1 Government Guaranteed Small Business Loans and Regional Growth Yong Suk Lee a, * a Freeman Spogli Institute for International Studies, Stanford University, Stanford 94305, USA November 5, 2017 Abstract This paper examines the impact of government guaranteed small business loans on regional growth. I construct a metro-level panel of the Small Business Administration’s guaranteed loans and examine economic growth between 1993 and 2002, across 316 metro areas in the US. A simple OLS regression finds a significant positive relationship between small business loans and regional growth. However, first-difference and instrumental variable regressions that mitigate endogeneity find no significant employment or income growth effects from small business loans. At least from an efficiency perspective, there seems to be no net gains to the regional economy from guaranteed small business loans. Keywords: Small Business Loans, Guaranteed Loans, Entrepreneurship, Regional Growth JEL Codes: L26, G18, K35, O18, R11 * Corresponding author at Freeman Spogli Institute for International Studies, Stanford University, 616 Serra Street, Email address: [email protected]

Transcript

1

Government Guaranteed Small Business Loans and

Regional Growth

Yong Suk Lee a, * a Freeman Spogli Institute for International Studies, Stanford University, Stanford 94305, USA

November 5, 2017

Abstract

This paper examines the impact of government guaranteed small business loans on regional

growth. I construct a metro-level panel of the Small Business Administration’s guaranteed loans

and examine economic growth between 1993 and 2002, across 316 metro areas in the US. A

simple OLS regression finds a significant positive relationship between small business loans and

regional growth. However, first-difference and instrumental variable regressions that mitigate

endogeneity find no significant employment or income growth effects from small business loans.

At least from an efficiency perspective, there seems to be no net gains to the regional economy

from guaranteed small business loans.

Keywords: Small Business Loans, Guaranteed Loans, Entrepreneurship, Regional Growth

JEL Codes: L26, G18, K35, O18, R11

* Corresponding author at Freeman Spogli Institute for International Studies, Stanford University, 616 Serra Street, Email address: [email protected]

2

Executive Summary

Despite the prevalence of financial policies that support small businesses, there is surprisingly

little research that examines how such policies affect regional economic growth. One of the most

widely used policy in this regard is the guaranteed loan program, whereby the government

guarantees a portion of the loans that financial institutions lend to small businesses. Given the

considerable interest policy makers have in supporting small businesses and creating jobs, the

lack of academic research on this topic is unfortunate. Scholars have examined the regional

growth consequences of entrepreneurship and how finance policies affect new venture creation.

However, we know little of how financial policies that promote new venture creation affect

regional growth. This paper's main objective is to empirically examine whether government

guaranteed small business loans indeed promote regional employment and income growth in the

United States.

A main challenge in empirically assessing the impact of small business loans on regional

economic growth is the fact that entrepreneurs tend to start businesses when the region’s

economy is doing well. In other words, a positive relationship between the number of small

business loans and regional growth may be driven by the good economic prospects of that region,

and it may not necessarily imply that the small business loans are causing regional growth. This

study addresses this empirical challenge by incorporating different econometric strategies – OLS

regressions, first-difference regressions, and instrumental variable regressions.

I match the Small Business Administration (SBA) loans data to each Metropolitan Statistical

Area (MSA) by year to create a metro-year level panel. I merge in various regional economic

data to this panel, and examine how SBA guaranteed loans affect regional employment and

income growth between 1993 and 2002 across 316 metro areas. A simple regression indicates

that the number of SBA loans to new businesses significantly and positively affects employment

and income growth. I then examine OLS regressions that control for initial regional

characteristics and Census Division fixed effects, first-difference growth regressions that control

for metro level fixed characteristics, and instrumental variable regressions using a variety of

instrumental variables. Despite using multiple econometric specifications, the results are

surprisingly robust. In all specifications, I consistently find that the impact of SBA guaranteed

3

loans on regional employment and income growth is statistically indistinguishable from zero,

and if any tends towards a negative effect.

