23

Governance, Transparency and Good Portfolio Management with Internet-based Tools www.mcubeit.com Dr. Arun Muralidhar

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | alden-farmer |

| View: | 18 times |

| Download: | 1 times |

Governance, Transparency and

Good Portfolio Management with

Internet-based Tools

www.mcubeit.com Dr. Arun Muralidhar

2

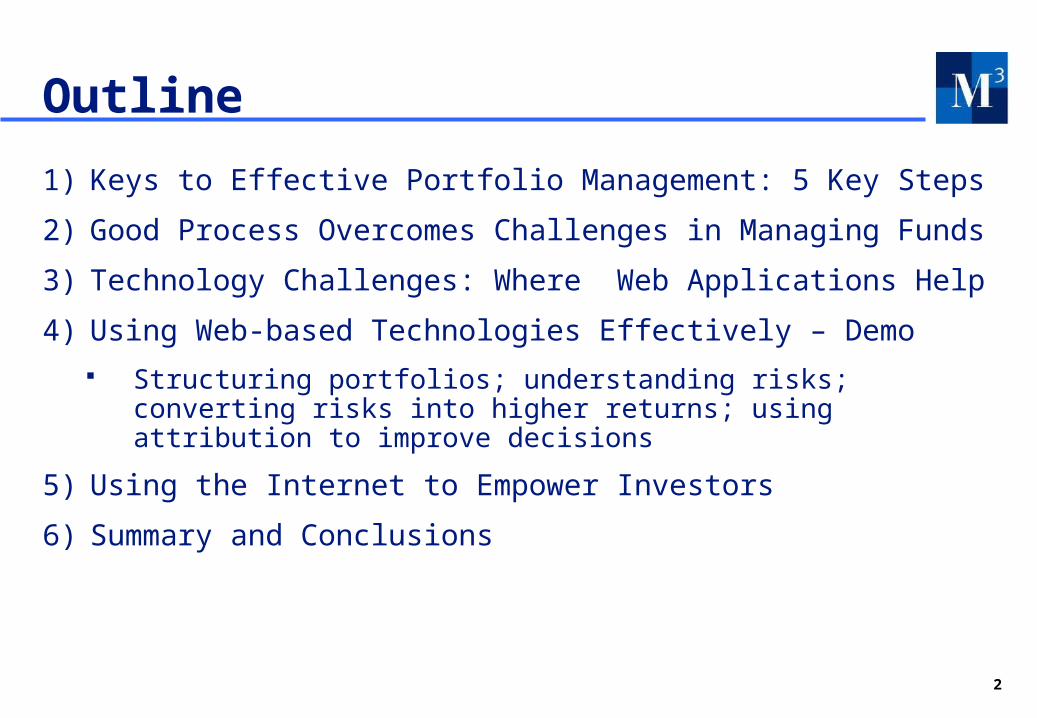

Outline

1) Keys to Effective Portfolio Management: 5 Key Steps

2) Good Process Overcomes Challenges in Managing Funds

3) Technology Challenges: Where Web Applications Help

4) Using Web-based Technologies Effectively – Demo

Structuring portfolios; understanding risks; converting risks into higher returns; using attribution to improve decisions

