67

INVESTOR PRESENTATION Good revenue growth in 2017 FEBRUARY 8, 2018

INVESTOR PRESENTATION

Good revenuegrowth in 2017

FEBRUARY 8, 2018

INVESTOR PRESENTATION

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 2

# 2-10 Kemira today

# 11-35 Latest news and financials

# 36-46 Pulp & Paper

# 47-52 Industry & Water

# 53-59 Oil & Gas

# 60-66 Appendix

SEGMENT SPLIT PRODUCTS

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 3

GEOGRAPHIES

Kemira in briefFY2017: REVENUE EUR 2,486 MILLION, OPERATIVE EBITDA EUR 311.3 MILLION, MARGIN 12.5%

25% Bleaching

and pulping

20%

Polymers

20% Other:

e.g. defoamers,

dispersants,

and biocides

20%

Coagulants

15%

Sizing

and

strength

Revenue by product category rounded to the nearest 5%

39%

AMERICAS

1.USA

2.Canada

3.Brazil

52%

EMEA

1.Finland

2.Sweden

3.Germany

9%

APAC

1.China

2.South

Korea

3. Indonesia

59%Pulp & Paper

41%Industry & Water

CUSTOMERS

8,000 Sold-to customers

16,000 Ship-to customers

EXAMPLES OF

LARGEST CUSTOMERS

Municipalities, e.g.

Frankfurt, London, New York,

Paris, Shanghai, Singapore

#1 in

water

treatment

in NA and

Europe

#1 in shale

in NA #1 globally

REVENUE EUR million

2 229

2 137

2 373 2 363

2 486

2013 2014 2015 2016 2017

OPERATIVE EBITDAOPERATIVE EBITDA MARGINEUR million

252 253

287

303311

11.3%

11.8%12.1%

12.8%

12.5%

2013 2014 2015 2016 2017

INV E S T OR P RE S E NT A T ION 4

Delivering profitable growth

FE B RUA RY 2018

1,0681,170

1,417 1,457 1,477

130137

171195

198

2013 2014 2015 2016 2017

REVENUE ANDOPERATIVE EBITDA

REVENUE BYPRODUCT CATEGORY

INV E S T OR P RE S E NT A T ION 5

REVENUE BY CUSTOMERTYPE AND MARKET GROWTH

Pulp & Paper – market leader with solid track record

MARKET ENVIRONMENT REVENUE BY GEOGRAPHIES AND

MARKET GROWTH BY REGION

CUSTOMER EXAMPLES

35%

Americas

50%

EMEA 15% APAC

35%

Bleaching

& pulping

25%

Sizing &

strength

20%Defoamers,

dispersants,

biocides and

other process

chemicals

10%

Polymers

10% Other 40%

Pulp

20%

Printing &

writing papers

40%

Board &

tissue

-1-2%2-3%1-2%Market

growth

2-3%0-1%0-1%Market

growth

AkzoNobel (pulp) #4

BASF (paper) #2

Solenis (paper) #3

Kemira (pulp and paper) #1

Ecolab (paper) #5

Note: Revenue by industry, product and geography rounded to the nearest 5%

FE B RUA RY 2018

220227 231 228

238248

259 264

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

MARKET POSITION REVENUE BYPRODUCT CATEGORY

INV E S T OR P RE S E NT A T ION 6

REVENUE BY APPLICATIONTYPE AND MARKET GROWTH

Industry & Water – strong positions in chosen categories

REVENUE AND ORGANIC GROWTH

(Y-O-Y) EUR million

REVENUE BY GEOGRAPHIES AND

MARKET GROWTH BY REGION

40%

Coagulants

40%

Polymers

20%

Other

products

such as

defoamers

and biocides

2-3%5-6%2-3%

45%

Americas

50%

EMEA

5%

APAC

70%

Water treatment 10%

Other

20%

Oil & Gas

5-6%3-4%3-4%

MUNICIPAL (40%),

customer examples

Amsterdam

Barcelona

Frankfurt

London

Oslo

Paris

Stockholm

Los Angeles

Montreal

New York City

Toronto

Melbourne

Shanghai

Singapore

INDUSTRIAL (60%),

customer examples

Market share in water

treatment in Europe

and North America

Market share in

polymers used for

friction reduction

in US shale fracking

>30%30%

-7%-5% -5% 0% +6%

+9%

2016 2017

+15%

Note: Revenue by industry, product and geography rounded to the nearest 5%

Market

growth

Market

growth

CUSTOMER EXAMPLES

FE B RUA RY 2018

+20%

Targets:

Above-the-market

growth and operative

EBITDA of 14-16%

Our targets and actions for profitable growth

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 7

ORGANIC GROWTH

• Investments in capacity

expansion

• Seize opportunities in growth

pockets

• Shale oil & gas business

• CEOR and oil sands

• Digitalization

• APAC

• R&D, new products

ACQUISITIONS

Very selective approach

• Strategic and synergistic fit

• Accretive to profitability

• Reasonable valuation

EFFICIENCY

• Manufacturing footprint and

utilization optimization

• BOOST – Operational excellence

• Organizational efficiencies

with new structure

• Complexity reduction

• Efficient processes

OPERATING COST

DISCIPLINE

Prudent cost culture

2015 2016 2017 Pulp &Paper

Group Pulp &Paper

Pulp &Paper

Group Industry &Water

Industry &Water

Industry &Water

Volatility &inflation

Mid- to long-term target

Our key actions to improve margins

INV E S T OR P RE S E NT A T ION 8

12.5%

Operative EBITDA

margin 14-16%

New

bleaching

capacity in

Finland

Optimization

of operations:

majority of

savings in

logistics

Oil sandsChemical

Enhanced

Oil Recovery

12.1% New

two segment

structure

12.8%

Estimated end of 2017 run-rate 100% 100% 75% 0% Low 25% Low Low

Full run-rate by EO 2017 EO 2017 2018 2019 1-2 yrs 2-3 yrs 2-5 yrs 3-5 yrs

AkzoNobel’s

paper

chemicals

Advanced

Water

Treatment

Volatility and

inflation

FE B RUA RY 2018

Acquisition

in China

Expansion of

pulp chemicals,

Oulu (FI)

Progress in profitable growth

INV E S T OR P RE S E NT A T ION 9

AcquisitionOpening / expansion of site Operational efficiencies

Opening of Tarragona

coagulant site (ES)

Acquisition BASF

AKD emulsion business

Opening of EMEA

service center

Expansion of dry

and emulsion

polyacrylamide

(US)

Opening of

Nanjing (CN)

site

Closure of

Longview (US)

