42

Goods and Services Tax (‘GST’) – Impact on Service Sector April 2017

Goods and Services Tax (‘GST’) – Impact on Service

Sector

April 2017

Sections

1. Definition

2. Supply

3. Schedules

4. Registration

5. Time and place of supply

6. Taxable value

7. Credit

8. Refunds & returns

9. Job work

10. SEZ, EOU & STPI

11. Transitional provision

GST Impact on Service Sector_________________________________________________________________________

1| Definition

GST Impact on Service Sector_________________________________________________________________________

Goods: means every kind of movable propertyother than money and securities but includesactionable claim, growing crops, grass andthings attached to or forming part of the landwhich are agreed to be severed before supplyor under a contract of supply.

S. 2(52) of CGST Act

Services: means anything other than goods,money and securities but includes activitiesrelating to the use of money or its conversion bycash or by any other mode, from one form,currency or denomination, to another form,currency or denomination for which a separateconsideration is charged.

S. 2(102) of CGST Act

Composite Supply: means a supply made by ataxable person to a recipient consisting of twoor more taxable supplies of goods or servicesor both, or any combination thereof, which arenaturally bundled and supplied in conjunctionwith each other in the ordinary course ofbusiness, one of which is a principal supply.

S. 2(30) of CGST Act

Mixed Supply: means two or more individualsupplies of goods or services, or anycombination thereof, made in conjunction witheach other by a taxable person for a singleprice where such supply does not constitute acomposite supply.

S. 2(74) of CGST Act

Definition

GST Impact on Service Sector_________________________________________________________________________

2| Supply

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

No such concept. Scope of Supply includes sale, transfer,

barter, exchange , license, rental, lease,

disposal etc.

(Supply not defined in the Constitution)

-ve impact as scope of supply has been enhanced.

Supply without consideration prescribed under

Schedule I will be treated as taxable supply for the

purpose of levy of GST.

There are various instances detailed under

Schedule II where the activities will be treated as

deemed supply of goods/ services.

Concept of Supply

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

Services means any activity carried out

by a person and includes a declared

service, but shall not include –

- An activity which constitutes merely –

a) A transfer of title on goods or

immovable property.

b) Deemed sales within the meaning of

clause (29A) of Article 366

- Services by an employee to the

employer

- Fee taken by any court or tribunal

“services” means anything other than

goods, money and securities but

includes activities relating to the use

of money or its conversion by cash

or by any

other mode, from one form, currency

or denomination, to another form,

currency or

denomination for which a separate

consideration is charged;

Ambit of Services have been extended beyond the

existing service tax law and covers everything other

than goods.

Works contract relating to immovable property is

considered as services.

Construction services deemed to be service

Food supplied in a restaurant is deemed to be service

Service

GST Impact on Service Sector_________________________________________________________________________

3| Schedules

GST Impact on Service Sector_________________________________________________________________________

SCHEDULE I

Activities to be treated as Supply even if made without

consideration

GST Impact on Service Sector_________________________________________________________________________

Permanent transfer or disposal of business assets where ITC has been availed on such assets

Supply between related or between distinct persons as specified in section25, when made in the course or furtherance of business

Gift exceeding fifty thousand rupees in value in a financial year by an employer to an employee

Import of services by a taxable person from a related person or from any of his other establishment outside India, in the course or furtherance of business

SCHEDULE II

Activities to be treated as Service

GST Impact on Service Sector_________________________________________________________________________

Transfer of right in goods or of individual share in goods without transfer of title

Lease, tenancy, easement, licence to occupy land or lease of letting out of building, renting of immovableproperty

Treatment or process which is applied to another person's goods(Job Work)

Goods meant for business usage put for private usage on direction of a person carrying on the business,with or without consideration

Construction of a building, except where the entire consideration is received after issuance of completioncertificate

Temporary transfer or right to use Intellectual Property Rights; development, designing of informationtechnology software; or right to use goods for cash, deferred payment or valuable consideration

Composite supply i.e. works contract or supply of goods fit for human consumption.

