6

1t Disc,ussion Materials Goldman Sachs Capital partners April {5, 2003 not lnclude the tdentry ol the padtes hereto or the,r respeAive aninat*, PROPRIETARY AND CONFIDENTIAL n a ldm ells

8/8/2019 GoldmanSachs Materials

http://slidepdf.com/reader/full/goldmansachs-materials 1/6

1t

Disc,ussion

Materials

Goldman

Sachs

Capital

partners

April

{5,

2003

not

lnclude the

tdentry

ol the

padtes

hereto

or

the,r respeAive

aninat*,

PROPRIETARY

AND

CONFIDENTIAL

n

a

ldm

ells

8/8/2019 GoldmanSachs Materials

http://slidepdf.com/reader/full/goldmansachs-materials 2/6

PROPRIETARY

AND

CONFI

DENTIAL

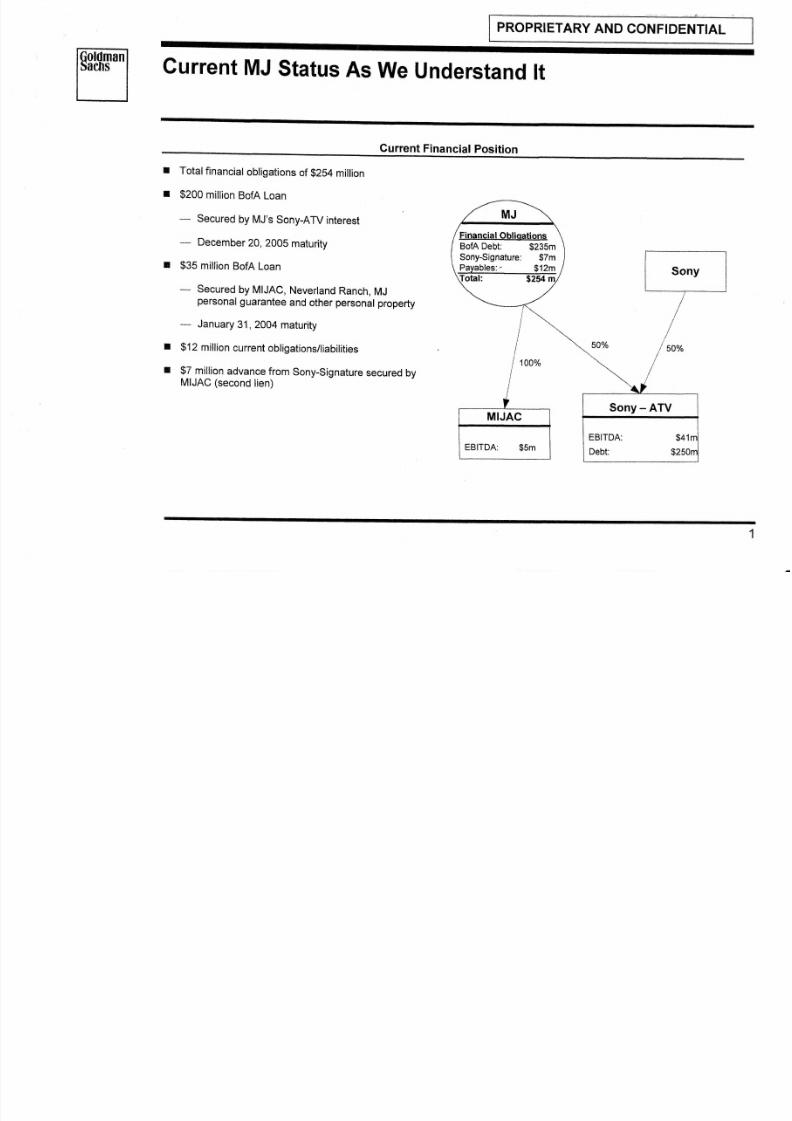

current

MJ

status

As

we

understand

lt

Current

Financial

Position

I

t

Total

financial

obligations

of

$2S4

million

$200

million

BofA

Loan

-

Secured

by MJ's

Sony-ATV

interest

-

December

20, 2005

maturity

$35

million

BofA Loan

-

Secured

by

MIJAC,

Neverland

Ranch,

MJ

personal

guarantee

and

other

personal

property

-

January

31, 2004

maturity

$1

2

million

current

obligations/liabilities

$7

million

advance

from

Sony-Signature

secured

by

MIJAC

(second

lien)

I

I

Financial Obliqations

BofA

Debt:

$235m

Sony-Signature:

$7m

Payables:-

$12m

Sony

-

ATV

EBITDA:

Debt:

8/8/2019 GoldmanSachs Materials

http://slidepdf.com/reader/full/goldmansachs-materials 3/6

I

PROPRTETARY

AND

CONFIDENT|AL

t-----'---l

BofA

Foreclosure

Scenario

t

MJ

cannot

transfer

his

Sony-ATV

interests

without

the

consent

of

Sony

t

lt-is

unlikely

that MJ

would

be

able

to take

advantage

of

his

exit

rights

under

the

Sony-ATV

operating

agreement

given

the

maturity

date

of

the

$200

million

BofA

loan

and

the expiration

date of

the

BofA

$200

million

put

right

r

Without

alternative

financing,

there

is

a

strong

risk

thatMJ cannot

avoid a

foreclosure

by BofA

unlesi

MJ

receives

the

cooperation

of

both Sony

and

BofA

I

:

t

BofA Foreclosure

Scenario

BofA

seizes

MJ's 50% interest

in

Sony-AW

BofA

seizes

MJ's

100%

interest

in

MIJAC

Total

of

$78

million in financial

obligations/liabilities

-

$59

million

tax liabilityl

-

$12

million cunent

obligations/liabilities

remain

outstanding

-

$7

million cash

advance

from

Sony-Signature

remains outstanding

-

MJ still

personally

liable

if

there is

a

short-fall

on

$35

million loan

lf

MJ does

nothing,

he may lose

his

music

publishing

assets

and

still

be

subject

to

a

substantial

amount

of

tax

and

other

riabirities

.>,

iiil.iil

'

Assumes

zero cost bas,b

for

Sony-ATV

and

MIJAC

and

Woceeds

rcceived

are

deemed

capitat income

taxable

at a 25%

capitat

gains

tax rate

2

8/8/2019 GoldmanSachs Materials

http://slidepdf.com/reader/full/goldmansachs-materials 4/6

PROPRIETARY

AND CONFIDENTIAL

our

understanding

of

MJ's

objectives

Financial

stabilization

and

vllue

Maximization

Relieve

current

debt

and

liabilities

and

create

a business

plafform

for

future

wealth

creation

-

Pay-off

significant

amount

of current

debt / liabilities

-

Receive

50%

of

new

music

company ("Music

LLC')

in

partnership

with Goldman

Sachs

Reduce

significant

amount

of short

and long-term

obligations

currenfly

outstanding

-

Eliminate

significant

amount

of

g23S

million

of

BofA

debt

which

is

secured

by

MJ's

interest

in Sony_ATV,

MlJAc,

Neverland

Ranch

and

an MJ

personal

guarantee

-

Eliminate

$12

million

of

current

obligations (e.g.

personal

expenses,

legal

fees,

etc.)

-

Remove

the second

lien on MIJAC

from

Sony-Signature $7 million advance

Generate

cash

proceeds

to

provide

a liquidity

cushion

as

MJ's new

business

initiatives

begin

generating

income

Position

MJ

to

be

the

"Bill

Gates"

of

the

music industry

-

Retain

equity

stake

in music

assets

to benefit from

future

value

creation

-

Own

smaller

stake in

a

potentially

much

larger,

multi-billion

dollar

company

No current

tax

liability

lmmediately

establish

financial

stability

and

limit

future

financial uncertainty

S Proposal

will help

MJ reduce

his financial

obligations

and

create a

platform

for

future

wealth

creation

I

I

T

I

3

8/8/2019 GoldmanSachs Materials

http://slidepdf.com/reader/full/goldmansachs-materials 5/6

PROPRIETARY

AND

CONFIDENTIAL

Goldman

Sachs'

proposal

Paying

off

MJ's

Financial

Obligaiions

/

Creating

Platform

for

Future

Wealth

Creation

I

MJ contributes

all

of

his

interests

in

sony-ATV

and

MIJAC

to

a

newly

created

vehicle

(,,Music

LLC")

in

partnership

with

Goldman

Sachs

Capital

partners

gdSCR,l

I

GS

Lender

to.provide

$135

million

in

cash

which

MJ

can

use

to

repay

his

current

liabilities

and his

BofA

loans

-

Cash

of

$35

million

to

pay

off

entire

$35

million

BofA

Loan

secured

against

MTJAC

-

Cash

of

$68

million

to

reduce

balance

on

$200

million

BofA

loanl ($t

gZ

million

balance

would

remain)