This paper offers several contributions to the literature. First of all, this is one of the few papers

that examine the impact of guaranteed small business loans on regional growth. Moreover, to

the best of my understanding, I believe this is the first paper that aims to estimate the causal

effects. The findings from this paper indicate that there may be no net efficiency gains from

government guaranteed small business loans, but these results do not speak to the general value

of SBA loans. The main objective of SBA loans is to support small businesses that have

difficulty getting loans through conventional means because of the lack of collateral, inequality

in the lending market, and asymmetric information. Researchers have found that other finance

methods or policies, such as venture capital or government programs that support technology

startups do promote regional growth. The literature that examines the economic growth effects of

entrepreneurship finance policy is relatively nascent. Future research on this topic, together with

findings from this paper and extant research, would help better inform the policy implications of

entrepreneurship finance policies.

4

1. Introduction

Guaranteed loan programs are widely used to support small businesses around the world

(Parker 2009, Beck et al. 2008, 2010a, Lelarge et al. 2010, Mullins and Toro 2017). In these

programs, governments encourage banks to lend to small businesses by guaranteeing a portion of

the principal in case the debtor defaults. Though the principal aim of guaranteed loan programs is

to support small business creation and growth, they could have an effect on regional growth. The

literature has documented the positive relationship between entrepreneurship and regional

growth (Fritsch 1997, Audretsch and Fritsch 2002, Fritsch and Mueller 2008, Glaeser et al. 2010,

2015, Lee 2017), and between guaranteed loans and entrepreneurship (Riding and Haines 2001,

Riding et al. 2007). However, there is surprisingly little research that examines whether a finance

policy that supports small businesses indeed promote regional growth. Entrepreneurship is

widely considered as an important source of job creation. Many governments have utilized

finance policies, such as the guaranteed loan programs, to help create new ventures in hopes of

adding jobs to the regional economy. However, a substantial number of new ventures actually do

not survive, and ex-ante it is not clear whether a finance policy that promotes start-ups would

create jobs on net. Given the considerable interest policy makers have in supporting small

businesses and creating jobs, it would be valuable to know whether a finance policy that supports

small businesses indeed promote regional growth. To this end, this paper examines whether

guaranteed loans approved by the Small Business Administration (SBA) promote regional

employment and income growth in the United States.

Guaranteed small business loans could impact regional growth through their effect on the

quality and quantity of new ventures. The loans could support the creation of high quality new

ventures that could not get funding from conventional banks. However, there could be negative

selection as well. Loan guarantees could encourage banks to finance more low quality ventures

in expectation of being bailed out by the government, and could attract entrepreneurs with lower

entrepreneurial ability. In terms of quantity, guaranteed loans could add new ventures to the

regional economy, or could replace or crowd out ventures that would have gotten loans through

conventional means. Conceptually, guaranteed loans can have both a positive and negative effect

on the quality and quantity of new ventures. Hence, the impact of guaranteed small business

loans on regional growth would ultimately depend on the net quality and quantity of new

ventures, and how those new ventures relate to factors relevant for regional growth, e.g.,

5

knowledge spillover, agglomeration effects, competition between new ventures and incumbents,

and pre-existing regional characteristics.

The transmission of knowledge has become an increasingly important source of

economic growth. Scholars have found that new ventures are better at exploiting knowledge and

entrepreneurs serve as the link that facilitates the spillover of knowledge within the regional

economy (Audretsch and Taylor Aldridge 2009, Acs et al. 2009, 2013a). New ventures

contribute to the agglomeration benefits of input sharing and improved matching between firms

and workers (Jacobs 1969, Carlino et al. 2007). Also, new firms compete with incumbents in the

region, and such competition could affect aggregate economic growth (Fritsch 2013). Finally, the

regional environment can influence how new ventures affect regional growth. The skill level of

the region’s workforce affects how firms utilize new knowledge and technology, and how

incumbents adapt to new entry and competition. The pre-existing industrial structure also affects

new venture creation and regional growth (Sternberg 2009). The net result from all these

different channels would determine how the new ventures created through SBA loans affect

regional growth. In this regard, identifying the net impact of SBA loans on regional growth

ultimately becomes an empirical exercise.