SCHEDULE III

Activities neither goods nor services

GST Impact on Service Sector_________________________________________________________________________

Services by an employee to the employer in the course of or in relation to his employment

Services by any court or Tribunal established under any law

Functions and duties performed by the Members of Parliament, State Legislature, Panchayats,Municipalities, local authorities, any post in pursuance of the provisions of the Constitution

Services of funeral, burial, crematorium or mortuary including transportation of the deceased

Actionable claims, other than lottery, betting and gambling

Sale of Land & Building subject to activity treated as service in case of Construction

4| Registration

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

A centralized registration is

available for service

providers under the

present regime

Registrations to be taken state-wise with a threshold of

limit of Rs. 20 lakh (Rs. 10 lakh for special category

States) ‘aggregate turnover’ in a financial year

Different registration can be taken for different business

verticals within a state at the option of the assessee.

-ve impact since registration has to be

obtained in every State of operation, if

required for business verticals as well.

This will increase compliances for service

providers.

Companies having PAN India operations will

treated as separate legal entity for each

registration even though they have a single

PAN.

Company to evaluate whether it is worth

having operations/warehouses in multiple

states.

Concept of Business Vertical is new.

As per the draft rules, SEZ and non SEZ

units

Registration

GST Impact on Service Sector_________________________________________________________________________

5| Time and place of supply

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

Earliest of the following –

1. Time when the invoice is issued if

issued within the prescribed limit, or

2. Date of completion of provision of

services, if invoice not issued within

the prescribed time limit, or

3. Time when payment is received

prior to (1) & (2)

Earliest of the following

1. Date on which the supplier issues the invoice

if issued within prescribed time limit or date of

payment which ever earlier; or

2. Date of provision of services, if invoice is not

issued within the prescribed time limit; or

3. Date on which the recipient shows the receipt

of the services in his books of accounts.

Time of supply under GST regime and

point of taxation under the service tax

Law remains same. There are no major

difference in the two.

Time of supply of services under forward

charge

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

Earliest of the following –

1. Date of payment to the service

provider.

2. Date immediately following

three months from the date of

invoice, if payment is not made

within three months.

Separately prescribed to be, earliest of –

1. Date on which payment is entered in the books or

debited in the bank account, or

2. Date immediately following sixty days from the date

of receipt of invoice, or

3. If not possible to determine from (1) & (2) Date of

entry in the books of accounts of recipient of supply.

Time limit for payment to service

providers has been reduced to 60 from

3 month in the present regime.

GST Impact on Service Sector_________________________________________________________________________

Time of supply of services under reverse charge

• Any supply where the location of the supplier and the place of supply are in different states.

Intrastate supply

• Any supply where the location of the supplier and the place of supply are in the same state.

Intrastate supply

Intra and Inter state supply of services

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

No Such Concept Supply of services in the course of interstate trade or

commerce means any supply where the location of the

supplier and the place of supply are in different states.

Intrastate supply of services means any supply where the

location of the supplier and the place of supply are in the

same state

-ve impact

Particulars Current Regime GST Regime Impact

General Provision Location of the service recipient Place of service recipient, if not known

then the place of supplier

No Change

Service provided directly in

relation to an immovable property

Place where the immovable property

is located or intended to be located.

Place where the immovable property is

situated.

No change

Performance based services -

(restaurant, personal grooming,

fitness, beauty treatment, health

services)

Location where the services are

actually performed.

Place of services actually performed. No change

Service in relation to training &

performance appraisal

Location where the services are

actually performed.

If provided to a registered person location

of such person, if not registered the place

of performance.

If provided to registered

person the Place of

supply shall be the

location of such person.

Services by way admission to

cultural event

The place where the event is actually

held .

The place where the event is held No Change

Services by way of organizing

event

The place where the event is actually

held .

If provided to registered person, the place

of such person, if not the place of event.

If event held outside India, location of the

recipient

If provided to registered

person, the place of such

person shall be the place

of supply.

Advertisement Services to

Central/State/UT/Statutory

body/local Authority

No such concept Each such state/UT and value shall be

proportionate to such state/UT.

Negative Impact

Place of Supply of Services

GST Impact on Service Sector_________________________________________________________________________

Particulars Current Regime GST Regime Impact

Services by way of

transportation of goods, mail or

courier

Place of destination of goods. If provided to registered person,

location of such person, if not location

of goods at which such goods are

handed over.

If provided to registered

person, the place of such

person shall be the place of

supply.

