport

Business Jet

Industrial

20 20 © 2013 Eaton. All rights reserved.

The Aerospace business is focused on three strategies to drive market outgrowth

Reliable Technologies • Investing in smart

components, materials and power density

• Best-in-class high pressure, dual-stage gear fuel pump

• Industry-leading hydraulic motor pumps

Systems Expertise • Offering integrated sub-

systems • Program management,

systems engineering, prototyping, testing labs

• Zonal “power on demand” hydraulics with lower power consumption

• Advanced hydraulic systems reduce weight by 5%

Aftermarket • $5B installed base

• Investing in aftermarket business unit

• Aligned with key segments • Improved response time

• Providing lower operating cost and service life extensions

• Focused on opportunities in both commercial and military markets

Industry’s Most Reliable Hydraulic Systems Motor Pumps

• $400M win on Embraer E2 • Up to 3x more reliable

Engine Build Up • $425M win on Rolls Royce Trent 97K

XWB engine • Optimized fuel, hydraulic and

air conveyance sub-systems

Aftermarket Sales 4% CAGR

2013 2017

21 21 © 2014 Eaton. All rights reserved.

Our Vehicle business provides targeted solutions for both commercial and passenger vehicle markets

Pickup and Delivery

• Americas: 68% • EMEA: 22% • APAC: 10%

2013 Sales of $3.8B

Business Mix

Market Mix

• Regulations create large opportunities for innovation

• Leader in fuel economy and emissions reduction

• Positioned to outgrow end markets

Why We Like Vehicle

Line Haul

Vocational

Passenger

Ag / Off Highway

Other

22 22 © 2013 Eaton. All rights reserved.

The Vehicle business is focused on three drivers of market outgrowth

Engine Technologies • Engine technology to

improve fuel economy and reduces emissions

• $9B engine-boosting market growing at 13% CAGR

• $5B valvetrain market growing at 4% CAGR

• Ward’s 10 Best Engines, 6 include Eaton

Automated Transmissions • $7B heavy-duty transmission

market growing at 6% CAGR

• Industry-leading technology saves fuel

• FullerAdvantage saves 2% in line haul segment

• UltraShift PLUS up to 19% on vocational trucks

• SmartAdvantage up to 6% in line haul segment

• Automation expected to grow to 30% of global market

Medium-Duty Market • $4B medium-duty market

growing at 6% CAGR

• Positioning our portfolio to expand global presence in pick-up & delivery and bus segments

• Dual clutch technology offers:

• 8-10% improved fuel economy

• Enhanced low-speed maneuverability

HD 1.8M

MD 1.6M

Global Commercial Vehicle Market (units)

25303540455055

2011

2015

2019

2023

CAFÉ Standards

for Automakers

(MPG)

23 © 2014 Eaton. All rights reserved.

Eaton – A Premier Power Management Company

• A balanced power management company

• Cooper acquisition creates a leading Electrical franchise

• Industrial businesses are well positioned for growth

• Summary and guidance

24 © 2014 Eaton. All rights reserved.

Strong cash flow and a stronger balance sheet provide future financial flexibility

Nea

r-ter

m

Long

er-te

rm

Capital Allocation Plans

Repurchase shares if we become overcapitalized or there is an opportunity to buy the shares at a sudden discount… …we have repurchased $2.0B in the last 10 years

Invest in acquisitions which advance our strategy and return at least 300 bps over our cost of capital… …expect to have capacity to ramp up acquisition program in 2015

Reinvest in the business to drive organic growth… …invest 3% of sales annually in capital expenses

Return cash to shareholders with a growing dividend… …grow dividends in line with earnings growth

Retire debt to strengthen our balance sheet… …in 2012 we committed to repaying $2.1B of term debt by 2016, with $1B remaining in 2015 and $240M in January of 2016

25 © 2014 Eaton. All Rights Reserved..

Summary of Q3 Results

• Record segment margins of 16% as productivity and effective cost control drove better-than-guidance performance in Q3

• Record free cash flow of $801M, adjusted for legal settlements, is 14% of sales

• Q4 market conditions are expected to be largely unchanged from Q3

• Full year 2014 operating EPS up 11% over 2013, in a year with modest 2% market growth

26 © 2014 Eaton. All Rights Reserved..

