Government Guarantees and Bank Vulnerability during a Crisis: Evidence from an Emerging Market By VIRAL V. ACHARYA AND NIRUPAMA KULKARNI * We analyze the performance of Indian banks during 2007–09 to study the impact of government guarantees on bank performance during a crisis. Vulnerable private-sector banks performed worse than safer private-sector banks; however, the opposite was true for state-owned banks. Vulnerable private-sector banks also experienced deposit withdrawals and shortening of deposit maturity. In contrast, vulnerable state-owned banks grew their deposit base and increased loan advances at cheaper rates, especially to politically important sectors, but with poorer ex- post performance. Our evidence suggests that access to stronger government guarantees and forbearance during an aggregate crisis allows state-owned banks to access and extend credit cheaply despite their under-performance. The global financial crisis of 2007–09 saw the widespread use of government guarantees to protect failing banks. While these guarantees keep markets well- functioning during periods of stress, they may induce banks to take excessive * Acharya: Department of Finance, Stern School of Business, New York University, 44 West 4th Street, Room 9-84, New York, NY-10012, US. Tel: +1 212 998 0354, Fax: +1 212 995 4256, e-mail: [email protected]. Acharya is also a Research Affiliate of the Centre for Economic Policy Research (CEPR) and Research Associate in Corporate Finance at the National Bureau of Economic Research (NBER). Kulkarni: CAFRAL, Research Department, Reserve Bank of India Main Building, Fort, Mumbai 400 001 Tel: +91 22 22694584 (O) +91 7506291802 (M), e- mail:[email protected]. We thank Abhijit Banerjee, Chetan Ghate, Manasa Gopal, Brinda Jagirdar, Hae Kang Lee, Devesh Kapur, Kenneth Kletzer, Renu Kohli, Rajnish Mehra, Dilip Mookherjee, Prachi Mishra, Urjit Patel and N. R. Prabhala for helpful comments. 1

Transcript

Government Guarantees and Bank Vulnerability during a

Crisis: Evidence from an Emerging Market

By VIRAL V. ACHARYA AND NIRUPAMA KULKARNI∗

We analyze the performance of Indian banks during 2007–09 to

study the impact of government guarantees on bank performance

during a crisis. Vulnerable private-sector banks performed

worse than safer private-sector banks; however, the opposite

was true for state-owned banks. Vulnerable private-sector banks

also experienced deposit withdrawals and shortening of deposit

maturity. In contrast, vulnerable state-owned banks grew their

deposit base and increased loan advances at cheaper rates,

especially to politically important sectors, but with poorer ex-

post performance. Our evidence suggests that access to stronger

government guarantees and forbearance during an aggregate

crisis allows state-owned banks to access and extend credit

cheaply despite their under-performance.

The global financial crisis of 2007–09 saw the widespread use of government

guarantees to protect failing banks. While these guarantees keep markets well-

functioning during periods of stress, they may induce banks to take excessive

∗ Acharya: Department of Finance, Stern School of Business, New York University, 44 West4th Street, Room 9-84, New York, NY-10012, US. Tel: +1 212 998 0354, Fax: +1 212 995 4256,e-mail: [email protected]. Acharya is also a Research Affiliate of the Centre for EconomicPolicy Research (CEPR) and Research Associate in Corporate Finance at the National Bureau ofEconomic Research (NBER). Kulkarni: CAFRAL, Research Department, Reserve Bank of IndiaMain Building, Fort, Mumbai 400 001 Tel: +91 22 22694584 (O) +91 7506291802 (M), e-mail:[email protected]. We thank Abhijit Banerjee, Chetan Ghate, Manasa Gopal,Brinda Jagirdar, Hae Kang Lee, Devesh Kapur, Kenneth Kletzer, Renu Kohli, Rajnish Mehra,Dilip Mookherjee, Prachi Mishra, Urjit Patel and N. R. Prabhala for helpful comments.

1

risks (Cordella and Yeyati (2003), Gorton and Huang (2004) and Gropp, Vesala

and Vulpes (2004)). The empirical literature on government guarantees has

focused until recently on the ex-ante impact of government guarantees on bank

risk-taking, leverage and cost of capital (Acharya, Anginer and Warburton (2014)

and references therein). The question of how these guarantees distort bank

behavior and outcomes during crisis periods has been relatively unexplored. One

difficulty in analyzing the impact of government guarantees is also accounting for

the counterfactual, that is, how would the absence of such guarantees impact bank

behavior and outcomes? India with its mix of state-owned banks or public sector

banks (PSBs) and private sector banks, provides one ideal setting to explore this

question. While state-owned banks in India are guaranteed by the government,

private sector banks are not (or, arguably, are guaranteed to a much weaker

extent).

We examine the impact of government guarantees on banks in India during

the global financial crisis of 2007–09. We look at ex-ante heterogeneity in bank

vulnerability to a market-wide shock for the period preceding the crisis (January

2007 to December 2007). Then, separately for private sector banks and PSBs,

we analyze during the financial crisis in 2008–09 the relationship between ex-

ante bank vulnerability and (i) realized stock returns; (ii) deposit flows and

corresponding deposit rates; (iii) loan advances and corresponding loans rates;

and, finally, (iv) loan performance in the aftermath of the crisis.

As a first step to determine the role played by government guarantees, we relate

ex-ante measures of bank vulnerability to realized stock performance during the

crisis. Our bank vulnerability measure, Marginal Expected Shortfall (MES) —

proposed by Acharya et al. (Forthcoming) — captures the tail dependence of

the stock return of a financial firm on the downside of the market as a whole.

2

It estimates the negative of the average stock return for a given financial firm

in the worst 5 percent days of the market index for a particular past period

(one year preceding a crisis in our case). The greater the MES, the more

vulnerable is the firm to aggregate downturns. The question then is whether

more vulnerable PSBs (private sector banks), as measured by ex-ante MES, fared

better or worse than PSBs (private sector banks) with lower vulnerability. We

find that more vulnerable private sector banks had lower stock returns during

the crisis compared to less vulnerable private sector banks as would be expected

during crisis periods. In contrast, more vulnerable PSBs had higher stock returns

compared to less vulnerable PSBs.

We next examine whether growth in deposit base of banks explains the

cross-sectional variation in stock performance during the crisis period. Private

sector banks with higher ex-ante vulnerability experienced deposit contraction

during the crisis. However, similar to the pattern observed in stock prices,

more vulnerable PSBs managed to grow their deposits. These cross-sectional

differences in deposit growth of PSBs can be attributed to (i) the presence of

explicit and implicit government guarantees for PSBs which led to a flight of

deposits from private sector banks to PSBs, and (ii) more vulnerable PSBs

increased deposit rates during the crisis in order to attract the deposit flows from

private sector banks. Both these ingredients are needed to explain the cross-

sectional heterogeneity in deposit growth of PSBs. We explain the reasoning

below.

First, the presence of government guarantees resulted in a flight-to-quality

from private sector banks to PSBs.1 The Bank Nationalization Act explicitly

1Anecdotal evidence supports this hypothesis. Following the credit crisis and thesubsequent fall of Lehman, many depositors shifted capital out of private and foreignbanks and moved it to government banks. For example, Infosys (a large Indianmultinational corporation) transferred nearly Rs.10 billion of deposits from ICICI to SBI

3

places all liability for PSBs on the government. These guarantees for PSBs can

also be implicit. For example, as the crisis of 2007–09 progressed the Indian

government announced a number of wide-ranging stimulus plans to jumpstart

the banking system. Public sector banks were promised capital injections to help

them maintain a risk-adjusted capital ratio of 12 percent. The government also

launched three fiscal stimulus packages during December 2008–February 2009.

Importantly, in the second stimulus package the government recapitalized state-

run banks and infused nearly Rs. 3,100 crores (approximately $0.5 billion) in

2008-09 as tier-I capital.2 Although deposits of both public and private sector

banks are insured by the Deposit Insurance and Credit Guarantee Corporation

(DICGC), government guarantees of PSBs still matter since deposit insurance

coverage is limited and only partially effective.3

Second, the presence of government guarantees can only explain a flight-to-

quality from private-sector banks to PSBs. To explain the cross-sectional result

that more vulnerable PSBs managed to attract the deposit outflow from the

private-sector banks, we show that vulnerable PSBs were also increasing their

deposit rates.4 Relative to the more vulnerable PSBs, less vulnerable PSBs did

just after Lehman’s collapse in the third quarter of 2008 (“Deposits with SBI zoompast Lehman collapse”, April 7, 2009. http://articles.economictimes.indiatimes.com2009-04-07news27639025 1 private-banks-bank-deposits-deposit-base). Private sector banks tooblamed this flight of funds from private to public sector banks on sovereign guarantee ofthe PSBs (“Pvt banks want deposit insurance cap hiked”, Business Line, January 17, 2009.http://www.thehindubusinessline.inbline20090117stories2009011751460600.html).

2See “India - First Banking Sector Support Loan Project”, June 26, 2009.(http://documents.worldbank.org/curated/en/2009/06/10746593/india-first-banking-sector-support-loan-project.)

3At that point, only Rs.100,000 (approximately $2000) per depositor per bank was covered bythe DIGC. Further, uncertainty and delay in processing deposit insurance claims rendered depositinsurance only partially effective. For example, Iyer and Puri (2012) analyze a bank run at anIndian co-operative bank and find that deposit insurance is only partially effective in preventingruns. They find that even depositors within the insurance limit but with larger deposit balancesare likely to run.

4In fact, this practice of PSBs increasing their deposits to chase deposit outflows from privatesector banks became so rampant that the finance ministry had to step in and stop public sector

4

not increase their deposit rates likely so as not to signal distress to the market. It

was this hike in deposit rates by more vulnerable PSBs that explains their deposit

growth. Alternate explanations, such as greater trust in PSBs, can only explain

the flight-to-quality component from private sector banks to PSBs but cannot

explain why it was the more vulnerable PSBs that were able to attract deposits.

Next, we turn to whether these deposit flows also impact lending. One could

argue that the increase in deposit base for PSBs is not harmful for the economy

as a whole if they are more willing to advance loans to the real economy resulting

in much needed credit in times of recession. State-owned banks tend to be

less responsive to macroeconomic shocks and thereby stabilize availability of

credit in the economy (Micco and Panizza (2006)). We do indeed find that

more vulnerable PSBs increased lending during the crisis. However, we find that

PSBs increased lending in those sectors and to those firms that receive greater

political backing, namely the priority sector (agriculture and small businesses)

and state-owned firms. Additionally, the PSBs did not commensurately increase

their lending rates to reflect the higher costs in borrowing (higher deposit rates).

Importantly, we find that lending during the crisis has an impact on subsequent

loan performance. More vulnerable private sector banks tightened lending during

the crisis and as a result had to restructure fewer loans in the period 2008 to

2015 following the crisis. In contrast, more vulnerable PSBs — which increased

lending but not at higher loan rates — did not witness a similar lowering of

restructured assets in the aftermath of the crisis.5

banks from excessively increasing their deposit rates (“Deposit funds with public sector banks,PSUs told”, Business Line, November 11, 2008. http://www.thehindubusinessline.comtodays-paperdeposit-funds-with-public-sector-banks-psus-toldarticle1641219.ece)

5Prior literature has also emphasized the political influence on state-owned banks. Sapienza(2004) finds that lending by state owned banks in Italy is influenced by the party to which thestate-owned bank is affiliated. Calomiris and Haber (2009) point to the nexus between politiciansand bankers in Mexico in the 1980s. Similar to our findings, banks directed loans to politicallyimportant sectors state-owned firms and politically important producer and consumer groups

5

Finally, we document that, consistent with the perception of greater

government support in case of stress for weaker PSBs, the government indeed

injected more capital into the more vulnerable PSBs.6

Section I presents our empirical hypotheses and discusses briefly the data used

in our analysis. Section II looks at the impact of government guarantees on stock

performance of public and private sector banks. Section III and Section IV look

respectively, at the impact on deposit growth and bank lending. Section V shows

our results on loan performance in the crisis and post-crisis period. Section VI

looks at capital injections into the PSBs. Section VII concludes. Appendix A

provides details on the stylized model used to motivate our empirical analysis.

Further details on the data used in our analysis are in Appendix B. The

institutional environment and the time-line of the crisis in India are provided

in Appendix C. Robustness results are discussed in Appendix D.

I. Empirical Analysis

A. Testable Hypotheses

In Appendix A, we motivate our empirical approach with a simple model. We

hypothesize that franchise values of more vulnerable banks that are protected

by government guarantees (PSBs) increase relative to unprotected banks (private

sector banks) during periods of crises. Additionally, we derive implications for

the difference in franchise values of more vulnerable PSBs relative to safer PSBs,

and this relative difference for private sector banks which are not guaranteed by

the government.

despite being economically unviable.6While we do not have enough statistical power to relate recapitalizations to our bank

vulnerability measure (MES), we find that qualitatively high MES banks had higher capitalinjections in Section VI.

6

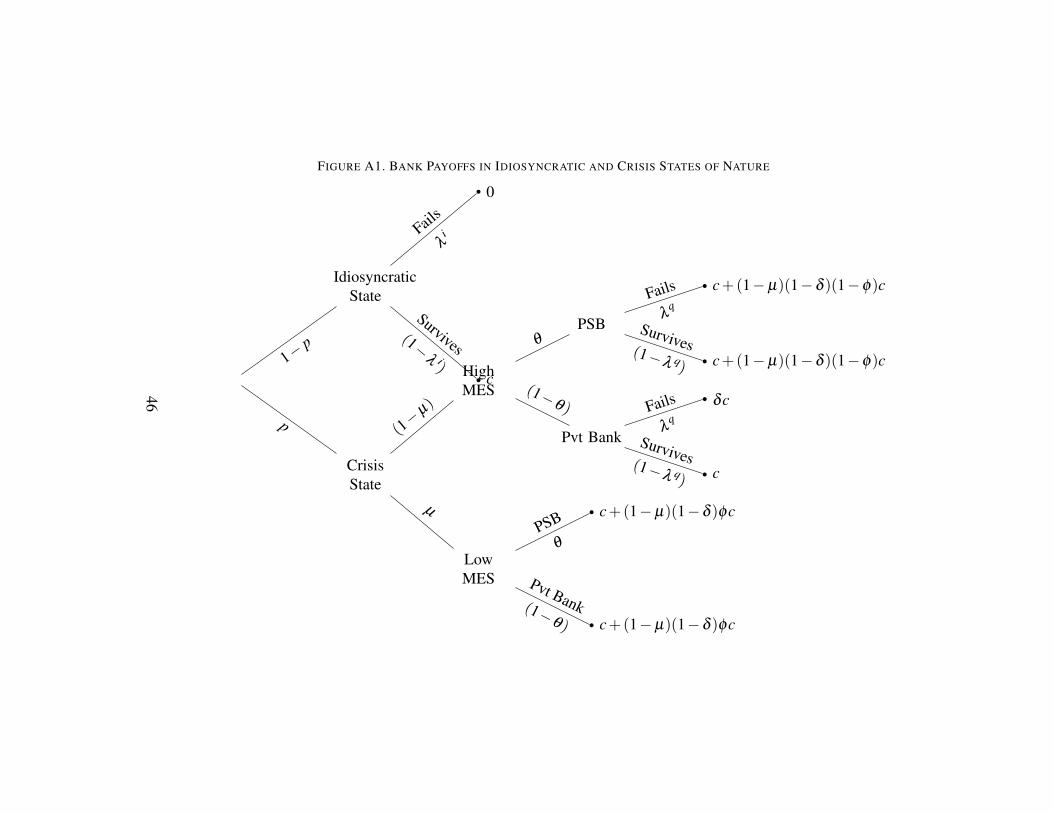

Here we summarize the intuition for the setup and its empirical implications.