Passenger transportation

Services

Place where the passenger

embarks on the conveyance

for a continuous journey

If provided to registered person,

location of such person, if not the

place of embarkation.

If provided to registered

person, the place of such

person shall be the place of

supply.

Services on board a

conveyance

The first scheduled point of

departure of that conveyance

for the journey

location of first scheduled departure of

such conveyance.

No Change

Banking & Financial Services Location of the service

provider.

Location of recipient of services on the

records of the supplier, if not the

location of the supplier.

Location of service recipient

shall be the place of supply.

Insurance Services No such concept If provided to registered person then

the location of such person, if not the

location of recipient as per the records

of the supplier.

Location of service recipient

shall be the place of supply.

Online Information and

database retrieval service

B to B transaction- the

location of service recipient

B to C transaction – the

location of service provider

B to B transaction- the location of

service recipient

B to C transaction – the location of

service provider

No Change

Place of Supply of Services

GST Impact on Service Sector_________________________________________________________________________

6| Taxable Value

GST Impact on Service Sector_________________________________________________________________________

Current Regime GST Regime Impact

Section 67 of the Finance Act 1994,

provide for valuation of taxable services –

1. Gross amount charged for services

provided, whether received in the

form of money or not.

2. Service tax determination of Value

rules prescribe rules for special

category services.

3. Notification 26/2012 provides for

various abatement schemes for the

determination of taxable value

Transaction value(TV) based valuation;

clarity on the inclusion/ exclusion of specific

transaction under the GST regime.

Post sale discount is allowed provided it is

mentioned in the agreement, known at the

time of supply and discount is linked to

specific tax invoices;

+ve impact due inclusion of post-sale

discount in calculating the transaction value.

Subsidy may form part of TV. This could

have -ve impact.

Company to carefully evaluate which

subsidies could impact valuation.

Where the value can’t be determined,

valuation rules would be resorted to, if not

Values may be notified in the manner

prescribed

Company also needs to track each post sale

discount to the relevant invoice. Accounting

will be cumbersome.

Valuation- Taxable value

GST Impact on Service Sector_________________________________________________________________________

Particulars Consideration Value

Goods &

Services

Consideration is not wholly in

money

a. Open market value

b. Money + money equivalent of the

consideration paid in Kind if such

amount is known at the time of supply

c. Like kind and quality

d. Money + money equivalent to the

consideration not in money as it can

be determined under Rule 4 or 5.

Rule 1: Valuation where consideration not

wholly in money

GST Impact on Service Sector_________________________________________________________________________

Notes:

Sub-rules a, b, c and d to be applied sequentially.

Rule 2: Value of supply of goods or services or both between

distinct or related persons, other than through an agent

Supply Consideration Parties Value

Goods / Services Not specified Related / distinct

person (S.25(4), (5))

Supply not made

through an agent

a. Open market value

b. Like kind & quality

c. As determined under rule 4

or rule 5

Provided where the recipient is eligible for full input tax credit, the value declared in the

invoice shall be deemed to be the open market value of goods or services.

NOTES

Distinct persons i.e. having multiple registrations or multiple establishments as under S.

25(4), (5) of the CGST Act.

Sub-rules a, b, and c to be applied sequentially.

GST Impact on Service Sector_________________________________________________________________________

Rule Conditions Valuation

Rule - 4 (Value of supply of goods or

services or both based on cost)

Where the value of supply of goods or

services or both is not determinable by any

of the preceding rules ( 1to 3)

Provided that in case of service provider,

directly rule 5 can be applied.

110% of the Cost of Production or

manufacture or cost of acquisition of such

goods or cost of provision of such services

Rule – 5 (Residual Method for

determination of value of supply of

goods and services or both)

Where the value of supply of goods or

services or both is not determinable by any

of the preceding rules ( 1 to 4)

Value shall be determined on reasonable

basis

Rule 7: Value of supply of services in

case of pure agent

Non obstante clause to exclude the

expenditure or costs incurred by the supplier

as a pure agent of the recipient of supply of

services from the value of supply, provided

all conditions of the Rule are fulfilled.