However, there is surprisingly little empirical research that causally examines this

question, and justifiably so - endogeneity hinders causal interpretation. This paper’s main

objective is to examine the aggregate impact of small business loans on regional employment

and income growth, while alleviating the endogeneity concerns that typically arise in such

analysis. Specifically, I match the SBA loans data to each Metropolitan Statistical Area (MSA)

by year and create an MSA-year level panel of new SBA loans. I then examine how the SBA

guaranteed loans affect regional employment and income growth between 1993 and 2002. A

standard OLS regression indicates that the number of new SBA loans significantly and positively

affects employment and income growth. However, if cities with higher growth potential have

more SBA loan applications and approvals, then the OLS estimates would overstate the true

impact of SBA loans on urban growth. To the contrary, if cities that were declining see higher

SBA loan applications and approvals, then the OLS estimates would be biased downwards.

Including variables that control for initial regional characteristics and Census Division fixed

effects substantially reduces the positive effect and the statistical significance of the coefficient

estimates. To further alleviate endogeneity, I examine the first-difference and instrumental

6

variable regressions and compare the results to the OLS estimates. The results indicate that the

impact of SBA guaranteed loans on regional employment, payroll, and wage growth are

statistically indistinguishable from zero, and if any tend towards a negative effect. Though fully

resolving endogeneity is difficult, comparing results from the different estimation methods shed

light on what the true impact might be, and this paper consistently find no evidence indicating

that government guaranteed small business loans have an effect on regional growth.

Prior research that examine the relationship between entrepreneurship and regional

growth generally find positive associations that vary depending on time, region, and firm size

(Audretsch and Fritsch 2002, Fritsch and Mueller 2008, Acs and Mueller 2008). Glaeser et al.

(2015) and Lee (2017) use quasi-experimental designs and find that entrepreneurship indeed has

a positive causal impact on regional employment and income growth. However, these papers

examine entrepreneurship in general, without focusing on the different types of financing

methods or finance policies that contribute to the creation of new ventures. Craig et al. (2007)

examine the impact of SBA loans on county growth in the United States and find statistically

significant effects that are positive but economically small in magnitude. However, they focus on

the short-term impact, i.e., the one-year after effect, of SBA loans on per capita income. I

examine regional growth over a longer time horizon and further tackle endogeneity by using

instrumental variable regressions. My paper contributes to the literature by conceptualizing how

a finance policy that aims to promote entrepreneurship and small businesses could influence

regional growth, and by empirically examining the causal impact of government guaranteed

small business loans on regional growth.

2. Small Business Loans and Regional Growth – a Theoretical Examination

2.1. New venture creation and regional growth

A relatively rich literature has examined new venture creation and net regional employment.

Fritsch (1997) initially finds a weak association between new firm formation and regional

employment growth in West Germany over a short period of time. However, Audretsch and

Fritsch (2002) and Fritsch and Mueller (2008) find that the regional growth effects from

entrepreneurship are not constant and vary over time and across regions. These results suggest

that pre-existing regional factors - e.g., incumbent firms, industrial structure, etc. - are important

to entrepreneurship's contribution to regional growth. Moreover, Acs and Mueller (2008) find

7

that the employment effects from new ventures differ by firm size. They find that start-ups with

greater than 20 and less than 500 employees are related to persistent employment growth.

Despite these findings, identifying the causal effect of entrepreneurship on regional growth

remains a challenging task. Forces that promote regional growth also promote local

entrepreneurship, and thus parsing out the causal relationship is difficult. If new venture creation

has no relevance for regional growth, small business loan policies that promote local

entrepreneurship would likely have little relevance for regional growth as well. Hence, knowing

whether or not entrepreneurship causally increases regional growth is fundamental to the

question of whether small business loan policies promote regional growth. Though still in its

nascent stage, recent research has made some progress using quasi-experimental designs, and we

now have some convincing evidence that show that entrepreneurship and the density of small

businesses indeed have a causal impact on regional growth (Glaeser et al. 2015, Lee 2017).

These quasi-experimental analyses confirm the positive impact of entrepreneurship on regional

growth, but speak little to the channels by which entrepreneurship generates regional growth.