In our model, we assume that if banks fail only due to an idiosyncratic shock,

then they are not guaranteed by the government and there is no difference in this

outcome between private sector banks and PSBs. In contrast, in the event of

an aggregate crisis, a private sector bank with high vulnerability (exposure) to

the crisis will lose its market share of deposits translating into lower cashflows.

The cash (deposit) outflows from failing private sector banks are captured by the

remaining banks, namely all the PSBs and the less vulnerable (in the context

of our empirical setting, low MES) private sector banks. While only the less

vulnerable private sector banks survive an aggregate crisis unscathed, all PSBs

survive regardless of their ex-ante exposure to aggregate risk as they enjoy

government guarantees.

We parameterize the split in the capture of market share from more vulnerable

private sector banks between less vulnerable banks (low MES private sector

banks and low MES PSBs) and the more vulnerable (high MES) PSBs with the

parameter φ . A low φ implies that the high MES PSBs are able to attract a greater

share of the demand for deposits from the failing private sector bank. Let ∆V PSB

represent the difference in franchise value between the high MES and low MES

PSBs. ∆V Pvt is analogously defined.

This simple model yields the following testable predictions:

1) As the probability of the aggregate crisis increases, ∆V Pvt decreases for

private sector banks.

2) As the probability of the aggregate crisis increases, ∆V PSB increases for

PSBs if government guarantees are strong for all PSBs and if φ < 0.5.

The intuition for the above two predictions is as follows. First, since private

sector banks do not have explicit government guarantees, the more vulnerable7

private sector banks will perform worse than the less vulnerable private sector

banks during a crisis.

To obtain the second prediction, a necessary condition is that PSBs have

government guarantees in a crisis. Since only PSBs are guaranteed during the

crisis, there should be a flight of deposits from the private sector banks to the

PSBs. This would be consistent with a “flight-to-quality” story. However, this

would not be sufficient to generate our empirical finding that more vulnerable

PSBs have higher deposit growth during the crisis compared to safer PSBs.

For this to be true, we also need that φ < 0.5. That is, vulnerable PSBs

need to actively attract deposits away from the failing vulnerable private sector

banks. This would be true if, say, more vulnerable PSBs gamble and manage to

attract deposits away from surviving banks — for example, by increasing their

deposit rates — in effect, exploiting or receiving greater value from government

guarantees compared to safer PSBs. Safer PSBs, on the other hand, may not be

willing to raise their deposit rates due to signalling concerns.

We will now describe our empirical hypotheses and methodology. To test the

hypotheses of how depositors and market investors react differently to public and

private sector banks, we run the regression specifications outlined below. All

specifications take the form:

yi,t = PSB+Pvt +βPSBspec ∗MES∗PSB+β

Pvtspec ∗MES∗Pvt

+γPSBspec ∗X ∗PSB+ γ

Pvtspec ∗X ∗Pvt + ei,t(1)

where yi,t is the dependent variable described below depending on the hypothesis

we are testing. MES is our measure of ex-ante bank vulnerability to an aggregate

crisis, dummy variable Pvt is 1 if the bank is a private sector bank and PSB is

8

1 if the bank is a public sector bank. X includes all the control variables. We

are interested in the coefficient β PSBspec and β Pvt

spec which will vary depending on the

hypothesis we are testing.7 For each hypothesis below we simply replace the

dependent variable and look at the corresponding specification.

HYPOTHESIS 1: More vulnerable PSBs, i.e., banks with greater aggregate risk

exposure, had higher returns during the crisis compared to less vulnerable PSBs.

Analogously, more vulnerable private sector banks had lower returns compared

to less vulnerable private sector banks.

To test this hypothesis, we use the specification in Equation 1 with the dependent

variable yi,t = Crisis Returni,t which is defined as the stock return from t − 1

(pre-crisis) to t (end of crisis). We are interested in the coefficient β PSBCrisisReturn

and β PvtCrisisReturn. From our hypothesis, we conjecture that β PSB

CrisisReturn > 0 and

β PvtCrisisReturn < 0. That is, more vulnerable private sector banks had lower returns

which is to be expected during a crisis. In contrast, more vulnerable PSBs fared

better than their less vulnerable counterparts.

Next, we conjecture that this pattern in stock returns is explained by deposit

flows of PSBs and private sector banks.

HYPOTHESIS 2: More vulnerable PSBs have higher deposit growth compared

to less vulnerable PSBs. In contrast, more vulnerable private sector banks have

lower deposit growth compared to less vulnerable private sector banks.

To test this hypothesis, we use the specification in Equation 1 with the dependent

variable yi,t = Deposit Growthi,t which is defined as the growth in deposits

7Note this is equivalent to the following regression:

Development Bank of India (IDBI)) are publicly listed of which 21 are PSBs and

17 are private sector banks.

In our analysis, we use the Marginal Expected Shortfall (MES) to measure the

ex-ante vulnerability of public and private sector banks to an aggregate crisis.

The MES measure captures the tail dependence of the stock return of a financial

firm on the market as a whole. The strength of the measure lies in its ability

to predict which firms are likely to be worst affected when a financial crisis

materializes, as demonstrated by Acharya et al. (Forthcoming) in their analysis

of the systemic risk of large U.S. financial institutions around the financial crisis

of 2007–09.

Specifically, MES estimates the expected losses for a stock conditional on a

crisis. Since extreme tail events such as a mild financial crisis happen once a

decade and severe crisis such as the Great Depression or the Great Recession only

once in several decades, the practical implementation of MES relies on “normal”

tail events. We use the normal tail events as the worst 5 percent market outcomes

at daily frequency over the pre-crisis period. In our analysis, we take the 5

percent worst days for the market returns as measured by the S&P CNX NIFTY

index during the period of 1st January, 2007 to 31st December, 2007, and then

compute the negative of the average stock return for any given bank for these 511

percent worst days. As such, MES is a statistical measure but Acharya, Pedersen,

Philippon and Richardson (2010a) provide a theoretical justification for it in a

model where the financial sector’s risk-taking has externalities on the economy

whenever the sector as a whole is under-capitalized.8 In our baseline analysis

we use the MES as our measure of ex-ante risk. Our results are also robust to

alternate measures of risk (see Appendix D). Indian stock market data is from

the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE). The

remaining variables and associated data sources used in our analysis in described

in Appendix B. Detail on the institutional environment and the time-line of how

the crisis progressed in India are provided in Appendix C.

II. Government Guarantees: Impact on Stock Returns

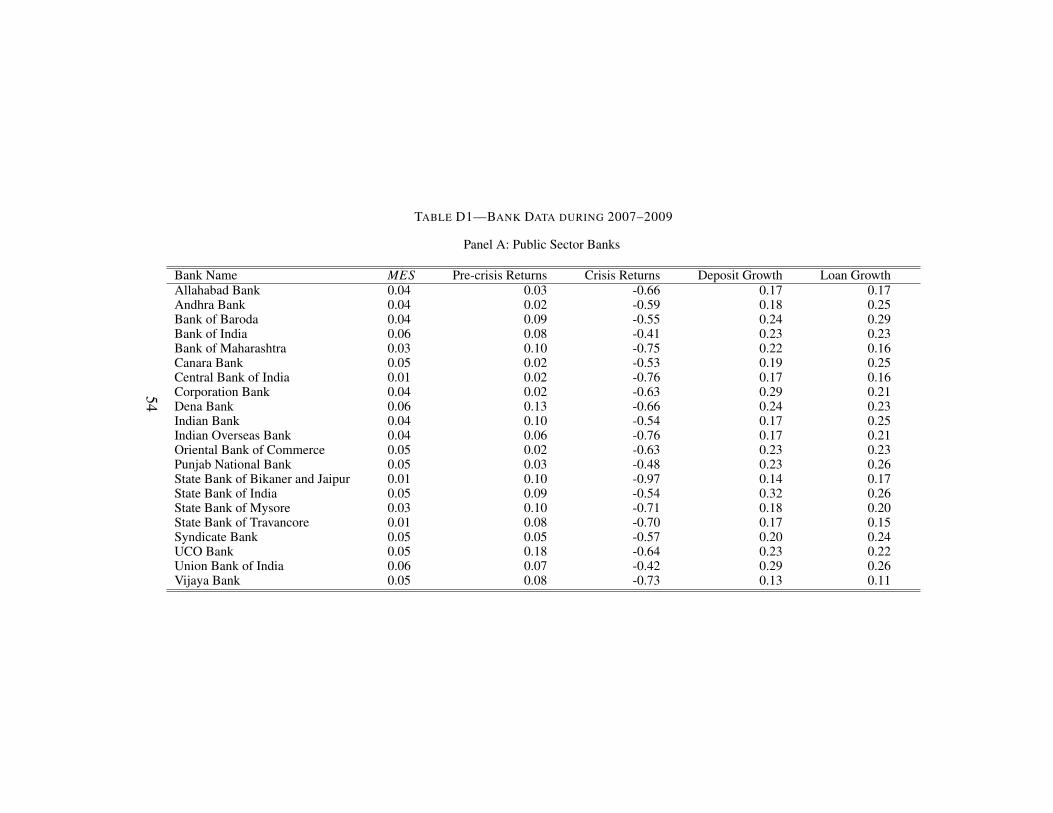

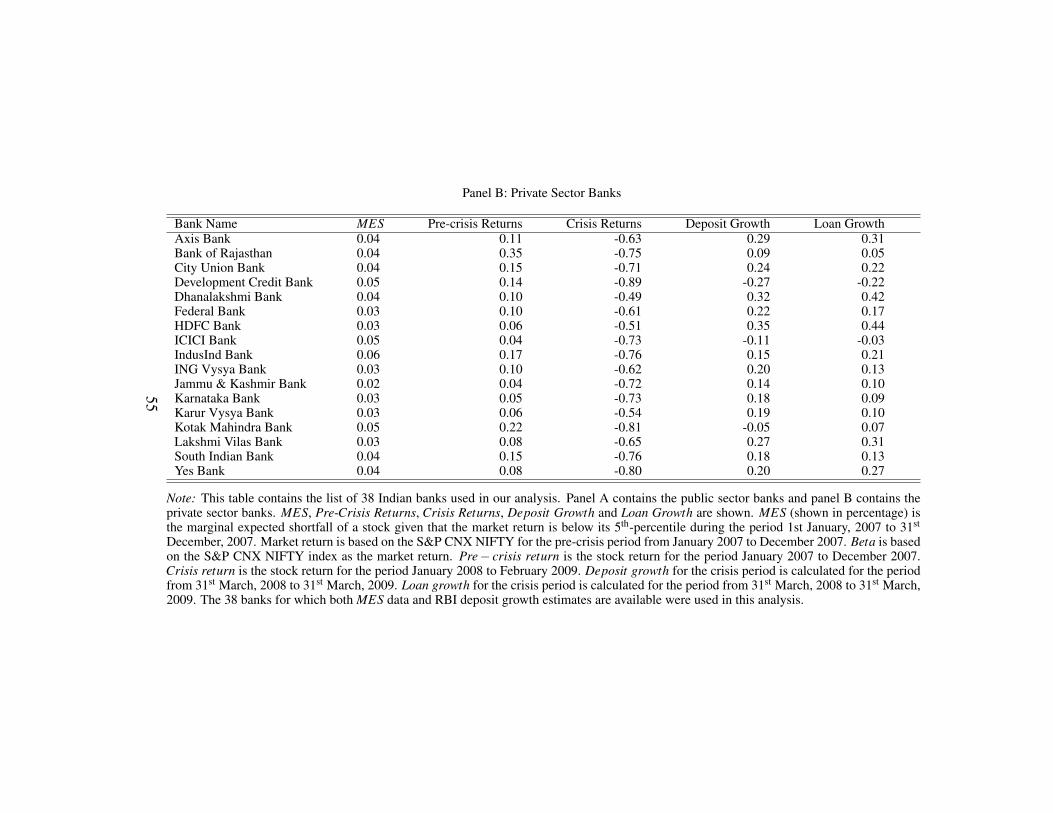

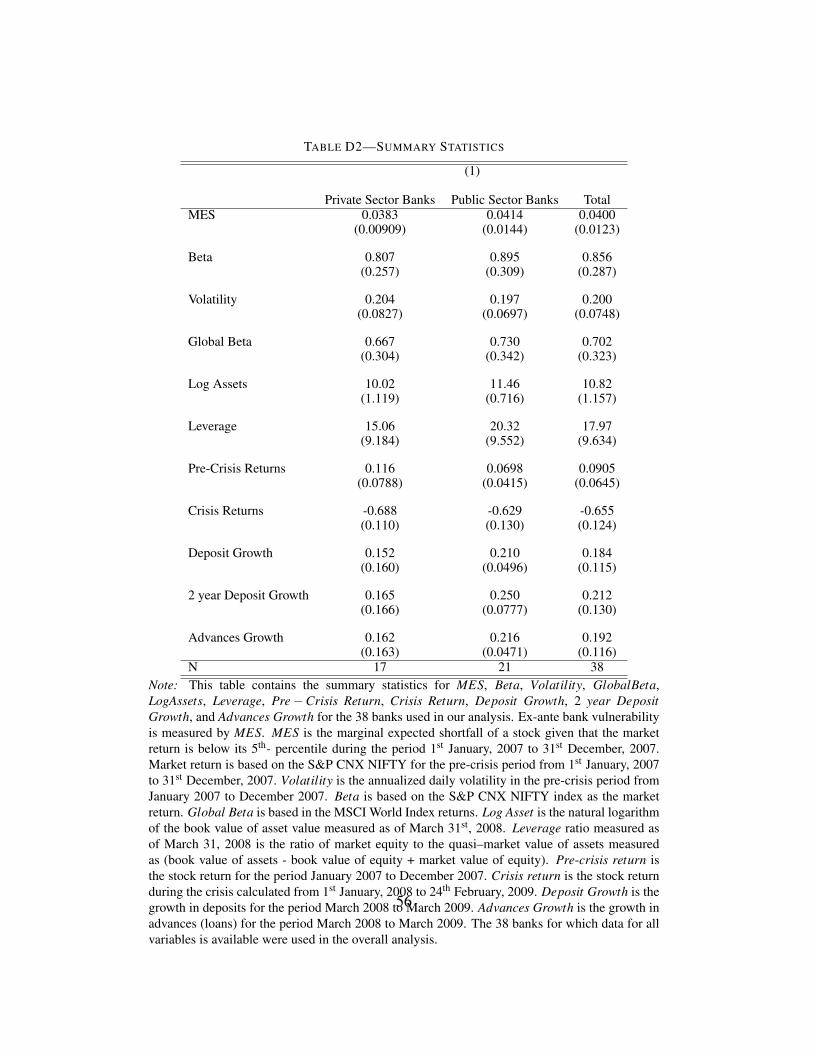

Table D2 in the appendix provides the summary statistics aggregated for all

38 banks and also aggregated separately for the 21 PSBs and 17 private sector

banks in our analysis. The significant loss of value for the bank stocks during

the crisis as suggested by the average realized return of -65.5 percent indicates