5) Using the Internet to Empower Investors

6) Summary and Conclusions

3

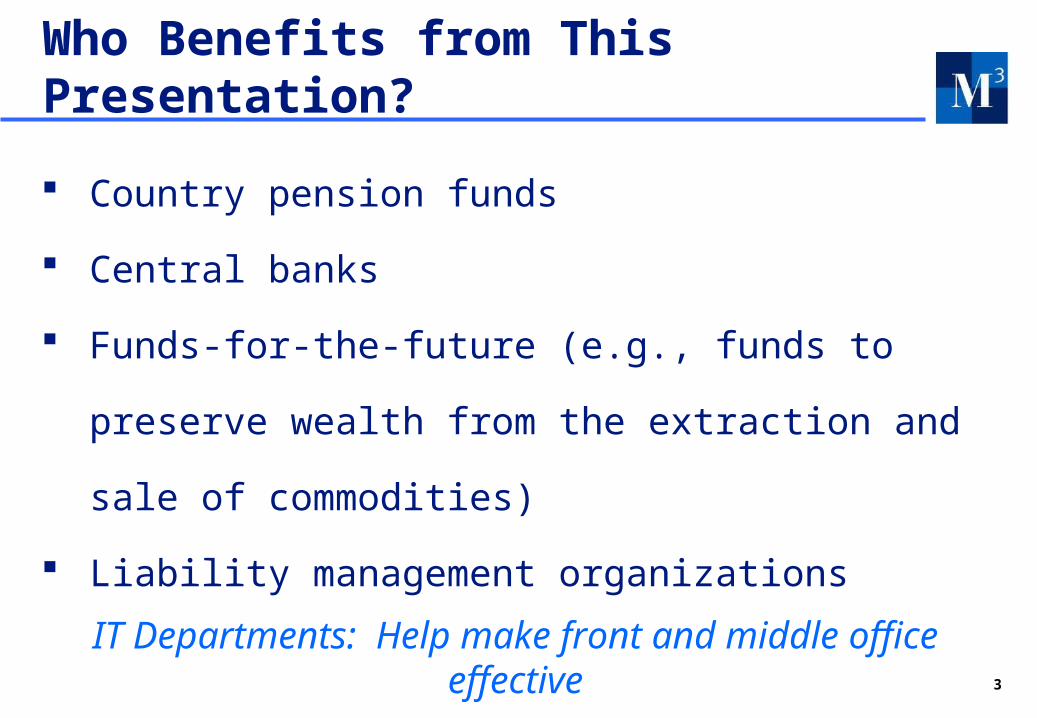

Who Benefits from This Presentation?

Country pension funds

Central banks

Funds-for-the-future (e.g., funds to preserve

wealth from the extraction and sale of

commodities)

Liability management organizations

IT Departments: Help make front and middle office effective

4

1. Key to Success – Effective Decisions

Good management = must make many decisions well

Must make these decisions in an informed manner

Process, transparency and governance are critical

Challenge: Can technology integrate front & back office?

Measure Risk

Evaluate Performance

Outperform Benchmark

Determine Benchmark

Set Objectives

Annual Daily MonthlyMonthly

5

1. Many Share Responsibility for a Fund

Asset-Liabilit

yRisk

Tactical & Benchmark

Risk

Manager/ActiveRisk

Responsibility

Monitor

Manage

Board of Governors

Internal Staff OutsideManagers

Annually Daily/Monthly Monthly

Strategic Decisions – Need Good Reporting

Effective Investment Decisions –

Need IT Support

ManagerSelection

Decisions – Good

Reporting

Responsibility

Decision Frequency

How to Manage the

Risk

Need good technology to track and manage all decisions

6

1. Portfolio =Many Decisions

Asset Allocation

Sector/ Region

al

Style Selectio

nManager Selection

Cash/Currency = 20%Equity = 40%

By Market (Local, US etc.)

Large Stocks/Small Stocks

By Market(Local, US, Euro)

Govt./Agency etc.

Bonds = 40%

P o r t f o l i o

Mgr

A

Mgr

B

Mgr

C

Mgr

D

Mgr

E

Mgr

F

Bank 1

for Deposit

s

Bank 2

for Deposit

s

7

1. Manage ongoing cash inflows and outflows

2. Evaluate and implement rebalancing

strategies

3. Manager selection and allocations

4. Asset, country, style, sector or currency

allocation

2. Challenges in Managing Portfolios

A portfolio is very dynamic – impacted daily.Each decision can be a source of return or,

if badly managed, can reduce returns

8

1. Resource constrained: financial (budget) and

staffing

2. “In public eye”: decisions are reviewed

publicly

3. Need to demonstrate that decisions not

political; need to show financial impact of

political constraints

4. Good governance and transparency critical

2. Challenges in Public Entities

Challenge: Can technology empower staff, to raise return and lower risk while

maintaining control?

9

SILO SYSTEMS – Narrow Applicability:

1) Focus on only one asset (stocks/bonds) or one

aspect (e.g., risk or performance

measurement; trading)