The transmission of knowledge has become an increasingly important source of

economic growth and scholars have found that new ventures and entrepreneurs play an important

role in facilitating knowledge spillover. Both new ventures and incumbent firms innovate from

new knowledge spillovers, but incumbents are more likely to make incremental changes,

whereas new ventures are more likely to generate radical innovation (Acs et al. 2009, 2013a).

Also, Audretsch and Taylor Aldridge (2009) find that entrepreneurs serve as the link that

facilitates the spillover of knowledge in the regional economy. Moreover, knowledge spillover

tends to be local. The physical proximity helps facilitate the spread of knowledge among firms

and workers within the same region (Jaffe et al. 1993, Audretsch and Feldman 1996).

Relatedly, the density of the region also affects the relationship between entrepreneurship

and regional growth because of agglomeration benefits. There are benefits of agglomeration not

only through knowledge spillover, but also through input sharing and the improved matching

between firms and workers. The benefits of agglomeration are real and have been empirically

identified in both the service sector (Arzaghi and Henderson 2008), as well as the manufacturing

sector (Greenstone et al. 2010). Moreover, Rosenthal and Strange (2003) identify a direct

spillover effect of entrepreneurship. New firm births spurs additional entrepreneurship nearby,

and such effect decays with distance.

8

Entrepreneurship also induces competition between new ventures and incumbent firms.

The growth of incumbent firms induced by the competition from new ventures can be important

for regional development. The magnitude of such indirect effect depends not only on the firms

but also the industry and region. Aghion et al. (2009) find that the productivity increase of

incumbents from new entry is particularly larger in sectors closer to the technology frontier. The

indirect effect from competition does not necessarily lead to employment growth. As firms

become more productive they could actually reduce inputs and workers. Competition from new

ventures would result in regional employment growth when the improved productivity of firms

increases overall demand (Fritsch 2013).

Finally, entrepreneurship's impact on regional growth depends on the regional

environment. The wide regional variation in entrepreneurship has motivated researchers to

examine the underlying causes behind such variation and explore how the regional

entrepreneurial environment might influence the regional economy. Regional characteristics

influence not only people's decision to become entrepreneurs, but also the success and growth of

firms (Sternberg 2009). The pre-existing industrial structure and incumbent firms affect new

venture creation and regional growth (Fritsch and Mueller 2008). Moreover, local entrepreneurs

play an important role in the formation of industrial clusters in the first place (Feldman 2001).

The region's organizational culture (Saxenian 1994), occupational structure (Parker 2005), and

skill level (Glaeser and Saiz 2004) also contribute to the regional variation in entrepreneurship

and economic growth. The entrepreneurial ecosystem has also been examined as a framework for

regional development. Entrepreneurs and the supporting actors - such as the venture capitalists,

lawyers, and accountants - in the ecosystem play a critical role in further developing the

entrepreneurial ecosystem and regional growth (Stam 2015).

2.2 SBA loans, the supply of local ventures, and regional growth.

By guaranteeing a substantial portion of the loan, government loan guarantee programs

encourage financial institutions to lend to small businesses that are unable to get financing

through conventional methods. If the financial market were already efficient, government

intervention may help create low quality ventures that are more likely to fail. However, in

practice there is market failure in the small business loan market - commercial lenders may not

lend to potential entrepreneurs because they lack sufficient collateral, may not have sufficient

9

information to properly assess the feasibility of small ventures, or may discriminate against

minority entrepreneurs. Credit constraint continues to be one of the most significant barriers to

entrepreneurs and small businesses (Kerr and Nanda 2011, Berger and Udell 1995). The SBA

intervenes and guarantees loans to correct some of these market failures and support new

ventures that otherwise would have not received funding. The impact of SBA loans on regional

growth would depend on how SBA loans affect the supply of local ventures and how those new

ventures relate to the channels described in the previous sections, i.e., knowledge spillover,

agglomeration effects, the competition with incumbents, and regional characteristics.