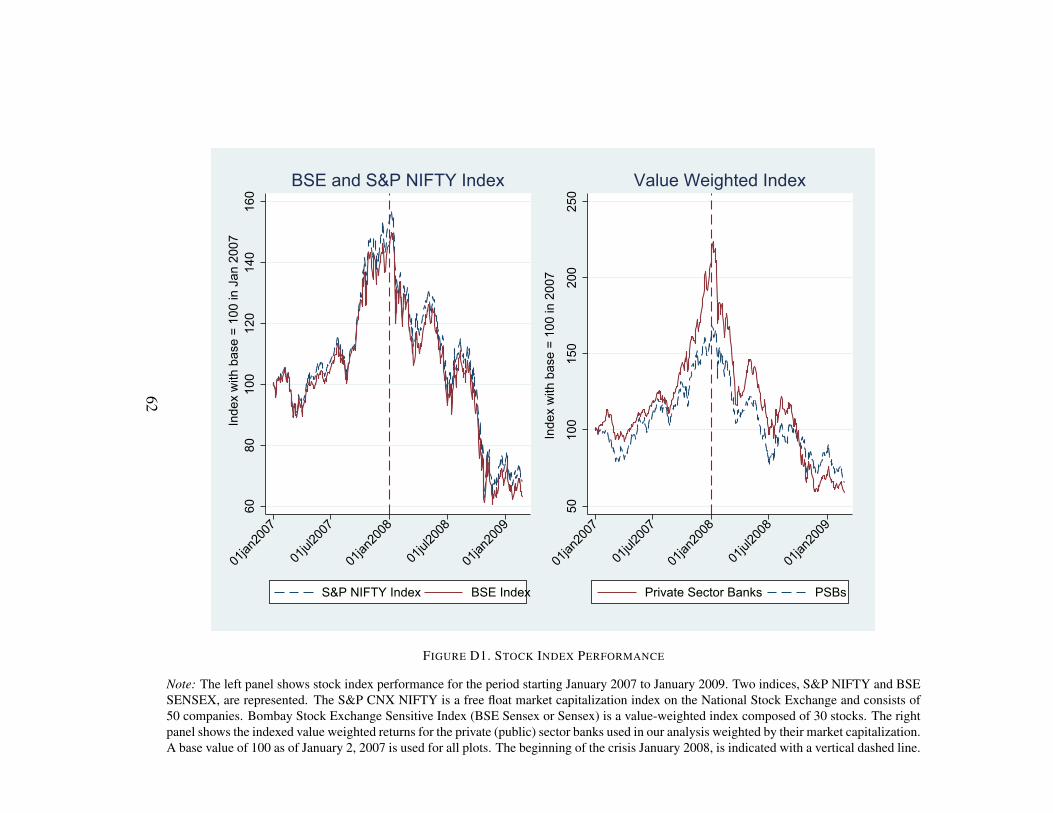

how trying this period was for the Indian banking industry as a whole. Figure D1

in the appendix shows that the stock market index — S&P CNX NIFTY index

— declined by nearly 60 percent from January 2008 to October 2008. Average

MES value measured in the pre-crisis period was 4.0 percent. What is important

for our analysis is whether a ranking of banks based on the normal-time MES

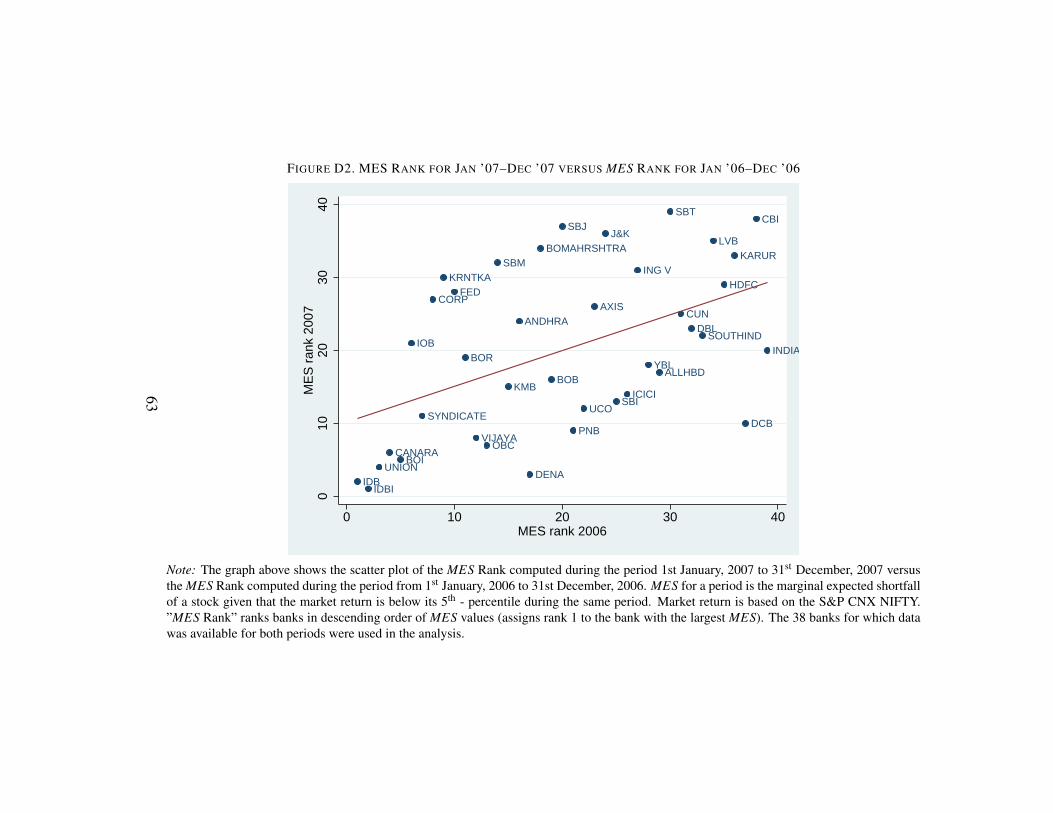

works well during the crisis. In Figure D2, we plot MES rankings from January

2006 -December 2006 against the MES ranks from January 2007 - December

2007 and show that MES rankings in 2006 were reflective of which banks would

8They show that the MES measure can be interpreted as one piece of the contribution of eachfinancial firm to the systemic risk in the event of a crisis, the other piece being the leverage of thefirm.

12

be systemically important in 2007 (also see Appendix D).

Table D2 in the Appendix also shows that average MES value is higher for

PSBs (4.14 percent) compared to private sector banks (3.83 percent). That is,

PSBs had on average negative 4.14 percent returns on the days the market return

(S&P CNX NIFTY) was below its 5th percentile for the pre-crisis period from

January 2007 to December 2007.

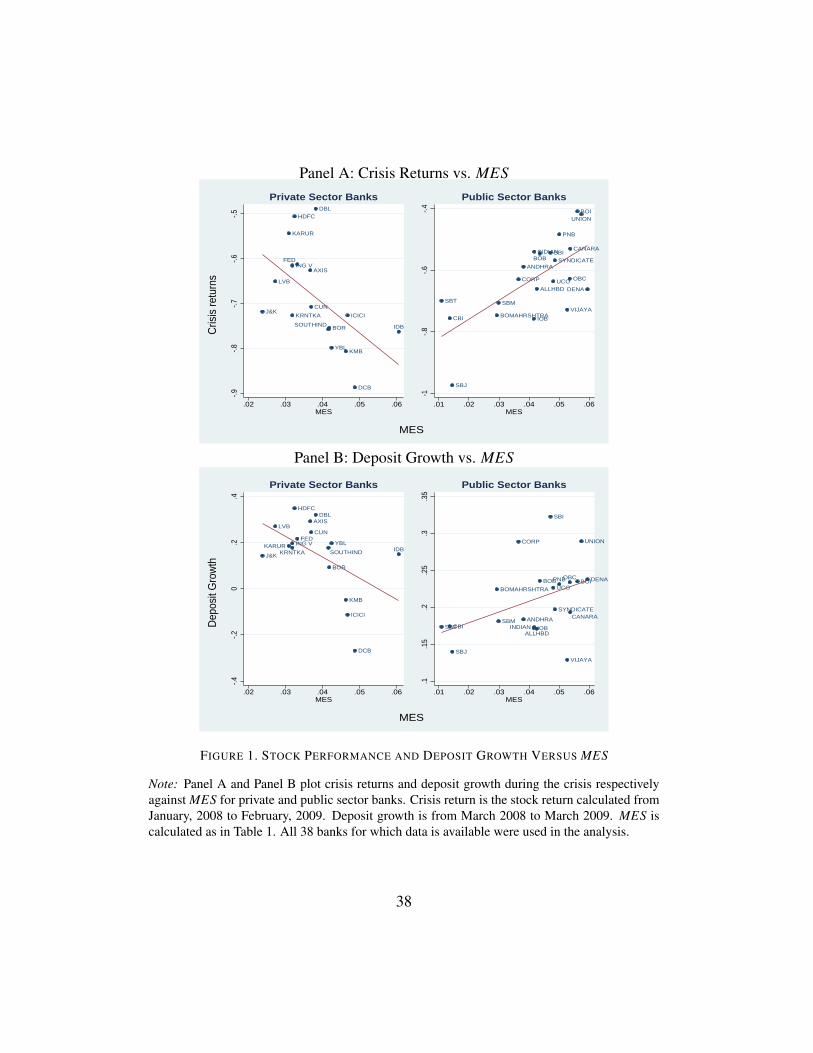

In Figure 1 Panel A we plot stock returns during the crisis against ex-ante

bank vulnerability as measured by MES. MES is able to explain a significant

proportion of realized returns for both private sector banks (R2 of 29.70%) and

PSBs (R2 of 46.10%) during the crisis. These plots show that private sector

banks with higher MES were worse hit during the market-wide downturn. More

vulnerable PSBs, however, had higher stock returns during the crisis. In the

absence of guarantees — as in the case of private sector banks — banks with

higher ex-ante bank vulnerability should perform worse during the crisis. We

conjecture in Hypothesis 1 that government guarantees may have helped more

vulnerable PSBs perform better during the crisis.

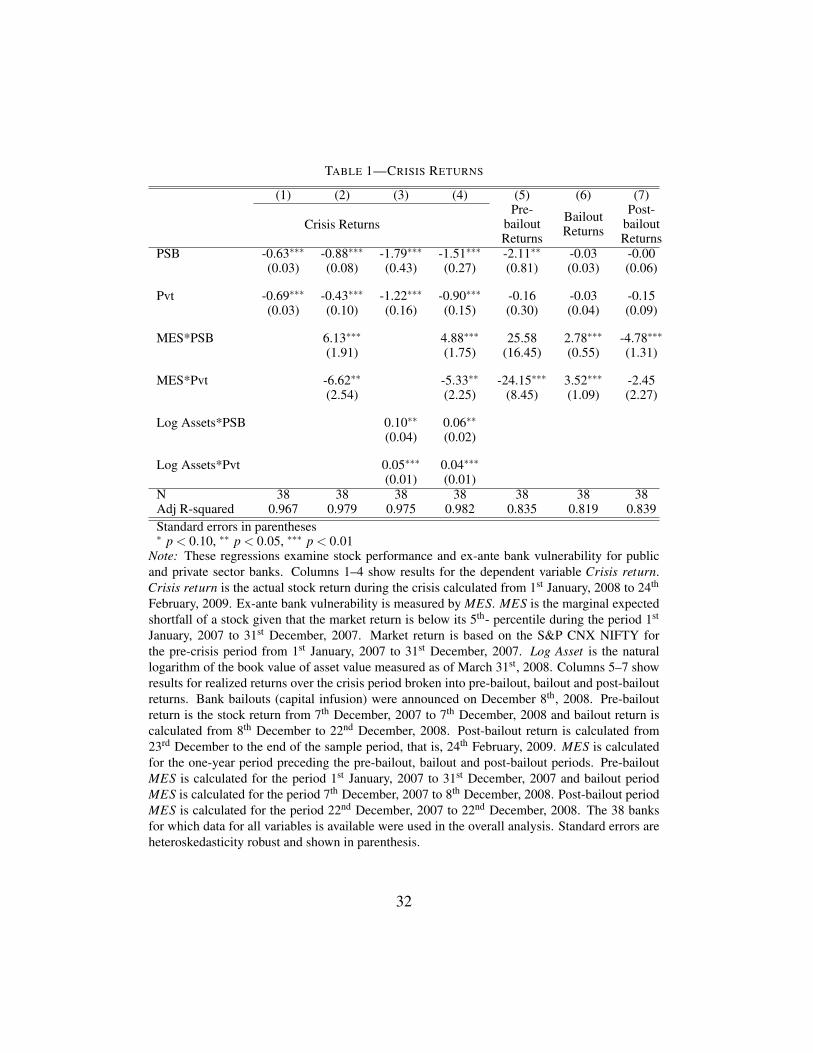

We analyze the above more formally and estimate the regression specification

in Equation 1. Table 1 shows the results of this regression with Crisis Return as

the dependent variable. From column 2, β PvtCrisisReturn indicated by the coefficient

for Pvt ∗ MES is negative and significant. A 1 percent increase in MES is

associated with a 6.62 percent decline in stock returns during the crisis. More

vulnerable private sector banks performed worse than less vulnerable private

sector banks. In contrast β PSBMES, the coefficient for PSB∗MES interaction term, is

positive and significant. A 1 percent increase in MES resulted in a 6.13 percent

increase in stock returns for PSBs. In contrast to the private sector banks which

are not explicitly guaranteed by the government, PSBs with greater ex-ante bank

13

vulnerability outperformed less vulnerable PSBs.

One could argue that the more vulnerable PSBs were merely the largest banks

and thus what we are capturing is merely an implicit too-big-to-fail guarantee. In

column 3 we control for the size of the bank using Log Assets. Asset value is the

quasi- market value of assets measured as the difference in book value of assets

and book value of equity added to the market value of equity. Log Assets can

also be thought of as controlling for a too-big-to-fail guarantee. From column

3, we see that the larger banks performed better during the crisis. Since the

coefficient on the interaction term Log Assets ∗PSB is positive, we are assured

that the negative β PSBCrisisReturn is not entirely driven by a too-big-to-fail guarantee

for the larger PSBs.9 The pooled regression with both MES and Log assets show

similar results though with slightly lower magnitudes for the coefficients in both

bank categories.