Rule 4, Rule 5 & Rule 7

GST Impact on Service Sector_________________________________________________________________________

Rule 6: Valuation under specific cases

GST Impact on Service Sector_________________________________________________________________________

Purchase or sale of foreign currency

Booking of air ticket through an agent

Life insurance

Token, Voucher or coupon redeemable against supply of service

Nil Value to be notified in specified cases

Current Regime GST Regime Impact

The concept of composition

scheme is not available in the

present regime for service

providers

• Applicable in case aggregate turnover upto 50 Lakhs

• Composition Scheme is not applicable for supplier of

service expect person engaged in composite supply

of food or any other article for human consumption.

Composite supply of food or any other article

for human consumption , as they have the

option of discharging tax on %age of

turnover.

Works Contract, since treated as service, no

more eligible for composition levy

Composition scheme

GST Impact on Service Sector_________________________________________________________________________

7| Credit

GST Impact on Service Sector_________________________________________________________________________

Particulars Current Regime GST Regime Impact

Cross utilisation of

credits

No input tax credit of the

VAT/CST paid on procurement

of goods against the Service

Tax liability.

Credit is available and hence,

seamless flow of credit.

Huge benefit to the Service community.

Impact on working capital will be reduced

due to allowance of credit of goods.

Import of

machineries –

SAD/CVD

Component

SAD paid on import of

machineries is cost in the

present regime.

CVD credit is eligible

No concept of SAD/CVD; IGST

credit can be utilised against the

SGST/IGST liability.

Service providers can utilise the IGST

credit on imported goods.

+ve impact as the net cash outflow will be

reduced due to availability of credit.

Reversal of Cenvat

credit

For a Trader-cum-Service

Provider, trading activity

considered as exempt service

and hence, reversal of

CENVAT Credit.

No such provision proposed; shall

be taxed due to the taxable event

being ‘Point of Supply’ (POS).

Reduction in complication of reversal of

cenvat due to seamless flow of credit

between goods and services.

Credit

GST Impact on Service Sector_________________________________________________________________________

Particulars Current Regime GST Regime Impact

Input tax credit/

CENVAT credit

Credit under VAT laws cannot

be used to discharge Central

tax liability and vice-versa;

Further, CST on inter-state

procurement is a cost to the

company

CGST allowed for CGST/IGST;

SGST allowed for SGST/IGST

IGST allowed for

IGST/CGST/SGST in the said order

+ve/ -ve impact - free flow of credit is a boon,

however, the same is subject to humungous

compliances, which shall inter alia include

matching of invoices, supplier making

payment of tax, submission of multiple of

returns, etc.

Vendor Management Policy/Credit period to

be re-looked to withhold payments until tax is

paid by the supplier

Return to be filed by the person availing the

credit compulsory in order to claim credit

Input Tax Credit Currently there are

restrictions

Restrictions shall continue. Input Credit to be tracked closely

Compliances Only two returns were

required to be filed in a year

and there are no requirement

to file invoice-wise details of

the sales & purchases under

the present regime.

Greater compliance since the

seller’s data is to match the

purchaser’s data;

-ve impact on availability of credit due to

matching of seller’s data with purchaser’s

data

Credit

GST Impact on Service Sector_________________________________________________________________________

Particulars Current Regime GST Regime Impact

Input Service

Distributor

ISD shall distribute the Cenvat credit to units,

subject to the following conditions –

The credit distributed against a

documents as prescribed in rule 9, does

not exceed the amount of service tax paid

thereon.

Credit of service tax attributable to service

used in a unit exclusively engaged in

manufacture of exempted goods or

providing exempted services shall not be

distributed.

The ISD shall distribute the credit of CGST,

SGST, UTGST and IGST to various recipients

in different states or same states having

different Business Verticals in such manner as

may be prescribed.

Pro-rated distribution of Input Tax Credit in

case of outputs being taxable (including zero-

rated supply) as well as exempt supplies

(based on the turnover).

Credit can be distributed against prescribed

document issued to each of the recipient

Distribution of

credit shall be

subject the

methods and

formulas

prescribed under

the Input Tax

Credit Rules.