2) Multiple systems; high cost to

integrate/maintain

3) Required extensive training and client IT

backup

4) Not designed by people who managed funds

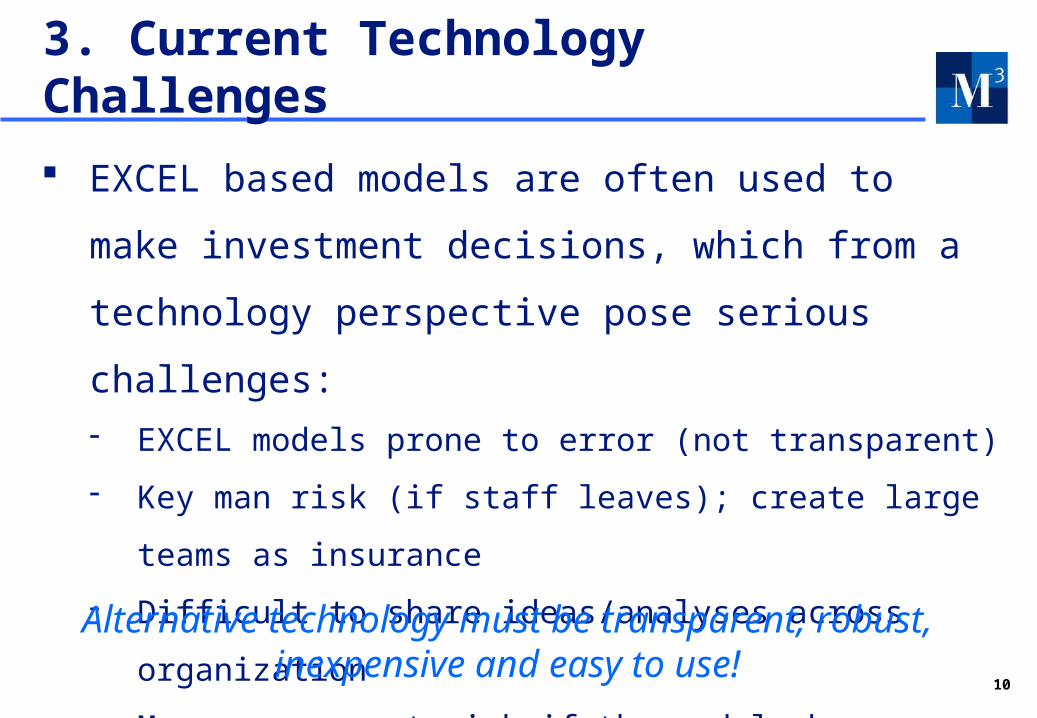

3. Current Technology Challenges

Senior managers are at risk – not knowing what is impacting the fund or how to correct

it

10

EXCEL based models are often used to make

investment decisions, which from a technology

perspective pose serious challenges: EXCEL models prone to error (not transparent)

Key man risk (if staff leaves); create large teams as

insurance

Difficult to share ideas/analyses across organization

Managers are at risk if the models have errors

3. Current Technology Challenges

Alternative technology must be transparent, robust, inexpensive and easy to use!

11

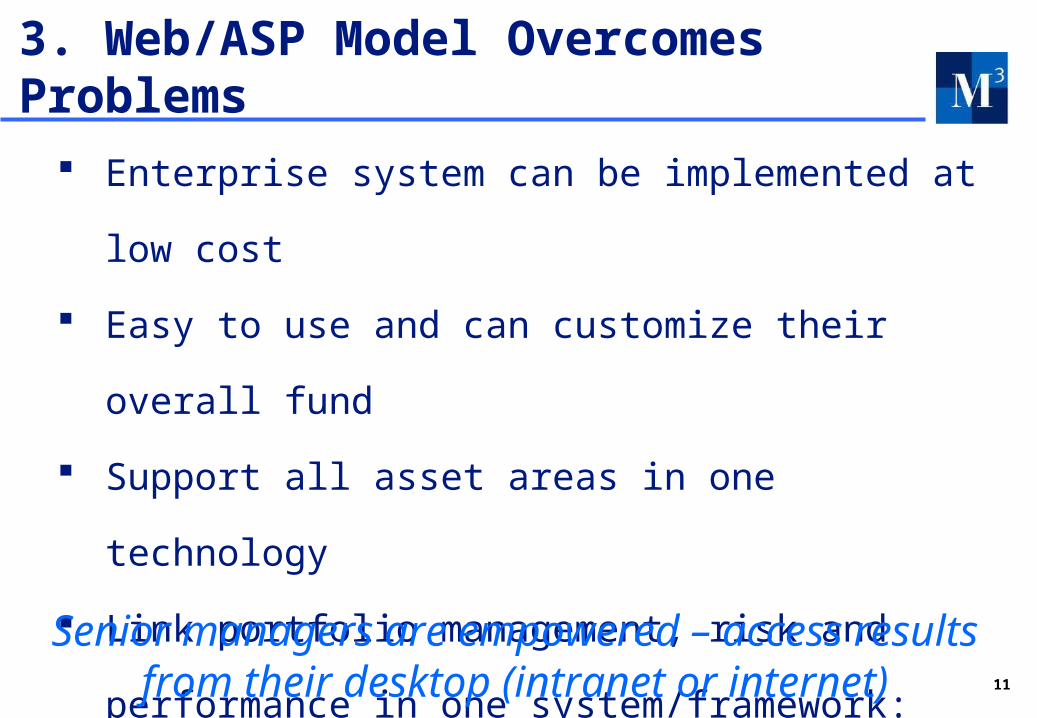

Enterprise system can be implemented at low

cost

Easy to use and can customize their overall

fund

Support all asset areas in one technology

Link portfolio management, risk and

performance in one system/framework:

transparent, flexible, quick

Data management can be simplified

3. Web/ASP Model Overcomes Problems

Senior managers are empowered – access results from their desktop (intranet or

internet)