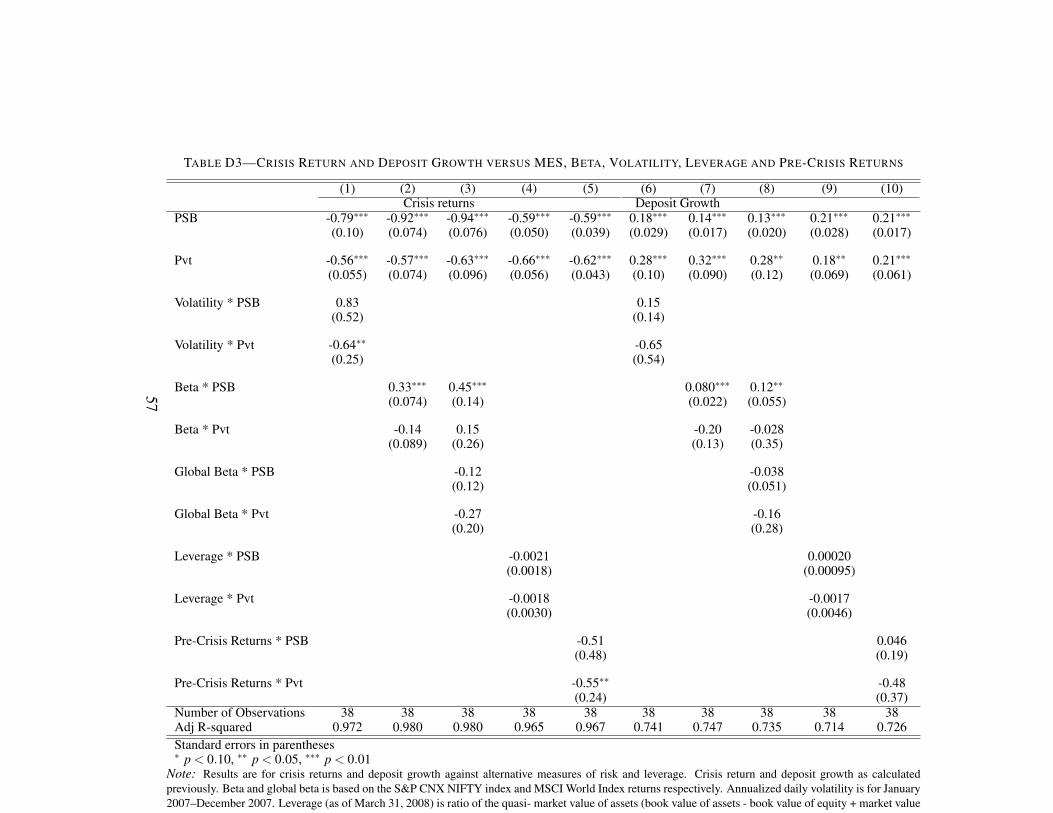

In Appendix D we also explore whether the “flight-to-quality” from private

sector banks to PSBs is due to the higher exposure of private sector banks to

global markets. Regression coefficients for a two factor model containing the

domestic market return and the global market return are shown in column 3 in

Table D3. The domestic beta coefficient measures sensitivity to the Indian NSE

stock market index whereas the global beta coefficient measures sensitivity to

the MSCI World market index. The coefficient for global beta is insignificant for

both public and private sector banks. Thus, the “flight-to-quality” from private

sector banks to PSBs does not seem to be due to differential exposure of more

vulnerable private sector banks to the global markets.

9Since PSBs tend to be on average larger than private sector banks (see Table D2) we cannotfully rule out that a too-big-to-fail guarantee played a role. Our model in Appendix A allows forany type of implicit or explicit guarantee. A too-big-to-fail guarantee in combination with thesebanks aggressively going after deposits can also yield the results in this paper. All we need toaccount for is that the most vulnerable banks were also not the biggest banks and the results forcolumn 4 show that our results are robust to this argument.

14

Columns 5–7 of Table 1 look at the impact of government guarantees on

stock returns as the crisis deepened. On December 8, 2008, the government of

India announced wide-ranging stimulus plans to jumpstart the banking system.

Specifically, PSBs were promised bailouts in the form of capital injections. We

examine bank returns around this announcement date. First, we divide our crisis

period into three sub-periods: pre-bailout (January 2008 to December 8, 2008),

bailout (2 week period following the announcement from December 8, 2008

to December 22, 2008), and post-bailout (December 23, 2008 to February 24,

2009).

From Table 1, column 5 we see that before the bailout announcement, more

vulnerable PSBs had higher returns whereas more vulnerable private sector banks

had lower returns. This can be potentially because the market expected the

government to step in only if a public sector bank failed. After the announcement

of the bailout, however, both vulnerable public and private sector banks had

higher returns (column 6). Since the announcement of capital infusion in PSBs

coincided with the announcement of a fiscal package, the market appears to

have priced in that private sector banks would also benefit from the stimulus

packages announced on December 8, 2008. That is, the market likely believed

that the fiscal package was substantial and would help the economy as a

whole. Post-bailout, specifically, after the two week period following the bailout

announcement, the relationship reverted to “normal” (column 7), that is, though

the coefficient for the interaction term with MES was negative for both public

and private sector banks, it is significant only for PSBs.

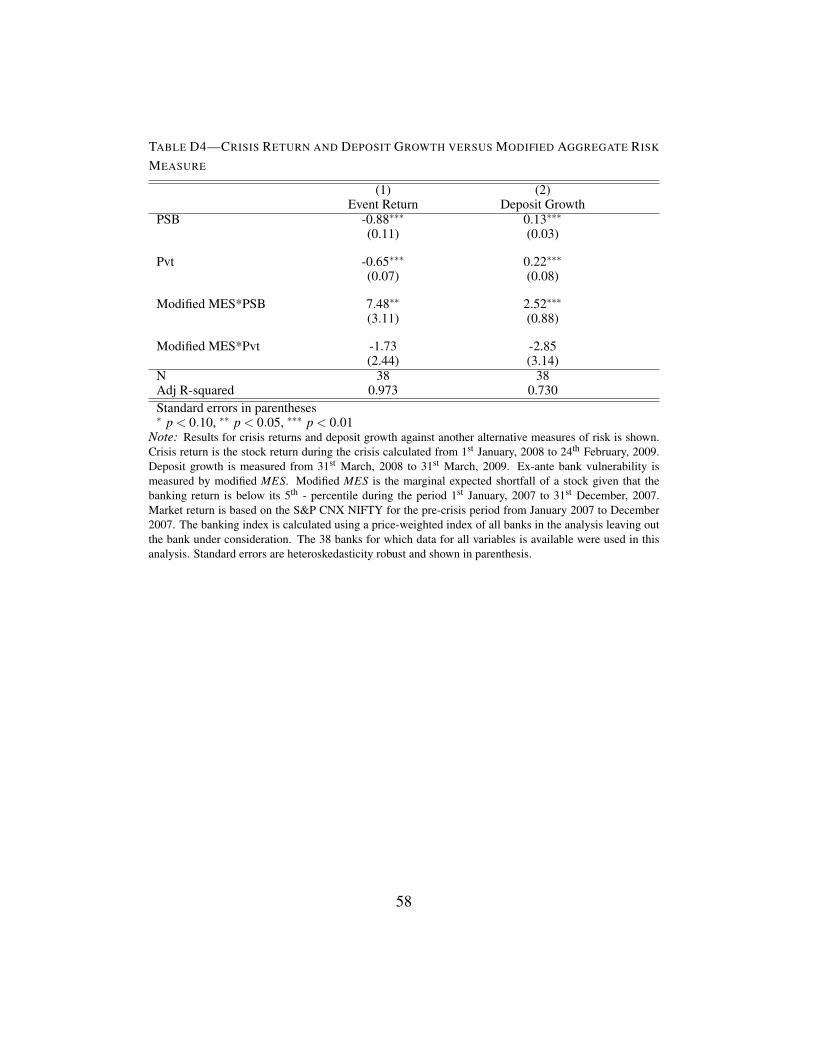

We conduct additional robustness checks in the appendix. In Table D4 in the

appendix, we show that our baseline results remain the same using a modified

version of the MES based on banking sector returns instead of the market index.

15

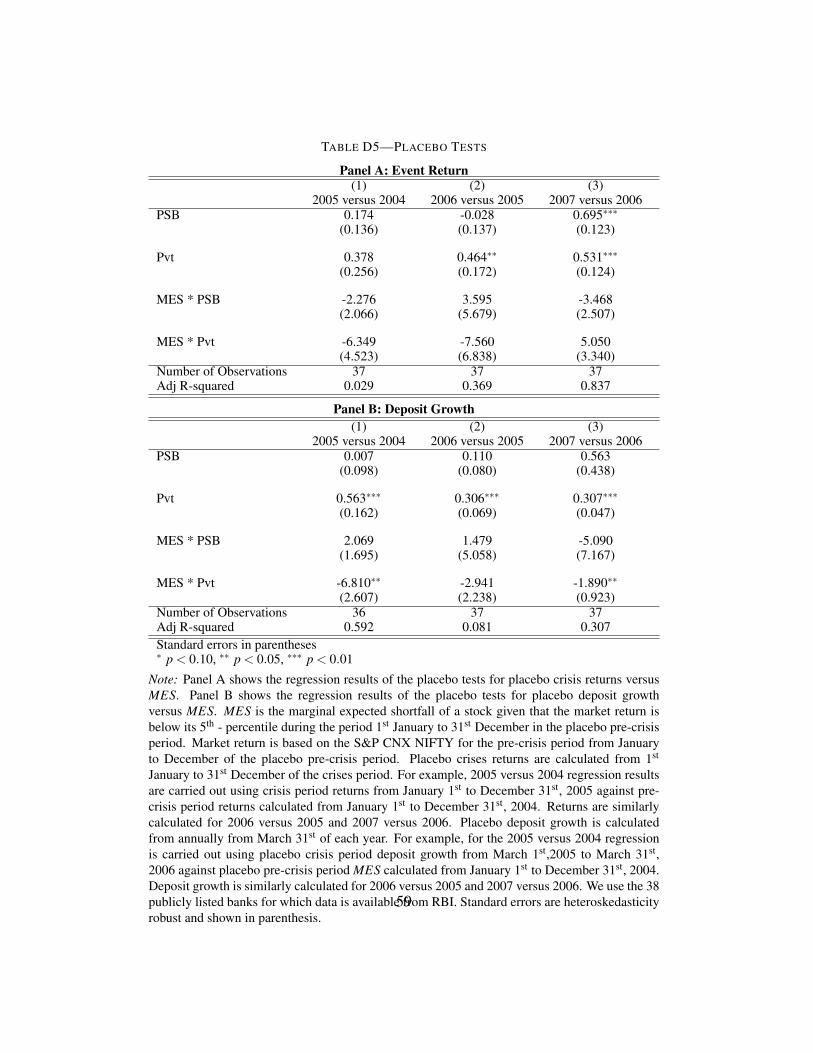

We conduct placebo tests using returns during placebo periods (non-crisis periods

being substituted for the crisis period) and do not find the differential effect on

public and private sector banks (see Table D5). Thus, only in times of a crisis do

government guarantees start to matter and affect private and public bank returns

differently. For further details, see Appendix D.

We documented so far the heterogeneity in crisis stock returns for private

and public sector banks and that bailouts appear to play a role in driving the

heterogeneity. Next, we explore whether this heterogeneity can be more directly

attributed to higher deposit growth of more vulnerable PSBs.

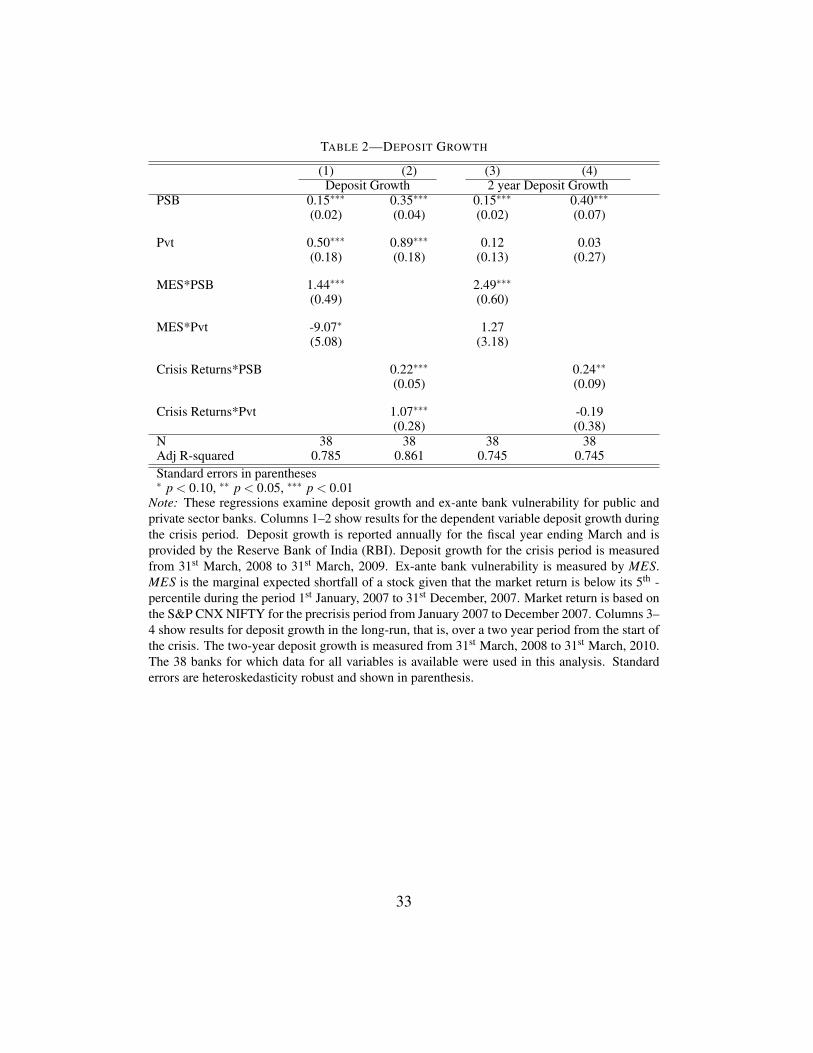

III. Impact on Deposits

We first look at deposit growth and then provide evidence for deposit rates.

A. Growth in Deposits

Growth in deposits for PSBs was strikingly different from that for private sector

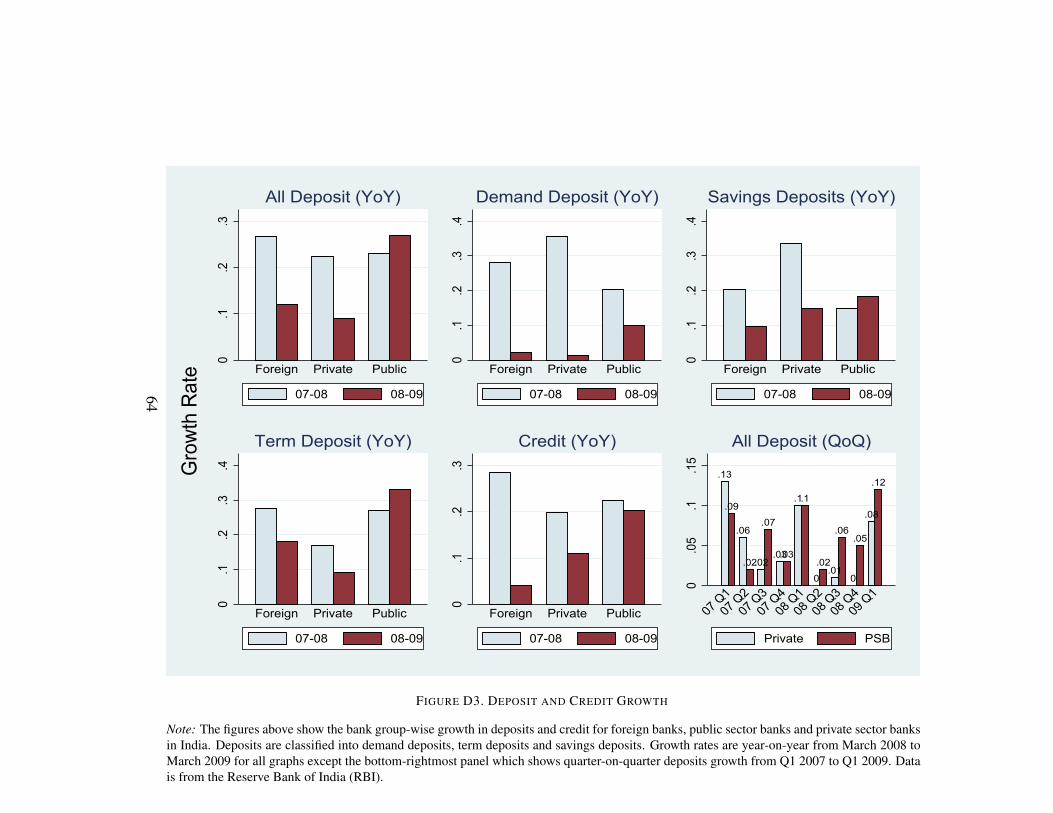

banks during the crisis. While the banking sector as a whole experienced a

slowdown in deposit growth, private sector banks were affected to a larger extent

(see Figure D3). RBI estimates indicate that deposits of PSBs grew by 26.9

percent during the crisis (March 2008 to March 2009) compared to 23.1 percent

a year earlier (March 2007 to March 2008).10 In comparison, for private sector

banks deposit growth slowed from 22.3 percent to a mere 9.1 percent in the same

period. While the above estimates refer to all 50 banks for which data is provided

by RBI, the deposit growth also show similar patterns when we restrict to the

38 banks used in our analysis (see Table D2). Looking at this aggregated data

10Deposit data is provided by RBI annually for the period ending March 31st of each year.Hence the annual deposit growth is calculated from March of previous year to March of currentyear.