Credit

GST Impact on Service Sector_________________________________________________________________________

Distribution of credit

Credit distribution by

ISD

IGST

Transferred as IGST Only

CGST/SGST

If Recipient and ISD are in

same state

CGST can be transferred as

CGST

SGST can be transferred as

SGST

If Recipient and ISD are in different states

Credit can e transferred as

IGST

GST Impact on Service Sector_________________________________________________________________________

8| Refunds and Returns

GST Impact on Service Sector_________________________________________________________________________

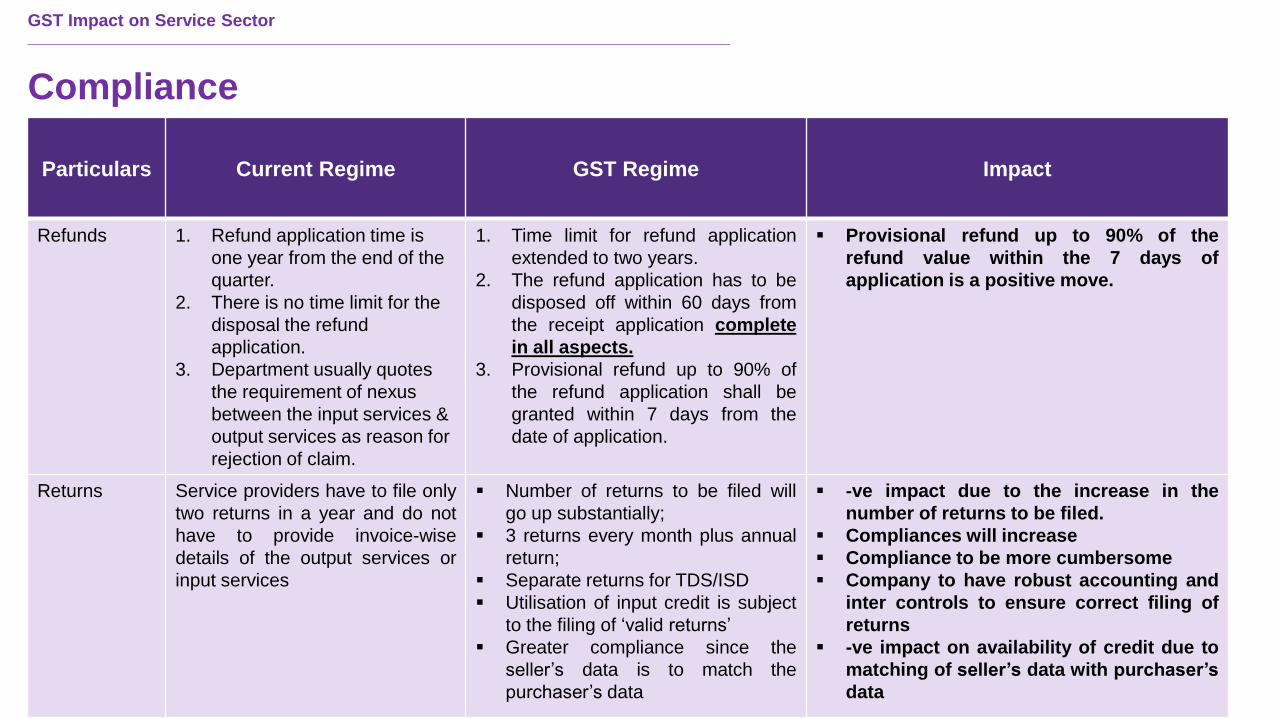

Particulars Current Regime GST Regime Impact

Refunds 1. Refund application time is

one year from the end of the

quarter.

2. There is no time limit for the

disposal the refund

application.

3. Department usually quotes

the requirement of nexus

between the input services &

output services as reason for

rejection of claim.

1. Time limit for refund application

extended to two years.

2. The refund application has to be

disposed off within 60 days from

the receipt application complete

in all aspects.

3. Provisional refund up to 90% of

the refund application shall be

granted within 7 days from the

date of application.

Provisional refund up to 90% of the

refund value within the 7 days of

application is a positive move.

Returns Service providers have to file only

two returns in a year and do not

have to provide invoice-wise

details of the output services or

input services

Number of returns to be filed will

go up substantially;

3 returns every month plus annual

return;

Separate returns for TDS/ISD

Utilisation of input credit is subject

to the filing of ‘valid returns’

Greater compliance since the

seller’s data is to match the

purchaser’s data

-ve impact due to the increase in the

number of returns to be filed.