12

Integrated system that allows user to follow specific process steps:

1. Specify a clear investment process (i.e., who makes

what decisions at what level of the fund) =

GOVERNANCE

2. Understand all the risks taken by the fund =

GOVERNANCE

3. Model decisions in a TRANSPARENT way (i.e., simple

so that anyone can understand/evaluate)

4. Attribute performance to improve decisions

4. Using Web-based Technologies Effectively

Governance, process & transparency = better returns

A Case Study:

13

Case Study: Step 1Articulate

Responsibilities/Decisions

Asset Allocation

Sector/ Region

al

Style Selectio

nManager Selection

Cash/Currency = 20%Equity = 40%

By Market (Local, US etc.)

Large Stocks/Small Stocks

By Market(Local, US, Euro)

Govt./Agency etc.

Bonds = 40%

P o r t f o l i o

Mgr

A

Mgr

B

Mgr

C

Mgr

D

Mgr

E

Mgr

F

Bank 1

for Deposit

s

Bank 2

for Deposit

s

14

Case Study: Step 2Use Portfolio Tree to Pinpoint

Risk

Risk= 1.5%

Maximum Drawdown = -7.5%

Structuring risk at total fund level=1.5% (or $300 mn)

From asset allocation and style tilts (excludes managers)

From allocations to assets other than fund benchmark

Allocation decisions have historically had big drawdowns

Risk = 1.5%

Maximum Drawdown = -5.5%

Risk = 3.2%

Maximum Drawdown = -11%

Risk = 1.8%

Maximum Drawdown = -6.8%

Pension

Fund

15

Case Study: Step 3Ensure Decisions Generate