16

one might conclude that a flight-to-quality led to PSBs increasing their deposit

base at the expense of private sector banks. However, this analysis based on the

aggregated data mask significant heterogeneity in deposit growth of PSBs.

Figure 1 Panel B relates deposit growth during the crisis to ex-ante bank

exposure to systemic risk as measured by MES. While more vulnerable private

sector banks had lower deposit growth, more vulnerable PSBs had higher deposit

growth during the crisis. A flight-to-quality channel can only explain deposits

moving from private sector banks to PSBs, but not to more vulnerable PSBs

relative to less vulnerable PSBs. Depositors should penalize banks with greater

ex-ante bank vulnerability and move money from the more vulnerable banks,

which are likely to fail during a crisis, to banks with lower vulnerability.

We conjecture (Hypothesis 2) that, government backing of PSBs distorts bank

behavior during aggregate crisis. More vulnerable PSBs with government

guarantees increase their deposit rates to attract more deposits.

To test this hypothesis, we run the regression specification of Equation 1

with the dependent variable, Deposit growth, measured for the crisis period

from January 2008 to February 2009 (see Table 2). For PSBs, the coefficient

for the interaction term MES ∗ PSB is positive and significant. For private

sector banks, the coefficient for the interaction term MES ∗Pvt is negative and

significant (column 1). A 1 percent increase in ex-ante bank vulnerability (MES)

is associated with a 1.44 percent increase in deposit growth for PSBs. A 1 percent

increase in MES for private sector banks resulted in a 9.07 percent decrease in

deposit growth during the crisis.

The goal in this section is to also link our findings in Section II on bank stock

performance during the crisis to deposit growth. In column 2, we explicitly test

this link by looking at deposit growth and crisis returns. Regression of deposit

17

growth against crisis returns shows that, both public and private sector banks

with higher crisis returns had higher deposit growth in line with our hypothesis.

Paralleling our analysis on event returns in Section II on pre-bailout, bailout and

post-bailout trends, we would like to see the patterns in deposit growth as the

crisis progressed. Since RBI publishes only aggregate data for deposit growth at

the quarterly frequency, we analyze deposit growth as the crisis deepened only at

the aggregate level. Thus, the data is for all 50 public and private sector banks in

India (as opposed to the 38 publicly listed banks that are used in our analysis).

Figure D3 (bottom-right panel) shows that initially when the crisis hit India

in 2008, both public and private sector banks had similar deposit growth rates

(10 percent in Q1 2008). As the crisis worsened, the disparity between public

and private sector banks became evident. PSB deposits grew by 1.7 percent, 5.5

percent and 5.2 percent compared to much lower growth rates of 0.0 percent, 1.0

percent and -0.3 percent for private sector banks in Q2, Q3 and Q4 of 2008. As

the government announced stimulus packages in December 2008, both public and

and 8.2 percent towards the end of the crisis. This trend is consistent with our

findings in Section II. In the pre-bailout period, explicit guarantees for PSBs

resulted in higher crisis returns for more vulnerable PSBs. Towards the end of

the crisis, bank stock returns returned to their pre-crisis patterns as one would

expect during “normal” times.

Does the flow of deposits revert back once the crisis is over? We hypothesize

that the cross-sectional differences in deposit growth for public and private sector

banks occur only during an aggregate crisis, since it is only during a crisis that

government guarantees become important. When the economy is doing well

and the possibility of a bailout is remote, the downside protection for PSBs

18

is essentially immaterial. Thus, deposit growth for both vulnerable public and

private sector banks should show the same pattern in normal times.11 Columns 2–

4 in Table 2 confirm this intuition. Deposit growth is for the two year period from

March 2008 to March 2010. The coefficient for the interaction term MES∗Pvt is

insignificant while the coefficient for the interaction term MES ∗PSB is positive

and significant (2.49) for PSBs. The two-year period includes both a crisis period

and a non-crisis period. For high MES private sector banks, deposits fell during

the crisis period but grew during the non-crisis period. In contrast, for high MES

PSBs, deposits grew during both crisis and non-crisis periods. These results point

to another interesting fact: crisis time guarantees result in a permanent shift in

deposits from private sector banks to PSBs. Deposits gained by PSBs during the

crisis do not revert in the period following the crisis suggesting that guarantees

during times of crisis have long-term effects on bank health.12

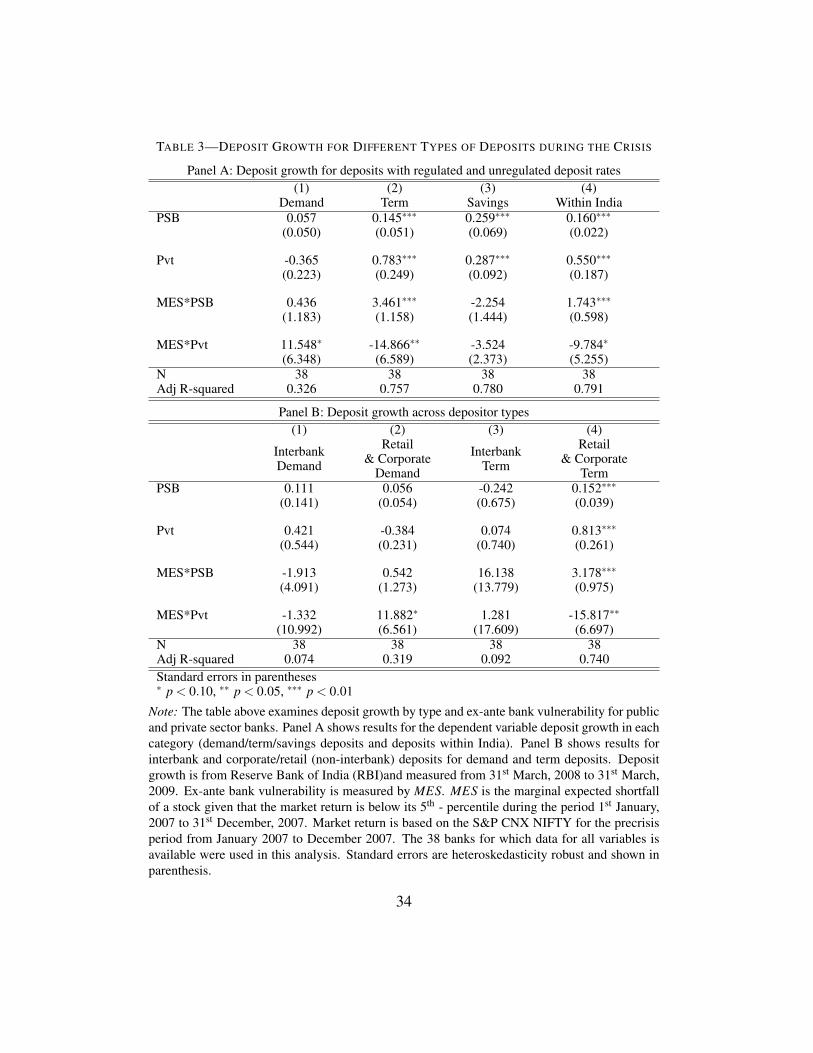

B. Deposit Rates

INDIRECT EVIDENCE

Why did depositors move deposits to the more vulnerable PSBs and not to

the safer PSBs? Did vulnerable PSBs increase their deposit rates to attract

deposits? Ideally, we would like to look at individual-level deposit data and see

whether more vulnerable PSBs indeed increased deposit rates during the crisis.

However, since RBI does not provide this information, we exploit heterogeneity

in government regulation of deposit rates across deposits of different types to test

the link between deposit rates and growth in deposits. We first provide evidence

11In our model in Section A, we explicitly make the assumption that government guaranteesplay no role in the idiosyncratic state. There is no asymmetry between public and private sectorbanks in this non-crisis state and government guarantees play no role.

12This is consistent with Iyer and Puri (2012) who find that depositors that run on the Indianbank in their analysis do not return back to the bank once the bank run is over.

19

exploiting this heterogeneity. We supplement this analysis by also providing

direct evidence from bank-level deposit rate data.

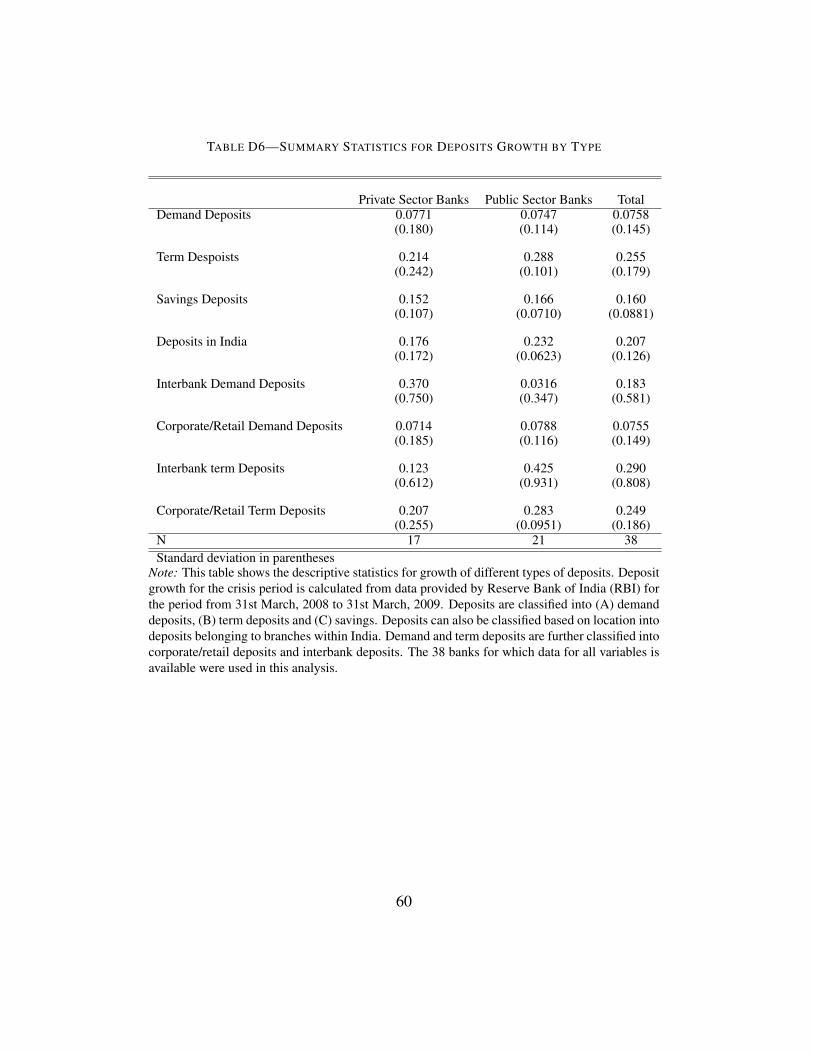

Deposits can be classified into a) demand deposits; b) savings bank deposits;

and, c) term deposits. Demand deposits, which account for 11 percent of all

deposits, are short maturity deposits and are withdrawable on demand. Saving

deposits, which account for 20 percent of all deposits, are a form of demand

deposit and are subject to restrictions on withdrawals. Term deposits, which

account for the majority (69 percent) of all deposits, are for a fixed period

typically longer than the maturity of demand deposits. One important distinction

between these different deposit types is that while banks can set deposit rates for

demand deposits and term deposits, savings deposit rates during this period were

heavily regulated by the government.13 We exploit this difference in regulation

of deposit rates to determine whether banks were actively increasing deposit rates

to attract deposits. Heavy regulation of savings deposits did not allow banks to

change deposit rates. In contrast, banks could potentially change deposit rates

for term and demand deposits.

Demand deposits grew on average at a slightly higher 7.71 percent for private

sector banks compared to 7.47 percent for PSBs (see Table D6). Average growth

rate for term deposits was higher for PSBs (28.8 percent) compared to private

sector banks (21.4 percent). This difference is consistent with the conjecture

that depositors perceived private sector banks to be more vulnerable and shifted

deposits to the lower maturity demand deposits whereas for PSBs depositors

shifted to the higher maturity term deposits in line with a flight-to-quality story.

The growth rate of savings deposits was higher for PSBs (16.6 percent) relative

13It was only after October 2011 that savings deposits were deregulated and banks wereable to change deposit rates (see “Deregulation of Savings Bank Deposit Interest Rate -Guidelines”, October 25, 2011 https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=6779&Mode=0).

20

to private sector banks (15.2 percent).

Table 3 shows the regression results for Equation 1 with the dependent variable

as the growth rate of deposits for each category. Demand deposit growth for

private sector banks is higher for banks with higher MES. In contrast, the

relationship between MES and demand deposit growth is weak for PSBs as they

did not experience a similar shortening of deposit maturity. On breaking down

demand deposits further into inter-bank and corporate/retail deposits (Panel B),

we see that the growth in demand deposits for private sector banks is driven by

the corporate/retail sector. In column 2 of Panel A, with growth in term deposits

as the dependent variable, we see the familiar result — more vulnerable PSBs

had higher term deposit growth whereas more vulnerable private sector banks

had lower term deposit growth. Further, the effect in term deposits is driven

by corporate and retail deposits (column 4, Panel B). Inter-bank term deposits

(column 3, Panel B), however, do not show the same pattern. Troubled banks

would like to borrow the most in a crisis at longer maturities, e.g., by offering

higher term deposit rates. Since inter-bank lending tends to be at the short end,

we see a weaker relationship in these shorter-term maturities. Overall, the above

results indicate that depositors were shifting away from term (longer maturity)

deposits at more vulnerable private sector banks to demand (shorter maturity)

deposits. On the other hand, PSBs witnessed deposit growth in the more stable

longer maturity term deposits.

Savings deposits growth (column 3, Panel A) does not exhibit a positive

relation with MES for PSBs. In fact for savings deposits, the coefficient for

the MES∗PSB and MES∗Pvt interaction terms are insignificant for both public

and private sector banks. Since savings deposit rates are set by the government

of India, the more vulnerable PSBs cannot increase their deposit rates to attract

21

deposits. Thus, the relationship for savings deposit growth with MES is the same

for both public and private sector banks as one would expect if PSBs did not

change their deposit rates.

Lastly in column 4 of Panel A we look at deposits within India. Banks can set

rates only for deposits within India whereas deposits rates for deposits outside

India are regulated by the RBI. Consistent with our hypothesis, for deposits

in branches within India, the coefficient of the interaction term MES ∗PSB is

positive and significant while the coeffcient for the interaction term MES ∗Pvt

is negative and significant. For deposits outside India (not shown), we do not

observe the same pattern.