AkzoNobel’s

paper chemicals

acquisition

Acquisition of Soto

Industries (US)

Closure of

Soave (IT)

Start-up of Ortigueira

(BR) sodium chlorate site

and announcement of

Joutseno (FI) expansion

Acquisition

of Polymer

Services (US)

Botlek (NL)

modernization

BOOST operational

excellence program

launch

Bradford (UK)

expansion

San Giorgio (IT)

expansion

Closures of Ottawa (CA)

and Zaramillo (ES)

Closure of site

Q416

Transportation

agreement with

Odyssey

Q117

Odyssey go-live

in North America

Two segment

structure

operational

Start-up of Joutseno

(FI) chlorate expansion

Announcement

of acquisition

via JV in China

Q114

Q217

Q314

Q414

Q115

Q215

Q415

Q116

Q214

Q317

Q216

11.3%2013 operative

EBITDA

12.5%2017 operative

EBITDA

Q315

Q316

FE B RUA RY 2018

Q417

Market expected to show healthy growth

Long-term drivers for growth, including:

• E-commerce drives the need for packaging material

• Growing middle class, increased standards of living and urbanization leads to higher usage of water, energy, tissue, and board

• Recycling and use of renewables leads to e.g. higher usage of strength chemicals

• Replacement of plastics with biodegradable products

• Regulation increases water treatment

• Scarcity of resources accelerates need to produce more with less

Challenges

• Risks to global GDP growth

• Decline in demand for printing and writing paper demand

• Regulatory changes 2017 2022

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 10

MARKET GROWTH BY BUSINESS AREAS:PULP & PAPER 1%, WATER TREATMENT 2-3%, OIL & GAS 5-6% P.A.

~20

~23

APAC

Relevant target market (EUR billion)

Management estimation based on various sources

EMEA

Americas

+ 3%

CAGR

2017-

2022

2-3%

2-3%

3-4%

INVESTOR PRESENTATION

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 11

Latest news andfinancials

2017 was tail-weighted as expected

Selected highlights in 2017

• Re-organization completed without disruptions to business

• Strong recovery in oil & gas

• Healthy volume growth in pulp & paper and water treatment

• Sales prices started to offset increasing raw material costs in H2

• Major projects executed

– Acquisition synergy program completed

– Sourcing of logistics with Odyssey commenced

– Start-up of new chlorate capacity in Finland

• CEOR investment for higher demand

Challenges faced in 2017

• Raw material availability and price increasesin certain areas

• Disruptions due to hurricanes Harvey and Irma as well as force majeure by Venator

• EUR/USD swiftly from 1.05 to 1.20

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 12

TARGETS:

Above-the-market

growth and operative

EBITDA of 14-16%

ACQUISITIONS ORGANIC GROWTH

OPERATING

COST DISCIPLINE EFFICIENCY

Key financial highlights

FY 2017

• Organic growth +6% driven by volumes

• Operative EBITDA increased according to outlook

– H1 EUR 6 million below prior year, margin 11.9%

– H2 EUR 14 million above prior year, margin 13.1%

• EPS impacted negatively by EUR 12.7 million settlement and prior year EPS includes gainon sale of electricity assets

• Board of Directors proposes a dividend ofEUR 0.53 per share

EUR million

(except ratios)

FY

2017

FY

2016

Δ%

Revenue 2,486 2,363 +5

Operative EBITDA 311.3 302.5 +3

of which margin, % 12.5 12.8 -

Operative EBIT 170.3 170.1 0

of which margin, % 6.9 7.2 -

Net profit 85.2 97.9 -13

EPS, EUR 0.52 0.60 -13

Dividend per share,

proposal by the BoD, EUR 0.53 0.53 0

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 13

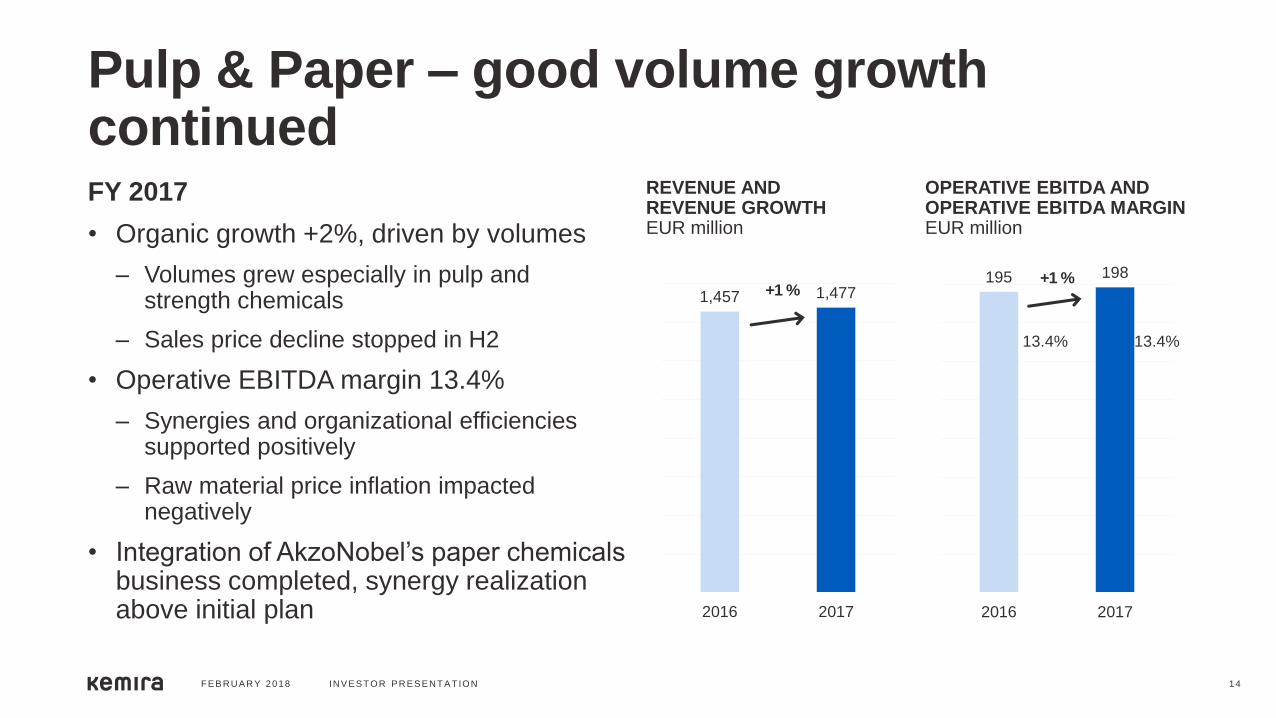

Pulp & Paper – good volume growth continuedFY 2017

• Organic growth +2%, driven by volumes

– Volumes grew especially in pulp andstrength chemicals

– Sales price decline stopped in H2

• Operative EBITDA margin 13.4%

– Synergies and organizational efficiencies supported positively

– Raw material price inflation impacted negatively

• Integration of AkzoNobel’s paper chemicals business completed, synergy realization above initial plan