Returns

Excess Return = 0.5%

Excess Return = 0.5%

Excess Return = 0.5%

Total Excess = 2%

Local Bonds Foreign bonds

Mortgage/Corporate

GovernmentBonds

Bonds

Total Portfolio

Equities CurrencyCash

1-mo LIBOR

Asset allocation strategy

Country allocation strategy

Sector allocation strategy

+

+

Manager Excess Return = 0.5%

+

Internal/External Managers

16

Local Bonds Foreign bonds

Mortgage/Corporate

GovernmentBonds

Bonds

Total Portfolio

Equities CurrencyCash

1-mo LIBOR

Naïve Rebalancing

Let Portfolio Drift

Sector allocation strategy

Internal/External Managers

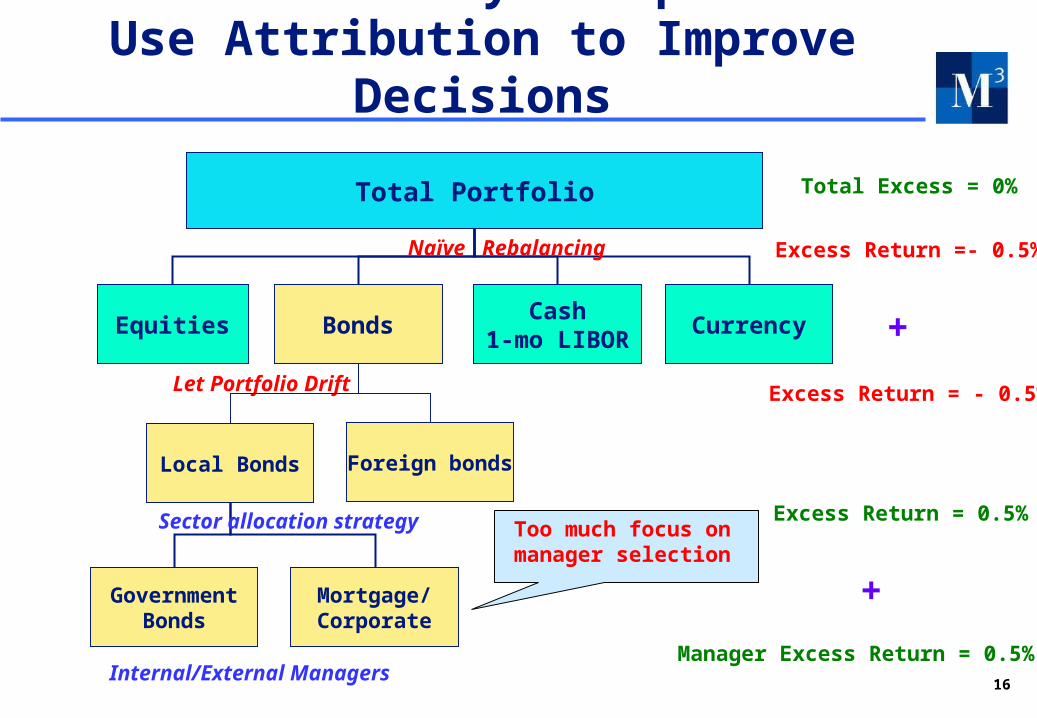

Case Study: Step 4Use Attribution to Improve

Decisions

Excess Return = 0.5%

Excess Return = - 0.5%

Excess Return =- 0.5%

Total Excess = 0%

+

Manager Excess Return = 0.5%

+

Too much focus on manager

selection

17

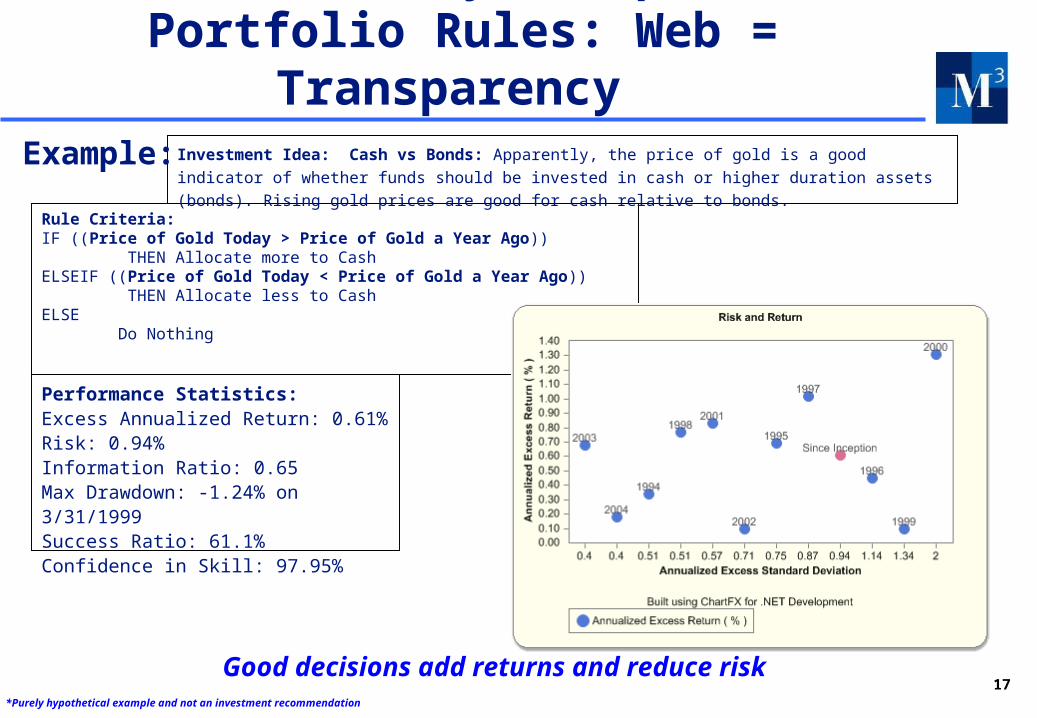

Case Study: Step 5Portfolio Rules: Web =

Transparency

Good decisions add returns and reduce risk

Rule Criteria: IF ((Price of Gold Today > Price of Gold a Year Ago)) THEN Allocate more to CashELSEIF ((Price of Gold Today < Price of Gold a Year Ago)) THEN Allocate less to Cash ELSE Do Nothing

Investment Idea: Cash vs Bonds: Apparently, the price of gold is a good indicator of whether funds should be invested in cash or higher duration assets (bonds). Rising gold prices are good for cash relative to bonds.