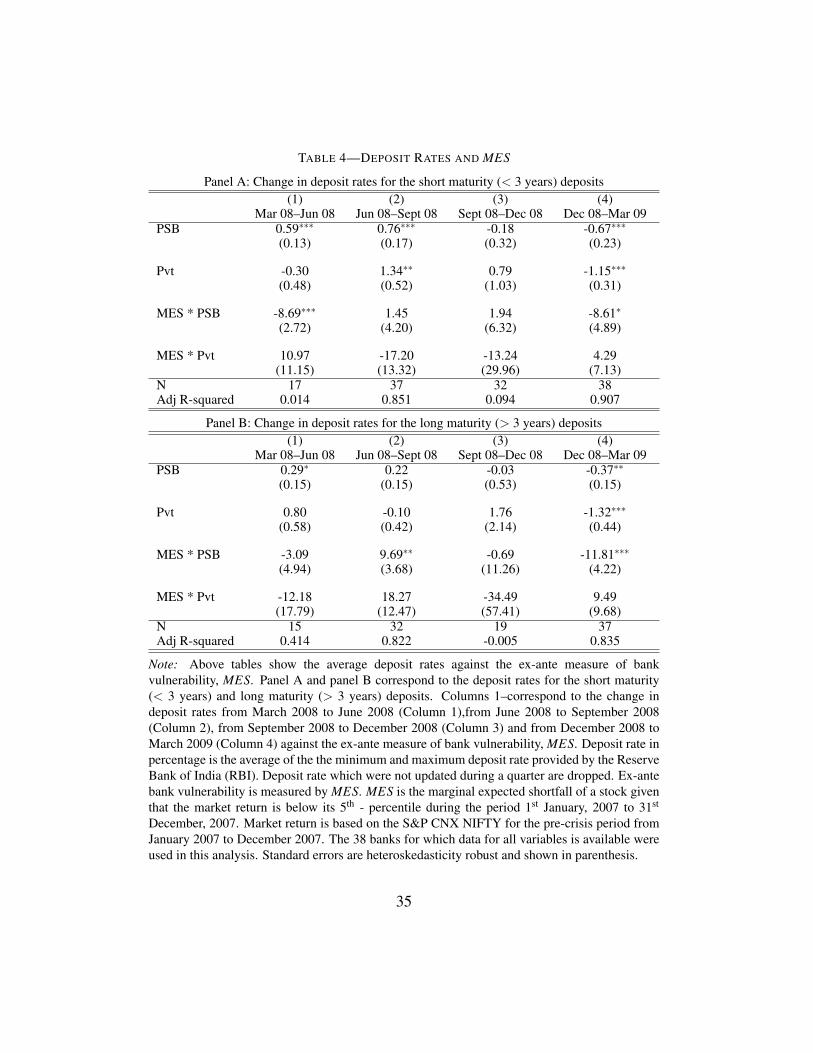

SOME DIRECT EVIDENCE

We now turn to average bank-level deposit rate data to show that banks did

indeed increase their deposit rates as the crisis progressed. We have deposit rates

only at the bank-level and the data is not disaggregated at the individual level.

Short-term deposits are deposits with maturity less than three years and long-

term deposits have maturities greater than three years. This data is not publicly

available and has been provided to us by RBI for each bank at the quarterly

frequency beginning March 2008. We use the average of the maximum and

minimum values of the deposit rate for each bank in each quarter.

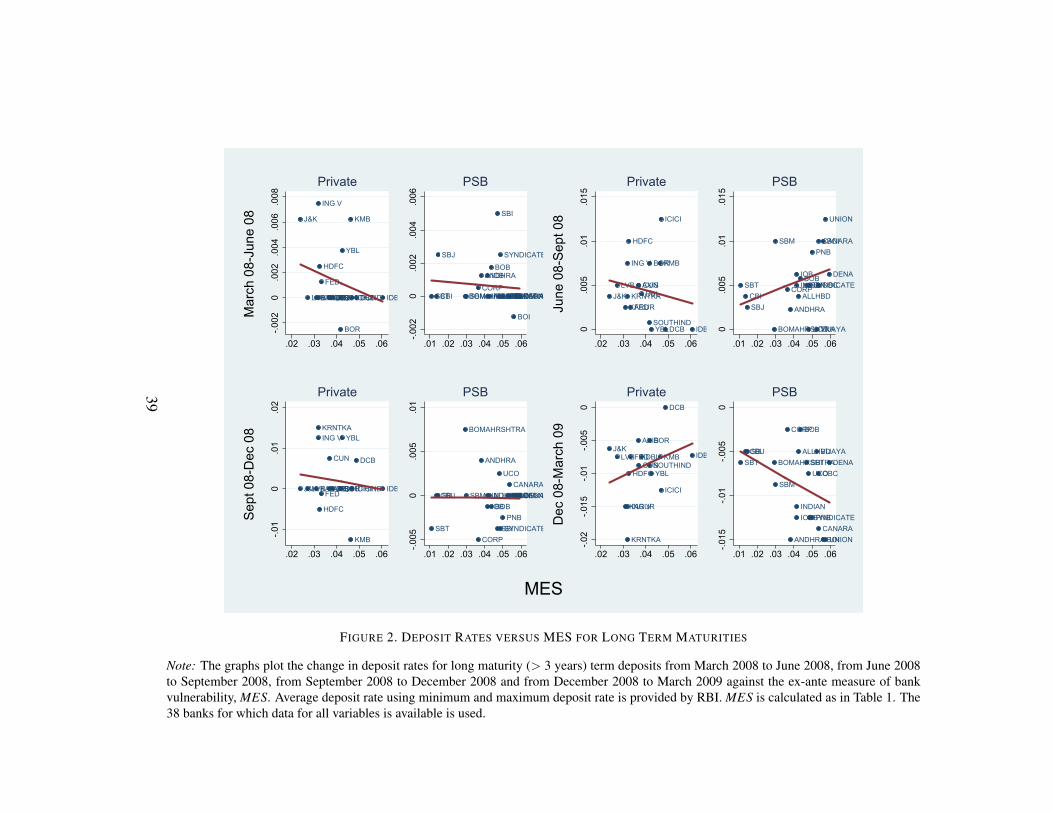

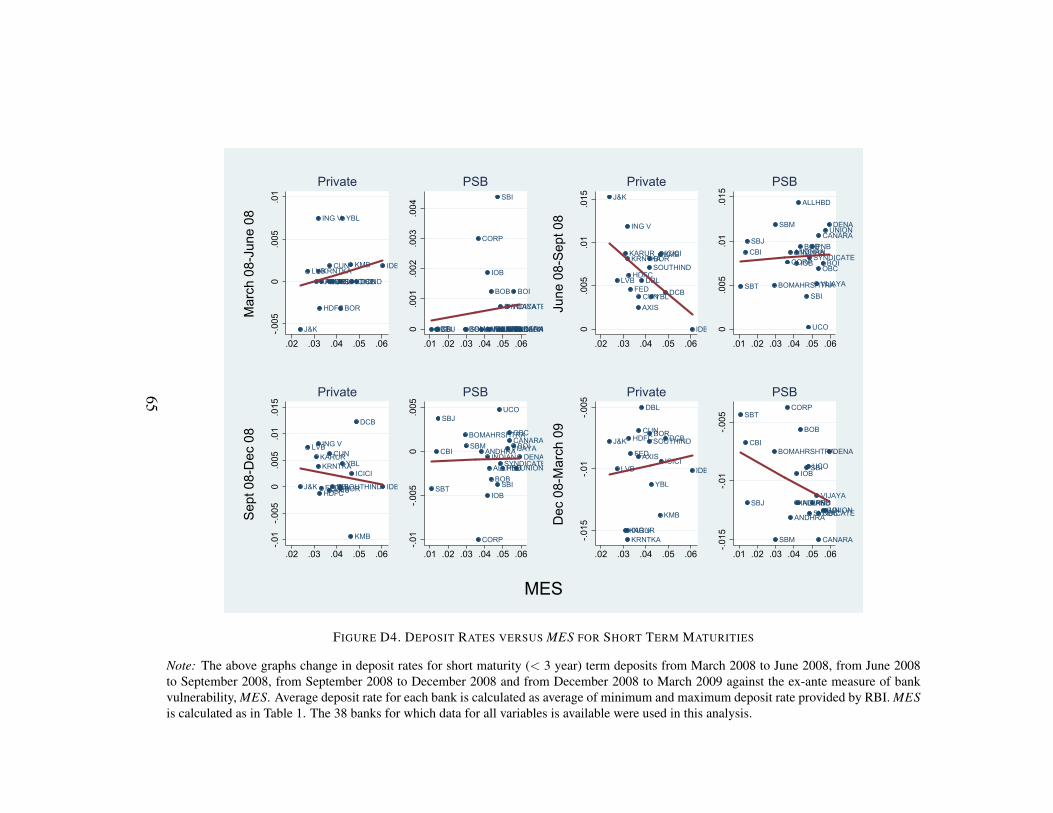

Figure 2 and Figure D4 provide the change in deposit rates for long-term

maturities and short-term maturities respectively, in each quarter of the crisis

against ex-ante bank vulnerability, i.e. MES. We observe an interesting trend

as the crisis progressed. Between June 2008 and September 2009, deposit

rates decreased for more vulnerable private sector banks and increased for more

vulnerable PSBs. This effect is more evident for the long-term deposits (Figure 2,22

top-right). It is only towards the end of the crisis that PSBs were in fact cutting

deposit rates. Again, this effect is more evident for long-term deposits (Figure 2,

bottom-right).14

Table 4 confirms our results with formal regressions. In these regressions, we

drop data points which were likely not updated. That is, we drop data points

where quarter-on-quarter changes were zero. From Panel A, we see that more

vulnerable private sector banks did not significantly change deposit rates for

short-term deposits. More vulnerable PSBs on the other hand decreased deposit

rates in the beginning (Panel A, column 1) and towards the end of the crisis (Panel

A, column 4). This is consistent with the previous section where we found that

more vulnerable PSBs did not have significant deposit growth for the shorter-

term deposits. In column 2 of Panel B, however, as the crisis deepened in Q3

2008, more vulnerable PSBs increased deposit rates for long-term deposits from

June 2008 to September 2008. Towards the end of the crisis, more vulnerable

PSBs started decreasing their deposit rates (Panel B, column 4) for long-term

deposits too.15 Finally, we conduct several robustness checks (see Appendix D)

to show that our results are robust to alternate measures of MES and to placebo

crisis periods.

Our analysis in this section shows that deposits shifted from private sector

banks to PSBs in the crisis period. By exploiting a regulatory policy, which

allowed banks to change deposit rates of only certain kinds of deposits, we show

that more vulnerable PSBs likely increased deposit rates. We also provide direct

14Note, however, due to the poor quality of data, many of the changes in deposit rates are zeroespecially for changes between March 2008 and June 2008 and between September 2008 andDecember 2008.

15Consistent with this effect of government guarantees on deposits, Acharya and Mora (2015)find that during the financial crisis of 2007–08, riskier commercial banks in the United Statesmanaged to attract more federally-insured deposits by offering higher rates even as they wereexperiencing a slow “run” (reduction in quantities as well as shortening of maturity) of uninsureddeposits.

23

evidence using aggregated deposit rates that more vulnerable PSBs were indeed

increasing deposit rates to attract deposit outflow from the private sector banks.

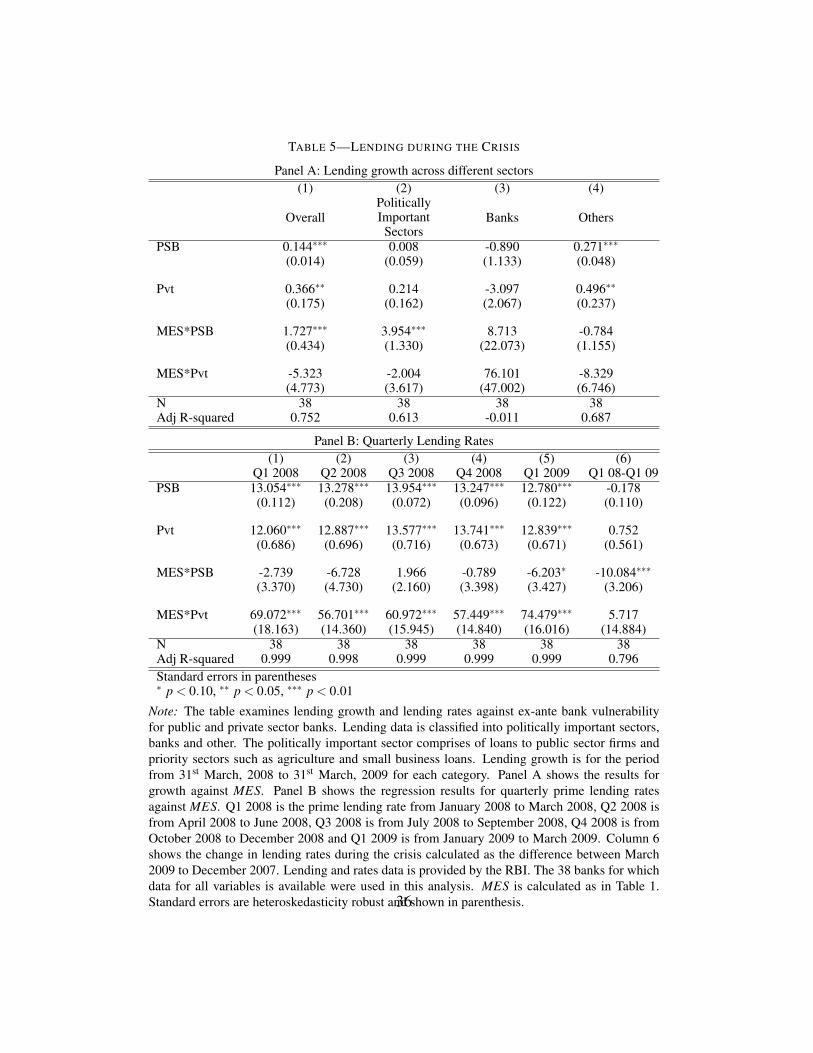

IV. Impact on Bank Lending

We now examine whether the increased flow of deposits into PSBs translated

into an increased flow of credit to the real economy. In line with the higher

deposit growth for PSBs in Section III, we find that credit did indeed grow at a

higher 21.6 percent for PSBs compared to 16.2 percent for private sector banks

during the crisis (see Table D7).

There are several reasons why state-owned banks may not cut back on lending

during crises. One argument is that vulnerable PSBs are socially maximizing

and therefore increase lending during crises and are thus helpful in maintaining

credit flow in the economy during crises periods. In contrast, a political economy

view suggests that political pressure leads to public sector banks lending during

crises but may also result in funding of inefficient investments. Both the social

motive and the political motive result in greater lending and subsequently higher

investment. The difference, however, is that in the former, state-owned banks

invest in projects which are welfare maximizing whereas in the latter the state-

owned banks invest in inefficient projects based on political motives. To see

which of the above motives were responsible for increased lending by banks we

turn to the data. We examine the impact of crisis time guarantees on both the

amount of lending as well as on bank lending rates.16

16The “lazy banking” theory (Banerjee, Cole and Duflo (2005)) says that managers of state-owned banks face an asymmetric incentive structure wherein they are penalized for making badloans but do not face harsh consequences for passing on good opportunities. At face value, sincePSBs increased lending our results seem to suggest that a “lazy banking” theory (Banerjee, Coleand Duflo (2005)) may not be at play. However, it could be that loan managers are more prone toincrease lending to existing customers and thus, we see an increase in lending to the politicallyimportant sectors. This distinction is not important for our analysis. What matters is how theseloans performed in the aftermath of the crisis and whether they were the more economically

24

A. Bank Lending

Column 1 of Table 5 indicates that more vulnerable PSBs did indeed increase

lending during the crisis. A 1 percent increase in ex-ante bank vulnerability as

measured by MES is associated with a 1.73 percent increase in lending. We next

look at what sectors drive this higher lending by the PSBs. In columns 2–4 we

split loan growth into lending to (i) politically important sectors; (ii) banks; and a

catch-all category (iii) other. The politically important sector comprises of loans

to public sector firms and to the priority sector which includes agriculture and

small businesses loans. Our results indicate that the increase in lending by the

vulnerable PSBs is driven by lending to politically important sectors. In column

2, we see that a 1 percent increase in ex-ante bank vulnerability, MES, resulted

in a 3.95 percent increase in lending by PSBs to the politically important sector.