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 14

1,457 1,477

2016 2017

195 198

2016 2017

REVENUE ANDREVENUE GROWTHEUR million

OPERATIVE EBITDA AND OPERATIVE EBITDA MARGINEUR million

+1 %+1 %

13.4% 13.4%

Industry & Water – growth driven by Oil & Gas recoveryFY 2017

• Strong revenue growth as North American oil & gas market recovered

– Oil & Gas revenue +56% to EUR 197 million

– Especially good demand for polymers used in shale oil & gas industry

– Demand for water treatment continued to increase, growth in coagulants +4%

• Operative EBITDA margin declined due to higher raw material prices as well as diluting revenue related to equipment sale and field trial

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 15

906

1,009

2016 2017

107114

2016 2017

REVENUE ANDREVENUE GROWTHEUR million

OPERATIVE EBITDA AND OPERATIVE EBITDA MARGINEUR million

+11% +6%

11.8%11.3%

Major actions to support profitability in 2018-2019

• Full contribution of new chlorate capacity in Finland

• Efficiencies from two segment structure

• BOOST program, e.g. transportation costs

• Acquisition / joint venture in China: closing expected in H1 and ramp-up in H2/18

• Focus to improve or reduce currently margin-dilutive businesses

Uncertainties

• Raw material availability and prices

• Regulatory changes, e.g. China

• Currencies

OPERATIVE EBITDAEUR million

287

303311

2015 2016 2017

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 16

Drivers for profitability improvement2018 OUTLOOK: KEMIRA EXPECTS ITS OPERATIVE EBITDA TO INCREASE FROM THE PRIOR YEAR

Outlook for 2018

Kemira expects its operative EBITDA to increase from the prior year(2017: EUR 311.3 million).

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 17

EUR

million

2013 2014 2015 2016 2017 2018

outlook

Operative

EBITDA

252 253 287 303 311 ”Increase”

Progressing our strategy forprofitable growth

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 18

GROUP’S MID- TO LONG-TERM TARGETS

Above-the-market growth

Operative EBITDA 14-16%

Gearing below 60%

Dividend policy: stable and competitive dividend

Balanced cash flow

and capex

Increase

efficiency

Grow by investing,

innovating and capturing

market

opportunities

Group’s organic revenue growth continued

• Group’s organic growth +11%

– Pulp & Paper +5%

– Industry & Water +20%

• Operative EBITDA margin 12.7%, +100 bps compared to prior year

– Sales prices and volumes main drivers, variable costs and FX were headwinds

596+9% -4% 0% 637

Q4 2016 Salesvolumes

Salesprices

Currencyimpact

Acquisitions Q4 2017

+2% 72.878.9 80.8

70.0 69.077.1

84,5 80,7

12.5% 13.4% 13.6%11.7% 11.3%

12.5%13,6% 12,7%

0

20

40

60

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 19

Q4 2017

Revenue and revenue growthEUR million

Operative EBITDA and operative EBITDA marginEUR million

Pulp & Paper – strong results in Q4

• Volume growth +4%, helped by recent chlorate capacity start-up in Finland and shutdown at major customer mill in comparison period

• Record-high profitability driven by volumes, lower fixed costs, higher utilization rates, and other positive items during the quarter

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 20

Revenue and organic revenue growth (y-on-y)EUR million

Operative EBITDA and operative EBITDA margin trendEUR million

362 361 365 369 372 369 363 373

0

100

200

300

400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

47,9 49,3 51,846,3 46,0 47,8 48,5

55,4

13,2% 13,7% 14,2%12,6% 12,4% 13,0% 13,4%

14,9%

0

20

40

60

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

+3% +1% -4% -2% 0% +1% +2% +5%

Industry & Water – good growth continued

• Growth rate exceptionally high, Oil & Gas +54% being the main factor in Q4 2017

– Also water treatment continued on good growth path, high-single digit growth in coagulants

• Profitability impacted due to higher raw material prices and margin-dilutive equipment sale as well as certain manufacturing related items

• Q4 profitability is typically weaker due to seasonality

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 21

Revenue and organic revenue growth (y-on-y)EUR million

Operative EBITDA and operative EBITDA margin trendEUR million

24.929.6 29,0

23.7 22.929.3

36,025,3

11,3%13,1% 12,5%

10,4% 9,6%11,8%

13,9%

9,6%

0

20

40

60

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

220 227 231 228 238 248 259 264

0

100

200

300

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

-7% -5% 0% +9% +15%-5% +6% +20%

SALES PRICE VS VARIABLE COST TREND

-200

-150

-100

-50

0

50

100

150

200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Brent oil, USD Sales prices* Variable costs*

SALES PRICES AND VARIABLE COSTS ONEBITDA LEVEL (CHANGE Y-O-Y)

9

5

-3-10

-16 -20

-10

-2-9

-18

-26-23

-16

-4

3

11

-18

-23

-23-13

0

1613 13

-30

-20

-10

0

10

20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017

Net impact on EBITDA (sales prices-variable costs)

Sales prices

Variable costs

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 22

Gap between variable costs and sales prices narrowing

* 12-month rolling change vs previous year in EUR million

54% 54%

59%

2015 2016 2017

Development of selected key figures

• Net debt EUR 694 million with average cost of debt 2.0% (2016: 2.1%)

• NWC ratio improved to 9.4% (10.2%)

• Reported tax rate in 2017 24.3% (23.5%)

– Going forward the US tax reform will lower income taxes for Kemira in the country, although short-term negative impact from new BEAT* provisions

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 23

2.2

NET DEBT / OPERATIVE EBITDA AND GEARING

2.1

Net debt

634m

Net debt

694mNet debt

642m

2.2

* BEAT = Base Erosion and Anti-Abuse Tax

• New chlorate plant in Brazil and new chlorate line in Finland

• Capacity additions due to integration of acq.