Performance Statistics:Excess Annualized Return: 0.61%Risk: 0.94%Information Ratio: 0.65Max Drawdown: -1.24% on 3/31/1999Success Ratio: 61.1%Confidence in Skill: 97.95%

Example:

*Purely hypothetical example and not an investment recommendation

18

Case Study: Step 6Deliver Detailed Reports Through

WebPerformance Measures

Benchmark

Strategy

Return % 6.47 9.25

Cum. Return % 36.79 55.64

Risk % 2.28 5.58

Return / Risk Ratio 2.84 1.66

Excess

2.78

18.85

3.55

0.78

Success ratio of the rule %

Average returns when positive %

Average returns when negative %

Max. consecutive periods of positive returns

Max. consecutive periods of negative returns

Max. relative loss for a period %

70 56.67

1.51 0.86

-1.02 -0.60

7 7

4 5

-2.54 -1.99

Success ratio of the rule %Success ratio of the rule %

Average returns when positive %Average returns when positive %

Average returns when negative %Average returns when negative %

Max. consecutive periods of positive returnsMax. consecutive periods of positive returns

Max. consecutive periods of negative returnsMax. consecutive periods of negative returns

Max. relative loss for a period %Max. relative loss for a period %

70 70 70 56.67 56.67 56.67

1.51 1.51 1.51 0.86 0.86 0.86

-1.02 -1.02 -1.02 -0.60 -0.60 -0.60

7 7 7 7 7 7

4 4 4 5 5 5

-2.54 -2.54 -2.54 -1.99 -1.99 -1.99

StrategyStrategyStrategy ExcessExcessExcess

19

1. Boards/Senior Managers can set fund structure

and monitor all decisions easily

2. Portfolio managers can use to make better

decisions

3. Middle office can use to evaluate

risks/performance

4. Web-technology for 3 Ms of Portfolio

Management: “Measure”, “Monitor” and

“Manage”

5. Mcube IT: Better Governance/Returns Through Web Applications

20

6. Summary & Conclusions Portfolio management = many decisions and requires many

groups to coordinate (board, front office, back office, external managers)

Silo systems make it difficult and expensive to manage fund

Web (internet/intranet) can overcome challenges

Can create customized portfolio structure, analysis and reports

Can create transparency for good governance, returns and risk management

AlphaEngineTM: adopt best practices quickly and easily

AppendixAppendix

22

Rule Rule DescriptionCash vs. Bonds, based on Gold

Duration choice based on price of gold. If the spot price of gold is higher than it was a year ago, overweight cash, otherwise overweight bonds

Stocks vs Bonds: Halloween Effect

Stocks tend to underperform bonds between June and Sept - apparently works in 16 out of 18 stock markets, so underweight stocks during this period

Stocks vs Bonds: Inflation/Growth

Equities undervalued when inflation rises (Modigliani-Cohn insight); equities favored when industrial production is increasing

Market Volatility Low equity volatility in a rising stock environment is bullish for equities.Oil and Economy Rising oil prices affect the economy and tend to depress equities.P/E Ratio Rule Value rule for equity (vs FI) using the S&P 500 P/EFed Model When equity yield is higher than treasury yield then buy equity, else

sell equityUnemployment Rate Buy stocks when the unemployment rate is falling (good for economy)US/International: LIBOR Rates

Overweight equity market with the stronger currency (higher interest rate)

US/EAFE: Favor Underperformer

Overweight equity market which has underperformed over past year (i.e., buy the laggard)

5. Converting Ideas To Rules to Give Good Process and Add Value

23

Rule Performance (1998-2004)

Rule

Excess Annualized

ReturnInformation

RatioConfidence

in SkillSuccess Ratio

Ratio Good /Bad Risk

Max Drawdown

Cash vs. Bonds, based on Gold 0.04% 0.20 68.8% 56.4% 1.30 -0.44%

Halloween Effect 0.98% 0.88 98.0% 63.8% 1.42 -1.58%

Inflation/ Growth 0.50% 0.57 93.1% 79.7% 1.07 -1.31%

Market Volatility 0.12% 0.11 67.8% 56.4% 1.41 -2.74%

Oil and Economy 0.45% 0.57 91.6% 70.5% 1.16 -0.84%

P/ E Ratio Rule 0.17% 0.39 87.1% 50.0% 2.12 -0.80%

Fed Model 0.47% 0.50 91.8% 61.5% 1.43 -2.17%

Unemployment Rate 0.51% 0.61 94.1% 59.0% 0.99 -1.11%

US/ EAFE: LIBOR Rates 0.17% 0.43 84.7% 55.1% 1.07 -0.71%

US/ EAFE: Favor Underperformer 0.53% 0.95 99.3% 64.1% 1.33 -1.07%