More vulnerable private sector banks, on the other hand, did not significantly

increase lending to these politically important sectors.

B. Lending Rates

In Section III, we established that vulnerable PSBs experienced an increased

inflow of deposits possibly by increasing their deposit rates. In this section, we

examine whether this higher cost of funding — higher deposit rates — translated

into higher lending rates on loans for PSBs. Panel B of Table 5 shows that more

vulnerable private sector banks had significantly higher lending rates throughout

the crisis from Q1 2008 to Q1 2009. More vulnerable PSBs which raised their

deposit rates and had higher borrowing costs, however, did not have similar

higher lending rates. Column 5 of Panel B, Table 5 shows that lending rates

were in fact 6 basis points lower for more vulnerable PSBs in Q1 2009 as the

viable projects.25

coefficient on the interaction term for MES ∗PSB indicates. Column 6 looks at

the change in lending rates from Q1 2008 to Q1 2009. More vulnerable PSBs

decreased lending rates by 10 basis points after the onset of the crisis.

More vulnerable PSBs potentially did not care about higher deposit rates eating

into their profit margins because they would be bailed out by the government in

the worst case. But one could argue that the effect of higher deposit rates is not

so severe since both consumers and the real economy benefit — consumers get

higher deposit rates and at the same time firms are not penalized with higher

lending rates. We find, however, that PSBs were lending mostly to the priority

and public sectors which are of particular interest to the government. The

findings in this section are consistent with the political economy view mentioned

previously. While these political interests may result in increased lending, this

might not necessarily be maximizing social welfare as the politically motivated

lending may result in inefficient investments. Next, we look at the impact of this

lack of market discipline on the long-term performance of loans.

V. Loan Performance and Capital Injections

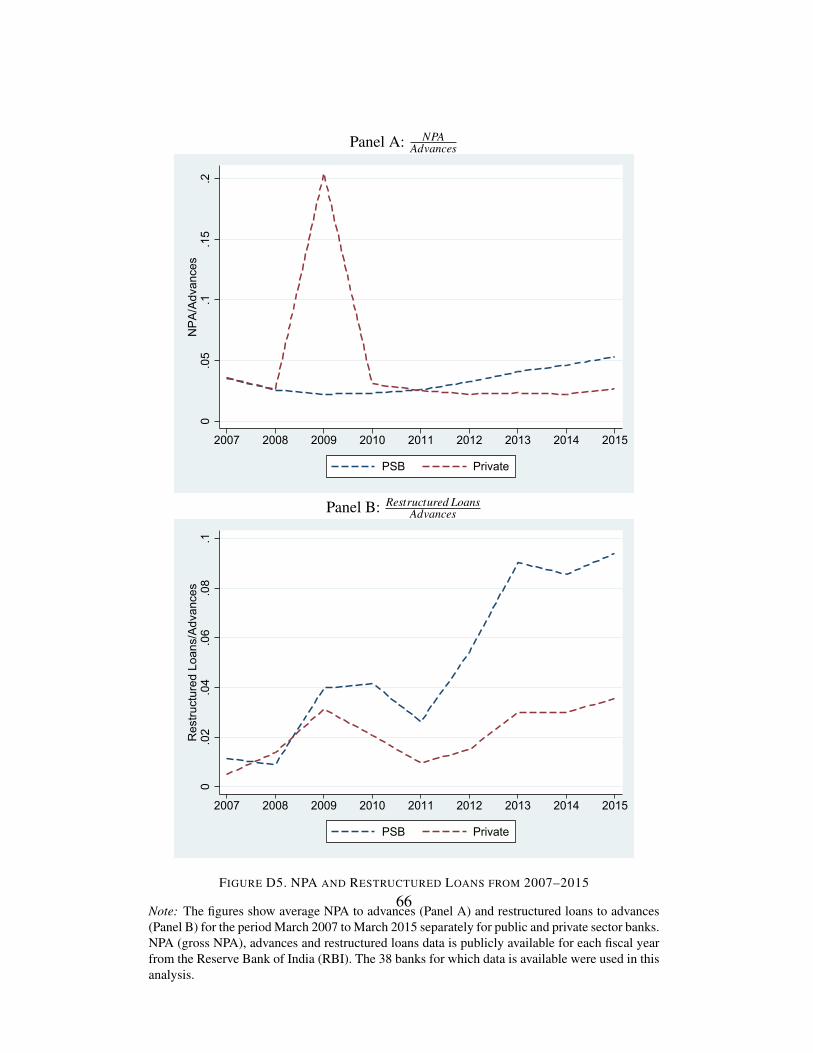

We now look at non-performing assets (NPAs) and restructured loans in the

aftermath of the crisis from March 2008 to March 2015. Loans are classified as

NPA if a borrower misses payments for 90 days (or 180 days in some cases).

Restructuring of loans modifies the terms of existing loans if the lender deems

the borrower is unable to repay the loan. Banks are less inclined to recognize bad

loans and more prone to restructure assets which allows them to not recognize

losses on bad loans first. Hence we focus on both NPAs and restructing of assets.

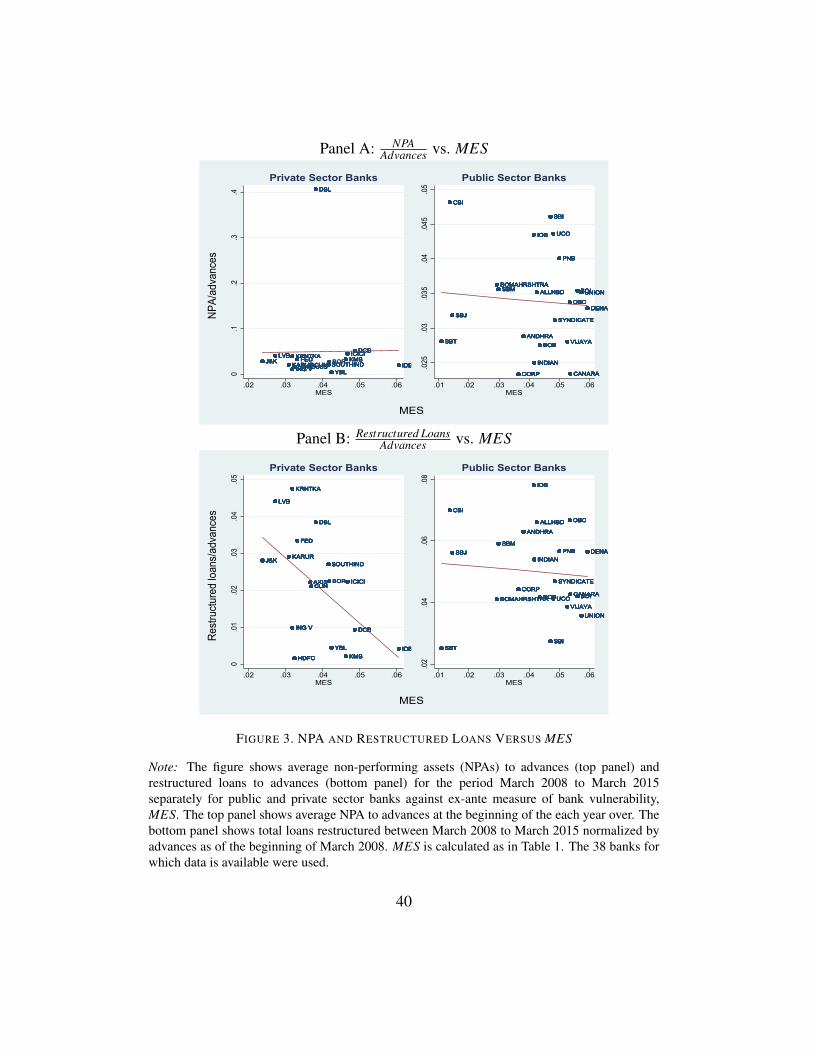

Following the crisis, the NPA to total loan advances remained relatively stable

for PSBs throughout the period whereas private sector banks had a spike in their26

NPAs in the period immediately following the crisis but have had lower overall

NPAs since then (Figure D5, Panel A). Restructured loans as a percentage of loan

advances rose for both private and public sector banks but rise was more stark for

PSBs (Figure D5, Panel B).17 On examining the cross-sectional heterogeneity

against ex-ante bank vulnerability, we see that MES and NPAs are not correlated

(Figure 3).18 However, more vulnerable private sector banks had on average

starkly lower restructurings (Figure 3).

More formal regressions in Table 6 shows similar results. Ex-ante bank

vulnerability and NPAs to loan advances are not significantly related (column

1). However, private sector banks with greater ex-ante bank vulnerability had

lower restructured loans (column 2). More vulnerable private sector banks had

1 percent lower ratio of restructured loans to loan advances. This might be

attributable to the more prudent lending by the vulnerable private sector banks

in contrast to vulnerable PSBs which increased lending to politically important

sectors and at lower loan rates. We do not see any effect on the NPAs of

PSBs probably because they are reluctant to recongnize bad loans.19 Hence,

we interpret the lower NPAs of more vulnerable private sector banks as the true

counterfactual wherein the market disciplines banks resulting in more prudent

lending. Lack of such market discipline in the case of PSBs implies that we do

17Note Bank of Rajasthan was merged with ICICI in 2010. Results are qualitatively similar ifwe drop these banks from the analysis.

18When we restrict to agricultural NPAs, we do see that more vulnerable PSBs had higheragricultural NPAs with a one percent higher MES corresponding to a 36 percent higheragricultural NPAs to total advances to the agricultural sector. There was no effect on the privatesector banks. Since this is likely driven by a large debt waiver program announced by thegovernment in 2008 (see Mukherjee, Subramanian and Tantri (2014), Gine and Kanz (2014)),we focus on the restructured loans.

19The process of recognizing NPAs and bank balance sheet clean-up is still on-going. The process of forcing PSBs to recognize bad loans on their balance sheetsis still on-going and thus may mask true health of these loans (See “Bank NPAs mayhit 8.5 % by March ”, June 28 2016, http://www.thehindu.com/business/Economy/financial-stability-report-released/article8784187.ece)

27

not observe similar lowering of restructured loans for PSBs.

VI. Capital Injections in PSBs

Next, we look at the extent of capital support provided by the Indian

government to the PSBs in the aftermath of the crisis as a direct measure of

government support received by different banks. Since the sample of banks that

received capital injections is small, we only provide a descriptive study. Evidence

suggests that weaker PSBs received greater capital injections. Beginning

December 2008, the government announced a number of capital injections for

PSBs. In February 2009, the government announced capital injections in 3

PSBs: UCO Bank, Central Bank of India and Vijaya Bank. Further, as part

of the 2010-2011 budget, the government announced additional capital infusion

in five PSBs: IDBI Bank, Central Bank, Bank of Maharashtra, UCO Bank and

Union Bank. The amount of capital injections was determined based on PSB

funding requirements and the need for a capital buffer. Effectively, the PSBs

which performed the worst during the crisis resulting in high capital depletion

were more likely to receive support from the government. As of March 2009, all

the banks mentioned above (except Union Bank) had less than 8 percent of Tier 1

capital. Based on the MES measure, these were also among the more vulnerable

banks in our analysis. For example, Union Bank had an MES of 5.74 percent

and Vijaya Bank had an MES of 5.27 percent. UCO Bank had a relatively lower

MES of 4.80 percent. In summary, more vulnerable PSBs did receive greater

ex-post government support. Such direct capital support was not provided to

more vulnerable private sector banks, consistent with our starting assumption

that PSBs have greater government support compared to the private sector banks.28

VII. Conclusion

In this paper, we examine the relatively strong performance of state-owned

banks in India compared to their private-sector counterparts during the global

financial crisis of 2007–09. While more vulnerable private sector banks

performed worse than less vulnerable private sector banks, vulnerable state-

owned banks performed better. We attribute this to the presence of government

guarantees which enabled more vulnerable state-owned banks to grow their

deposit base by increasing their deposit rates. While they also increased loan

advances, they did so at cheaper rates and especially to politically important

sectors. Ex-post, these loan advances have been associated with greater non-

performance and restructuring of assets, thus sowing the seeds of an economic

slowdown in investments in India (as documented in Acharya, Mishra and

Prabhala (2005)).

Our findings are, in fact, consistent with the experience worldwide: financial

institutions with greater access to government guarantees have survived the crisis

or even expanded post-crisis while the ones without such access have failed

or shrunk. A striking case in point has been the growth of the government-

sponsored enterprises (Fannie Mae and Freddie Mac) and commercial banks in

the United States - both sets of institutions with explicit government support and

ready access to central bank emergency lending. These institutions expanded

their holdings of mortgage-backed securities while investment banks and hedge

funds deleveraged and sold these securities (He, Khang and Krishnamurthy

(2010)). Eventually, Fannie Mae and Freddie Mac effectively failed and were put

under the United States government conservatorship in September 2008. Thus,

even though access to government guarantees might be considered a source of

financial stability during a crisis, our results suggest that greater presence of29

government institutions in the financial sector (or greater extent of government

intervention in a crisis) is likely to be associated with the misfortune of crowding

out the private financial sector in the long run.

REFERENCES

Acharya, Viral, and Nada Mora. 2015. “A Crisis of Banks as Liquidity

Providers.” Journal of Finance.

Acharya, Viral, D. Anginer, and A.J. Warburton. 2014. “The End of Market

Discipline? Investor Expectations of Implicit State Guarantees.” NYU Stern

School of Business, Working Paper.

Acharya, Viral, Prachi Mishra, and N.R. Prabhala. 2005. “Bank Financing in

India.” Working paper, CAFRAL.

Acharya, Viral V., Lasse Heje Pedersen, Thomas Philippon, and Matthew P.

Richardson. Forthcoming. “Measuring Systemic Risk.” Review of Financial

Studies.

Banerjee, Abhijit, Shawn Cole, and Esther Duflo. 2005. “Bank Financing

in India.” India’s and China’s Recent Experience with Reform and Growth,

Wanda Tseng and David Cowen, eds.

Calomiris, Charles W., and Stephen H. Haber. 2009. Fragile by Design: The

Political Origins of Banking Crises and Scarce Credit.

Cordella, T., and E. Yeyati. 2003. “Bank bailouts: Moral Hazard vs. Value

Effect.” Journal of Financial Intermediation, 12: 300–330.

Gine, Xavier, and Martin Kanz. 2014. “The Economic Effects of a Borrower

Bailout: Evidence from an Emerging Market.” Working paper.30

Gorton, G., and L. Huang. 2004. “Liquidity, Efficiency and Bank Bailouts.”

American Economic Review, 94: 455–83.

Gropp, Reint, Jukka Vesala, and Giuseppe Vulpes. 2004. “Equity and Bond

Market Signals as Leading Indicators of Bank Fragility.” Journal of Money,

Credit and Banking, 38: 399–428.

He, Zhiguo, In Gu Khang, and Arvind Krishnamurthy. 2010. “ Balance Sheet

Adjustments in the 2008 Crisis.” IMF Economic Review, 58: 118–156.