• Polymer capacity in Italy and UK

50 60 59

53 58 65

78

95 66

2015 2016 2017

CAPEX guidance 160-200 MEUR in 2018

Expansion Improvement Maintenance

190

CAPITAL EXPENDITURE EXCLUDING

ACQUISITIONSEUR million and share of revenue

213

RECENT LARGEST VALUE CREATING

INVESTMENTS

CAPEX GUIDANCE

• In 2018, capital expenditure estimated to beEUR 160-200 million

– Includes capacity expansion in Oil & Gas

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 24

182

7.7%

9.0%7.6%

Dividend proposal EUR 0.53 per share

Kemira’s dividend policy is to pay a stable and competitive dividend

Board of Directors’ proposal to the AGM a dividend of EUR 0.53 per share, totaling EUR 81 million

Kemira has paid dividend every year since listing of shares in 1994

Kemira offers attractive dividend yield

0,53 0,53 0,53 0,53 0,53 0,53 0,53

5.8% 4.5% 4.4% 5.4% 4.9% 4.4% 4.6%

2011 2012 2013 2014 2015 2016 2017

INV E S T OR P RE S E NT A T ION 25

Dividend per share Dividend yield

FE B RUA RY 2018

*

Kemira’s dividend yield calculated using the share price at year-end

*BoD proposal to the AGM 2018

VARIABLE COST SPLIT 2017EUR 1.5 billion

TOP 10 RAW MATERIALSBY SPEND

1. Sodium hydroxide

2. Acrylonitrile

3. Colloidal silica dispersion

4. Amines

5. Aluminium hydrate

6. Petroleum solvents

7. Sodium chloride (salt)

8. Acrylic ester

9. Acrylic acid

10. Fatty acid

Top 10 account for 43%of Kemira’s raw material spend

INV E S T OR P RE S E NT A T ION 26

EXPOSURE TO OIL RELATEDRAW MATERIALS

Kemira’s variable cost split and top raw materials

30%Oil & gas

related

70%Not oil

related

70%Raw materials

10%Electricity & energy

20%Logistics

FE B RUA RY 2018

NET DEBT / OPERATIVE EBITDA AND GEARING

42% 41% 42%

54% 54%59%

2012 2013 2014 2015 2016 2017

GROSS DEBT MATURITY PROFILE,END OF 2017 EUR 861 MILLION

INV E S T OR P RE S E NT A T ION 27

Debt portfolio is well diversified

1.9x2.1x 2.1x2.2x1.8x 2.2x

532m 694m456m 486m 634m642m

NET DEBT

OPERATIVE EBITDA

FE B RUA RY 2018

249m 311m252m 253m 303m287m

0

50

100

150

200

250

300

350

400

450

2018 2019 2020 2021 2022 2023 2024

Bilaterals Bonds Undrawn RCF Others

150

200196

110

205

400

Key figures and ratios – 5-year summary

EUR million (except ratios) 2013 2014 2015 2016 2017

Revenue 2,229.1 2,136.7 2,373.1 2,363.3 2,486.0

Operative EBITDA 251.9 252.9 287.3 302.5 311.3

of which margin 11.3% 11.8% 12.1% 12.8% 12.5%

Operative EBIT 164.2 158.3 163.1 170.1 170.3

of which margin 7.4% 7.4% 6.9% 7.2% 6.9%

Cash flow from operations 200.3 74.2 247.6 270.6 205.1

Capital expenditure, excluding acq. 133.5 140.6 181.7 212.6 190.1

Gearing at period-end 41 42 54 54 59

Inventories 170 197 207 217 224

Personnel at period-end 4,453 4,248 4,685 4,818 4,732

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 28

* Restated figures reflect the change of IAS 19, Employee Benefits

Per share figures – 5-year summary

2013 2014 2015 2016 2017

Earnings per share, EUR -0.21 0.59 0.47 0.60 0.52

Cash flow from operating activities

per share, EUR

1.32 0.49 1.63 1.78 1.35

Equity per share, EUR 7.32 7.57 7.76 7.68 7,61

Dividend per share, EUR

(*2017 proposal to the AGM)

0.53 0.53 0.53 0.53 0.53*

Share price, EUR, end of period 12.16 9.89 10.88 12.13 11.50

Market capitalization, EUR million

(excl. treasury shares)

1,849 1,504 1,654 1,848 1,752

Number of shares, million

(excl. treasury shares)