--

cash

of

$z

million

for

pre-payment

penarty

for

the

BofA

roans

-*

Cash

of

$1G

million

to

handle

other

current

obligations

-

cash

of

$g

million payable on a monthly basis for the first

year

-

No

intended

current

tax

liability

r

MJ

will

receive

$3.5

million-per

Vggr

for

5

years

-

during

Year

1

,

MJ

will

receive

$12

million

($1

million

per

month)

due

to

$9

million

proceeds

from

GS

Lender

r

MJ

will

receive

an

initial

50%

common

equity

stake

in

Music

LLC in

partnership

w1h

GSCp

for

future

wealth

creation

opportunity

t

GSCP

proposal

pro-vides

MJ

with

an

equivalent

pre-tax

valuation

of

$S1g

million2

or ZO.4xtrailing

EBITDA

on

a

net

present

value

basis3

-

ln

other

words,

MJ

would

have

to

sell

his interests in sony-ATV and MIJAC

for

20.4x

EBITDA

to

generate

thesame amount

of

after{ax

proceeds

on

a

net

present

value

basis

as

the GSCP

proposal

-

EMI's

current

stock

price

implies

that

its

music

publishing

business

is

valued

at between

g.7x

to

1Z.2xEB|TDA4

.-

Press

reports

suggest

that

AOL

Time

Warner

may

look

to

sellWarner-Chappell

for 10-12x

EBITDA

'r1 :y t^:r:l2tt

to.,adiustnent

due

fo irteresf

res

eve account

(g2Am

as ot

January

s1,

2OAs)

-

Assumes

$394

nillion

in

equity value

and

$125

miltion

in

debt

a

Assumes

recorde

d music

is

vatued'at

between

e'.ox

andi,.ox

traiting

EBITDA.

Aptil

11,

2oo3

stock

price

of

GBp 0.g7.

4

8/8/2019 GoldmanSachs Materials

http://slidepdf.com/reader/full/goldmansachs-materials 6/6

Potential

Alternatives

to

Gscp

proposal

Existing

Arrangements

with

Sony

and

BofA

t

Do

nothing

/

BofA

forecloses

on

debt

-

BofA

forecloses

on

$235

million

debt

secured

against

Sony-AW,

MlJAc,

Neverland

Ranch

and MJ

personally

-

MJ

would

owe

$59

million

in

taxesl

upon

foreclosure

which

he would

have

to

fund

from

other

sources

r

Refinance

BofA

loans

-

lf

successful

in

refinancing,

MJ would

long-term

instabi

lity/u

ncertainty

-

However,

there

is

significant

refinancing

risk

on the

$200m

loan

since

it

may

be

dependent

on

Sony

extending (i)

the

put

obligation

to

BofA

and

(ii)

the

o6ligation

to

pay

a

$6.5

million

annual

distribution

to

pay

interest

-

lf

BofA exercises.its

put

right

on the

$200 million loan, MJ would lose

his

interest

in sony-ATV and

owe

$s0

million

in

taxesl

at the

time

of

the

put

which

he will

have

to fund

from other

sources

Exercise

$200 mittion

put

right

to

Sony

-

MJ

can

put

his

interests

in

sony-ATV

to

sony

for

$200

million

between

Dec.

1,

2005

and

Feb.

2g,2006

-

Under

the

terms

of

his

$200

million

Bof4

loan,

MJ

would

have

to

use

the

proceeds

to repay

the

BofA

loan,

leaving

MJ

with

a

tax

liability

of

$50

millionl

that

he

would

have

to fund

from

other

sources

Exercrbe

Exit

Rights

under

sony-ATV

operating

Agreement

-

MJ

can

commence

the

exercise

of his

exit rights

October

1, 2005

in order

to

sell his interest

-

lt

is

unlikely

that

MJ

will

be able

to take

advantage

of

his

exit

rights

due

to the

insufficient amount

of time

MJ

has

to conclude

the

exit

process

due

to

the

BofA

l6an

maturity

dale

and

the expiration

of

the

$200

million

put

-

lf

MJ

sold,

he

would

have

a high

valuation

hurdle

(17x

trailing

EBITDA2)

to

generate

enough

proceeds

the

BofA

debt

and

the

resultinii.*

liability

(GSCP

proposal's

purchase

multipte

is 20.4x

on

pre-tax

Npv

ollili

'

Assumes

zero

cosl

basis

and

proceeds

are deemed

capitat

income

taxabte

at capital

gains

tax rate

of

25%

if::::::

2y:l:: p"ry yy:.r, JAC

althe

sani

tiTti,g

eaffoniittiiti'r"-[ii:i"#ii_nru

,n,",ur,.

o,

remain

in

the

same

position

that

he

is in

today

-

i.e.

short-term

relief,

miilion

EBTTDA

for

purposes

of

catcitating

nuftiple

a value

that

generates

sufficient

after-tax

proceeds

to

pay potential

taxiiaoititi6s

upon

exil

Assu/res

a

g2g.s