More talented and skilled entrepreneurs would better exploit new knowledge to generate

radical innovations and generate positive externalities to the regional economy. They would

better take advantage of the agglomeration benefits and regional characteristics, and better spur

competition that could induce incumbents to innovate. Furthermore, high quality new ventures

can transform regions into entrepreneurial hubs by actively creating strong local networks and

attracting venture capital to the region (Feldman 2001). Bosma and Sternberg (2014) highlight

the importance of differentiating the types of entrepreneurs and show that some regions have

more entrepreneurs motivated by opportunities in the market. Hence, whether SBA loans

generate positive or negative selection in new ventures is critical to regional growth.

Theoretically, there could be both positive and negative selection into SBA backed

entrepreneurship. If the loan guarantees create moral hazard, banks may finance more low

quality ventures in expectation of being bailed out by the government. Also, loan guarantees

might attract entrepreneurs that are not only credit constrained but have lower entrepreneurial

ability. These would be instances of negative selection induced by SBA loans. On the other hand,

if high ability entrepreneurs are the ones shun from conventional lending due to the lack of

collateral, SBA guaranteed loans could generate positive selection. The complexity and the

bureaucracy associated with the SBA loan application process itself could generate positive

selection of entrepreneurs who have the organizational skills to better manage a business. The

evidence on whether there is negative or positive selection is mixed, with some of the earlier

research finding higher default rate among SBA loans (Mandel 1992), and more recent evidence

finding no difference in default rate between government guaranteed loans and conventional

business loans (KPMG 1999). Again these are more correlational results, rather than causal, and

10

it is likely that the specifics of the loan guarantee scheme, e.g., guarantee fraction, interest rate

differential, etc., would affect the results.

In addition to the quality of new ventures, the net quantity of new ventures would affect

the degree to which knowledge spillover, incumbent competition effects, and agglomeration

benefits generate regional growth. Thus, it is important to identify whether the SBA loans

actually create 'additional' firms in the regional economy. If SBA loans crowd out commercial

lending, there would be little additionality. Entrepreneurs who get funding through the SBA loan

program may have been able to get funding even in the absence of government guaranteed loans.

Empirically estimating the counterfactual of whether banks would have underwritten a loan to

the same venture or whether entrepreneurs would have pursued entrepreneurship in the absence

of SBA guaranteed loans is quite difficult. The evidence from the literature is limited and not

causal, but tend to find that guaranteed loans are related to additional ventures in the economy

(Riding and Haines 2001, Riding et al. 2007). Though I focus on two aspects of loan guarantee

schemes relevant for regional growth, i.e., selection and additionality, there are other aspects of

loan guarantee schemes that the literature examines. Parker (2009) presents an overarching

perspective on this, as well as other finance policies aimed at promoting entrepreneurship.

In sum, the impact of SBA loans on regional growth depends on the net quantity and

quality of new ventures. A net increase in the number of high quality ventures would spur

knowledge spillover and agglomeration effects. On the other hand, negative selection of

entrepreneurs and no net increase in the number of new ventures could have a negative or no

effect on regional growth. Theoretically, the effects could go either way and vary based on

regional characteristics. The net result from all the different channels would determine how the

new ventures created through SBA loans affect regional growth. In this regard, identifying the

impact of SBA loans on regional growth ultimately becomes an empirical exercise.

3. Data and empirical framework

3.1 Data

For the empirical analysis, I construct a panel of SBA loans with the Metropolitan

Statistical Area (MSA) as the regional unit of analysis for the years 1993 and 2002. An MSA in

the United States consists of one or more counties that contain an urbanized area with at least

50,000 people and the adjacent counties that have close economic ties to the major urbanized

11

area. MSAs typically center around one large city, but some MSAs contain more than one large

city. MSAs are not legal administrative regions but are used for statistical purposes by

government agencies to capture all the major urban areas in the United States. The census

boundaries of MSAs can change after each census cycle. I use this ten-year period to maintain

consistent regional boundaries within the same census cycle.