152.0 152.1 152.1 152.4 152.4

P/E ratio - 16.7 23.3 20.1 22.3

P/CF ratio 9.2 20.2 6.7 6.8 8.5

P/B ratio 1.7 1.3 1.4 1.6 1.5

Dividend yield, % 4.4 5.4 4.9 4.4 4.6

INV E S T OR P RE S E NT A T ION 29FE B RUA RY 2018

EUR million Q4 2017 Q4 2016 Δ% 2017 2016 Δ%

Revenue 636.5 596.5 +7 2,486.0 2,363.3 +5

Operative EBITDA 80.7 70.0 +15 311.3 302.5 +3

margin 12.7% 11.7% - 12.5% 12.8% -

Operative EBIT 44.0 36.1 +22 170.3 170.1 0

margin 6.9% 6.1% - 6.9% 7.2% -

Net profit 25.8 18.2 +42 85.2 97.9 -13

Earnings per share, EUR 0.16 0.11 +45 0.52 0.60 -13

Cash flow from operations 71.4 102.4 -30 205.1 270.6 -24

Capex excl. acquisitions 64.2 89.4 -28 190.1 212.6 -11

Net debt 694 634 +10 694 634 +10

NWC ratio (year-end) 9.4% 10.2% - 9.4% 10.2% -

Operative ROCE (rolling 12 months) 9.7% 9.9% - 9.7% 9.9% -

Personnel at period-end 4,732 4,818 -2 4,732 4,818 -2

Key figures

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 30

EUR million Q4 2017 Q4 2016 2017 2016

Net profit for the period 26 18 85 98

Total adjustments 37 50 204 187

Change in net working capital 18 48 -34 29

Finance expenses -6 -12 -25 -20

Income taxes paid -4 -2 -25 -23

Net cash gen. from operating activities 71 102 205 271

Purchases of subsidiaries and acquisit. 0 0 0 2

Capital expenditure -64 -89 -190 -213

Proceeds from sale of assets 2 0 3 37

Change in long-term loan receivables -5 0 -5 1

Cash flow after investing activities 4 13 13 98

Cash flow

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 31

EUR million Q4 2017 Q4 2016 Δ% 2017 2016 Δ%

Revenue 372.8 368.6 +1 1,476.9 1,457.3 +1

Operative EBITDA 55.4 46.3 +20 197.7 195.3 +1

margin 14.9% 12.6% - 13.4% 13.4% -

Operative EBIT 30.9 24.5 +26 104.8 111.6 -6

margin 8.3% 6.6% - 7.1% 7.7% -

Operative ROCE*, % 9.0% 10.0% 9.0% 10.0%

Capital expenditure 41.1 56.3 -27 138.3 125.1 +11

Cash flow after investing activities 4.4 19.8 -78 15.7 105.7 -85

KEY FINANCIALS

Pulp & Paper

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 32

*12-month rolling average

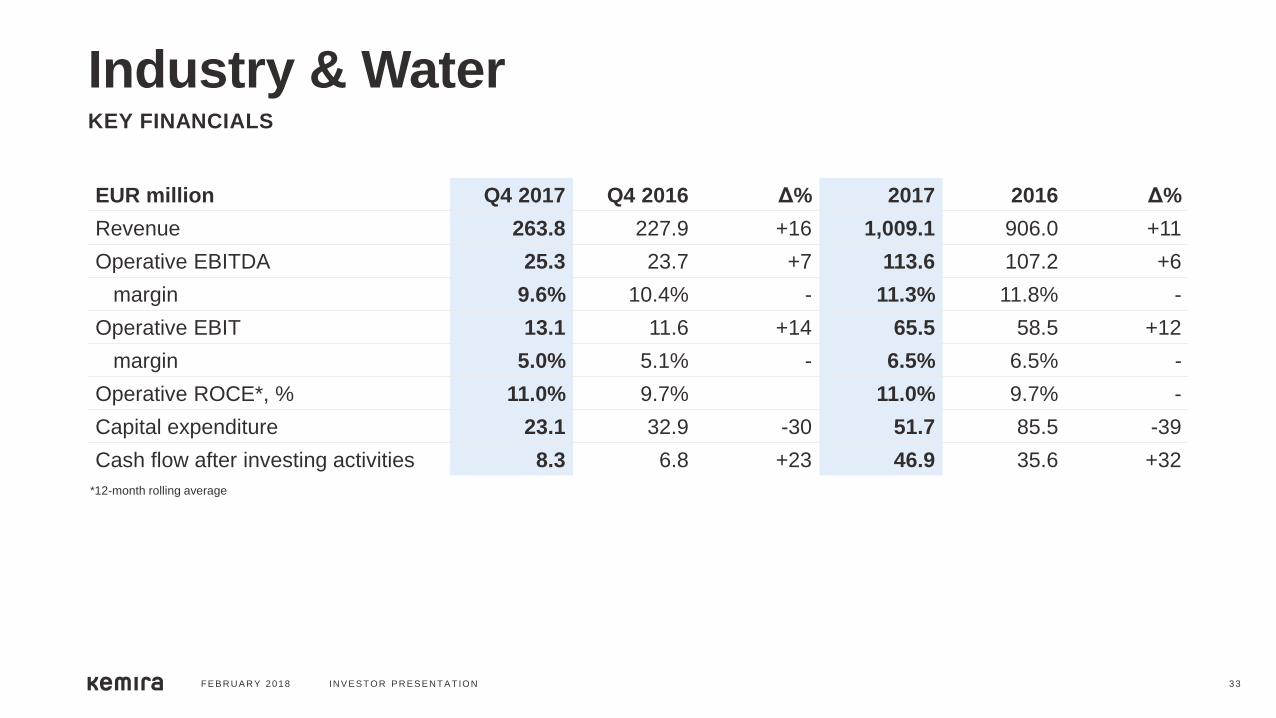

EUR million Q4 2017 Q4 2016 Δ% 2017 2016 Δ%

Revenue 263.8 227.9 +16 1,009.1 906.0 +11

Operative EBITDA 25.3 23.7 +7 113.6 107.2 +6

margin 9.6% 10.4% - 11.3% 11.8% -

Operative EBIT 13.1 11.6 +14 65.5 58.5 +12

margin 5.0% 5.1% - 6.5% 6.5% -

Operative ROCE*, % 11.0% 9.7% 11.0% 9.7% -

Capital expenditure 23.1 32.9 -30 51.7 85.5 -39

Cash flow after investing activities 8.3 6.8 +23 46.9 35.6 +32

KEY FINANCIALS

Industry & Water

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 33

*12-month rolling average

FY 2017

Revenue split by country

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 34

USA 27%

Canada 6%

Brazil 3%

Uruguay 2%

Other Americas 1%

Finland 14%Sweden 6%

Germany 5%

Poland 3%

UK 3%

Spain 2%

Other APAC 4%

Korea 1%China 4%

Russia 2%

Netherlands 2%

France 2%

Italy 2%

Other EMEA 9%

Norway 2%

Revenue and cost distribution per currency

Currency exchange rates had around EUR +2 million impact on the operative EBITDAin 2017.

Guidance: 10% change in our main foreign currencies would approximately haveEUR 10 million impact on operative EBITDA on an annualized basis

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 35

42% EUR 13% Others

KEMIRA REVENUE DISTRIBUTION 2017 KEMIRA COST DISTRIBUTION 2017

3% CNY

2% BRL

5% CAD

35% USD

10% Others

4% CNY

6% CAD

8% SEK

30% USD

42% EUR

INVESTOR PRESENTATION

Pulp & Paper –driving growth as market leader

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 36

Above-the-market

growth and operative

EBITDA of 14-16%

Our winning formula to continue growth

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 37

INVEST IN GROWTH

AND R&D

• Capacity additions

• More than 10 new products in

2016 and 2017

IMPROVE CUSTOMER

EXPERIENCE

• TOP 50 customers are EUR 1bn

• Customer satisfaction to 98%

MAXIMIZE CAPACITY

UTILIZATION

• Bleaching ran flat out 9 years

• Paper chemicals varying

REDUCE COMPLEXITY

• Group: 240 products out in 2016

• Around 250 products out in 2017

MANAGE FIXED COSTS

• 2017 business overheads

below 2016 level

ENHANCE

PERFORMANCE CULTURE

• New mgmt. structure

• Employee engagement – 15/16

survey items improved since 2015

Board and paper production shiftingto emerging markets

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 38

GROWTH OF

BOARD AND PAPER

PRODUCTION

BY REGION 2015-2030

55mt growth in APAC

by 2030

BIGGEST PRODUCERS

ARE:

China, USA, Japan,

Germany, India, Sweden,

Korea, Canada, Finland,

Brazil

BIGGEST GROWTH

AREAS ARE:

China, India, Indonesia,

Brazil, Russia, Vietnam

TOTAL BOARD &

PAPER PRODUCTION:

2015: 402 million tons

2030: 461 million tons

CAGR%: around 1 % / annum

Source: Pöyry

North America

2015: 82 mt

2030: 75 mt

Latin America

2015: 21 mt

2030: 31 mt

. Europe

2015: 85 mt

2030: 78 mt

Oceania

2015: 4 mt

2030: 4 mt

China

2015: 106 mt

2030: 139 mt

E. Europe

2015: 18 mt

2030: 26 mt

Africa

2015: 4 mt

2030: 6 mt

Japan

2015:26 mt

2030:21 mt

Rest of Asia

2015: 55 mt

2030: 82 mt

Strong market positions and strategic investments

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 39

REGION MARKET POSITION GROWTH TREND GROWTH STRATEGY

EMEA

North America

APAC

South America

#1

#2/3

#1

#3

Exceptional customer

experience

Transformation from paper

to board

Continue to grow with major

players (TCM) and assess

future investments

Assess future bleaching

investments

TCM = Total Chemistry Management

Board and paper production in APAC willbe bigger than Europe and North America combined by 2020

>90% of global board and paper production growth in APAC

Kemira now #1 with close to 10% share in APAC

• Revenue doubled to aroundEUR 200 million in 3 years

Fragmented market provides good potential for profitable growth

Continue to grow revenue and market share

PULP & PAPER RELEVANT CHEMICALSMARKET 2017

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 40

We have become market leader in APAC

EMEA

North

America

APAC

South America 2-3%

2-3%

-1-0%

0-1%

CAGR 2017-2022

Strong demand in pulp market creating growth opportunitiesNew pulp mill projects are driven byincreasing demand for board and tissue

• Food and liquid packaging board isgrowing particularly fast in Asia

• Pulp is produced close to wood sources andthen shipped to board, paper, and tissue mills

• Growth in board = 1 new pulp mill per year

Multiple pulp mill projects realised and expected in Northern Europe creating opportunities for Kemira to grow withthe market

In addition, a few large scale pulp millprojects expected in South America

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 41

Confirmed new capacity /

debottlenecking 2016-2020

Possible new mills 2020-2022

• Kemira’s capacity in sodium chlorate was fully utilized, hence the need for additional capacity

• Capacity doubled in Joutseno with around EUR 50 million investment

• Investment realized according to budget and start-up was ahead of schedule in early September 2017

• Part of the production will be shipped to APAC to support the growth in the region

KEMIRA BLEACHING CHEMICALS REVENUE GROWTH

2014 2015 2016 2017

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 42

Successful value creating investments –case Joutseno

+7% +10% +6% +5%

CAGR

+ 7%

Acquisition via JV in China

• Agreed to form joint venture with Tiancheng

• NewCo will produce mainly AKD wax and its key raw material fatty acid chloride (FACL)

– AKD is sizing chemical used in board and paper to createresistance against liquid absorption

– NewCo also plans to produce coagulants for water treatment

• Kemira strengthens its position and secures supply of key raw material for AKD wax

• Kemira will have 80% of NewCo

– Investment for 80% around EUR 55 million

– Closing expected in H1 2018

• Ramp-up in H2/18 after completion investments

– Good contribution to P&L in 2019 after ramp-up

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 43

AKD WAX SUPPLIED FROM YANZHOU, CHINA TO KEMIRA SITES GLOBALLY

We leverage acquisition synergieswith our global production

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 44

Telêmaco

Borba

Washougal

St. CatharinesHelsingborg

Joutseno

Nanjing

Hallam

Gunsan

Pasuruan

Wellgrow

Krems

TarragonaYanzhou

NewCo

Acquisition in China is excellentstrategic fitAcquired asset fulfills our key criteria for acquisitions

GROWTH – End-products in growing markets

APAC – Enables profitable growth in APAC

SUPPLY – Backward integr. & self-sufficiency (FACL)

SUSTAINABILITY – FACL from renewable raw material

LOCATION – Close to our existing production

PROFITABILITY – Accretive in 2019 after ramp-up

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 45

END-PRODUCTSWHERE AKD WAXIS USED

Pulp & Paper

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 46

TECHNOLOGY AND MARKET LEADER

Value chain part covered by Kemira

RAW

MATERIALSINTERMEDIATES PRODUCTS APPLICATIONS

CUSTOMER

INDUSTRIESCUSTOMERS

Electricity

Sodium chloride(salt)

Crude tall oil

Cationic monomer

Acrylonitrile

Acrylic acid

Olefins

Fatty acids

Maleic anhydride

Sulfur

Tall oil rosin

AKD Wax

Isomerized olefinsAcrylamide

Sodium chlorate

Hydrogen peroxide

Polymers

Defoamers

Coagulants

Biocides

Sizing

Strength Additives

Surface additives

Colorants

Sulfuric acid

Pulping

Bleaching

Retention

Wet-end processcontrol

WQQM

Sizing

Strength

Surface treatment

Coloring

Pulp

Packagingand board

Printingand writing

Tissue

All the major global paper and pulp producers

MAIN COMPETITORS: BASF, Akzo Nobel, Solenis, Ecolab, SNF

INVESTOR PRESENTATION

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 47

Industry & Water -stronger platformfor profitable growth

New structure creates growth andefficiency opportunities Leveraging the full potential of new combined segment

• Full geographical reach in all regions

• Global polymer expert network

• Water treatment expertise for O&G and Mining

Structural change means faster decision making

More efficient development and roll-out of new innovations

Important part of segment’s profitability improvement

• On Group-level cost savings EUR 15-20 million

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 48

Oil &

Mining

Municipal

& Industrial

70%Water

treatment

20%Oil & Gas

10%Other

applications

Industry

& Water

0

20

40

60

80

2015 2016

Water Treatment Oil & Gas

• Multiple initiatives ongoing to boost growth in both businesses

Profitable growth opportunities ahead...

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 49

BUSINESS

AREA

REGION GROWTH INITIATIVES

IN 2015-2017

WATER

TREATMENT

EMEA Desalination

BioGas

Sludge dewatering

Middle East and Africa

NA Odor control

Sludge dewatering

APAC Deep sludge dewatering

OIL & GAS GLOBAL CEOR

Oil sands in Canada

REVENUE IN GROWTH

INITIATIVESEUR million

+ 65%

…fueled by strong innovation pipeline

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 50

>20Continuous

ideas inflow

PROJECTS UNDER

EVALUATION

Enhanced Oil Recovery

PROJECTS UNDER DEVELOPMENT AND EARLY

COMMERCIALIZATION

PROJECTED 10-YR

NPV

8

EUR

650 million

Oil sands

Shale oil & gas

Solid liquid separation (incl. AWT)Sludge dewatering, nutrients recovery, mining processes

Desalination, re-use & disinfection(incl. AWT)

2

3

12

1

# OF

PROJECTS

AWT = Advanced Water Treatment

The next generation of sludge treatment will focus on customer performance and value created