Iyer, Rajkamal, and Manju Puri. 2012. “Understanding Bank Runs :

The Importance of Depositor-bank Relationships and Networks.” American

Economic Review, 102(4): 1414–1445.

Micco, Alejandro, and Ugo Panizza. 2006. “Bank ownership and lending

behavior.” Economics Letters, 93: 248 – 254.

Mukherjee, Saptarshi, Krishnamurthy Subramanian, and Prasanna Tantri.

2014. “Costs and Benefits of Debt Moratoria: Evidence from a Natural

Experiment in India.” Working paper.

Sapienza, Paola. 2004. “The effects of government ownership on bank lending.”

N 38 38 38 38 38 38 38Adj R-squared 0.967 0.979 0.975 0.982 0.835 0.819 0.839Standard errors in parentheses∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01

Note: These regressions examine stock performance and ex-ante bank vulnerability for publicand private sector banks. Columns 1–4 show results for the dependent variable Crisis return.Crisis return is the actual stock return during the crisis calculated from 1st January, 2008 to 24th

February, 2009. Ex-ante bank vulnerability is measured by MES. MES is the marginal expectedshortfall of a stock given that the market return is below its 5th- percentile during the period 1st

January, 2007 to 31st December, 2007. Market return is based on the S&P CNX NIFTY forthe pre-crisis period from 1st January, 2007 to 31st December, 2007. Log Asset is the naturallogarithm of the book value of asset value measured as of March 31st, 2008. Columns 5–7 showresults for realized returns over the crisis period broken into pre-bailout, bailout and post-bailoutreturns. Bank bailouts (capital infusion) were announced on December 8th, 2008. Pre-bailoutreturn is the stock return from 7th December, 2007 to 7th December, 2008 and bailout return iscalculated from 8th December to 22nd December, 2008. Post-bailout return is calculated from23rd December to the end of the sample period, that is, 24th February, 2009. MES is calculatedfor the one-year period preceding the pre-bailout, bailout and post-bailout periods. Pre-bailoutMES is calculated for the period 1st January, 2007 to 31st December, 2007 and bailout periodMES is calculated for the period 7th December, 2007 to 8th December, 2008. Post-bailout periodMES is calculated for the period 22nd December, 2007 to 22nd December, 2008. The 38 banksfor which data for all variables is available were used in the overall analysis. Standard errors areheteroskedasticity robust and shown in parenthesis.

32

TABLE 2—DEPOSIT GROWTH

(1) (2) (3) (4)Deposit Growth 2 year Deposit Growth

N 38 38 38 38Adj R-squared 0.785 0.861 0.745 0.745Standard errors in parentheses∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01

Note: These regressions examine deposit growth and ex-ante bank vulnerability for public andprivate sector banks. Columns 1–2 show results for the dependent variable deposit growth duringthe crisis period. Deposit growth is reported annually for the fiscal year ending March and isprovided by the Reserve Bank of India (RBI). Deposit growth for the crisis period is measuredfrom 31st March, 2008 to 31st March, 2009. Ex-ante bank vulnerability is measured by MES.MES is the marginal expected shortfall of a stock given that the market return is below its 5th -percentile during the period 1st January, 2007 to 31st December, 2007. Market return is based onthe S&P CNX NIFTY for the precrisis period from January 2007 to December 2007. Columns 3–4 show results for deposit growth in the long-run, that is, over a two year period from the start ofthe crisis. The two-year deposit growth is measured from 31st March, 2008 to 31st March, 2010.The 38 banks for which data for all variables is available were used in this analysis. Standarderrors are heteroskedasticity robust and shown in parenthesis.

33

TABLE 3—DEPOSIT GROWTH FOR DIFFERENT TYPES OF DEPOSITS DURING THE CRISIS

Panel A: Deposit growth for deposits with regulated and unregulated deposit rates(1) (2) (3) (4)

Demand Term Savings Within IndiaPSB 0.057 0.145∗∗∗ 0.259∗∗∗ 0.160∗∗∗

N 38 38 38 38Adj R-squared 0.074 0.319 0.092 0.740Standard errors in parentheses∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01

Note: The table above examines deposit growth by type and ex-ante bank vulnerability for publicand private sector banks. Panel A shows results for the dependent variable deposit growth in eachcategory (demand/term/savings deposits and deposits within India). Panel B shows results forinterbank and corporate/retail (non-interbank) deposits for demand and term deposits. Depositgrowth is from Reserve Bank of India (RBI)and measured from 31st March, 2008 to 31st March,2009. Ex-ante bank vulnerability is measured by MES. MES is the marginal expected shortfallof a stock given that the market return is below its 5th - percentile during the period 1st January,2007 to 31st December, 2007. Market return is based on the S&P CNX NIFTY for the precrisisperiod from January 2007 to December 2007. The 38 banks for which data for all variables isavailable were used in this analysis. Standard errors are heteroskedasticity robust and shown inparenthesis.

34

TABLE 4—DEPOSIT RATES AND MES

Panel A: Change in deposit rates for the short maturity (< 3 years) deposits(1) (2) (3) (4)

Mar 08–Jun 08 Jun 08–Sept 08 Sept 08–Dec 08 Dec 08–Mar 09PSB 0.59∗∗∗ 0.76∗∗∗ -0.18 -0.67∗∗∗

MES * PSB -3.09 9.69∗∗ -0.69 -11.81∗∗∗(4.94) (3.68) (11.26) (4.22)

MES * Pvt -12.18 18.27 -34.49 9.49(17.79) (12.47) (57.41) (9.68)

N 15 32 19 37Adj R-squared 0.414 0.822 -0.005 0.835

Note: Above tables show the average deposit rates against the ex-ante measure of bankvulnerability, MES. Panel A and panel B correspond to the deposit rates for the short maturity(< 3 years) and long maturity (> 3 years) deposits. Columns 1–correspond to the change indeposit rates from March 2008 to June 2008 (Column 1),from June 2008 to September 2008(Column 2), from September 2008 to December 2008 (Column 3) and from December 2008 toMarch 2009 (Column 4) against the ex-ante measure of bank vulnerability, MES. Deposit rate inpercentage is the average of the the minimum and maximum deposit rate provided by the ReserveBank of India (RBI). Deposit rate which were not updated during a quarter are dropped. Ex-antebank vulnerability is measured by MES. MES is the marginal expected shortfall of a stock giventhat the market return is below its 5th - percentile during the period 1st January, 2007 to 31st

December, 2007. Market return is based on the S&P CNX NIFTY for the pre-crisis period fromJanuary 2007 to December 2007. The 38 banks for which data for all variables is available wereused in this analysis. Standard errors are heteroskedasticity robust and shown in parenthesis.

35

TABLE 5—LENDING DURING THE CRISIS

Panel A: Lending growth across different sectors(1) (2) (3) (4)

N 38 38 38 38 38 38Adj R-squared 0.999 0.998 0.999 0.999 0.999 0.796Standard errors in parentheses∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01

Note: The table examines lending growth and lending rates against ex-ante bank vulnerabilityfor public and private sector banks. Lending data is classified into politically important sectors,banks and other. The politically important sector comprises of loans to public sector firms andpriority sectors such as agriculture and small business loans. Lending growth is for the periodfrom 31st March, 2008 to 31st March, 2009 for each category. Panel A shows the results forgrowth against MES. Panel B shows the regression results for quarterly prime lending ratesagainst MES. Q1 2008 is the prime lending rate from January 2008 to March 2008, Q2 2008 isfrom April 2008 to June 2008, Q3 2008 is from July 2008 to September 2008, Q4 2008 is fromOctober 2008 to December 2008 and Q1 2009 is from January 2009 to March 2009. Column 6shows the change in lending rates during the crisis calculated as the difference between March2009 to December 2007. Lending and rates data is provided by the RBI. The 38 banks for whichdata for all variables is available were used in this analysis. MES is calculated as in Table 1.Standard errors are heteroskedasticity robust and shown in parenthesis.36

TABLE 6—NON-PERFORMING ASSETS AND RESTRUCTURED LOANS

MES * PSB -0.036 -0.081 -0.12(0.075) (0.23) (0.29)

MES * Pvt 0.060 -0.97∗∗∗ -0.90∗∗∗(0.28) (0.15) (0.32)

N 297 297 297Adj R-squared 0.041 0.656 0.154Standard errors in parentheses∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01

Note: These regressions examine non-performing assets (NPA)/advances and restructured advances/totaladvances and ex-ante bank vulnerability for public and private sector banks. Column 1 shows results forthe dependent variable NPA/advances. Column 2 shows results for the dependent variable for restructuredloans/advances. Column 3 shows results for the dependent variable (NPA + restructured loans)/advances.Data is for the period 2008 to 2015. NPA (gross NPA), advances and restructured loans data is reportedannually for the fiscal year ending March and is provided by the Reserve Bank of India (RBI). NPA (grossNPA, advances and restructured loans are as of March of each year. Ex-ante bank vulnerability is measuredby MES. MES is the marginal expected shortfall of a stock given that the market return is below its 5th -percentile during the period 1st January, 2007 to 31st December, 2007. Market return is based on the S&PCNX NIFTY for the pre-crisis period from January 2007 to December 2007. The 38 banks for which datafor all variables is available were used in this analysis.

37

Panel A: Crisis Returns vs. MES

J&K

AXIS

BOR

CUN

DCB

DBL

FED

HDFC

ICICI

IDB

ING V

KRNTKA

KARUR

KMB

LVB

SOUTHIND

YBL

-.9-.8

-.7-.6

-.5

.02 .03 .04 .05 .06MES

Private Sector Banks

SBI

SBJ

SBMSBT

ALLHBD

ANDHRA

BOB

BOI

BOMAHRSHTRA

CANARA

CBI

CORP

DENA

INDIAN

IOB

OBC

PNB

SYNDICATE

UCO

UNION

VIJAYA

-1-.8

-.6-.4

.01 .02 .03 .04 .05 .06MES

Public Sector Banks

Cris

is re

turn

s

MES

Panel B: Deposit Growth vs. MES

J&K

AXIS

BOR

CUN

DCB

DBL

FED

HDFC

ICICI

IDBING V

KRNTKAKARUR

KMB

LVB

SOUTHIND

YBL

-.4-.2

0.2

.4

.02 .03 .04 .05 .06MES

Private Sector Banks

SBI

SBJ

SBMSBT

ALLHBD

ANDHRA

BOB BOIBOMAHRSHTRA

CANARA

CBI

CORP

DENA

INDIAN IOB

OBCPNB

SYNDICATE

UCO

UNION

VIJAYA

.1.1

5.2

.25

.3.3

5

.01 .02 .03 .04 .05 .06MES

Public Sector Banks

Dep

osit

Gro

wth

MES

FIGURE 1. STOCK PERFORMANCE AND DEPOSIT GROWTH VERSUS MES

Note: Panel A and Panel B plot crisis returns and deposit growth during the crisis respectivelyagainst MES for private and public sector banks. Crisis return is the stock return calculated fromJanuary, 2008 to February, 2009. Deposit growth is from March 2008 to March 2009. MES iscalculated as in Table 1. All 38 banks for which data is available were used in the analysis.

38

AXIS

BOR

CUN DCBDBL

FED

HDFC

ICICI IDB

ING V

KRNTKAKARUR

KMB

LVB SOUTHIND

YBL

J&K

-.002

0.0

02.0

04.0

06.0

08

.02 .03 .04 .05 .06

Private

SBI

SBJ

SBMSBT ALLHBD

ANDHRABOB

BOI

BOMAHRSHTRACANARACBICORP

DENAINDIAN

IOB

OBCPNB

SYNDICATE

UCOUNIONVIJAYA

-.002

0.0

02.0

04.0

06

.01 .02 .03 .04 .05 .06

PSB

Mar

ch 0

8-Ju

ne 0

8

AXIS

BOR

CUN

DCB

DBL

FED

HDFC

ICICI

IDB

ING V

KRNTKAKARUR

KMB

LVB

SOUTHINDYBL

J&K

0.0

05.0

1.0

15

.02 .03 .04 .05 .06

Private

SBI

SBJ

SBM

SBTALLHBD

ANDHRA

BOB

BOI

BOMAHRSHTRA

CANARA

CBICORP

DENAINDIANIOB

OBC

PNB

SYNDICATE

UCO

UNION

VIJAYA0.0

05.0

1.0

15

.01 .02 .03 .04 .05 .06

PSB

June

08-

Sept

08

AXISBOR

CUN DCB

DBLFED

HDFC

ICICI IDB

ING VKRNTKA

KARUR

KMB

LVB SOUTHIND

YBL

J&K

-.01

0.0

1.0

2

.02 .03 .04 .05 .06

Private

SBI

SBJ SBM

SBT

ALLHBD

ANDHRA

BOBBOI

BOMAHRSHTRA

CANARACBI

CORP

DENAINDIANIOB

OBC

PNBSYNDICATE

UCO

UNIONVIJAYA

-.005

0.0

05.0

1

.01 .02 .03 .04 .05 .06

PSB

Sept

08-

Dec

08

AXISBOR

CUN

DCB

DBLFED

HDFC

ICICI

IDB

ING V

KRNTKA

KARUR

KMBLVBSOUTHINDYBL

J&K

-.02

-.015

-.01

-.005

0

.02 .03 .04 .05 .06

Private

SBISBJ

SBM

SBTALLHBD

ANDHRA

BOB

BOI

BOMAHRSHTRA

CANARA

CBI

CORP

DENA

INDIANIOB

OBC

PNBSYNDICATE

UCO

UNION

VIJAYA

-.015

-.01

-.005

0

.01 .02 .03 .04 .05 .06

PSB

Dec

08-

Mar

ch 0

9

MES

FIGURE 2. DEPOSIT RATES VERSUS MES FOR LONG TERM MATURITIES

Note: The graphs plot the change in deposit rates for long maturity (> 3 years) term deposits from March 2008 to June 2008, from June 2008to September 2008, from September 2008 to December 2008 and from December 2008 to March 2009 against the ex-ante measure of bankvulnerability, MES. Average deposit rate using minimum and maximum deposit rate is provided by RBI. MES is calculated as in Table 1. The38 banks for which data for all variables is available is used.

Note: The figure shows average non-performing assets (NPAs) to advances (top panel) andrestructured loans to advances (bottom panel) for the period March 2008 to March 2015separately for public and private sector banks against ex-ante measure of bank vulnerability,MES. The top panel shows average NPA to advances at the beginning of the each year over. Thebottom panel shows total loans restructured between March 2008 to March 2015 normalized byadvances as of the beginning of March 2008. MES is calculated as in Table 1. The 38 banks forwhich data is available were used.

40

For Online Publication: Appendix

A. Model

This section presents a simple model to motivate our empirical work. We

build a simple model to explain how government guarantees can distort behavior

and outcomes for these protected banks. We then compare their outcomes and

behavior with banks that do not enjoy such government guarantees. To maintain

consistency with our empirical hypothesis in the context of India, we shall refer

to the protected banks in the model as PSBs (PSBs) and the unprotected banks

as private sector banks. In India state-owned banks or PSBs enjoy explicit

government guarantees whereas private sector banks do not have these explicit

government guarantees.

Consider the following simple model (see Figure A1). Nature selects either

of two states, the idiosyncratic state or the crisis state. The idiosyncratic states

occurs with a probability (1− p) and a crisis state occurs with a probability p.

When the idiosyncratic state occurs either of two things can happen –either the

bank fails with a probability λ i in which case it gets a payoff of 0 or it survives

with a probability (1−λ i) in which case it gets a payoff of c. c can be thought

of as the cashflows of the bank or the franchise value of the bank. In case of an

idiosyncratic shock and subsequent bank failure, there is no difference between