There are a variety of loan guarantee schemes (LGSs) around the world. Though the

specifics differ, LGSs typically guarantee funding to new ventures unable to get conventional

loans from banks. The LGS lender is in charge of nominating the venture and requests approval

by the government. Once approved, the government underwrites a portion of the loan. The

maximum guarantee amount varies by country - ranging from 50 to 65% in France, 70-85% in

the UK, and up to 85% in Canada. In the United States, the SBA underwrites up to 85% of the

loan. The SBA’s main form of guaranteed lending is the Small Business Loan, also known as the

7(a) loan program.1 Commercial lenders structure Small Business Loans according to the SBA’s

guidelines, and borrowers pay additional loan premiums and arrangement fees that can be

substantial. Parker (2009) presents more detailed information on the different LGSs. I construct

the SBA loans data by aggregating the universe of SBA approved loans to the MSA level. The

individual SBA loans data contains a rich set of variables including the loan amount, loan date,

business location, lender, and whether the loan was to a new business or existing business.2 I use

this information to identify the loans that were given out to new small businesses and map each

loan to a metro area and a year. I then aggregate the count and approval amount to generate the

MSA level variables. There are some miscodes and missing information in the data, particularly

pertaining to the business location. I first match the loan data to the census geographic

definitions based on the place name and Zip Code when available. The loans were then matched

to a county and then linked to an MSA.3 The number of SBA loans and the approved amount for

1993 are the aggregate values for all loans approved during the fiscal year, i.e., July 1992 - June

1993. As Table 1 indicates, the average number of SBA loans approved to new businesses with

less than 20 employees in 1993 was 11.7, but the spread is quite wide with a minimum value of 0 1 There also is the Certified Development Company Loan, also known as the 504 Loan Program. The Certified Development Company (CDC) loan provides financing for fixed assets, such as, land, buildings, or machines, through a certified development company. The CDC is only available to existing small businesses that plan to expand its business and cannot be used to start a new business and hence is not subject of interest in this study. 2 This data was purchased from Coleman Publishing. 3 Some of the loan data had missing reports and miscodes. In the end I was able to match 93% of the data to a county, which were in turn matched to MSAs.

12

and a maximum of 130. The average amount of SBA loans approved at the metropolitan level in

1993 was about $1,823,000.

[INSERT TABLE 1 HERE]

The outcome variables used to examine regional growth are the change in total

employment, total payroll, and average wage of the MSA between 1993 and 2002 in log terms.

The total employment and payroll data, which includes all forms of compensations, including

salaries, wages, benefits, and bonuses, come from the Statistics of U.S. Businesses (SUSB)

Annual data set. Average wage in the MSA was constructed as total payroll divided by total

employment. As Table 1 indicates, employment grew by 17.7 percent, total payroll by 29.5

percent, and wage by 10 percent over the 10-year period. Again there is substantial variation in

regional growth with some MSAs experiencing negative growth over the same period.

The regressions include control variables that capture the regional characteristics of the

MSAs. I include initial employment, population, median family income, and percent college

educated and above using data collected from the Census. Initial employment and population are

included to control for the initial economic condition and the size of the MSA. The median

family income and percent college and above are included to control for the average skill level

and human capital of the MSA. I capture the cost of living and the housing market condition of

each MSA by controlling for the cost of housing using the Federal Housing Finance Agency’s

House Price Index (HPI). The HPI measures single-family house prices based on the average

price change in repeat sales or refinancing of the same property. Transportation infrastructure has

been found to have a significant effect on urban growth (Duranton and Turner 2012). I proxy for

the level of infrastructure using a road density measure from Burchfield et al. (2006). The major

road density measure is defined as the length (meters) of major roads, i.e., the various interstate

and state highways, divided by the metro area in hectares. The number of incumbents could

affect how new ventures impact regional growth through competition effects. I control for the

initial number of establishments in each MSA based on size, i.e., establishments with 19 or less

employees, 20-499 employees, and 500 employees or above. Though these control variables

would capture a large part of the initial regional characteristics, I additional include the nine

Census Divisions fixed effects. There are 329 MSAs in the 1993 to 2002 census data. I drop

13

Anchorage, Honolulu, and MSAs that have missing information and eventually end up with a

balanced panel of 316 MSAs.4

3.2. Empirical framework

In examining the impact of SBA loans on regional growth, I use a standard growth

regression framework, which has widely been used to examine economic growth across

countries or regions (Levine and Renelt 1992, Mankiw et al. 1992, Glaeser et al. 1992,