KemConnect Smart Dewatering combines a complete chemicals portfolio, continuous chemistry optimizationand real-time monitoring to a new business model

ADVANCED WATER TREATMENT CASE EXAMPLE

Innovation case – KemConnect Smart Dewatering

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 51

Dewatering Today Smart DewateringTomorrow

Disposal

Cost

KemConnect

Service Fee

Disposal

Cost

Customer

Net Savings

Chemical Cost

Industry & Water

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 52

TECHNOLOGY AND MARKET LEADER IN WATER TREATMENT AS WELLAS IN NICHE APPLICATIONS IN OIL & GAS

MAIN COMPETITORS

Coagulants: mainly local small companies, Feralco, USALCO, Kronos, PVS,

Polymers: SNF, Solvay, Ecolab, Solenis, BASF Value chain part covered by Kemira

INTERMEDIATES PRODUCTS APPLICATIONS SALES CHANNELS CUSTOMERS

Acrylonitrile

Acrylic acid

Sulfuric acid

Hydrochloric acid

Aluminium hydrate

Iron ore

Pickling liquor

Copperas

Various monomers

Acrylamide

Cationic monomer

Polymers (EPAM, DPAM)

Al Coagulants

Fe Coagulants

Dispersants &antiscalants

Biocides

Emulsifiers

Defoamers

Formulations

Raw water & waste water treatment

Sludge treatment

Friction reduction

Enhanced oil recovery

Tailings treatment

Mining processes

Direct sales

Distributor/reseller

Service companies

RAW

MATERIALS

Municipalities

Private operators

Industrial customers

Pumpers

Oil & Gas operators

Service companies

Mine operators

INVESTOR PRESENTATION

Oil & Gas – well positioned for growth in niche areas

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 53

Resilient business set for growth

Growing market demand with our selective market diversification assuring growth

Kemira’s offering

• Process efficiencies: polymers that reduce energy consumption by 60% in shale oil fields

• Cost reduction: higher concentrated liquids that make offshore oil recovery more cost effective (CEOR)

• Addressing environmental regulations: tailing treatment in oil sands

New innovative technologies driving expansion

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 54

0

50

100

150

200

250

2013 2014 2015 2016 2017

REVENUE IN GROWTH INITIATIVESEUR million

REVENUE IN GROWTH INITIATIVESEUR million

25%Other

50%Shale fracking

25%Oil sands and

Chemical Enhanced

Oil Recovery Figures rounded to closest 5%

Oil

Price

+ 56%

in 2017

Our innovations make shale industrymore efficientSHALE MARKET

• Polymer market size +200M EUR and growing at double digit today

• Polymer more favorable product based on cost/performance

KEMIRA

• Provides unique chemistries, friction reducers,that reduce energy needed during hydraulic fracturing

• Volume growth over 100% in 1-9/2017

• Differentiating from competitors with innovative products

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 55

Market shares

in polymers used

for fracking

#1 market

position with

over 30%

market share

KEMIRA

Others

Competitor B

Competitor C

Competitor A

Long-term growth potential in CEOR

CHEMICAL ENHANCEDOIL RECOVERY MARKET

• CEOR market sizeEUR 1bn of whichEUR 500 million accessible to Kemira

• Market growth estimatedto be 5% driven by decline of production from existing fields

KEMIRA

• Kemira’s MaxXtract solution tailored specifically to customer needs, incorporating chemistry, equipment and services

• Kemira’s knowhow in polymers helps oil producers

• Potential for > EUR 100 million revenue in 5 years

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 56

Substantial long-term growth

potential within existing

CEOR projects and

through new projects

Growth in CEOR supported by approximately EUR 30 million investment• We will expand our polymer capacity for Chemical

Enhanced Oil Recovery within Oil & Gas business

• After prudent development in R&D and successful field trials, the investment will be done on the basis of anticipated uptake in customer demand

• Additional capacity will be built to Kemira’s existing manufacturing site at Botlek, Netherlands

• New capacity is expected to be in commercial operation by the beginning of 2019

• Investment is part of earlier announcedEUR 160-200 million capital expenditure for 2018

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 57

Oil sands has grown from 0 to aboveEUR 30m in 3 yearsOIL SANDS MARKET

• Market size is aroundEUR 400 million

• Projects are capex-heavybut developed projects are considered as sunken costs

KEMIRA

Offers total solutions to reduce environmental concerns

Customer base expanding

Revenue has grown to above EUR 30 million in 3 years

Target to more than double current revenues in 2-3 years

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 58

Companies

operating in oil

sands market (examples)

Oil & Gas well positioned for growthin niche areas

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 59

Diversification –

EUR 200 million

Growing in shale,

oil sands and CEOR

Bigger and

better

Strong player in three

core areas (shale,

oil sands, CEOR),

including service

capabilities

Oil & Mining Industry & Water:

Global Oil and Gas

2009

PHASE I

2017

PHASE II

2022

PHASE III

New business –

EUR 30 million

Niche position in

niche market

INVESTOR PRESENTATION

Appendix

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 60

SHAREHOLDERS ON JANUARY 31, 2018

% OF SHARES

1. Oras Invest 18.2%

2. Solidium (owned by State of Finland) 16.7%

3. Varma Mutual Pension Insurance Company 3.4%

4. Ilmarinen Mutual Pension Insurance Comp. 2.1%

5. Kemira Oyj 1.9%

Total number of shares 155,342,557

Foreign ownership of shares 26.0%

Total number of shareholders 35,542

KEMIRA BOARD OF DIRECTORS

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 61

Kemira – largest shareholders andBoard of Directors

JARI PAASIKIVI

Chairman

Member since 2012

Oras Invest Oy, CEO

KERTTU

TUOMAS

Vice Chairman

Member

since 2010

WOLFGANG

BÜCHELE

Member in

2009-2012 and

since 2014

KAISA

HIETALA

Member

since 2016

TIMO

LAPPALAINEN

Member since

2014

SHIRLEY

CUNNINGHAM

Member

since 2017

Kemira’s Management Board

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 62

Jukka Hakkila, Chief Legal Officer, acts as secretary of Management Board and Board of Directors