Compliances will increase

Compliance to be more cumbersome

Company to have robust accounting and

inter controls to ensure correct filing of

returns

-ve impact on availability of credit due to

matching of seller’s data with purchaser’s

data

Compliance

GST Impact on Service Sector_________________________________________________________________________

9| Job work & E-Commerce

GST Impact on Service Sector_________________________________________________________________________

Job-work

Principal

Supply of goods , without payment of Tax

Job worker

Return of goods, Job work charges

No tax on transfer of goods to Job worker by principal

Principal eligible for input tax credit

Bring back inputs/capital goods, within a period of one/three years respectively.

If not brought back within the prescribed time limit, will be treated as taxable supply at the time when the same

is sent to job worker.

The job-work charges shall be taxed as services as per entry no. 3 in Schedule II of the CGST Act.

GST Impact on Service Sector_________________________________________________________________________

Particulars Current Regime GST Regime Impact

E Commerce E commerce operators

treated as traders.

However, registered

vendors are discharging

tax.

TCS @ 1% on net value of supplies for E

commerce operators for supplies made

through them.

Central Government may notify categories of

services, tax on intra state supplies of such

services shall be paid by the E commerce

operators if such services are supplied through

it.

Burden of payment of tax has been

shifted from the registered vendor to the

e-commerce operators.

In case of any input-output mismatch, the

liability of matching the invoices rests

with the e-commerce operators

E-Commerce

GST Impact on Service Sector_________________________________________________________________________

10| SEZ, EOU & STPI

GST Impact on Service Sector_________________________________________________________________________