Henderson et al. 1995). In practice, I run the following regression:

Base controls Yes Yes Yes Yes Yes Yes Yes Yes Yes Census division fixed effects No No No No No No Yes Yes Yes R squared 0.088 0.081 0.023 0.309 0.304 0.300 0.416 0.411 0.411

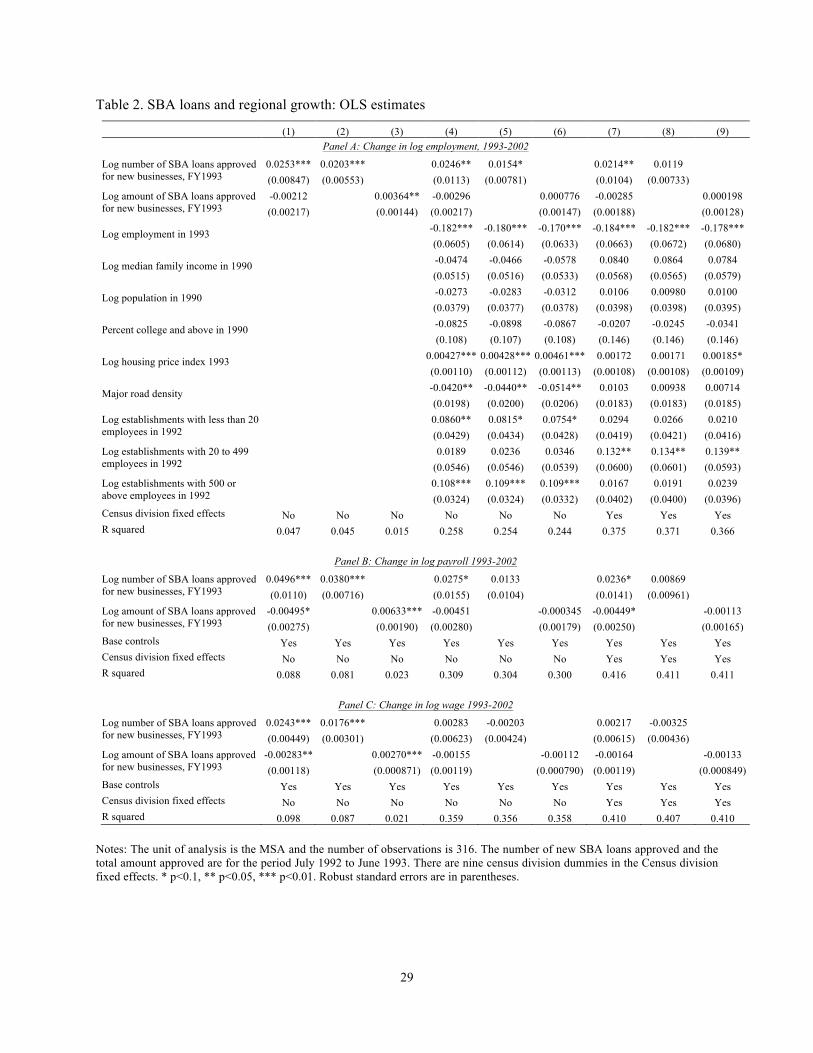

Panel C: Change in log wage 1993-2002

Log number of SBA loans approved for new businesses, FY1993

Base controls Yes Yes Yes Yes Yes Yes Yes Yes Yes Census division fixed effects No No No No No No Yes Yes Yes R squared 0.098 0.087 0.021 0.359 0.356 0.358 0.410 0.407 0.410

Notes: The unit of analysis is the MSA and the number of observations is 316. The number of new SBA loans approved and the total amount approved are for the period July 1992 to June 1993. There are nine census division dummies in the Census division fixed effects. * p<0.1, ** p<0.05, *** p<0.01. Robust standard errors are in parentheses.