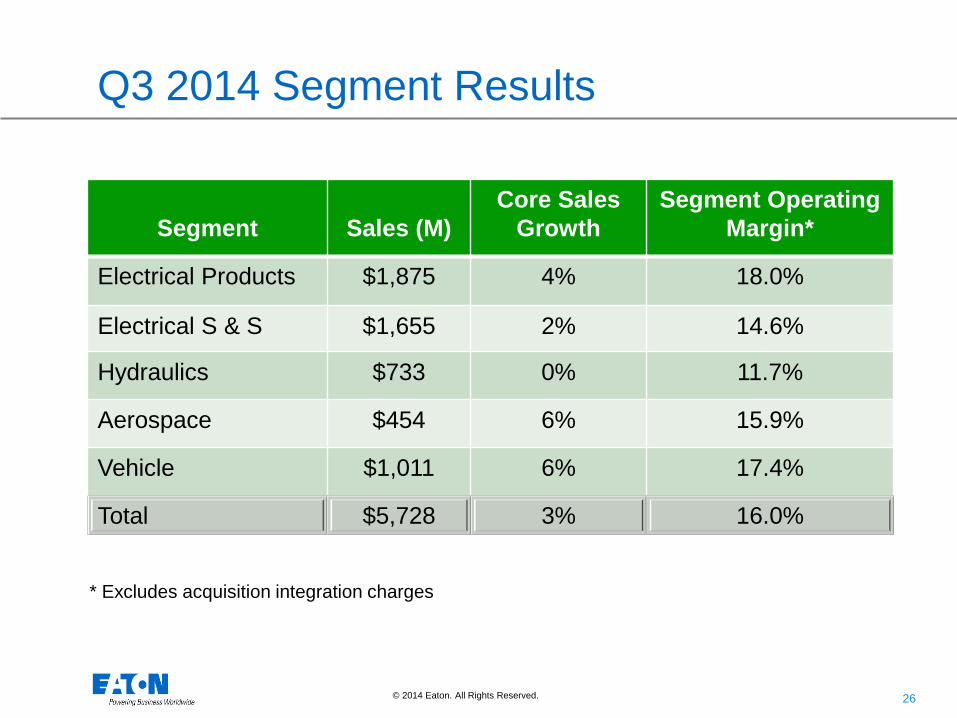

Q3 2014 Segment Results

Segment

Sales (M)

Core Sales Growth

Segment Operating Margin*

Electrical Products $1,875 4% 18.0%

Electrical S & S $1,655 2% 14.6%

Hydraulics $733 0% 11.7%

Aerospace $454 6% 15.9%

Vehicle $1,011 6% 17.4%

Total $5,728 3% 16.0%

* Excludes acquisition integration charges

27 © 2014 Eaton. All Rights Reserved..

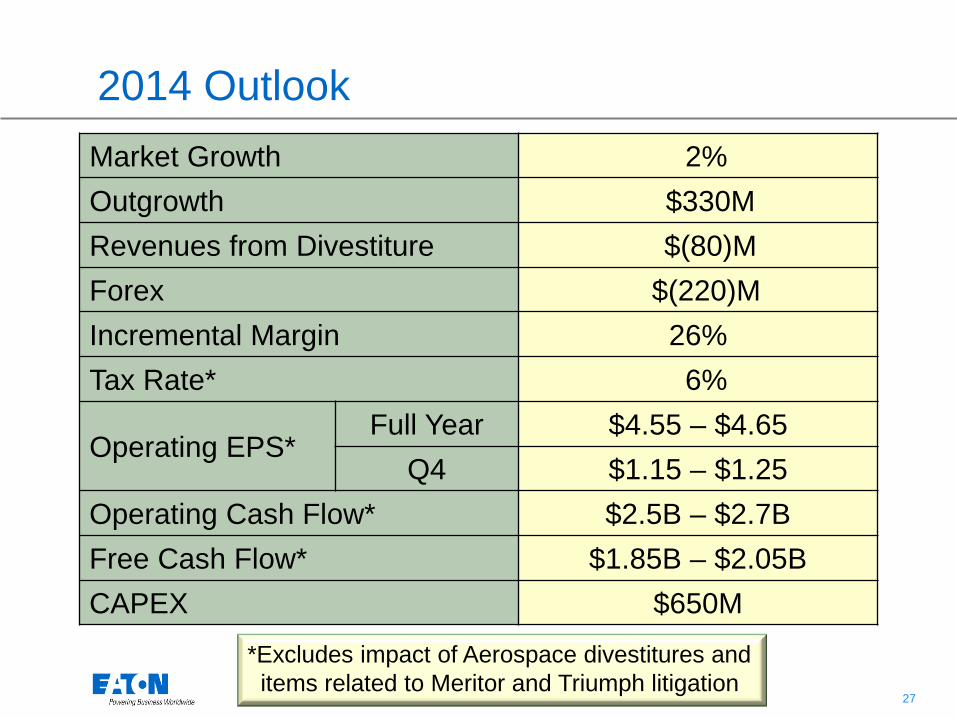

2014 Outlook Market Growth 2% Outgrowth $330M Revenues from Divestiture $(80)M Forex $(220)M Incremental Margin 26% Tax Rate* 6%

Operating EPS* Full Year $4.55 – $4.65

Q4 $1.15 – $1.25 Operating Cash Flow* $2.5B – $2.7B Free Cash Flow* $1.85B – $2.05B CAPEX $650M

*Excludes impact of Aerospace divestitures and items related to Meritor and Triumph litigation

28 © 2014 Eaton. All Rights Reserved..

Initial 2015 Outlook

• Market growth expected to be similar to 2014

• Incremental Cooper synergies of $150M

• Expected benefits of $35M in 2015 from Q2 2014 restructuring in Industrial Sector

• Tax rate expected to increase from 6% in 2014 to 9%-11% in 2015

• By mid-year 2015, expect to have significant and growing available cash to deploy

29 © 2014 Eaton. All rights reserved.