PRESIDENT AND CEO

Jari Rosendal

PULP & PAPER

Kim Poulsen

OPERATIONAL

EXCELLENCE

Esa-Matti Puputti

INDUSTRY & WATER

Antti Salminen

CFO

Petri CastrénHUMAN RESOURCES

Eeva SalonenCTO

Matthew R. Pixton

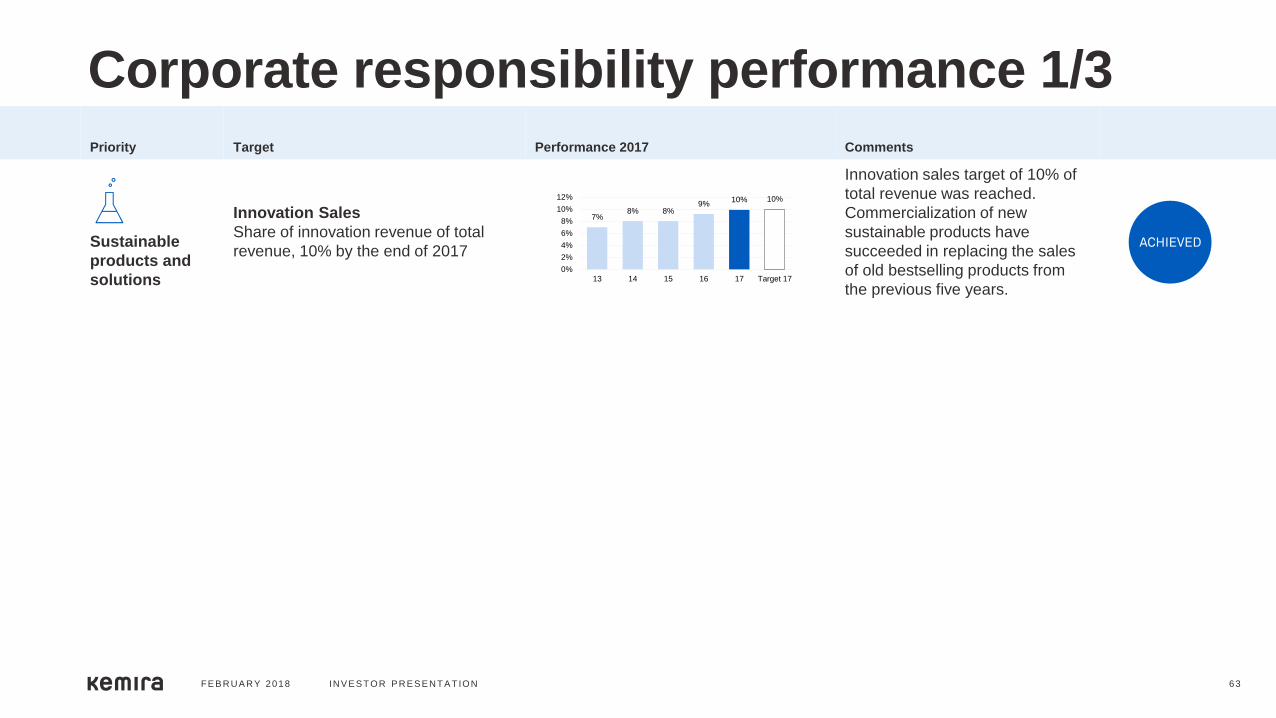

Corporate responsibility performance 1/3

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 63

Priority Target Performance 2017 Comments

Sustainable

products and

solutions

Innovation Sales

Share of innovation revenue of total

revenue, 10% by the end of 2017

Innovation sales target of 10% of

total revenue was reached.

Commercialization of new

sustainable products have

succeeded in replacing the sales

of old bestselling products from

the previous five years.

7%8% 8%

9%10% 10%

0%

2%

4%

6%

8%

10%

12%

13 14 15 16 17 Target 17

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 64

Priority Target Performance 2017 Comments

Responsible

operations and

supply chain

Climate change

Kemira Carbon Index ≤ 80

by end of 2020 (2012 = 100)

Slight decrease in carbon index

compared to 2016, due to

increased use of carbon neutral

energy sources and continuous

implementation of energy

efficiency projects.

People Safety

Achieve zero injuries on long term;

TRIF* 2.0 by end of 2020

In 2017, TRIF increased to 3.9

(3.4). The increase in incidents

were related to contracted work at

our premises. Also the severity of

incidents increased, including 3

permanent disabilities.

Supplier Management

5 sustainability audits for highest risk**

suppliers every year during 2016–2020,

average, cumulative target 25 by 2020

Four SMETA (Sedex Members

Ethical Trade Audit) audits in

collaboration with an external

service provider was conducted

with no business stopping results.

Majority of the corrective actions

were related to health and safety

and labor practices.

* TRIF = Number of Total Recordable Injury Frequency per million hours, Kemira + contractor

** Suppliers with lowest sustainability assessment score

10088 91 92 86 85 80

0

20

40

60

80

100

120

12 13 14 15 16 17 Target20

5,8

7,2

3,43,9

2,0

0,0

2,0

4,0

6,0

8,0

14 15 16 17 18 19 Target20

4

8

25

0

5

10

15

20

25

30

2016 2017 Target 2020

Corporate responsibility performance 2/3

FE B RUA RY 2018 INV E S T OR P RE S E NT A T ION 65

Priority Target Performance 2017 Comments

People and

integrity

Employee engagement index based

on Voices@Kemira biennial survey

The index at or above the external

industry norm Participation rate in

Voices@Kemira 75% or above

Due to the reorganization, the

biennial employee engagement

survey was postponed from

autumn 2017 until spring 2018, to

give managers at least six months

with their new teams before

engaging in the survey.

Leadership development activities

provided, average

Two (2) leadership development

activities per people manager position

during 2016–2020, cumulative target

1,500 by 2020

Steady rate of participation in both

internal and external leadership

development activities continued

in 2017 at 542 and actual

cumulative total so far 1,036. The

activities also included on-the-job

learning opportunities in corporate

development projects.

494

1 036

1 500

0

500

1000

1500

2000

2016 2017 Target 2020

58%67%

75%85%

0%

50%

100%

2013 2015 2017

Engagement Participation

Corporate responsibility performance 3/3

Important information about financial figuresKemira provides certain financial performance measures (alternative performance measures) on non-GAAP basis. Kemira believes that alternative performance measures, such as organic growth*, EBITDA, operative EBITDA, cash flow after investing activities, and gearing followed by capital markets and Kemira management, provide useful information of its comparable business performance and financial position. Selected alternative performance measures are also used as performance criteria in remuneration.

Kemira’s alternative performance measures should not be viewed in isolation to the equivalent IFRS measures and alternative performance measures should be read in conjunction with the most directly comparable IFRS measures. Definitions of the alternative performance measures can be found in the Definitions of the key figures in this report, as well as at www.kemira.com > Investors > Financial information.

All the figures in this interim report have been individually rounded and consequently the sum of individual figures may deviate slightly from the sum figure presented.

* Revenue growth in local currencies, excluding acquisitions and divestments

FE B RUA RY 8 , 2018 FY 2017 RE S ULT S 66