30

Table 3. SBA loans and regional growth: first-difference estimates

(1) (2) (3) (4) (5) (6) (7) (8) (9)

Change in 5 year employment growth,

(1997 to 2002 growth) - (1993 to 1998 growth)

Change in 5 year payroll growth,

(1997 to 2002 growth) - (1993 to 1998 growth)

Change in 5 year wage growth,

(1997 to 2002 growth) - (1993 to 1998 growth)

ΔLog number of SBA loans approved for new businesses, 1993-97

Base controls Y Y Y Y Y Y Y Y Y R squared 0.577 0.576 0.576 0.585 0.585 0.582 0.568 0.567 0.566

Notes: The unit of analysis is the MSA and the number of observations is 316. The number of new SBA loans approved and the total amount approved are for the period July 1992 to June 1993. Base controls include the change in log employment, payroll, population, house price index, establishments by the three size categories, the 1990 percent college educated and log median family income, and major road density. * p<0.1, ** p<0.05, *** p<0.01. Robust standard errors are in parentheses.

31

Table 4. SBA loans and regional growth: 2SLS Estimates

(1) (2) (3) (4) (5)

Panel A - 1st Stage: Dependent variable: Log number of SBA loans approved to new small businesses in 1993

Log years since banking deregulation -0.294** -0.233* -0.227* -0.235* (0.130) (0.124) (0.124) (0.123)

Log number of SBA lender in 1985 0.360*** 0.349*** 0.377*** 0.380*** (0.0661) (0.0660) (0.0646) (0.0636)

Log employment in mining in 1993 -0.0275** -0.0249** (0.0124) (0.0122)

Log employment in agriculture in 1993 -0.0328** (0.0133)

R squared 0.667 0.691 0.694 0.704 0.709

Panel B - 2SLS : Dependent variable: Change in log employment, 1993-2002 Log number of SBA loans approved to new small businesses, 1993

1st stage F-statistic 5.15 29.67 17.59 14.54 11.63 Base controls Y Y Y Y Y Census division fixed effects Y Y Y Y Y

Notes: Panel A presents the first stage of the 2SLS regression and Panels B to D present the 2SLS estimates. The unit of analysis is the MSA and the number of observations is 316 for columns (1) to (3) and 314 for columns (4) and (5). The number of new SBA loans approved is for the period July 1992 to June 1993. Base controls are initial employment, median family income, population, percent college degree and above, the house price index, the number of initial establishments by the three size categories, and major road density. The Kleibergen-Paap rk Wald F statistics are reported as the 1st stage F-statistics. * p<0.1, ** p<0.05, *** p<0.01. Robust standard errors are in parentheses.

32

Table 5. Robustness tests

(1) (2) (3)

1993 to 2002 change in

log employment log payroll log wage

Panel A: Control for minimum wage

Log small business births in 1992-93 -0.0178 -0.0233 -0.00551

Census division fixed effects Y Y Y Notes: Results are from the 2SLS regressions that include all four instrumental variables in column (5) of Table 4. The unit of analysis is the MSA and the number of observations is 314. The number of new SBA loans approved is for the period July 1992 to June 1993. Base controls include initial employment, median family income, population, percent college degree and above, the house price index, the number of initial establishments by the three size categories, and major road density The Kleibergen-Paap rk Wald F statistics are reported as the 1st stage F-statistics. * p<0.1, ** p<0.05, *** p<0.01. Robust standard errors are in parentheses.

33

Appendix Table 1. Year of interstate banking deregulation by state

State Year of interstate banking deregulation State Year of interstate banking

deregulation AK 1987 MT 1993 AL 1982 NC 1990 AR 1986 ND 1985 AZ 1989 NE 1987 CA 1987 NH 1986 CO 1988 NJ 1989 CT 1983 NM 1982 DE 1988 NV 1985 DC 1985 NY 1991 FL 1985 OH 1985 GA 1985 OK 1987 HI 1995 OR 1986 IA 1985 PA 1986 ID 1986 RI 1984 IL 1986 SC 1986 IN 1991 SD 1988 KS 1992 TN 1985 KY 1984 TX 1987 LA 1987 UT 1984 MA 1978 VA 1988 MD 1985 VT 1985 ME 1983 WA 1987 MI 1986 WI 1988 MN 1986 WV 1987 MO 1988 WY 1987 MS 1986

Note: Year of interstate branching collected from the St. Louis Federal Reserve publications at www.stlouisfed.org/publications.