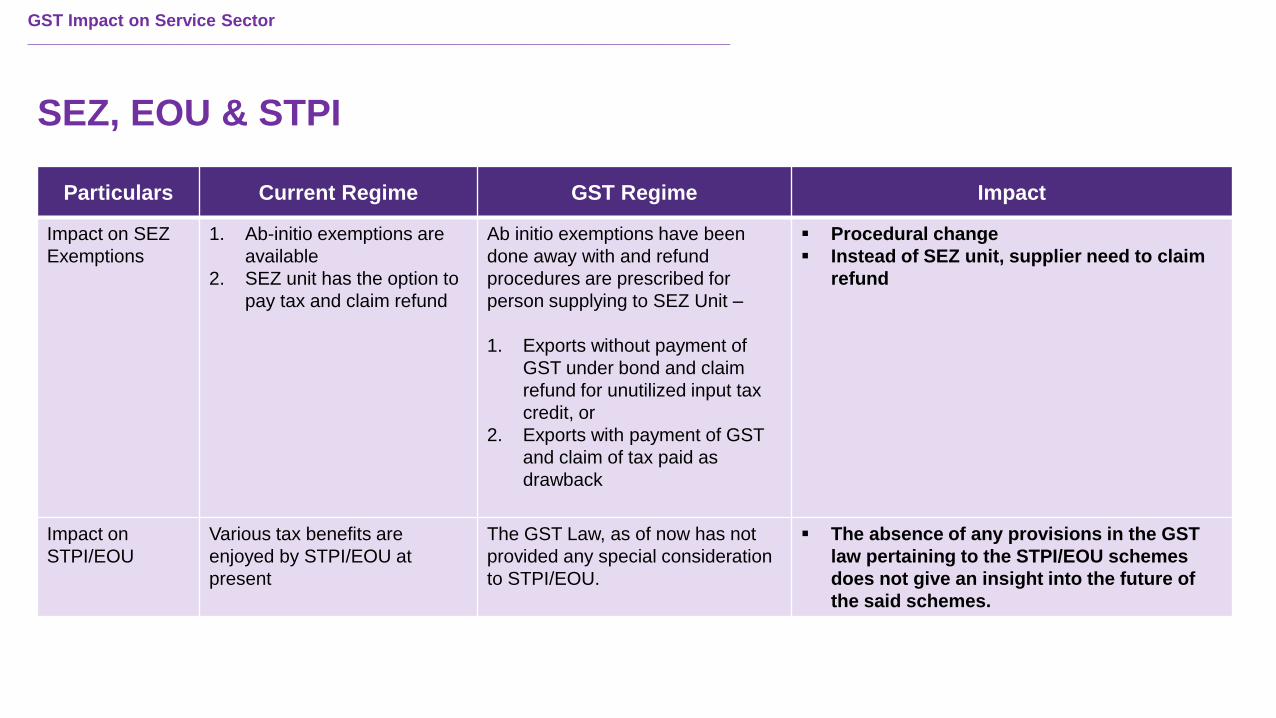

Particulars Current Regime GST Regime Impact

Impact on SEZ

Exemptions

1. Ab-initio exemptions are

available

2. SEZ unit has the option to

pay tax and claim refund

Ab initio exemptions have been

done away with and refund

procedures are prescribed for

person supplying to SEZ Unit –

1. Exports without payment of

GST under bond and claim

refund for unutilized input tax

credit, or

2. Exports with payment of GST

and claim of tax paid as

drawback

Procedural change

Instead of SEZ unit, supplier need to claim

refund

Impact on

STPI/EOU

Various tax benefits are

enjoyed by STPI/EOU at

present

The GST Law, as of now has not

provided any special consideration

to STPI/EOU.

The absence of any provisions in the GST

law pertaining to the STPI/EOU schemes

does not give an insight into the future of

the said schemes.

SEZ, EOU & STPI

GST Impact on Service Sector_________________________________________________________________________

11| Transitional Provisions

GST Impact on Service Sector_________________________________________________________________________

Transitional Provisions

• Migration of existing taxpayers - All registered persons under existing laws & having a valid PAN shall be given provisional RC which would beliable to cancellation if the conditions as prescribed are not complied with.

• Amount of CENVAT Credit carried forward to be allowed as ITC - A registered person, other than a composition dealer, may take eligible ITCcarried forward in the return furnished under existing law.

• Amount of credit on Capital Goods not carried forward to be allowed in certain cases not availed under current law - A registered person,other than a composition dealer, may take credit of un-availed CENVAT credit not carried forward in respect of CG in the return furnished underexisting law.

• Credits in respect of inputs in case the supplier is providing exempt supplies under existing laws - Eligible ITC based on invoices issuednot earlier than 12 months is available on inputs, semi finished goods and finished goods in stock as on the appointed day, if they are used inproviding taxable supplies under the GST Act.

• Credits in respect of inputs in case the supplier is providing both taxable and exempt supplies under existing laws – A registeredperson, who was engaged in providing both taxable and exempted supplies, shall be entitled to take credit carried forward in return and credit ofeligible duties in respect of inputs held as stock relating to exempted goods or services if the same is to be used for making taxable supplies underGST law.

• Credit of Input & Input Services in Transit - Credit on duty paid is allowable if duty is paid under the existing & entered in books within 30 daysfrom appointed day.

• Transitional provisions for ISD - The ITC on account of any service received prior to appointed day by ISD shall be eligible for distribution ascredit under this Act even if the invoice is received after the appointed day.

GST Impact on Service Sector_________________________________________________________________________

Transitional Provisions

• Unutilized credit through centralised Registration – Eligible credit may be taken if the same is carried forward in the last return in respect ofthe period ending with the day immediately preceding the appointed day

• CENVAT Credit reversed for non payment of consideration to supplier - Where the CENVAT credit availed on input services under theexisting law is reversed for the non payment of consideration to the supplier, such credit can be reclaimed if the consideration is paid within 3months from the appointed day.

• GST not leviable when inputs/ semi-finished goods are sent to the job worker - If inputs/semi-finished goods sent to a job worker is receivedback to the place of business of the principal within 6 months from the appointed day, GST is not leviable. However, in case of delay, input taxcredit on the said inputs/semi-finished goods is recoverable as per the provisions of the GST law.

• Upward revision of prices / contracts - If price of goods/ services is revised upwards on or after the appointed day, the supplier has to issue asupplementary invoice/ debit note within 30 days of price revision, which shall be considered as an outward supply as per the GST law.

• Downward revision of prices/ contracts - If price of goods/ services is revised downwards on or after the appointed day, the supplier has toissue a credit note within 30 days of price revision, which shall be considered to have been issued in respect of an outward supply as per the GSTlaw.

GST Impact on Service Sector_________________________________________________________________________

Thank You !